Kenya Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

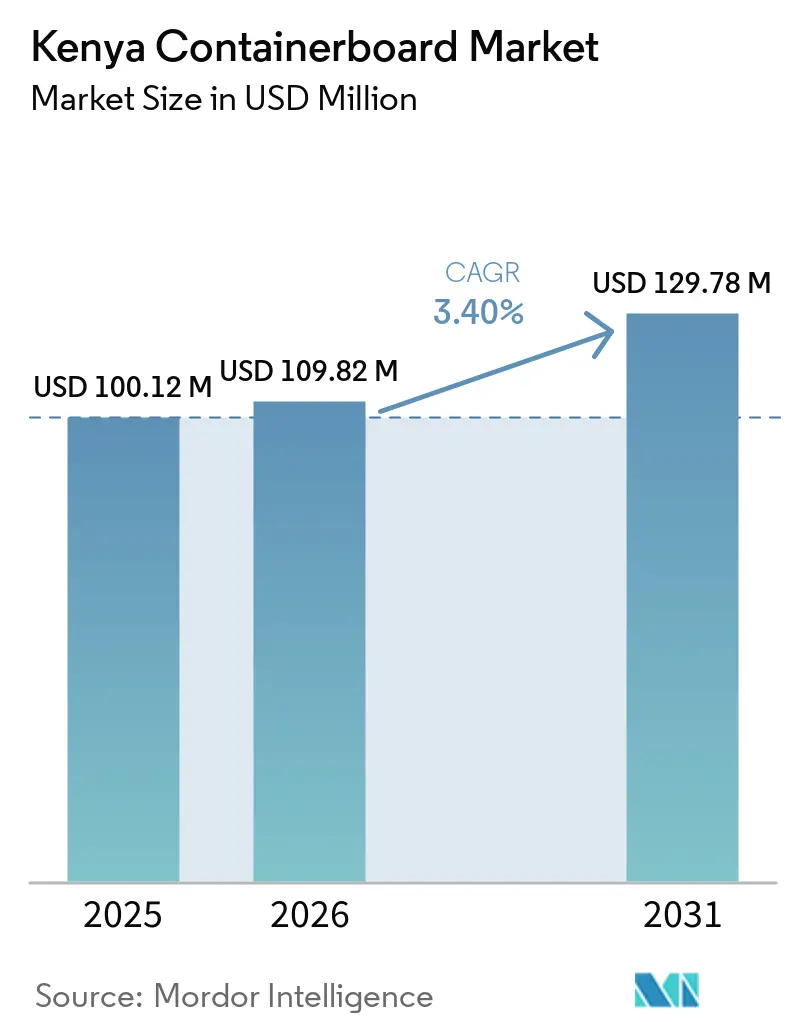

| Base Year Market Size (2025) | USD 100.12 Million |

| Market Size (2026) | USD 109.82 Million |

| Market Size (2031) | USD 129.78 Million |

| Growth Rate (2026 - 2031) | 3.40% CAGR |

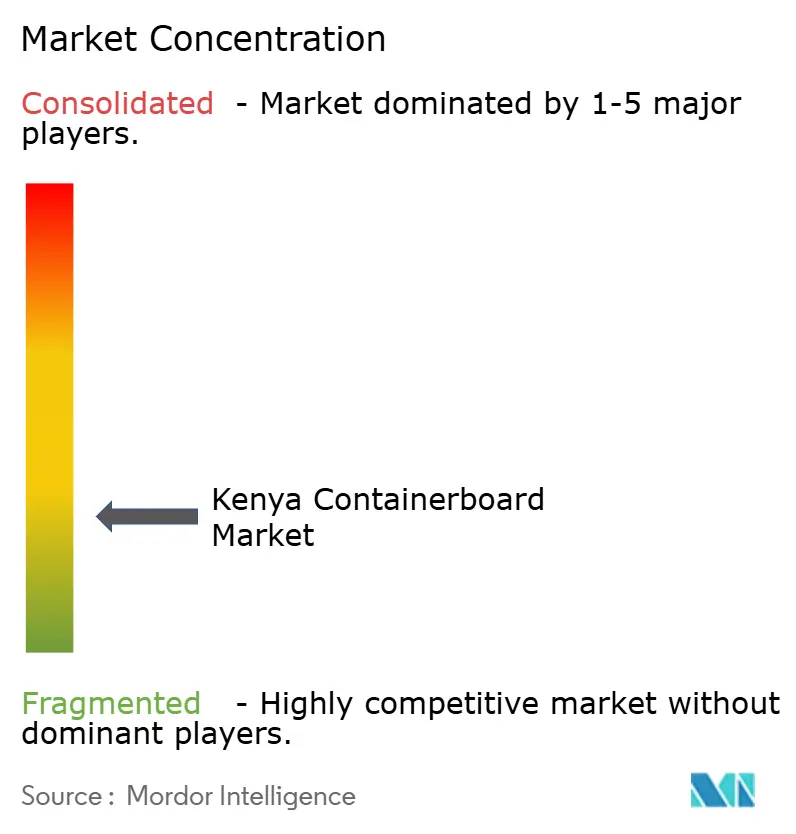

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kenya Containerboard Market Analysis by Mordor Intelligence

The Kenya Containerboard Market size is expected to increase from USD 100.12 million in 2025 to USD 109.82 million in 2026 and reach USD 129.78 million by 2031, growing at a CAGR of 3.40% over 2026-2031.

The Kenya containerboard market is expanding at a measured pace because food processing, export horticulture, and digital commerce are broadening demand while input costs remain under pressure. The Finance Act 2025 raised costs for corrugated box converters through a 25% excise duty on imported kraftliner from July 1, 2025, which matters because export-grade inputs still lack reliable domestic substitutes. Demand conditions remain supportive because Kenya’s food processing base is widening the use of secondary and transit corrugated packaging across dairy, beverages, grain milling, and prepared foods. Export agriculture and online retail are also pushing the Kenya containerboard market toward stronger box performance, better moisture resistance, and more reliable transit packaging across longer routes and more touchpoints. At the same time, EPR enforcement, tighter plastic packaging rules, and persistent electricity cost pressure mean the Kenya containerboard market is growing through active cost and policy management rather than through passive volume expansion.

Key Report Takeaways

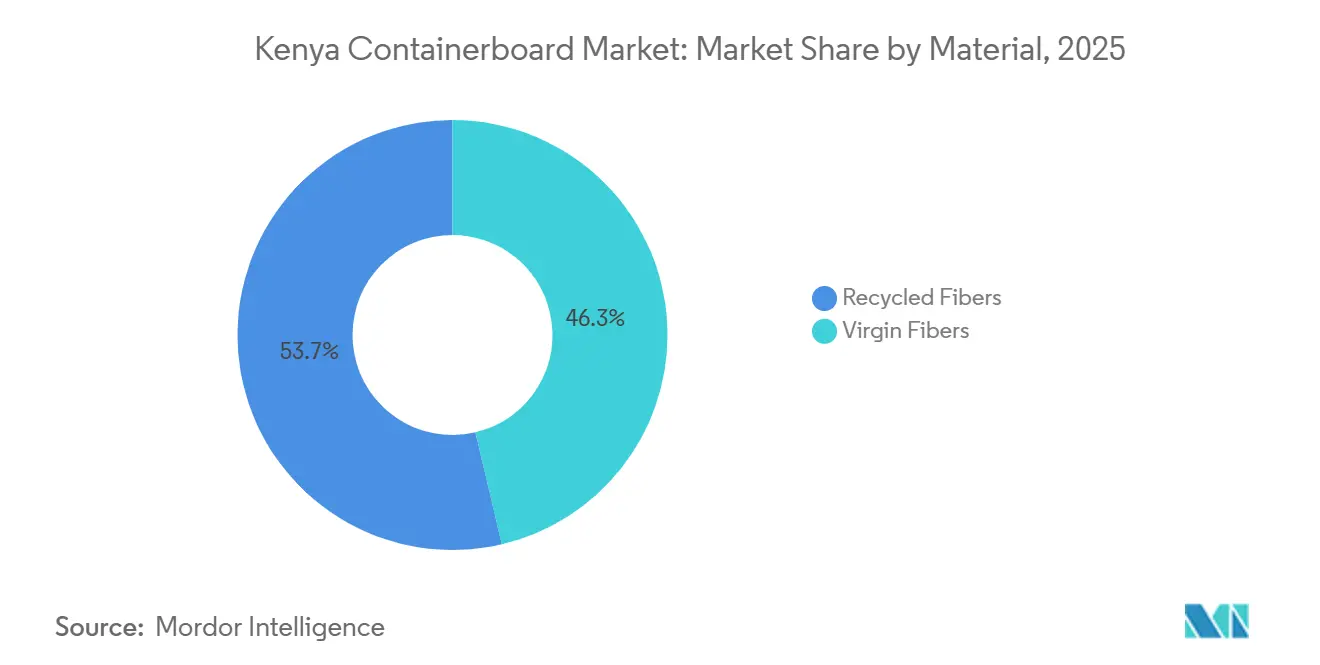

- By material, recycled fibers led with 53.68% of the Kenya containerboard market share in 2025, while virgin fibers are forecast to expand at a 4.41% CAGR through 2031.

- By product type, testliners held 34.61% share of the Kenya containerboard market size in 2025, while flutings recorded the highest projected CAGR at 4.27% through 2031.

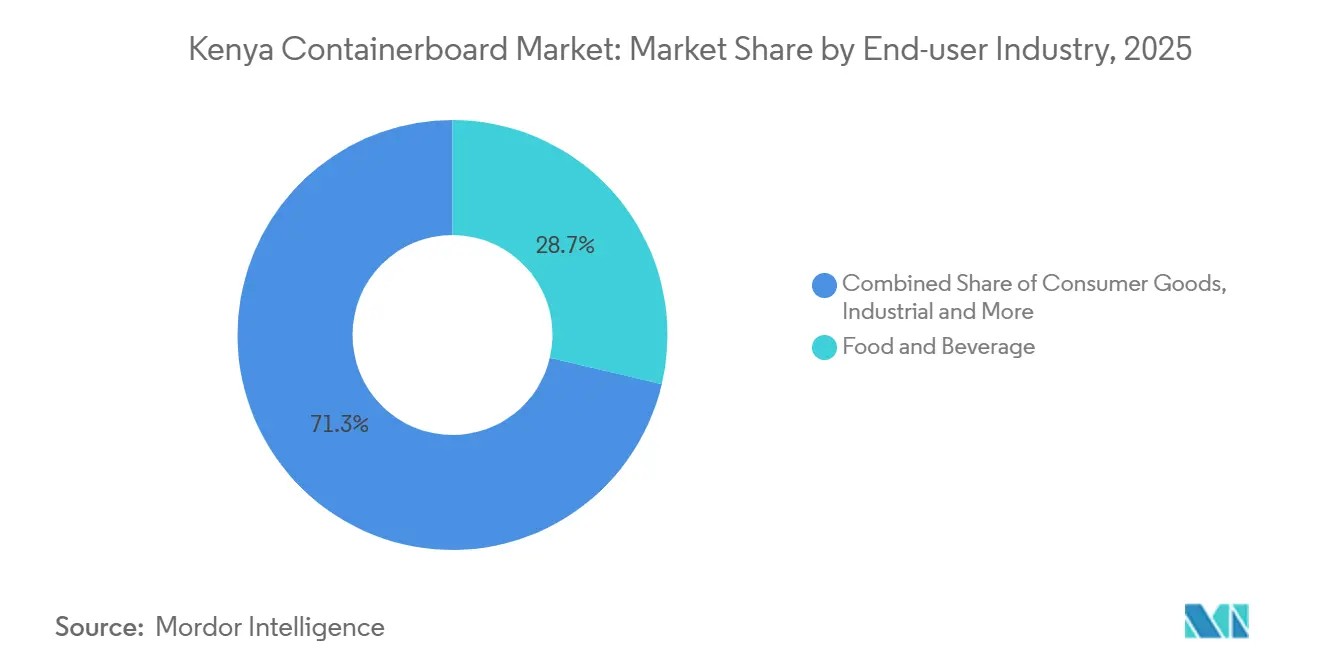

- By end-user industry, food and beverage accounted for 28.67% share of the Kenya containerboard market size in 2025 and is also advancing at a 3.87% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Kenya Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth In Processed Food, Dairy, And Packaged Beverage Output | +0.9% | National, concentrated in Nairobi, Eldoret, and Mombasa food processing corridors | Medium term (2-4 years) |

| Expansion Of Corrugated Packaging Needs In Horticulture Exports | +0.7% | National, with early gains in Naivasha, Timau, and Meru horticultural belts | Short term (≤ 2 years) |

| Extended Producer Responsibility And Plastic Substitution | +0.5% | National, with spillover to regional supply chains serving Tanzania and Uganda | Medium term (2-4 years) |

| Rising E-Commerce And Modern Retail Distribution | +0.4% | National, urban cores including Nairobi and Mombasa, emerging rural e-commerce belt | Medium term (2-4 years) |

| Shift Toward Recycled Fiber And Circular Packaging Inputs | +0.3% | National, with supply-chain links to bagasse-producing Kisumu and western Kenya | Long term (≥ 4 years) |

| Demand For Higher-Performance Boxes For Longer Export Routes | +0.2% | Export hubs, Jomo Kenyatta International Airport and Port of Mombasa corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growth In Processed Food, Dairy, And Packaged Beverage Output

Kenya’s food processing sector was valued at USD 9 billion in 2024 and is projected to reach USD 13 billion by 2030 under government-backed agro-industrial plans, which gives the Kenya containerboard market a broad and durable demand base.[1]Invest Kenya, “Agro-processing Sector Pack,” Invest Kenya, investkenya.go.ke Dairy shows how this demand builds because Kenya produced more than 5 billion liters of milk in 2024, supported by 40 licensed milk processors, 173 cottage dairy industries, and 67 mini-dairies that all require corrugated secondary packaging for case packing and transport. The Kenya containerboard market is also benefiting from the spread of cold-chain and organized distribution into tier-2 and tier-3 cities, where sealed carton cases are replacing informal handling for more products. More than 1,200 companies operate across beverages, grain milling, meat, dairy, and prepared foods, which keeps packaging demand broad rather than dependent on a narrow customer base.[2]United States Department of Agriculture Foreign Agricultural Service, “Agricultural Trade in Kenya - Opportunities for US Exporters in a Changing Landscape,” USDA Foreign Agricultural Service, apps.fas.usda.gov This breadth supports the Kenya containerboard market because recurring food shipments need reliable transit protection even when consumers trade down within product categories.

Expansion Of Corrugated Packaging Needs In Horticulture Exports

Horticulture remains one of the most specification-sensitive demand pools in the Kenya containerboard market because export routes are long and product damage directly affects realized value. Kenya’s agricultural exports reached USD 4.3 billion in 2024, with cut flowers at USD 777.4 million and avocados at USD 161.8 million, which shows the scale of export-linked packaging needs. Flower exports were also projected to rise in 2025, which reinforces short-cycle demand for moisture-resistant cartons and transit-ready box formats. Export cartons for flowers and fresh produce require wet-strength and burst performance that recycled-fiber grades do not consistently deliver, so demand for virgin kraftliner remains structurally important in the Kenya containerboard market. That quality gap prevents full substitution into lower-cost domestic grades and keeps export packaging decisions tied to performance first and cost second.

Extended Producer Responsibility And Plastic Substitution

Kenya’s EPR framework became more formal after NEMA gazetted the Sustainable Waste Management regulations in November 2024 and Kenya Law published Legal Notice 62 of 2025 in March 2025, which created a clearer compliance setting for packaging producers. The regulations require producer registration, annual reporting, and verified waste management systems, which gives fiber-based packaging a compliance advantage where recycling channels already exist. This matters for the Kenya containerboard market because paper corrugates and cardboard fall within a system where recovery pathways are more established than for many single-use plastic formats. The result is not an immediate full replacement of plastics, but a gradual shift in formal supply chains toward corrugated secondary packaging for non-hazardous products. Over time, this regulatory direction supports the Kenya containerboard market by changing procurement logic from lowest upfront cost toward compliance, recovery, and material traceability.

Rising E-Commerce And Modern Retail Distribution

Digital retail is widening the addressable demand pool for the Kenya containerboard market beyond traditional FMCG channels. Kenya’s e-commerce revenues reached USD 762 million in 2024, and the sector recorded a 10.9% CAGR from 2020 to 2024, while the user base was expected to reach 40 million in 2026. Rural customers now account for 60% of total platform orders on one major marketplace, which means packaging demand is spreading into routes that previously relied on loose or informal shipment methods. Corrugated transit cartons are favored for multi-touchpoint handling through motorbike delivery, aggregation hubs, and regional dispatch points, which supports steady volume growth in the Kenya containerboard market. The product mix is also shifting toward lighter shippers and faster-assembly formats for urban fulfillment, which is improving the outlook for fluting grades alongside standard box demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Import Dependence For Kraftliner And Virgin Fiber Inputs | -0.5% | National, most acute for Nairobi-based converters supplying horticulture exporters | Short term (≤ 2 years) |

| High Electricity And Manufacturing Cost Burden | -0.4% | National, concentrated in Nairobi and Thika industrial zones | Medium term (2-4 years) |

| EPR Implementation Uncertainty And Compliance Complexity | -0.2% | National, with early gains in Nairobi and Mombasa formal retail channels | Medium term (2-4 years) |

| Competition From Lower-Cost Flexible Plastic Formats | -0.2% | National, most pronounced in informal and peri-urban retail channels | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Import Dependence For Kraftliner And Virgin Fiber Inputs

The biggest structural restraint on the Kenya containerboard market is the continued dependence on imported virgin kraftliner for export-grade boxes. The Finance Act 2025 imposed a 25% excise duty on kraftliner and kraft paper from July 1, 2025, which raised the cost of a 10-kg avocado carton by KES 26, or USD 0.20, and a standard flower box by KES 50, or USD 0.39. Government crisis talks in September 2025 acknowledged that wet-strength and food-contact kraft paper grades were not reliably available from domestic mills, which confirmed that policy protection had moved ahead of local supply capability. In 2026, manufacturers continued to press for duty removal, warning that export packaging costs could rise by as much as 17% without relief. This keeps the Kenya containerboard market exposed to both domestic tax policy and global recovered fiber cycles, with few effective hedging options for smaller converters.

High Electricity And Manufacturing Cost Burden

Electricity remains a core cost drag for the Kenya containerboard market because pulping, drying, and corrugation all require a steady power supply. Rai Paper’s Webuye mill paid KES 754 million, or USD 5.8 million, in electricity costs between its 2016 acquisition and 2025, underscoring how large energy expenses can become even for a scaled operator. Smaller converters have less bargaining power on tariffs and less capacity to absorb line stoppages, so load-shedding raises waste, disrupts throughput, and weakens delivery consistency. Larger players that can support cogeneration or other energy backstops have a clear operating advantage, as already evident in Western Kenya’s integrated paper and sugar complexes. This cost gap is likely to push the Kenya containerboard market toward gradual consolidation, as scale increasingly matters for energy resilience as much as for procurement.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fiber Dominates While Virgin Grades Drive Premium Demand

Recycled fibers accounted for 53.68% of the Kenya containerboard market share in 2025, which reflects the strong position of domestic mills that rely on OCC streams and agricultural fiber by-products. Kibos Paper and Packaging illustrates this model because its Kisumu operation produces more than 75 TPD of paper from bagasse and recycled inputs and reports a 90% material recycling rate. That operating structure fits well with the compliance direction under Kenya’s EPR framework, where recovery-ready paper packaging has a stronger long-term position than harder-to-recycle alternatives. The Kenya containerboard market has therefore built much of its local supply base around circular input systems rather than virgin pulp expansion.

Rai Paper’s Webuye mill also shifted away from virgin wood-pulp inputs after Kenya’s logging restrictions and was producing 27,600 tonnes annually in 2025 from OCC and bagasse-blend inputs. This supports the local supply position of recycled grades, but it does not eliminate the quality limits faced by the Kenya containerboard industry in high-specification export applications. Virgin fibers are forecast to expand at a 4.41% CAGR through 2031, which makes them the fastest-growing material segment in the Kenya containerboard market size even though their volume base is smaller. Export horticulture keeps this segment commercially necessary because moisture resistance and higher burst performance still depend on virgin kraftliner more than on recycled alternatives. The Kenya containerboard industry therefore remains split between a locally anchored recycled base and an import-reliant premium layer.

By Product Type: Testliners Lead While Flutings Gain From E-Commerce And Export Needs

Testliners held 34.61% of the Kenya containerboard market size in 2025, which made them the leading product type in the domestic supply chain. Their position reflects a practical fit between local recycled-fiber production and the needs of food, consumer goods, and industrial box users that require dependable but not premium-grade facing material. In the Kenya containerboard market, testliners remain the standard option where converters must balance price sensitivity with acceptable transit performance. This is why most locally produced corrugated boxes continue to rely on testliner-heavy configurations for routine domestic movement.

Flutings are forecast to expand at a 4.27% CAGR through 2031, which gives them the fastest growth rate among product types in the Kenya containerboard market. Growth is being supported by rising e-commerce shipments, where lighter-basis-weight shippers and efficient dimensional design matter more than maximum burst strength, and by greater use of double-wall constructions for longer export routes. Shri Krishana Overseas added meaningful local capacity when its Kisaju facility moved into commercial operation in early 2026, raising output capacity from 3,000 tonnes to 22,000 tonnes annually for testliner and fluting supply aimed at horticulture export and FMCG users. That investment should improve local availability in the mid-market, but kraftliners remain non-substitutable in the Kenya containerboard market where exporters need high-specification cartons. The balance across grades therefore continues to reflect a clear divide between domestic price-led demand and export performance-led demand.

By End-User Industry: Food And Beverage Anchors Scale And Growth

Food and beverage accounted for 28.67% share of the Kenya containerboard market size in 2025 and is also set to grow at a 3.87% CAGR through 2031, which makes it both the largest and the fastest-growing end-user segment. This position reflects the structure of Kenya’s food manufacturing base, where more than 1,200 companies operate across dairy, beverages, grain milling, and prepared foods. The Kenya containerboard market benefits from this recurring demand because these categories require secondary cases, transit cartons, and retail-ready packs through the year rather than in short export windows. The food and beverage segment also aligns closely with EPR and formal retail requirements, which helps keep packaging standards on an upward path.

Industry discussion in March 2026 at Propak East Africa centered on food-safe and recyclable packaging, which showed that suppliers and buyers are actively upgrading packaging formats for the FMCG channel. Consumer goods remain an important secondary demand pool in the Kenya containerboard market because regional brand owners are standardizing corrugated secondary packaging across East African distribution routes. Industrial users such as agrochemical, paint, and hardware producers provide steady baseline volume, while pharmaceuticals and horticulture require more specialized boxes with tighter quality demands. This mix means the Kenya containerboard market is supported by both broad-volume sectors and smaller premium applications. It also means segment growth is not relying on a single customer group, even though food and beverage remains the clearest volume anchor.

Geography Analysis

The Kenya containerboard market is national in scope, but internal demand and production patterns remain uneven across the country. Nairobi and its wider industrial corridor, including Thika, Athi River, and Ruiru, hold the largest concentration of corrugated box converting activity in the Kenya containerboard market because they sit close to major FMCG plants, industrial customers, and logistics services. This corridor handles both imported board and locally produced recycled grades, which gives it the broadest customer reach across domestic and export-related packaging demand. Mombasa plays a different role because it is the main logistics gateway for imported kraftliner and OCC, and it also links Kenyan exporters to sea routes serving Europe and Gulf markets. The Nairobi-Mombasa spine therefore shapes cost, lead time, and working capital conditions for a large share of the Kenya containerboard market.

Western Kenya is becoming more important as a production base because its input structure differs from that of the Nairobi corridor. Kibos Paper and Packaging near Kisumu benefits from direct access to bagasse from the adjacent sugar complex, which gives it a raw-material advantage compared with converters that depend mainly on urban waste collection or imported recovered fiber.[3]Kibos Sugar and Allied Companies, “Environment,” Kibos Sugar and Allied Companies, kibossugar.co.ke Rai Paper’s Webuye operation in Bungoma County was producing 27,600 tonnes annually in 2025 and is targeting expansion to 74,100 tonnes through a modernization plan valued at KES 931 million, or USD 7.2 million. If these western Kenya assets keep scaling, the Kenya containerboard market will have a deeper domestic supply base for recycled-fiber grades and somewhat lower reliance on imported testliner and medium.

Regional competitiveness also matters because export packaging costs influence Kenya’s position in horticulture and other traded goods. Export stakeholders warned in 2026 that packaging inflation linked to the excise duty on kraftliner could weaken Kenya’s competitiveness against other producer countries, which shows how closely the Kenya containerboard market is tied to trade performance. At the same time, the government continued to present Kenya as a gateway economy under the AfCFTA and signaled support for more local packaging capacity linked to agricultural exports. This leaves the Kenya containerboard market with a mixed geographic outlook, where logistics scale and institutional depth support investment, but input-cost policy still affects cross-border competitiveness.

Competitive Landscape

The Kenya containerboard market is fragmented at the converter level and concentrated upstream, which creates a layered competitive structure across the value chain. More than a dozen corrugated box manufacturers operate around Nairobi’s industrial zones and compete on price, delivery, account reliability, and end-use specialization rather than on strong product differentiation. At the board manufacturing stage, the field is much narrower, with Kibos Paper and Packaging, Rai Paper, and East African Paper Mills forming the main domestic production base for locally available grades. This supply structure means many converters in the Kenya containerboard market still depend on imported kraftliner when they serve premium export applications. As a result, competitive strategy is shaped as much by input access and energy resilience as by customer acquisition.

One visible strategic move came from Shri Krishana Overseas, which listed on the Nairobi Securities Exchange in July 2025 and then brought its Kisaju facility into commercial production in early 2026, expanding annual capacity from 3,000 tonnes to 22,000 tonnes.[4]Shri Krishana Overseas PLC, “SKL Expands Capacity Sevenfold with New Kajiado Facility,” Shri Krishana Overseas PLC, skl.co.ke That step shows a clear push toward scale in the Kenya containerboard market, especially in horticulture export and FMCG packaging. Kibos Paper and Packaging is following a different route through upstream integration, using bagasse and recycled fiber at a reported 90% recycling rate to create a lower-cost raw-material model. Its bagasse-to-paper production process also points to process-based differentiation in a market where many converters otherwise compete on service and price.

A third strategic move came from Printcare Packaging East Africa, which opened its Nairobi plant in March 2025 to serve tea, pharmaceutical, beverage, horticulture, and FMCG packaging requirements in Kenya and the wider region. Converters such as Dodhia Packaging Kenya and Carton Manufacturers Ltd continue to compete through high-mix orders, customer-specific carton specifications, and quality-system discipline rather than through raw-material integration. The main whitespace in the Kenya containerboard market remains in high-performance moisture-resistant export cartons, certified specialty boxes for regulated sectors, and fiber-based formats aligned with tighter recovery rules. That is why the Kenya containerboard market still offers room for focused entrants even though price competition remains strong in standard box production.

Kenya Containerboard Industry Leaders

East African Packaging Industries Ltd

Kibos Paper and Packaging Limited

Dodhia Packaging Kenya Ltd

East African Paper Mills Limited

Carton Manufacturers Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Kenya's Fresh Produce Exporters Association of Kenya submitted formal testimony to Parliament under Finance Bill 2026 deliberations, warning that the 25% excise duty on kraftliner risks ceding horticulture export market share to Ethiopia, Egypt, Morocco, and Colombia. FPEAK cited the horticulture sub-sector's contribution of 5% of GDP and approximately KES 150 billion, approximately USD 1.16 billion, in annual foreign exchange earnings, urging zero-rating of key packaging inputs to preserve competitiveness.

- March 2026: Shri Krishana Overseas PLC commenced commercial operations at its new Kisaju, Kajiado County corrugated packaging facility, expanding annual capacity from 3,000 to 22,000 tonnes. The expansion, partially financed through an SBM Bank debt facility of KES 271 million, approximately USD 2.1 million, targets horticulture export, floriculture, and FMCG packaging demand and represents one of the largest single-site capacity additions in Kenya's corrugated packaging segment in recent years.

- March 2026: The 10th Propak East Africa Expo convened at Sarit Expo Centre, Nairobi, drawing more than 5,000 participants from over 35 countries. Industry leaders issued a formal call for manufacturers to adopt modern packaging standards to safeguard global market competitiveness under the AfCFTA framework, with the Institute of Packaging Professionals Kenya CEO Joseph Nyongesa emphasizing the dual imperative of environmental compliance and trade-grade packaging performance.

Kenya Containerboard Market Report Scope

The Kenya Containerboard Market encompasses the production, distribution, and consumption of containerboard used in the manufacture of corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The market is driven by the increasing demand for sustainable, lightweight, and durable packaging solutions.

The Kenya Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the size outlook for Kenya containerboard demand through 2031?

The Kenya containerboard market was valued at USD 100.12 million in 2025, stood at USD 109.82 million in 2026, and is projected to reach USD 129.78 million by 2031 at a 3.40% CAGR.

What is driving corrugated box demand in Kenya the most?

Food processing, dairy, packaged beverages, horticulture exports, and e-commerce are the main demand drivers. Food and beverage alone held 28.67% of demand in 2025.

Why does Kenya still depend on imported kraftliner?

Export sectors such as flowers and avocados need moisture-resistant and high-burst cartons that local recycled grades do not consistently match. That keeps virgin kraftliner structurally important.

Which material segment leads demand in Kenya?

Recycled fibers led with 53.68% share in 2025 because domestic mills rely on OCC and bagasse-based inputs. Virgin fibers are smaller but are growing faster at a 4.41% CAGR.

Which product type is growing fastest in Kenya?

Flutings are expected to post the fastest growth at a 4.27% CAGR through 2031, supported by e-commerce packaging needs and more use of double-wall export boxes.

How are policy changes affecting packaging producers in Kenya?

The 25% excise duty on imported kraftliner has raised converter costs, while EPR and tighter plastic rules are improving the long-term position of fiber-based packaging in formal supply chains.

Page last updated on: