Germany AI-powered Energy Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

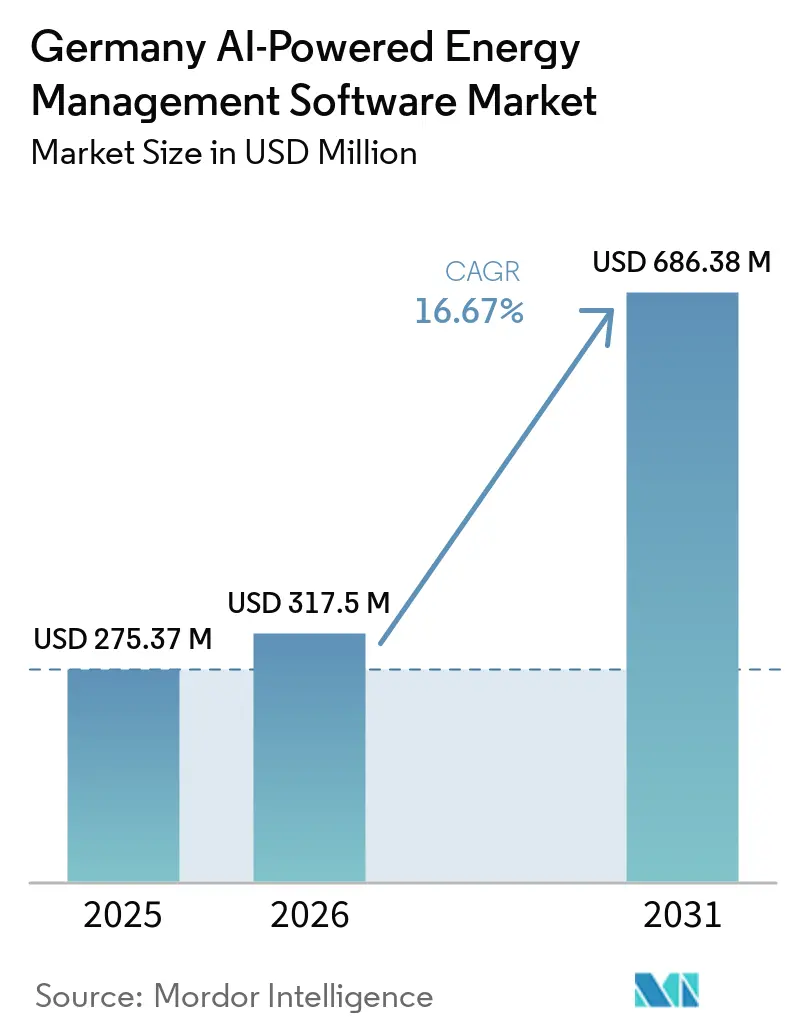

| Base Year Market Size (2025) | USD 275.37 Million |

| Market Size (2026) | USD 317.5 Million |

| Market Size (2031) | USD 686.38 Million |

| Growth Rate (2026 - 2031) | 16.67% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany AI-powered Energy Management Software Market Analysis by Mordor Intelligence

The Germany AI-powered Energy Management Software Market size is expected to increase from USD 275.37 million in 2025 to USD 317.50 million in 2026 and reach USD 686.38 million by 2031, growing at a CAGR of 16.67% over 2026-2031. The growth path is tied to Germany’s energy transition, where higher renewable penetration is pushing utilities, building operators, and industrial users to manage demand and supply with greater precision. The Germany AI-powered Energy Management Software Market is also benefiting from the need to balance flexible loads such as heat pumps, electric vehicle charging, and storage assets in real time. At the same time, the slow rollout of intelligent metering systems is limiting data depth across part of the installed base, which keeps forecasting quality uneven in some use cases. Buyers are increasingly favoring adaptive software and hybrid system designs because they can work with existing infrastructure while still supporting continuous model updates. The competitive field remains moderately fragmented, and vendor selection is increasingly shaped by operational reliability, integration capability, and the ability to support compliance-heavy energy environments.

Key Report Takeaways

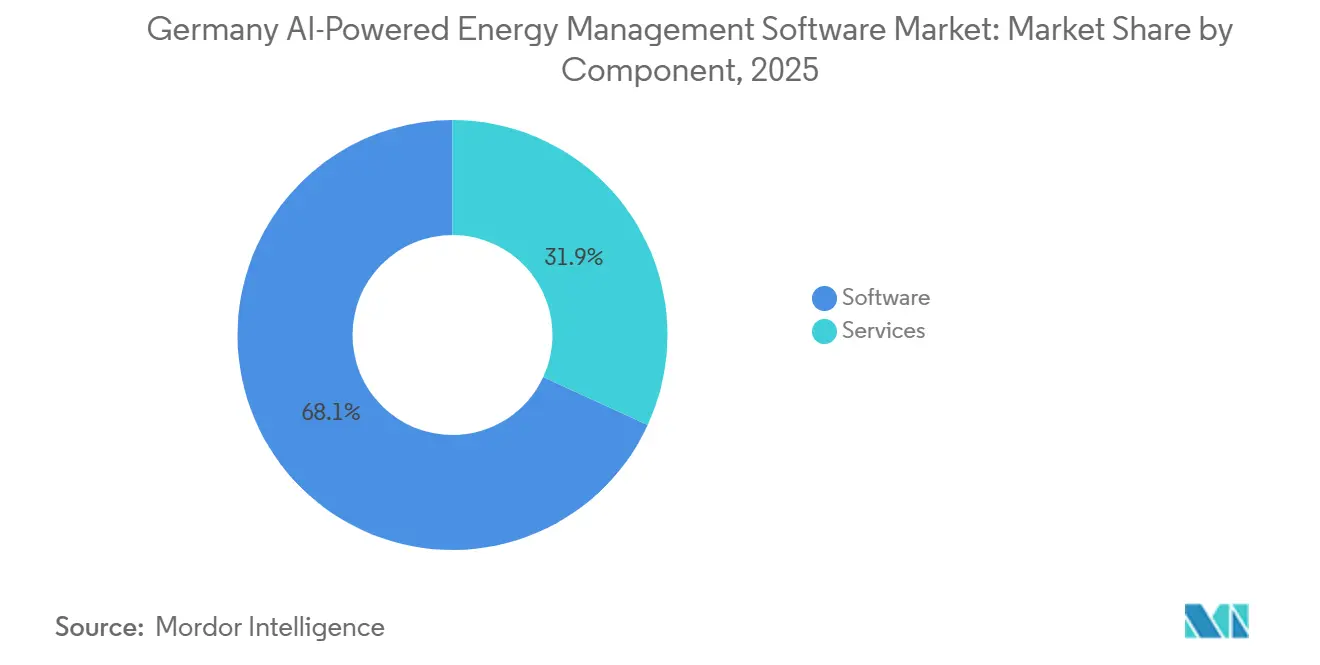

- By component, software accounted for 68.12% of the Germany AI-powered Energy Management Software Market share in 2025, while services are projected to expand at a 18.23% CAGR through 2031.

- By deployment mode, cloud-based deployment held 52.04% share in 2025, while hybrid deployment is projected to grow at an 18.97% CAGR through 2031.

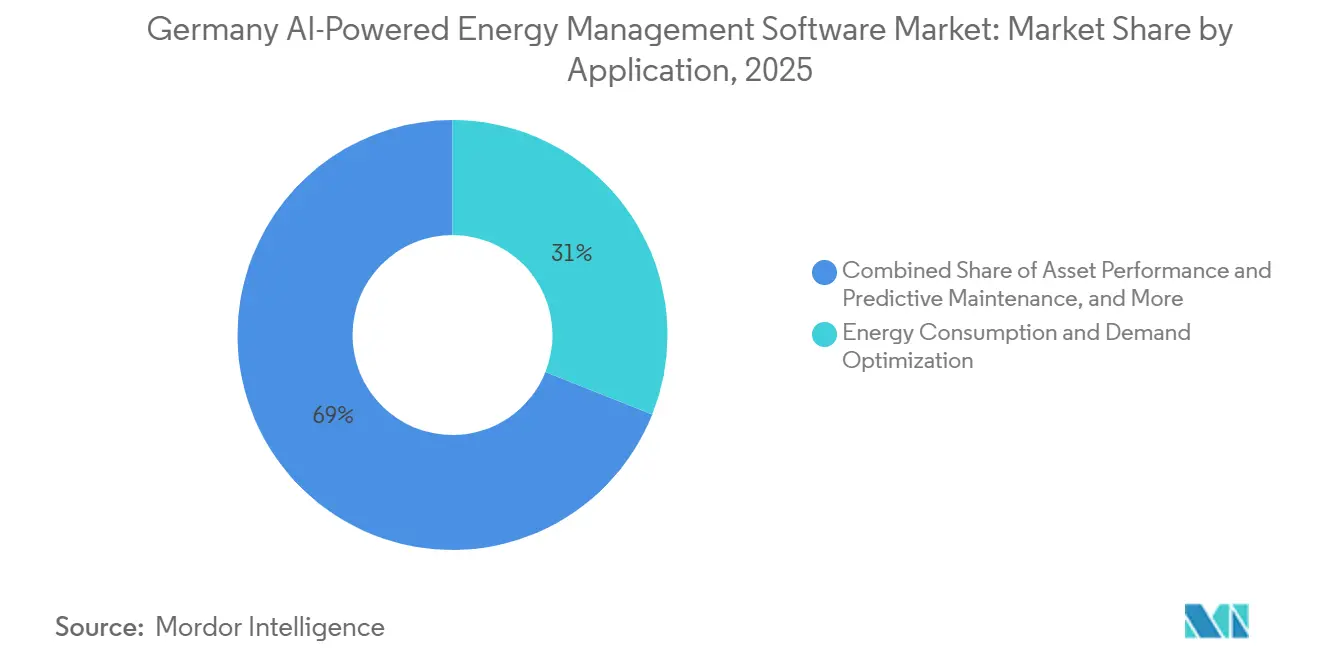

- By application, energy consumption and demand management accounted for 31.02% of the Germany AI-powered Energy Management Software Market in 2025, while asset performance and predictive maintenance are projected to grow at a 21.12% CAGR through 2031.

- By end user, commercial buildings held 39.17% share in 2025, while industrial facilities are projected to grow at a 20.50% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany AI-powered Energy Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Grid Flexibility Requirements | +3.5% | Germany-wide, acute in North Rhine-Westphalia and Baden-Württemberg industrial corridors | Short term (≤ 2 years) |

| Rising Demand For AI-Driven Load Management | +3.0% | Germany-wide, urban commercial and industrial concentration in Bavaria, Hesse, and Hamburg | Short term (≤ 2 years) |

| Expanding Smart Building Retrofit Programs | +2.5% | Germany-wide, concentrated in Bavaria and North Rhine-Westphalia | Medium term (2-4 years) |

| Growing Need For Automated Energy Compliance | +2.0% | Germany-wide with EU-level spillover to cross-border operators | Medium term (2-4 years) |

| Utility Incentives For Demand Response Programs | +1.5% | Germany-wide, early traction in high-renewable regions such as Schleswig-Holstein and Bavaria | Medium term (2-4 years) |

| Increased Adoption Of Edge-Aware Computing | +1.2% | Germany-wide, industrial clusters and critical infrastructure operators | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Grid Flexibility Requirements

Germany’s target to move to 80% renewable electricity by 2030 and fossil-free power generation by 2035 is pushing grid operators to rely on faster digital balancing tools.[1]International Energy Agency, “Germany 2025 - Energy Policy Review,” IEA, iea.org The Dena SET Pilot 4 showed that AI-based control of flexibility in nonresidential buildings can operate with dynamic tariffs and time-variable grid charges in a real operating environment.[2]Deutsche Energie-Agentur, “SET Pilot 4: KI-Basierte Steuerung Von Flexibilitäten Im Nichtwohngebäude,” dena, dena.de That matters because manual control methods cannot keep pace when renewable output, building demand, and flexible loads shift across short time intervals. The Germany AI-powered Energy Management Software Market is therefore seeing stronger demand for platforms that can forecast, dispatch, and optimize with limited delay. This driver is strongest where industrial load density is high, and grid stability needs are more immediate.

Rising Demand For AI-Driven Load Management

Germany’s commercial and industrial power use is under added pressure from electrification, which is increasing the value of flexible and data-driven load control. The Dena pilot confirmed that a hybrid cloud-edge AI energy management system can respond to dynamic tariffs and variable grid charges in ways that align with real operating needs. C3 AI has also demonstrated in enterprise energy deployments that high-frequency forecasting can combine load and price signals within a single decision environment. Buyers now see these tools less as optional analytics and more as a way to reduce peak exposure and improve operational control. The Germany AI-powered Energy Management Software Market is benefiting from this shift, as demand management is becoming a daily operating requirement rather than a pilot use case.

Expanding Smart Building Retrofit Programs

Germany has a large stock of occupied buildings, many of which were built before 1990, making retrofit-led efficiency gains central to future energy demand control. The building sector also accounts for a significant share of final energy use, so even small operational improvements can yield substantial savings at scale. MeteoViva stated in May 2026 that its AI-powered building energy management solution was already managing more than 500 buildings covering 11.5 million sqm across 19 countries. That installed base shows that retrofit-focused AI control is moving from isolated pilots to repeatable deployment across operating assets. The Germany AI-powered Energy Management Software Market is benefiting from retrofits, which create recurring needs for integration, tuning, monitoring, and ongoing performance support.

Growing Need For Automated Energy Compliance

As AI moves deeper into grid and building operations, buyers are placing more weight on traceable control logic, usable records, and dependable reporting outputs. The European Commission’s 2025 smart grid study highlighted that trust, transparency, and governance remain central to broader AI adoption in electricity systems. The Dena pilot also showed that AI control gains acceptance when data flows, tariff logic, and control actions can be clearly followed within the operating process. This is pushing the Germany AI-powered Energy Management Software Market toward vendors that can pair optimization with structured operational documentation. The result is a stronger demand for platforms that support both performance improvement and audit-ready energy records.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Building Data And Legacy Infrastructure | -2.5% | Germany-wide, disproportionate in Eastern Germany and mid-tier municipal utilities | Medium term (2-4 years) |

| Cybersecurity And Data Sovereignty Concerns | -2.0% | Germany-wide, elevated for critical infrastructure operators | Short term (≤ 2 years) |

| High Integration And Change Management Costs | -1.5% | Germany-wide, pronounced in SME and municipal utility segments | Medium term (2-4 years) |

| Limited Trust In Autonomous Control Systems | -1.0% | Germany-wide, highest friction in utilities with legacy operational culture | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Building Data And Legacy Infrastructure

Germany amended the Messstellenbetriebsgesetz in February 2025 to accelerate smart meter rollout, which showed that deployment was still behind what the energy transition requires. Dena also identified faster smart meter rollout as one of the unresolved structural conditions for scaling AI-based flexibility control. Where buildings and utility systems still operate with incomplete device, meter, and control records, AI models start from weaker inputs. That slows the Germany AI-powered Energy Management Software Market because buyers want proof of performance before they expand deployments across older portfolios. Legacy infrastructure, therefore, remains a practical barrier even when long-term demand conditions are favorable.

Cybersecurity And Data Sovereignty Concerns

Energy control platforms in grids, buildings, and industrial sites handle operational data that buyers treat as highly sensitive. The European Commission’s smart grid study noted that trust, governance, and secure data handling are central to the wider deployment of AI across network operations. Dena’s pilot design relied on a hybrid cloud-edge architecture, reflecting the need to keep some control functions close to the asset while leveraging broader optimization capabilities. This adds complexity because vendors must demonstrate stable operation across both local and remote environments simultaneously. The Germany AI-powered Energy Management Software Market, therefore, faces longer qualification cycles when utilities and industrial users seek stronger assurance of data control and system resilience.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Platforms Lead Delivery Across Use Cases

Software captured 68.12% of the German AI-Powered Energy Management System market in 2025, which shows that buyers are prioritizing adaptable digital layers over hardware-led replacement cycles. Software leadership is tied to its ability to work with existing building automation, smart meter gateways, and utility control environments without forcing a full rebuild of installed systems. The Germany AI-powered Energy Management Software Market also favors software, as subscription models can update forecasting and optimization logic as the generation mix and tariff environment change. Services are projected to expand at a 18.23% CAGR through 2031, as implementation, model retraining, support, and operational tuning continue after the initial rollout.

This segment is also shaped by the move away from single-purpose tools toward platforms that combine forecasting, monitoring, predictive maintenance, and demand response in a single operating layer. Buyers across utilities, buildings, and industrial sites are trying to reduce system fragmentation, which supports broader software adoption in the Germany AI-powered Energy Management Software Market. In January 2026, Itron deepened its Microsoft collaboration and integrated generative AI technology into the Intelligent Edge Operating System, demonstrating how major vendors are expanding software capabilities across their installed infrastructure base. Software, therefore, remains the anchor segment, while services grow faster as deployments become more operationally complex.

By Deployment Mode: Hybrid Setups Match Real-Time Control Needs

Cloud-based deployment held 52.04% of the Germany AI-powered Energy Management Software Market size in 2025, supported by easier scaling, lower upfront burden, and faster access to updated AI tools. On-premises setups still matter where operators want tighter local control over operational data and site-level decision paths.[3]European Climate, Infrastructure and Environment Executive Agency, “Unlocking The Potential Of AI And Generative AI In European Smart Grids,” Publications Office of the European Union, europa.eu Hybrid deployment is projected to grow at a 18.97% CAGR through 2031, as it combines local response speed with broader optimization across connected assets. That balance is important in the Germany AI-powered Energy Management Software Market, where site responsiveness and centralized analytics both carry weight.

The Dena pilot provided a practical reference point by using a hybrid cloud-edge architecture for AI-based flexibility control in a non-residential building. The model works because facilities can react quickly on-site while still using broader datasets for optimization and learning. The Germany AI-powered Energy Management Software Market is therefore moving beyond a simple cloud-versus-on-premises choice toward deployment models built around control speed, auditability, and integration depth. Vendors that can demonstrate clean data flows across the edge and the cloud are likely to win more utility and industrial tenders.

By Application: Demand Control Leads While Predictive Uses Expand Faster

Energy consumption and demand management accounted for 31.02% of the Germany AI-powered Energy Management Software Market in 2025, reflecting its role as the first deployment point for many buyers. This application usually arises from a clear operational problem: the need to reduce energy waste, manage peaks, and respond better to changing grid conditions. The Germany AI-powered Energy Management Software Market is also seeing broader demand for renewable forecasting and distributed energy resource management as higher renewable penetration increases balancing complexity. That shift is moving AI from periodic planning into daily operating control for utilities and large energy users.

Asset performance and predictive maintenance are projected to grow at a 21.12% CAGR through 2031, making it the fastest-growing application area in this market. The appeal lies in the fact that the same data stack used for energy control can also detect equipment drift, support maintenance scheduling, and improve system uptime. The Germany AI-powered Energy Management Software Market is also expanding into pricing, dispatch, and other trading-related decisions as flexible assets and storage systems become more valuable in dynamic electricity markets. This broadening application scope gives vendors more room to expand within existing customer accounts after the first energy management use case is proven.

By End User: Commercial Buildings Lead While Industrial Facilities Gain Speed

Commercial buildings held 39.17% of the Germany AI-powered Energy Management Software Market share in 2025, making them the largest end-user segment. This lead reflects the combination of large addressable floor area, stronger pressure to improve operating efficiency, and the need for clearer building-level energy records. meteoviva’s stated footprint of more than 500 buildings across 19 countries, including major German reference sites, shows that building operators are already willing to scale AI control once the model is proven. The Germany AI-powered Energy Management Software Market has gained early traction in this segment because control improvements can be measured across portfolios and translated into operating outcomes.

Industrial facilities are projected to grow at a 20.50% CAGR through 2031, making them the fastest-growing end-user segment. Germany’s energy-intensive manufacturing regions face stronger pressure to shape demand, protect margins, and operate more flexibly as grid conditions change. Utilities remain strategically important in the Germany AI-powered Energy Management Software Market because their adoption affects the quality of grid-side data and the pace of demand response expansion. Residential buildings are still smaller in current revenue terms, but their long-run potential improves as smart meter availability expands and connected home energy control becomes easier to deploy.[4]Bundesministerium Für Wirtschaft Und Energie, “Bundesrat Bestätigt Änderungen Für Schnelleren Smart-Meter-Rollout,” Bundesministerium Für Wirtschaft Und Energie, bundeswirtschaftsministerium.de

Geography Analysis

Germany AI-powered Energy Management Software Market size stood at USD 275.37 million in 2025, and it is forecast to reach USD 686.38 million by 2031. Germany stands apart as a single national market because its energy transition, industrial base, and utility structure create a distinct demand pattern for AI-led energy control. Renewable electricity accounted for more than 60% of national output in 2024, underscoring the need for better balancing, forecasting, and flexible load orchestration. The Germany AI-powered Energy Management Software Market is also shaped by a highly distributed utility landscape, with many local operators managing different procurement speeds and system maturity levels. That mix creates strong demand, but it also slows standardization across the country. IEA.ORG

North Rhine-Westphalia and Baden-Württemberg remain central to industrial demand due to their concentration of automotive, chemical, and heavy manufacturing activity. Bavaria is another important growth area, supported by a mix of industrial technology activity and major commercial building deployments that already use AI-based control systems. Hamburg and Hesse support commercial uptake because dense office, logistics, and service-sector assets benefit from tighter energy visibility and faster control. Eastern states also present room for storage optimization and renewable-linked control applications where generation patterns and local load are less balanced.

Germany is interconnected with 9 neighboring countries, which raises the value of better forecasting and flexible power management inside a wider European electricity system. The European Commission’s 2025 study identified Germany as one of the leading national markets for AI grid intelligence deployment in Europe. The Germany AI-powered Energy Management Software Market therefore rewards vendors that can fit local operating conditions while still supporting regional power system dynamics. Local implementation knowledge remains important because utility structures, building stock quality, and digital readiness still vary across regions.

Competitive Landscape

The Germany AI-powered Energy Management Software Market remains moderately fragmented, and no single vendor holds a dominant share. Global providers such as Itron, C3.ai, Landis+Gyr, Siemens, ABB, and Schneider Electric compete alongside Germany-rooted specialists such as meteoviva, gridX, Lumenaza, Tibber, Smappee, and ZENNER International GmbH & Co. KG. This broad field means competition is spread across utilities, commercial buildings, industrial facilities, and emerging distributed energy use cases. Large multinational vendors usually enter with established metering, grid, or automation relationships that give them a path into larger contracts. Germany-based specialists compete more on localized integration, building-level control depth, and the ability to execute in domestic operating environments.

In January 2026, Itron expanded its Microsoft collaboration and integrated generative AI into the Intelligent Edge Operating System, strengthening its software layer for utility data workflows. In March 2025, Itron and Microsoft had already opened natural-language access to grid and metering data, showing a clear push to make complex energy data easier for operators to use. In May 2025, Landis+Gyr introduced the L440 LTE-based load-switching device for EMEA markets, expanding its grid flexibility offering for retailers and network operators. These moves show that large vendors are trying to integrate metering, control, and AI services within a single customer stack.

In May 2026, Bregal Milestone completed a majority growth investment in Meteoviva, which added financial backing to a vendor already managing more than 500 buildings and 11.5 million sqm across 19 countries. In April 2026, ZENNER reported that its LoRaWAN network had reached 11 million active sensors, which strengthens the monitoring and data layer that energy management solutions can build on. The Germany AI-powered Energy Management Software Market still has room to grow in municipal utilities and mid-sized industrial sites, where legacy integration work and limited procurement capacity often slow adoption more than demand does. Vendors that combine proven operating data, practical deployment support, and flexible system design are likely to remain better positioned as adoption broadens.

Germany AI-powered Energy Management Software Industry Leaders

ecoplanet GmbH

BrainBox AI Inc.

Bidgely, Inc.

AutoGrid Systems, Inc.

Verdigris Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Bregal Milestone completed a majority growth investment in meteoviva GmbH, Aachen, an AI-powered building energy management provider managing 500-plus buildings covering 11.5 million sqm across 19 countries. The deal funds accelerated European expansion and continued investment in meteoviva's autonomous control and AI roadmap. meteoviva is the first provider in its category certified by the German Sustainable Building Council (DGNB).

- April 2026: ZENNER International GmbH & Co. KG's Minol-ZENNER Group LoRaWAN network reached 11 million active sensors, up from 10 million in September 2025, as the company accelerated its nationwide smart water and energy monitoring rollout targeting full Smart Water Solution deployment by year-end 2026.

- January 2026: Itron deepened its AI collaboration with Microsoft, integrating Microsoft's generative AI Copilot technology into the Itron Intelligent Edge Operating System (IEOS) to enable natural-language queries for utility data science functions, expanding a collaboration originally launched in March 2025.

- May 2025: Landis+Gyr introduced the L440 LTE-based load-switching device for EMEA markets, expanding its grid flexibility portfolio with an IoT-standard LTE alternative to its G3-PLC solutions, enabling real-time load management for energy retailers and network operators across European utility networks.

Germany AI-powered Energy Management Software Market Report Scope

The Germany AI-powered Energy Management Software Market Report is Segmented by Component (Software, Services), Deployment Mode (Cloud-Based, On-Premises, Hybrid), Application (Energy Consumption, Asset Performance, Smart Grid, Renewable Forecasting, Energy Trading), and End User (Utilities, Commercial Buildings, Industrial Facilities, Residential Buildings). The Market Forecasts are in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance |

| Smart Grid and Distributed Energy Resource (DER) Management |

| Renewable Energy Forecasting and Integration |

| Energy Trading, Pricing and Market Intelligence |

| Utilities |

| Commercial Buildings |

| Industrial Facilities |

| Residential Buildings |

| By Component | Software |

| Services | |

| By Deployment Mode | Cloud-Based |

| On-Premises | |

| Hybrid | |

| By Application | Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance | |

| Smart Grid and Distributed Energy Resource (DER) Management | |

| Renewable Energy Forecasting and Integration | |

| Energy Trading, Pricing and Market Intelligence | |

| By End User | Utilities |

| Commercial Buildings | |

| Industrial Facilities | |

| Residential Buildings |

Key Questions Answered in the Report

What is the size outlook for the Germany AI-powered Energy Management Software Market?

The Germany AI-powered Energy Management Software Market size is expected to rise from USD 317.50 million in 2026 to USD 686.38 million by 2031, at a CAGR of 16.67% over 2026-2031.

Which component leads adoption in Germany AI-powered energy management software?

Software led with 68.12% share in 2025 because buyers prefer adaptable platforms that work with existing infrastructure and allow ongoing model updates.

Which deployment model is growing the fastest in Germany?

Hybrid deployment is the fastest-growing model, with an 18.97% CAGR through 2031, because it combines local response speed with broader cloud-based optimization.

What is the largest application area in this space?

Energy consumption and demand management was the largest application in 2025, with a 31.02% share, as it is usually the first use case buyers adopt.

Which end-user group is expanding the fastest?

Industrial facilities are projected to grow at a 20.50% CAGR through 2031, supported by rising pressure to manage peak demand and operate more flexibly.

What is slowing wider adoption across Germany?

Slow smart meter rollout, fragmented building data, legacy systems, and longer qualification cycles around secure data handling are still limiting faster scale-up.

Page last updated on: