Iran Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

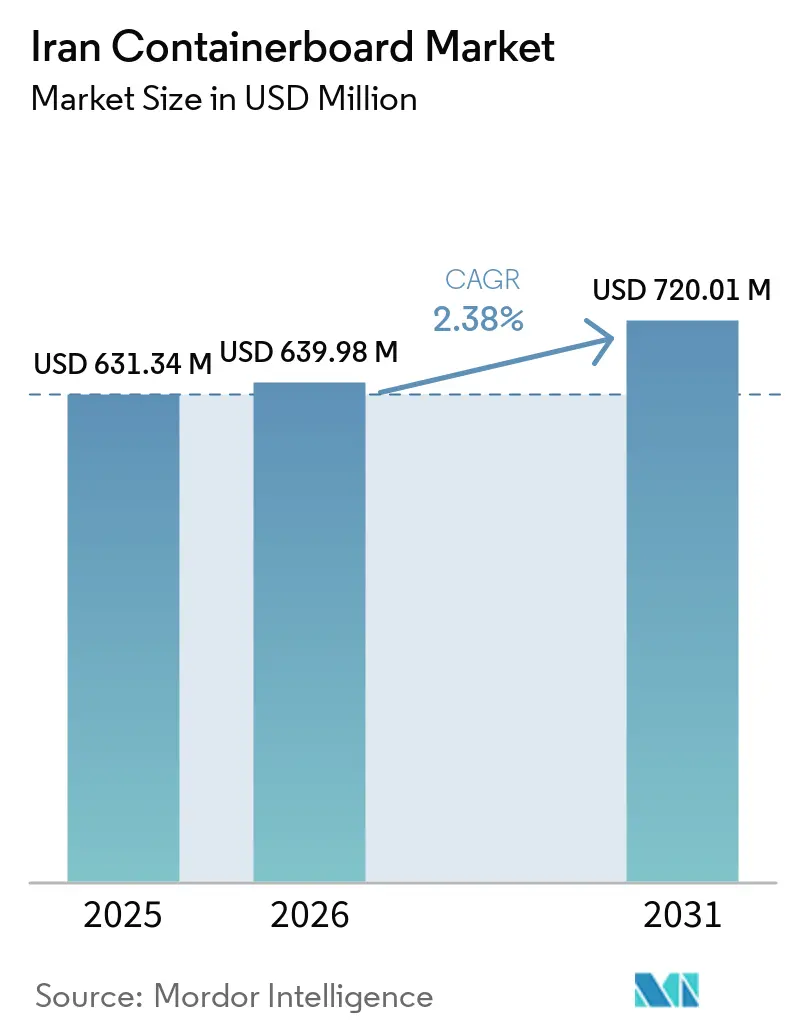

| Base Year Market Size (2025) | USD 631.34 Million |

| Market Size (2026) | USD 639.98 Million |

| Market Size (2031) | USD 720.01 Million |

| Growth Rate (2026 - 2031) | 2.38% CAGR |

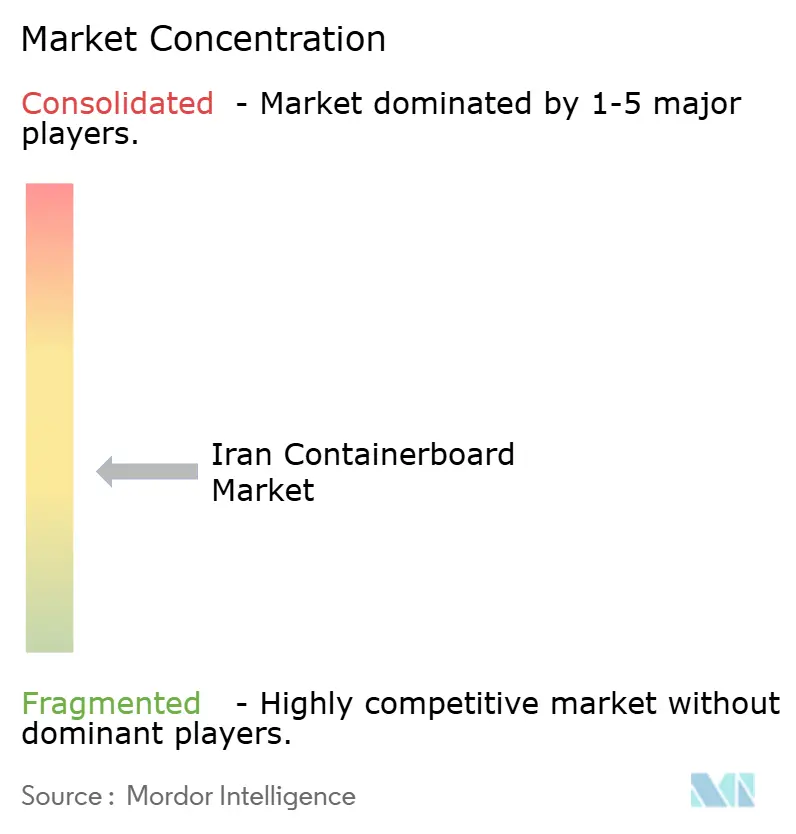

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Iran Containerboard Market Analysis by Mordor Intelligence

The Iran Containerboard Market size is projected to expand from USD 631.34 million in 2025 and USD 639.98 million in 2026 to USD 720.01 million by 2031, registering a CAGR of 2.38% between 2026 to 2031.

Demand in the Iran containerboard market remains tied to food processing and consumer goods, where urbanization and higher packaged-goods consumption continue to widen the base for corrugated and linerboard demand. Iran also has installed corrugated manufacturing capacity of more than 3 million tons, while actual annual production stays near 1 million tons, which means the sector still operates at close to one-third of rated output. That gap reflects energy interruptions, sanction-related supply friction, and aging converting machinery rather than weak end-market demand. The Iran containerboard market is also receiving support from cross-material substitution as higher plastic prices in 2026 push more FMCG suppliers toward paper-based secondary packaging. At the same time, the country’s position next to Iraq, Afghanistan, Turkey, Pakistan, and the Caspian economies gives domestic suppliers a practical freight advantage in nearby export markets.

Key Report Takeaways

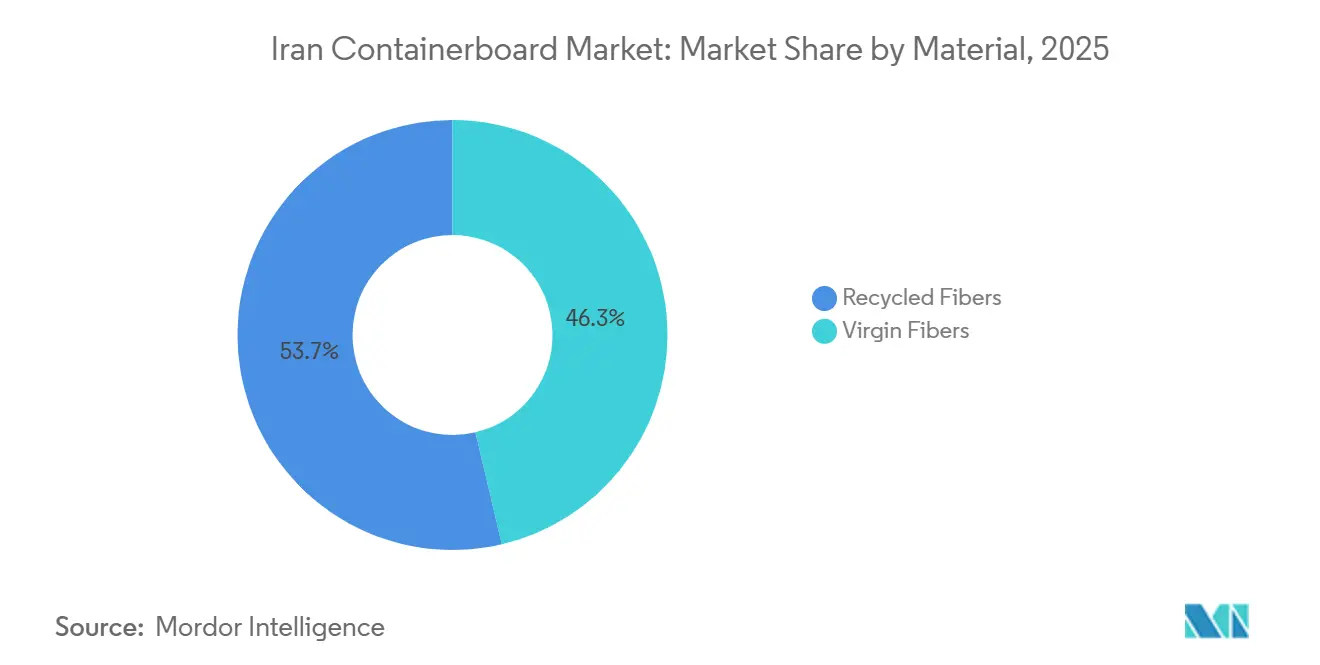

- By material, recycled fibers led with 53.68% of the market in 2025, while virgin fibers recorded the highest projected CAGR at 4.41% through 2031.

- By product type, testliners held 34.60% of the Iran containerboard market in 2025, while flutings posted the fastest projected CAGR at 4.29% through 2031.

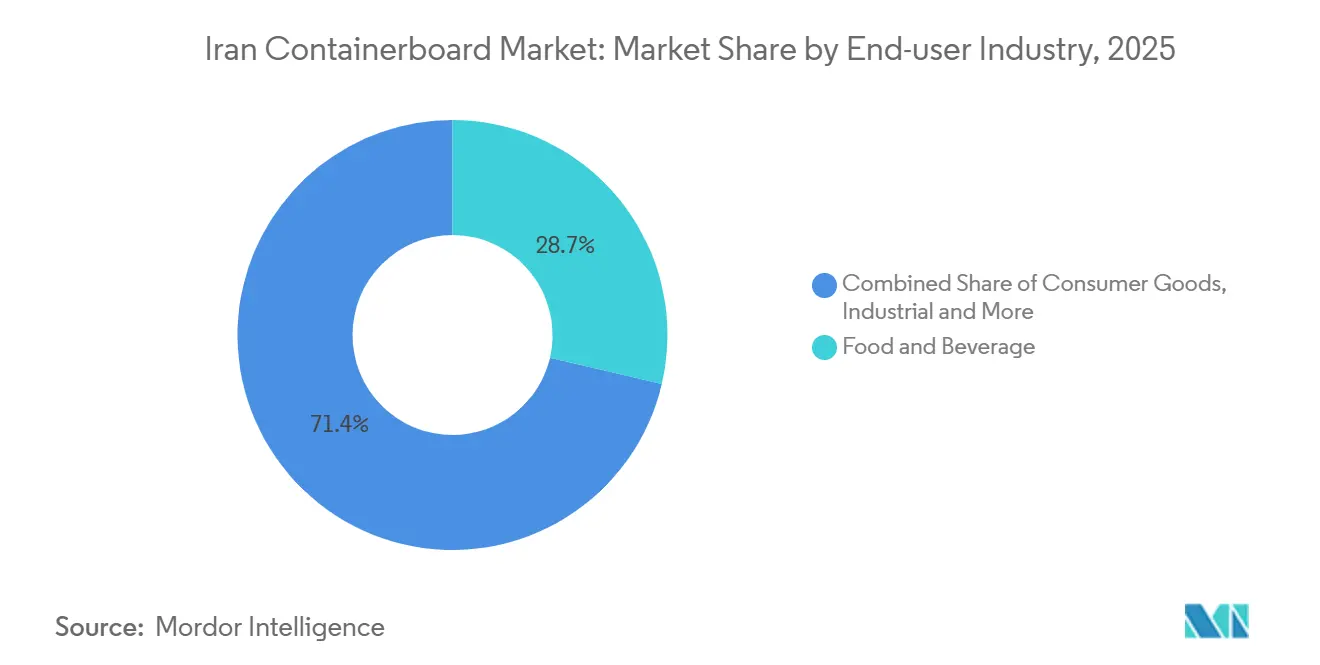

- By end-user industry, food and beverage accounted for 28.65% of the market in 2025 and also recorded the highest projected CAGR at 3.93% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Iran Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Packaged Food and Beverage Output | +0.7% | National, concentrated in Tehran, Isfahan, and Khuzestan industrial corridors | Medium term (2-4 years) |

| Growth in Produce and Protein Cold-Chain Cartons | +0.5% | National, with early gains in northern agri-hubs such as Gilan and Mazandaran and in protein-processing zones | Long term (≥ 4 years) |

| E-commerce and Parcel Shipments Expanding Corrugated Demand | +0.4% | Urban-centric, especially Tehran, Mashhad, and Isfahan | Short term (≤ 2 years) |

| Plastic-to-Paper Substitution in Secondary Packaging | +0.3% | Global spillover into Iran, strongest in export-oriented FMCG supply chains | Short term (≤ 2 years) |

| Export White-Space in Neighboring Paper-Based Packaging Trade | +0.2% | Iraq, Afghanistan, and the CIS corridor | Medium term (2-4 years) |

| Domestic Recycled-Fiber Capacity Additions Improving Supply Security | +0.1% | Isfahan, Zanjan, and the Aras Free Trade Zone | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Packaged Food and Beverage Output

The Iran containerboard market continues to draw its most stable support from food processing and packaged consumer staples. Urban dietary shifts are raising demand for convenient and pre-packed foods, which increases the need for corrugated packaging in plant handling, warehousing, and shipment. Cold-chain expansion in dairy, protein, and ready-meal distribution is also adding pressure for better board performance across the Iran containerboard market. Pars Paper Industries Group directly targets food packaging applications through unbleached and bleached kraft linerboard lines made from bagasse-based pulp in Khuzestan.[1]Pars Paper Industries Group, “Official Company Profile and Product Information,” Pars Paper Industries Group, parspaper.ir Industry association reporting in January 2026 stated that food and beverage converters represented the single largest domestic corrugated end-use base. Food manufacturers shipping to Iraq and Afghanistan also create packaging demand at origin and again for export movement, which keeps this driver central to the Iran containerboard market.

Growth In Produce And Protein Cold-Chain Cartons

The Iran containerboard market is also benefiting from the gradual buildout of cold-chain distribution for produce and protein products. Northern provinces such as Gilan and Mazandaran long relied on simpler corrugated formats, but newer cold-storage and specialized packaging projects are pushing substrate requirements higher. Academic reporting in 2025 on a specialized seedling packaging and cold-storage center showed how infrastructure investment is tightening the link between refrigerated logistics and packaging quality. This shift supports coated and moisture-resistant fluting grades that can tolerate chilled distribution and multi-stage handling across the Iran containerboard market. Protein and dairy applications are moving faster because wet-strength and barrier-treated cartons are becoming more relevant in milk, yogurt, and related chains. If this mix keeps improving, the Iran containerboard market can lift revenue per ton before overall shipment volumes change materially.

E-Commerce And Parcel Shipments Expanding Corrugated Demand

The Iran containerboard market gained a fresh layer of demand as e-commerce and parcel flows expanded through 2025. Higher smartphone use, wider mobile payment adoption, and stronger consumer acceptance of online retail have increased the number of dedicated corrugated shipping cases needed per order. Parcel logistics also favor lighter and more printable B-flute and micro-flute formats, which were less central in Iran’s older industrial corrugated mix. Taw Paper Company has positioned part of its packaging paper offer around grades suited to lighter-weight carton applications, and its Aras Free Trade Zone facility remains oriented to packaging papers that match these needs. The free-zone location also shortens lead times for domestic delivery and for shipments into the South Caucasus market. That combination keeps parcel demand as a near-term support factor for the Iran containerboard market even when broader industrial demand remains uneven.

Plastic-To-Paper Substitution In Secondary Packaging

The Iran containerboard market is receiving a near-term tailwind from disruption in regional petrochemical and plastic supply chains during 2026. Plastic prices rose to near four-year highs as oil and petrochemical flows from the region were disrupted. That price pressure pushed consumer goods producers to accelerate secondary packaging trials with corrugated and other paper-based formats. In practical terms, mills in the Iran containerboard market that once competed against low-cost shrink-wrap are now seeing trial orders from FMCG producers that previously had little reason to switch materials. The effect is important because it adds demand that was not embedded in older planning assumptions for paper-based secondary packaging. It also supports the Iran containerboard market beyond domestic sales because export-oriented FMCG supply chains face the same material-cost pressure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Power and Gas Outages Disrupting Mill Utilization | -0.6% | National, most severe in summer peak months across industrial parks | Short term (≤ 2 years) |

| Sanctions-Linked Constraints on Pulp, Chemicals, and Spare Parts | -0.5% | National, particularly acute for mills reliant on imported specialty pulp and chemicals | Long term (≥ 4 years) |

| OCC Quality Variability and Recovered-Fiber Inflation | -0.3% | National, with strongest exposure in Isfahan, Yazd, and Tehran corridors | Medium term (2-4 years) |

| Demand Weakness in Discretionary Consumer Goods Packaging | -0.2% | Urban consumer markets such as Tehran, Tabriz, and Mashhad | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Power And Gas Outages Disrupting Mill Utilization

Power and gas instability remains the sharpest operating restraint for the Iran containerboard market. Close to 50% of industrial park production capacity was halted by power outages, showing how broad the disruption became during 2024. Paper and board mills are more exposed than many other industries because they depend on steady steam, heat, and electrical loads through wet-end and drying operations. When those processes stop unexpectedly, mills face equipment stress, basis-weight inconsistency, and higher broke rates instead of saleable output. These conditions help explain why installed capacity in the Iran containerboard market stays far above realized production even when end-use demand remains present. Until energy reliability improves, the Iran containerboard market is likely to remain structurally underutilized rather than demand-constrained.

Sanctions-Linked Constraints On Pulp, Chemicals, And Spare Parts

Sanctions remain the second major restraint on the Iran containerboard market because they restrict access to critical inputs and maintenance items. Restrictions tied to dual-use goods and petrochemical products connected to Iran matter for mills because specialty pulp, sizing agents, starch-based chemicals, and spare parts become harder and costlier to source under banking and trade limits.[2]Council of the European Union, “Council Implementing Regulation (EU) 2025/1980 of 29 September 2025 Implementing Regulation (EU) No 267/2012 Concerning Restrictive Measures Against Iran,” EUR-Lex, eur-lex.europa.eu Even goods that can still move often pass through third-country intermediaries, which raises landed cost and stretches lead times across the Iran containerboard market. Chinese suppliers have covered part of the spare-parts gap, but compatibility issues can still complicate planned maintenance and product upgrades. These supply frictions keep the Iran containerboard market from responding fully when demand improves in food packaging, cold-chain cartons, and export-oriented applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled-Fiber Base Entrenched, Virgin Grades Target Premium Niches

Recycled fibers held 53.68% of Iran containerboard market share in 2025, which kept them at the center of the material mix in an import-constrained operating environment. Mills in Yazd, Isfahan, and the greater Tehran belt remained heavily dependent on OCC collection and recycled-fiber procurement to support containerboard output in 2025 and 2026. The core advantage of this model is cost, because recovered fiber is more accessible than imported virgin pulp when trade routes and foreign currency remain under pressure. At the same time, quality variability in locally collected OCC continues to affect furnish consistency because municipal waste-separation systems remain uneven across the country. That means recycled fiber stays dominant in the Iran containerboard industry, but the full margin benefit is diluted by quality-management costs and the need for tighter furnish control.

Virgin fibers in the Iran containerboard market size are projected to expand at a 4.41% CAGR through 2031, which makes them the fastest-growing material segment. Brand owners moving into premium kraft and barrier-treated linerboards are the main source of support because these applications need better burst strength, printability, and performance consistency. This shift is still selective rather than broad, since most volume remains concentrated in cost-sensitive grades across the Iran containerboard market. Pars Paper’s bagasse-based kraft linerboard gives the company a distinct position because it offers virgin-like performance without relying on imported wood pulp. That model matters for the Iran containerboard industry because non-wood fiber sourcing can protect premium-grade output when sanctions and logistics pressure make imported virgin pulp less dependable.

By Product Type: Testliners Lead Volume, Fluting Emerges As The Growth Engine

Testliners commanded 34.60% of Iran containerboard market share in 2025, which reflected their role as the standard outer ply across commodity food, consumer goods, and industrial boxes. Their lead position comes from the structure of domestic production, where many mills use recycled OCC furnish to make grades suited to existing converting equipment and prevailing transport conditions. That gives testliners a broad installed base across the Iran containerboard market, especially where cost control matters more than premium specification. The grade also fits the needs of price-sensitive converters that compete mostly in standard corrugated formats and high-volume jobs. As long as commodity applications dominate the mix, testliners are likely to remain the volume anchor of the Iran containerboard market.

Flutings are projected to advance at a 4.29% CAGR through 2031, which makes them the fastest-growing product type in the Iran containerboard market size. This expansion is tied to rising demand for medium grades used in single-wall and double-wall cartons for cold-chain produce, proteins, and pharmaceutical secondary packaging. Those applications need stronger ring-crush and flat-crush performance than basic commodity cartons, so fluting demand is improving even when broader market growth remains moderate. Pishtazan Cellulose Shargh’s Isfahan facility is part of the newer investment base focused on liner, testliner, and fluting grades from recycled furnish. If cold-chain and higher-specification transit packaging continue to expand, flutings will remain the clearest product growth engine within the Iran containerboard market.

By End-User Industry: Food And Beverage Anchors Growth Across The Forecast

Food and beverage accounted for 28.65% of the Iran containerboard market size in 2025 and is projected to grow at a 3.93% CAGR through 2031, which makes it both the largest and the fastest-growing end-user segment. This pattern is notable because containerboard markets often see a more industrial or mixed-use demand center holding the largest share, while Iran continues to rely on packaged food demand as the main stabilizer. The segment remained resilient because food volumes are less exposed to discretionary spending pressure than many consumer goods categories. That resilience supports baseline box consumption across the Iran containerboard market even when wider economic conditions stay uneven. It also reinforces why producers with reliable food-grade board quality have a stronger path to steady order flow.

Consumer goods remained the second important demand pool, covering personal care, household products, and apparel-related packaging in the Iran containerboard market. This segment has been less stable because weaker purchasing power puts pressure on discretionary product volumes and the related corrugated demand base. Industrial end users still require heavier corrugated formats for machinery, chemicals, and building products, but their packaging draw is more sensitive to construction and manufacturing cycles. Other end-user industries, including pharmaceuticals and agricultural inputs, remain smaller in volume but more demanding in terms of substrate performance and specification control. The overlap between food and pharmaceutical packaging needs is gradually raising demand for barrier-treated and higher-performance board, which exposes a capability gap that some mills with aging machinery still struggle to fill in the Iran containerboard market.

Geography Analysis

The Iran containerboard market remained geographically concentrated around the country’s main industrial and consumption corridors in 2025 and 2026. The Greater Tehran and Alborz belt continued to serve as the densest converting zone because it sits close to the country’s largest food and consumer goods manufacturing base. That proximity keeps freight cycles shorter and gives converters faster access to customers that consume high volumes of corrugated packaging. Northern Iran also held a core production role through Mazandaran Wood and Paper Industries in Sari, where reported integrated capacity stood at 175,000 metric tons.[3]Ghasem Mohammadi, “We Must Activate the Enormous Potential of the Wood and Paper Industry,” Mizan Online, mizanonline.ir

The northern cluster matters not only for current output but also for the longer-term scale potential of the Iran containerboard market. Company leadership at Mazandaran Wood and Paper Industries stated publicly that the sector still has large underused production and export capacity if operating conditions improve. Khuzestan supports a different competitive model because Pars Paper draws on sugarcane bagasse from Haft Tepe for kraft linerboard production. That feedstock base reduces direct exposure to imported wood and chemical pulp, which is an important advantage when sanctions and trade finance remain restrictive. East Azerbaijan has also become more relevant through Taw Paper’s Aras Free Trade Zone facility, where border access and free-zone infrastructure help shorten logistics to Turkey, the South Caucasus, and Central Asia.

Isfahan has emerged as a newer cluster within the Iran containerboard market through recent investment in recycled-fiber-based liner, testliner, and fluting capacity. Pishtazan Cellulose Shargh’s setup in Segzi Industrial Town reflects how new projects are following local waste streams and lower-cost industrial land rather than only traditional paper centers. Zanjan adds scale through Rasha Caspian Iranian Paper Manufacturing Complex, which reported annual capacity of 350,000-380,000 metric tons and exports to 22 countries. This spread across northern, central, western, and border-linked zones gives the Iran containerboard market a wider industrial footprint than current realized output levels would suggest. Plastic supply disruption in 2026 also improved regional export interest in paper-based packaging, which supports the geographic logic of serving nearby markets from Iran rather than from more distant suppliers.

Competitive Landscape

The Iran containerboard market remained highly fragmented in 2026, with more than 200 sheet and board producers and over 5,000 downstream converters competing across standard grades. No single producer held a dominant position, which kept price competition intense and limited the room for broad-based margin expansion. Rasha Caspian and Pars Paper stood out more for scale, integration, and technical differentiation than for outright market control.[4]Rasha Caspian Iranian Paper Manufacturing Complex, “Official Company Profile,” Rasha Caspian Iranian Paper Manufacturing Complex, en.rasha-paper.com This structure continues to suppress reinvestment cycles in the Iran containerboard market because many smaller players compete mainly on price.

The better-performing companies rely on operating model advantages rather than scale alone in the Iran containerboard market. Pishtazan Cellulose Shargh has built a liner-to-fluting product range from one site, which helps it serve corrugated integrators with a more complete offer. Rasha Caspian also introduced an online environmental monitoring system at the outlet of its wastewater treatment plant, which shows that compliance-led investment is entering the competitive logic of the sector. These moves do not change fragmentation immediately, but they do show where stronger operators are trying to separate themselves in the Iran containerboard market.

The clearest white space remains in coated and barrier-treated fluting grades for cold-chain and pharmaceutical corrugated uses. No domestic supplier has yet established reliable large-scale supply in these higher-specification niches, which keeps the field open for better-capitalized entrants. Smaller converters such as Sahand Carton Company, Azim Carton, and Part Carton still compete mainly on price and proximity to customers rather than on technical grade differentiation. That leaves the Iran containerboard market with a split structure, where commodity grades are crowded while higher-performance substrates remain relatively underdeveloped. The most durable advantage is likely to come from steadier input access, newer machinery, and product consistency that can support both domestic premium demand and regional export ambitions.

Iran Containerboard Industry Leaders

Rasha Caspian Iranian Paper Manufacturing Complex

Pars Paper Industries Group

Papyrus Kaveh Paper Company

Modern Green Paper Company

Sayan Gostar Irsa Paper Industry

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Iran's Iran Corrugated and Board Association held its annual industry managers' gathering on December 23, 2025, at the Parsian Evin Hotel in Tehran. The session, chaired by Association CEO Aliqoli Hosni Azami, identified technology gaps, aging machinery, raw-material price volatility, and OCC quality inconsistency as the 4 most urgent structural constraints to capacity utilization improvement.

- October 2025: The European Union reimposed nuclear-related sanctions against Iran under the JCPOA snapback mechanism, with Council Implementing Regulation (EU) 2025/1980 entering into force on September 30, 2025. The regulation reintroduced restrictions on dual-use goods and petrochemical products, tightening the import environment for specialty pulp, starch chemicals, and paper-mill spare parts.

Iran Containerboard Market Report Scope

The Iran Containerboard Market encompasses the production, distribution, and consumption of containerboard used in the manufacture of corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The market is driven by the increasing demand for sustainable, lightweight, and durable packaging solutions.

The Iran Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the size of the Iran containerboard market in 2025 and 2031?

The Iran containerboard market was valued at USD 631.34 million in 2025 and is forecast to reach USD 720.01 million by 2031, growing at a 2.38% CAGR during 2026-2031.

Which material segment leads the Iran containerboard space?

Recycled fibers led the market in 2025 with a 53.68% share, supported by the availability and cost position of OCC-based furnish.

Which product type is growing fastest in Iran’s containerboard business?

Flutings are projected to grow at a 4.29% CAGR through 2031 because cold-chain produce, protein, and other protective carton uses are expanding.

Why does food and beverage matter so much for demand in Iran?

Food and beverage accounted for 28.65% of demand in 2025 and also posted the highest end-user CAGR at 3.93%, making it the main volume anchor.

What is holding back faster growth for producers in Iran?

Power and gas outages, sanction-related constraints on pulp and chemicals, aging machinery, and recovered-fiber quality issues continue to limit utilization and upgrades.

Where are the main growth opportunities for suppliers over the next few years?

The best openings are in cold-chain cartons, e-commerce shipping cases, paper substitution for plastic secondary packaging, and export-oriented higher-specification grades.

Page last updated on: