Ghana Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 54.52 Million |

| Market Size (2026) | USD 56.12 Million |

| Market Size (2031) | USD 64.23 Million |

| Growth Rate (2026 - 2031) | 2.74% CAGR |

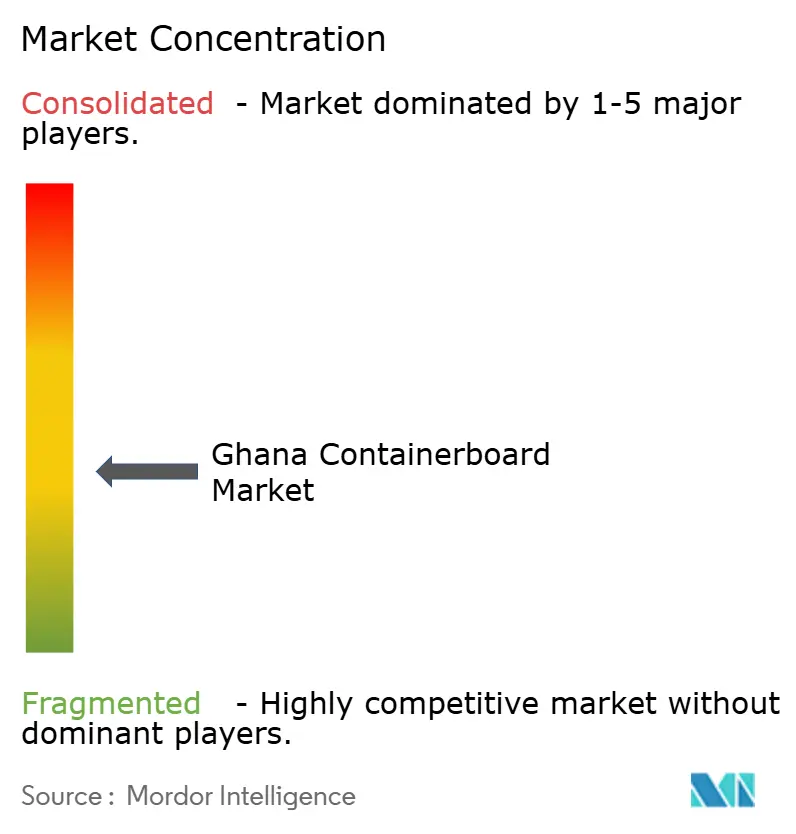

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ghana Containerboard Market Analysis by Mordor Intelligence

The Ghana Containerboard Market size is projected to expand from USD 54.52 million in 2025 and USD 56.12 million in 2026 to USD 64.23 million by 2031, registering a CAGR of 2.74% between 2026 to 2031.

The Ghana containerboard market remains structurally tied to imports because domestic converters still depend on base paper sourced from Asian, European, and South African mills, which keeps conversion margins sensitive to currency swings and freight cycles. Demand has held up better than supply conditions because food, beverage, and broader FMCG packaging needs continued to rise in 2025, which supported corrugated secondary packaging across both formal retail and informal trade channels. That mix of firmer consumption and elevated landed input costs explains why the Ghana containerboard market is growing, yet still faces margin pressure rather than demand weakness. The market is also moving toward a more quality-sensitive mix as export packaging, industrial transit boxes, and compliance-linked packaging specifications gain more weight alongside traditional domestic retail demand. Competition is moderate, with local converters defending speed and customer relationships while imported board and finished corrugated solutions remain a persistent check on local capacity expansion, and the clearest opportunities sit in recyclable paper substitution, export-grade packaging, and policy support around input duties.

Key Report Takeaways

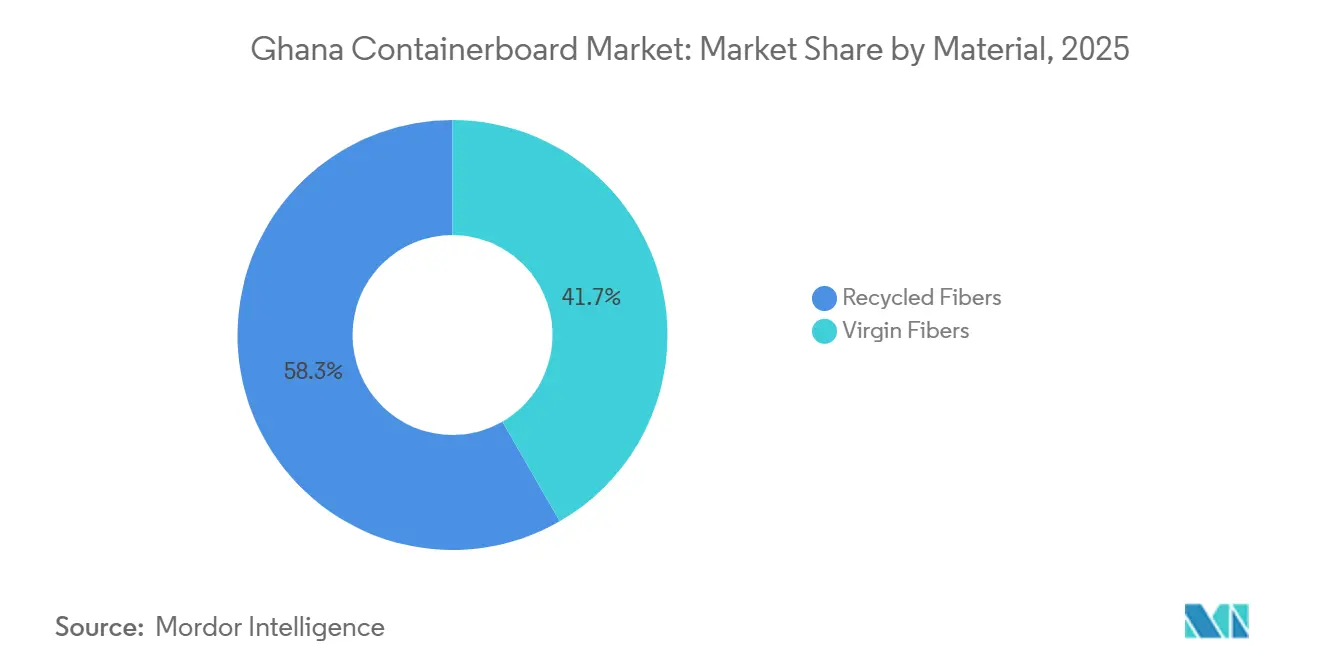

- By material, recycled fibers held 58.32% of the Ghana containerboard market share in 2025, while virgin fibers are forecast to record the fastest growth at a 4.41% CAGR through 2031.

- By product type, kraftliners accounted for 46.43% of the Ghana containerboard market size in 2025, while flutings are projected to advance at a 4.32% CAGR during 2026-2031.

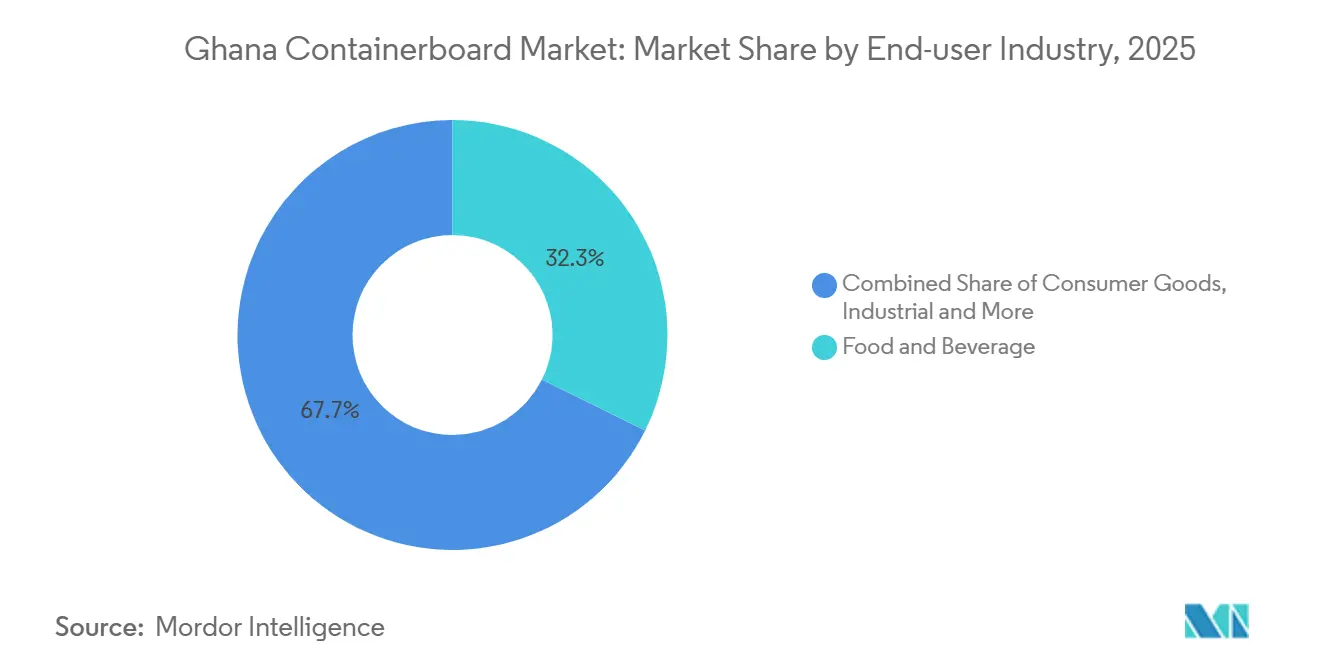

- By end-user industry, food and beverage captured a 32.32% share in 2025, while industrial is set to expand at the highest CAGR of 3.68% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Ghana Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Food and Beverage Packaging Consumption | +0.8% | National, concentrated in Greater Accra, Ashanti, and Central regions | Short term (≤ 2 years) |

| Expanding Trade and Export Packaging Demand | +0.6% | National, with early export-corridor gains in Tema and Takoradi | Medium term (2-4 years) |

| Greater Shift Toward Recyclable Paper-Based Packaging | +0.4% | National, with strongest regulatory influence in urban commercial zones | Medium term (2-4 years) |

| Industrial and Logistics Activity Supporting Corrugated Demand | +0.3% | National, concentrated in free zones and industrial corridors near Tema | Medium term (2-4 years) |

| Styrofoam Phase-Out Accelerating Paper Substitution | +0.3% | National, across food-service and retail distribution channels | Short term (≤ 2 years) |

| EU Packaging Compliance Pressure Lifting Export-Grade Box Demand | +0.2% | Export-oriented zones, spill-over to domestic producers supplying agri-food exporters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Food and Beverage Packaging Consumption

Ghana’s food and beverage manufacturing base delivered the strongest demand signal for the Ghana containerboard market in 2025 because packaged goods volumes rose across everyday consumption categories. FMCG volume sales increased 13.7% year over year in 2025, while food categories alone recorded an 18.9% volume increase and contributed 74.4% of the total volume gain. The same report showed that value sales rose 41.8%, which suggests producers moved into higher-value packaged formats and needed stronger secondary packaging for transport and shelf handling. That matters for the Ghana containerboard market because secondary packaging specifications are improving faster than shipment volumes, which favors higher-basis-weight board grades over lighter constructions in many food and beverage applications. As consumption conditions stabilize further in 2026, the Ghana containerboard market is likely to keep drawing support from routine packaged food distribution across modern trade and informal retail channels.

Expanding Trade and Export Packaging Demand

Export growth is widening the addressable demand base for the Ghana containerboard market beyond domestic retail packaging and into more specification-heavy transit packaging.[1]Ghana Export Promotion Authority, “Ghana's Non-Traditional Exports Hit USD 5 Billion in 2025, Up 30.7%,” Ghana News Agency, gna.org.gh Ghana’s non-traditional exports reached USD 5.0069 billion in 2025, up 30.7% from USD 3.83 billion in 2024. Processed and semi-processed goods contributed USD 3.09 billion, which was a 52.78% increase, and Europe absorbed USD 2.29 billion of total non-traditional export earnings after a 55.34% rise. Every additional flow of horticultural produce, cocoa derivatives, and processed food into export channels raises the need for corrugated cases that can meet stacking, handling, and destination-market documentation requirements. This keeps the Ghana containerboard market closely tied to trade growth, and it also shifts a greater share of future demand toward board grades that can serve export packers with consistent strength and traceability.

Greater Shift Toward Recyclable Paper-Based Packaging

The regulatory direction in Ghana is moving packaging demand toward paper-based formats, which gives the Ghana containerboard market a structural tailwind beyond normal volume growth.[2]Ministry of Environment, Natural Resources and FRESHPPACT, “MENR, FRESHPPACT Launch Roadmap to Ditch Plastics,” Citi Newsroom, citinewsroom.com In April 2025, the Ministry of Environment, Natural Resources and the FRESHPPACT coalition launched a plastic-alternatives policy roadmap in Accra, described as the first of its kind in West Africa. The push toward extended producer responsibility and better end-of-life management makes corrugated packaging more attractive in secondary and tertiary applications because it fits more easily into recycling and recovery systems than many multilayer plastic formats. Royal Crown Ghana Limited has also promoted corrugated packaging as a practical route to meet environmental and standards expectations, which shows that market participants are already adjusting product positioning before the full regulatory framework is finalized. As these policy changes move from roadmap to enforcement, the Ghana containerboard market is likely to benefit from substitution demand even if broader economic conditions stay uneven.

Industrial and Logistics Activity Supporting Corrugated Demand

Industrial expansion is adding a different layer of demand to the Ghana containerboard market because manufacturing and logistics users need heavier transit packaging than routine retail channels. Ghana’s Trade Minister stated in April 2026 that the country must lead AfCFTA implementation, and that position supports continued attention on agro-processing zones, light manufacturing, and export corridors. The AfCFTA Secretariat’s May 2026 implementation partnership with Rendeavour adds to that direction by linking industrialization plans with special economic zones and logistics development. Ghana also recorded higher imports than exports within the AfCFTA preferential trading system in early 2026, which reinforces the policy push to expand domestic manufacturing capacity and with it the need for industrial corrugated packaging. This matters for the Ghana containerboard market because bulk bins, component shippers, and warehouse-ready boxes use more board per shipment and can support steadier plant utilization than fragmented consumer goods orders.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Import Dependence and Foreign Exchange Exposure | -0.5% | National, most acute for converters in Greater Accra and Kumasi | Short term (≤ 2 years) |

| Port and Freight Volatility Disrupting Input Costs | -0.4% | National, concentrated at Tema Port as primary containerboard import gateway | Short term (≤ 2 years) |

| 20% Cardboard Raw-Material Duty Weakening Local Conversion Economics | -0.3% | National, affects all converters importing parent rolls classified as finished goods | Medium term (2-4 years) |

| Power and Water Tariff Escalation Raising Conversion Costs | -0.2% | National, concentrated in energy-intensive paper conversion and corrugation facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Import Dependence and Foreign Exchange Exposure

Raw material dependence remains the most persistent constraint on the Ghana containerboard market because the country still lacks domestic pulp and base-paper manufacturing capacity. Ghana Revenue Authority tariff schedules place certain finished and semi-finished cardboard materials in a 20% duty band, which adds a structural cost layer to imported board and limits the ability of converters to offset pressure through operating efficiency alone. Utility tariff reviews also kept exchange-rate exposure visible through 2025 and into 2026, which shows how currency movements flow directly into conversion economics in paper packaging. This weakens long-term contracting because large packaging buyers prefer stable delivered costs, while converters hesitate to commit to capacity upgrades when imported input prices can reset quickly after currency moves. As a result, the Ghana containerboard market continues to expand in demand terms, but profitability and investment timing remain exposed to the cedi and to landed board prices.

Port and Freight Volatility Disrupting Input Costs

Port-side disruption remains a direct operating risk for the Ghana containerboard market because most parent rolls enter through imported freight channels tied to Tema. Early-2025 congestion at Tema Port disrupted discharge schedules and increased demurrage exposure for manufacturers and importers, which pushed cost volatility well beyond the headline ocean freight rate. The Ghana Shippers’ Authority imposed an interim cap of GH¢720 per TEU on container administrative charges in May 2026, and the need for that intervention itself shows how unstable logistics charges had become for import-dependent supply chains. For converters, this means landed input costs can change materially even when mill prices remain steady because port fees, delays, and handling costs all sit between procurement and production. That makes working capital discipline almost as important as sourcing strategy in the Ghana containerboard market, especially for firms serving customers that expect short lead times and stable quoted prices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled-Fiber Supply Chain Evolves Toward Quality-Graded Sourcing

Recycled fibers held a 58.32% share of the Ghana containerboard market in 2025, which reflects the clear cost advantage of recovered paper sourcing over fully imported virgin pulp. Local converters have long relied on recycled inputs for medium and testliner applications, while the standards environment has not yet imposed recycled-content verification requirements strict enough to displace that model at scale. Even so, virgin fibers are the fastest-growing material segment at a 4.41% CAGR through 2031 because export-grade boxes increasingly need better burst strength, compression performance, and documentation than recycled constructions usually provide. The EU packaging and packaging waste regulation applies from August 12, 2026, and its emphasis on recyclability and traceability strengthens the case for certified virgin-fiber supply in export-facing applications.

That shift does not mean recycled grades are losing their relevance inside the Ghana containerboard industry, because the domestic FMCG and trade channel still buys on cost more than on premium specification. Ghana’s non-traditional export earnings rose to USD 5.0069 billion in 2025, and processed as well as semi-processed goods accounted for USD 3.09 billion of that total, which expands the customer base for stronger export corrugated packaging. Europe absorbed USD 2.29 billion of those export earnings, which keeps documentation and compliance requirements highly relevant for converters serving exporters. Recycled board therefore remains the mass-market option for local distribution, while virgin-fiber kraftliners are gaining weight in higher-value export use cases that need more predictable performance. In practical terms, the Ghana containerboard market is moving toward a layered material mix where cost-led domestic demand and compliance-led export demand coexist rather than replace one another.

By Product Type: Kraftliners Drive Volume as Flutings Capture Incremental Growth

Kraftliners accounted for 46.43% of the Ghana containerboard market size in 2025, which shows how central outer-liner strength remains for export cases and heavier transit packaging. That position is supported by Ghana’s cocoa, horticulture, and processed-food flows, where cartons must hold shape through inland transport, warehousing, and maritime shipment. Testliners remained the second major product group because they offer a lower-cost option for domestic secondary packaging where price still outweighs premium strength in many customer accounts. Against that stable base, flutings are projected to expand at a 4.32% CAGR through 2031 as overall box output rises across food manufacturing, logistics, and industrial handling. The Ghana containerboard market is therefore seeing its fastest product growth in the board grade that scales most directly with total corrugated production volumes rather than with any one export niche.

This pattern also fits the country’s broader economic direction because fluting demand grows every time manufacturers and distributors add more corrugated boxes to routine product movement. Ghana’s trade and industrial policy focus under AfCFTA supports more warehousing, assembly, and processing activity, which naturally raises the need for corrugated structures used in storage, shipping, and retail-ready handling. That matters because fluting is required across board constructions, whether the facing liner is premium kraft or lower-cost testliner. Kraftliners should continue to anchor value in the Ghana containerboard market, but flutings are likely to capture a larger share of incremental volume as industrial shipments and logistics-linked corrugated usage expand. This keeps product competition centered on balancing strength, cost, and availability rather than on a simple shift away from any single board grade.

By End-User Industry: Food and Beverage Anchors Volume While Industrial Gains the Fastest Pace

Food and beverage held a 32.32% share of the Ghana containerboard market in 2025, which confirms its role as the main volume anchor across both domestic distribution and export packaging. FMCG volume sales rose 13.7% in 2025, and that same improvement translated into higher corrugated demand across packaged food, soft drinks, and other fast-moving consumer categories. Consumer goods remained the next broad demand pool, supported by packaged home care, personal care, and general retail products that continue to move through growing distribution networks. Even so, the industrial segment is projected to grow the fastest at a 3.68% CAGR through 2031 because manufacturing and logistics activity is becoming a more important source of corrugated demand than it was in the past. That shift broadens the Ghana containerboard market beyond its historical reliance on everyday consumer packaging and gives converters a larger base of heavier-duty applications to serve.

The difference between these end users matters because industrial contracts tend to be larger, steadier, and less fragmented than FMCG box orders. Ghana’s policy push around AfCFTA implementation continues to support agro-processing and light manufacturing corridors, which should raise demand for component shippers, bulk bins, and warehouse transit packaging. Ghana also recorded a GH¢47.2 billion trade surplus in Q4 2025, driven by strong gold and cocoa exports, and that export strength indirectly supports industrial corrugated use around processing, intermediate handling, and supply movement. Food and beverage will remain the base-load user for the Ghana containerboard market, but industrial packaging is likely to carry more of the growth burden over the forecast period. Other end-user industries such as pharmaceuticals, agricultural inputs, and e-commerce fulfillment still represent a smaller pool, yet they add steady incremental demand as formal distribution systems continue to deepen.

Geography Analysis

The Ghana containerboard market is a single-country market, but demand and conversion activity remain concentrated in a few corridors rather than spread evenly across the country. Greater Accra and Tema form the core zone because food processing, retail distribution, and import logistics are clustered there, which makes that corridor the operational center of board sourcing and corrugated box conversion. This concentration also means that logistics conditions around Tema have an outsized effect on the Ghana containerboard market because imported parent rolls and related packaging inputs move through that axis before reaching converters nationwide. Ashanti, led by Kumasi, represents the next major demand pocket because it serves domestic staples distribution, cocoa-linked trade, and light industrial activity across inland commercial routes. Takoradi and the Western Region are smaller in absolute volume, yet they still matter because industrial cargo, export handling, and energy-linked activity create recurring needs for transit and protective corrugated packaging.

The country’s geography also matters at a regional policy level because Ghana’s role as host of the AfCFTA Secretariat gives packaging demand a stronger industrial and trade dimension than simple domestic consumption figures would suggest. The Trade Minister stated in April 2026 that Ghana must lead the AfCFTA success story, which supports continued focus on export competitiveness, special economic zones, and industrial scaling. The AfCFTA Secretariat’s implementation partnership with Rendeavour in May 2026 reinforced that direction by linking industrialization to logistics corridors and production hubs. In that setting, the Ghana containerboard market is shaped not only by where consumption sits today, but also by where future manufacturing and export corridors are being built.

Export geography adds a second layer to the demand picture because external destination markets influence box quality requirements inside Ghana. Ghana’s non-traditional export earnings reached USD 5.0069 billion in 2025, and Europe accounted for USD 2.29 billion of that total, which makes Europe the most important external demand signal for higher-specification corrugated packaging.[3]Ghana Export Promotion Authority, “Ghana's Non-Traditional Exports Hit USD 5 Billion in 2025, Up 30.7%,” Ghana News Agency, gna.org.gh That trade mix keeps horticulture, cocoa derivatives, and processed food at the center of export packaging demand because these products need strong and compliant boxes for long-distance shipment. Calls for a roadmap to align Ghana’s packaging regulations with EU standards ahead of tighter enforcement raise the practical relevance of traceable and recyclable corrugated packaging for export users. This means the geographic profile of the Ghana containerboard market extends beyond domestic regions and into destination-market requirements, especially where EU compliance standards influence local board selection and converter sourcing. For suppliers that can meet those expectations, export geography will remain one of the clearest routes to value growth even if domestic pricing stays tight.

Competitive Landscape

The Ghana containerboard market has a moderately fragmented structure at the converter level, with domestic companies such as Royal Crown Ghana Limited, G-Pak Limited, Ghana Carton Boxes Manufacturing Company Limited, Wordsworthy Press and Packaging Ltd., and Athera Company Limited serving food, consumer goods, and agricultural packaging demand. These firms mostly operate as converters rather than integrated board producers, so they remain dependent on imported parent rolls for corrugating, cutting, and printing. That dependence is the main structural weakness in the competitive landscape because a weaker cedi or a change in landed board prices flows quickly into margins and pricing decisions. Local players therefore compete more on lead time, customization, and customer familiarity than on a raw cost edge. The Ghana containerboard market also faces pressure from imported finished corrugated products and imported board, while tariff classifications on certain cardboard materials do not fully shield local conversion economics from that competition.

Competitive differentiation is increasingly tied to sustainability credentials and export-compliance capability rather than simple domestic cost positioning. Companies that can align with Ghana Standards Authority labeling expectations and with the documentation needs of export packers are better placed to secure higher-value orders than converters focused only on short-run local supply. Smurfit Westrock reported improved EMEA and APAC demand in Q1 2026 and said containerboard prices increased during March and April 2026, which shows that global producers supplying African markets still have strong pricing influence.[4]Smurfit Westrock plc, “Smurfit Westrock Reports First Quarter 2026 Results,” Smurfit Westrock Newsroom, smurfitwestrock.com Mondi reported stronger corrugated packaging and flexible packaging sales volumes in its Q1 2026 trading update and had already completed a EUR 1.2 billion, USD 1.28 billion, capacity expansion across corrugated and flexible packaging operations, which strengthens its ability to serve import-driven markets through a broader supply footprint. Mpact’s FY2025 revenue rose 5% to ZAR 14 billion, USD 757 million, and the company reported solid volume gains in containerboard and agricultural packaging, which confirms that regional suppliers remain relevant to West African packaging chains even when they are not physically based in Ghana.

Recent corporate actions also show how external supply developments can reshape local competition inside the Ghana containerboard market. Mondi confirmed plant closures across parts of its European packaging network as part of footprint optimization, which may change how supply is routed into African markets over time. Mpact confirmed the closure of its Springs paper mill after the loss of a key customer to imported board, which highlights how global oversupply can make imports more competitive in regional markets and keep pressure on local conversion investment. The open space in this market remains a fully integrated domestic model that combines waste-paper collection, testliner production, and corrugated conversion, because that would reduce foreign exchange exposure and improve supply control. Until such a model emerges, competition in Ghana will continue to revolve around imported board access, service reliability, and the ability to meet stricter export and sustainability requirements.

Ghana Containerboard Industry Leaders

Royal Crown Ghana Limited

Wordsworthy Press & Packaging Ltd.

G-Pak Limited

Ghana Carton Boxes Mfg. Co. Ltd.

Snew Plastics & More Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Ghana's Environmental Protection Authority announced a nationwide ban on the production, importation, distribution, sale, and use of all expanded polystyrene foam products, effective January 1, 2027, covering food packaging containers, takeaway packs, disposable cups, and foam cushioning materials. The ban is the most significant single regulatory event for the containerboard market in recent history, as it directly redirects food-service and food-retail packaging demand toward paper-based corrugated and folded alternatives, expanding the addressable corrugated demand pool substantially.

- April 2026: Smurfit Westrock plc reported improved EMEA and APAC demand in Q1 2026, with containerboard prices increasing during March and April 2026 as a result of higher energy costs and strengthening demand. The company indicated that its corrugated business will implement the containerboard price increase in the second half of 2026 following the customary time lag, which is likely to lift import landed costs for Ghanaian converters sourcing from European and South African mill suppliers in H2 2026.

- April 2026: Ghana's non-traditional exports reached USD 5.0069 billion in 2025, a 30.7% increase over USD 3.83 billion in 2024, with processed and semi-processed goods rising 52.78% to USD 3.09 billion. Europe absorbed USD 2.29 billion of total NTE earnings, rising 55.34%, underscoring the intensifying demand for export-grade corrugated packaging compliant with EU recyclability and traceability requirements ahead of PPWR's August 2026 enforcement date.

Ghana Containerboard Market Report Scope

The Ghana Containerboard Market encompasses the production, distribution, and consumption of containerboard used in the manufacture of corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The market is driven by the increasing demand for sustainable, lightweight, and durable packaging solutions.

The Ghana Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current and forecast value of Ghana containerboard demand?

The Ghana containerboard market size stood at USD 54.52 million in 2025, rises to USD 56.12 million in 2026, and is projected to reach USD 64.23 million by 2031 at a 2.74% CAGR.

Which material type leads containerboard use in Ghana?

Recycled fibers led with a 58.32% share in 2025 because they offer a cost advantage for domestic converters compared with fully imported virgin pulp.

Which product type is growing fastest in Ghana containerboard applications?

Flutings are the fastest-growing product type, with a projected 4.32% CAGR from 2026 to 2031, as box output rises across logistics, food manufacturing, and industrial handling.

Which end-user group drives the most demand for corrugated board in Ghana?

Food and beverage remains the largest end-user, with a 32.32% share in 2025, supported by higher packaged food and beverage volumes across domestic and export channels.

What are the main risks affecting converter margins in Ghana?

The main risks are import dependence, foreign exchange exposure, port and freight volatility, tariff-related input costs, and utility price changes that directly affect conversion economics.

Why are export markets becoming more important for board suppliers in Ghana?

Export flows are pushing demand toward stronger and more traceable packaging, especially after Ghana’s non-traditional exports reached USD 5.0069 billion in 2025 and Europe absorbed USD 2.29 billion of that total.

Page last updated on: