Asia-Pacific Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 70.86 Billion |

| Market Size (2026) | USD 73.30 Billion |

| Market Size (2031) | USD 92.05 Billion |

| Growth Rate (2026 - 2031) | 4.66% CAGR |

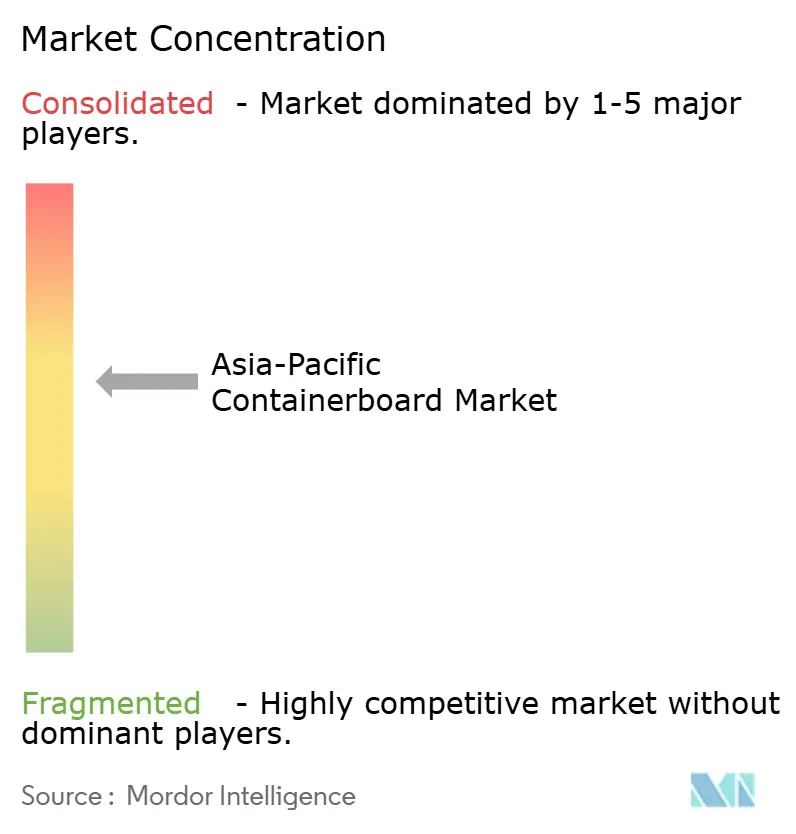

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Containerboard Market Analysis by Mordor Intelligence

The Asia-Pacific containerboard market size is expected to grow from USD 70.86 billion in 2025 to USD 73.3 billion in 2026 and is forecast to reach USD 92.05 billion by 2031 at 4.66% CAGR over 2026-2031. The Asia-Pacific containerboard market is supported by greater use of corrugated packaging in e-commerce, food distribution, and industrial supply chains, which has made demand more durable across the region. Plastic substitution policies, cold-chain expansion, and the move toward certified paper-based packaging are also widening the addressable use base for producers and converters. At the same time, large Chinese integrated mills continue to shape pricing, investment, and capacity discipline across the Asia-Pacific containerboard market, as their scale enables them to remain active even when selling prices soften. This keeps near-term pricing recovery in check, but it also pushes the Asia-Pacific containerboard market toward lighter, stronger, and more specialized grades that offer better value per tonne.

Key Report Takeaways

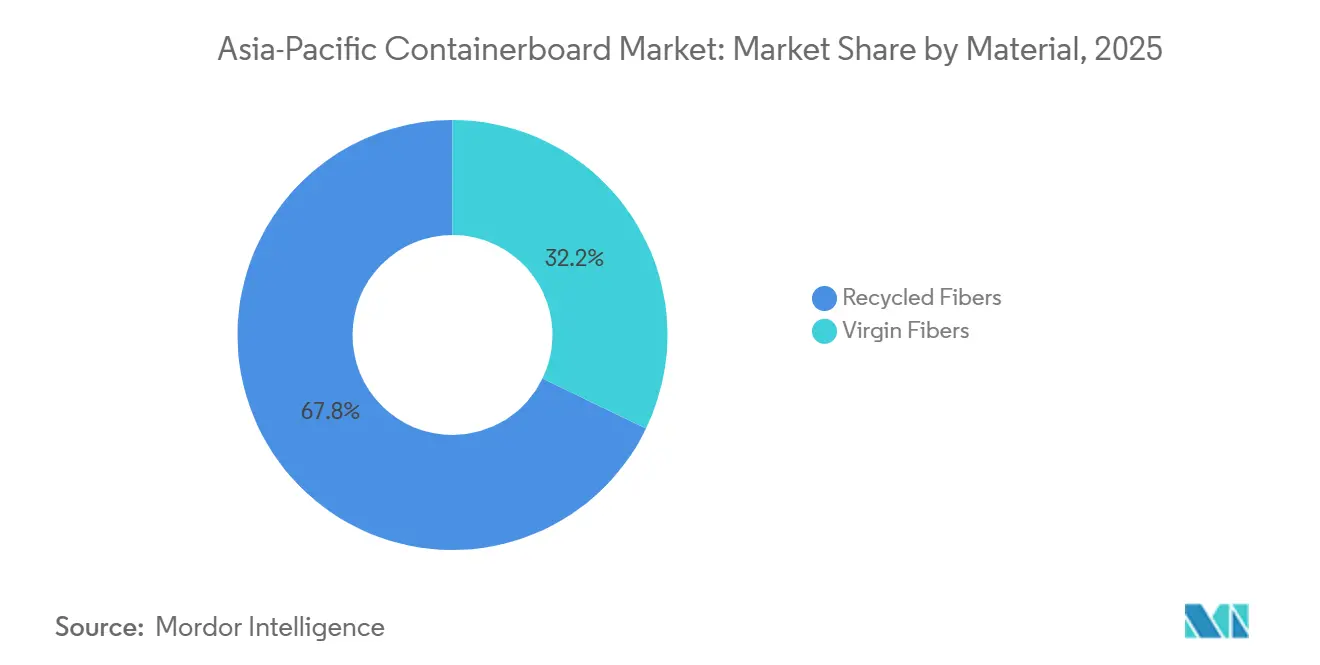

- By material, recycled fibers captured with 67.83% of the Asia-Pacific containerboard market share in 2025.

- By product type, the Asia-Pacific containerboard market size for flutings is projected to grow at a 5.69% CAGR to 2031.

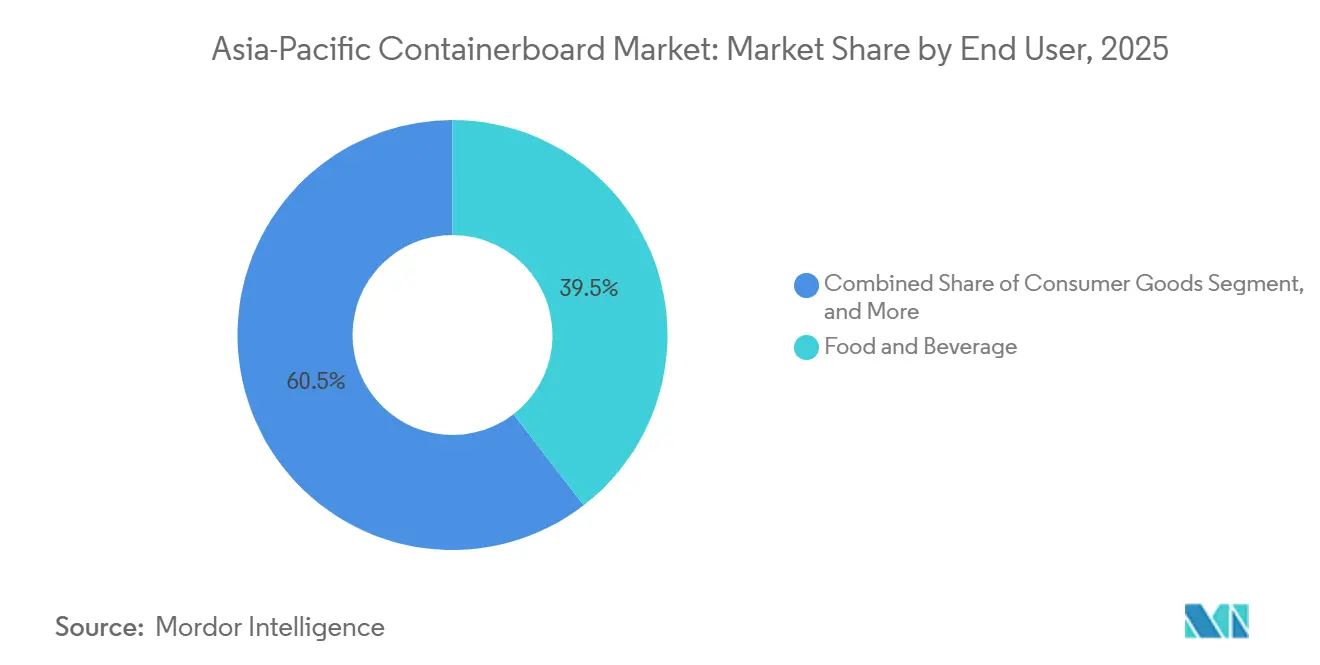

- By end user, the food and beverage industry accounted for 39.54% of the Asia-Pacific containerboard market share in 2025.

- By geography, the Asia-Pacific containerboard market in India is projected to grow at a 6.46% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing E-Commerce Packaging Demand | +1.8% | Global, concentrated in China, India, and Southeast Asia | Short term (≤ 2 years) |

| Government Bans on Single-Use Plastics | +0.9% | China, India, Indonesia, Australia, and Southeast Asia | Medium term (2-4 years) |

| Expansion of Cold-Chain Logistics Infrastructure | +0.7% | China, India, and Southeast Asia | Medium term (2-4 years) |

| Rising Consumer Preference for Sustainable Packaging | +0.5% | APAC-wide, concentrated in Japan, South Korea, and Australia | Long term (≥ 4 years) |

| Integration of Smart Packaging Sensors in Corrugated Boxes | +0.3% | China, India, South Korea, and Japan | Long term (≥ 4 years) |

| Capacity Expansion by Regional Mill Owners | +0.2% | China, Indonesia, and India | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing E-Commerce Packaging Demand

Growing e-commerce activity remains the strongest immediate driver of the Asia-Pacific containerboard market, as corrugated formats already handle an estimated 80% of e-commerce parcels in major regional economies. The demand pattern is also changing in quality terms because algorithm-led packaging fitment systems can reduce corrugated board use per shipment by up to 30%, yet they increase the need for lighter and more consistent performance grades. This is pushing the Asia-Pacific containerboard market toward fluting and liner grades that can perform reliably in automated fulfillment, high-speed sortation, and dense parcel networks. It also favors converters that can turn short runs quickly near logistics clusters, where service speed now matters as much as board cost. Because parcel shipping remains a recurring logistics need rather than a one-time retail trend, the Asia-Pacific containerboard market keeps a firmer demand base than many other paper grades.

Government Bans on Single-Use Plastics

Plastic phase-out policies are steadily expanding the addressable demand base for the Asia-Pacific containerboard market into food service, fresh produce, pharmaceutical distribution, and seafood transport. In Australia, South Australia moved ahead with bans on additional single-use plastic items in September 2025, which strengthened the shift toward paper-based alternatives in food-related applications. Across the region, compliance rules are making traceability, recycled content, and food-safety certification more important in procurement decisions, which supports higher-value supply in the Asia-Pacific containerboard market. That changes competition because mills without certification infrastructure struggle to access regulated categories even if they remain cost-competitive in commodity grades. It also gives the Asia-Pacific containerboard market a source of demand that is less tied to trade swings or consumer spending cycles than traditional box demand.

Expansion of Cold-Chain Logistics Infrastructure

Cold-chain packaging is becoming increasingly important in the Asia-Pacific containerboard market because it offers better pricing and lower demand elasticity than standard brown box applications. Healthcare and food distributors in Japan and South Korea are increasing the use of coated paperboard in controlled-temperature logistics, partly because rigid paper-based formats support RFID integration and tamper-evident sealing more effectively than flexible films. SCG Packaging also deployed AI, machine learning, and a Logistics Management Control Center across its cold-chain packaging operations in 2025, demonstrating how service quality is becoming part of product value in the Asia-Pacific containerboard market.[1]SCG Packaging Public Company Limited, “Annual Report 2025 (Form 56-1 One Report),” SCG Packaging, scgp.listedcompany.com Japan’s food contact material positive list, which became effective in June 2025, further supported the use of compliant paper-based formats in chilled food chains. In India, the cold-chain buildout for pharmaceuticals and processed foods is driving the adoption of corrugated insulated formats and recyclable alternatives to expanded polystyrene in tertiary packaging.

Rising Consumer Preference for Sustainable Packaging

Sustainability requirements are moving from brand messaging into purchasing specifications, which is raising the quality threshold in the Asia-Pacific containerboard market. This shift is most visible in consumer goods and food packaging, where multinational buyers increasingly prefer recyclable, certified, and traceable paper-based formats across their regional supply chains. Packaging reported that sustainable product lines accounted for 59% of FY2025 sales revenue, indicating that customers are already paying for certified, differentiated packaging at scale. The same report highlighted FSC-certified and BRCGS PM-compliant offerings, which suggests that certification is becoming a practical route to supplier preference rather than a niche feature. In the Asia-Pacific containerboard market, this supports greater resilience for mills that can combine scale with sustainability credentials, while leaving purely commodity suppliers more exposed to spot-price competition.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Old Corrugated Container Prices | -1.2% | Global, acute in China, Southeast Asia, and India | Short term (≤ 2 years) |

| Supply Overhang from New Mega-Mills in China | -0.8% | China-led, spillover to Southeast Asia and South Korea | Medium term (2-4 years) |

| Intensifying Competition from Flexible Packaging Formats | -0.4% | Southeast Asia, including Indonesia, Thailand, Vietnam, and India | Long term (≥ 4 years) |

| Stringent Effluent Regulations Increasing Compliance Costs | -0.3% | China, India, and Indonesia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Old Corrugated Container Prices

Old corrugated container price swings remain a direct margin risk for the Asia-Pacific containerboard market because recycled grades dominate regional supply and many mills still depend on purchased fiber. When recovered fiber costs move faster than finished board prices, smaller producers lose pricing flexibility, and working capital tightens quickly. Larger integrated groups are better protected because they can offset external price swings through collection systems, pulp integration, or a broader operating base. Nine Dragons Paper’s FY2025 results showed that raw-material cost efficiency supported profits even as average selling prices declined, highlighting the advantage of scale during volatile input cycles. This keeps the Asia-Pacific containerboard market structurally uneven, with integrated leaders more able to defend margins than import-dependent commodity mills.

Supply Overhang from New Mega-Mills in China

Supply additions in China continue to restrain the Asia-Pacific containerboard market, as new capacity enters a region where pricing has not fully recovered. Even when demand improves, excess output from large Chinese mills can delay price normalization across neighboring markets through trade flows and benchmark pressure. The effect is strongest in the Asia-Pacific containerboard market because Chinese producers combine scale, integration, and broad customer coverage, which lets them stay active during weaker pricing periods. Oji Holdings’ strategic shift away from some oversupplied commodity exposure and toward higher-growth packaging investments in India and Southeast Asia also reflects how uneven regional demand-supply conditions remain. A firmer recovery will depend on tighter capacity discipline, stronger end demand, and continued enforcement of efficiency standards that raise the cost of operating outdated mills.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fiber Scale Meets Quality Upgrading

Recycled fibers led with 67.83% of the Asia-Pacific containerboard market share in 2025, which reflects the region’s dependence on secondary fiber for standard corrugated production. This position gives the Asia-Pacific containerboard market a cost advantage in large-volume box demand, especially in e-commerce and consumer staples, where price discipline remains important. Recycled grades also align with the region’s growing circular packaging systems, as rising parcel volumes and retail distribution create a steady stream of recoverable board. At the same time, the Asia-Pacific containerboard industry still faces uneven fiber quality, exposure to imported pulp in several markets, and operating disruptions when recovered paper specifications are inconsistent.

Virgin fibers are forecast to grow at a 5.37% CAGR from 2026 to 2031, the fastest pace among material categories in the Asia-Pacific containerboard market. That growth reflects a quality upgrade rather than a broad replacement of recycled economics, with food-contact, pharmaceutical, and premium shipping formats demanding higher purity, printability, and consistency in strength. Nine Dragons Paper started production at new bleached folding boxboard lines at Jingzhou and Beihai in 2025, adding 1.2 million tonnes per annum of higher-value virgin-grade capacity as it diversified beyond its recycled corrugating base. The result is a two-track Asia-Pacific containerboard market where recycled fiber keeps volume leadership, while virgin grades capture the faster growth in premium and compliance-heavy uses.

By Product Type: Kraftliners Hold the Base While Flutings Gain Speed

Flutings are projected to grow at a 5.69% CAGR from 2026 to 2031, making them the fastest-growing type in the Asia-Pacific containerboard market. This reflects the need for stronger corrugating medium in automated fulfillment, faster delivery models, and export packaging for electronics and other fragile goods. As automation standards tighten, buyers are placing greater value on compression strength, run consistency, and compatibility with robotic handling systems, favoring higher-performance fluting grades in the Asia-Pacific containerboard market. This also gives fluting suppliers a stronger route to differentiation than what is usually available in commodity board categories.

Kraftliners accounted for 43.79% of the Asia-Pacific containerboard market in 2025, supported by their role as the outer-facing layer in corrugated board across nearly every end-use category. Oji Holdings raised domestic containerboard and corrugated container prices in Japan by 10% or more, effective October 2025, indicating that higher-grade liner products still had room for selective price recovery in mature markets.[2]Oji Holdings Corporation, “1st-Half of FY2025 Summary of Financial Business Results,” Oji Holdings, ojiholdings.co.jp Testliners continue to serve much of the high-volume e-commerce and FMCG box demand because they balance acceptable strength with lower cost, especially where procurement remains volume led. White-top and higher-graphics liner variants are also gaining space as branding moves onto shipping cartons, which adds another value layer to the Asia-Pacific containerboard market.

By End User: Food Packaging Leads, Industrial Demand Lifts the Ceiling

The industrial segment is forecast to expand at a 6.15% CAGR from 2026 to 2031, which makes it the fastest-growing end-user category in the Asia-Pacific containerboard market. This pattern is important because it shows that growth is no longer tied only to consumer shipments, with electronics and component manufacturing in India and Southeast Asia creating additional demand for engineered corrugated transport packaging. Industrial buyers usually require stronger specifications, better consistency, and more reliable logistics performance, which raises the value profile of demand for the Asia-Pacific containerboard market. As nearshoring expands, these export-oriented applications should continue to support structurally stronger demand beyond seasonal retail cycles.

Food and beverage accounted for 39.54% of the Asia-Pacific containerboard market in 2025, making it the largest end-user segment by a clear margin. Organized retail growth, processed food consumption, and cold-chain expansion are keeping corrugated packaging central to food movement across the Asia-Pacific containerboard market. In Japan and South Korea, the shift toward compliant paper-based tray and tray-seal formats is also supporting coated and food-safe grades with stronger pricing potential. Consumer goods and the broader group of other end users still add meaningful demand across personal care, pharmaceuticals, textiles, and household products, which keeps the Asia-Pacific containerboard market diversified across both retail and industrial channels.

Geography Analysis

China held 52.17% of the Asia-Pacific containerboard market share in 2025, which made it the dominant country segment by a wide margin. Its lead comes from manufacturing scale, domestic consumption, and its central role in regional corrugated box production and trade. The Asia-Pacific containerboard market remains heavily influenced by China because pricing, capacity additions, and procurement standards in that country often shape conditions for nearby markets as well. Nine Dragons Paper reported FY2025 revenue of RMB 63,240.5 million (USD 8.71 billion) and net profit of RMB 2,201.7 million (USD 303 million), indicating that leading Chinese mills preserved earnings through raw material efficiency and integration. That ability to stay profitable at softer prices keeps China at the center of the Asia-Pacific containerboard market’s competitive balance.

India is forecast to grow at a 6.46% CAGR from 2026 to 2031, making it the fastest-growing major country market in the Asia-Pacific containerboard market. FMCG expansion, rising e-commerce activity, and domestic packaging investment are driving that momentum and attracting strategic attention from regional suppliers. Oji Holdings committed JPY 270 billion (USD 1.8 billion) in growth investment under its Medium-Term Management Plan 2027, with India and Southeast Asia identified as priority regions for packaging expansion. Japan and South Korea are more mature parts of the Asia-Pacific containerboard market, but they still support higher-spec demand tied to food safety, electronics packaging, and disciplined price management.

Indonesia and the wider Southeast Asian group add a different layer to the Asia-Pacific containerboard market because they combine fast-rising domestic box demand with growing regional manufacturing relevance. SCG Packaging reported that 65% of its recovered paper was sourced domestically and 35% internationally in FY2025, which shows how regional players are building more structured fiber systems around local demand centers.[3]Nine Dragons Paper (Holdings) Limited, “Announcement of Annual Results for the Year Ended 30 June 2025,” Nine Dragons Paper, doc.irasia.com These markets benefit from FMCG growth, food distribution upgrades, and export manufacturing, all of which support broader demand for corrugated formats in the Asia-Pacific containerboard market. As a result, the rest of Asia-Pacific is increasingly important not just as a demand destination, but also as a location for conversion, fiber recovery, and specialized packaging investment.

Competitive Landscape

The Asia-Pacific containerboard market is moderately concentrated at the integrated mill level, but it stays fragmented at the converting stage, where many local box plants compete on service and delivery speed. The leading pattern in the Asia-Pacific containerboard market is the divide between Chinese majors that pursue scale and raw-material control, and Japanese or Southeast Asian groups that emphasize premium applications and selective regional growth. That difference matters because scale-based competition pressures commodity grades, while certification, automation, and application know-how create room for margin in higher-value segments. The Asia-Pacific containerboard market, therefore, rewards companies that can combine large asset bases with disciplined capital allocation rather than simply add capacity. It also explains why the strongest players are expanding in very different ways across the region.

Oji Holdings exited containerboard manufacturing in New Zealand and redirected capital toward India and Southeast Asia, indicating a clear preference for markets with a better demand-supply balance and stronger packaging growth. Nine Dragons Paper disclosed more than RMB 700 million (USD 96 million), in environmental-facility capital expenditure in FY2025 alongside ongoing pulp and paper investment, signaling a strategy built on both cost leadership and compliance. SCG Packaging expanded its use of AI, machine learning, and deep learning across production, energy, logistics, and inventory management in FY2025, while also reporting 140 patents in registration globally. These moves show that the Asia-Pacific containerboard market is being shaped as much by operating systems and product quality as by raw tonnage.

Smurfit Westrock reported USD 2.76 billion in net sales for its EMEA and APAC segment in Q1 2026 and said its APAC operations significantly outperformed peers on improving demand and customer wins. Marubeni also continued to operate through majority-owned containerboard manufacturing subsidiaries in Vietnam and Japan, which adds another layer of regional competition anchored in cross-border industrial networks.[4]Marubeni Corporation, “Marubeni Corporation Integrated Report 2025,” Marubeni Corporation, marubeni.com The most attractive openings in the Asia-Pacific containerboard market remain in pharmaceutical cold-chain packaging, export-oriented electronics applications, and recyclable food-service formats where certification and coating capability matter. In practical terms, that means the Asia-Pacific containerboard market is becoming less of a pure commodity contest and more of a capability contest in selected high-value niches.

Asia-Pacific Containerboard Industry Leaders

Smurfit Westrock plc

International Paper Company

Oji Holdings Corporation

Visy Industries Holdings Pty Ltd.

Rengo Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Smurfit Westrock's Q1 2026 results confirmed that its EMEA and APAC business continued to grow with an improving demand profile and customer wins, containerboard prices in the region increased in March and April 2026 due to higher energy costs and strengthened demand.

- February 2026: Lee and Man Paper Manufacturing's Guigang, Guangxi, subsidiary entered into a RMB 1,500 million (USD 207 million) fixed-asset loan agreement to fund Phase I construction of its new Guigang mill, planned to produce 800,000 tonnes per annum of sanitary paper and 1 million tonnes per annum of pulp upon completion.

- September 2025: Nine Dragons Paper Holdings Limited announced FY2025 annual results, year ended June 30, 2025, reporting total revenue of RMB 63,240.5 million (USD 8.71 billion), net profit of RMB 2,201.7 million (USD 303 million), up 177.3% year-on-year, on record sales volume of 21.5 million tonnes.

- September 2025: Visy Industries Holdings Pty Ltd. completed a USD 30 million upgrade to its 100% recycled paper mill on Gibson Island, Brisbane, Australia, enabling production of new containerboard grades for Queensland's agricultural and food and beverage industries, the project involved 100,000 staff hours and 170 workers over the upgrade period.

Asia-Pacific Containerboard Market Report Scope

The scope of this report covers the Asia-Pacific containerboard market, including an analysis of market trends, growth drivers, challenges, and opportunities. Containerboard is the material used to produce corrugated boxes, primarily consisting of linerboard and corrugating medium. This report examines the market dynamics, supply chain, and competitive landscape, providing insights into the industry's current state and future prospects within the Asia-Pacific region.

The Asia-Pacific Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), End User (Food and Beverage, Consumer Goods, Industrial, and More), and Geography (China, India, Japan, South Korea, Indonesia, and Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End Users |

| China |

| India |

| Japan |

| South Korea |

| Indonesia |

| Rest of Asia-Pacific |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End User | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End Users | |

| By Geography | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current size of the Asia-Pacific containerboard market?

The Asia-Pacific containerboard market was valued at USD 70.86 billion in 2025, is estimated at USD 73.3 billion in 2026, and is forecast to reach USD 92.05 billion by 2031 at a 4.66% CAGR.

Which segment leads to demand by material?

Recycled fibers led demand with a 67.83% share in 2025 because they remain the cost-effective base for standard corrugated board production across the region.

Which board type is growing the fastest in Asia-Pacific?

Flutings are projected to grow at a 5.69% CAGR from 2026 to 2031, supported by automated fulfillment, stronger logistics requirements, and export packaging needs.

Which end-user group creates the largest revenue base?

Food and beverage was the largest end-user segment with a 39.54% share in 2025, supported by organized retail, processed food consumption, and cold-chain packaging demand.

Which country offers the strongest growth opportunity through 2031?

India is forecast to grow at a 6.46% CAGR from 2026 to 2031, making it the fastest-growing major country market in the region.

What is shaping competition among major containerboard producers in Asia-Pacific?

Competition is being shaped by raw-material integration, certification, automation, and selective expansion into India and Southeast Asia, while large Chinese mills still influence regional pricing and supply conditions.

Page last updated on: