Middle East and Africa Cartonboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

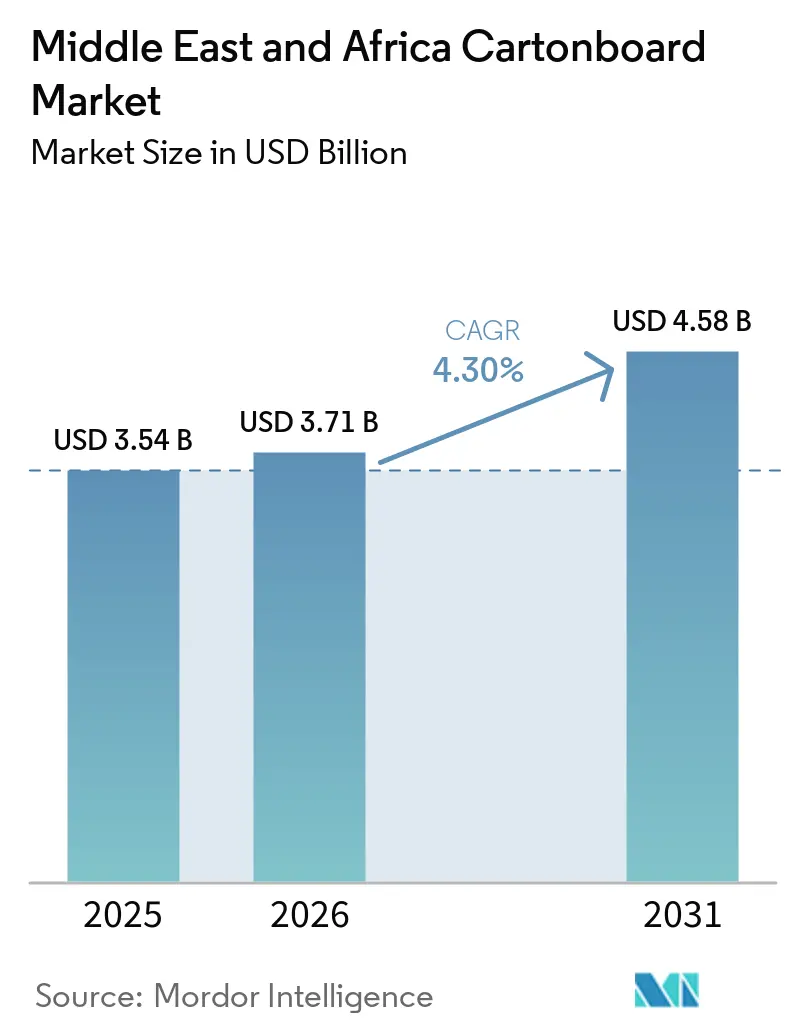

| Base Year Market Size (2025) | USD 3.54 Billion |

| Market Size (2026) | USD 3.71 Billion |

| Market Size (2031) | USD 4.58 Billion |

| Growth Rate (2026 - 2031) | 4.30% CAGR |

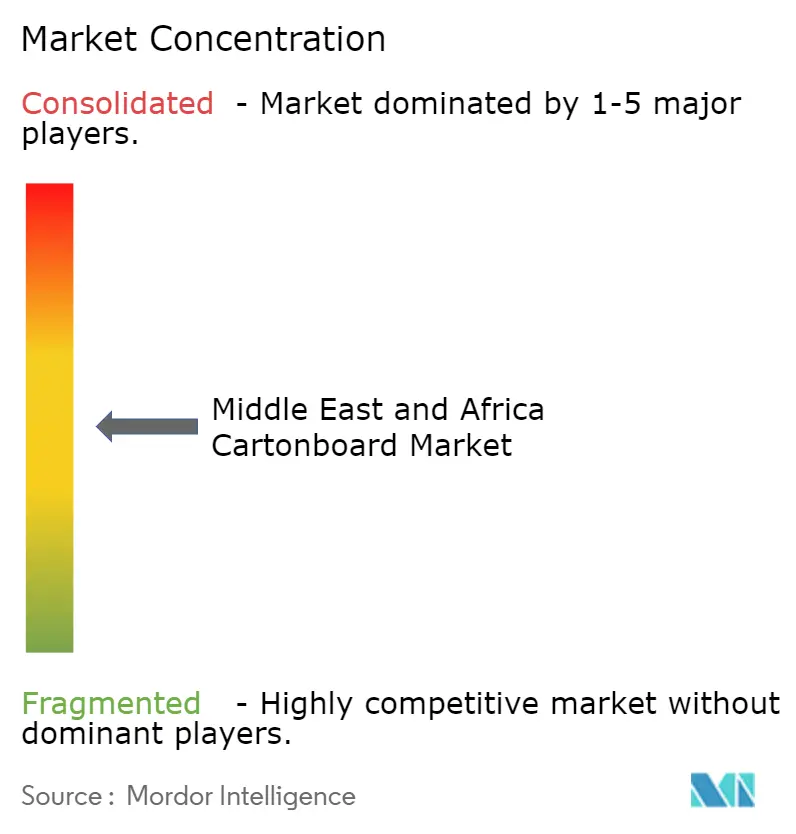

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East and Africa Cartonboard Market Analysis by Mordor Intelligence

The Middle East And Africa Cartonboard Market size was valued at USD 3.54 billion in 2025 and is estimated to grow from USD 3.71 billion in 2026 to reach USD 4.58 billion by 2031, at a CAGR of 4.30% during the forecast period (2026-2031).

Growth is being supported by tighter plastic rules in key Gulf markets, wider packaged food consumption as cities grow and modern retail spreads, and stronger demand for premium board in pharmaceutical packaging. The Middle East and Africa cartonboard market is also becoming more commercially uneven, because imported board from Europe and Asia often lands at prices below local production costs even while carton demand keeps rising. Brand owners are moving toward virgin-fiber and higher-performance grades where food-contact standards, hygiene expectations, and print quality carry more weight in purchase decisions. Saudi Arabia remains the main demand center because its FMCG production base, hypermarket expansion, and food processing investment keep carton consumption broad and repeatable. The Middle East and Africa cartonboard market therefore shows steady volume support, but converter margins remain under pressure from freight volatility, import competition, and limited local raw material depth.

Key Report Takeaways

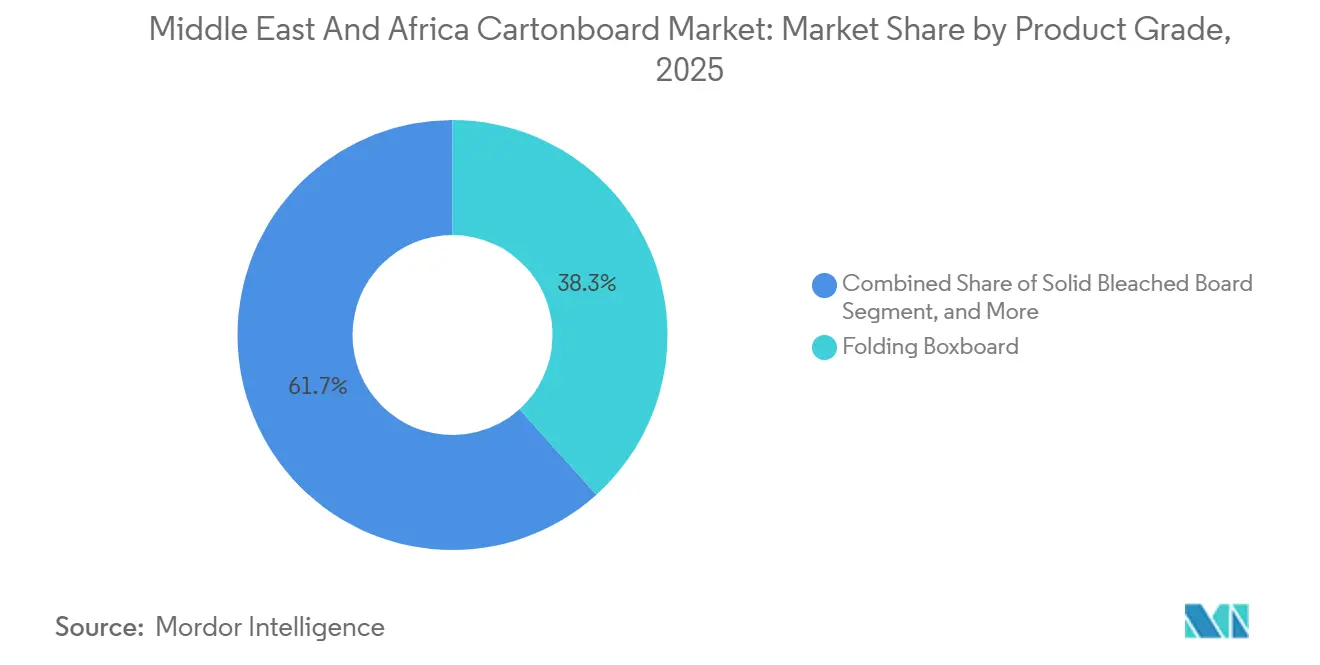

- By product grade, Folding Boxboard held 38.32% of the Middle East and Africa cartonboard market share in 2025, while Solid Bleached Board is forecast to expand at a 7.53% CAGR through 2031.

- By packaging format, Folding Cartons accounted for 56.15% of the Middle East and Africa cartonboard market size in 2025, while Other Packaging Formats, including cups, foodservice containers, and trays, are advancing at a 5.45% CAGR through 2031.

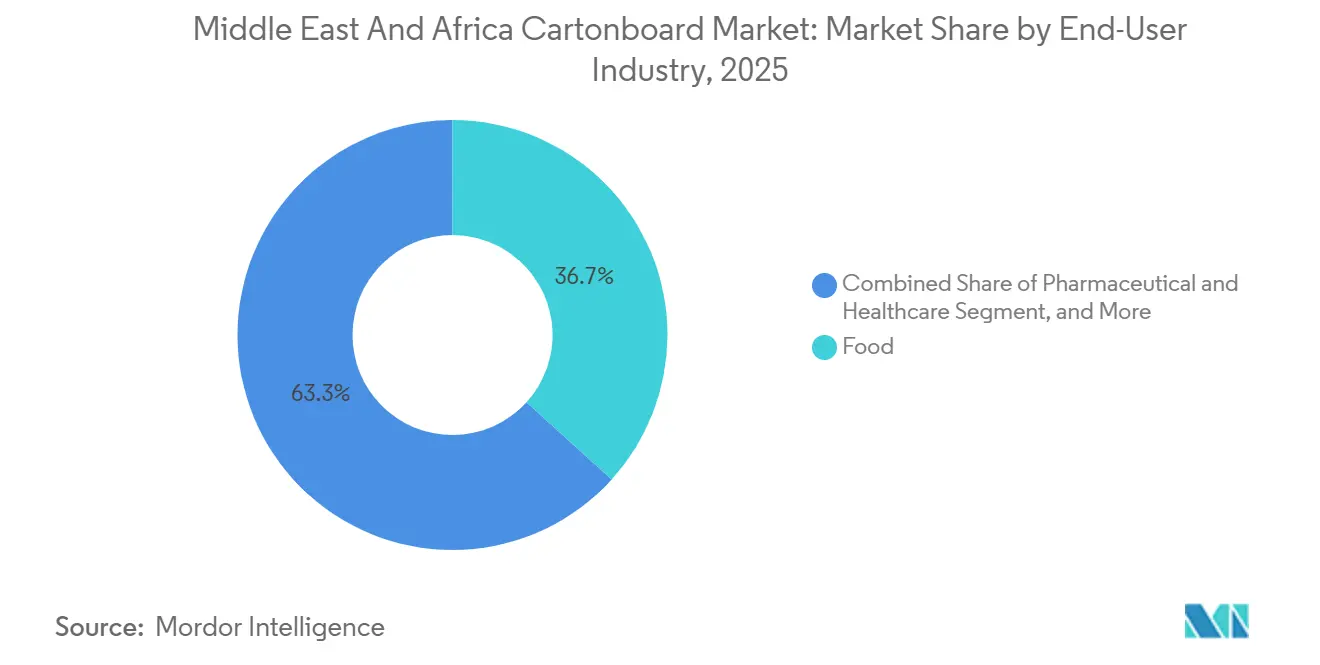

- By end-user industry, food held 36.73% of regional value in 2025, while pharmaceutical and healthcare packaging is expected to grow at a 6.67% CAGR through 2031.

- By geography, Saudi Arabia commanded 33.27% of regional value in 2025, while South Africa is projected to record the fastest regional growth at a 5.64% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East and Africa Cartonboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastic Substitution and Packaging Regulation Tailwinds | +1.4% | UAE and Saudi Arabia (primary), accelerating adoption across GCC with spill-over to Egypt and Turkey | Short term (≤ 2 years) |

| Rising Packaged Food Consumption | +1.1% | GCC core markets, with increasing contribution from North Africa and urbanizing Sub-Saharan Africa | Medium term (2-4 years) |

| Beverage Carton Demand From Dairy and Juice | +0.8% | Saudi Arabia and UAE (dominant), Turkey (growing), East African school milk programs as secondary pull | Medium term (2-4 years) |

| Pharmaceutical and Healthcare Packaging Localization | +0.5% | Saudi Arabia and UAE (primary), secondary cascade across GCC as localization requirements deepen | Long term (≥ 4 years) |

| Halal-Certified Food Export Expansion | +0.3% | Saudi Arabia, UAE, and Turkey as established halal export hubs supplying global Muslim-majority markets | Medium term (2-4 years) |

| Hot-Climate Preference for Shelf-Stable Cartons | +0.2% | GCC core, spill-over to Sub-Saharan Africa and North Africa where cold chain infrastructure is limited | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Plastic Substitution And Packaging Regulation Tailwinds

The UAE's second phase under Ministerial Decision No. 380 of 2022 became effective on January 1, 2026, and it prohibited the import, manufacture, and trade of plastic beverage cups and lids, cutlery, food containers, and plates, all of which map directly to fiber-based alternatives.[1]Ministry of Climate Change and Environment, “Commencement of the Second Phase of Ministerial Decision No. 380 of 2022 on Single-Use Plastic Products,” Ministry of Climate Change and Environment, moccae.gov.ae That shift turns cartonboard demand into a compliance-driven purchase rather than a voluntary sustainability option for many foodservice and take-away formats. The pressure is not falling evenly across the supply base, because larger converters can document traceability, material composition, and production consistency more easily than smaller facilities. That difference improves the position of certified regional converters that can meet multinational procurement standards without long qualification cycles. It also increases the need for better grade selection, cleaner surfaces, and more stable converting performance where direct food contact is involved. The Middle East and Africa cartonboard market receives a near-term demand lift from this regulatory shift because packaging redesign is replacing simple material reduction in several visible consumer applications.

Rising Packaged Food Consumption

Rising packaged food consumption continues to provide the broadest demand base for the region, especially where urban growth, modern retail rollout, and busier household routines are changing everyday purchase behavior. Smaller households and less time for fresh meal preparation are supporting ready-to-eat, shelf-stable, and convenience-led food formats that use cartons in primary and secondary packaging chains. This trend matters because plastic restrictions are pushing brand owners in several categories to redesign packaging structures rather than make minor material changes. Folding Boxboard and food service board benefit most where producers want food-contact acceptance, stronger shelf appearance, and dependable converting performance at scale. Turkey adds a useful processing dimension because it serves as both a large converter of cartonboard and a packaged food supplier into GCC channels. The Middle East and Africa cartonboard market therefore keeps a strong consumption floor even when input cost volatility and import competition complicate converter profitability.

Beverage Carton Demand From Dairy And Juice

Beverage cartons remain supported by dairy and juice, where ambient distribution and hot climates favor shelf-stable formats over chilled systems that require more costly cold-chain support. This is especially important in Gulf markets, where UHT dairy and aseptic juice formats fit the region's logistics conditions and retail economics more naturally than refrigerated alternatives. Tetra Pak signed agreements at the UAE's Meliha Dairy Factory covering USD 8 million in processing infrastructure and a USD 3.5 million Tetra Top filling line, showing how new dairy capacity is being tied directly to carton-based systems.[2]Tetra Pak International S.A., “The UAE's First-of-Its-Kind Organic Dairy Farm in Sharjah Raises Sustainability Benchmarks with Tetra Pak's End-to-End Processing and Filling Solutions,” Tetra Pak, tetrapak.com Plant-based beverages in the UAE are also favoring cartons because premium positioning, hygiene signals, and sustainability messaging are easier to communicate in this format. Smaller juice pack sizes are gaining relevance as producers adjust pack architecture and portion sizes, which can increase board use through more frequent design changes and higher unit counts. That keeps liquid packaging board steady inside the Middle East and Africa cartonboard market even while other grades face sharper swings in spot buying and landed costs.

Pharmaceutical And Healthcare Packaging Localization

Pharmaceutical and healthcare packaging is the fastest-growing end-user segment, at a 6.67% CAGR from 2026 to 2031, because local manufacturing incentives and stricter compliance expectations are pushing more packaging activity closer to domestic production bases. Saudi Pharmaceutical Chemicals Company states that it developed what it describes as the Kingdom's first national pharmaceutical primary packaging facility, and the company positions the project as a way to reduce import dependence and support Vision 2030 manufacturing goals. That direction raises demand for premium cartonboard in secondary packs that need clean surfaces, stable machinability, and consistent print performance on high-speed lines. Serialization, tamper-evident features, and detailed pack information also make higher-quality bleached grades more relevant than recycled substitutes in regulated healthcare uses. The Middle East and Africa cartonboard market benefits because pharmaceutical demand is value-rich as well as volume-supportive, which improves the regional grade mix even when general FMCG pricing stays highly competitive. It also raises barriers to entry, since converters without controlled processes and compliance documentation find it harder to qualify for healthcare contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imported Pulp and Board Price Volatility | -1.2% | Global in origin, most acute in MEA markets with no local board production capacity | Short term (≤ 2 years) |

| Limited Recovered Fiber and Collection Infrastructure | -0.7% | Africa (most severe, South Africa, Nigeria, Egypt), moderate across the GCC | Long term (≥ 4 years) |

| Red Sea and Long-Haul Freight Disruptions | -0.5% | GCC import-dependent markets, East Africa and Egypt along Suez-dependent import corridors | Short term (≤ 2 years) |

| Power, Water, and Currency Stress on Converters | -0.4% | Sub-Saharan Africa (power), Turkey and Egypt (currency), South Africa (municipal infrastructure) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Imported Pulp And Board Price Volatility

The Middle East and Africa cartonboard market remains heavily exposed to imported pulp, recycled fiber, and finished board, which keeps converter margins closely tied to global price cycles. Capacity additions in Europe and Asia, producer currency moves, and shipping bottlenecks can all reach local input costs quickly because the region has limited ability to offset them with local raw material depth. Mayr-Melnhof said in its Q1 2026 trading statement that geopolitical tensions in the Middle East were creating noticeable cost pressure on energy, transportation, and chemicals, while its 2025 results also flagged interruption risk for its 2 Middle Eastern packaging plants. The timing of these shocks matters just as much as the price level, because board cost resets often reach converters before FMCG customers accept packaging price increases. That gap compresses margins, weakens cash flow, and leaves smaller operators more exposed than scale converters with stronger customer contracts. The Middle East and Africa cartonboard market can keep growing under these conditions, but returns become more uneven across product grades, converter sizes, and import corridors.

Limited Recovered Fiber And Collection Infrastructure

Limited recovered fiber and collection systems keep domestic recycled-board economics weak across much of the region, especially outside the few markets with established paper recovery networks. This reduces the ability of converters and local producers to build a cheaper local alternative to imported virgin grades in White-Lined Chipboard and related product categories. Even where collection exists, electricity, water, and municipal service instability can still weaken production economics and interrupt operating continuity. South Africa illustrates that structural problem, because the reported closure of Springs Mill removed the country's only domestic cartonboard production base and pushed future growth further toward imports. The result is a slower path to local supply development even though food, agriculture, retail, and healthcare packaging needs are still expanding across the region. This keeps the Middle East and Africa cartonboard market structurally dependent on external board supply for longer than converters and end users would prefer.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Grade: Premium Board Gains From Compliance And Print Quality

Folding Boxboard held 38.32% of the market in 2025, giving it the largest role in the Middle East and Africa cartonboard market because it fits food, personal care, and healthcare cartons with a broadly accepted specification base. Its balance of stiffness, print quality, and food-contact suitability keeps it central where shelf appeal and compliance need to coexist inside mass-market and premium retail channels. The grade also benefits from the shift toward virgin-fiber surfaces, since brand owners are placing more weight on hygiene, material integrity, and consistent converting performance. In the Middle East and Africa cartonboard industry, this makes Folding Boxboard the commercial default for many secondary packs even when raw material prices move higher. Imported European supply still matters heavily, and Metsä Board said in April 2026 that geopolitical tensions in the Middle East were increasing logistics and certain raw material costs, with further effects expected in later quarters.

Solid Bleached Board is expanding at a 7.53% CAGR, the fastest among product grades, because pharmaceutical packs, premium cosmetics cartons, and higher-end foodservice applications need brightness, cleanliness, and precise print results. Liquid Packaging Board remains steadier, supported by long-term aseptic relationships with dairy and juice producers rather than short-cycle spot buying. Tetra Pak's investment at the UAE's Meliha Dairy Factory shows how new processing and filling assets continue to reinforce ambient dairy and juice carton demand in the region. White-Lined Chipboard and Solid Unbleached Board still serve cost-led and strength-led applications, but they are less exposed to the premium compliance pull that now shapes the Middle East and Africa cartonboard market. The broader grade mix shows a move away from purely price-based buying and toward function-based specification, especially where regulatory scrutiny, export presentation standards, and product safety demands are rising.

By Packaging Format: Foodservice Uses Gain On The Base Of Folding Cartons

Folding Cartons accounted for 56.15% of the packaging format mix in 2025, which gave them the clearest lead in the Middle East and Africa cartonboard market size across food, pharmaceuticals, and personal care packs. Their leadership reflects format flexibility, because the same converting base can serve blister-pack cartons, dry food boxes, cosmetics cartons, and other retail packs with different finishing requirements. This breadth also helps converters protect plant utilization when one end-market softens and another improves. Premium print and finishing capabilities are becoming more valuable inside this format, since regional buyers in cosmetics, fragrance, tobacco, and premium retail place visible weight on shelf presentation. The result is that folding cartons remain the stable center of demand even as faster-growing adjacent uses continue to narrow part of the lead.

Other Packaging Formats, including cups, food containers, and trays, are forecast to grow at a 5.45% CAGR through 2031 as delivery-led food consumption and quick-service channels keep expanding across urban markets. The UAE's second phase of Ministerial Decision No. 380 of 2022 came into force on January 1, 2026, covering plastic beverage cups, lids, cutlery, food containers, and plates that fiber-based substitutes can replace directly. That policy gives foodservice cartonboard the clearest direct regulatory pull of any packaging format in the region. Liquid packaging remains structurally steady because UHT dairy and aseptic juice formats still fit the Gulf's ambient distribution model better than chilled alternatives. At the same time, the Middle East and Africa cartonboard market stays exposed to imported specialty foodservice grades, which means logistics shocks can affect this fast-growing format faster than local demand alone would suggest.

By End-User Industry: Healthcare Upgrades A Food-Led Demand Base

Food represented 36.73% of regional value in 2025, making it the volume anchor for the Middle East and Africa cartonboard market share through packaged staples, processed foods, and halal-oriented retail lines. Food demand remains broad-based because modern retail expansion, inventory-building practices, and the need for longer shelf-life formats continue to support carton usage across many product categories. The segment is also moving toward better board specifications, as retailers and producers want stronger graphics, tamper evidence, cleaner food-contact positioning, and better shelf-ready presentation. That raises average value per tonne even when physical volume growth is moderate and price competition remains intense. Food therefore remains the base that stabilizes the Middle East and Africa cartonboard market while other end-user categories reshape the regional grade mix.

Pharmaceutical and healthcare packaging is set to grow at a 6.67% CAGR through 2031, making it the fastest-expanding end-user group and the clearest source of premiumization. Saudi Pharmaceutical Chemicals Company links its national primary packaging facility to lower import reliance and stronger local pharmaceutical manufacturing, which supports a broader ecosystem for regulated packs. Tobacco continues to require high-print-quality cartons even where unit volumes are mature or declining, which preserves a steady specification base for converters. Cosmetics and toiletries remain a high-value niche, especially in GCC markets where brand presentation and specialty finishes matter more than very large shipment volumes. The remaining uses, including toys, apparel, automotive, household goods, electrical products, and foodservice, add breadth to demand but are less central to the sustainability-led specification shift that is reshaping the Middle East and Africa cartonboard market.

Geography Analysis

Saudi Arabia held 33.27% of regional value in 2025, giving it the leading position in the Middle East and Africa cartonboard market because FMCG manufacturing, packaged food demand, and food processing investment are concentrated there. Its scale matters beyond domestic consumption, because national manufacturing expansion creates repeat carton demand across food, healthcare, personal care, and retail supply chains. The UAE plays a different role, acting as the region's premium converting and packaging development hub for cosmetics, luxury goods, and pharmaceutical packs. The UAE also moved the regulatory agenda forward when the second phase of its single-use plastic decision took effect in January 2026, which strengthens fiber-based packaging adoption in visible consumer applications.[3]Ministry of Climate Change and Environment, “Commencement of the Second Phase of Ministerial Decision No. 380 of 2022 on Single-Use Plastic Products,” Ministry of Climate Change and Environment, moccae.gov.ae Turkey remains important within the Middle East classification used here, since it combines sizable food processing capacity with meaningful cartonboard converting activity and export reach into Gulf markets.

South Africa is projected to grow at a 5.64% CAGR through 2031, which makes it the fastest-growing geography in the Middle East and Africa cartonboard market even though its supply position has become more import dependent. Demand is supported by modern retail expansion, agricultural export packaging, and its role as a distribution gateway into Sub-Saharan Africa. Egypt is also strengthening as a converting location because its large urban population and processed food base continue to widen local packaging demand. Nigeria has scale, but power constraints and currency stress keep converter economics harder than in the region's faster-developing packaging markets. Together, these patterns show that growth outside the Gulf is real, but it often depends on infrastructure quality as much as on end-user demand.

The rest of Africa, including Morocco, Kenya, Ghana, Ethiopia, and several smaller Sub-Saharan markets, represents an early-stage expansion tier for the Middle East and Africa cartonboard market. Morocco has built a more active paper and board manufacturing base, while several East and West African markets are still at a much earlier converting stage. In these markets, rising urban populations and low starting levels of packaged food consumption can support durable demand additions once formal retail deepens. The geographic mix therefore combines mature Gulf demand centers, emerging North African converting hubs, and a longer-term Sub-Saharan growth runway.

Competitive Landscape

The Middle East and Africa cartonboard market remains fragmented at the converting level, with regional leaders competing alongside many smaller operators that serve local FMCG and retail customers. That fragmented downstream picture sits beside a more concentrated upstream supply base, where imported board from major European and Scandinavian mills still shapes grade availability, procurement patterns, and pricing discipline. Mayr-Melnhof's 2 Middle Eastern packaging plants contributed around 2% of group sales and 6% of group adjusted EBITDA in 2025, which shows that even a limited regional footprint can matter financially when operating conditions tighten.[4]Mayr-Melnhof Karton AG, “Annual Results 2025,” Mayr-Melnhof Karton AG, mm.group The same company said in Q1 2026 that geopolitical tensions in the Middle East were putting noticeable pressure on energy, transportation, and chemicals, underscoring how external shocks pass through to local packagers. This structure keeps pricing intense in standard conversion work, while higher-value niches reward certification, print quality, dependable sourcing, and scale.

Hotpack Global completed a minority equity investment from Gulf Islamic Investments in May 2026 to support recently commissioned manufacturing capacity and a new specialized food packaging facility in Al Kharj, Saudi Arabia, which strengthens its position in local food packaging supply. United Carton Industries Company also approved a SAR 75.9 million (USD 20.24 million) expansion for Ras Al Khaimah Packaging Ltd., with construction starting in Q2 2026 and completion targeted for Q3 2027. These moves show how scale operators are investing closer to end demand instead of relying only on imported finished packaging. Emirates Printing Press represents another competitive path, since advanced inline cold-foil and digital finishing capabilities help it defend premium accounts that commodity converters cannot serve easily. Napco National's 2025 acquisition of Arabian Flexible Packaging also points to a broader regional push toward cross-selling and portfolio expansion around large multinational customer bases.

White-space opportunities are strongest in pharmaceutical secondary packaging, foodservice carton conversion, and certified sustainable solutions for export-oriented halal food producers. Billerud's Evolution program, a SEK 1.4 billion (USD 131 million) investment with SEK 400 million (USD 37 million) planned for 2026, is aimed at raising premium board capacity and could broaden future sourcing options for buyers looking beyond Europe's traditional supply base. The certification demands attached to regulated healthcare packs also protect incumbents with established quality systems from lower-cost entry in the most attractive niches. The Middle East and Africa cartonboard market therefore stays fragmented in conversion, but competitive advantage is becoming more concentrated around scale, technology, compliance, and sourcing resilience.

Middle East and Africa Cartonboard Industry Leaders

Mayr-Melnhof Karton AG

Stora Enso Oyj

Tetra Pak International S.A.

Metsä Board Corporation

Sappi Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Hotpack Global Holding completed a minority equity investment by GII (Gulf Islamic Investments), with proceeds allocated to scale up recently commissioned manufacturing capacity and to commission a new specialized food packaging facility in Al Kharj, Saudi Arabia, among the Kingdom's largest food packaging projects, backed by long-term supply agreements with major customers and aligned with Saudi Arabia's Vision 2030 industrial development goals.

- April 2026: Metsä Board Corporation reported comparable EBITDA of EUR 17 million (USD 18.7 million) for Q1 2026, noting that Middle East geopolitical tensions were adding pressure to logistics costs and certain raw material costs, with further impacts anticipated in subsequent quarters, while the company cited its high energy self-sufficiency as a competitiveness buffer during the period.

- January 2026: United Carton Industries Company (UCIC) board approved a SAR 75.9 million (USD 20.24 million) expansion project for its wholly owned UAE subsidiary Ras Al Khaimah Packaging Ltd., with construction commencing in Q2 2026 and targeted completion in Q3 2027, expanding UCIC's UAE production footprint and reinforcing its position in the GCC's second-largest packaging market.

Middle East and Africa Cartonboard Market Report Scope

The Middle East and Africa Cartonboard Market encompasses the production, distribution, and application of cartonboard materials for packaging. Key product grades in the market include Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board. These grades are used across various packaging formats, including folding cartons, liquid packaging, sleeves, trays, cups, and foodservice containers. Due to their recyclability, printability, and sustainable packaging attributes, these cartonboard solutions are widely used across sectors such as food, beverage, pharmaceuticals, tobacco, cosmetics, and more.

The Middle East and Africa Market is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, Other Packaging Formats), End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics, Other End-User Industries), and Geography (Saudi Arabia, United Arab Emirates, Turkey, Rest of Middle East, South Africa, Egypt, Nigeria, and Rest of Africa). The Market Forecasts are in Value (USD).

| Solid Bleached Board |

| Solid Unbleached Board |

| Folding Boxboard |

| White-Lined Chipboard |

| Liquid Packaging Board |

| Food Service Board |

| Folding Cartons |

| Liquid Packaging |

| Sleeve and Tray |

| Other Packaging Formats (Cups, Foodservice Containers) |

| Food |

| Beverage |

| Pharmaceutical and Healthcare |

| Tobacco |

| Cosmetics and Toiletries |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Product Grade | Solid Bleached Board | |

| Solid Unbleached Board | ||

| Folding Boxboard | ||

| White-Lined Chipboard | ||

| Liquid Packaging Board | ||

| Food Service Board | ||

| By Packaging Format | Folding Cartons | |

| Liquid Packaging | ||

| Sleeve and Tray | ||

| Other Packaging Formats (Cups, Foodservice Containers) | ||

| By End-User Industry | Food | |

| Beverage | ||

| Pharmaceutical and Healthcare | ||

| Tobacco | ||

| Cosmetics and Toiletries | ||

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) | ||

| By Geography | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the size of the Middle East and Africa cartonboard market in 2026?

The market is valued at USD 3.71 billion in 2026 and is projected to reach USD 4.58 billion by 2031, growing at a 4.30% CAGR over 2026 to 2031.

Which product grade leads cartonboard demand across the Middle East and Africa?

Folding Boxboard led the region in 2025 with a 38.00% share because it is widely used across food, pharmaceutical, and personal care secondary packaging.

Which end-user group is expanding the fastest in regional cartonboard demand?

Pharmaceutical and healthcare packaging is the fastest-growing end-user segment, with a 6.67% CAGR through 2031, supported by localization, compliance, and premium board needs.

Why are foodservice carton applications gaining momentum in the region?

Growth is being driven by delivery platforms, quick-service restaurant expansion, and the UAE's January 2026 plastic restrictions on cups, lids, cutlery, food containers, and plates.

Which country currently leads demand and which one is growing the fastest?

Saudi Arabia led regional value with 33.27% in 2025, while South Africa is forecast to post the fastest growth at a 5.64% CAGR through 2031.

What are the main risks affecting converter profitability in this sector?

The biggest pressures come from imported pulp and board price volatility, freight disruptions, limited recovered fiber systems, and infrastructure stress that raises production and sourcing costs.

Page last updated on: