North America Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

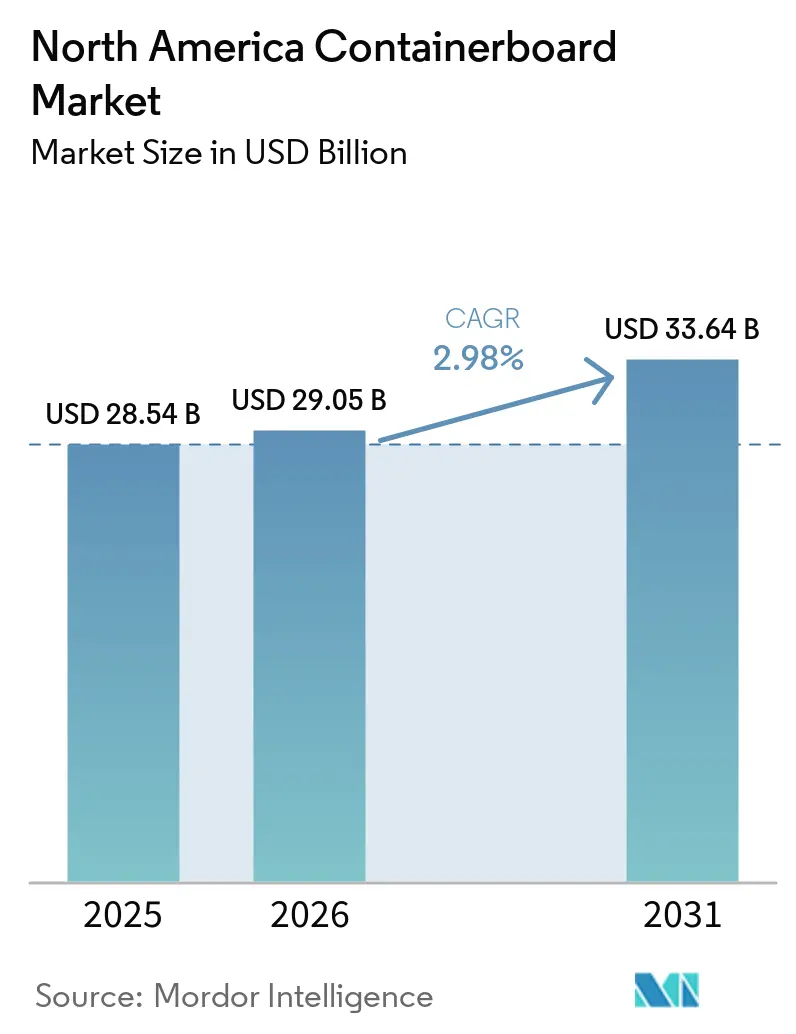

| Base Year Market Size (2025) | USD 28.54 Billion |

| Market Size (2026) | USD 29.05 Billion |

| Market Size (2031) | USD 33.64 Billion |

| Growth Rate (2026 - 2031) | 2.98% CAGR |

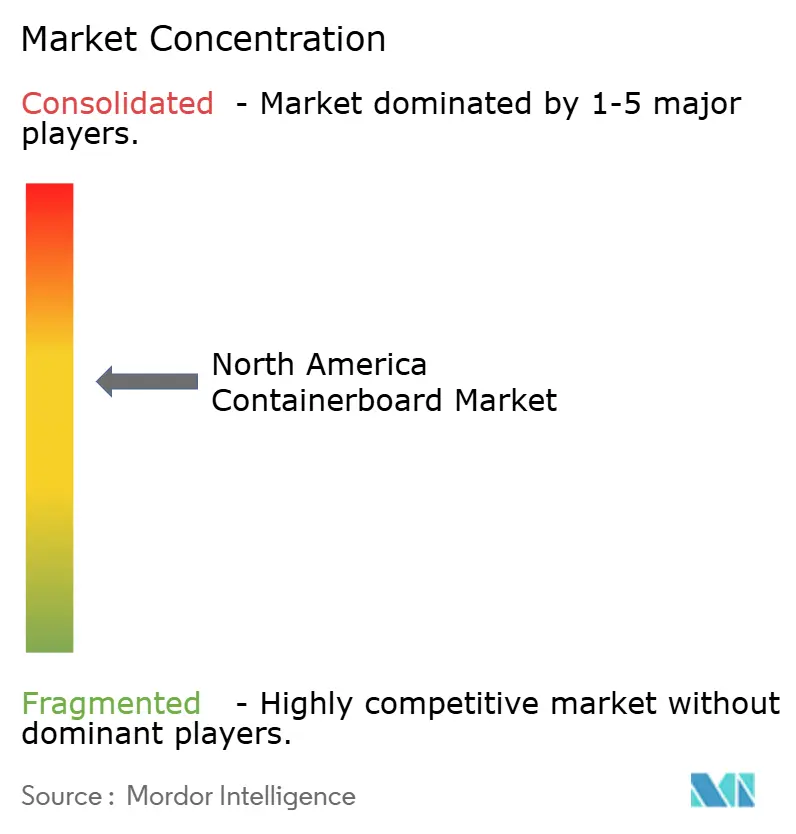

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Containerboard Market Analysis by Mordor Intelligence

The North America containerboard market size is projected to expand from USD 28.54 billion in 2025 and USD 29.05 billion in 2026 to USD 33.64 billion by 2031, registering a CAGR of 2.98% between 2026 and 2031. The North America containerboard market entered this forecast period after a clear supply reset, as containerboard production fell 8% year over year in Q1 2026 and several major producers had already removed high-cost capacity during 2025. Demand in the North America containerboard market continues to be supported by e-commerce shipping volumes, broader corrugated customer additions, and steady activity across distribution networks, even while consumer spending remains selective. Sustainability standards are also strengthening the North America containerboard market, as recycled fiber content has become more embedded in mainstream specifications and plastic reduction rules are pushing more secondary packaging toward fiber-based formats. Competition in the North America containerboard market is shaped by large integrated producers that are combining portfolio rationalization with targeted mill upgrades, recycled-grade expansion, and customer service investments to protect margins and capture higher-value demand. Near-term growth remains measured because operating economics still face pressure from recovered paper swings, uneven energy costs, and a demand backdrop that is improving but not yet broad based across every end market.

Key Report Takeaways

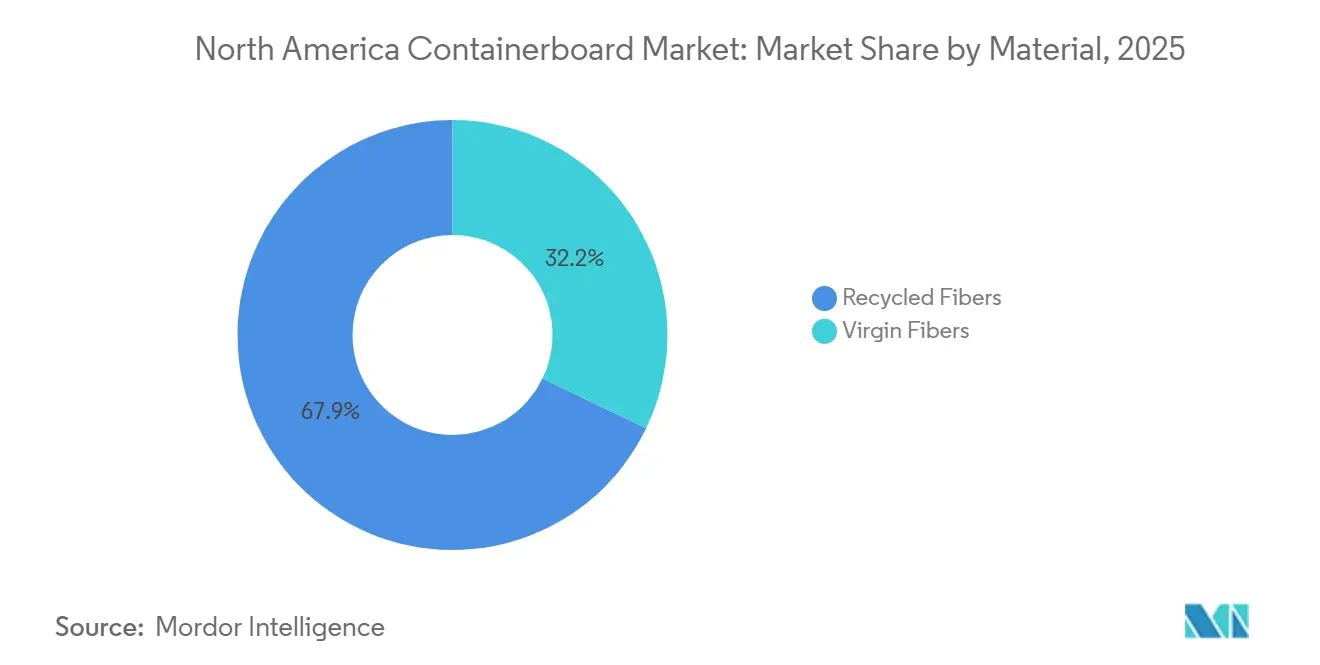

- By material, virgin fibers captured with 32.15% of the North America containerboard market share in 2025.

- By product type, the North America containerboard market size for flutings is projected to grow at a 4.17% CAGR to 2031.

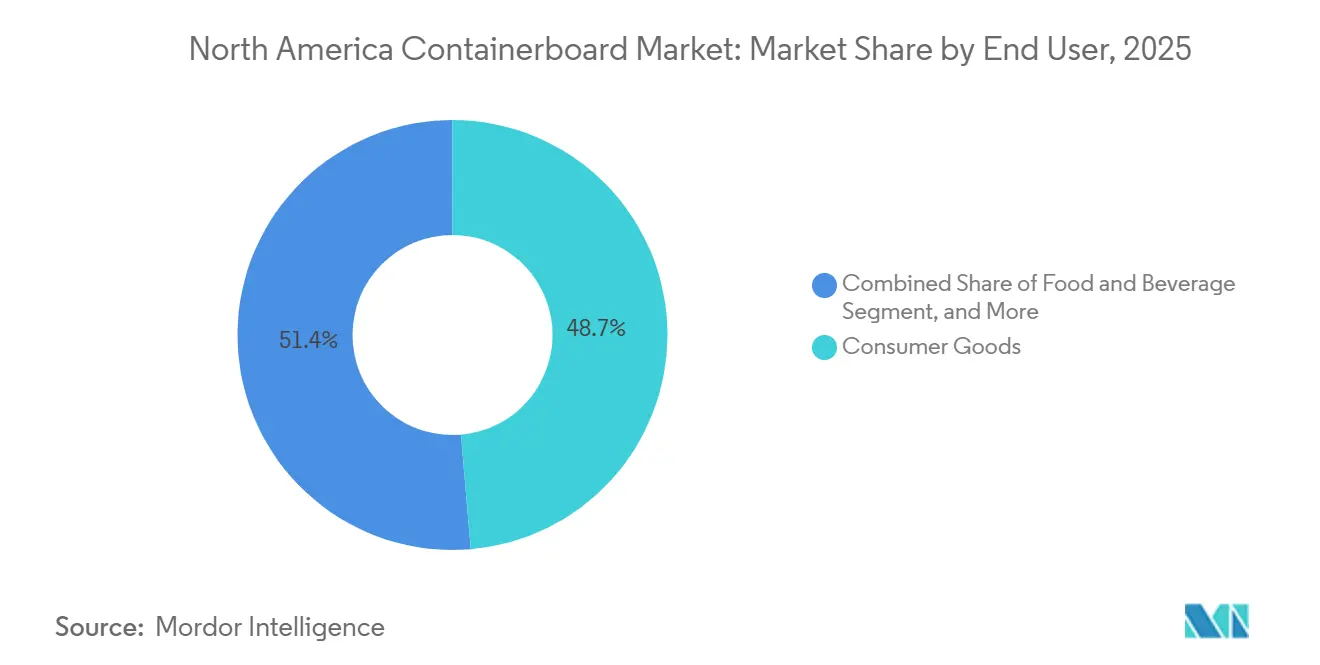

- By end user, consumer goods captured with 48.65% of the North America containerboard market share in 2025.

- By geography, the North America containerboard market size for Mexico is projected to grow at a 4.96% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth In E-Commerce Packaging Demand | +0.8% | Global, concentrated in the US and Mexico e-commerce distribution corridors | Short term (≤ 2 years) |

| Increasing Demand for Sustainable Packaging Solutions | +0.6% | Global, strongest regulatory pull in western United States, Canada, and EU-influenced supply chains | Medium term (2-4 years) |

| Surge In Food and Beverage Takeaway and Delivery Services | +0.5% | US and Canada urban centers, growing in Mexico Tier-1 cities | Short term (≤ 2 years) |

| Replacement of Plastic Packaging Due to Regulatory Bans | +0.4% | National, early gains concentrated in California, Oregon, Washington, and Québec | Medium term (2-4 years) |

| Advancements In High-Performance Lightweight Containerboard Grades | +0.3% | Global, principal manufacturing benefit across US integrated mills | Long term (≥ 4 years) |

| Strategic Capacity Expansions Near Regional Distribution Hubs | +0.2% | United States South and Southeast, Mexico nearshoring clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth In E-Commerce Packaging Demand

E-commerce remains the most durable volume driver for the North America containerboard market because direct shipment models require corrugated protection across fulfillment, sorting, and last-mile delivery. Packaging Corporation of America reported that corrugated shipments per shipping day were up 4.5% year over year in January 2026 and up 3% through mid-February, indicating that box demand was recovering faster than many broad retail indicators. This demand carries a built-in packaging intensity advantage because goods shipped to homes usually need more fiber per order than goods moved through store shelves. Smurfit Westrock said its addition of more than 600 new corrugated customers in Q1 2026 was driven by e-commerce and value-added formats, indicating that the North America containerboard market is benefiting from mix improvement as much as from simple shipment growth.[1]Smurfit Westrock, “Smurfit Westrock Reports First Quarter 2026 Results,” smurfitwestrock.com The effect is stronger in grocery and fresh food delivery, where producers need thicker, more moisture-resistant board formats to protect temperature-sensitive, heavier products during transport.

Increasing Demand for Sustainable Packaging Solutions

Sustainability has become a basic buying requirement in the North America containerboard market rather than a premium feature that only a small set of customers seeks out. The Corrugated Packaging Alliance and Fiber Box Association reported in 2025 that corrugated containers outperformed reusable plastic containers across several environmental indicators under baseline US conditions, providing brand owners with a clearer basis for switching secondary packaging formats. The same assessment period showed that the average recycled fiber content in US containerboard reached 31.8%, indicating that recycled content is now built into regular-grade specifications rather than sitting in a narrow specialty tier. This matters commercially because mills that can blend recycled content into standard linerboard and medium grades can meet procurement targets across a wider customer base without expanding product complexity. As compliance rules tighten across states and provinces, the North America containerboard market is likely to reward producers that combine recycled furnish access, converting reach, and stable performance across mainstream packaging applications.

Surge In Food and Beverage Takeaway and Delivery Services

Food delivery and takeaway activity has created a steady demand pocket within the North America containerboard market that does not move in perfect step with wider consumer goods spending. Meal kits, grocery delivery, and restaurant takeaway all depend on corrugated secondary packaging that can handle stacking pressure, moisture exposure, and higher unit handling frequency. Packaging Corporation of America said food and beverage delivery volumes were among the end uses showing earlier demand improvement in Q1 2026, which confirms that this channel is helping support orders during a mixed recovery period. The regional effect is important because Mexico continues to expand its e-commerce and food distribution infrastructure while also producing 4 million tons of cardboard annually and still importing a substantial share of containerboard from the United States. That cross-border packaging loop means added takeaway and grocery demand in Mexican cities can also lift mill utilization and converting flows elsewhere in the North America containerboard market.

Replacement of Plastic Packaging Due to Regulatory Bans

Plastic reduction rules are creating a direct substitution path into the North America containerboard market, especially in states and provinces that are moving faster on producer responsibility rules. California’s SB 54 requires a 25% reduction in covered plastic packaging by 2032, and the state projected USD 241 million of incremental output growth for converted paper product manufacturing in California during 2026 as packaging formats shift. Washington’s producer responsibility law also moved forward material decisions by requiring packaging producers to register with a Producer Responsibility Organization by July 2026. These rules favor lighter, more recyclable fiber-based formats, supporting innovation in linerboard and medium grades that can replace plastic without imposing major compliance costs on brand owners. The result is that larger integrated suppliers in the North America containerboard market are positioned to win broader conversion programs rather than isolated stock-keeping unit changes, which improves order visibility and downstream plant utilization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility In Recovered Paper Prices | -0.8% | Global, most acute in the US recycled-board mills dependent on OCC furnish | Short term (≤ 2 years) |

| Energy Cost Fluctuations Impacting Production Economics | -0.5% | North America's core, most severe in Canadian provinces and the western United States, with elevated industrial electricity rates | Medium term (2-4 years) |

| Limited Railcar Availability Disrupting Intra-Regional Supply Chains | -0.3% | National, paper and forest product corridors in eastern and midwestern United States | Medium term (2-4 years) |

| Growing Competition From Molded Fiber Packaging In Produce Sector | -0.2% | Global, concentrated in North American fresh produce and egg packaging applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility In Recovered Paper Prices

Recovered paper pricing remains the most visible input risk for recycled fiber producers in the North America containerboard market because old corrugated containers are the core furnish for many board grades. The market is exposed to abrupt price movement when supply from box recovery does not keep up with mill demand, since furnish availability depends on collection behavior and the pace at which used boxes return to the recycling stream. The Recycling Partnership estimated US residential curbside recovery rates for all recyclable materials at 20% in 2024, indicating a significant structural recovery gap that could tighten feedstock availability when demand improves. This gap matters because capacity management alone cannot solve furnish stress if recovered volumes remain inconsistent across cities and states. As a result, the North America containerboard market is likely to continue to see margin pressure and uneven pricing discipline until collection systems and recovery quality improve materially.

Energy Cost Fluctuations Impacting Production Economics

Energy costs remain a major operating restraint for the North America containerboard market because paper drying and mill operations are power-intensive, and asset lives are long. Packaging Corporation of America said it permanently retired the No. 2 Kraft machine and Kraft pulping operations at Wallula after Washington state electricity rates rose 89% over 2 years, underscoring how quickly cost shifts can force structural footprint decisions. The same company also announced a USD 250 million gas turbine program for its Riverville, Jackson, and DeRidder mills, reflecting a strategic move toward greater energy independence in areas where economics are more favorable. Academic research published in 2025 found that drying accounts for 57% of total energy use in the United States' pulp and paper sector, which helps explain why savings are hard to capture quickly with existing mill infrastructure. This leaves producers in the North America containerboard market with a difficult balance between keeping legacy assets running, redirecting output to lower-cost facilities, and funding long-lead-time energy upgrades that only pay back over multiple years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Virgin Fiber’s Premium Positioning Sustains Its Lead

Virgin fibers held 32.15% of the North America containerboard market share in 2025 and are projected to grow at a 3.62% CAGR through 2031, keeping this grade in both the leading and fastest-growing positions within the material split. This lead reflects the stronger performance of kraft pulp-based linerboard, with higher burst strength, better print quality, and applications where consistency matters more than simple cost reduction. The North America containerboard industry still relies on virgin fiber, where export packaging, food contact needs, and heavier-duty transport formats leave limited room for substitution. That demand profile gives virgin grades a firmer pricing position, even as customers continue to expand recycled-content targets across broader packaging portfolios.

At the same time, the material picture is becoming more balanced as leading producers expand their recycled-grade capabilities alongside their virgin fiber assets. International Paper’s April 2026 agreement to acquire NORPAC’s Longview mill, which produces 1 million tons of containerboard annually and focuses on lightweight, high-performance recycled grades, shows that even large virgin fiber players are repositioning to meet recycled demand on the West Coast.[2]International Paper, “International Paper to Acquire North Pacific Paper Company,” prnewswire.com The 31.8% average recycled fiber content already documented in US containerboard indicates that recycled furnish is now central to mainstream product design, not an edge case. Over time, that means the gap between virgin and recycled grades in the North America containerboard market may narrow at lower basis weights, while premium heavy duty applications continue to defend a clearer virgin fiber advantage.

By Product Type: Testliners Gain Ground Against Legacy Kraftliner Specifications

Flutings held a 29.63% share in 2025, while testliners are projected to expand at a 4.17% CAGR within the North America containerboard market size through 2031. Flutings retained the largest share because the corrugating medium is essential in nearly every corrugated board construction, so its demand closely follows overall box production. Testliners are growing faster because they give converters a practical way to reduce weight and costs in e-commerce secondary packaging without sacrificing functional protection in routine shipping conditions. Kraftliners still hold a solid place in export, industrial, and regulated applications where mechanical performance limits substitution.

This shift is being reinforced by packaging design tools that help shippers use less board per shipment while preserving product protection. Smurfit Westrock said it demonstrated AI-enabled packaging design tools to more than 200 customers during its Q1 2026 European Innovation Event and continues to use its customer experience center network to support design optimization. The commercial effect is that lighter recycled liner grades can capture more new programs when customers focus on freight, material efficiency, and environmental targets simultaneously. Within the North America containerboard industry, this supports a gradual move away from legacy-grade specifications toward more engineered solutions that better match packaging performance to actual shipment needs.

By End User: Consumer Goods Anchor Demand While Industrial Uses Add Stability

Consumer goods accounted for 48.65% of the North America containerboard market value in 2025, and consumer goods are also projected to grow at the fastest 4.45% CAGR through 2031. This makes consumer goods the clearest demand anchor in the North America containerboard market because it covers electronics, household products, personal care, apparel, and general merchandise that already move heavily through corrugated channels. E-commerce adds to this strength because higher online order penetration tends to deepen box usage inside a segment that already uses fiber packaging at scale. The combination of breadth and shipping intensity gives this segment a stronger floor than narrower vertical categories.

Food and beverage remains an important second-tier segment because takeaway, direct-to-consumer delivery, and moisture-sensitive transport needs continue to support demand for protective corrugated formats. Industrial demand also matters because nearshoring and manufacturing investment can lift packaging needs for components, chemicals, and intermediate goods even when household spending is uneven. Packaging Corporation of America said reindustrialization policy is positive for corrugated products demand in manufacturing corridors, which supports the case for steadier industrial box requirements over the medium term. The remaining end uses, including agriculture and specialty applications, give the North America containerboard market additional room in export linked corridors where produce handling and cold chain packaging need durable corrugated trays and boxes.

Geography Analysis

The United States remained the leading production and consumption center in the North America containerboard market in 2025 because it combines the region’s deepest e-commerce network, the largest corrugated converting base, and the broadest consumer goods manufacturing footprint. AF and PA reported that North American containerboard production fell 8% year over year in Q1 2026, which shows how strongly the 2025 round of capacity removals reset supply conditions entering the forecast period. Packaging Corporation of America said corrugated shipments per day, including acquired Greif operations, rose 21.8% year over year in Q1 2026, while legacy volumes increased 2.8%, which indicates that demand recovery is broadening beyond acquired volume.[3]Packaging Corporation of America, “Packaging Corporation of America Reports First Quarter 2026 Results,” sec.gov The United States also remains the main location for many strategic upgrades and reconfiguration decisions, which keeps it central to both pricing discipline and supply flexibility in the North America containerboard market. That concentration gives US mills and converters an outsized role in serving regional e-commerce, industrial, and cross-border packaging flows.

Canada accounted for 21.17% of the North America containerboard market share in 2025, supported by integrated forestry to packaging supply chains in Québec, Ontario, and British Columbia. The country benefits from strong fiber access and established packaging manufacturing, which supports a reliable supply base for regional customers. At the same time, high cost asset pressure is visible in footprint decisions, including Smurfit Westrock’s January 2026 plan to close one paper machine at La Tuque and an extrusion facility in Pointe-aux-Trembles. This means Canada remains strategically important in the North America containerboard market, even as producers become more selective about which mills can deliver competitive returns over the forecast period.

Mexico is projected to grow at a 4.96% CAGR through 2031, making it the fastest expanding country market in the North America containerboard market. ANFEC linked this outlook to cross border nearshoring activity, stronger domestic e-commerce infrastructure, and the country’s role in agricultural export packaging. Mexico produced 4 million tons of cardboard annually in 2025 and still imported a substantial share of containerboard from the United States, which shows how tightly its packaging growth is tied to wider regional supply chains. ANFEC’s 2026 outlook also pointed to softer short term operating conditions, but the longer term investment case remained intact because manufacturing relocation and export packaging demand continue to support board usage. Bio Pappel’s McKinley Packaging opened its seventh US corrugated box plant in Lancaster, Texas in January 2025, which illustrates how Mexico linked producers are building capacity on both sides of the border to serve the North America containerboard market more directly.

Competitive Landscape

The North America containerboard market became more concentrated after major transactions completed across 2024 and 2025, including the formation of Smurfit Westrock, International Paper’s combination with DS Smith, and Packaging Corporation of America’s acquisition of Greif’s containerboard business. TAPPI Paper 360 said these moves left 65% of regional containerboard capacity in the hands of Smurfit WestRock, International Paper, and Packaging Corporation of America, which raised the strategic importance of scale, integration, and mill network quality.[4]Leslee Masters, “PCA/Greif Deal Continues Industry Trend of Consolidation,” paper360.tappi.org This structure gives the leading group greater leverage in pricing actions, supply rationalization, and customer service coverage across major converting corridors. It also means competition is shifting away from simple volume growth and toward mix quality, operating cost control, and the ability to offer both virgin and recycled solutions across regional accounts.

Strategic moves since early 2026 show that leading companies are not following the same playbook across the North America containerboard market. International Paper agreed to acquire NORPAC for USD 360 million in April 2026, expanding its recycled-grade position on the West Coast and improving system flexibility in a region with distinct sustainability needs. Smurfit Westrock completed a major upgrade at its Florence, South Carolina kraft linerboard mill in March 2026, broadening basis weight range and lowering manufacturing costs across fiber, energy, and maintenance categories. Packaging Corporation of America reconfigured its Wallula mill and separately launched a gas turbine program at 3 mills, which shows a sharper focus on energy economics and recycled linerboard positioning. These examples show that the North America containerboard market is being shaped by targeted asset decisions rather than broad based capacity additions.

Competition below the top tier is centered on product specialization, service speed, and the ability to meet sustainability focused procurement requirements without losing cost competitiveness. High performance lightweight recycled linerboard for e-commerce and food linked corrugated formats remains one of the clearest open spaces because these applications demand both performance tuning and efficient converting support. International Paper’s 2024 Annual Report also highlighted a portfolio of hundreds of packaging related intellectual property assets, which suggests that research, formulation, and certified fiber sourcing are becoming part of the competitive moat alongside simple scale. That leaves the North America containerboard market as a concentrated field with active room for innovation, but not a closed market where smaller or more specialized players have no route to growth.

North America Containerboard Industry Leaders

Smurfit Westrock plc

International Paper Company

Packaging Corporation of America

Cascades Inc.

Graphic Packaging Holding Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: International Paper announced a definitive agreement to acquire North Pacific Paper Company from One Rock Capital Partners for USD 360 million.

- April 2026: Packaging Corporation of America reported Q1 2026 results showing corrugated shipments including acquired Greif operations up 19.9%, or 21.8% per day, versus Q1 2025, with containerboard mills running at full capacity.

- March 2026: Smurfit Westrock completed a major upgrade at its Florence, South Carolina kraft linerboard mill, installing a 330-inch paper machine that expanded the facility’s containerboard basis weight range from, 23 lb to 56 lb.

- February 2026: Packaging Corporation of America completed reconfiguration of its Wallula, Washington containerboard mill, permanently retiring the No. 2 paper machine and kraft pulping operations due to an 89% increase in Washington state electricity rates over 2 years.

North America Containerboard Market Report Scope

The scope of this report covers the North America containerboard market, including an analysis of market trends, growth drivers, challenges, and opportunities. Containerboard is the material used to produce corrugated boxes, primarily consisting of linerboard and corrugating medium. This report examines market dynamics, supply and value chain, and the competitive landscape, providing insights into the current market landscape and future growth prospects over the forecast period.

The North America Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), End User (Food and Beverage, Consumer Goods, Industrial, and More), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End Users |

| United States |

| Canada |

| Mexico |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End User | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End Users | |

| By Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the projected value of North America containerboard by 2031?

The market is expected to reach USD 33.64 billion by 2031, rising from USD 29.05 billion in 2026 at a 2.98% CAGR over 2026 to 2031.

What is driving demand for containerboard in North America?

The main demand drivers are e-commerce shipping, sustainable packaging adoption, food delivery packaging needs, and plastic replacement under producer responsibility rules.

Which country is growing fastest in the region?

Mexico is the fastest growing country segment, with a projected CAGR of 4.96% through 2031, supported by nearshoring, e-commerce expansion, and agricultural export packaging.

Which material segment leads the region?

Virgin fibers led with a 32.15% value share in 2025 and also posted the fastest projected growth within the material category at 3.62% through 2031.

Which product type is expanding the fastest?

Testliners are projected to grow at a 4.17% CAGR through 2031, while flutings held the largest product type share at 29.63% in 2025.

What are the main risks affecting producer margins?

The biggest risks are recovered paper price volatility, uneven energy costs across mill locations, and a demand recovery that is still moderate rather than broad based.

Page last updated on: