South America Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

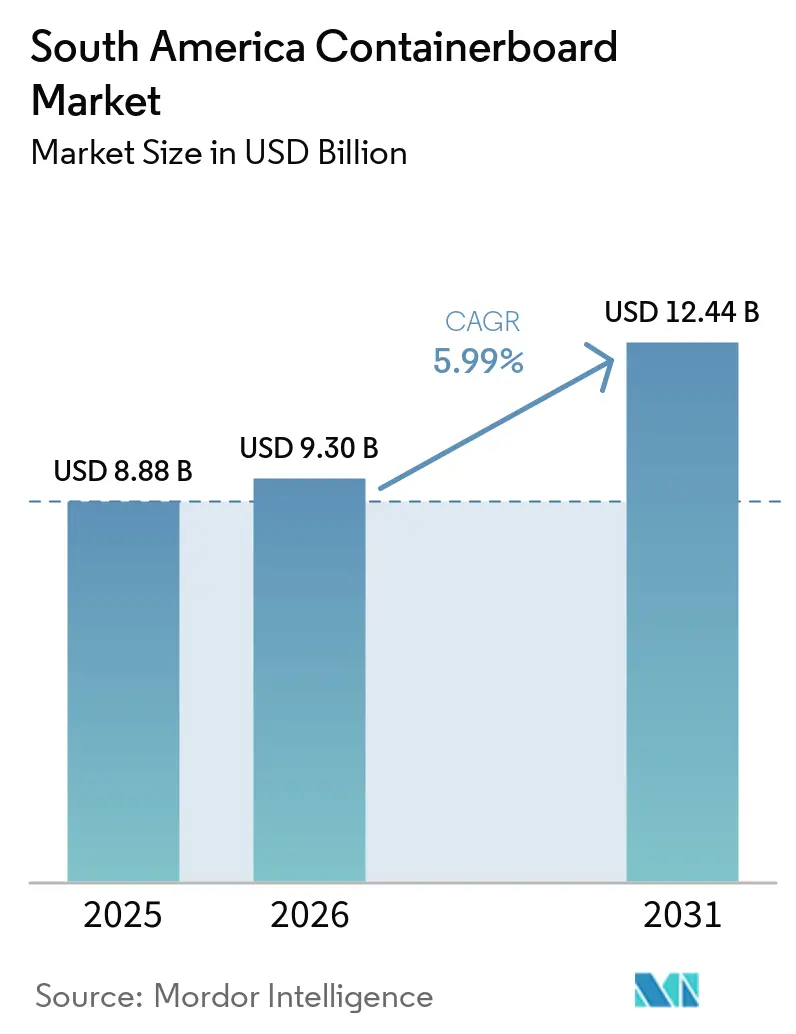

| Base Year Market Size (2025) | USD 8.88 Billion |

| Market Size (2026) | USD 9.30 Billion |

| Market Size (2031) | USD 12.44 Billion |

| Growth Rate (2026 - 2031) | 5.99% CAGR |

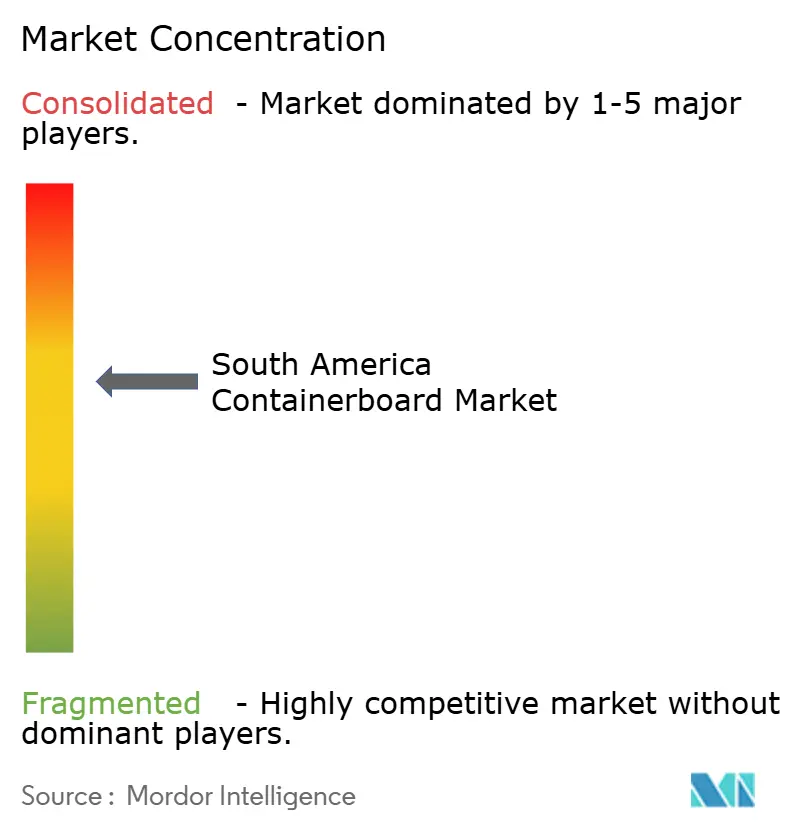

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Containerboard Market Analysis by Mordor Intelligence

The South America containerboard market was valued at USD 8.88 billion in 2025 and is projected to reach USD 12.44 billion by 2031, expanding at a CAGR of 5.99% during 2026-2031. Growth in the South America containerboard market is being supported by stronger agricultural export flows, rising substitution of plastic packaging with fiber-based formats, and large capacity programs from integrated pulp and paper producers. The region’s supply base remains structurally strong because major players control fiber sourcing, paper manufacturing, and downstream conversion, which gives them a better position to manage demand swings and product mix changes. Demand in the South America containerboard market is also broadening beyond food staples as urban retail, e-commerce fulfillment, and consumer goods packaging deepen across second-tier cities. At the same time, recovered fiber cost volatility and weak inland logistics keep margin pressure on recycled-fiber producers and slow the transmission of pricing adjustments across the region.

Key Report Takeaways

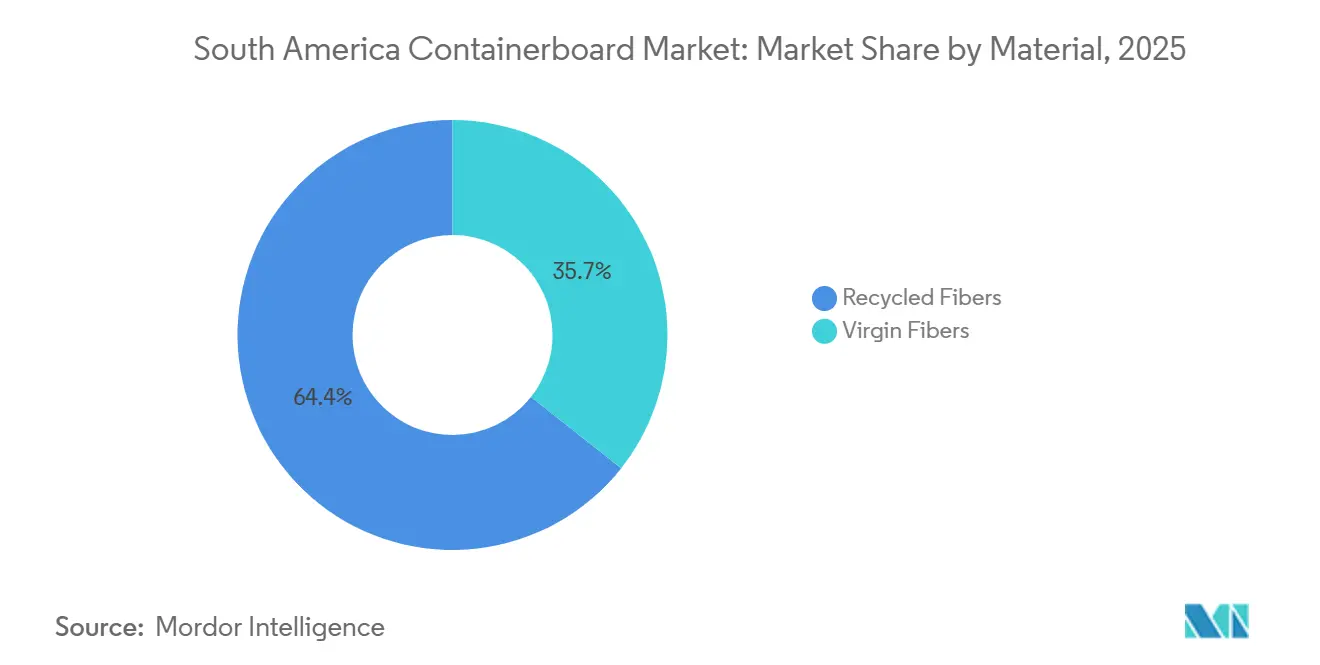

- By material, recycled fibers captured with 64.35% of the South America containerboard market share in 2025.

- By product type, the South America containerboard market size for flutings is projected to grow at a 6.83% CAGR to 2031.

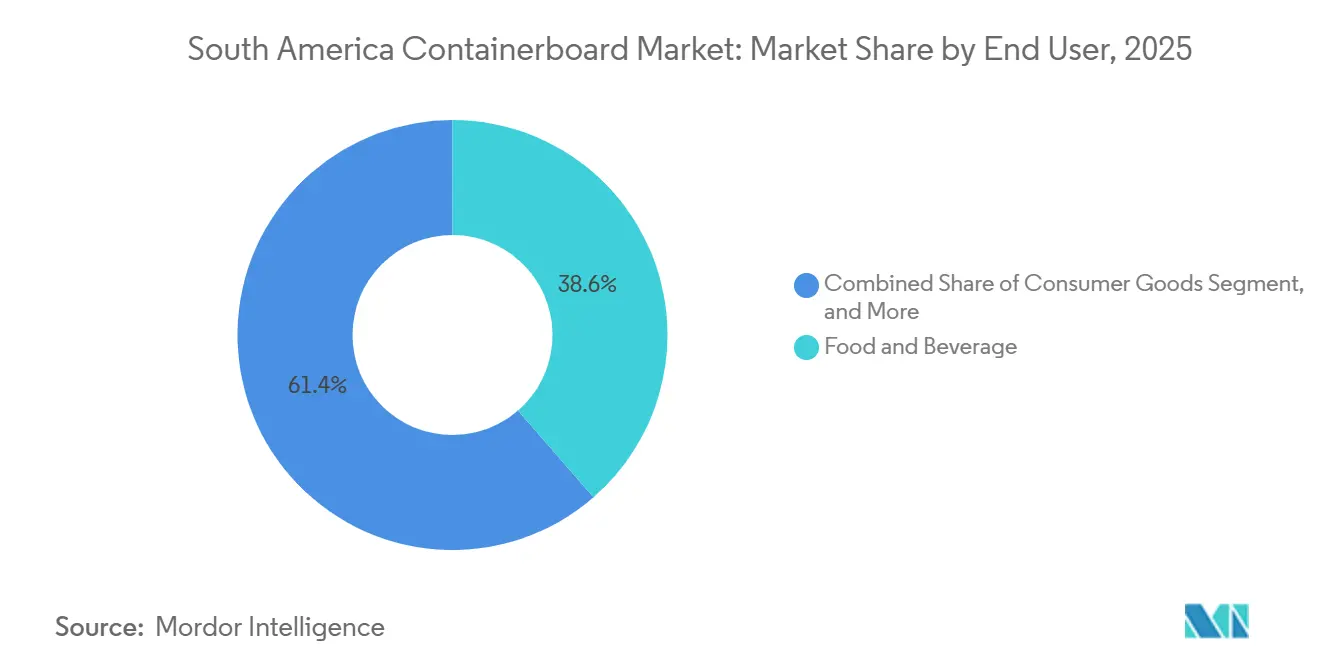

- By end user, the food and beverage industry accounted for 38.61% of the South America containerboard market share in 2025.

- By geography, the South America containerboard market in Peru is projected to grow at a 6.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce Boom Fueling Corrugated Packaging Demand | +1.8% | Brazil, Colombia, Chile, Argentina, and growing spill-over to Peru and Ecuador | Short term (≤ 2 years) |

| Surging Agricultural Exports Requiring Robust Boxes | +1.3% | Brazil, Chile, Peru, Argentina | Medium term (2-4 years) |

| Increasing Substitution of Plastic with Fiber-Based Packaging | +0.8% | Colombia, Brazil, Chile, nascent in Peru and Ecuador | Medium term (2-4 years) |

| Capacity Expansions by Domestic Pulp and Paper Majors | +0.6% | Brazil, Chile, Argentina | Long term (≥ 4 years) |

| Rising Government Tariffs on Imported Old Corrugated Containers | +0.4% | Brazil, Argentina, selective impact in Colombia and Chile | Medium term (2-4 years) |

| Digital Print Adoption Enabling High-Margin Short Runs | +0.2% | Brazil, Colombia, Chile | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Boom Fueling Corrugated Packaging Demand

The South America containerboard market is seeing e-commerce compress the old gap between online retail growth and packaging conversion investment. Brazil opened 2026 with record corrugated board shipments of 343,000 tonnes in January, up 2.3% year over year, which showed that box demand remained firm at the start of the year. Animal protein and fast-moving consumer goods accounted for 30% of total corrugated demand in Brazil, keeping order flow active for producers tied to retail and fulfillment channels. Returns logistics is also changing design priorities, because shippers now want lighter boxes while still upgrading secondary packaging quality for repeat handling. Producers that invested in lightweight fluting and printable liner surfaces have been better placed to capture short-run, higher-margin work that standard kraft-focused mills struggle to match on turnaround time. Fastmarkets had already projected 5% full-year growth in corrugated box shipments in Brazil for 2024, so the South America containerboard market entered 2026 on top of a firm operating base rather than a weak rebound cycle.

Surging Agricultural Exports Requiring Robust Boxes

The South America containerboard market is benefiting from export agriculture, as these supply chains require stronger, moisture-resistant, and cold-chain-ready corrugated formats. Brazil’s agribusiness exports reached a record USD 169.2 billion in 2025, and beef export value rose 39.9% while volume increased 20.4%, which reinforced demand for heavyweight corrugated boxes in long-distance protein trade. Those trade corridors to China, the European Union, and the Middle East stretch transport distance and handling intensity, which raises packaging requirements per shipment. Peru set a historic agricultural export record in 2025, shipping 540 products to 115 markets, including 767,230 tonnes of avocados and 343,537 tonnes of blueberries, keeping fresh-produce box demand on an upward trajectory. Chile also posted record fresh fruit and vegetable export revenue in 2025, and packaging is increasingly being used as a competitive tool in multimodal cold-chain movement to North American and European retailers. This is why the South America containerboard market is drawing support from agriculture in a steadier way than domestic fast-moving consumer goods demand, because export programs are tied to long-running trade flows and certification requirements.

Increasing Substitution of Plastic with Fiber-Based Packaging

The South America containerboard market is also being pushed forward by regulations that make fiber-based packaging easier to use than many plastic formats. Colombia’s Law 2232 took effect in July 2024 and restricted single-use plastic items across foodservice, retail, and public consumption settings, with a compliance path that extends to 2030. Brazil added another strong signal when Federal Decree No. 12,688, published in October 2025, created a mandatory reverse-logistics system for plastic packaging with a 32% recovery target for 2026 and a 22% recycled-content requirement, while mixed packaging containing paper or cardboard was explicitly exempted. A peer-reviewed review comparing the European PPWR and Brazil’s Decree No. 12,688/2025 identified FSC chain-of-custody certified paperboard and corrugated board as lower-risk compliance choices when designed for recycling.[1]Food Packaging Forum, “2025 Regulatory and Waste Management Updates from South America,” Food Packaging Forum, foodpackagingforum.org Regional policy momentum also extends across Chile and Ecuador, while MERCOSUR Resolution No. 02/25 updated technical rules for cellulosic food-contact materials, providing paper-based packaging with a clearer regulatory path.

Capacity Expansions by Domestic Pulp and Paper Majors

The South America containerboard market is being reshaped by a scale of capacity investment that few other regions are matching. Arauco’s Sucuriú project in Mato Grosso do Sul is under construction with an investment of at least USD 4.6 billion, a target of 3.5 million tonnes per year of bleached hardwood kraft pulp, and a startup expected in the second half of 2027. CMPC’s Natureza project in Rio Grande do Sul is targeting 2.5 million tonnes per year with an investment of USD 4.5-4.6 billion and startup in the second half of 2029. Smurfit Westrock approved a USD 150 million investment plan for Brazil in May 2025, including USD 31 million for the Três Barras kraftliner mill, where capacity is expected to rise 6%-10% by the end of 2027. Klabin is projecting an additional 80,000 tonnes of productive capacity in 2026 from efficiency gains and the ongoing ramp-up of its Ortigueira paper machines, at a cost of BRL 3.3 billion (USD 617 million). These projects support the South America containerboard market because the region remains in the lowest-cost quartile of global pulp production, with an estimated fiber cost advantage of USD 100-150 per tonne over other producing regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Recovered Paper Prices Pressuring Margins | -1.0% | Brazil, Argentina, Colombia, moderate in Chile and Peru | Short term (≤ 2 years) |

| Limited Intermodal Logistics Infrastructure | -0.7% | Brazil, Argentina, Colombia, localized in Peru and Chile | Long term (≥ 4 years) |

| Slowdown in Consumer Spending Amid Currency Depreciation | -0.5% | Argentina, Brazil, moderate in Colombia and Peru | Short term (≤ 2 years) |

| Water-Use Restrictions Affecting Pulp Mills | -0.3% | Chile, southern Brazil, emerging in Colombia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Recovered Paper Prices Pressuring Margins

Recovered paper volatility remains one of the clearest cost risks in the South America containerboard market, especially for producers that rely on recycled fiber and cannot switch their mix toward virgin inputs. OCC imports resumed across the region in the third quarter of 2024 as converters secured supply for fruit export seasons, and price indices rose sharply as local currencies weakened against the USD. Domestic collection rates remain structurally low across much of the region, so local recovered fiber supply does not respond quickly when converter demand rises. Brazil’s flexible plastic packaging sector was operating with only 5% recycled content, against a 2026 target of 22%, indicating broader weaknesses in collection and recovery systems and leaving less clean material available for the paper circuit. That leaves recycled-fiber producers exposed to a two-sided squeeze, because imported OCC becomes more expensive while domestic recovery quality also weakens. In the South America containerboard market, this cost pressure matters most for testliner and recycled-fluting suppliers, who are being asked by box makers to hold pricing steady while fiber inputs remain unstable.

Limited Intermodal Logistics Infrastructure

Limited transport integration remains a structural barrier in the South America containerboard market because low fiber costs do not automatically translate into low delivered paper costs. A June 2025 study by Infra S.A., ONTL, and Fiesp found that Brazil’s freight matrix was 68.2% highway-dependent, while rail accounted for only 15.5% of freight movement. The Port of Santos recorded average container dwell times above 40 hours in 2025, and 55% of vessels at major Brazilian ports faced delays or schedule changes in March 2025. A peer-reviewed study on Brazil’s railway system found that concession renewals kept the strongest rail access focused on minerals and agricultural bulk, while general cargo retained only a marginal and unreliable position. The World Bank Logistics Performance Index ranked Brazil 51, Colombia 66, and Argentina 73, indicating a regional logistics gap relative to higher-performing trade systems. Until inland connectivity improves, the South America containerboard market will continue to favor coastal mills and rail-linked assets over inland producers, which face slower, more expensive distribution.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fibers Lead While Virgin Grades Accelerate

Recycled fibers held 64.35% of the South America containerboard market share in 2025, supported by integrated recovery networks and the cost efficiency of testliner and recycled-fiber fluting in domestic conversion. The South America containerboard market has long depended on recovered paper from industrial and commercial generators, especially in the Greater São Paulo and Curitiba belts, where integrated circuits have shaped procurement and production routines. MERCOSUR Resolution No. 02/25 updated technical requirements for cellulosic food-contact materials in 2025 and called for recycled-fiber articles to keep diisopropylnaphthalene, or DIPN, as low as technically feasible, which added a stronger food-safety dimension to sourcing decisions. That change is prompting some food-contact packaging buyers to scrutinize recycled content, particularly as export certifications and product-contact rules tighten.

Virgin fibers remain the smaller material category, but they are the fastest-growing segment with a 6.61% CAGR through 2031 in the South America containerboard market. Within the South America containerboard industry, this growth is tied to rising demand for premium kraft-grade liners for agricultural export packaging and boxes that must withstand moisture and stacking stress. Klabin’s Ortigueira unit produces Eukaliner and has installed capacity above 900,000 tonnes per year across Paper Machines 27 and 28, giving it a strong position in higher-performance liner grades.[2]Klabin S.A., “Klabin Strengthens Its Containerboard Paper Production Chain with Robust Presence in Asia and Europe,” Klabin, klabin.com.br Material choice in the South America containerboard industry is therefore moving away from a simple cost debate and toward a mix of compliance, strength, and surface quality requirements that favor premium virgin grades in selected end uses.

By Product Type: Kraftliners Dominate as Fluting Records Fastest Expansion

Kraftliners accounted for 48.63% share of the South America containerboard market size in 2025, reflecting Brazil’s strong export-grade production base and its ability to serve both domestic converters and external markets. Brazilian kraftliner exports rose 16% in the first 9 months of 2024 to around 322,000 tonnes, and Argentina accounted for 28% of that total, confirming the regional pull for Brazilian liner grades. Testliners held the next-largest position in the product mix because recycled-fiber circuits remain important for domestic fast-moving consumer goods and retail packaging. Fluting is the fastest-growing product type with a 6.83% CAGR through 2031, as converters respond to demand for lighter boxes in e-commerce, food retail, and retail-ready formats.

This part of the South America containerboard market is shifting toward designs where compression performance and printability matter more than board caliper alone. Smurfit Westrock’s wider system approach to liner and medium supply shows how leading producers are increasingly managing these grades together rather than as separate commodities. Klabin’s Paper Machine 28 at Ortigueira was designed as a hybrid machine capable of producing kraftliner and paperboard, providing grade-switching flexibility as demand patterns change. That flexibility is becoming more valuable in the South America containerboard market because thinner, higher-performance corrugated formats are gaining share faster than traditional heavier grades in some retail and fulfillment applications.

By End User: Food And Beverage Leads While Consumer Goods Rises Fastest

Food and beverage accounted for 38.61% of the South America containerboard market in 2025, driven by the region’s export position in protein, fresh produce, and processed foods. In Brazil, animal protein alone accounted for nearly 26% of corrugated box demand, with beef and pork at 21% and poultry at 4%, making food logistics one of the most direct links between trade flows and packaging demand. This gives the South America containerboard market a more defensive demand layer, as export-oriented food shipments can remain firm even when domestic consumer confidence is weaker. Industrial end use remains a stable contributor to chemicals, capital goods, and industrial components, though it lacks the same growth drivers as consumer-facing packaging.

Consumer goods are the fastest-growing end-user category with a 6.88% CAGR through 2031, helped by e-commerce expansion and the need for secondary and tertiary packaging that works in automated fulfillment settings. A GIZ study on retail packaging in Brazil, Colombia, and Mexico highlighted a shift toward paper-based clamshells and structural corrugated formats as extended producer responsibility rules tighten the use of plastic packaging in consumer goods chains. Producers that can offer lightweight, printable, and recyclable corrugated solutions are better placed to capture the higher-value mix developing in this part of the South America containerboard market. That is why end-user demand is gradually broadening from food-led volume toward a more balanced mix that includes retail, personal goods, and other branded packaged products.

Geography Analysis

Brazil held 58.17% of the South America containerboard market share in 2025, supported by planted forest assets, integrated paper machines, and a deep corrugated conversion base. Brazilian agribusiness export revenue reached a record USD 38.1 billion in the first quarter of 2026, driven by soybeans, beef, coffee, and sugar.[3]Paulo Santos, “Brazil’s Agribusiness Exports Hit Record in Q1,” Valor International, valorinternacional.globo.com This export profile gives the South America containerboard market in Brazil a recurring source of corrugated transport demand that helps offset softness in domestic consumption. Brazil’s Kraftliner mills operated at 94% in 2024, which showed that near-term volume headroom was already tight before new projects come on stream. The country’s export reach is also expanding through Argentina, Italy, and Asian markets, while northern port corridors are becoming more relevant for mills seeking to reduce inland transport distances.

Peru is the fastest-growing geography, and this part of the South America containerboard market size is projected to expand at a 6.74% CAGR through 2031. Peru shipped 540 agricultural products to 115 international markets in 2025, including 767,230 tonnes of avocados and 343,537 tonnes of blueberries, creating direct demand for ANDINA's export-ready corrugated boxes. The country also secured 23 new phytosanitary access agreements in 2025, while Colombia is benefiting from rising urban consumption and broader cold-chain distribution, which support food delivery and packaged retail. Chile’s record 2025 exports of fresh fruit and vegetables continued to support agricultural corrugated demand, with packaging designs increasingly focused on biodegradable materials and better multimodal cold-chain performance.

Argentina absorbed 28% of Brazil’s external kraftliner volumes in the first 9 months of 2024, which shows how strongly its corrugating sector depends on imported liner supply. Argentina’s containerized exports rose 11.3% in 2025, helped in part by policy changes around grains, which supported additional demand for agricultural corrugated packaging. The rest of South America, including Ecuador, Bolivia, Uruguay, and Paraguay, remains a smaller but emerging consumption base, and Smurfit Westrock’s acquisition of Cartomanabí in Ecuador shows that leading producers see the Andean corridor as the next area for volume expansion. Argentina’s currency volatility continues to weigh on packaging investment, while Uruguay and Paraguay provide smaller but steadier demand tied to Mercosur agricultural flows.

Competitive Landscape

The South America containerboard market is moderately concentrated, with a small group of vertically integrated producers controlling fiber, paper, and corrugated conversion across key countries. This structure gives leading companies stronger pricing influence and better cost control than smaller stand-alone converters. Smurfit Westrock reported a 20.2% adjusted EBITDA margin for South America and broader regional operations in the first quarter of 2026, which shows the earnings benefit of scale and integration in the current operating environment. The South America containerboard market is also showing a clear strategic pattern, with producers combining fiber-cost discipline, capacity management, and selective expansion into underpenetrated geographies. That pattern matters because market leaders are no longer competing only on tonnage; they are also competing on machine flexibility, logistics reach, and their ability to serve higher-specification corrugated applications.

Smurfit Westrock completed the acquisition of Cartomanabí in Ecuador in March 2026, adding more than 50,000 tonnes of annual corrugated capacity tied to agriculture, protein, fast-moving consumer goods, and industrial customers. In May 2025, the company also approved a USD 150 million investment plan for Brazil, including USD 31 million for the Três Barras kraftliner mill and funding for artificial intelligence tools to improve forest productivity and reduce downtime. Suzano’s Ribas do Rio Pardo pulp mill reached nominal capacity of 2.55 million metric tonnes per year within 1 year of ramp-up, which set a new operating benchmark for large integrated fiber projects in the region.[4]ANDRITZ, “Suzano’s Ribas do Rio Pardo Mill Reaches Nominal Capacity in Record Time with ANDRITZ Technologies,” ANDRITZ, andritz.com Klabin said it expects another 80,000 tonnes of productive capacity in 2026 through efficiency gains and continued ramp-up at Ortigueira, which reflects a disciplined approach to expanding output without overextending leverage.

White-space opportunities in the South America containerboard market remain strongest in digital-print-enabled short runs, lightweight fluting for automated fulfillment centers, and moisture-resistant export boxes for Andean produce corridors. Smaller converters can still compete in these niches through faster specification cycles and lower minimum orders, especially in consumer goods packaging. Even so, technology adoption is widening the gap, because leading producers are embedding artificial intelligence and predictive maintenance into capital allocation and operational planning. As new greenfield pulp projects from Arauco and CMPC move forward, the South America containerboard market is likely to see cost advantages shift toward players that can combine low-cost eucalyptus fiber, modern assets, and better inland logistics acces.

South America Containerboard Industry Leaders

Smurfit Westrock plc

International Paper Company

Stora Enso Oyj

Cascades Inc.

Mondi plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Smurfit Westrock reported Q1 2026 South America and broader regional net sales of USD 540 million with an adjusted EBITDA margin of 20.2%, confirming regional outperformance despite currency headwinds. The company reaffirmed its full-year 2026 adjusted EBITDA guidance of USD 5.0-5.3 billion and raised containerboard prices by a net USD 20 per tonne in Q1, with an additional USD 30 per tonne implemented in April.

- March 2026: Smurfit Westrock completed the acquisition of Cartomanabí, a corrugated packaging company in Montecristi, Ecuador, with annual production capacity exceeding 50,000 tonnes serving agricultural, protein, fast-moving consumer goods, and industrial sectors, this was the first acquisition completed by the combined Smurfit Westrock entity and reinforces its position as the leading pan-regional corrugated supplier in South America.

- March 2026: Valor International reported that new South American pulp capacity projects, led by Arauco's USD 4.6 billion Sucuriú mill, 3.5 million tonnes per year, Mato Grosso do Sul, and CMPC's USD 4.5 billion Natureza mill, 2.5 million tonnes per year,

- February 2026: Klabin's chief executive confirmed expectations of increased paper production in 2026, projecting an additional 80,000 tonnes of productive capacity from operational efficiency gains and ramp-up of the Ortigueira paper machines, while targeting leverage reduction to below 3.0 times net debt to EBITDA.

South America Containerboard Market Report Scope

The scope of the report covers the analysis of the South America containerboard market, including production, consumption, and trade of containerboard materials. Containerboard is the paperboard used primarily for the manufacture of corrugated boxes and packaging materials. The study examines market trends, key drivers, challenges, and opportunities within the region, providing insights into the market dynamics during the forecast period.

The South America Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), End User (Food and Beverage, Consumer Goods, Industrial, and More), and Geography (Brazil, Argentina, Colombia, Chile, Peru, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End Users |

| Brazil |

| Argentina |

| Colombia |

| Chile |

| Peru |

| Rest of South America |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End User | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End Users | |

| By Geography | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

What is the size outlook for the South America containerboard market?

The South America containerboard market was valued at USD 8.88 billion in 2025 and is projected to reach USD 12.44 billion by 2031 at a CAGR of 5.99% during 2026-2031.

Which material segment leads demand across the region?

Recycled fibers led demand with a 64.35% share in 2025, reflecting the region’s long-standing dependence on recovered fiber in integrated mill systems.

What product category is growing the fastest?

Fluting is the fastest-growing product type and is projected to expand at a 6.83% CAGR through 2031, supported by lighter corrugated formats used in e-commerce and food retail.

Why does Brazil remain the key country in this space?

Brazil held 58.17% of regional demand in 2025 because it combines planted forest assets, integrated mills, a large corrugated conversion base, and strong agricultural export flows.

What are the main risks affecting producer margins?

The biggest risks are volatile recovered paper prices and weak intermodal logistics, both of which raise delivered costs and make pricing adjustments harder to pass through.

Which end users are shaping future demand most strongly?

Food and beverage remains the largest end user with a 38.61% share in 2025, while consumer goods is growing fastest at a 6.88% CAGR as e-commerce and retail packaging needs expand.

Page last updated on: