Israel Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

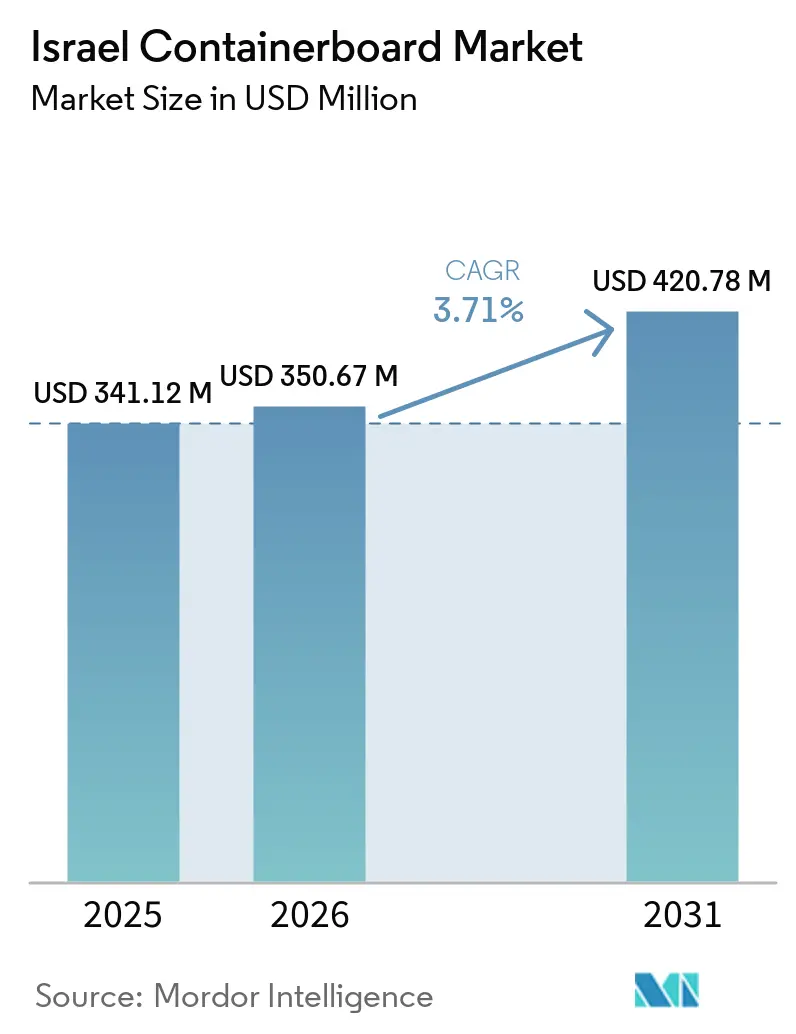

| Base Year Market Size (2025) | USD 341.12 Million |

| Market Size (2026) | USD 350.67 Million |

| Market Size (2031) | USD 420.78 Million |

| Growth Rate (2026 - 2031) | 3.71% CAGR |

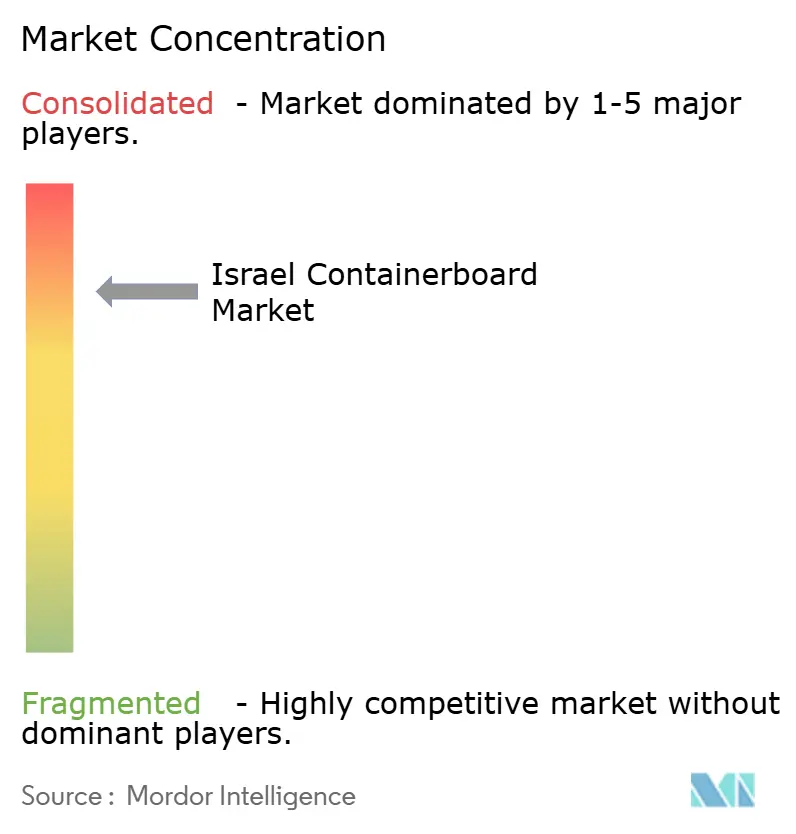

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Israel Containerboard Market Analysis by Mordor Intelligence

The Israel Containerboard Market size was valued at USD 341.12 million in 2025 and is estimated to grow from USD 350.67 million in 2026 to reach USD 420.78 million by 2031, at a CAGR of 3.71% during the forecast period (2026-2031).

The Israel containerboard market is being supported by steady demand from food processors, fresh-produce exporters, and e-commerce fulfillment networks that need dependable corrugated packaging at scale. A stricter regulatory setting around packaging recovery and recycled content is also pushing the Israel containerboard market toward stronger use of OCC-based grades and more disciplined fiber procurement. The Israel containerboard market remains shaped by a concentrated domestic supply base, which improves local responsiveness but also keeps buyers alert to supply concentration and grade availability. Import dependence for selected grades still matters, especially where food-contact performance, moisture resistance, or export requirements remain difficult to meet with recycled inputs. Security-related shipping disruptions add another layer of volatility, which makes domestic recovery, mill efficiency, and local converter agility more important to the Israel containerboard market over the forecast period.

Key Report Takeaways

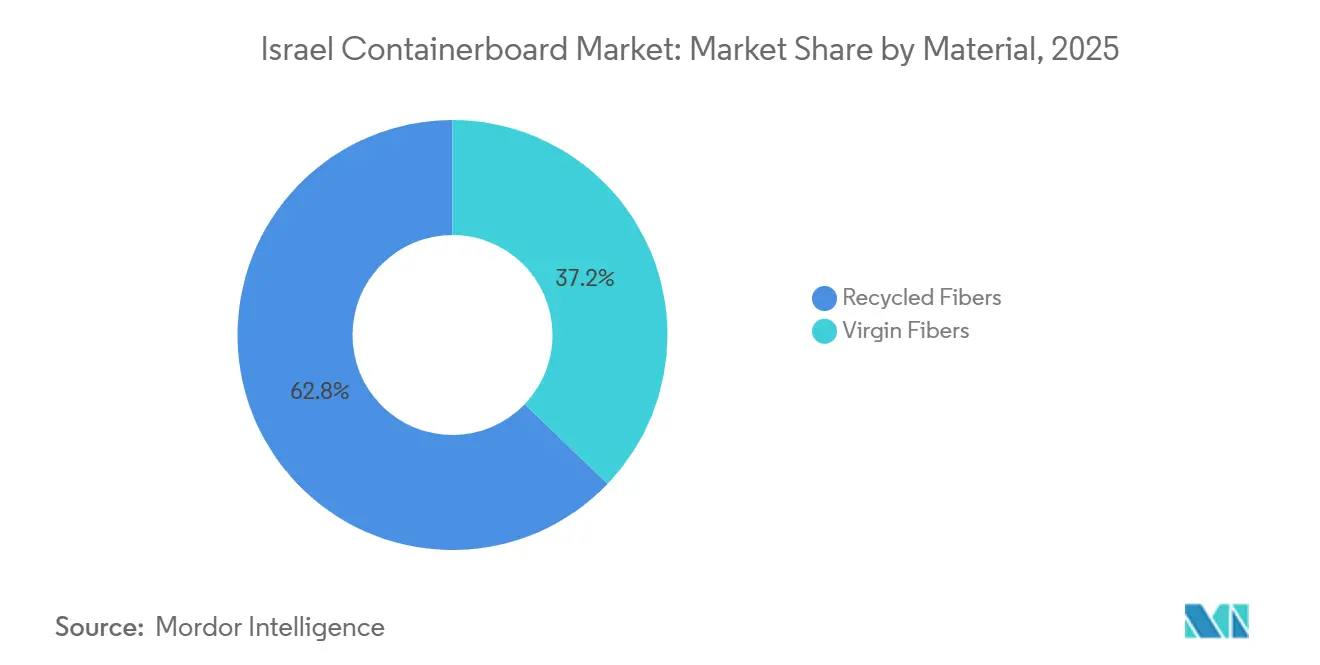

- By material, recycled fibers held 62.83% of the Israel containerboard market in 2025, while virgin fibers are projected to record the fastest growth at a CAGR of 4.41% through 2031.

- By product type, kraftliners accounted for 53.79% of revenue in 2025, while flutings are expected to expand at a CAGR of 4.17% through 2031.

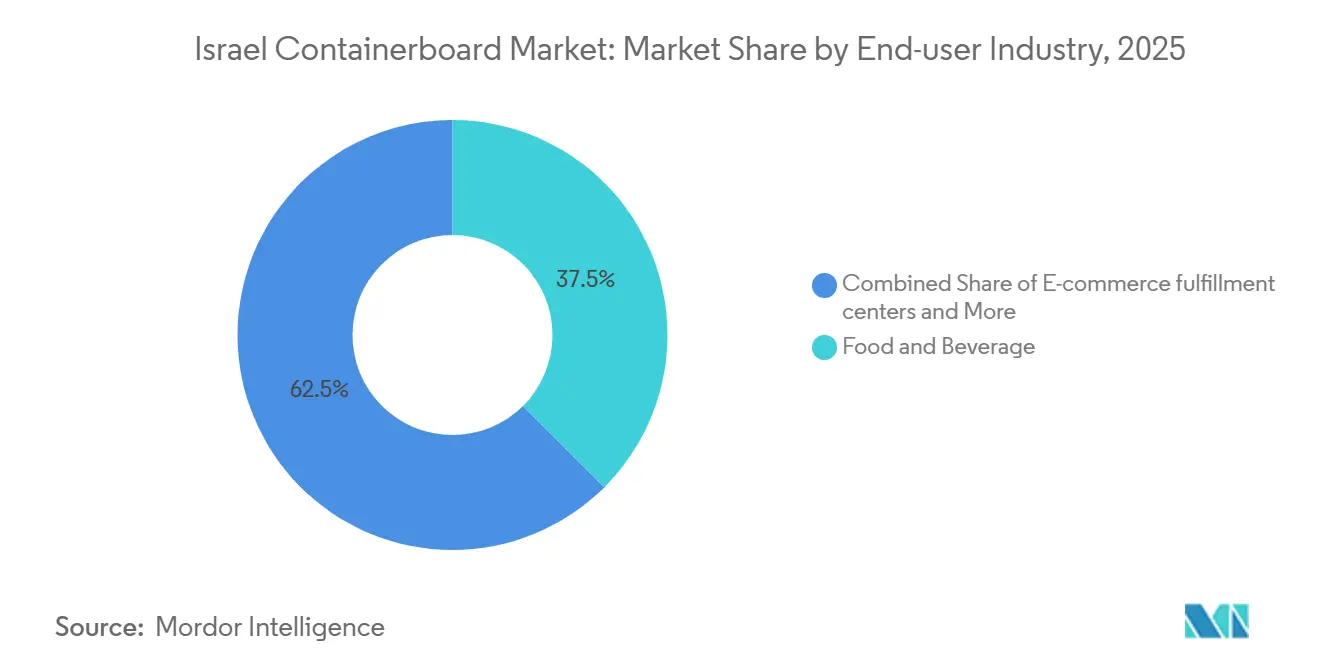

- By end-user industry, food and beverage held 37.54% of the Israel containerboard market share in 2025, while e-commerce fulfillment centers posted the fastest projected CAGR at 4.85% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Israel Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Food And Beverage Shipment Volumes | +2.1% | National, concentrated in Tel Aviv-Haifa industrial corridor | Short term (≤ 2 years) |

| Growing E-commerce Fulfillment Demand | +1.4% | National, with demand concentration in Greater Tel Aviv and Central District logistics zones | Short term (≤ 2 years) |

| Tightening Packaging Waste And Recycled Content Compliance | +0.9% | National, with regulatory influence from the Ministry of Environmental Protection and alignment with EU packaging standards | Medium term (2-4 years) |

| Higher Fresh Produce Export Packaging Intensity | +0.7% | National, with significant activity in Northern Israel, the Negev Desert, and the Sharon Plain export hubs | Short term (≤ 2 years) |

| Hadera OCC Upgrade Improving Domestic Supply Security | +0.5% | National, centered on the Hadera mill | Short term (≤ 2 years) |

| Household Collection Reform Expanding Recoverable Fiber Streams | +0.3% | National, with early gains in municipalities using orange-bin systems that cover 70% of the population | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Food And Beverage Shipment Volumes Sustain Baseline Containerboard Demand

The Israel containerboard market continues to draw core volume support from a food processing base that spans more than 3,000 facilities and remains one of the most dependable packaging users in the country.[1]U.S. Department of Agriculture Foreign Agricultural Service, “Food Processing Ingredients Annual, Tel Aviv, Israel, IS2025-0009,” Foreign Agricultural Service, apps.fas.usda.gov The top 40 food companies employed more than 41,000 workers and generated USD 23.19 billion in combined revenue as of 2022, and that operating base has grown further in the period covered by the current market narrative. Demand from this channel stays resilient because corrugated transit packaging remains essential even when consumer conditions weaken, since producers still need consistent burst strength and stacking performance in distribution. Packaging intensity has also moved higher because individually sized packaged formats have gained ground over family-sized formats since late 2023, which raises the number of corrugated units needed for the same product volume. Large processors such as Tnuva, Osem-Nestle, Strauss, and the Central Company for Beverages Distribution have expanded retail-ready packaging requirements, which supports demand for higher-quality liners and fluting. Public health packaging standards further reinforce the preference for certified board in food applications, which keeps this driver central to the Israel containerboard market through the forecast period.

Growing E-Commerce Fulfillment Demand Reshapes Secondary Packaging Specifications

The Israel containerboard market is also benefiting from online retail expansion, with Israel’s e-commerce revenue exceeding USD 10.2 billion in 2025 and maintaining one of the stronger growth profiles in the region.[2]U.S. Department of Commerce International Trade Administration, “Israel - eCommerce,” Country Commercial Guides, trade.gov E-commerce fulfillment creates different packaging needs than store distribution because it favors lighter board combinations with higher burst performance and tighter fit for parcel shipment. Same-day and next-day delivery expectations in the Greater Tel Aviv area are pushing fulfillment centers to process more individual orders per hour, which raises containerboard use even without a matching rise in average order value. This shift is lifting demand for fluting grades and performance-oriented recycled liners rather than purely volume-driven commodity formats, which is changing the mix of products consumed within the Israel containerboard market. New direct-to-consumer requirements also favor better print quality, cleaner presentation, and more precise board engineering, which increases pressure on converters to upgrade equipment and board selectio. As a result, e-commerce is not only adding volume to the Israel containerboard market, it is also shifting demand toward more technically specified grades and faster conversion cycles.

Tightening Packaging Waste And Recycled Content Compliance Favors Recycled-Fiber Grades

The Israel containerboard market is being pushed further toward recycled-fiber grades by the regulatory direction set under the Packaging Law and the 2026 waste-sector work process launched by the Ministry of Environmental Protection. That process targets at least 50% household packaging waste collection and aims to align recycling targets more closely with European standards, which raises the compliance bar for packaging placed on the local market.[3]Ministry of Environmental Protection, “The Ministry of Environmental Protection Launches the Multi-Sectoral Work Process for the Regulation of the Waste Sector,” Government of Israel, gov.il The commercial effect is broader than domestic regulation alone because Israeli exporters serving Europe and the United Kingdom already face customer pressure around recycled content and documentation. Tamir’s role as the main compliance body under the Packaging Law gives the system a structured route for collection and recovery, which improves the long-term economics of recycled containerboard production. Additional municipal investment in sorting capacity is improving the quality and availability of recovered fiber, which supports more stable feedstock for local producers. This driver strengthens the recycled side of the Israel containerboard market, even as converters that lack closed-loop sourcing remain exposed to rising compliance costs and procurement pressure.

Higher Fresh Produce Export Packaging Intensity Strengthens Demand For Moisture-Resistant Grades

The Israel containerboard market gains added support from export agriculture because fresh produce supply chains need corrugated packaging that can hold shape and strength under cold-chain and humid conditions. Export packaging for avocado, citrus, dates, and vegetables typically requires more specialized board formats than standard domestic retail movement, especially when boxes must meet destination-country handling and quality requirements.[4]Negev Produce, “Company Website,” Negev Produce, negev-produce.com That requirement tends to raise board intensity per unit because moisture resistance, crush retention, and transport durability matter more in export logistics than in short domestic routes. The food export base also overlaps with customers that operate under internationally recognized packaging and safety specifications, which supports premium demand for better-performing liner and fluting combinations. As agricultural exporters expand shipments into Europe and North America, packaging decisions move beyond price and become tied more closely to compliance, transit protection, and presentation at destination. This makes export agriculture a smaller but technically influential demand source within the Israel containerboard market, especially for grades that recycled fibers do not yet fully replace.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exposure To Imported Virgin Fiber And Concentrated Supply Sources | -0.8% | National, especially for converters dependent on Scandinavian softwood kraft and North American hardwood pulp, with added certification pressure on export-linked supply chains | Medium term (2-4 years) |

| Shipping And Security Disruptions Raising Lead Times And Freight Risk | -0.5% | National, especially along the Haifa and Ashdod port corridors and connected sea lanes through the Red Sea, Suez Canal, and Strait of Hormuz | Short term (≤ 2 years) |

| Higher Producer Responsibility And Compliance Costs | -0.4% | National, affecting manufacturers and importers registered under Packaging Law and Tamir compliance frameworks | Medium term (2-4 years) |

| OCC Quality Losses From Weak Household Source Separation | -0.3% | National, with stronger effects outside mature orange-bin collection zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Imported Virgin Fiber Dependence Creates Structural Cost And Supply Fragility

The Israel containerboard market still depends on imported virgin fiber for applications where recycled inputs do not consistently meet food-contact, moisture, or export-grade performance thresholds. Domestic capacity is centered on recycled-fiber production, which means virgin-grade availability is shaped more by foreign suppliers and logistics conditions than by local mill decisions. This creates exposure to global kraft pulp cycles and to supply concentration among a relatively limited group of European and North American producers serving export-oriented converters. Compliance expectations linked to export markets add another cost layer because documentation and chain-of-custody requirements can no longer be treated as a low-priority back-office issue. Buyers that have not diversified toward recycled grades or multi-source procurement remain more exposed when imported virgin inputs tighten or arrive late. This restraint does not stop growth in the Israel containerboard market, but it does narrow margins and limits flexibility in the highest-specification end uses.

Shipping And Security Disruptions Raise Lead Time And Freight Risk

The Israel containerboard market also faces recurring disruption from maritime instability because imported paper and pulp grades move through sea lanes that have become less predictable since late 2023. Carrier rerouting through the Cape of Good Hope has added 10-14 days to average voyage times on affected services, directly extending replenishment cycles for imported board and fiber. For converters working on short lead times, that delay raises the need for safety stock and working capital, especially when demand from food and e-commerce customers remains time-sensitive . Freight uncertainty also weakens the economics of spot buying because the final landed cost becomes harder to predict at the point of procurement. A practical effect is that domestic OCC-based production becomes more valuable during shipping stress, even when imported grades remain technically stronger in selected applications . This operating imbalance is one reason the Israel containerboard market places growing strategic value on local fiber recovery and mill reliability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fibers Dominate, But Virgin Fiber Premium Widens

Recycled fibers held 62.83% of the Israel containerboard market share in 2025, which reflected the country’s OCC-based production model and the policy support built around packaging recovery. The domestic position of recycled fiber strengthened after the Hadera mill upgrade brought online a 1,080 bdmt-per-day OCC line in Q3 2024, expanding throughput and improving contamination control in recovered fiber processing . That operational change improved local supply security and reduced the need to rely on imported recycled grades for core applications, especially in standard testliner and fluting output . Tamir’s orange-bin collection system now reaches around 70% of Israeli households, which gives recycled board production a broader and more structured domestic feedstock base than many smaller markets can access. The 2026 waste-sector process adds another layer of support because higher collection and recycling targets encourage better fiber recovery and reinforce the commercial logic of recycled grades.

Virgin fibers remain the smaller material segment, yet they are expected to grow at a CAGR of 4.41% through 2031 because certain applications still require performance that recycled inputs do not consistently deliver. Fresh-produce export packaging, food-contact board, and high-humidity logistics continue to favor virgin-based grades where crush resistance, cleanliness, and moisture behavior must remain tightly controlled. This means the Israel containerboard market does not move in a straight line toward full recycled substitution, even under stronger compliance pressure. Instead, the material mix is likely to keep splitting by performance need, with recycled fibers winning on regulation and local availability while virgin fibers defend premium positions in stricter end uses. Over time, rising recycled-content expectations in export channels may narrow the premium held by virgin fibers, but that change will depend on whether recycled grades can close specification gaps without increasing converter risk.

By Product Type: Kraftliners Lead, Flutings Accelerate On E-Commerce And Lightweight Trends

Kraftliners accounted for 53.79% of revenue in 2025, which kept them as the leading product type in the Israel containerboard market because food transit, produce handling, and industrial movement still rely heavily on strong outer liners. Their lead reflects a practical need for burst strength, stacking stability, and better moisture tolerance in applications where handling conditions are demanding and product loss is costly. Kraftliners also remain closely tied to agricultural export and food distribution, both of which require dependable outer-board performance across longer or colder logistics chains. Testliners sit below kraftliners in price and performance, and they continue to serve large-volume packaging programs where cost control matters more than premium specifications. This keeps testliners relevant in consumer goods and standard transport packaging, even if they do not carry the same growth profile as fluting grades.

Flutings are expected to record the fastest product-type growth at a CAGR of 4.17% through 2031, which shows how packaging demand is shifting toward lighter and more engineered corrugated structures. E-commerce plays a central role in that shift because parcel delivery needs cushioning, weight efficiency, and better board balance rather than only thick-wall construction. Mondi’s November 2025 portfolio extension for food packaging, which added broader corrugated and solid board options with digital printing capabilities, illustrates how suppliers are upgrading medium and fluting propositions for premium channels. Smurfit Westrock also reported stronger EMEA demand and price increases in March and April 2026, which signaled firmer imported board pricing for Israeli converters sourcing from Europe. The result is a product mix in the Israel containerboard market that still centers on kraftliners for volume, but increasingly rewards fluting suppliers that can meet lighter, faster, and more specification-driven demand patterns.

By End-User Industry: Food And Beverage Anchors Volume, E-Commerce Drives Mix Shift

Food and beverage held 37.54% of the Israel containerboard market share in 2025, making it the largest end-user segment because Israel has a broad processing base and a high need for corrugated transit packaging across retail and export channels. The Israel containerboard market size for e-commerce fulfillment centers is projected to expand at a 4.85% CAGR through 2031, which makes that sub-segment the fastest-growing end-user demand pool over the forecast period. Food manufacturers remain the volume anchor because they ship consistently, run at scale, and use packaging formats that must protect goods through warehousing, transport, and shelf replenishment. The rise of smaller pack sizes since 2023 has increased corrugated unit demand within food distribution, which supports volume even when final consumption growth is less dramatic. Consumer goods and industrial users make up the balance of demand, with requirements tied to imported merchandise, domestic distribution, and equipment movement through the main port-linked logistics network.

E-commerce fulfillment centers stand out because their growth changes packaging mix more visibly than packaging volume alone. Rapid-delivery models require more exact box sizing, cleaner printing, and lighter board combinations, which pushes converters toward tighter fluting and liner pairing rather than the heavier grades common in food export. This shift is prompting converter investment in process control and grade selection as much as in raw throughput. The green packaging direction noted for food companies in Israel is also nudging major brands toward certified recycled board, which gives converters room to price compliance-linked packaging at a premium. Taken together, the Israel containerboard industry remains anchored by food volume, but growth is increasingly shaped by end uses that reward specification accuracy, regulatory readiness, and shorter turnaround times.

Geography Analysis

The Israel containerboard market is unusually dependent on one integrated domestic mill at Hadera, while selected grades still come in through import channels linked to major European suppliers. Demand is concentrated in the Tel Aviv-Haifa corridor, where food processors, logistics operators, and consumer goods activity sit closest to major transport and port infrastructure. That narrow coastal concentration means disruption at Haifa or Ashdod can affect inbound inputs and outbound packaged goods at the same time, which amplifies operating risk across the Israel containerboard market .

Import geography still matters because domestic production does not fully cover every performance grade needed by converters and exporters. European suppliers remain relevant for premium liners, testliners, and specialized board used in food, export, and high-specification applications. The Red Sea and Suez route would normally offer the most direct path for much of this trade, but security disruption has forced rerouting patterns that lengthen transit times and complicate liner planning . Added voyage time raises the need for buffer inventory and weakens the economics of just-in-time procurement for converters serving short lead-time domestic customers . This geographic exposure creates a persistent cost floor for imported grades and improves the relative position of locally produced recycled board, even when imported products still hold performance advantages in selected uses .

Israel’s agricultural export zones in the Northern Galilee, the Negev Desert, and the Sharon Plain add a second geographic layer to demand because box performance needs change once produce enters export logistics. Exporters in these areas need corrugated packaging that can meet quality, phytosanitary, and transit handling requirements for European and North American destinations. That requirement increases the importance of reliable regional converter access and dependable delivery into packing houses, not just supply into the main urban corridor. The Israel containerboard market therefore combines a compact domestic footprint with a surprisingly varied set of geographic needs, ranging from urban fulfillment and food processing to export agriculture and port-linked industrial movement.

Competitive Landscape

The Israel containerboard market shows a semi-concentrated structure at the mill level and a fragmented structure at the converter level, which creates a competitive pattern that is tighter in board supply than in box conversion. Infinya Containerboard remains the country’s only integrated recycled containerboard producer, and its position is supported by a link between fiber recovery, board manufacturing, and downstream packaging activities. That structure gives Infinya an advantage in supply security, lead times, and recovered-fiber access, especially during periods when import routes become less predictable. The Hadera OCC upgrade, delivered with ANDRITZ technology and operating from Q3 2024, strengthened that position by adding 1,080 bdmt per day of recycled pulping capacity and lowering contamination-related losses .

Further downstream, rivalry becomes more fragmented because converters such as Best Carton, Cargal, Triplex Containers, Ducart Packaging Industries, and smaller family-owned firms compete on service speed, print quality, and application fit rather than mill scale alone. That part of the Israel containerboard market is more exposed to procurement swings because many converters depend on either domestic board from Infinya or imported supply from European producers. Global suppliers remain active reference points for Israeli buyers, and strategic moves by those suppliers continue to shape local sourcing options. Mondi expanded its corrugated and solid board offer for food packaging in November 2025, which improved its position in premium and digitally enabled applications relevant to Israeli converters. Smurfit Westrock reported stronger EMEA demand, customer wins, and containerboard price increases in Q1 2026, which directly affected imported board benchmarks for the Israel containerboard market.

Saica Group added another strategic move in May 2026 when it announced the acquisition of Thimm Group, extending its European corrugated network and strengthening its ability to serve export-grade and shelf-ready demand through established channels. Competitive whitespace remains visible in food-contact certified recycled liner, moisture-resistant coated grades for fresh produce, and higher-graphic corrugated formats for direct-to-consumer shipping. This means the Israel containerboard market is not fully locked into commodity competition, because technical capability and compliance readiness still create room for differentiation. At the same time, the broader market remains disciplined by one dominant domestic producer, active import competition, and converters that must balance cost, turnaround time, and grade performance on a daily basis.

Israel Containerboard Industry Leaders

Infinya Containerboard Ltd.

Mondi plc

Smurfit Westrock plc

Saica Group

W. Hamburger GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Saica Group announced the acquisition of Thimm Group, a leading European corrugated board and display solutions provider with approximately EUR 539 million (approximately USD 582 million) in 2024 revenues and around 2,500 employees. The transaction, pending antitrust approval, extends Saica's corrugated converting footprint into Germany, Poland, the Czech Republic, and Romania, strengthening its ability to supply retail-ready and export-grade containerboard solutions to Israeli converters through European import channels.

- April 2026: Smurfit Westrock reported improved EMEA demand and containerboard price increases of USD 20 per ton during Q1 2026, with a further USD 30 per ton increase implemented in April, primarily due to higher energy costs and better market conditions. EMEA and Asia Pacific operations continued volume growth and customer wins, directly affecting import-price benchmarks for Israeli containerboard buyers relying on European supply.

- January 2026: International Paper announced plans to separate into two independent, publicly traded packaging solutions companies, one for North America and one for EMEA. The structural change is expected to complete within 12-15 months. The EMEA separation, with USD 400 million earmarked for preparation investment during 2026, will create a standalone European containerboard and corrugated packaging entity that is likely to reassess supply relationships with smaller markets including Israel.

Israel Containerboard Market Report Scope

The Israel Containerboard Market encompasses the production, distribution, and consumption of containerboard used in the manufacture of corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The market is driven by the increasing demand for sustainable, lightweight, and durable packaging solutions.

The Israel Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, E-Commerce Fulfillment Centers, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| E-Commerce Fulfillment Centers |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| E-Commerce Fulfillment Centers | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current size and future outlook for the Israel containerboard market?

The Israel containerboard market was valued at USD 341.12 million in 2025, reaches USD 350.67 million in 2026, and is projected to reach USD 420.78 million by 2031 at a 3.71% CAGR.

Which material segment leads containerboard demand in Israel?

Recycled fibers led with 62.83% share in 2025 because domestic production is built around OCC recovery, regulatory compliance, and the Hadera recycled-fiber platform.

What is the fastest-growing end-use area for containerboard in Israel?

E-commerce fulfillment centers are the fastest-growing end-use area, with a projected 4.85% CAGR through 2031, driven by parcel shipping, faster delivery cycles, and more exact box specifications.

Why does food and beverage remain so important for corrugated demand in Israel?

Food and beverage held 37.54% share in 2025 because Israel has a broad processing base, steady shipment volumes, and packaging formats that need reliable corrugated transit protection.

What is the main supply-side risk for buyers and converters?

The biggest risk comes from exposure to imported virgin fiber and shipping disruption, which can lengthen lead times, raise inventory needs, and increase landed cost volatility for higher-specification grades.

Which companies most influence competitive conditions in Israel?

Infinya remains the key domestic producer, while Mondi, Smurfit Westrock, Saica Group, and International Paper influence import options, product upgrades, and pricing conditions tied to European supply.

Page last updated on: