Europe Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 31.86 Billion |

| Market Size (2026) | USD 32.32 Billion |

| Market Size (2031) | USD 36.77 Billion |

| Growth Rate (2026 - 2031) | 2.61% CAGR |

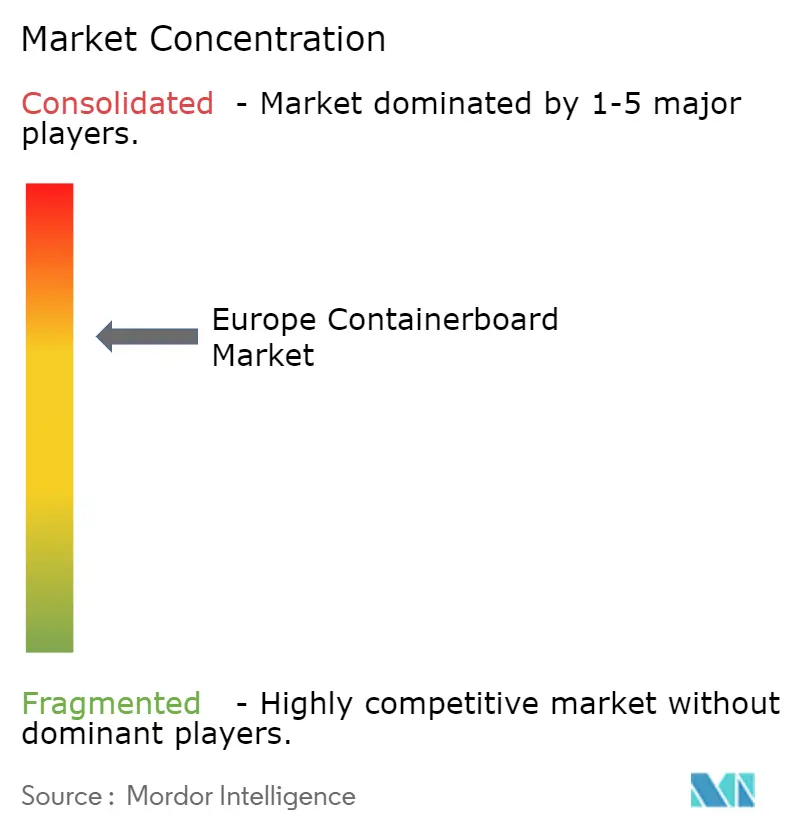

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Containerboard Market Analysis by Mordor Intelligence

The European containerboard market is projected to reach USD 31.86 billion in 2025, USD 32.32 billion in 2026, and USD 36.77 billion by 2031, growing at a CAGR of 2.61% from 2026 to 2031. The Europe containerboard market is entering this period amid policy changes, fiber substitution, logistics demand, and input-cost pressure, all of which are shaping purchasing and capacity decisions simultaneously. The PPWR is pushing producers and converters to align pack design with stricter recyclability rules, while brand owners continue to shift selected packaging formats away from plastics and toward fiber-based alternatives. E-commerce still supports box demand, but the requirement is no longer just higher volume, as converters are also being asked to deliver lighter, stronger, and more print-capable grades. Margin pressure remains uneven across the region because energy costs and recovered paper availability differ by country, affecting mill economics and pricing flexibility. Competitive strategy is therefore centered on vertical integration, specialty-grade development, recovered-fiber security, and footprint expansion into applications where service speed and performance consistency matter most.

Key Report Takeaways

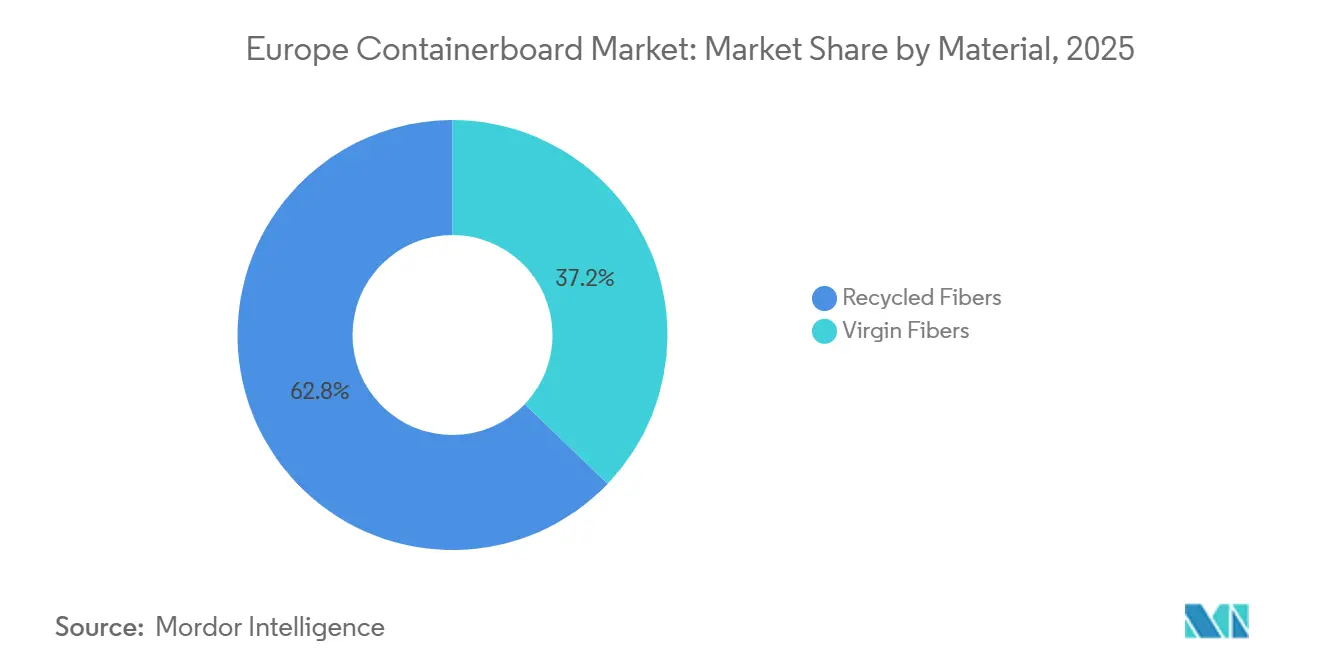

- By material, recycled fibers captured with 62.83% of the Europe containerboard market share in 2025.

- By product type, the Europe containerboard market size for flutings is projected to grow at a 4.17% CAGR to 2031.

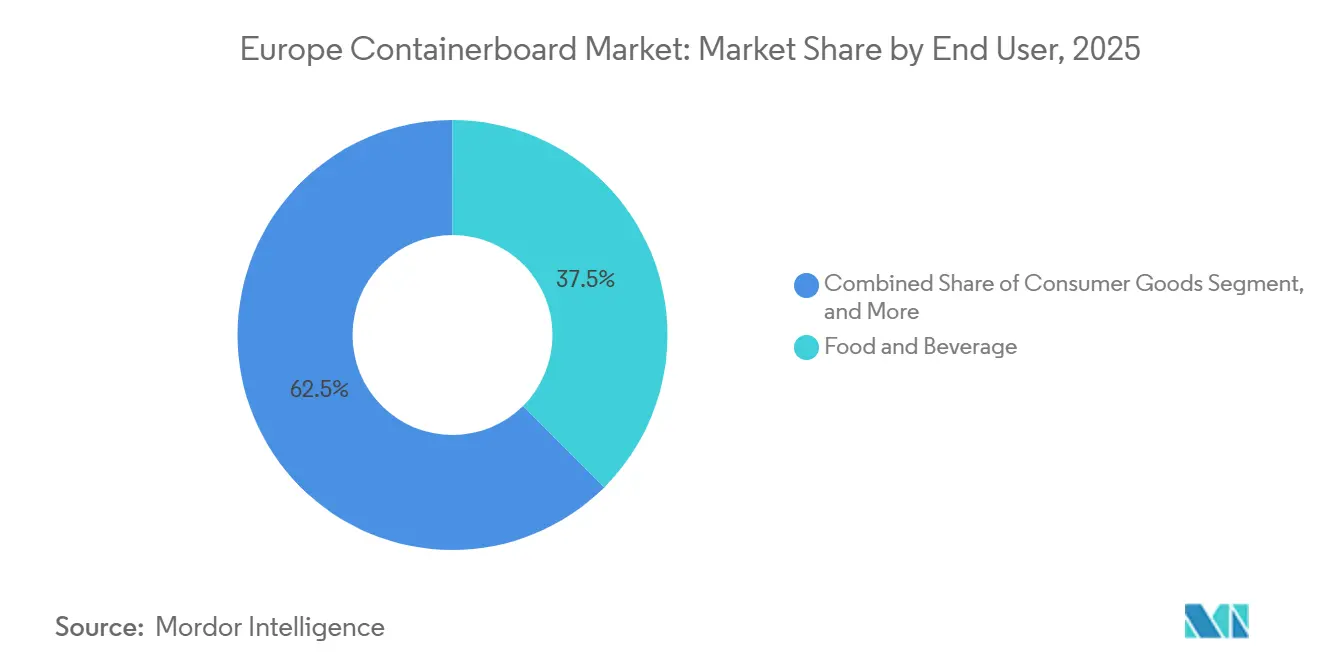

- By end user, the food and beverage industry accounted for 37.54% of the Europe containerboard market share in 2025.

- By geography, the Europe containerboard market in Spain is projected to grow at a 4.96% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in E-Commerce and Online Retail | +0.7% | Global, with concentrated impact in Germany, France, United Kingdom, and Benelux | Medium term (2-4 years) |

| Stringent Sustainability Regulations Favoring Recyclable Packaging | +0.5% | EU-wide, early compliance pressure in Germany, Netherlands, and Scandinavia | Short term (≤ 2 years) |

| Rising Demand for Shelf-Ready Packaging in Retail Chains | +0.4% | Western Europe, Germany, France, United Kingdom, spilling over to Southern and Eastern Europe | Medium term (2-4 years) |

| Increasing Substitution of Plastic with Paper-Based Packaging | +0.4% | EU-wide, most pronounced in food service applications in Germany, Italy, and Spain | Short term (≤ 2 years) |

| Expanding Cross-Border Fruit Export Corridors Requiring Humidity-Resistant Containerboard | +0.2% | Spain, Italy, the Netherlands, and Central and Eastern Europe | Long term (≥ 4 years) |

| Adoption of Digital Watermarking in Containerboard for Enhanced Sortation | +0.1% | EU core, Germany, Belgium, France, and Denmark leading early adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in E-Commerce and Online Retail

E-commerce continues to provide durable support for the Europe containerboard market, even though the pace now reflects a steadier logistics cycle rather than the earlier pandemic spike. The demand pattern is also changing because online retailers increasingly want right-sized boxes, stronger stacking performance, and better digital print-readiness rather than standard brown transit cases. That shift is important because it changes fiber mix and board specification, not only shipment volume. Germany already shows how this influence works in practice, with shipping packaging accounting for 6.7% of corrugated board revenue in 2024, even though its effect on quality standards extends well beyond that share. Early 2026 also opened with a better volume trend than many producers expected, which supports a more active restocking and packaging-conversion cycle in key markets. As a result, the Europe containerboard market is seeing demand shift toward lighter yet more capable board combinations that balance transport efficiency and brand presentation.

Stringent Sustainability Regulations Favoring Recyclable Packaging

Regulation is one of the clearest demand shapers for the Europe containerboard market, as the PPWR entered into force on February 11, 2025, and is scheduled to be broadly applied from August 12, 2026. The regulation requires all packaging placed on the EU market to be recyclable by 2030 and introduces a recyclability performance framework that will influence packaging choices across product categories. This creates a direct commercial advantage for fiber-based formats that already fit established collection and sorting systems better than many mixed-material packs. Italy provides a useful signal of readiness, as corrugated packaging recycling reached 92.5% in 2024, already above the EU's 2030 target of 85%. Germany also continued to report paper recovery rates above 90%, reinforcing the structural importance of recycled containerboard across the region. The Europe containerboard market therefore benefits not only from sustainability messaging, but also from a regulatory framework that increasingly rewards pack formats designed for high recovery and strong sorting outcomes.

Rising Demand for Shelf-Ready Packaging in Retail Chains

Shelf-ready packaging has moved into the mainstream across grocery retail, discount formats, and fast-turn e-commerce replenishment within the Europe containerboard market. Retailers now prefer tear-strip, easy-open, exact-fit corrugated trays that move directly from pallet to shelf, reducing labor and product handling. That shift rewards board grades with consistent printability, dimensional accuracy, and compression strength, because poor box performance quickly creates store-level inefficiency. Germany's food and beverage segment remained the largest end-use outlet for corrugated board in 2024, accounting for 43.10% of corrugated revenue, which shows why retail-led specification changes matter so much for producers. Italy is moving in a similar direction, as the food sector accounted for 62.7% of domestic corrugated output, keeping demand focused on dependable, presentation-ready transport formats. This is why the Europe containerboard market is seeing lighter board structures gain favor only when they still deliver the stiffness, print surface, and stacking reliability that modern shelf-ready applications require.

Increasing Substitution of Plastic with Paper-Based Packaging

Plastic substitution remains a direct demand driver for the Europe containerboard market because compliance pressure and brand commitments are now translating into active packaging redesign. The PPWR includes restrictions on selected single-use packaging formats from 2030, prompting companies to evaluate fiber-based alternatives earlier in the cycle. Fresh produce and food service are among the clearest application areas because they combine transport needs, moisture exposure, and visible consumer-facing sustainability goals. Mondi's 2026 collaboration with Pacapime Hungary shows how producers are positioning containerboard solutions for fruit and vegetable transit, where freshness protection and pack performance go hand in hand.[1]Mondi, “Pacapime Hungary and Mondi's Containerboard Are Keeping Fruit and Vegetables Fresh and Protected with High-Quality Packaging,” Mondi, mondigroup.com This is not a one-time replacement wave because each converted application creates follow-on demand for better coatings, better runnability, and more stable food-contact performance. The Europe containerboard market, therefore, benefits from substitution in both volume and value terms, especially when converters can meet moisture, safety, and branding requirements without reverting to plastic-based pack structures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Wastepaper Collection Rates and Prices | -0.5% | Europe-wide, sharpest in Italy, Germany, and the United Kingdom | Short term (≤ 2 years) |

| High Energy Costs in Europe's Paper Mills | -0.4% | Italy most exposed, also the Netherlands and Germany, while France and Scandinavia are better positioned | Medium term (2-4 years) |

| Growing Competition From Lightweight Microflute Solid Board | -0.2% | Western Europe, Germany, France, and the United Kingdom in consumer goods and cosmetics packaging | Long term (≥ 4 years) |

| Potential Supply Squeeze of Tall Oil Rosin Affecting Virgin Kraftliner Strength Additives | -0.1% | Finland, Sweden, and Germany are key virgin-fiber mill regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Wastepaper Collection Rates and Prices

Recovered-paper volatility remains the most immediate operating risk for the Europe containerboard market, especially for mills that rely fully on recycled fiber. In April 2025, OCC grades 1.04 and 1.05 rose by EUR 20-30 per ton (USD 22-33 per ton) across Europe as collection volumes weakened and export competition tightened supply. This pressure matters because recycled-fiber demand is being lifted by regulation at the same time that the feedstock base can tighten when consumer activity softens, or export demand improves. That mismatch creates a difficult margin structure for recycled containerboard producers, as higher raw-material costs do not always cleanly pass through to board pricing. It also explains why some mid-tier groups are seeking to secure asset collections and long-term feedstock channels rather than relying solely on open-market OCC purchases. The Europe containerboard market, therefore, faces a recurring tension in which circular-economy targets support demand, but the economics of collected fiber can still limit how profitably that demand is served.

High Energy Costs in Europe's Paper Mills

High energy costs continue to limit margin recovery in the Europe containerboard market because paper production remains highly exposed to electricity and process heat. The burden is not evenly distributed, which means mills in countries with weaker energy economics face a more persistent disadvantage even when demand conditions improve. Gas-dependent recycled containerboard mills are especially vulnerable because testliner and fluting production can absorb cost shocks faster than many end-use contracts can be repriced. Burgo Group's March 2026 renewable energy agreement shows how paper producers are trying to reduce that exposure by adopting a more controlled energy mix rather than relying solely on market-based purchasing.[2]Burgo Group, “Renewable Energy Agreement,” Burgo Group, burgo.com That cost gap has already encouraged operating-rate discipline, seasonal downtime, and greater caution around volume-led pricing decisions. Producers with cogeneration assets, biomass access, or stronger internal energy management are better positioned to defend margins, which is why decarbonization and power strategy now carry direct commercial importance in the Europe containerboard market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fiber Dominance Conceals a Structural Quality Gap

Recycled fibers held 62.83% of the Europe containerboard market share in 2025, reflecting the region's mature OCC collection systems, the policy premium on circularity, and the cost advantage recycled grades can retain when input conditions are stable. This leadership position is reinforced by the fact that Germany's corrugated board sector sourced more than 81.8% of its paper input from recycled fiber in 2024. The recycled-fiber base also aligns well with the direction of EU packaging policy, as it supports established recovery infrastructure and brand-owner sustainability targets. At the same time, the regional picture is not uniform, as Italy still relies heavily on higher-quality virgin grades for food-contact and export-oriented applications. That unevenness is important because it shows that the Europe containerboard market is not moving toward recycled content at the same pace or with the same performance trade-offs in every country.

Virgin fibers remain the smaller material segment, but they are forecast to grow at a 3.62% CAGR through 2031, as converters and brand owners still need performance certainty in moisture-sensitive, export, and food-grade applications. The issue is not only strength, because purity, barrier compatibility, and process consistency also matter where recycled input quality can vary from batch to batch. This creates a practical ceiling for recycled substitution in parts of the Europe containerboard industry, even as regulation continues to favor circular content. It also explains why producers continue to invest in premium kraftliner and hybrid solutions, even when product failure is more costly than a higher fiber bill. The Europe containerboard market will therefore keep a large recycled base, but growth in virgin-backed and performance-led grades will continue where reliability matters more than the lowest possible raw-material cost.

By Product Type: Kraftliner Scale Endures While Fluting Innovation Accelerates

Kraftliners accounted for 53.79% of the Europe containerboard market in 2025, confirming their entrenched role in heavy-duty packaging, food-contact formats, and higher-performance logistics chains. This position is supported by the need for dependable burst strength, stronger surfaces, and better conversion behavior in demanding applications. Testliners remain essential to the region's high-volume corrugated box system, especially where recycled content, cost control, and broad recyclability are the main purchasing priorities. Even so, the most dynamic change is occurring in fluting, which is forecast to grow at a 4.17% CAGR through 2031 as lightweight double-wall and shelf-ready structures gain wider acceptance. The product mix in the Europe containerboard market is therefore shifting toward smarter board combinations rather than a simple replacement of one grade family by another.

Fluting is advancing because converters are being asked to reduce board weight without sacrificing compression strength, stacking stability, or transport protection. That requirement is becoming more evident in the production logistics, shelf-ready retail packs, and e-commerce formats that must perform across both transit and presentation stages. Mondi's fresh-produce packaging collaboration in Central Europe reflects this direction, where containerboard is being engineered for stronger protection and operational efficiency in fruit and vegetable shipments. At the same time, kraftliner remains hard to fully displace in applications where wet strength, food safety, or a premium print appearance still justify a higher material cost. The Europe containerboard market is therefore seeing innovation concentrate in fluting design and board architecture, while kraftliner continues to anchor the upper end of the performance curve.

By End User: Food And Beverage Anchors Volume While Industrial Applications Grow Faster

Food and beverage accounted for 37.54% of the Europe containerboard market in 2025, making it the largest end-use segment across the region. Its strength comes from steady demand across fresh produce, processed foods, beverages, and food service, which keeps box consumption tied to essential goods rather than discretionary spending alone. Germany illustrates this anchor role clearly, as food and beverages accounted for 43.10% of corrugated board revenue in 2024. Italy points in the same direction, with the food sector accounting for 62.7% of domestic corrugated output, led by fresh produce, processed foods, and beverages. This concentration matters because it keeps the Europe containerboard market closely linked to supply chains that require hygiene, print quality, moisture control, and dependable delivery timing.

Consumer goods remain another important demand pool, supported by health and beauty, household care, and e-commerce-led retail formats that increasingly require better graphics and lighter, more tailored boxes. The industrial segment is smaller today but is forecast to grow at the fastest pace, with a 4.45% CAGR through 2031. That growth is tied to nearshoring, machinery movement, durable goods transit, and export packaging requirements that rely on stronger multi-wall constructions. The Europe containerboard market, therefore, combines a defensive food-led base with an industrial growth pocket that benefits when manufacturing activity moves closer to Europe consumption centers. This balance helps explain why producers are trying to serve both high-volume staple demand and specialized, heavy-duty packaging applications simultaneously.

Geography Analysis

Germany held 21.17% of the Europe containerboard market share in 2025, making it the largest country market in the region. Its position rests on the scale of its export-oriented manufacturing base and the density of its corrugated converting network, which together create broad and diversified box demand. Germany's corrugated board capacity utilization averaged 81.3% in 2024, 7.8% points below the long-term average, suggesting persistent overcapacity in parts of the system. Germany also retained a strategic advantage in recycling, with corrugated board recycling reaching 95.3% in 2024, which supports stable demand for recycled testliner and other circular grades. France and Spain remain important Western European markets, but Germany still shapes regional pricing, grade mix, and investment more than any other single country.

Italy presents a more mixed picture in the Europe containerboard market. Corrugated production recovered to 7.9 billion m² in 2024, up 2.8% year over year, which showed that food-linked packaging demand remained resilient after two weaker years. The market also benefits from a large food sector and a growing e-commerce channel, but its mills face greater cost pressures than several regional peers, limiting operating flexibility. The United Kingdom adds another challenge, as post-Brexit packaging trade now faces greater administrative and logistical complexity, making pricing recovery harder and strengthening the case for capacity rationalization.

Spain is forecast to be the fastest-growing country segment in the Europe containerboard market, with a 4.96% CAGR through 2031. The driver is a combination of import substitution, domestic e-commerce development, and a packaging system that is increasingly self-directed following the post-2022 break from earlier Europe supply patterns. Food and beverage still provides the volume base there, while online retail is shaping the most dynamic incremental demand. Beyond Spain, Central and Eastern Europe, including Poland, Hungary, Austria, the Czech Republic, and the Benelux countries, offers stronger growth potential than the mature Western core because nearshoring is pulling packaging-intensive manufacturing closer to EU borders. The Europe containerboard market, therefore, combines a slower but larger Western base with faster expansion corridors in the east, and that geographic split is becoming more relevant for investment and asset-allocation decisions.

Competitive Landscape

The Europe containerboard market shows moderate-to-high consolidation at the producer level, even though corrugated converting remains more fragmented. Smurfit Westrock stands as the strongest pan-Europe integrated player following the July 2024 merger of Smurfit Kappa and WestRock, and the combined group reported EUR 10.86 billion (USD 11.7 billion) in net sales in EMEA and APAC in 2025. In Q1 2026, its EMEA and APAC segments delivered USD 421 million in adjusted EBITDA, with a 15.2% margin, underscoring the earnings benefits of scale and vertical integration.[3]Smurfit Westrock plc, “Smurfit Westrock Reports First Quarter 2026 Results,” Business Wire, businesswire.com That breadth, which spans containerboard production, corrugated conversion, and retail-facing design, reduces the pricing room available to smaller independent converters. The European containerboard market is therefore increasingly shaped by groups that can combine fiber access, plant efficiency, geographic reach, and customer service under one operating model.

Mid-tier companies such as SAICA Group, VPK Packaging Group NV, and Hamburger Containerboard are responding by expanding their footprints, integrating backward into recovered paper collection, and focusing on specialty applications that large systems do not always serve as efficiently. Mondi has followed an organic investment route, using the Duino recycled containerboard project and the Świecie kraftliner expansion to improve grade mix, regional supply coverage, and quality positioning. International Paper's acquisition of DS Smith also adds another large integrated competitor with meaningful corrugated capabilities in Europe. The Europe containerboard market rewards these strategies because fiber security, asset location, and application focus are becoming more decisive than simple installed tonnage.

There is still room for smaller specialists in humidity-resistant fluting, digital-print-ready white testliner, and lightweight double-wall formats for shelf-ready packaging. These areas matter because customers often value fast development cycles, local technical support, and reliable response times as much as scale. Digital watermarking may also strengthen differentiated pack design over time, since industrial trials under HolyGrail 2.0 showed that technology can improve performance in real packaging environments. Strategic moves since 2025 have included Smurfit Westrock's asset rationalization, SAICA's push to secure recovered-paper collection, and producer investment in energy resilience, including Burgo Group's renewable energy agreement announced in March 2026.[4]SAICA, “SAICA's push to secure recovered paper,” Saica.com The Europe containerboard market is concentrated enough for scale to matter, but still open enough for regional challengers to win in niches where speed, specialization, and closer customer support carry clear value.

Europe Containerboard Industry Leaders

Smurfit Westrock plc

International Paper Company

Stora Enso Oyj

Mayr-Melnhof Karton AG

Huhtamäki Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Smurfit Westrock is reviewing its London Stock Exchange listing, expected to conclude in May 2026, as part of a strategy to reduce administrative complexity while retaining its primary NYSE listing.

- March 2026: Burgo Group strengthened its energy strategy with a new renewable energy agreement announced on March 31, 2026, as part of its decarbonization plan involving increased biomethane use and cogeneration system renewals.

- March 2025: Sonoco Products Company announced a EUR 60 per tonne (USD 64.8 per tonne) price increase for all grades of core board and paperboard in Europe, effective April 7, 2025, citing OCC shortages and elevated energy costs across Europe.

- March 2025: Spain's Ministry of Industry and Tourism granted EUR 32.7 million (USD 34.6 million) to SAICA for a decarbonization project at its El Burgo de Ebro plant. The total investment for the project reached EUR 101.5 million (USD 107.3 million), with an expectation to generate 440 jobs.

Europe Containerboard Market Report Scope

The scope of this report covers the Europe Containerboard Market, which includes the analysis of market trends, growth drivers, challenges, and opportunities. Containerboard is the material used to produce corrugated boxes, primarily consisting of linerboard and corrugating medium. The study examines market dynamics, the supply chain, and the competitive landscape, providing insights into the industry's current state and future outlook.

The Europe Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Type (Kraftliners, Testliners, and Flutings), End User (Food and Beverage, Consumer Goods, Industrial, and More), and Geography (Germany, France, Italy, Spain, United Kingdom, Russia, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End Users |

| Germany |

| France |

| Italy |

| Spain |

| United Kingdom |

| Russia |

| Rest of Europe |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End User | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End Users | |

| By Geography | Germany |

| France | |

| Italy | |

| Spain | |

| United Kingdom | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current size and forecast for the Europe containerboard market?

The Europe containerboard market was valued at USD 31.86 billion in 2025, entered 2026 at USD 32.32 billion, and is forecast to reach USD 36.77 billion by 2031 at a 2.61% CAGR.

Which material segment leads to demand across Europe?

Recycled fibers led with a 62.83% share in 2025, supported by strong OCC collection systems and policy support for circular packaging.

Which product type is growing the fastest in containerboard?

Flutings are forecast to expand at a 4.17% CAGR through 2031 as lightweight double-wall and shelf-ready packaging formats gain wider use.

Which end-use sector contributes the most volume?

Food and beverage was the largest end user in 2025 with a 37.54% share, supported by steady demand from fresh produce, processed foods, beverages, and food service.

Which country is the largest contributor in Europe?

Germany led with a 21.17% share in 2025 due to its export-oriented industrial base, a dense corrugated converting network, and strong recycling infrastructure.

Where is the fastest country-level growth expected through 2031?

Spain is projected to record the fastest growth at a 4.96% CAGR, supported by import substitution and the continued build-out of domestic e-commerce packaging demand.

Page last updated on: