Host Computer Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

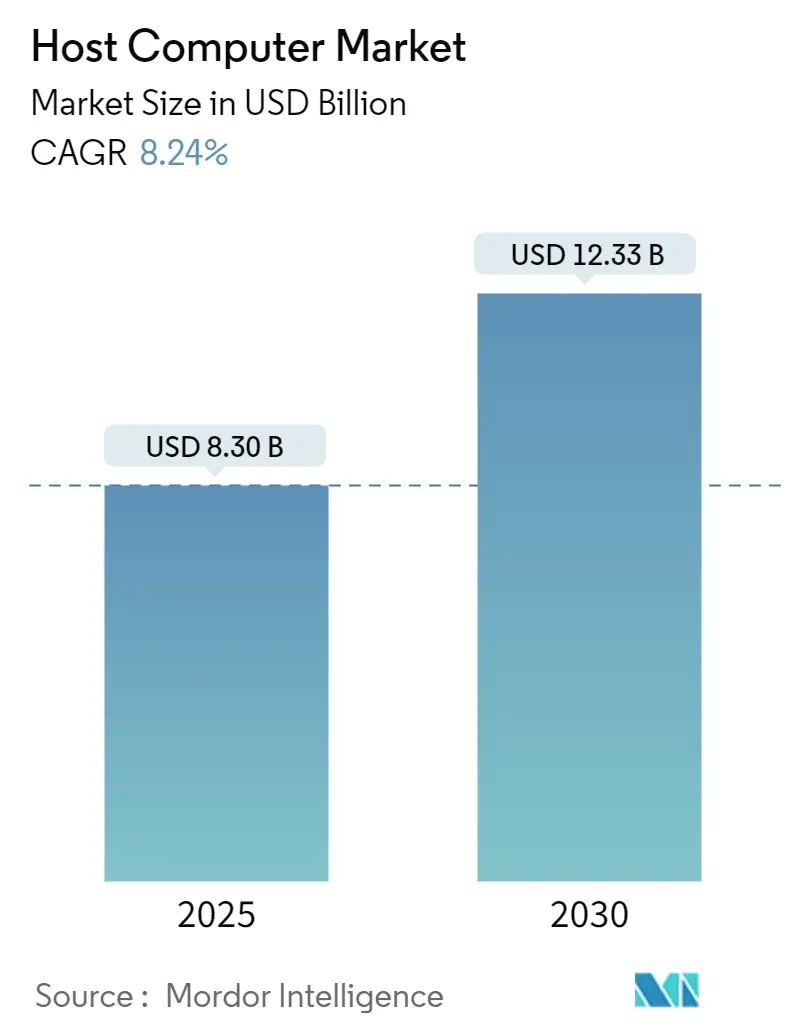

| Market Size (2025) | USD 8.30 Billion |

| Market Size (2030) | USD 12.33 Billion |

| Growth Rate (2025 - 2030) | 8.24% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Host Computer Market Analysis by Mordor Intelligence

The host computer market size is estimated to be USD 8.3 billion in 2025 and is projected to reach USD 12.33 billion by 2030, reflecting an 8.24% CAGR over the forecast period. Momentum stems from hyperscale data center investments, the escalating need for AI-ready compute, and a decisive pivot toward hybrid infrastructure architectures. Energy-efficient blade and rack designs, coupled with Linux-centric deployments, are widening adoption in regulated sectors and digital-first enterprises. Vendors are racing to add GPU density, liquid cooling, and open-source firmware as immediate differentiators. At the same time, public-private sustainability mandates and semiconductor supply safeguards are shaping long-term procurement norms.

Key Report Takeaways

- By technology, cloud-based host computers led the market with a 42.44% share, while hybrid deployments are forecasted to expand at a 10.22% CAGR through 2030.

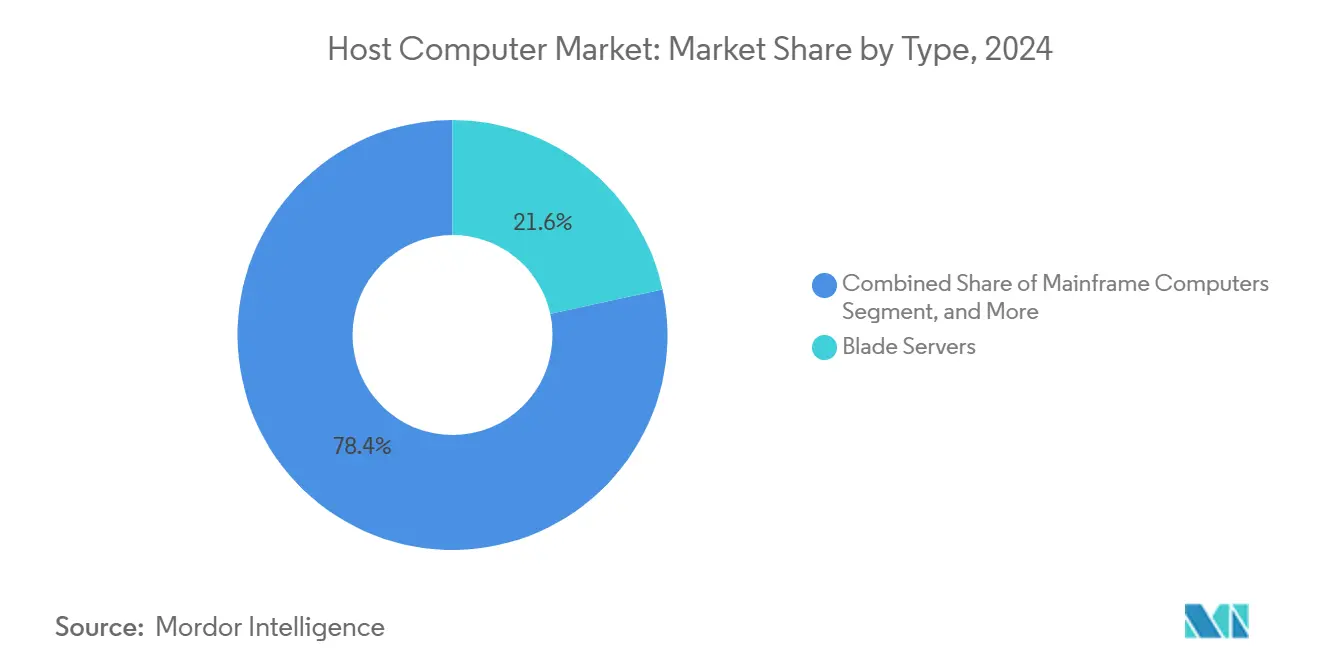

- By type, blade servers captured 21.6% of the 2024 host computer market share and are projected to rise at a 10.06% CAGR through 2030.

- By application, cloud computing accounted for 35.59% of the 2024 host computer market size, whereas artificial intelligence and machine learning are projected to advance at an 8.67% CAGR through 2030.

- By end-user industry, IT and telecom commanded 29.67% of the 2024 host computer market size, while healthcare recorded the highest projected CAGR at 8.91% through 2030.

- By deployment mode, shared hosting accounted for 38.78% of the host computer market size in 2024 while cloud hosting is projected to advance at a 9.89% CAGR through 2030.

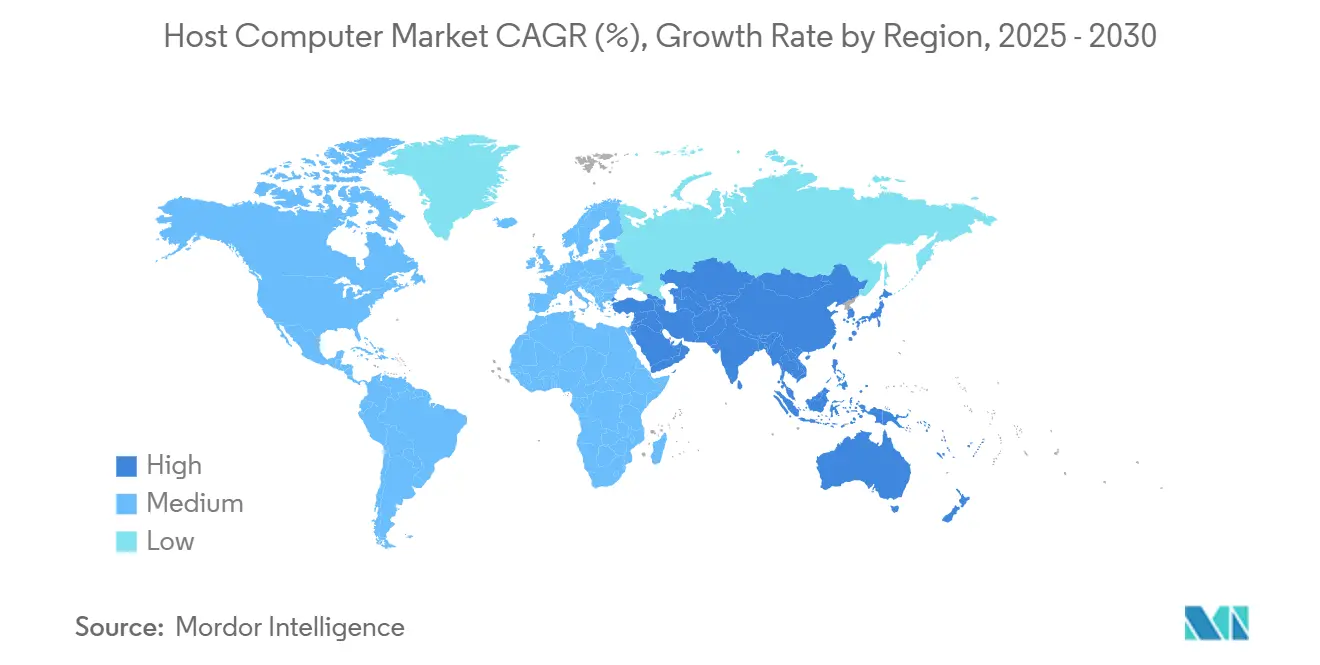

- By geography, Asia Pacific is set to expand at a 9.45% CAGR between 2025-2030, outpacing North America’s mature base.

Global Host Computer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of cloud computing across enterprises | +2.10% | Global | Short term (≤ 2 years) |

| Expansion of data centers and hyperscale computing | +1.80% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Growth in big data analytics and AI workloads | +2.00% | North America, Europe, Asia Pacific | Medium term (2-4 years) |

| Shift towards virtualization and software-defined infrastructures | +1.00% | Global | Short term (≤ 2 years) |

| Emergence of edge-to-cloud host computer orchestration | +0.70% | North America, Europe | Long term (≥ 4 years) |

| Adoption of open-source RISC-V architectures in host servers | +0.50% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Cloud Computing Across Enterprises

Cloud migration remains the leading catalyst for the host computer market, with hyperscalers elevating 2025 capital outlays to meet multi-tenant and hybrid demand.[1]Microsoft Corporation, “2025 Annual Report,” MICROSOFT.COM Enterprises favor container orchestration, such as Kubernetes, and Linux-based instances to accelerate DevOps cycles while staying compliant with GDPR and HIPAA. Higher core counts and integrated accelerators are now table stakes for new deployments, driving up average selling prices. Early adopters in the Asia Pacific and North America are also benchmarking liquid-cooled racks to curb power usage effectiveness. Together, these factors reinforce near-term revenue visibility for vendors across the host computer industry.

Expansion of Data Centers and Hyperscale Computing

Fresh capacity from more than 200 announced hyperscale facilities in 2025 underpins steady server refresh volumes. Government land-grant incentives in India, Malaysia, and Indonesia are expanding the hyperscale footprint, while green-energy credits in the Nordics and North America are supporting renewable-powered campuses. Operators prioritize modular pods, immersive cooling, and on-site substation builds to offset rising power densities that exceed 30 kW per rack. ISO 50001 compliance is increasingly embedded in procurement scorecards, positioning energy-optimized host computer configurations as the default across tender requests.

Growth in Big Data Analytics and AI Workloads

Enterprise AI use cases, ranging from real-time fraud detection to precision diagnostics, require GPU-dense compute, high-bandwidth memory, and NVMe fabrics.[2]NVIDIA Corporation, “Annual Report 2025,” NVIDIA.COM Blade and rack servers optimized for accelerators top purchase lists in healthcare, BFSI, and manufacturing. Demand for deterministic latency also drives the rollout of edge servers that cache and infer locally before syncing to the cloud. Regulatory focus from the FDA and EMA on traceability mandates tamper-proof logging, driving uptake of immutable storage and hardware-root-of-trust modules within next-generation host computer market deployments.

Shift Towards Virtualization and Software-Defined Infrastructures

Software-defined infrastructure decouples workloads from physical assets, letting administrators orchestrate resources across hybrid estates.[3]Red Hat Inc., “Red Hat Virtualization 2025,” REDHAT.COM Containers now outpace hypervisor installs, streamlining CI/CD pipelines and cutting licensing costs. ISO/IEC 27001 frameworks encourage enterprises to implement consistent security policies across bare-metal, virtual, and cloud environments. As operational complexity rises, automation tooling and infrastructure-as-code adoption escalate, compressing provisioning times from weeks to hours and solidifying virtualization as an indispensable growth lever for the host computer market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial capital expenditure for advanced host computers | -1.60% | Global, with acute impact in Asia-Pacific | Short term (≤ 2 years) |

| Energy consumption concerns and cooling costs | -1.20% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Supply chain volatility for advanced semiconductor components | -1.00% | Global | Short term (≤ 2 years) |

| Skills gap in managing heterogeneous host computer environments | -0.80% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Expenditure for Advanced Host Computers

The cost of GPU-rich blade enclosures, liquid cooling, and redundant power systems remains prohibitive for mid-sized enterprises.[4]Dell Technologies Inc., “2025 10-K Filing,” DELLTECHNOLOGIES.COM Semiconductor shortages add pricing pressure, pushing organizations to favour pay-as-you-use cloud bursts. Accelerated depreciation allowances and tax holidays mitigate the impact in select jurisdictions, but adoption gaps persist in emerging economies, which weigh on near-term unit volumes.

Energy Consumption Concerns and Cooling Costs

Utility rates climbing above USD 0.10 per kWh in parts of Europe and Asia heighten operating costs, prompting operators to pilot liquid or rear-door heat exchanger cooling. Carbon taxes and ESG disclosures further incentivize renewable procurement, yet grid constraints slow progress in legacy urban hubs. Vendors able to guarantee 30% lower power draw per compute unit secure a competitive preference, making efficiency a strategic differentiator across the host computer market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Modularization Drives Performance and Density

Blade servers generated notable traction, accounting for 21.6% of 2024 shipments and adding USD 1.46 billion to the host computer market size. This sub-category is forecast to compound at 10.06% annually, aided by edge deployments that value modular swaps and chassis-level management. Blade form factors condense CPU and GPU nodes, allowing up to 20 blades per 6U chassis a design that cuts floor space by one-third compared to traditional racks. Over the forecast horizon, increased ASIC offload and the adoption of liquid cooling trays are anticipated, extending the segment’s appeal. Mainframes and minicomputers continue to support banking transaction systems and public-sector records, although their upgrade cycles have elongated beyond seven years, tempering volume growth.

Rack servers remain the workhorse class for scale-out data centers, offering flexibility while supporting multi-vendor component sourcing. Incremental gains in telemetry and BIOS-level security have preserved relevance. Workstations serve specialized CAD and media workflows; the category benefits from integrated AI accelerators and upgraded graphics pipelines. Collectively, diversified form factors keep the host computer market resilient to shocks from single segments, while positioning vendors for broad bid participation.

By Technology: Hybrid Deployments Shape Future Architectures

Cloud-based host computers held a 42.44% revenue share in 2024, translating to USD 3.52 billion within the host computer market. Hybrid estates, however, are projected to register the fastest growth, increasing at a rate of 10.22% annually until 2030. Enterprises balance data sovereignty and latency needs by placing low-latency workloads on-premises while scaling burst capacity into the public cloud. Managed service providers are increasingly bundling on-premises gear under consumption-based contracts, blending opex predictability with hardware control. On-premises deployments persist in defense, government, and heavily regulated financial sectors due to compliance requirements.

Vendor roadmaps emphasize seamless workload migration, observability, and unified security controls across private and public domains. Such features drive platform stickiness and unlock cross-sell for observability suites, reinforcing revenue depth in the host computer industry. Open-source RISC-V proof-of-concepts signal further diversification, although commercial adoption will mature gradually after 2027.

By Application: AI and ML Accelerate Infrastructure Demands

Cloud computing applications dominated with 35.59% of 2024 revenue, equal to USD 2.94 billion of the host computer market size. Artificial intelligence and machine learning workloads are projected to record the strongest growth path, with an 8.67% CAGR through 2030, driven by enterprise retraining cycles and the adoption of generative models. GPU-dense nodes, high-speed interconnects, and software stacks such as CUDA and ROCm form core procurement criteria for AI buyers.

Big data analytics and HPC are also advancing, demanding high core counts and parallelism. Networking and data processing remain foundational, underpinning every vertical’s digital operation. For compliance-heavy sectors, PCI DSS and HIPAA frameworks dictate strict encryption and access controls, compelling procurement of hardware root-of-trust modules and tamper-proof logs. These combined factors sustain multi-segment demand across the host computer market.

By End User Industry: Healthcare Surges Amid Digital Transformation

IT and telecom operators led 2024 consumption, accounting for 29.67% of shipments and USD 2.46 billion of the host computer market size. They refresh server fleets on 36-month cycles to support 5G rollouts and OTT streaming. Healthcare is forecasted to register the highest growth of 8.91% CAGR, driven by the scaling of telehealth, imaging analytics, and EHR modernization. AI-assisted diagnostics require hospitals to invest in GPU clusters, while regulators enforce strict uptime and encryption standards.

BFSI sustains demand for low-latency trading and fraud analytics infrastructures. Manufacturing embraces digital twins and smart factory controls, leveraging edge-based host computers. Across all verticals, the skills gap in multi-platform orchestration amplifies appetite for managed services, further anchoring revenue in the wider host computer industry.

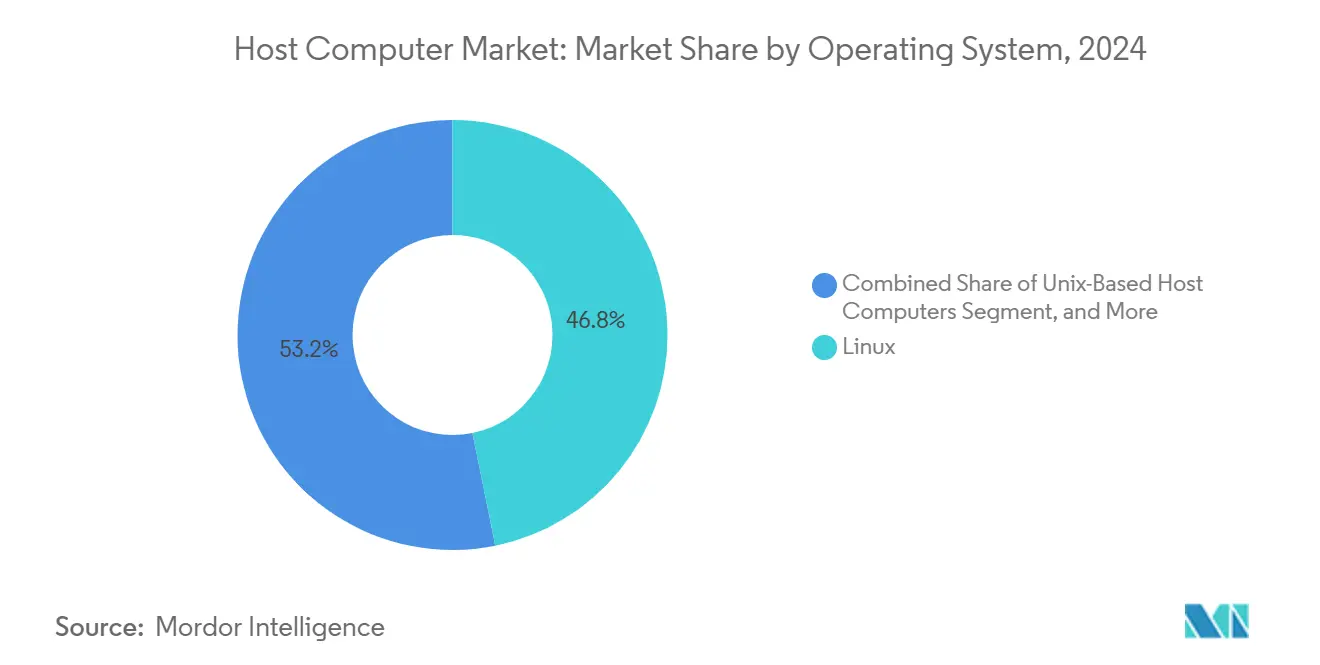

By Operating System: Linux-Based Systems Dominate

Linux secured 46.81% of 2024 deployments, translating to USD 3.87 billion within the host computer market. Favourable licensing, robust container support, and an expansive developer base drive preference in AI, cloud, and edge workloads. Enterprises reinforce compliance by referencing the Open Chain ISO/IEC 5230 standard, ensuring updated component inventories and vulnerability patches.

Windows-based systems continue to favour enterprise line-of-business applications, particularly in mid-market organizations that depend on Active Directory. UNIX variants persist in legacy finance and government estates. Collectively, heterogenous OS footprints necessitate orchestration suites capable of cross-platform policy enforcement, sustaining growth momentum for automation vendors.

By Deployment Mode: Shared Hosting Remains Prevalent

Shared hosting accounted for 38.78% of 2024 revenue, reflecting the cost-effective provision of compute resources for SMB websites and SaaS startups. Cloud hosting represents the fastest-growing trajectory, with a 9.89% CAGR amid surging microservice adoption. Dedicated hosting and colocation secure interest from enterprises balancing latency, compliance, and cost. Operators bundle SOC 2 and ISO/IEC 27001 certifications as default credentials, de-risking customer audits and lifting confidence in outsourced infrastructure.

Marketplace-style portals ease seat expansion and automated ticketing, trimming operational overhead. In parallel, serverless functions, GPU instances, and managed databases enhance the value proposition, expanding the total addressable market for the host computer market.

Geography Analysis

North America accounted for 34.23% of 2024 revenue, equal to USD 2.84 billion in the host computer market. Hyperscalers headquartered in the United States commit multibillion-dollar construction budgets, while state-level clean-energy credits accelerate the adoption of renewable generation. AI platform rollouts across healthcare and fintech sustain demand for GPU-dense nodes. Regulatory influences from the U.S. Department of Energy on PUE reporting, as well as evolving state privacy statutes, encourage investment in efficient and auditable architectures. Competitive intensity rises as managed service providers partner with semiconductor fabs to secure chip availability.

The Asia Pacific is forecast to exhibit a 9.45% CAGR through 2030, the fastest growth rate globally. Digital financial inclusion, nationwide 5G, and cloud-first policies in India, China, and Indonesia are headline drivers. Government incentives, including zero-duty server imports and property tax abatements, attract hyperscale builders. Data localization requirements prompt cloud vendors to deploy local availability zones, driving sustained demand for servers. Emerging hubs such as Australia and South Korea champion edge data centers paired with renewable integration, bolstering green compute uptake.

Europe follows steady expansion, balanced by mature Western markets and catch-up investment in Central and Eastern member states. GDPR-driven data residency obligations spur in-region hosting, while the European Green Deal incentivizes 2030 climate targets. Operators pilot district-heating reuse of server exhaust and adopt waste-heat regulations, aligning sustainability with bottom-line gains. Colocation capacity in Frankfurt, Amsterdam, Paris, and Dublin continues to sell out, underscoring persistent demand across the host computer market.

Competitive Landscape

The market structure remains moderately concentrated, with Dell Technologies, Hewlett Packard Enterprise, and Lenovo each retaining diverse server portfolios and global channel depth. These vendors bundle integrated management suites, edge-capable form factors, and flexible consumption financing to defend share. Entrants leveraging open-source RISC-V cores aim to undercut x86 incumbents on total cost, although ecosystem maturity may delay meaningful share gains until after 2027.

Strategic alliances emerge as a hedge against semiconductor constraints, exemplified by joint design centers between server OEMs and leading foundries. Patent filings on liquid cooling manifolds and AI workload scheduling underscore R&D prioritization of energy optimization and accelerator utilization. Vendors publicize their conformity to ISO 50001 and ISO/IEC 27001 as competitive proof points. Meanwhile, ODMs headquartered in Taiwan and China extend white-label offerings to cloud providers seeking customization. Collectively, innovation cadence and supply resilience define long-term positioning in the host computer market.

Host Computer Industry Leaders

Dell Technologies Inc.

Hewlett Packard Enterprise Company

International Business Machines Corporation

Cisco Systems Inc.

Lenovo Group Limited.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Dell Technologies and Intel announced a USD 200 million joint investment to develop next-generation liquid-cooled servers optimized for AI workloads, targeting hyperscale data centers in North America and Asia Pacific.

- September 2025: HPE completed the acquisition of a leading-edge computing startup to bolster its hybrid cloud and AI portfolio, expanding its presence in the Asia Pacific region and accelerating time-to-market for edge-to-cloud orchestration solutions.

- August 2025: Lenovo has launched a new line of modular blade servers with integrated AI accelerators, targeting healthcare and financial services clients who seek scalable, energy-efficient infrastructure for machine learning applications.

- July 2025: IBM unveiled its OpenShift-based mainframe solution, enabling seamless integration of legacy workloads with cloud-native applications, with early adoption reported in the BFSI sector.

Global Host Computer Market Report Scope

The Host Computer Market Report is Segmented by Type (Mainframe Computers, Minicomputers, Microcomputers, Workstations, Servers, Blade Servers, Rack Servers), Technology (Cloud-Based Host Computers, On-Premises Host Computers, Hybrid Deployments), Application (Data Processing, Cloud Computing, Virtualization, Networking, Big Data Analytics, Artificial Intelligence and Machine Learning, High-Performance Computing), End User Industry (IT and Telecom, Banking, Financial Services, and Insurance, Healthcare, Government, Manufacturing, Retail, Media and Entertainment, Education, Others), Operating System (Windows-Based Host Computers, Linux-Based Host Computers, UNIX-Based Host Computers), Deployment Mode (Free Hosting, Shared Hosting, Dedicated Hosting, Collocated Hosting), and Geography (North America, South America, Europe, Asia Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Mainframe Computers |

| Minicomputers |

| Microcomputers |

| Workstations |

| Servers |

| Blade Servers |

| Rack Servers |

| Cloud-Based Host Computers |

| On-Premises Host Computers |

| Hybrid Deployments |

| Data Processing |

| Cloud Computing |

| Virtualization |

| Networking |

| Big Data Analytics |

| Artificial Intelligence And Machine Learning |

| High-Performance Computing (HPC) |

| IT And Telecom |

| Banking, Financial Services, And Insurance (BFSI) |

| Healthcare |

| Government |

| Manufacturing |

| Retail |

| Media And Entertainment |

| Education |

| Other End-User Industries |

| Windows-Based Host Computers |

| Linux-Based Host Computers |

| Unix-Based Host Computers |

| Free Hosting |

| Shared Hosting |

| Dedicated Hosting |

| Collocated Hosting |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Type | Mainframe Computers | |

| Minicomputers | ||

| Microcomputers | ||

| Workstations | ||

| Servers | ||

| Blade Servers | ||

| Rack Servers | ||

| By Technology | Cloud-Based Host Computers | |

| On-Premises Host Computers | ||

| Hybrid Deployments | ||

| By Application | Data Processing | |

| Cloud Computing | ||

| Virtualization | ||

| Networking | ||

| Big Data Analytics | ||

| Artificial Intelligence And Machine Learning | ||

| High-Performance Computing (HPC) | ||

| By End User Industry | IT And Telecom | |

| Banking, Financial Services, And Insurance (BFSI) | ||

| Healthcare | ||

| Government | ||

| Manufacturing | ||

| Retail | ||

| Media And Entertainment | ||

| Education | ||

| Other End-User Industries | ||

| By Operating System | Windows-Based Host Computers | |

| Linux-Based Host Computers | ||

| Unix-Based Host Computers | ||

| By Deployment Mode | Free Hosting | |

| Shared Hosting | ||

| Dedicated Hosting | ||

| Collocated Hosting | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the 2025 valuation of the host computer market?

The host computer market size is valued at USD 8.3 billion in 2025.

How fast is the market expected to grow by 2030?

It is projected to reach USD 12.33 billion by 2030, registering an 8.24% CAGR.

Which technology segment currently holds the largest share?

Cloud-based host computers led with a 42.44% share in 2024.

Which region is forecast to expand the fastest through 2030?

Asia Pacific is set to advance at a 9.45% CAGR over the forecast period.

What hardware type is growing quickest?

Blade servers are projected to post a 10.06% CAGR between 2025-2030.

Which end-user vertical shows the highest growth outlook?

Healthcare is expected to grow at an 8.91% CAGR through 2030.

Page last updated on: