Middle East and Africa Agriculture Drones Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

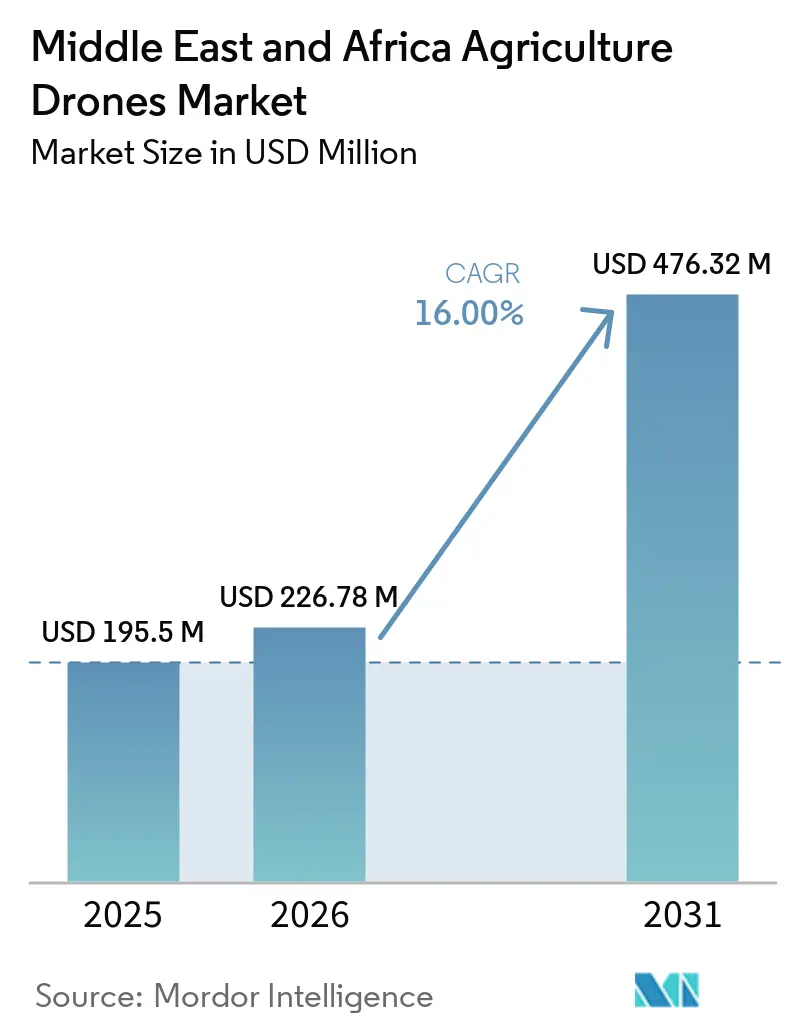

| Base Year Market Size (2025) | USD 195.5 Million |

| Market Size (2026) | USD 226.78 Million |

| Market Size (2031) | USD 476.32 Million |

| Growth Rate (2026 - 2031) | 16.00% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East and Africa Agriculture Drones Market Analysis by Mordor Intelligence

The Middle East and Africa agriculture drones market size is projected to expand from USD 195.5 million in 2025 and USD 226.8 million in 2026 to USD 476.3 million by 2031, registering a CAGR of 16.0% between 2026 and 2031. The Middle East and Africa agriculture drones market is entering a broader adoption phase after earlier demand was centered on a limited set of large commercial farms in South Africa and the Gulf. Freshwater depletion across the Arabian Peninsula and the Nile Basin is turning precision irrigation from a discretionary investment into a basic operating need for commercial agriculture, thereby supporting sustained demand for equipment and services over the forecast period. Government food-security programs in Saudi Arabia and the United Arab Emirates (UAE) are also expanding adoption, as public procurement can fund smart-farming systems at a scale many growers cannot finance on their own. The market is also benefiting from rising labor pressures, higher spraying costs, and greater interest in outcome-based service models that reduce the capital burden on smaller farms. Additionally, the market features diverse competition, including large drone manufacturers, software providers, mapping firms, and service companies. This diversity creates opportunities for specialized offerings in the agriculture drone market in the Middle East and Africa, which continue to grow.

Key Report Takeaways

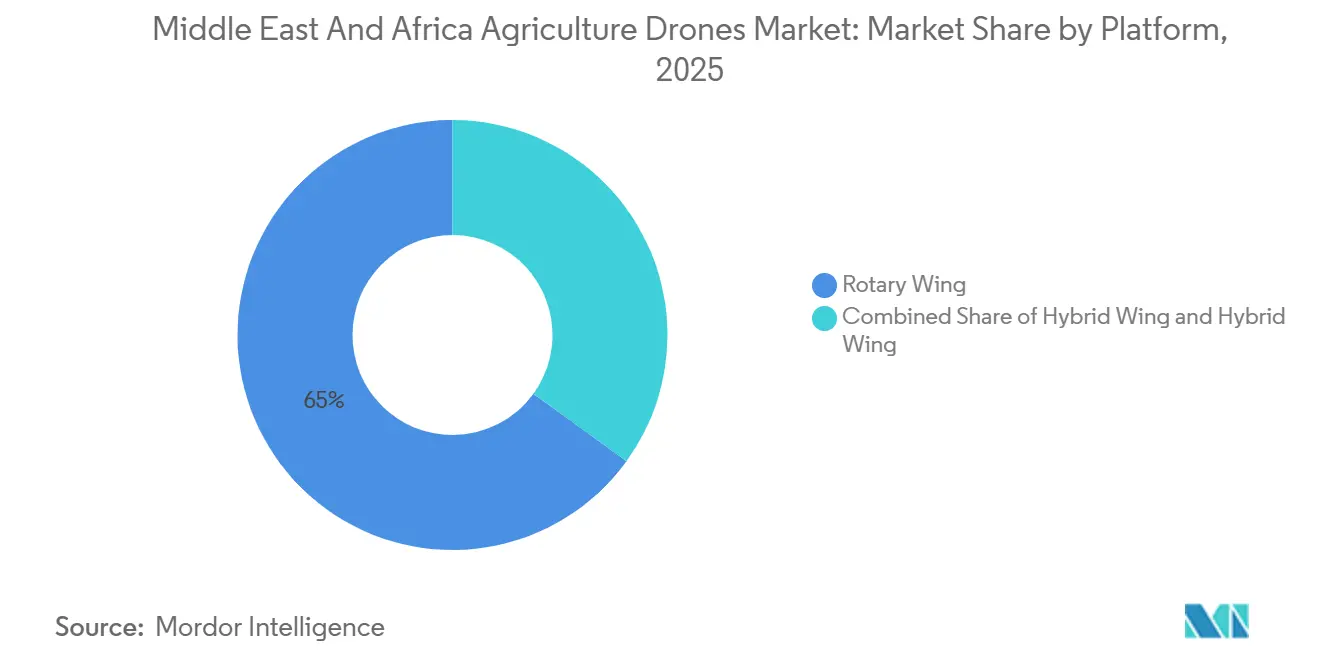

- By platform, rotary-wing drones held the largest Middle East and Africa agriculture drones market share, accounting for 65.0% in 2025, while fixed-wing platforms are projected to grow at the fastest CAGR of 16.5% from 2026 to 2031.

- By application, crop monitoring and field surveillance accounted for the largest Middle East and Africa agriculture drones market share, representing 38.0% in 2025, whereas crop spraying and spreading is projected to grow at the fastest CAGR of 18.0% from 2026 to 2031.

- By component, hardware held the largest Middle East and Africa agriculture drones market share, accounting for 63.0% in 2025, while the services segment is projected to grow at the fastest CAGR of 17.2% from 2026 to 2031.

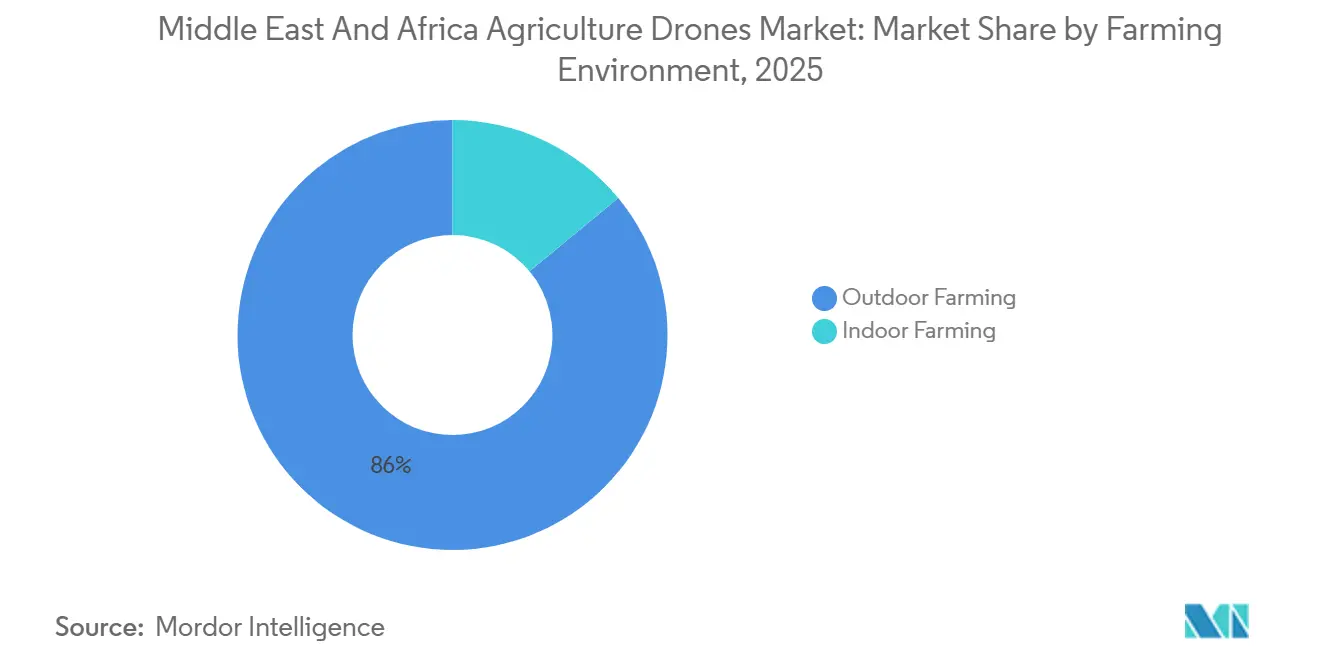

- By farming environment, outdoor farming represented the largest Middle East and Africa agriculture drones market share, accounting for 86.0% in 2025, whereas indoor farming is projected to grow at the fastest CAGR of 17.0% from 2026 to 2031.

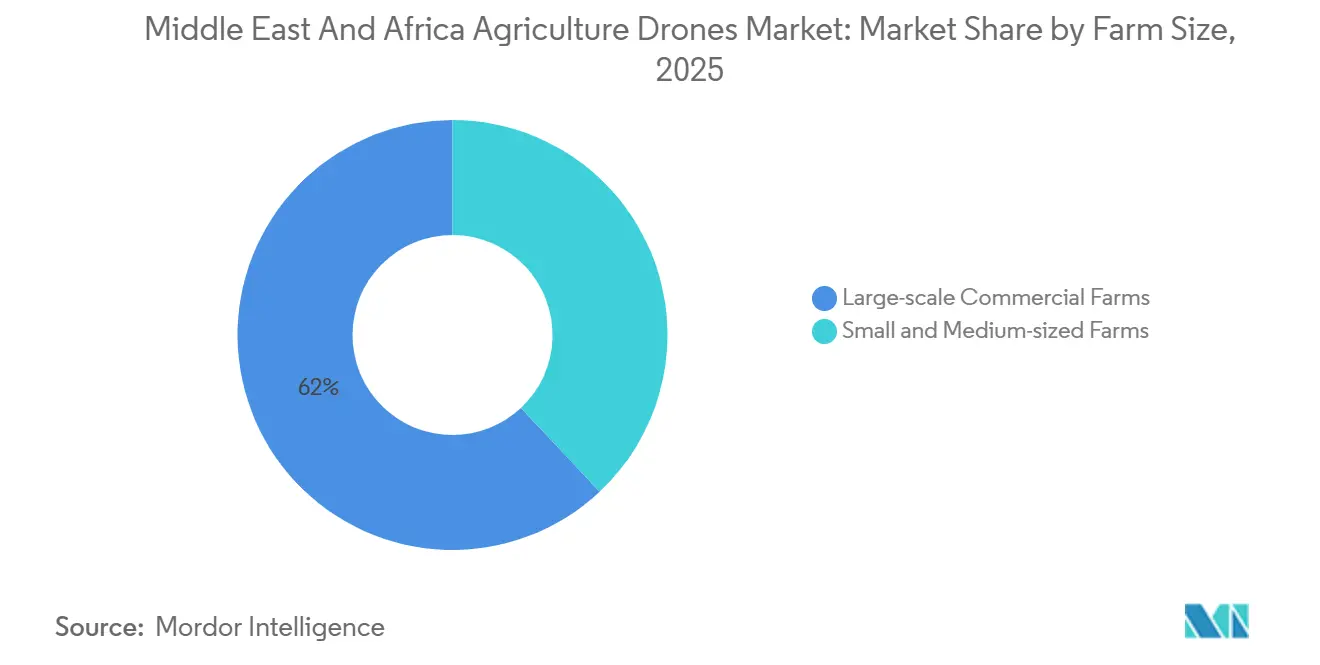

- By farm size, large-scale commercial farms held the largest Middle East and Africa agriculture drones market share, accounting for 62.0% in 2025, while small and medium-sized farms are projected to grow at the fastest CAGR of 16.8% from 2026 to 2031.

- By geography, South Africa accounted for the largest Middle East and Africa agriculture drones market share, representing 34.0% in 2025, while also being projected to grow at the fastest CAGR of 17.6% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East and Africa Agriculture Drones Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Water-stress driven precision irrigation | +4.50% | Middle East and Africa (MEA) core, highest in Saudi Arabia, the United Arab Emirates (UAE), Egypt, and South Africa | Medium term (2-4 years) |

| Farm labor shortages and spray-cost inflation | +3.80% | Global, with stronger effect in South Africa and Gulf commercial farms | Short term (≤ 2 years) |

| Food-security programs and smart-farming incentives | +3.50% | Middle East and Africa (MEA) core, strongest in Saudi Arabia and the United Arab Emirates (UAE), with spillover to Egypt and North Africa | Medium term (2-4 years) |

| Return on Investment (ROI) on high-value crops and plantation monitoring | +3.20% | South Africa, Kenya, Egypt citrus and vineyard belts, and Saudi date farms | Short term (≤ 2 years) |

| Drone-as-a-service expansion for grower clusters | +2.80% | South Africa and West Africa clusters, with spillover to Gulf cooperatives | Medium term (2-4 years) |

| Export-traceability and carbon-data requirements | +2.50% | South Africa export chain, United Arab Emirates (UAE) re-export hubs, and spillover to Morocco | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Water-Stress Driven Precision Irrigation

Freshwater scarcity remains a significant long-term growth driver for the agriculture drones market in the Middle East and Africa, as governments and farm operators increasingly focus on precision irrigation and resource optimization. Countries such as Saudi Arabia and the United Arab Emirates (UAE) heavily depend on non-renewable water sources, driving demand for drone-based technologies such as thermal imaging, multispectral monitoring, and precision field assessment to enhance water management and crop monitoring [1]Source: Saudi Ministry of Environment, Water and Agriculture, “Official Website,” Saudi Ministry of Environment, Water and Agriculture, mewa.gov.sa. National food security initiatives and agricultural modernization programs are further promoting the adoption of drones, particularly among large commercial farms and institutional farming projects capable of deploying drone fleets at scale. Consequently, precision irrigation and water-use optimization are transitioning from productivity-enhancing tools to essential operational requirements within the regional agriculture market.

Farm Labor Shortages and Spray-Cost Inflation

The agriculture drones market in the Middle East and Africa is being driven by labor shortages and rising field-spraying costs, which enhance the economic feasibility of drone-based operations in commercial farming systems. Precision drone spraying is gaining popularity among growers and farming cooperatives for its ability to reduce per-hectare spraying costs, improve application efficiency, and optimize chemical use compared to traditional spraying methods. The demand is particularly robust in high-value crop cultivation, where growers prioritize better spray timing, improved canopy penetration, and accurate dosage application while reducing reliance on manual labor. Consequently, recurring drone-based agriculture service models are becoming increasingly significant in key commercial farming areas across the region.

Food-Security Programs and Smart-Farming Incentives

The Middle East and Africa agriculture drones market is benefiting from food security programs in Gulf countries, where government funding is helping expand the use of drone-based farming technologies. Saudi Arabia’s agricultural sufficiency agenda and the United Arab Emirates (UAE) long-range food security strategy both support the deployment of smart farming, which gives drone vendors access to institutional buyers with larger budgets and longer planning horizons than individual growers. This changes revenue quality for suppliers because public and quasi-public contracts tend to be larger, more standardized, and easier to scale across service agreements. It also favors vendors that can support enterprise procurement, operator training, and compliance, rather than just hardware delivery. As a result, state-backed demand is helping the Middle East and Africa agriculture drones market grow faster than it did before 2025, when adoption was concentrated in a narrow band of large private farms.

Return on Investment (ROI) on High-Value Crops and Plantation Monitoring

High-value crops continue to strengthen the business case for the Middle East and Africa agriculture drones market, as avoided crop loss often matters more than direct input savings. Aerobotics uses its Drone Scan platform across South Africa’s orchard regions to provide tree-level visibility into plant health, enabling earlier intervention against pests and diseases in export-oriented fruit operations. In these settings, a single avoided disease event or a more targeted spray cycle can justify drone spending more quickly than in broad-acre commodity agriculture. This makes citrus, grapes, dates, sugarcane, and export horticulture especially favorable use cases across the region. The same economics explain why premium monitoring and targeted spraying systems are gaining traction within the Middle East and Africa agriculture drones market, even when capital budgets remain tight.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Beyond Visual Line of Sight (BVLOS) and aerial spray rules | -3.50% | Pan-Middle East and Africa (MEA), with highest friction in sub-Saharan Africa and cross-border Gulf operations | Medium term (2-4 years) |

| High upfront cost and weak farm financing | -3.00% | Sub-Saharan Africa and Egypt, with lower friction in the Gulf because of public procurement | Short term (≤ 2 years) |

| Rural charging, Real-Time Kinematic (RTK), and spare-parts gaps | -2.50% | Rest of Africa, where infrastructure density is low, partly offset in South Africa and United Arab Emirates (UAE) | Long term (≥ 4 years) |

| Limited agronomic prescription data and pilot skills | -2.00% | Pan-Middle East and Africa (MEA), strongest in East and West African smallholder corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Beyond Visual Line of Sight (BVLOS) and Aerial Spray Rules

Regulation remains a significant structural challenge in the Middle East and Africa agriculture drones market, as differing certification and flight rules across countries hinder seamless scaling for operators. In January 2026, Saudi Arabia updated the General Authority of Civil Aviation Regulations (GACAR) Part 107, introducing European Union Aviation Safety Agency (EASA)-aligned risk-based Standard Scenarios for commercial Beyond Visual Line of Sight (BVLOS) operations. These updates have the potential to significantly reduce approval timelines for compliant operators. This development is crucial, as service providers need predictable regulatory frameworks to establish regional drone fleets rather than operating on a fragmented, country-specific basis. Additionally, CropLife Africa Middle East published a regional framework for drone-based pesticide application in 2025 to address the lack of clear, enforceable spraying standards in many African markets [2]Source: CropLife Africa Middle East, “Guidelines for Development of Regulatory Frameworks for Use of Drones in Pesticides Application in Africa Middle East,” CropLife Africa Middle East, croplifeafrica.org. However, until more countries harmonize regulations on licensing, pilot certification, and spraying standards, the agriculture drones market in the Middle East and Africa will continue to impose additional operating costs on regional drone service providers.

High Upfront Cost and Weak Farm Financing

The Middle East and Africa agriculture drones market also faces financing and infrastructure barriers outside the most developed agriculture corridors. Upfront investment requirements remain high because growers must invest not only in drones but also in batteries, Real-Time Kinematic (RTK) positioning systems, spare parts, and operator training. Commercial agriculture spraying drones in South Africa are priced in the high USD 11,000 range before taxes, highlighting the significant capital commitment required for first-time adoption. In rural farming regions, infrastructure limitations and inconsistent technical support can also reduce the operational efficiency of precision spraying and mapping activities. As a result, shared-service and cooperative ownership models are emerging as important adoption pathways across the Middle East and Africa agriculture drones market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Fixed-Wing Economics Reshape Long-Horizon Growth

Rotary-wing drones accounted for the largest 65.0% share of the Middle East and Africa agriculture drones market in 2025, driven by their hover capability, low-altitude precision, and operational flexibility across spraying, crop surveillance, and livestock monitoring applications. Their adoption remains particularly strong in orchard, vineyard, and date-farming operations where precise low-level maneuverability is essential. In contrast, the fixed-wing platforms market is projected to grow at the fastest CAGR of 16.5% from 2026 to 2031, supported by rising adoption among large plantation operators seeking wider field coverage, longer flight endurance, and lower per-hectare surveying costs.

Hybrid-wing systems currently contribute less to overall revenue but are attracting interest from buyers seeking vertical takeoff capabilities combined with improved cruising efficiency for larger agricultural areas. In the Middle East and Africa agriculture drones market, rotary-wing systems dominate deployment volumes due to their suitability for spraying and short-range monitoring. However, fixed-wing and hybrid platforms are gradually gaining traction in applications requiring longer survey distances, broader field coverage, and higher operational efficiency, where hover performance is less critical. Over time, platform adoption is anticipated to become more application-specific, with rotary-wing drones maintaining dominance in precision spraying, while fixed-wing systems expand their role in plantation mapping and large-scale field intelligence operations.

By Component: Services Momentum Signals a Value-Chain Shift

Hardware accounted for the largest market share, 63.0%, in the Middle East and Africa agriculture drones market in 2025. This reflects the market's current emphasis on fleet deployment and core operational infrastructure. Growers across the region are prioritizing investments in aircraft platforms, payload systems, batteries, and supporting equipment before expanding into advanced analytics capabilities. In contrast, the services market is projected to grow at the fastest CAGR of nearly 17.2% from 2026 to 2031, driven by the increasing adoption of Drone-as-a-Service (DaaS) models. These models appeal to growers seeking lower upfront investment requirements and outsourced operational support.

The market is gradually transitioning from hardware-focused purchasing to recurring revenue models centered on analytics, agronomic advisory, operator training, and managed spraying services. This shift is enhancing the importance of software integration, field intelligence capabilities, regulatory support, and reliable execution quality in commercial farming operations. Consequently, companies that can integrate drone platforms with agronomic services and precision agriculture insights are projected to strengthen their competitive position in the Middle East and Africa agriculture drones market.

By Farming Environment: Indoor Agriculture Unlocks a Gulf-Led Niche

Outdoor farming accounted for the largest market share, 86.0%, in the Middle East and Africa agriculture drones market in 2025. This dominance is attributed to the region’s extensive open-field crop cultivation, orchard farming, and pasture-based agricultural systems. Large-scale farming operations in countries such as South Africa and Saudi Arabia are driving demand for drone-based applications, including spraying, crop monitoring, and field mapping. These trends are supported by larger farm sizes, higher crop values, and stronger capital availability in these regions. In contrast, the indoor farming market size is projected to grow at the fastest CAGR of 17.0% from 2026 to 2031, driven by increasing investments in controlled-environment agriculture and greenhouse farming projects across the Gulf region.

The indoor farming opportunity is closely tied to climate-resilient greenhouse infrastructure and controlled-environment agriculture systems, which require advanced monitoring of factors such as humidity, carbon dioxide levels, canopy health, and microclimate conditions. These specialized requirements are boosting demand for drone sensing technologies and precision monitoring capabilities, which are less prevalent in conventional outdoor operations. As a result, outdoor farming is projected to remain the primary revenue contributor, while indoor farming emerges as a high-value growth segment in the Middle East and Africa agriculture drones market.

By Application: Crop Spraying and Spreading Demand Reshapes the Application Revenue Mix

Crop monitoring and field surveillance accounted for the largest market share, approximately 38%, in the Middle East and Africa agriculture drones market by 2025. This growth is driven by lower capital requirements and the increasing adoption of precision agriculture practices in commercial farming operations. Field mapping and soil analysis continue to see strong demand, particularly among export-oriented farms that require accurate field records and survey-grade monitoring capabilities. Meanwhile, the crop spraying and spreading segment is projected to grow at the fastest CAGR of 18.0% from 2026 to 2031, supported by advancements in payload capacity, wider field coverage, and enhanced cost competitiveness compared to conventional spraying methods.

Variable-rate application, while currently a smaller segment, is gaining importance as growers focus on optimizing chemical usage, improving crop quality, and adopting prescription-based farming practices. Livestock monitoring applications are also expanding, particularly in large ranching operations, through the use of thermal and Red, Green, and Blue (RGB) imaging technologies. Furthermore, CropLife Africa Middle East’s 2025 guidance on drone-based pesticide application is fostering more consistent regulatory and compliance frameworks for agricultural spraying activities across the region. Consequently, the Middle East and Africa agriculture drones market is gradually transitioning from monitoring-focused applications to increased adoption of active crop treatment and precision spraying operations.

By Farm Size: Small and Medium-Sized Farms Emerge as a Volume Multiplier

Large-scale commercial farms held the largest market share, accounting for 62.0% of the Middle East and Africa agriculture drones market in 2025. This dominance is attributed to their ability to spread fleet costs across a larger area, manage compliance and training expenses, and leverage in-house technical capabilities for operations. These farms often focus on higher-value crops and operate within export-oriented production systems, thereby enhancing the economic feasibility of drone-supported monitoring and spraying. Conversely, the market size for small and medium-sized farms is anticipated to grow at the fastest CAGR of 16.8% from 2026 to 2031, driven by the adoption of shared-service and cooperative drone deployment models.

The key change is that small growers no longer need to buy a full fleet to participate in digital field operations. GreenCape’s smallholder sugarcane case in 2025 showed that a shared-service approach can reduce spray costs and improve application results, a commercial structure that can widen participation beyond large farm enterprises [3]Source: GreenCape, “The Business Case for Precision Drone Spraying, A Smallholder Sugarcane Cooperative in KwaZulu-Natal,” GreenCape, greencape.co.za. This makes small and medium-sized farms a volume multiplier for the Middle East and Africa agriculture drones market, even if average revenue per farm remains below that of large commercial operations. The long-term upside depends on whether service providers, cooperatives, and financing models can scale quickly enough to convert interest into routine use across dispersed grower clusters.

Geography Analysis

South Africa held the largest market share, accounting for 34.0% of the Middle East and Africa agriculture drones market in 2025, and it is also projected to be the fastest-growing country at a CAGR of 17.6% from 2026 to 2031. The country benefits from a diversified, export-oriented agricultural sector, including citrus, sugarcane, vineyards, and deciduous fruit cultivation. Additionally, it has a relatively mature commercial drone services ecosystem. Adoption is expanding beyond large commercial estates as shared-service and cooperative deployment models enhance accessibility for growers. These factors reinforce South Africa’s position as the leading regional market for precision spraying, crop monitoring, and drone-based field intelligence applications.

Saudi Arabia is also one of the fastest-growing agricultural drone markets in the region. Food security initiatives, water-efficiency requirements, and the increasing adoption of smart farming technologies in large-scale agricultural projects drive growth. The United Arab Emirates is also emerging as a key market, particularly for controlled-environment agriculture, greenhouse monitoring, and precision horticulture applications. Investments in climate-resilient farming systems and high-efficiency crop production technologies support this growth. Meanwhile, Egypt is gradually strengthening its position through precision irrigation initiatives and drone-supported agricultural monitoring programs to improve climate resilience and water management practices.

The broader Middle East and Africa regions present significant long-term growth potential. However, adoption in some markets is constrained by regulatory complexities, financing limitations, and infrastructure gaps. Service-led deployment models are projected to play a more prominent role than direct fleet ownership, especially among small and medium-sized farming operations. Efforts toward regulatory harmonization and evolving agricultural drone guidelines are anticipated to facilitate the wider adoption of drone-based spraying, crop monitoring, and precision agriculture applications across the region.

Competitive Landscape

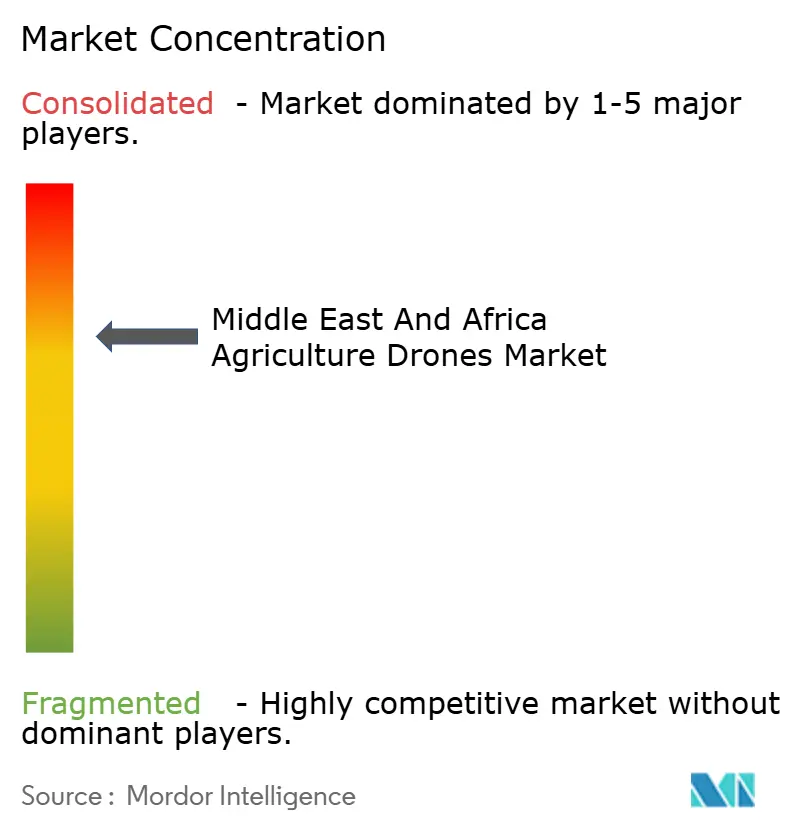

The Middle East and Africa agriculture drones market is moderately concentrated in 2025. The leading companies in this market include SZ DJI Technology Co., Ltd., XAG Co., Ltd., EagleNXT, Parrot Drone SAS, and Aerobotics. SZ DJI Technology Co., Ltd. maintains its leadership position due to its extensive agricultural drone portfolio, large installed base, and robust distribution network across South Africa and Gulf markets. XAG Co., Ltd. has secured a strong market position by focusing on autonomous agricultural operations and high-payload drone systems designed for commercial farming. Aerobotics distinguishes itself with orchard-focused analytics and crop intelligence solutions that support export-oriented fruit production systems.

Software and analytics capabilities are becoming increasingly significant in the Middle East and Africa agriculture drones market. Companies are moving beyond aircraft sales by incorporating drone imagery, field intelligence, mapping, and agronomic insights into comprehensive precision agriculture workflows. This trend is driving demand for data interpretation, crop-specific analytics, and operational support services in commercial farming. Specialized providers are strengthening their positions in niche applications such as orchard analytics, precision spraying, and livestock monitoring, where localized expertise and field-level insights are critical competitive advantages.

Strategic competition in the market is shifting from hardware scalability alone to integrated service delivery and precision agriculture ecosystems. Large manufacturers benefit from their broad product portfolios, extensive distribution networks, and fleet scalability. Meanwhile, smaller companies remain competitive by offering specialized analytics, localized technical support, and crop-specific operational expertise. The market is gradually transitioning toward integrated drone service models that combine aircraft access, agronomic intelligence, regulatory support, and field execution capabilities for commercial agriculture operations across the Middle East and Africa.

Middle East and Africa Agriculture Drones Industry Leaders

SZ DJI Technology Co., Ltd.

XAG Co., Ltd.

EagleNXT

Parrot Drone SAS

Aerobotics, (Pty) LTD

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: XAG Co., Ltd. unveiled the P150 Max at Agritechnica 2025, reflecting growing demand for heavy-payload agricultural drones designed to improve spraying efficiency and reduce labor dependency across commercial farming operations in the Middle East and Africa.

- September 2025: SZ DJI Technology Co., Ltd. launched the Agras T100 in South Africa, expanding the commercialization of high-capacity agricultural spraying drones for citrus, maize, sugarcane, and vineyard operations across large-scale farming regions.

- March 2025: BUCRA launched a drone-based sensing and digital irrigation advisory initiative in Egypt’s Nile Delta, supporting climate-resilient agriculture and precision water-management practices across North African farming systems.

Middle East and Africa Agriculture Drones Market Report Scope

The agricultural drones market comprises unmanned aerial vehicles (UAVs) used in farming activities, including crop monitoring, spraying, seeding, field mapping, irrigation assessment, and precision agriculture. These drones enhance farm productivity, optimize resource usage, reduce reliance on manual labor, and facilitate data-driven decision-making for both commercial and small-scale agricultural operations.

The Middle East and Africa Agriculture Drones Market is Segmented by Platform (Rotary Wing, Fixed Wing, and Hybrid Wing), by Component (Hardware, Software, and Services), by Farming Environment (Outdoor and Indoor), by Application (Crop Monitoring, Field Mapping, Crop Spraying, Variable Rate Application, and Livestock Monitoring), by Farm Size (Large-scale Commercial and Small and Medium-sized), and by Geography ( Middle East (Saudi Arabia, United Arab Emirates (UAE), and Rest of Middle East) and Africa (South Africa, Egypt, and Rest of Africa)). The Market Forecasts are provided in terms of Value (USD).

| Rotary Wing |

| Fixed Wing |

| Hybrid Wing |

| Hardware |

| Software |

| Services |

| Outdoor Farming |

| Indoor Farming |

| Crop Monitoring and Field Surveillance |

| Field Mapping and Soil Analysis |

| Crop Spraying and Spreading |

| Variable Rate Application |

| Livestock Monitoring |

| Large-scale Commercial Farms |

| Small and Medium-sized Farms |

| Middle East | Saudi Arabia |

| United Arab Emirates (UAE) | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Platform | Rotary Wing | |

| Fixed Wing | ||

| Hybrid Wing | ||

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Farming Environment | Outdoor Farming | |

| Indoor Farming | ||

| By Application | Crop Monitoring and Field Surveillance | |

| Field Mapping and Soil Analysis | ||

| Crop Spraying and Spreading | ||

| Variable Rate Application | ||

| Livestock Monitoring | ||

| By Farm Size | Large-scale Commercial Farms | |

| Small and Medium-sized Farms | ||

| By Geography | Middle East | Saudi Arabia |

| United Arab Emirates (UAE) | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of Middle East and Africa agricultural drones demand by 2031?

The sector is projected to reach USD 476.3 million by 2031, up from USD 226.8 million in 2026, supported by a 16.0% CAGR over 2026 to 2031.

Which country leads adoption across the region?

South Africa held the largest country share in 2025 at 34%, supported by its export-crop base and maturing commercial drone services ecosystem.

Which platform category leads current revenue?

Rotary-wing drones led platform revenue in 2025 with a 65% share because they fit spraying, monitoring, and low-altitude operations in fragmented farm settings.

Which application is expanding the fastest?

Crop spraying and spreading is the fastest-growing application, projected to advance at a 18% CAGR through 2031 as payload capacity and field coverage improve.

Page last updated on: