Middle East And Africa Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

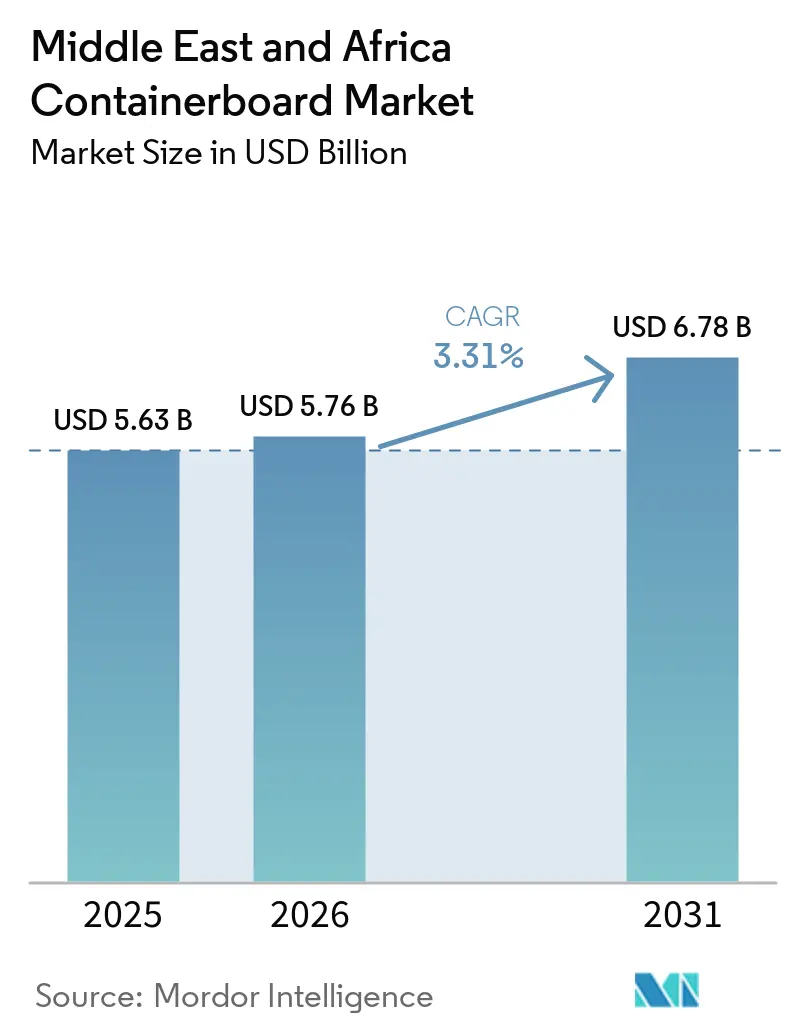

| Base Year Market Size (2025) | USD 5.63 Billion |

| Market Size (2026) | USD 5.76 Billion |

| Market Size (2031) | USD 6.78 Billion |

| Growth Rate (2026 - 2031) | 3.31% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Containerboard Market Analysis by Mordor Intelligence

The Middle East and Africa containerboard market size is projected to expand from USD 5.63 billion in 2025 and USD 5.76 billion in 2026 to USD 6.78 billion by 2031, registering a CAGR of 3.31% between 2026 and 2031. The Middle East and Africa containerboard market is being supported by the steady expansion of e-commerce fulfillment, the resilience of fresh-produce export chains, and a wider policy shift toward fiber-based packaging in place of single-use plastics. Growth conditions remain uneven across the region because GCC countries are adding local recycled board capacity, while several parts of sub-Saharan Africa still depend on imports for stronger linerboard used in export transit packaging. Freight disruptions across the Red Sea and Gulf trade lanes are also changing pricing behavior, meaning the Middle East and Africa containerboard market is responding more to local supply and route risk than to global benchmark moves alone. Competition continues to reflect a two-layer structure in which integrated mill operators compete on fiber access, machine efficiency, and product consistency, while a much larger set of corrugated converters competes on service levels, location, and delivery responsiveness. Even with persistent exposure to OCC prices, freight costs, and energy inflation, the Middle East and Africa containerboard market is benefiting from better domestic OCC collection in the GCC and from policy support tied to Saudi Vision 2030, UAE Vision 2031, and AfCFTA-linked manufacturing and logistics development.

Key Report Takeaways

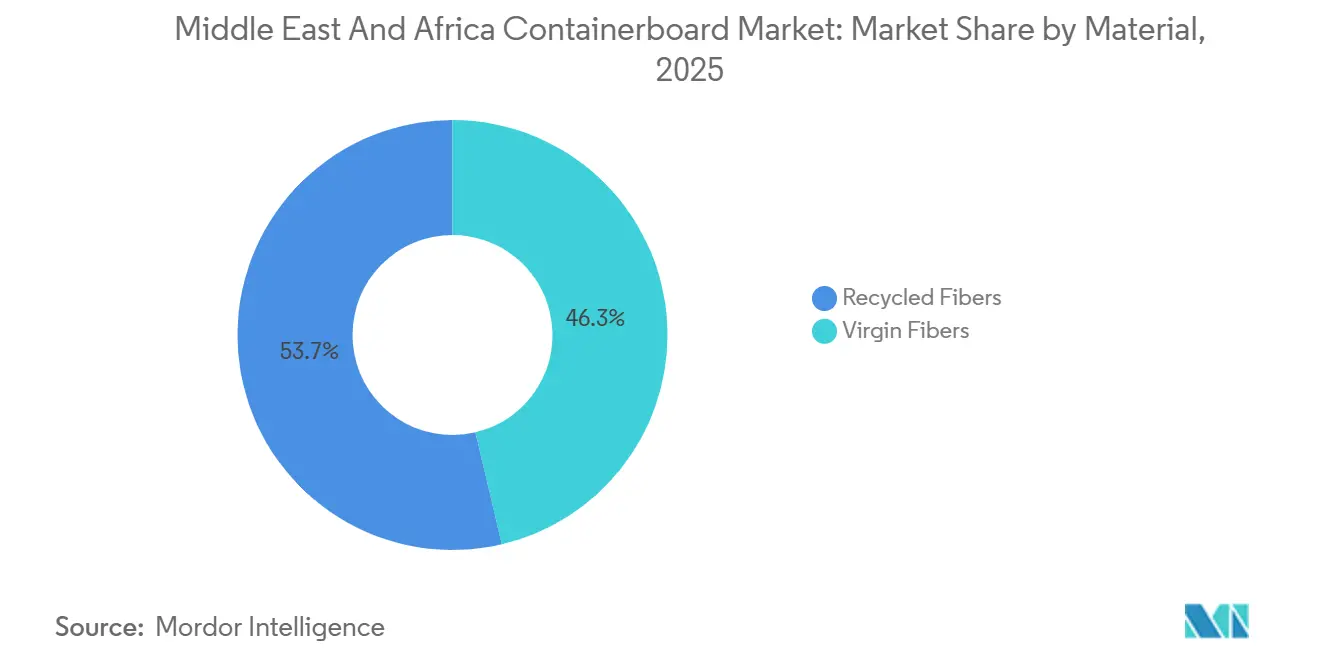

- By material, recycled fibers captured with 53.68% of the Middle East and Africa containerboard market share in 2025.

- By product type, the Middle East and Africa containerboard market size for flutings is projected to grow at a 4.29% CAGR to 2031.

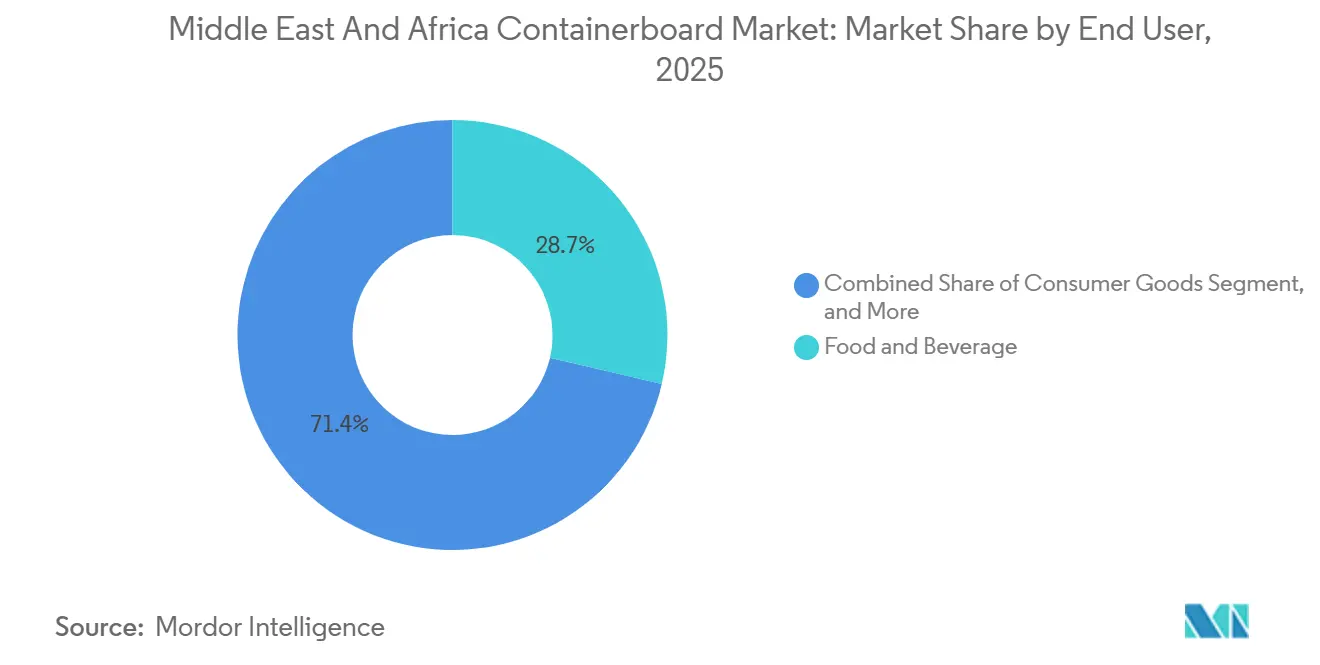

- By material, food and beverage captured with 28.65% of the Middle East and Africa containerboard market share in 2025.

- By geography, the Middle East and Africa containerboard market in South Africa is projected to grow at a 4.38% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East And Africa Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce And Omnichannel Parcel Growth | +0.9% | Global, concentrated in Saudi Arabia, the UAE, South Africa, and Nigeria | Short term (≤ 2 years) |

| Food Delivery and Fresh-Produce Export Intensity | +0.8% | South Africa, Saudi Arabia, Egypt, Turkey | Medium term (2-4 years) |

| Plastic Substitution and Packaging EPR Momentum | +0.6% | Kenya, Nigeria, Ghana, Egypt, UAE, and spill-over to regional supply chains | Medium term (2-4 years) |

| Lightweight Low-Basis-Weight Board Upgrades | +0.4% | GCC core, spill-over to North Africa | Medium term (2-4 years) |

| AfCFTA-Led Need for Stronger Transit Packaging | +0.3% | Continental Africa, early gains in South Africa, Nigeria, Ghana, Morocco | Long term (≥ 4 years) |

| Digital Print Adoption Enabling High-Margin Short Runs | +0.2% | UAE, Saudi Arabia, South Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce and Omnichannel Parcel Growth

Online retail is changing corrugated demand in the GCC faster than broader output indicators would usually suggest, and the Middle East and Africa containerboard market is now seeing a clearer shift toward fulfillment-driven packaging demand. Saudi Arabia's non-oil private sector PMI remained above 53 for most of 2025, indicating sustained activity in commerce and logistics, which typically consume large volumes of corrugated packaging. The more meaningful change is in parcel design, because e-commerce operators in Saudi Arabia and the UAE are requesting right-sized, die-cut corrugated formats that reduce cubic weight for last-mile deliveries. That requirement is lifting demand for lightweight fluting media and stronger testliners simultaneously, which is one reason the Middle East and Africa containerboard market is showing faster momentum in flutings than in more mature grades. Working capital pressure among corrugators has at times slowed the conversion of parcel demand into actual board offtake, so mills that can support customers on service, flexibility, and credit terms are in a better position to hold share.

Food Delivery and Fresh-Produce Export Intensity

Agricultural packaging remains one of the most resilient demand pools in the Middle East and Africa containerboard market, as fresh-produce exports create concentrated, recurring demand for high-performance corrugated trays and boxes. South Africa's citrus and pome fruit export cycle, which peaks from February to July, drives predictable demand for packaging that meets EU phytosanitary and food-contact requirements while also protecting produce during long transit. Sappi reported that packaging and specialty paper sales volumes rose 8% year on year in FY2025, with improved containerboard demand driven mainly by a strong citrus season.[1]Sappi Limited, “Results for the Fourth Quarter and Year Ended September 2025,” Sappi, sharenet.co.za MPact also reported strong volume growth in containerboard and agricultural packaging, and described the agricultural segment as structurally attractive due to export-oriented growth. Because these mills plan around Northern Hemisphere retail and harvest calendars as much as domestic cycles, the Middle East and Africa containerboard market benefits from export-linked food packaging that is not fully tied to local consumer sentiment.

Plastic Substitution and Packaging EPR Momentum

Policy pressure on single-use plastics is creating a durable demand tailwind for fiber-based formats, widening the addressable base for the Middle East and Africa containerboard market. Kenya's Sustainable Waste Management Regulations under Legal Notice No. 176 of 2024 came into force in May 2025, and explicitly include paper and its corrugated products, cardboard, and carton within mandatory lifecycle accountability. In parallel, several governments in the region tightened restrictions on single-use plastic applications in 2025, which made fiber alternatives more relevant in food service, FMCG, and secondary transit packaging. These measures do not need to eliminate plastics overnight to influence purchasing, because even a moderate cost or compliance disadvantage can make corrugated formats easier to justify where substitution is straightforward. As a result, the Middle East and Africa containerboard market is benefiting from regulatory momentum, even though a fully harmonized regional circular economy framework has yet to take shape.

Lightweight Low-Basis-Weight Board Upgrades

Lightweighting is becoming a practical procurement priority for large brand owners and e-commerce platforms, and the Middle East and Africa containerboard market is adjusting to that shift through demand for stronger low-grammage board. Buyers increasingly want recycled containerboard in the 75-150 g/m² range because it reduces shipping weight while preserving stacking and compression performance during distribution. Red Sea Paper's PM2 entered trial production in December 2025, with capacity configured around white-top testliner, gypsum board, and corrugating medium in that exact weight range, demonstrating how quickly local supply is being aligned with this specification trend. At the same time, better structural box design is allowing corrugated plants to lower grammage without losing edge crush strength, so board demand is becoming more quality-sensitive than volume-only. This keeps pressure on mills to improve refining, fiber management, and consistency, and it favors producers that can deliver lighter grades with reliable performance across the Middle East and Africa containerboard market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imported OCC, Pulp, And Kraft Liner Price Volatility | -0.9% | Global, concentrated in GCC, Turkey, Egypt | Short term (≤ 2 years) |

| Red Sea and Gulf Shipping-Disruption Cost Shocks | -0.6% | GCC core, North Africa, East Africa | Short term (≤ 2 years) |

| Water Scarcity and Mill-Effluent Constraints | -0.4% | GCC, Egypt, South Africa | Medium term (2-4 years) |

| Water-Use Restrictions Affecting Pulp Mills | -0.2% | South Africa, Morocco, Egypt | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Imported OCC, Pulp, And Kraft Liner Price Volatility

Raw material risk remains the clearest constraint on the Middle East and Africa containerboard market because the region has almost no domestic virgin wood fiber pulp base and still depends heavily on imported OCC bales and kraft liner. This exposure became more visible in 2025 when higher recovered paper costs hit margins even as shipment volumes improved for major regional players. MPact said recovered paper prices rose significantly in the first half of 2025, and that cost pressure contributed to a 14.5% decline in EBITDA even though containerboard sales volumes increased 20.3% in the same period. The feedback loop is important because new recycled machine capacity improves local availability of board, but it can also intensify competition for the same OCC pool and raise input prices again. That means the Middle East and Africa containerboard market can gain from domestic scale while still struggling to convert that scale into stable margin expansion.

Red Sea and Gulf Shipping-Disruption Cost Shocks

Geopolitical disruption in key maritime corridors has moved from a temporary concern to a structural cost issue for the Middle East and Africa containerboard market. The World Bank reported that traffic through the Suez Canal and Bab el-Mandeb was down by 75% by the end of 2024, while rerouting around the Cape of Good Hope increased cargo travel distances by 48% and journey times by up to 45%. Those disruptions raise freight, insurance, and working capital needs for mills importing fiber or exporting converted packaging, and they also make delivery performance harder to manage for regional corrugators. In April 2026, GCC containerboard price indices moved higher after the partial closure of the Strait of Hormuz, which showed how quickly route risk can feed through to regional board prices. The result is a Middle East and Africa containerboard market where pricing is increasingly shaped by sub-regional logistics exposure, with the UAE and Gulf import routes carrying a different risk profile from Jeddah-linked and more locally anchored supply chains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fibers Lead, While Virgin Grades Gain On Quality Needs

Recycled fibers held 53.7% of the Middle East and Africa containerboard market share in 2025, which reflects the region's practical dependence on OCC-based testliner and fluting in a fiber-deficient environment. The dominance of recycled grades is reinforced by the production profile in Saudi Arabia, the UAE, and Kuwait, where domestic containerboard capacity is centered on recycled fiber rather than virgin pulp. Cost discipline and sustainability requirements are both supporting this pattern, so buyers often see recycled board as the most workable balance between availability and economics. That is why the Middle East and Africa containerboard market continues to rely on recovered fiber even when imported OCC costs become more volatile.

Virgin fibers are projected to grow at a 4.4% CAGR through 2031, and that faster pace reflects a quality premium rather than a broad shift away from recycled grades. Mondi's Duino mill in Italy added 420,000 tonnes per year of recycled containerboard capacity designed to serve European customers and international routes, including flows connected to the Middle East and Africa containerboard market, which underlines the continued competitive pressure from well-capitalized exporters.[2]Mondi Group, “Integrated Report and Financial Statements 2025,” Mondi Group, mondigroup.com Food-contact applications, stronger burst-strength needs, and pharma-adjacent packaging still favor virgin-based linerboard, where recycled input cannot deliver consistent performance at scale. Multinational customers are also placing greater weight on chain-of-custody and certification standards, and that creates a specification gap for some regional recycled-fiber suppliers.

By Product Type: Testliners Anchor Demand, While Flutings Benefit from Lightweighting

Testliners accounted for 34.6% of the Middle East and Africa containerboard market in 2025, confirming their position as the most widely produced and consumed grade across the region. Their lead comes from the recycled-fiber mill base in the GCC and from the mature corrugated box footprint in Saudi Arabia and the UAE, where standard transport packaging still depends heavily on testliner-facing combinations. These grades remain central to FMCG distribution because they serve a broad mix of regular slotted containers and secondary transport packs. For that reason, the Middle East and Africa containerboard market still uses testliners as its core-volume grade, even as newer specialty needs are emerging around them.

Flutings are forecast to grow at a 4.3% CAGR through 2031, and this faster expansion is being driven by demand for lighter and more moisture-resistant corrugating medium. The need is especially evident in coastal and export-linked markets, where boxes move through humid conditions and along ambient distribution chains. Lighter fluting also aligns with the broader push toward right-sized packaging in e-commerce and food delivery, as it helps reduce shipping weight without compromising structural integrity. Red Sea Paper's PM2 is aligned with this opportunity through output in the 75 to 150 g/m² range, which gives the Middle East and Africa containerboard market a more direct local answer to a specification that often relied on imports in the past.

By End User: Food And Beverage Sets the Pace Across Scale and Growth

Food and beverage accounted for 28.7% of the Middle East and Africa containerboard market in 2025 and is expected to expand at a 3.9% CAGR through 2031, making it both the largest and the fastest-growing end-user category. The segment draws demand from supermarkets, convenience packaging, export produce shipments, dates and fruit boxes, and the growing food-delivery channel in the GCC. It also benefits from the way regional food logistics is becoming more organized, with better cold chain handling and wider use of structured secondary packaging. This provides the Middle East and Africa containerboard market with a dependable volume base tied to both daily consumption and export activity.

Mpact said agricultural packaging delivered good volume growth and described that export-oriented segment as structurally attractive, which supports the strength of the food and beverage channel. Sappi also linked improved containerboard demand in FY2025 to a robust citrus season, showing how closely seasonal produce flows influence demand for boxes and trays. Consumer goods remain the next-largest user base, supported by packaging for electronics, personal care, and household goods in formal retail and free-trade zone operations. Industrial users provide steadier base-load demand, while pharmaceutical and retail-ready formats are giving the Middle East and Africa containerboard market a smaller but increasingly strategic opportunity in clean and tamper-evident secondary packaging.

Geography Analysis

Saudi Arabia accounted for 35.7% of the Middle East and Africa containerboard market share in 2025, which made it the largest single national market in the region. Demand in Saudi Arabia is tied to non-oil private-sector activity, fulfillment center expansion, food processing growth, and ongoing efforts to localize more packaging supply under Vision 2030. The UAE remains smaller in domestic consumption, but it plays an outsized role as a re-export and logistics platform because Jebel Ali and related trade routes pull corrugated packaging into regional redistribution networks. Turkey also adds a distinct export-oriented supply base to the Middle East and Africa containerboard market, while the rest of the Gulf continues to show rising consumption with significant import dependence.

South Africa is forecast to grow at a 4.4% CAGR through 2031, which gives it the fastest trajectory among the geographic segments in the Middle East and Africa containerboard market. That performance reflects the country's fruit-export strength, mill upgrade activity, and partial insulation from Asian import pressure through currency dynamics and local value-chain depth. Mpact's ZAR 1.3 billion (USD 70 million) Mkhondo Mill upgrade was substantially completed by the end of 2025 and added a new pulp mill module and sodium lignosulphonate plant to improve higher-value output and export capability.[3]Mpact Group Limited, “Annual Results FY2025: Mpact Delivers Revenue Growth and Higher NAV, EBITDA Resilient in Challenging Conditions,” Mpact, mpact.co.za Sappi said South African containerboard demand remained healthy in Q1 FY2026 and continued to be supported by agricultural activity, which confirms how strongly the country's box demand follows export crop cycles.

Egypt remains one of the larger African demand centers because it has a relatively mature corrugated converting base around the Nile Delta and Greater Cairo industrial areas. Its cost position is still sensitive to imported linerboard and freight cycles, so logistics shocks can move quickly through local converting margins. Nigeria is expanding with urbanization and formal FMCG distribution, but limited domestic containerboard production means many corrugators still depend on imported linerboard and medium. Morocco is also becoming more relevant as a regional supply point into parts of Africa, and AfCFTA can support stronger intra-African trade in boxes and paper-based transit packaging as logistics networks improve. Across the broader region, the Middle East and Africa containerboard market is becoming more locally differentiated because route disruption in the Red Sea and Gulf has increased the value of nearby supply, shorter lead times, and more secure sourcing structures.

Competitive Landscape

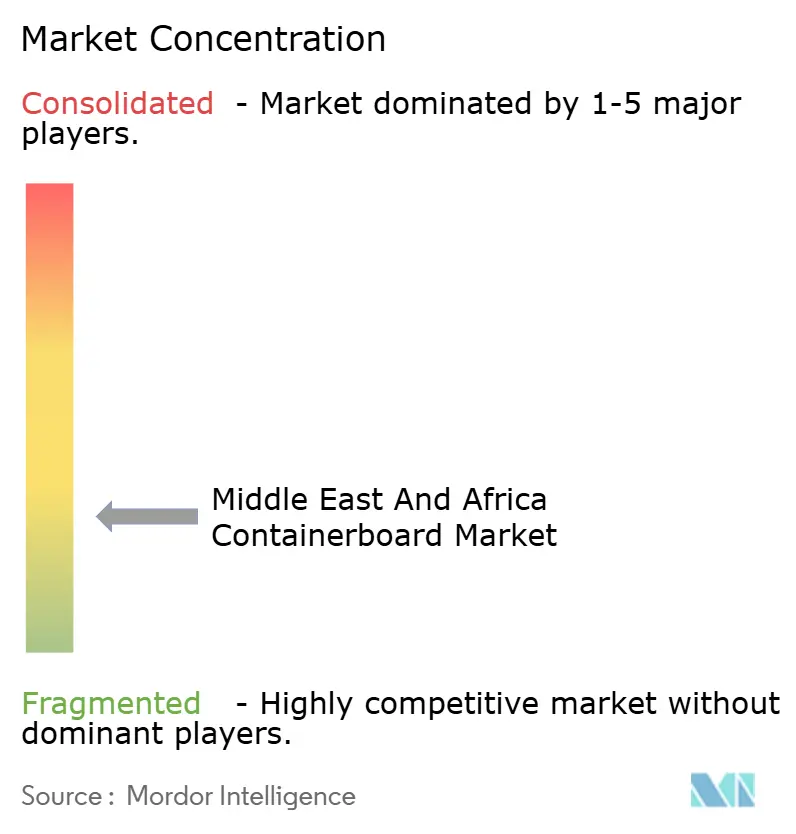

The Middle East and Africa containerboard market remains fragmented at the converter level, but it is more concentrated among integrated paper mill operators that control fiber access, production quality, and machine efficiency. A small group of mill-based participants competes on consistency and input security, while a much larger set of corrugated box converters competes on speed, local service, and customer proximity. In the African sub-region, Mondi and Mpact stand out for their vertical integration and operational depth, giving them advantages that import-dependent players cannot easily replicate. This structure means the Middle East and Africa containerboard market rewards scale and reliability at the mill level, but still leaves room for many smaller converting businesses in local delivery niches.

Sappi reduced FY2026 capital expenditure to USD 260 million to preserve cash, while pointing to healthy South African containerboard demand linked to agriculture, signaling a selective and disciplined approach to capital deployment.[4]Sappi Limited, “FY26 Q1 Results - the Period Ended December 2025,” Sappi Limited, sappi-ir-reports.co.za Mondi opened its recycled containerboard mill at Duino in 2025 and reported that 100% of its operations were ISO 14001 certified, which strengthened its credibility with multinational packaging buyers seeking quality and environmental compliance. These steps show that the Middle East and Africa containerboard market is being shaped by investment in cost control, grade capability, certification, and export reach rather than price competition alone.

A wider technology gap is also emerging between larger producers and smaller regional firms. Bigger operators are better placed to use predictive maintenance, inline inspection, automated order handling, and tighter OCC management, which helps them deliver more stable quality and shorter commercial cycles. At the same time, the clearest white space in the Middle East and Africa containerboard market remains in specialty grades such as moisture-resistant semi-chemical fluting, white-top testliner, and barrier-coated linerboard that can replace plastic-laminated formats. That keeps the market open to new partnerships and selective joint ventures, especially where local-content policies in Saudi Arabia and the UAE align with international technology holders and domestic investors.

Middle East And Africa Containerboard Industry Leaders

Napco National CJSC

United Carton Industries Company

Mondi plc

Sappi Limited

Middle East Paper Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Mpact Group Limited reported full-year FY2025 results with ZAR 14.0 billion (USD 757 million) in revenue, resilient underlying EBITDA of ZAR 1.5 billion (USD 81 million), and substantially completed the ZAR 1.3 billion (USD 70 million) Mkhondo Mill upgrade.

- February 2026: Sappi Limited reported a loss of USD 37 million for Q1 FY2026 with adjusted EBITDA of USD 90 million, driven by lower dissolving wood pulp prices, rand appreciation, and oversupply in global paperboard markets.

- January 2026: Red Sea Paper formally commenced trial production on its PM2 in December 2025, adding approximately 178,000 tons per year of white-top test liner, gypsum board, and corrugating medium (75 to 150 g/m²) to the Saudi Arabian market.

- December 2025: Mondi plc opened its EUR 200 million (USD 236 million) recycled containerboard mill at Duino, Italy, producing 420,000 tons per year of waste-based fluting (from 80 g/m²) and testliner (from 90 g/m²).

Middle East And Africa Containerboard Market Report Scope

The scope of this report covers the analysis of the containerboard market in the Middle East and Africa. Containerboard is the paperboard used primarily for the manufacture of corrugated boxes and packaging solutions. This study examines market trends, growth drivers, challenges, and opportunities within the region, providing insights into the supply chain, demand patterns, and competitive landscape. The report also includes a detailed assessment of market dynamics and forecasts for the study period.

The Middle East and Africa Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Type (Kraftliners, Testliners, and Flutings), End User (Food and Beverage, Consumer Goods, Industrial, and Other End Users), and Geography (Saudi Arabia, United Arab Emirates, Turkey, Rest of Middle East, South Africa, Egypt, Nigeria, and Rest of Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End Users |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Material | Virgin Fibers | |

| Recycled Fibers | ||

| By Product Type | Kraftliners | |

| Testliners | ||

| Flutings | ||

| By End User | Food and Beverage | |

| Consumer Goods | ||

| Industrial | ||

| Other End Users | ||

| By Geography | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the 2026 value of the Middle East and Africa containerboard market?

The Middle East and Africa containerboard market stood at USD 5.76 billion in 2026 and is forecast to reach USD 6.78 billion by 2031 at a 3.3% CAGR.

Which material category leads to demand across the region?

Recycled fibers led the region in 2025 with 53.7% share, reflecting the strong role of OCC-based production in GCC containerboard mills.

Which product type is growing the fastest in containerboard across Middle East and Africa?

Flutings are forecast to grow fastest, at a 4.3% CAGR through 2031, supported by lightweighting, humidity-resistance requirements, and e-commerce box optimization.

Why are food and beverages so important for demand in this region?

Food and beverage held a 28.65% share in 2025 and is set to grow at a 3.93% CAGR, as it serves supermarkets, food delivery, and export produce chains simultaneously.

Which country is the largest demand center in Middle East and Africa?

Saudi Arabia was the largest country market in 2025 with 35.69% share, supported by packaging localization, e-commerce growth, and food-processing expansion.

Which geography is expected to grow the fastest through 2031?

South Africa is expected to grow the fastest at 4.38% CAGR, helped by fruit-export packaging demand and mill upgrades led by major domestic producers.

Page last updated on: