Japan AI-powered Energy Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

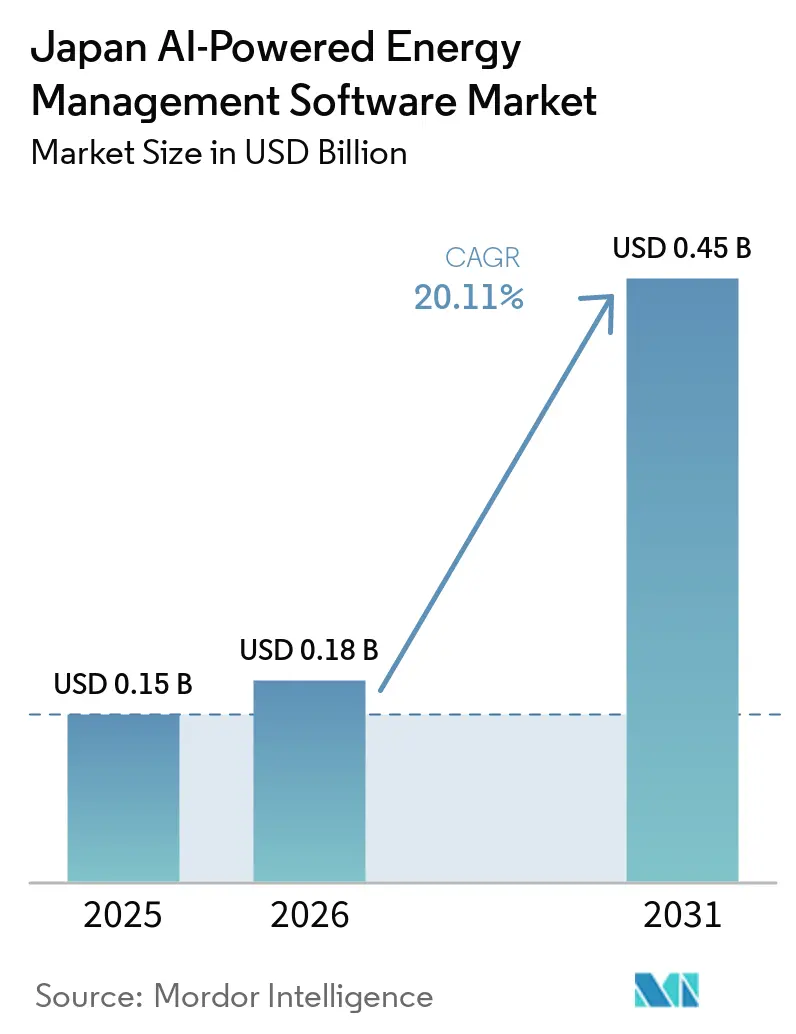

| Base Year Market Size (2025) | USD 0.15 Billion |

| Market Size (2026) | USD 0.18 Billion |

| Market Size (2031) | USD 0.45 Billion |

| Growth Rate (2026 - 2031) | 20.11% CAGR |

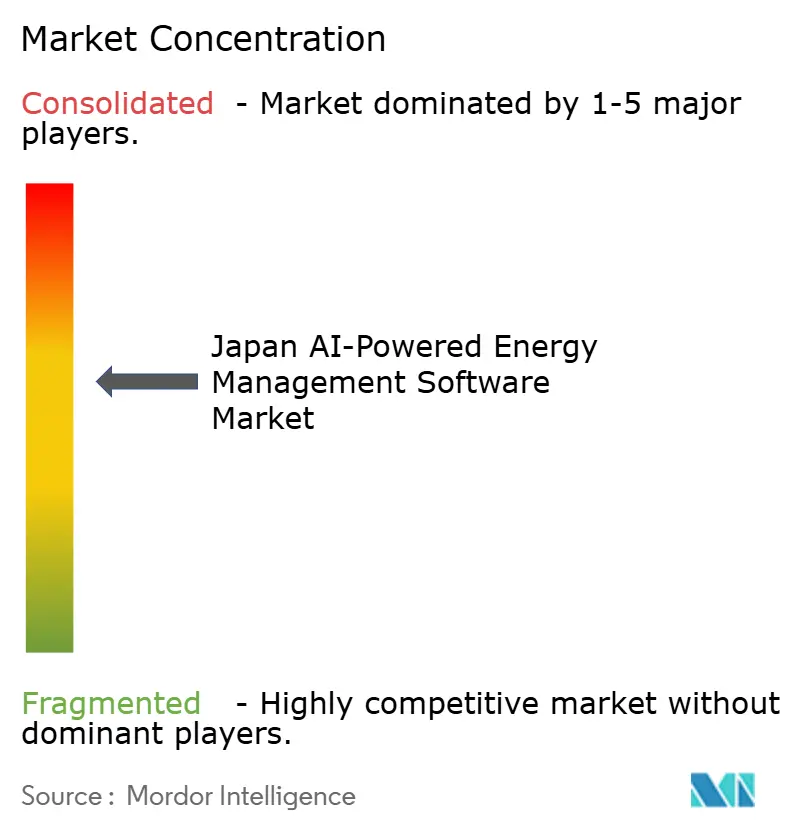

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan AI-powered Energy Management Software Market Analysis by Mordor Intelligence

The Japan AI-powered Energy Management Software Market size was USD 0.15 billion in 2025 and is projected to reach USD 0.45 billion by 2031, at a CAGR of 20.11% from 2026 to 2031. The Japan AI-powered Energy Management Software Market expanded as electricity procurement became more difficult amid volatile wholesale pricing, tighter balancing rules, and continued reliance on imported LNG. The shift also strengthened demand from utilities, large enterprises, and energy-intensive facilities that needed better forecasting, automated load control, and clearer cost visibility across daily operations. Another layer of demand came from data centers, green transformation funding programs, and emissions compliance rules, which made energy monitoring and optimization more important in routine investment decisions. The Japan AI-powered Energy Management Software Market also benefited from the wider adoption of smart meters, facility sensors, and cloud-connected control systems, which improved the quality of the operating data available to software platforms. Competition stayed active because Japanese incumbents brought strong local integration capabilities, while global vendors pushed AI-led upgrades, platform partnerships, and grid-facing software offerings to win larger and longer contracts.

Key Report Takeaways

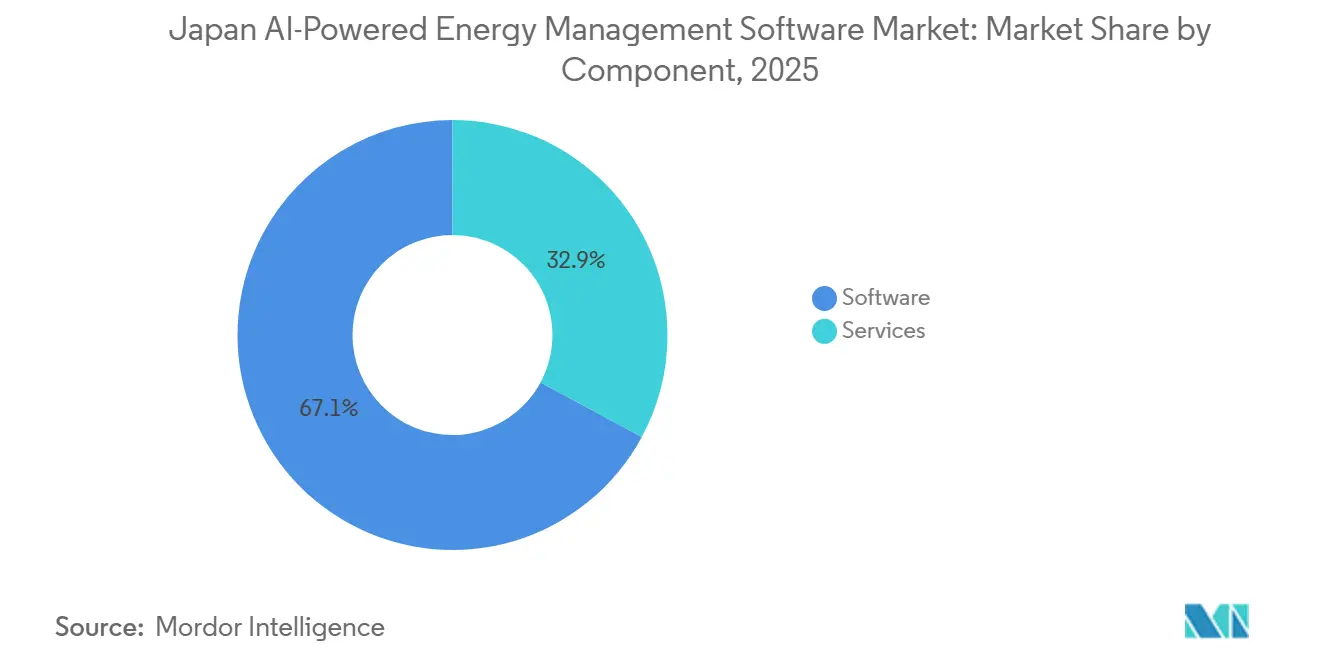

- By component, software held 67.14% of the Japan AI-powered Energy Management Software Market share in 2025, while services are projected to expand at a 20.22% CAGR through 2031.

- By deployment mode, cloud-based deployment accounted for 57.18% of the market in 2025, while hybrid deployment is projected to grow at a 20.34% CAGR through 2031.

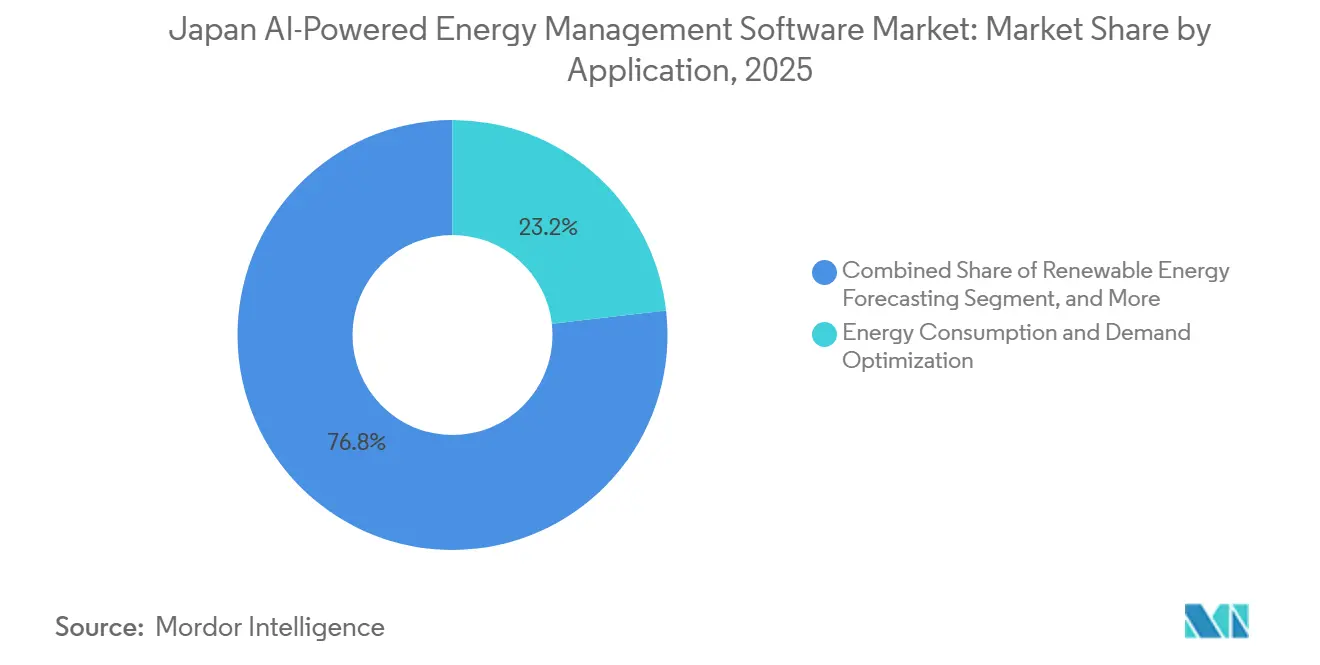

- By application, energy consumption and demand optimization accounted for 23.19% of the market in 2025, while renewable energy forecasting and integration are projected to grow at a 20.46% CAGR through 2031.

- By end user, utilities held 34.11% of the Japan AI-powered Energy Management Software Market share in 2025, while industrial facilities are projected to register the highest CAGR of 20.57% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan AI-powered Energy Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Electricity Price Volatility In Japan | +3.8% | National, with highest intensity in Chubu and Greater Tokyo market zones | Short term (≤ 2 years) |

| Rapid Smart Meter and IoT Sensor Penetration Across Commercial Buildings | +3.4% | Kanto, Kansai, and Chubu commercial urban centers | Medium term (2-4 years) |

| Strong Corporate Decarbonization Programs and Net-Zero Commitments | +3.1% | National, concentrated in Kanto and Kansai enterprise hubs | Medium term (2-4 years) |

| Growing Demand For AI-Based Load Shifting and Peak Demand Optimization | +2.8% | Kanto, Kansai, and Chubu urban and industrial corridors | Short term (≤ 2 years) |

| Grid Congestion Management Needs in Dense Urban and Industrial Corridors | +2.4% | Greater Tokyo, Osaka-Kobe-Kyoto corridor, and Nagoya metropolitan zone | Medium term (2-4 years) |

| Expansion of Renewable Energy Integration Requiring Dynamic Energy Orchestration | +1.9% | Kyushu, Tohoku, and Hokkaido renewable-dense regions, with spillover to central Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Electricity Price Volatility in Japan

Japan’s wholesale electricity market has shifted beyond short seasonal swings and entered a phase of broader structural volatility. The April 2026 end of JERA Group’s intra-group power purchase agreements pushed major volumes into the open spot market and lifted prices in the Tokyo and Chubu areas to levels not seen since the 2022 energy crisis.[1]Institute of Energy Economics Japan, “Managing Electricity Price Volatility Risk and the Importance of Electricity Futures,” Institute of Energy Economics Japan, eneken.ieej.or.jp The electricity futures market also gained greater prominence through 2025 as participants sought stronger hedging tools against recurring price shocks. Rule changes that moved balancing to 30-minute intervals in April 2026 and adjusted imbalance pricing raised the cost of forecast errors for retailers and large energy users. That shift made the Japan AI-powered Energy Management Software Market more relevant because buyers needed faster demand forecasting and procurement support, not just static energy reporting. In this setting, the Japan AI-powered Energy Management Software Market moved closer to a core operating tool for entities exposed to daily market pricing.

Rapid Smart Meter and IoT Sensor Penetration Across Commercial Buildings

Japan completed the first-generation rollout of smart meters across 86 million electricity customer connections by the end of 2024.[2]Institute of Energy Economics Japan, “Managing Electricity Price Volatility Risk and the Importance of Electricity Futures,” Institute of Energy Economics Japan, eneken.ieej.or.jp Second-generation installations then began, adding bidirectional communication and more granular interval data for facility operators and software vendors. That data quality mattered because AI models perform better when they can match occupancy patterns, weather shifts, equipment behavior, and market prices in shorter cycles. The commercial building base in Tokyo, Osaka, and other dense urban markets also kept adding sub-metering and connected sensors, expanding the usable operating data available within large properties. This supported the Japan AI-powered Energy Management Software Market by lowering the need for fresh metering investment at the point of software adoption. Vendors that combined smart meter feeds with HVAC controls, facility systems, and market data gained a clearer edge over basic monitoring platforms.

Strong Corporate Decarbonization Programs and Net-Zero Commitments

Large Japanese companies turned their climate targets into more direct operating requirements, which supported software demand. Ricoh raised its fiscal 2030 Scope 1 and 2 reduction target to 75% versus fiscal 2015 levels in April 2026 under the SBTi Net-Zero Standard.[3]Ricoh, “Ricoh Raises Decarbonization Targets Under New ESG Strategy in the Latest Mid-Term Strategy,” Ricoh, ricoh.com Marubeni also reported that its Scope 3 Category 15 emissions fell to 24 million tons in FY2025, which was ahead of its 2030 target path. Japan’s ETS launch in fiscal year 2026 under the GX Promotion Act put a direct cost on unmanaged energy use and made auditable energy data more important in procurement decisions. The GX financing framework added another push because enterprises seeking access to green transformation support had to demonstrate a clear energy-efficiency visualization. As a result, the Japan AI-powered Energy Management Software Market benefited from a mix of compliance pressure, board-level target tracking, and funding-linked reporting requirements.

Growing Demand for AI-Based Load Shifting and Peak Demand Optimization

The April 2026 balancing reform widened participation and made demand response more complex to manage. It opened low-voltage resources such as household batteries and EV aggregators to broader market activity and shifted the operating rhythm to 30-minute intervals. Enel X Japan demonstrated the scale of this opportunity by delivering 7 GW of demand response across 19 dispatch days during summer 2025.[4]Enel X Japan, “Tight Supply and Demand Drives New Demand Response Record in the Capacity Market,” Enel X Japan, enelx.com The IEEJ Outlook 2026 also pointed to significant long-term savings potential from AI-led demand-side applications, with industrial use cases accounting for the largest share of that opportunity. At the same time, projected growth in battery storage under Japan’s strategic energy plan expanded the number of distributed assets that required active coordination. This made the Japan AI-powered Energy Management Software Market more valuable to customers seeking software that turns flexible loads, storage assets, and price signals into measurable cost savings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Complexity with Legacy Building Management Systems | -1.5% | Kanto and Kansai, where older commercial building stock is concentrated | Medium term (2-4 years) |

| Shortage of Energy Data Talent and AI Operations Expertise | -1.2% | National, with most acute skill gaps outside greater Tokyo | Long term (≥ 4 years) |

| Cybersecurity and Data Governance Concerns In Connected Energy Platforms | -0.9% | National, with early emphasis on critical infrastructure in Tokyo and Osaka | Long term (≥ 4 years) |

| Long Enterprise Sales Cycles and High Solution Customization Costs | -0.7% | National, with greater friction in regional and mid-market accounts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Integration Complexity with Legacy Building Management Systems

A large share of Japan’s older commercial buildings still runs on proprietary control systems that were not built for modern AI integration. That creates extra work around middleware, interface development, hardware upgrades, and site-level commissioning before a new platform can run reliably. The IEEJ Outlook 2026 also noted that institutional readiness and investment barriers continue to slow demand-side AI adoption in the energy system. The problem is not only technical, as many buildings are also tied to long-term service agreements with incumbent automation providers. That slows decision-making even when energy savings and reporting needs are clear. The Japan AI-powered Energy Management Software Market, therefore, faced longer sales cycles in older building stock, while vendors that worked inside existing control environments had a better chance of lowering deployment friction.

Shortage Of Energy Data Talent and AI Operations Expertise

Japan’s declining working-age population created a real capacity gap in its energy digitalization programs. AI-led energy management requires a blend of power systems knowledge, data science, and software integration skills, and many enterprises do not have that mix in-house. The IEEJ Outlook 2026 identified skill shortages as one of the main institutional barriers to AI-driven energy savings. This shortage extended procurement timelines because buyers with limited internal expertise often took longer to assess vendor claims and implementation scope. It also raised the risk of weak pilot outcomes, which can reduce confidence in broader rollouts after the first project. The Japan AI-powered Energy Management Software Market continued to move forward, but managed services and outsourced operations gained additional value because many utilities and industrial users could not build these capabilities quickly enough on their own.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Held The Largest Share While Services Scaled Faster

Software held 67.14% of the Japan AI-powered Energy Management Software Market share in 2025, and it remained the core revenue base for the category. That position came from the widespread use of analytics platforms and demand response orchestration tools, and from the development of building energy dashboards across utilities and large facilities. The segment also benefited from Japan’s earlier move toward digital infrastructure in utility operations and commercial energy management, where buyers had long favored licensed platforms over stand-alone support contracts. Japan Meteorological Association’s selection in January 2026 for all three forecasting functions in the country’s next-generation central dispatch command system showed how deeply advanced software had moved into grid operations. Once software becomes part of core dispatch and balancing workflows, procurement standards tend to rise around reliability, latency, and forecast precision. That shift supported the Japan AI-powered Energy Management Software Market, as utilities and enterprise buyers increasingly expected energy software to operate as a live layer rather than a simple reporting tool.

Services are projected to expand at a 20.22% CAGR from 2026 to 2031, making it the fastest-growing component in the Japan AI-powered energy management software industry. Buyers increasingly preferred outcome-based support because they wanted vendors to absorb a greater share of the integration and operating burden. That was especially relevant when projects needed to connect smart meters, IoT sensors, JEPX feeds, and older building systems simultaneously. The GX2040 vision also strengthened demand for managed services, as compliance reporting and energy visualization became more important for applications supporting green transformation. As a result, the Japan AI-powered energy management software industry saw services shift from a supporting role to a stronger growth engine, with steadier recurring revenue potential for vendors.

By Deployment Mode: Cloud-Based Deployment Led While Hybrid Adoption Accelerated

Cloud-based deployment accounted for 57.18% of the Japan AI-powered Energy Management Software Market size in 2025, making it the largest deployment model. Its lead reflected a strong enterprise preference for scalable SaaS tools that could aggregate data across many facilities without heavy local infrastructure. Cloud environments are also suited to the demands of virtual power plant coordination, multi-site forecasting, and centralized analytics because they can ingest large streams of meter and sensor data in parallel. That mattered more as balancing intervals shortened, and users needed faster decision support for procurement and load scheduling. The Japan AI-powered Energy Management Software Market also benefited from cloud systems, which made updates, model retraining, and remote oversight easier for vendors serving geographically dispersed customers. On-premises systems remained relevant, but they served a narrower role in settings where cybersecurity and operational technology controls kept critical data inside enterprise networks.

Hybrid deployment is projected to grow at a 20.34% CAGR from 2026 to 2031, making it the fastest-moving option in this part of the Japan AI-powered Energy Management Software Market. Many Japanese organizations still run mixed technology environments, so they need cloud analytics layered on top of their local operational systems rather than a full migration to a single model. ETS compliance added to this pattern because companies needed auditable records and stronger control over sensitive operating data while still using cloud-scale analytics and reporting tools. Fujitsu’s December 2025 pilot with the University of Tokyo also showed that cloud workloads can be linked to live grid conditions and electricity market pricing in Japan’s operating environment. That result supported hybrid adoption by demonstrating practical value in combining on-site control, cloud intelligence, and market-linked optimization without requiring a complete rebuild of existing infrastructure.

By Application: Demand Optimization Stayed Largest While Renewable Forecasting Grew Fastest

Energy consumption and demand optimization held 23.19% of the market in 2025 and remained the largest application area. It led because it gave buyers a clear entry point into AI-based energy management through load monitoring, peak demand control, and scheduling against market prices. These use cases were easier to justify because they could deliver direct operating savings more quickly than more specialized applications. The application mix also included asset performance and predictive maintenance, which became more relevant as aging infrastructure increased the cost of equipment failure. Hitachi Energy’s HMAX Energy suite, launched in March 2026, showed that AI-led asset monitoring can reduce revenue loss from equipment breakdowns by up to 60% and transformer failures by up to 50%. Smart grid, DER management, and energy trading applications also grew in importance as distributed assets and price exposure increased across the Japanese power system.

Renewable energy forecasting and integration is projected to grow at a 20.46% CAGR from 2026 to 2031, making it the fastest-growing application in the Japan AI-powered Energy Management Software Market. This part of the market gained momentum because the rise of variable renewable generation increased the cost of weak forecasting and poor coordination. Japan’s grid connection framework, queue discipline, and transmission bottlenecks continued to constrain renewable integration, which raised the value of better orchestration software. Kyushu Electric Power and GRID began full commercial operation of an AI-powered supply-demand planning optimization system in April 2026 to improve daily planning quality and reduce fuel costs. Fujitsu’s April 2026 IP licensing agreement with Chugoku Electric Power Transmission and Distribution also showed that dynamic line rating and AI-based wind forecasting were becoming licensable operating capabilities rather than internal tools.

By End User: Utilities Led Revenue While Industrial Facilities Advanced The Fastest

Utilities held 34.11% of the market in 2025, giving them the largest end-user position in the Japan AI-powered Energy Management Software Market. Their lead came from long-standing demand for grid management software, renewable integration tools, capacity market optimization, and compliance-related reporting systems. Utility contracts also tend to be broad in scope and longer in duration, which helps preserve revenue concentration in this end-user group. The buyer base included the 10 regional transmission and distribution utilities, as well as liberalized electricity retailers that needed stronger forecasting and market response tools. Japan Meteorological Association’s role in the next-generation central dispatch command system reinforced the importance of forecast quality and software reliability in utility procurement. Commercial buildings remained the next major user group because energy monitoring obligations and tenant expectations continued to support AI-based HVAC and building optimization systems.

Industrial facilities are projected to register the highest CAGR of 20.57% through 2031, making them the fastest-growing end-user segment in the Japan AI-powered Energy Management Software Market. Manufacturers faced a direct combination of high electricity procurement costs, decarbonization pressure, and a growing need to coordinate multiple energy assets at the site level. Japan’s ETS framework made this more urgent because inefficient energy use now carried a clearer financial consequence for large operations. Marubeni’s FY2025 emissions result showed that disciplined portfolio-level energy monitoring can support faster progress against stated reduction targets. Industrial sites also added on-site renewables, batteries, and cogeneration systems, increasing the need for software that could manage microgrid-style environments across multiple processes simultaneously. This supported growth in the Japanese AI-powered energy management software industry because factories needed software that could move from measurement into automated operational control.

Geography Analysis

Kanto remained the largest regional revenue center in the Japan AI-powered Energy Management Software Market because it combined the country’s densest base of corporate headquarters, data centers, premium commercial buildings, and major utility operations. TEPCO’s service territory and the broader Greater Tokyo area created the highest-value customer base for advanced forecasting, load management, and building optimization platforms. National data center electricity demand was projected to rise from 15 billion kWh in fiscal year 2022 to 25 billion kWh by fiscal year 2030, and much of that new demand is expected to land in Kanto. This mattered because data center operators need fine-grained scheduling across both physical infrastructure and digital workloads. TEPCO’s effort to cut its grid connection waiting list by the end of 2026 also increased pressure on operators to show more responsive energy behavior. Rich environmental data across the Tokyo basin further supported better demand forecasting and operational tuning for software platforms serving this region.

Kansai and Chubu emerged as the next major demand centers for different reasons. Kansai drew demand from a large commercial real estate base and a strong concentration of electronics and chemical manufacturing. Chubu stood out because its automotive and aerospace supply chains are energy-intensive and more exposed to the value of active load shifting and procurement management. The April 2026 wholesale price surge in the Chubu area market heightened the urgency for industrial buyers who needed better hedging and scheduling tools. Osaka’s Expo 2025 also raised visibility for smart energy systems across commercial and hospitality settings. Together, these patterns supported the Japan AI-powered Energy Management Software Market by keeping demand broad across both service-led urban customers and production-led industrial clusters.

Kyushu, Tohoku, and Hokkaido emerged as important growth zones for renewable forecasting and DER coordination in the Japan AI-powered Energy Management Software Market. These regions carry a larger share of installed wind and solar capacity and therefore face stronger day-to-day balancing and curtailment challenges. Kyushu was especially active because renewable curtailment occurred on more than 100 days per year, making AI-based supply-demand planning and virtual power plant software even more valuable. Hokkaido and Tohoku are also expected to strengthen demand as transmission expansion under the strategic energy plan supports larger flows of renewable energy over time. The broader spread of carbon pricing obligations from fiscal year 2026 also widened the addressable base for emissions tracking and energy reporting beyond Tokyo and Osaka. This regional shift gave the Japanese AI-powered energy management software market a wider opportunity set, not just a metropolitan one.

Competitive Landscape

The Japan AI-powered Energy Management Software Market showed moderate concentration, with large global automation and industrial software vendors holding prominent positions, while domestic technology groups and newer specialists also remained active. Global names such as Schneider Electric, Siemens, and Hitachi competed through local subsidiaries, established account relationships, and utility partnerships. Japanese players such as NEC, Fujitsu, Mitsubishi Electric, and Toshiba held an advantage in legacy integration because many local building and grid environments were built before modern API standards became common. That local system knowledge mattered because buyers often preferred vendors who could work within existing operational setups rather than forcing a full replacement. The market, therefore, rewarded companies that combined software capability with regulatory familiarity, utility relationships, and credible delivery capacity in older operating environments.

Hitachi Energy’s March 2026 launch of HMAX Energy showed one clear competitive strategy. The company packaged AI, digital twins, asset health monitoring, and predictive failure detection into a service suite tied directly to critical energy infrastructure. That move aligned with a broader incumbent approach in the market, in which vendors sought to embed AI into hardware-intensive, asset-intensive environments rather than sell analytics in isolation. Fujitsu’s April 2026 IP licensing agreement with Chugoku Electric Power Transmission and Distribution followed a similar pattern by turning grid operating know-how into renewable integration and maintenance services. Hitachi Energy’s January 2026 work with Microsoft on the Ellipse enterprise asset management platform also showed how major players were linking AI tools with broader enterprise data and operations environments.

Open opportunities remained strongest in parts of the market that older platform models have served less. Residential and small commercial demand response, cross-asset portfolio optimization, and software for mixed renewable fleets remained areas where cloud-native vendors could still gain traction. The April 2026 balancing reforms supported that opening because lower-voltage resources and distributed assets became more relevant in active market participation. The transition of trading activity toward deeper system integration also lowered some entry barriers for vendors that built lighter software architectures. At the same time, the market remained difficult for new entrants that lacked local implementation depth or access to long-standing energy customers. This kept competition active, but it did not remove the practical edge that larger incumbents still held in utility-scale and highly customized deployments.

Japan AI-powered Energy Management Software Industry Leaders

Schneider Electric SE

Siemens AG

Honeywell International Inc.

Johnson Controls International plc

ABB Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Kyushu Electric Power and five major Japanese energy companies, including Tokyo Gas, Panasonic Electric Works, Toho Gas, and West Japan Railway, collectively invested in Shizen Connect, targeting a 2 million kW virtual power plant platform by 2030 that aggregates distributed batteries and solar assets across multiple regional grids using AI-based energy orchestration.

- April 2026: Fujitsu Limited and Chugoku Electric Power Transmission and Distribution signed an IP licensing agreement, effective April 15, 2026, covering dynamic line rating technology and AI-driven wind forecasting, enabling Fujitsu to launch a new grid operation and maintenance service that reduces renewable curtailment and supports drone-based transmission inspection at scale.

- April 2026: Kyushu Electric Power and GRID Inc. commenced full-scale commercial operation of an AI-powered supply-demand plan optimization system that automates daily grid planning, reduces fuel costs through precision scheduling, and standardizes operational quality across dispatch workflows.

- April 2026: Hitachi Energy launched EcoSpace, a digital sustainability platform that quantifies the environmental footprint of power grid projects across their full lifecycle, forming part of the HMAX Energy portfolio and enabling utilities and grid developers to convert sustainability reporting from a compliance obligation into a strategic planning tool.

Japan AI-powered Energy Management Software Market Report Scope

The Japan AI-powered Energy Management Software Market refers to platforms and services that leverage artificial intelligence to optimize energy consumption, improve asset performance, and enable smarter grid and distributed energy resource (DER) management. These solutions include predictive maintenance, renewable energy forecasting, demand-side optimization, and market intelligence for energy trading and pricing.

The Japan AI-powered Energy Management Software Market report is segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Application (Energy Consumption and Demand Optimization, Asset Performance and Predictive Maintenance, Smart Grid and Distributed Energy Resource (DER) Management, Renewable Energy Forecasting and Integration, and Energy Trading, Pricing and Market Intelligence), End User (Utilities, Commercial Buildings, Industrial Facilities, and Residential Buildings). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance |

| Smart Grid and Distributed Energy Resource (DER) Management |

| Renewable Energy Forecasting and Integration |

| Energy Trading, Pricing and Market Intelligence |

| Utilities |

| Commercial Buildings |

| Industrial Facilities |

| Residential Buildings |

| By Component | Software |

| Services | |

| By Deployment Mode | Cloud-Based |

| On-Premises | |

| Hybrid | |

| By Application | Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance | |

| Smart Grid and Distributed Energy Resource (DER) Management | |

| Renewable Energy Forecasting and Integration | |

| Energy Trading, Pricing and Market Intelligence | |

| By End User | Utilities |

| Commercial Buildings | |

| Industrial Facilities | |

| Residential Buildings |

Key Questions Answered in the Report

What is the current size and forecast of Japan AI-powered energy management software demand?

The Japan AI-powered Energy Management Software Market size was USD 0.15 billion in 2025 and is projected to reach USD 0.45 billion by 2031, at a CAGR of 20.11% from 2026 to 2031.

What is driving software adoption in Japan’s energy management space?

The main drivers are wholesale electricity price volatility, wider smart meter and IoT deployment, stronger decarbonization programs, and growing demand for AI-based load shifting and peak optimization.

Which component leads revenue in Japan’s AI-powered energy management software space?

Software led with 67.14% share in 2025 because utilities and enterprises already relied on analytics platforms, demand response engines, and building dashboards for daily operations.

Which deployment model is growing fastest in Japan?

Hybrid deployment is growing fastest at a 20.34% CAGR through 2031 because many organizations need cloud analytics while keeping sensitive operational data in local environments.

Which application area is expanding the fastest?

Renewable energy forecasting and integration is projected to grow at a 20.46% CAGR through 2031 as curtailment, balancing, and grid coordination challenges become more important.

Which end-user group offers the strongest growth outlook?

Industrial facilities are projected to grow at a 20.57% CAGR through 2031 because manufacturers face high electricity costs, tighter emissions compliance, and more on-site energy assets to manage.

Page last updated on: