Desktop Workstation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

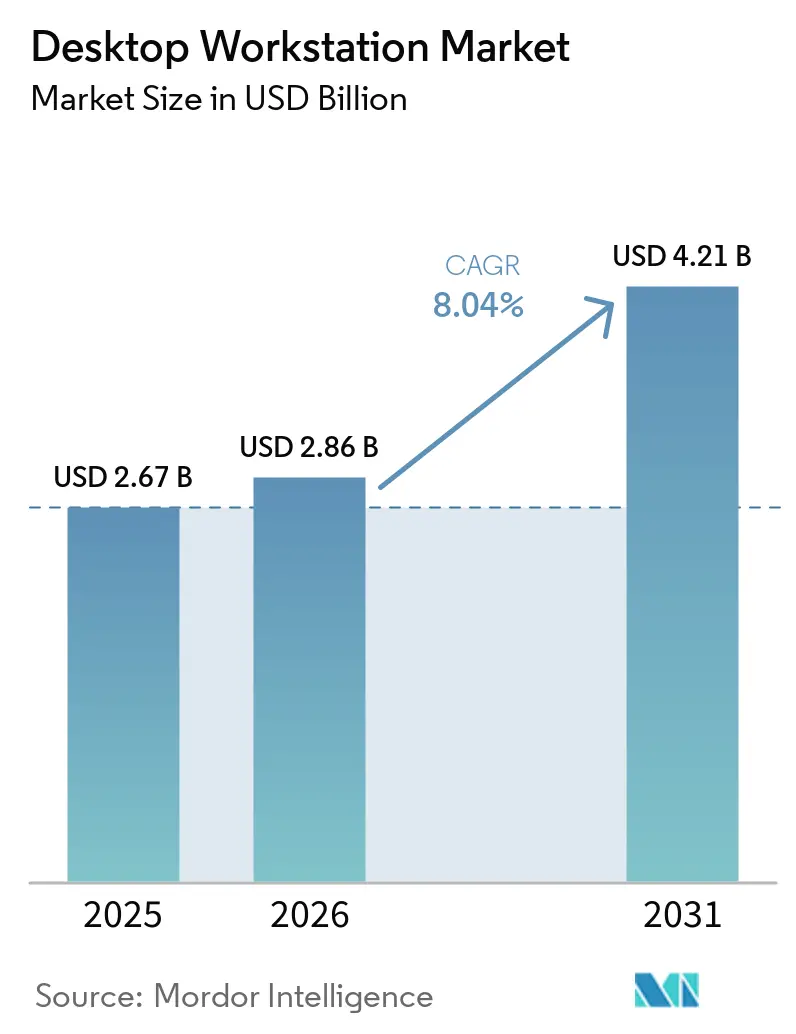

| Market Size (2026) | USD 2.86 Billion |

| Market Size (2031) | USD 4.21 Billion |

| Growth Rate (2026 - 2031) | 8.04% CAGR |

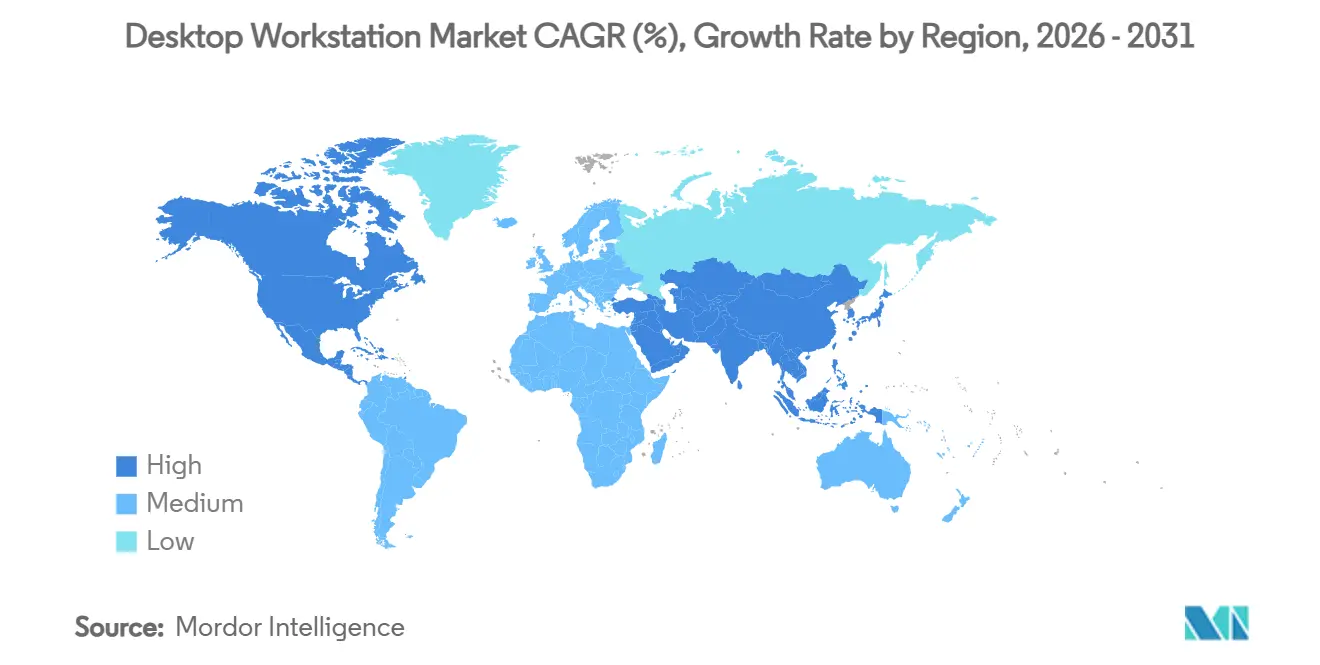

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

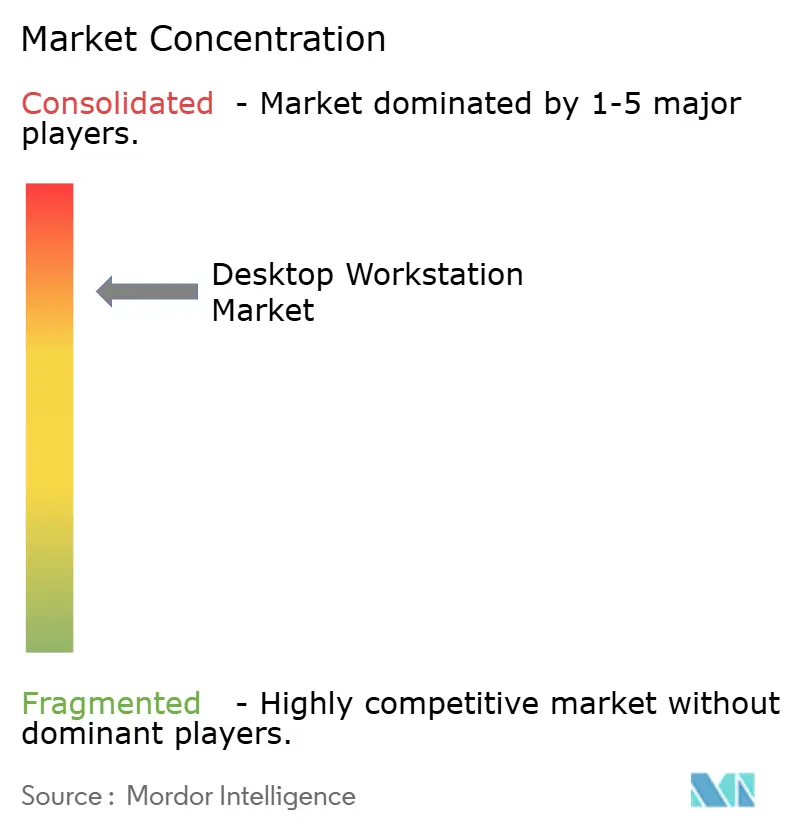

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Desktop Workstation Market Analysis by Mordor Intelligence

The desktop workstation market size expanded from USD 2.67 billion in 2025 to USD 2.86 billion in 2026 and is projected to reach USD 4.21 billion by 2031, advancing at an 8.04% CAGR over 2026-2031. Demand is accelerating as enterprises re-balance hybrid AI strategies, shifting more inference and visualization workloads back to local compute for cost, compliance, and latency advantages. The renewed focus on on-premises processing is unfolding alongside a technology refresh that pairs GPU-dense architectures with high-core-count CPUs, extending the relevance of workstations even as cloud options proliferate. Vendors are differentiating through liquid-cooled designs, modular chassis expanders, and bundled software that simplifies migration between desk-side and data-center environments. Price sensitivity among small and medium enterprises tempers volume growth, yet value-added services such as white-glove deployment and multiyear support contracts continue to attract premium-segment buyers. Together, these cross-currents set the stage for durable mid-single-digit expansion through the forecast horizon.

Key Report Takeaways

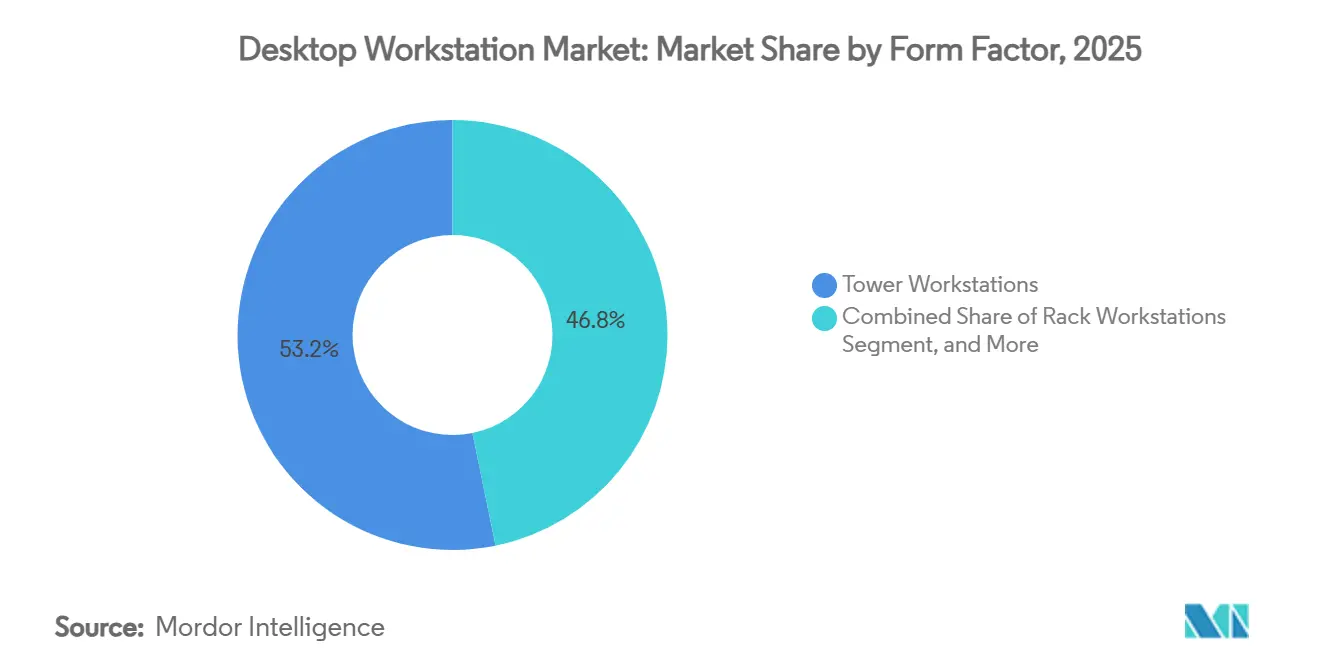

- By form factor, tower workstations accounted for 53.21% of the desktop workstation market share in 2025, and rack systems are projected to lead growth at an 8.84% CAGR through 2031.

- By processor type, x86-based platforms held 74.36% share in 2025, while ARM-based units are forecast to expand at an 8.96% CAGR.

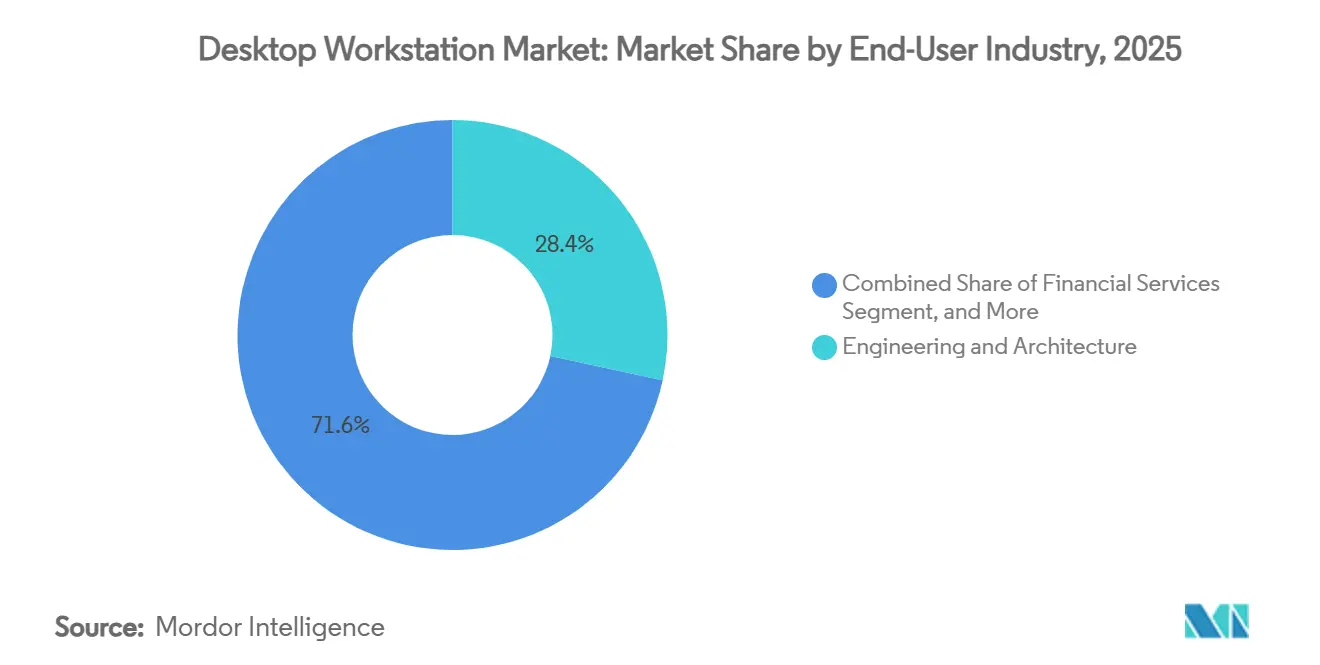

- By end-user industry, engineering and architecture accounted for 28.37% of revenue in 2025, whereas scientific research workloads are the fastest riser, with a 9.44% CAGR.

- By sales channel, direct sales accounted for 62.19% of revenue in 2025 and are tracking an 8.24% CAGR through 2031.

- By geography, North America commanded 39.49% share in 2025, with Asia-Pacific advancing at a 9.04% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Desktop Workstation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of AI and Real-Time Ray Tracing Workloads | +2.1% | Global, with concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Increasing Content Creation Demands in Virtual Production Pipelines | +1.3% | North America and Europe, spillover to Asia-Pacific | Medium term (2-4 years) |

| Shift to Hybrid Work Driving Demand for Remote-Capable Rack Workstations | +1.0% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Growing Use of Engineering Simulation Requiring High-Core Count CPUs | +0.9% | Global, strong in Europe and Asia-Pacific manufacturing hubs | Long term (≥ 4 years) |

| Regulatory Push for Secure, On-Premise Data Processing in Sensitive Industries | +0.8% | Europe (GDPR), North America (financial services, healthcare) | Medium term (2-4 years) |

| Emergence of ARM-Based Workstations Optimized for Energy Efficiency | +0.6% | Asia-Pacific and Europe, early adoption in sovereign-AI initiatives | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of AI and Real-Time Ray Tracing Workloads

Enterprises are refreshing fleets to accommodate local large-language-model tuning and cinematic-quality path tracing. NVIDIA’s RTX PRO 6000 Blackwell GPU, launched in March 2026, adds fourth-generation RT Cores and RTX Mega Geometry units that enable interactive scene builds for virtual production. Dell’s Precision 9 T6 tower supports up to five 300-watt GPUs and 4 terabytes of DDR5 ECC memory, turning desk-side systems into mini-clusters for multi-agent AI workflows. HP test data showed that Z Boost GPU sharing achieved 5.7x faster rendering in CATIA and Siemens NX, proving that tightly networked workstations can substitute for remote render farms. The shift is tilting budgets toward GPU-dense configurations and reinforcing the strategic role of the desktop workstation market in AI development and visualization.

Increasing Content Creation Demands in Virtual Production Pipelines

LED volume stages surpassed 300 worldwide by late 2025, creating a persistent need for systems that can stream 10-bit HDR imagery at 60 frames per second to multi-million-pixel walls. NVIDIA’s Blackwell family integrates fifth-generation Tensor Cores that accelerate AI-based denoising, letting smaller studios achieve cinema-grade output with fewer GPUs.[1]NVIDIA Corporation, “NVIDIA Launches AI-First DGX Personal Computing Systems With Global Computer Makers,” nvidianews.nvidia.com Lenovo’s ThinkStation P5 Gen 2 wraps dual RTX PRO 6000 Blackwell Max-Q cards in a rack-ready enclosure, bridging desk-side iteration and studio infrastructure. As real-time compositing becomes mainstream, creative agencies increasingly specify workstation bundles that integrate latency-optimized storage and 25-gigabit networking, bolstering revenue for high-margin peripherals.

Shift to Hybrid Work Driving Demand for Remote-Capable Rack Workstations

Remote models rely on 1:1 mapping between rack-mounted hardware and off-site users, preserving application responsiveness while easing office-space constraints. HP’s Z4 Rack G6i pairs Intel Xeon W-600 CPUs with NVIDIA Blackwell GPUs in a 2U format that fits standard data-center rows. Dell’s CoreStation, introduced in 2025, applies similar logic, giving engineers dedicated resources without tethering them to a physical desk. Where 100 megabits-per-second links are available, user experience rivals local towers, pushing the desktop workstation market toward centralized deployments that still count as individual unit sales.

Growing Use of Engineering Simulation Requiring High-Core Count CPUs

Finite-element and fluid-dynamics tasks once relegated to clusters now run on CPUs packing upward of 96 cores. AMD’s Threadripper PRO 9000 WX-Series brings 192 threads into a single socket and outperforms Intel’s Xeon W9-3595X by 107% in Autodesk Revit benchmarks.[2]Advanced Micro Devices, “Dell x AMD: Reinventing Workstations, Advancing AI,” amd.com Intellectual-property protection and predictable scheduling motivate automotive and aerospace firms to keep sensitive CAD data in-house, reinforcing workstation budgets in Europe and Asia-Pacific manufacturing corridors. As simulation nests deeper in digital-twin workflows, workstation vendors that secure ISV certifications for Ansys, Siemens, and Dassault suites capture an outsized share of refresh spending.

Restraints Impact Analysis*

| Restraint | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Cloud Workstations Reducing Hardware Refresh Cycles | -1.2% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Supply Chain Volatility for Advanced GPUs and Chipsets | -0.9% | Global, acute in Asia-Pacific manufacturing | Medium term (2-4 years) |

| Rising Average Selling Prices Limiting Adoption in SMEs | -0.7% | Global, most pronounced in South America and Middle East and Africa | Short term (≤ 2 years) |

| Rapid Obsolescence Due to Accelerated CPU and GPU Roadmaps | -0.5% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Cloud Workstations Reducing Hardware Refresh Cycles

Desktop-as-a-Service (DaaS) offerings enable firms to rent GPU time on an hourly basis, providing a cost-effective alternative to purchasing expensive hardware outright. This approach extends the replacement intervals for on-premises systems from the typical 3 years to up to 5 years, allowing businesses to optimize their capital expenditures. The model is particularly well-suited for handling episodic rendering and design peaks, where the demand for high-performance computing resources fluctuates. However, this shift in usage patterns has led to a decline in annual unit shipments, especially in regions with robust fiber connectivity. In such areas, minimal network latency ensures seamless performance, making DaaS a more attractive option. Users increasingly prefer thin clients for accessing cloud platforms such as AWS, Azure, or NVIDIA DGX Cloud instances. This strategy allows organizations to defer significant capital expenditures until their workloads stabilize, offering greater flexibility and scalability in managing their IT infrastructure.

Supply Chain Volatility for Advanced GPUs and Chipsets

Scarcity of HBM3E and slow GDDR7 yield ramps push OEM lead times into multi-month windows. NVIDIA prioritized GB200 and H200 data-center volumes over workstation SKUs during the 2026 Blackwell launch, forcing Dell, HP, and Lenovo to ration top-tier cards. Tenstorrent’s QuietBox 2 sidestepped bottlenecks by using GDDR6, yet traded off bandwidth on memory-heavy AI training. Until memory supply stabilizes, pricing and availability will fluctuate, complicating procurement plans across the desktop workstation market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form Factor: Rack Systems Gain Hybrid-Work Traction

Rack workstations generated a 8.84% CAGR through 2031, while towers retained 53.21% of 2025 revenue, highlighting the coexistence of these two formats rather than one cannibalizing the other in the desktop workstation market. IT teams increasingly prefer rack workstations to centralize multi-kilowatt GPU arrays within controlled cooling environments. This design approach is exemplified by HP’s Z8 Fury G6i, which supports up to four RTX PRO 6000 Blackwell GPUs while maintaining efficient use of office space by avoiding encroachment on floor plans.

Small-form-factor and mobile workstation models cater to space-constrained environments but are generally limited to single-GPU configurations. For instance, Lenovo’s ThinkPad P1 Gen 9 features a 55 TOPS NPU, demonstrating that laptop-class silicon can now handle entry-level AI inference tasks.[3]Lenovo Group, “Lenovo Teams With NVIDIA on Gigawatt AI Factories Program,” news.lenovo.com Additionally, modular side panels, such as HP’s Max Side Panel, enhance the longevity of tower workstations by enabling enterprises to delay transitioning to rack systems while still accommodating larger GPUs. Vendors that effectively balance thermal management and noise levels are well-positioned to capture incremental demand in the desktop workstation market, particularly in industries such as creative studios and financial trading floors, where performance and reliability are critical.

By Processor Type: ARM Challenges x86 Hegemony

x86 platforms controlled 74.36% of 2025 revenue, maintaining their dominance in the desktop workstation market. However, ARM-based configurations are projected to grow at a compound annual growth rate (CAGR) of 8.96%, gradually increasing their market share by 2031. This growth is driven by advancements in ARM architecture, which offer improved energy efficiency and performance scalability, making them increasingly attractive for specific use cases. NVIDIA’s DGX Spark, which combines Grace-Blackwell chips with 128 gigabytes of unified memory, exemplifies this trend by delivering approximately 1 petaflop of AI compute power within a sub-600-watt power envelope, showcasing the potential of ARM-based systems in high-performance computing.

RISC-V, while still in its early stages, is emerging as an influential player in the market. Tenstorrent’s USD 9,999 QuietBox 2, equipped with 480 Tensix cores and liquid cooling, is designed for sovereign-compute buyers who prioritize open instruction sets for greater control and flexibility. Additionally, RISC-V International’s RVA23 profile and ACPI 6.6 support streamline firmware development, simplifying the deployment of desktop operating systems. Although other processor types remain niche, they represent strategic opportunities in the market, particularly for post-Moore accelerators aimed at government laboratories and specialized research institutions. These developments highlight the growing diversification in processor technologies within the desktop workstation market.

By End-User Industry: Scientific Research Outpaces Legacy Verticals

Engineering and architecture accounted for 28.37% of 2025 sales, driven by the widespread adoption of CAD (Computer-Aided Design) and BIM (Building Information Modeling) tools, which remain integral to these industries. However, scientific research is emerging as the fastest-growing segment of the desktop workstation market, with a 9.44% CAGR. This growth is fueled by the increasing shift of computationally intensive tasks, such as protein folding, molecular dynamics, and genomics, from shared computing clusters to desk-side nodes. For instance, Tenstorrent’s QuietBox 2 demonstrated its capabilities by predicting a 686-amino-acid structure in just 49 seconds, a performance that is 55 times faster than traditional CPU-only computations.

The media and entertainment industry continues to invest heavily in real-time color grading and animation workflows, which require high-performance desktop workstations. However, the trend of outsourcing batch rendering tasks to cloud services is exerting downward pressure on workstation prices. Meanwhile, sectors such as healthcare, life sciences, and financial services continue to demand desktop workstations. This stability is attributed to the need to comply with stringent regulations, including HIPAA (Health Insurance Portability and Accountability Act), GDPR (General Data Protection Regulation), and risk modeling standards. These requirements ensure the continued relevance of desktop workstations for handling regulated data workflows, thereby supporting the overall market size.

By Sales Channel: Direct Sales Sustain Premium Positioning

Direct engagement accounted for 62.19% of the 2025 turnover and is projected to grow at an 8.24% CAGR. This growth is driven by offerings such as bespoke BIOS tuning, on-site installation services, and multi-year support tiers, which help offset rising component costs. Major players like Dell, HP, and Lenovo have established specialized teams to manage ISV certification audits, ensuring application stability and reliability for their customers.

Indirect channels, on the other hand, cater to cost-sensitive accounts. System integrators such as BOXX and Puget Systems stand out by offering unique features like liquid cooling and overclocking capabilities. Regional dynamics play a significant role in shaping these sales strategies. In North America, mature procurement practices favor direct relationships with manufacturers, whereas in the Asia-Pacific region, value-added distributors are preferred for their ability to offer localized financing options and language support. These variations in regional preferences contribute to the broader desktop workstation industry's agility and adaptability across different sales motions.

Geography Analysis

North America accounted for 39.49% of 2025 revenue as U.S. enterprises refreshed AI hardware, yet growth is moderating compared with that of emerging regions. Regulatory forces such as HIPAA and state-level privacy statutes continue to anchor workloads locally, safeguarding a baseline of demand even as cloud adoption rises. Additionally, the region benefits from a mature IT infrastructure and a strong presence of key market players, which ensures consistent demand for high-performance desktop workstations. The increasing adoption of AI-driven applications in industries such as healthcare, finance, and manufacturing further supports market stability.

Asia-Pacific is the growth engine, with a 9.04% CAGR projected through 2031. China’s semiconductor self-sufficiency push elevates workstation budgets for electronic design automation, while South Korea’s foundry expansions and Japan’s sovereign-AI initiatives accelerate unit sales. India’s engineering services sector leverages local compute to reduce WAN traffic, increasing desktop workstation market penetration for CAD and simulation tasks. Furthermore, the region's rapid industrialization and growing investments in R&D activities are driving demand for advanced computing solutions. The rise of smart manufacturing and the adoption of Industry 4.0 technologies are also driving growth in the desktop workstation market in this region.

Europe records steady gains amid GDPR enforcement. Germany’s automotive sector uses digital twin simulations, and the United Kingdom’s trading floors favor GPU-rich towers for sub-millisecond analytics. The region's focus on sustainability and energy-efficient technologies is also influencing workstation designs, with vendors introducing products that align with these priorities. South America plus Middle East, and Africa show smaller but rising adoption in construction, media, and energy, constrained by pricing sensitivity and limited vendor financing. However, increasing digital transformation initiatives and government support for technological advancements are gradually improving market conditions in these regions. Vendors that tailor channel incentives and local-language support stand to unlock incremental share, particularly by addressing the unique needs of small and medium-sized enterprises (SMEs) in these markets.

Competitive Landscape

Dell Technologies, HP Inc., and Lenovo Group collectively account for a significant majority of unit shipments, leveraging their procurement scale and strong relationships with Independent Software Vendors (ISVs) to secure certification roadmaps. These companies have consistently maintained their leadership positions by integrating cutting-edge technologies into their product lines. In March 2026, all three introduced new lines featuring NVIDIA Blackwell GPUs and Intel Xeon W-600 CPUs, which combine high performance with forward compatibility to meet evolving market demands. Dell’s Pro Max with GB300 offers seamless workload migration by linking directly to Dell AI Factory, while HP’s Z Boost enhances operational efficiency by pooling GPU capacity across departments, catering to enterprise-level requirements.

Meanwhile, challenger architectures are making significant strides in the market. NVIDIA’s ARM-based DGX Spark, Fujitsu’s MONAKA-linked platforms, and Tenstorrent’s RISC-V QuietBox 2 are gaining traction among buyers who prioritize energy efficiency, open ecosystems, or alternative architectures. These platforms are designed to address specific needs, such as reducing power consumption or enabling greater customization. Boutique builders like BOXX, Puget Systems, and Velocity Micro are also carving out a niche by offering highly specialized solutions, including custom liquid-cooling systems and overclocked GPUs. By focusing on service quality and tailored configurations, these companies are using customer-centric approaches to compete effectively, even against larger players.

Additionally, integrated Neural Processing Units (NPUs) on Intel Core Ultra and AMD Ryzen AI chips deliver up to 55 TOPS (Tera Operations Per Second), enabling mid-range mobile workstations to perform on-device inference tasks more efficiently. This advancement is particularly significant for professionals requiring AI-driven workloads without relying on cloud-based solutions. Furthermore, RISC-V’s newly established firmware standards are lowering entry barriers for developers and manufacturers, fostering innovation and competition.[4]DeepComputing, “DC-ROMA RISC-V AI PC,” deepcomputing.io These developments indicate that the desktop workstation market is likely to feature a more diverse and heterogeneous CPU landscape by the end of the decade, driven by both established leaders and emerging challengers.

Desktop Workstation Industry Leaders

Fujitsu Limited

HP Inc.

Apple Inc.

Dell Technologies Inc.

Lenovo Group Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: HP Inc. introduced the Z8 Fury G6i with up to four RTX PRO 6000 Blackwell Max-Q GPUs and unveiled the Max Side Panel chassis expander.

- March 2026: Dell Technologies launched the Precision 9 T6 tower and the Pro Max with the GB300 desk-side system.

- March 2026: Lenovo revealed the ThinkStation P5 Gen 2 desktop, the ThinkPad P1 Gen 9 mobile workstation, and a 1,000 Wh/L silicon-anode battery proof-of-concept.

- March 2026: Tenstorrent began shipping the liquid-cooled QuietBox 2 RISC-V AI workstation at a USD 9,999 entry price.

Global Desktop Workstation Market Report Scope

The Desktop Workstation Market is the global industry that encompasses the design, development, manufacturing, and distribution of high-performance computing systems specifically engineered to handle compute-intensive, graphics-heavy, and mission-critical professional workloads. These systems are widely used in domains requiring advanced processing power, reliability, scalability, and precision, such as 3D rendering, simulation, data analysis, and complex design workflows.

The Desktop Workstation Market Report is Segmented by Form Factor (Tower, Small Form Factor, Rack, and Mobile or All-in-One), Processor Type (x86-Based, ARM-Based, RISC-V, and Other Processors), End-User Industry (Media and Entertainment, Engineering and Architecture, Healthcare and Life Sciences, Financial Services, Scientific Research, and Other End-User Industries), Sales Channel (Direct, and Indirect or Reseller), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Tower Workstations |

| Small Form Factor Workstations |

| Rack Workstations |

| Mobile or All-in-One Workstations |

| x86-Based Workstations |

| ARM-Based Workstations |

| RISC-V Workstations |

| Other Processor Types |

| Media and Entertainment |

| Engineering and Architecture |

| Healthcare and Life Sciences |

| Financial Services |

| Scientific Research |

| Other End-User Industries |

| Direct Sales |

| Indirect or Reseller Sales |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Form Factor | Tower Workstations | ||

| Small Form Factor Workstations | |||

| Rack Workstations | |||

| Mobile or All-in-One Workstations | |||

| By Processor Type | x86-Based Workstations | ||

| ARM-Based Workstations | |||

| RISC-V Workstations | |||

| Other Processor Types | |||

| By End-User Industry | Media and Entertainment | ||

| Engineering and Architecture | |||

| Healthcare and Life Sciences | |||

| Financial Services | |||

| Scientific Research | |||

| Other End-User Industries | |||

| By Sales Channel | Direct Sales | ||

| Indirect or Reseller Sales | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will desktop workstation market size be by 2031?

It is forecast to reach USD 4.21 billion by 2031, reflecting an 8.04% CAGR over 2026-2031.

Which form factor is expanding fastest?

Rack workstations are projected to advance at an 8.84% CAGR as hybrid-work setups favor remote-capable hardware.

What share did x86 systems hold in 2025?

X86 platforms captured 74.36% of desktop workstation market share in 2025.

Why is Asia-Pacific growing more quickly than North America?

Manufacturing digitization, semiconductor design, and government-backed AI programs drive a 9.04% CAGR in the region, outpacing the mature North American base.

Which end-user group shows the highest growth rate?

Scientific research workloads lead with a 9.44% CAGR thanks to protein-folding, molecular dynamics, and genomics tasks that favor local GPU acceleration.

How are vendors differentiating their products?

Leading companies integrate Blackwell GPUs, liquid cooling, and modular chassis while bundling software that bridges on-premise and cloud AI workflows.

Page last updated on: