United Arab Emirates Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

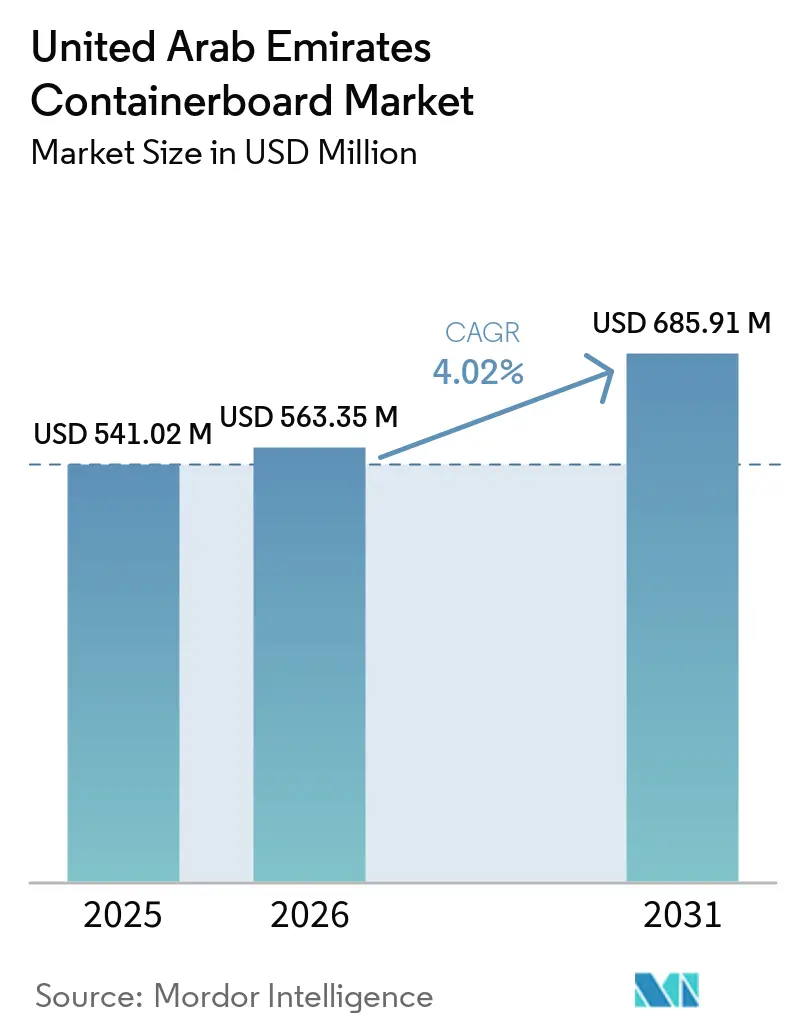

| Base Year Market Size (2025) | USD 541.02 Million |

| Market Size (2026) | USD 563.35 Million |

| Market Size (2031) | USD 685.91 Million |

| Growth Rate (2026 - 2031) | 4.02% CAGR |

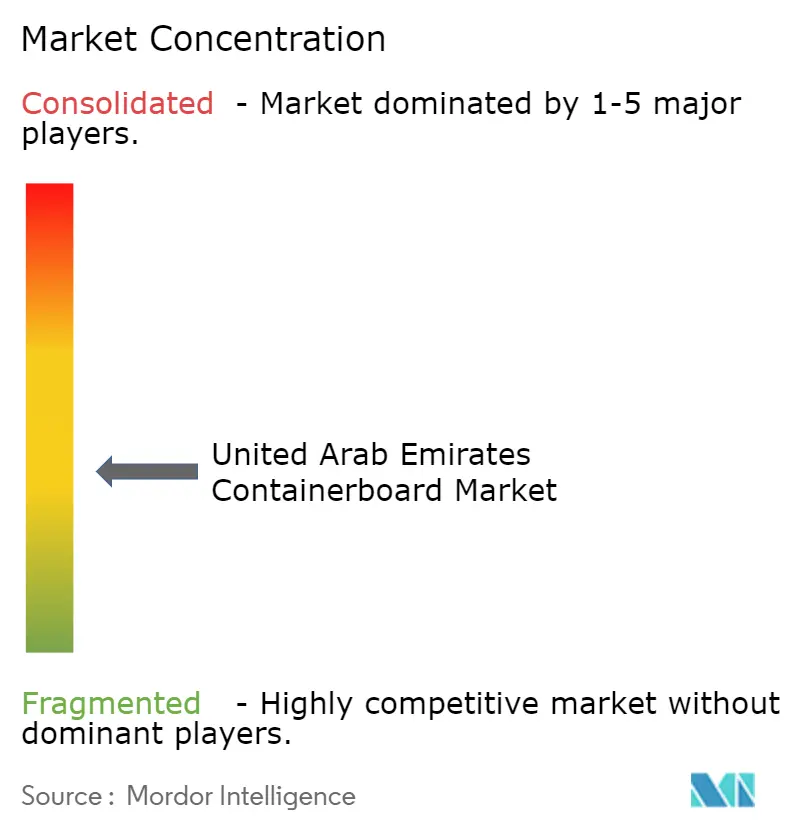

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Containerboard Market Analysis by Mordor Intelligence

The United Arab Emirates containerboard market size was valued at USD 541.02 million in 2025 and estimated to grow from USD 563.35 million in 2026 to reach USD 685.91 million by 2031, at a CAGR of 4.02% during the forecast period 2026-2031. The market is well-positioned in Gulf packaging substrates, as the country combines strong local consumption with a re-export role that connects Sub-Saharan Africa, South Asia, and the broader Middle East. Growth is being supported by 3 linked shifts: full enforcement of the single-use plastic ban from January 2026, steady expansion in parcel volumes tied to online retail, and the start-up of a USD 54 million recycled containerboard mill in KEZAD that lowers reliance on imported corrugating medium. Demand is also becoming more concentrated along the Abu Dhabi-Dubai corridor, where mills, converters, logistics assets, and fulfillment hubs are reducing transport friction between paper production and box conversion. Competitive conditions remain active rather than consolidated because several corrugated players serve trade flows linked to Jebel Ali and other logistics nodes, not only domestic buyers. At the same time, the UAE containerboard market is facing cost pressure from fluctuations in OCC prices and maritime route disruptions, pushing mills and converters to place greater emphasis on domestic fiber sourcing, inland logistics, and supply security.

Key Report Takeaways

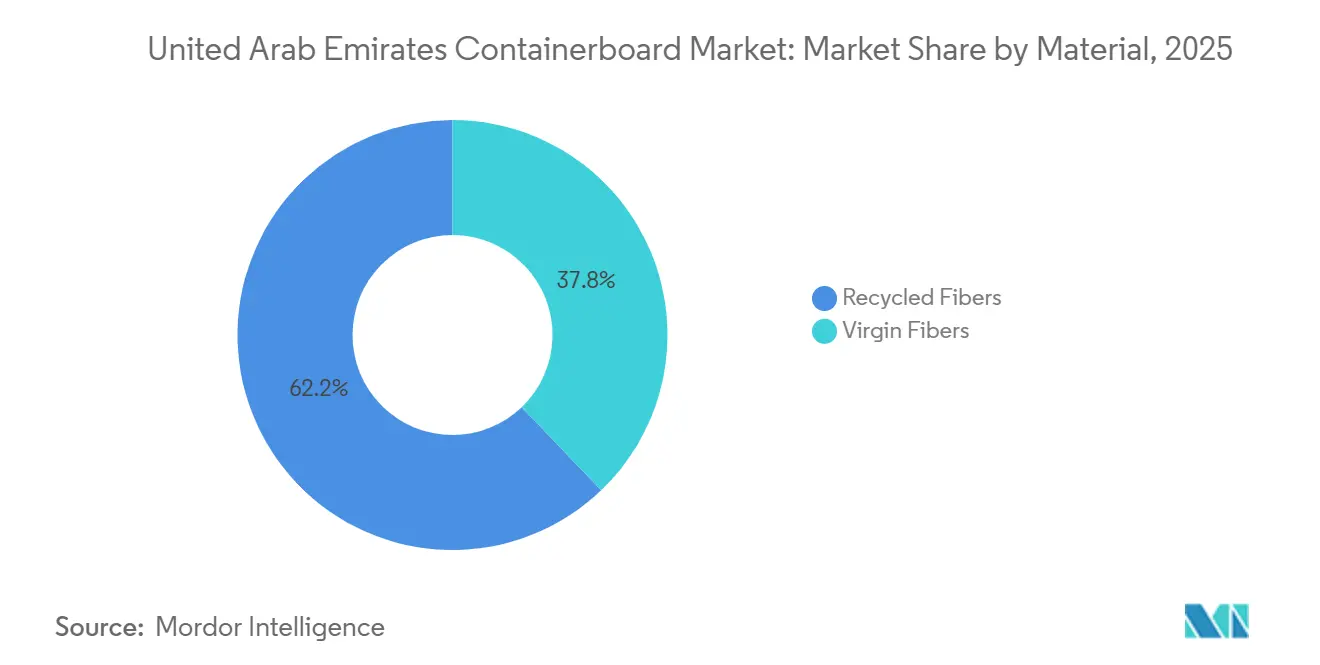

- By material, recycled fiber captured 62.16% of the United Arab Emirates containerboard market share in 2025.

- By product type, the UAE containerboard market size for the kraftliners segment is forecast to advance at a 4.48% CAGR through 2031.

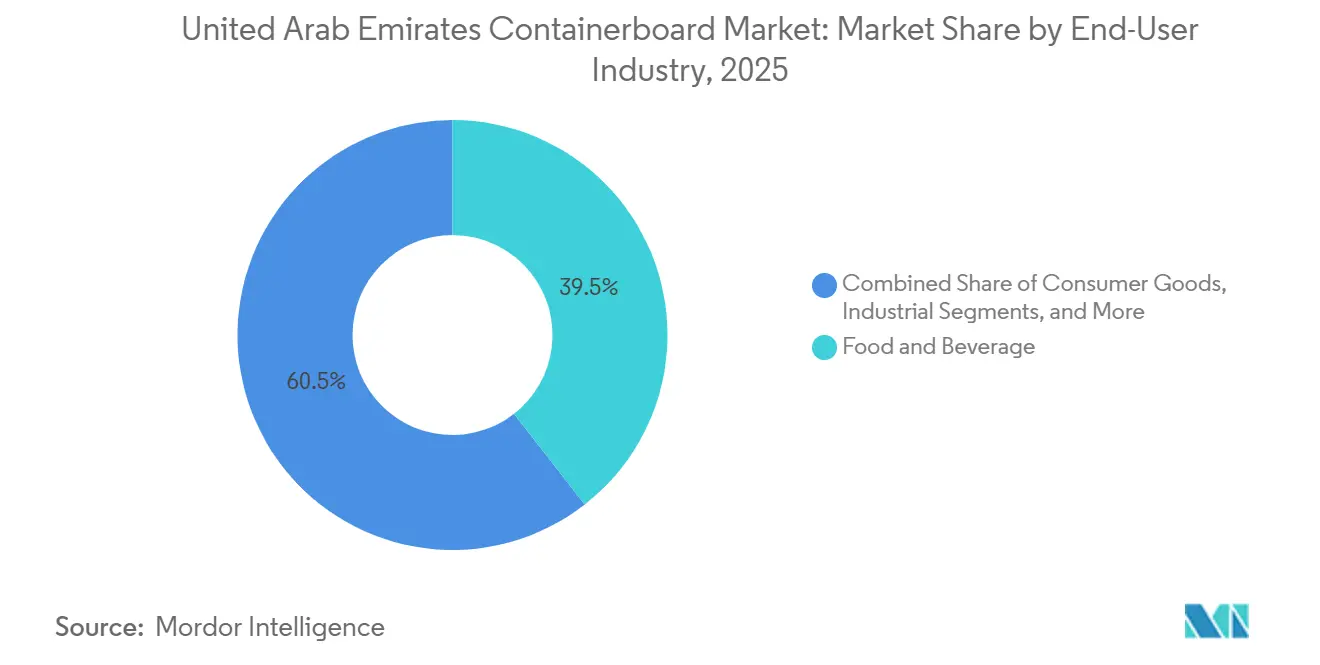

- By end-user industry, food and beverage captured 39.46% of the UAE containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Arab Emirates Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Recyclable Transit Packaging in Food and Beverage | +0.9% | UAE-wide, strongest in Dubai cold-chain and Abu Dhabi agri-export hubs | Short term (≤ 2 years) |

| E-Commerce and Quick-Commerce Parcel Growth | +1.2% | UAE-wide, concentrated in Dubai South, Al Quoz, and Abu Dhabi industrial zones | Short term (≤ 2 years) to Medium term (2-4 years) |

| Packaging EPR and Single-Use Plastic Substitution | +0.8% | Initial rollout in Abu Dhabi and Dubai, national scale by late 2026 | Short term (≤ 2 years) to Medium term (2-4 years) |

| New Domestic Recycled Containerboard Capacity in KEZAD | +0.5% | Abu Dhabi-centric, with supply spill-over to Northern Emirates converters | Medium term (2-4 years) |

| Jebel Ali Re-Export and Fulfillment Hub Expansion | +0.4% | Dubai-centric, spill-over to Sharjah and Northern Emirates logistics zones | Medium term (2-4 years) |

| Digital Print and Right-Sized Box Adoption | +0.3% | UAE-wide, early adoption in Dubai e-commerce and FMCG sectors | Medium term (2-4 years) to Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce and Quick-Commerce Parcel Growth

The United Arab Emirates containerboard market is benefiting from rising online retail activity, with UAE e-commerce reaching AED 32.3 billion (USD 8.79 billion) in 2024 and projected to exceed AED 50.6 billion (USD 13.7 billion) by 2029, reflecting sustained parcel generation across retail categories. By end-2025, total online retail in the country was valued at AED 57 billion (USD 15.5 billion), and penetration exceeded 17%, indicating that parcel-based distribution is becoming a more standard route to market rather than a niche channel. Quick-commerce adds greater packaging intensity than standard e-commerce because smaller baskets are usually shipped as separate orders rather than consolidated multi-item consignments, which increases corrugated usage per unit of merchandise sold. Platforms such as Noon.com, Amazon.ae, and Carrefour UAE's rapid-delivery services require frequent replenishment of corrugated SKUs during each operating shift, which favors local converters that can respond quickly to lead times and assortments. That demand pattern is particularly supportive of small-format mailers based on B-flute and E-flute testliner structures, as these grades better fit fast-moving parcel applications than bulk transit formats. As a result, each gain in digital retail penetration is feeding a more regular and higher-frequency order book for the UAE containerboard market than would be expected from merchandise value growth alone

Rising Demand for Recyclable Transit Packaging in Food and Beverage

The United Arab Emirates containerboard market is also supported by food and beverage packaging demand that extends beyond domestic grocery sales into export logistics, cold-chain shipments, and food-service conversion. The sector serves a resident base of nearly 10 million people and a visitor economy of over 17 million arrivals annually, which broadens the packaging load moving through retail, hospitality, and port-linked food distribution channels. Fresh and perishable exports routed through Jebel Ali cold-chain facilities require moisture-resistant, high-strength corrugated transit packaging that maintains shape during sharp humidity and temperature changes. Since January 2026, corrugated trays made with recycled fiber and a barrier coating have been replacing EPS formats in fresh-produce logistics following the ban on Styrofoam food containers. The National Food Security Strategy 2051 is adding another layer of demand because hydroponics and aquaculture output needs dedicated corrugated runs with branding and handling requirements that differ from standard brown-box formats. This keeps food-linked containerboard demand on a relatively stable footing, even when general freight volumes become more cyclical across the wider logistics system.[1]DP World, “DP World Reports Record USD 24.4 Billion Revenue and USD 6.4 Billion EBITDA for 2025,” DP World, dpworld.com

Packaging EPR and Single-Use Plastic Substitution

The UAE containerboard market is gaining from policy change as MOCCAE and Tadweer Group signed an MoU in July 2025 to launch the country’s first EPR pilot for packaging, electronics, and batteries across Abu Dhabi and Dubai. The pilot included 26 corporate signatories to an EPR Pledge, which provides a broader base for the shift toward take-back obligations, reporting, and recycled-content requirements than a narrow municipal initiative. This change is important for converters because buyers are likely to place more value on certified recyclable grades and lifecycle documentation, rather than short-term price. The expected national rollout in 2026 can pressure importers of plastic packaging more than fiber-based suppliers, which supports substitution in food-service, retail, and logistics applications. At the same time, the phased plastic ban moved from bags in January 2024 to cups, cutlery, lids, plates, straws, stirrers, and food containers in January 2026, which has already changed procurement choices across food-service channels.[2]UAE Legislation Portal, “Federal Law No. 12 of 2018 On Integrated Waste Management,” UAE Government, uaelegislation.gov.ae That combination of regulatory pressure and product substitution is reshaping the material mix in favor of corrugated and molded-fiber formats across the United Arab Emirates containerboard market.

New Domestic Recycled Containerboard Capacity in KEZAD

The UAE containerboard market received a major supply-side boost when Star Paper Mill’s AED 200 million (USD 54 million) recycled containerboard plant at KEZAD was officially inaugurated on May 7, 2026. The facility covers 90,000 square meters and has an annual capacity of 135,000 tonnes, with trial production having started on April 11, 2026. Its product slate includes testliner, fluting, kraft top liner, and recycled bag paper, serving both mainstream corrugated demand and adjacent paper packaging needs for converters. The mill sources up to 80% of its feedstock from domestic waste paper, helping reduce exposure to imported OCC swings that have unsettled converter margins in recent years. With this addition, the country’s 6 recycled containerboard mills together produce nearly 675,000 metric tonnes per year, reinforcing the UAE’s role as a supplier of packaging materials within the GCC. The practical effect is that converters in Abu Dhabi, Dubai, and the Northern Emirates now have a stronger domestic sourcing option when maritime conditions or imported fiber prices become unstable

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imported Kraftliner and OCC Price Volatility | -0.8% | Global, most acutely felt by UAE-based importers and mills reliant on US and European OCC | Short term (≤ 2 years) to Medium term (2-4 years) |

| Strait of Hormuz and Red Sea Route Disruption Risk | -0.9% | UAE Gulf ports, including Jebel Ali, Khor Fakkan, and Fujairah, with spill-over across GCC | Short term (≤ 2 years) |

| Fiber-Quality Inconsistency in Domestic Recovery Streams | -0.4% | UAE-wide, more acute in Northern Emirates with thinner OCC collection networks | Medium term (2-4 years) to Long term (≥ 4 years) |

| Returnable Plastic Crates in Fresh Produce Logistics | -0.3% | UAE fresh produce supply chain hubs, particularly Abu Dhabi and Dubai wholesale markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Imported Kraftliner and OCC Price Volatility

The United Arab Emirates containerboard market continues to face margin pressure from sharp fluctuations in OCC prices across global recovered paper markets. US OCC prices rose from USD 33 per tonne in February 2023 to USD 106 per tonne in August 2024, then fell to USD 44 per tonne by November 2025, which shows how quickly feedstock conditions can reverse for converters that buy into global cycles. For UAE buyers of virgin kraftliner used in premium corrugated grades for electronics and consumer goods exports, these swings translate into unstable pricing and weaker visibility on contract margins. The imbalance between corrugated demand and OCC collection volumes remains a structural issue, so domestic recovery improvements alone are unlikely to eliminate volatility from the system. Indian containerboard exporters were offering material to UAE buyers at prices close to those of local mills in early 2026, while buyers also reported quality inconsistencies, making it harder for domestic suppliers to maintain pricing discipline. As recycled-content rules become more important under waste management reform, competition for the same recovered-paper pool can tighten further, making cost control across the UAE containerboard market more difficult.

Strait of Hormuz and Red Sea Route Disruption Risk

The UAE containerboard market is also exposed to maritime disruption because a large share of fiber imports, finished paper movements, and export-linked corrugated demand depends on Gulf shipping lanes. The partial closure of the Strait of Hormuz from late February 2026 led to war surcharges of USD 3,000-3,500 per 40-foot container, with major carriers diverting away from Jebel Ali toward Jeddah or smaller UAE ports. These changes added delays and higher clearance costs, and corrugator demand weakened when export-oriented customers cut back their own order schedules during the disruption. Brent crude near USD 109 per barrel in early May 2026 added another layer of cost pressure on mills, because energy exposure is different from freight exposure, and both were moving upward at the same time. Supply-chain tracking also showed that nearly 10% of the global container fleet was constrained in the region, while Cape of Good Hope diversions could extend transit times by up to 2 weeks, which is difficult for mills operating with lean inventory. The earlier Red Sea crisis had already shown how serious these corridor shocks can be, with the World Bank documenting a 75% decline in vessel traffic through the Bab El-Mandeb Strait in 2024.[3]World Bank, “The Red Sea Crisis, Impact on Global Trade and Maritime Transport,” World Bank Open Knowledge, worldbank.org

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fiber Keeps Its Lead While Virgin Grades Gain in Premium Applications

Recycled fibers held 62.16% of the United Arab Emirates containerboard market share in 2025, which reflects the strength of local waste-paper collection, the installed RCCM base, and converter preference for cost-competitive domestic supply. The country had 6 operational recycled containerboard mills, and together they provided the industrial backbone that kept recycled grades central to mainstream box demand. That position strengthened further after Star Paper Mill brought its 135,000-tonne KEZAD facility into operation, with up to 80% domestic feedstock sourcing, which reduced logistics exposure to imported recovered paper. Recycled grades also align with policy direction because EPR development and waste management reform are placing greater emphasis on traceable recovery streams and higher recycled content in packaging procurement. This makes the recycled segment a structural anchor for the UAE containerboard industry, especially in food distribution, general freight, and high-volume e-commerce formats that do not require the highest paper performance ceiling. Domestic recycled supply also gives converters more room to manage working capital and lead times when freight conditions change quickly at Gulf ports.

Virgin fibers remained the smaller material segment, yet they are projected to grow at a 4.39% CAGR through 2031, faster than the overall market and pointing to steady premiumization in selected applications. Demand is coming from brand owners in electronics, healthcare, and fine-food categories that need better burst strength, cleaner appearance, and more consistent print surfaces than current domestic recycled streams always deliver. The 2026 Strait of Hormuz disruption highlighted that dependence on imported virgin kraftliner creates both supply and cost risks, which may push converters to look more closely at local quality upgrades and resilience planning. Even so, the likely scaling of recycled-content expectations under the EPR framework should preserve recycled fiber's lead position in the medium term. The resulting pattern is a clear two-tier structure in the UAE containerboard industry, where recycled grades dominate volume while virgin grades retain a premium role in quality-sensitive end uses

By Product Type: Testliners Hold the Volume Base and Kraftliners Post the Strongest Growth

Testliners accounted for 42.53% of the United Arab Emirates containerboard market in 2025, making them the largest product type in a market supported by recycled-fiber economics and broad corrugated box demand. Their lead reflects compatibility with the country’s RCCM mill base and their widespread use in general-purpose shipping cases for food-service, parcel distribution, and ordinary freight movement. Cost remains a major advantage for testliners over virgin kraftliner, and improved top-coating has also widened their use where better print appearance is needed without moving fully into premium paper grades. This keeps Testliner as the default specification across many Dubai and Abu Dhabi corrugated runs tied to online retail and food distribution. In practical terms, the product’s scale position means that changes in parcel volumes, food transit needs, and converter scheduling continue to flow first into testliner demand across the UAE containerboard industry.

Kraftliners are projected to grow at a 4.48% CAGR through 2031, placing them ahead of the market average and signaling a stronger pull from premium, export-oriented, and print-sensitive packaging formats. Their higher burst strength makes them better suited to heavy-duty industrial handling and refrigerated export shipments where structural performance is more important than lowest cost. They also align with the spread of higher-definition digital print lines in corrugated plants serving cosmetics, electronics, and fashion labels that want better presentation through retail and direct-to-consumer channels. Fluting, as the inner corrugated medium, is expected to move more closely with overall box output, but the start-up of the KEZAD mill will improve domestic availability of both fluting and testliner. Another product-level shift is coming from right-sized box systems, where thinner flute options such as E-flute and F-flute can increase fluting intensity in small-parcel formats even as outer dimensions shrink. That means the UAE containerboard industry is not moving away from volume grades, but it is becoming more differentiated between value-led and performance-led specifications.

By End-User Industry: Food and Beverage Leads Current Demand While Consumer Goods Adds the Strongest Incremental Growth

Food and beverage accounted for 39.46% of the United Arab Emirates containerboard market in 2025, making it the largest end-user segment, as it combines domestic FMCG distribution with export-oriented fresh-produce movement. The segment’s scale is tied to high-throughput retail flows, hospitality demand, and temperature-controlled logistics that need durable corrugated cases and trays across many stock-keeping units. The January 2026 extension of the plastic ban to Styrofoam food containers, cups, lids, and related items is widening fiber-based substitution in food-service channels beyond standard transport packaging. Corrugated tray formats are therefore gaining relevance in applications that previously relied on foam or other plastic-heavy options. The food and beverage segment also benefits from the fact that cold-chain exports require packaging performance that is not easily deferred when freight conditions soften, which gives it a more durable demand floor than some discretionary categories.[4]DP World, “DP World Reports Record USD 24.4 Billion Revenue and USD 6.4 Billion EBITDA for 2025,” DP World, dpworld.com

Consumer goods are projected to grow at a 4.56% CAGR through 2031, the fastest pace among end users, as Dubai free zones continue to host regional hubs for the distribution of cosmetics, apparel, and electronics. These categories need higher-quality printed corrugated boxes, and they are less willing to rely on plain commodity formats because packaging also supports presentation, handling, and brand consistency. Industrial packaging remains strategically important as manufacturing expands under Operation 300 billion, as exporters of petrochemicals, pharmaceuticals, and advanced materials need protective corrugated packaging that meets international transit requirements. Other end users, including retail, hospitality, and specialty e-commerce, are also growing as plastic-to-fiber substitution extends into categories that once relied more on rigid or flexible plastics. This leaves the United Arab Emirates containerboard industry with a broad demand base where food and beverage supplies scale, while consumer goods contributes the more premium and faster-growing mix shift.

Geography Analysis

The UAE containerboard market is concentrated along 2 connected emirate corridors, Abu Dhabi-KEZAD and the Dubai-Sharjah manufacturing and logistics belt, where most mills, corrugators, converters, and fulfillment assets are clustered. Dubai remains central because Jebel Ali handled a record 16.5 million TEUs in 2025, while DP World also reported strong growth in origin-and-destination cargo and breakbulk volumes that support both inbound paper supply and outbound corrugated trade. This gives Dubai a dual role as an import gateway for virgin kraftliner and OCC, and as an export platform for domestically produced corrugated packaging bound for East Africa, South Asia, and the Levant. Because of that trade linkage, converter demand in the UAE does not move solely with local consumption; it can also rise or fall with re-export activity. The partial Strait of Hormuz closure from February 2026 made this visible when export flows slowed and corrugator orders weakened, even though domestic demand remained more stable.

Abu Dhabi is becoming more important on the upstream side of the value chain as Operation 300 billion and KEZAD incentives encourage local paper production and converter co-location. The new Star Paper Mill facility gives the emirate a stronger supply role in testliner, fluting, and related grades, which reduces dependence on imported material from India, Turkey, and Europe. Sharjah remains relevant through its base of mid-scale converters serving hospitality and retail packaging, while Ras Al Khaimah adds industrial exposure through packaging linked to ceramics, building materials, and food processing. Northern Emirates players still face thinner OCC collection networks, which affects fiber consistency and keeps them more exposed to imported feedstock conditions than converters in Abu Dhabi and Dubai.

The United Arab Emirates containerboard market also benefits from a regional trade position that places it within 4 air or sea hours of nearly 2 billion consumers across South Asia, East Africa, and the Middle East, which supports the durability of the re-export model. Jebel Ali’s rail terminal, currently operating at 800,000 TEUs annually, is being expanded to 1.6 million TEUs, which should improve inland flexibility when maritime routes are disrupted. Competition from Indian exporters remains the main external pressure, as they can reach the UAE at near-local prices, although buyers have also noted quality inconsistencies in those imports. Smaller Gulf markets such as Oman and Bahrain still represent useful export outlets for UAE corrugated manufacturers that can use Jebel Ali distribution reach, and KEZAD bonded logistics to serve nearby demand

Competitive Landscape

The UAE containerboard market has nearly 20 active manufacturers and converters, a high count relative to domestic consumption, reflecting the importance of trade-linked packaging demand through free zones and port infrastructure. The leading names include Arabian Packaging Co. LLC, Union Paper Mills LLC, Star Paper Mill Paper and Tissue Industries. LLC, and Hotpack Packaging LLC, while many smaller converters remain active in niche print runs, specialty customer groups, and sub-regional supply lanes. This creates moderate concentration rather than a tightly controlled structure, because established firms anchor scale, while the mid-market remains divided among many operators serving specific industries and order profiles. Business models fall into 2 broad groups: integrated producers with paper-machine assets and converter-focused firms that compete through print quality, right-sized capability, and delivery responsiveness. The structure gives buyers options, but it also makes the UAE containerboard market sensitive to shifts in freight, feedstock, and trade routes because not all players have the same sourcing depth or operating leverage.

Star Paper Mill provided the clearest strategic move in 2026 when it inaugurated its KEZAD recycled containerboard facility, adding 135,000 tonnes of annual capacity and strengthening upstream supply inside the country. The company had already signed distribution agreements with Heinzel Sales and Ekman, targeting 68,000 tonnes of recycled paper exports across the GCC, the Middle East, Africa, and South America, indicating that some UAE producers are expanding beyond domestic demand into regional trade. Hotpack Global made another important move when it completed a minority equity investment by GII in May 2026, with the capital aimed at widening its regional manufacturing footprint under long-term customer supply agreements. These actions suggest that scale, supply assurance, and regional reach are becoming more important competitive tools than price alone in the United Arab Emirates containerboard market.

The clearest open spaces remain barrier-coated containerboard for moisture-sensitive food and pharmaceutical exports and digitally printable corrugated lines for short-run e-commerce work. Much of the barrier-coated need is still met through imports, leaving domestic mills room to raise product capability as food security and export programs expand. Short-run digital-print corrugated is also underpenetrated because many converters still rely on flexographic setups with run lengths too long for micro-brands and subscription-style packaging demand. Compliance with the EPR pilot and local enforcement of Cabinet Resolution No. 380 of 2022 are making certified recyclable grades and lifecycle documentation more relevant in procurement decisions, favoring suppliers that can support traceability and customer reporting. Right-sized box systems that digitally cut and erect corrugated fanfold material are beginning to enter regional distribution operations, and wider use in UAE fulfillment centers would support more demand for E-flute testliner while reducing dependence on standard pre-made box inventories

United Arab Emirates Containerboard Industry Leaders

Arabian Packaging Co. LLC

Star Paper Mill Paper & Tissue Ind. LLC

RAK Packaging Company Ltd.

ZamZam Packaging Mat. Ind. L.L.C.

Unipack Containers & Carton Products LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: H.E. Dr. Sultan Ahmed Al Jaber, UAE Minister of Industry and Advanced Technology, officially inaugurated Star Paper Mill's AED 200 million (USD 54 million) recycled containerboard manufacturing facility in KEZAD at the Make it in the Emirates 2026 forum in Abu Dhabi. Spanning 90,000 square metres with an annual capacity of 135,000 tonnes of testliner, fluting, and kraft top liner, the plant sources up to 80% of feedstock from domestic waste paper, directly reducing the UAE's dependence on imported containerboard grades.

- May 2026: Hotpack Global Holding Ltd. announced the completion of a minority equity investment by GII (Gulf Islamic Investments). The capital is directed toward expanding Hotpack's regional manufacturing footprint, including commissioning a new facility in Al Kharj, Saudi Arabia, described as one of the Kingdom's largest specialized food packaging plants, under long-term customer supply agreements.

- April 2026: Star Paper Mill commenced trial production on its new PM1 paper machine at the KEZAD Abu Dhabi facility on April 11, 2026, with rated capacity of 134,000 tonnes per year producing testliner, fluting, kraft, and bag-paper grades. The startup coincided with a softening of UAE corrugator demand as Strait of Hormuz disruptions curtailed downstream export orders.

- March 2026: The partial closure of the Strait of Hormuz by Iran's IRGC, effective February 28, 2026, triggered war surcharges of USD 3,000-3,500 per 40-foot container on shipments transiting Gulf ports. Jebel Ali was effectively bypassed by major carriers, with PIX Testliner GCC rising 2.44% to USD 494.23 per tonne and PIX Fluting GCC rising 2.70% to USD 469.67 per tonne in the 4 weeks to May 5, 2026.

United Arab Emirates Containerboard Market Report Scope

The United Arab Emirates Containerboard Market encompasses the production, distribution, and consumption of containerboard used in the manufacture of corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The increasing demand for sustainable, lightweight, and durable packaging solutions drives the market.

The United Arab Emirates Containerboard Market Report is Segmented by Material (Virgin Fibers and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the UAE containerboard market size in 2026 and how large will it be by 2031?

The UAE containerboard market was estimated at USD 563.35 million in 2026 and is forecast to reach USD 685.91 million by 2031, growing at a 4.02% CAGR over 2026-2031.

Which material type leads containerboard demand in the UAE?

Recycled fiber led demand with 62.16% share in 2025, supported by local OCC collection, 6 operating recycled mills, and policy support for higher recycled-content packaging.

Which product type is growing the fastest in UAE containerboard?

Kraftliners are projected to post the fastest growth at a 4.48% CAGR through 2031, helped by demand from premium consumer goods, refrigerated exports, and better print performance.

Which end-user sector generates the most demand for containerboard in the UAE?

Food and beverage remained the largest end-user segment with 39.46% share in 2025 because it combines domestic FMCG distribution, food-service conversion, and export-oriented fresh-produce logistics.

Why is Abu Dhabi KEZAD becoming important for containerboard supply?

KEZAD now hosts Star Paper Mill's new recycled containerboard facility with 135,000 tonnes of annual capacity, which lowers import dependence and shortens supply lines for local converters.

What are the main risks affecting UAE containerboard demand and margins?

The biggest risks are OCC and kraftliner price volatility and shipping disruption through the Strait of Hormuz and Red Sea routes, both of which can raise costs and weaken export-linked box demand.

Page last updated on: