Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

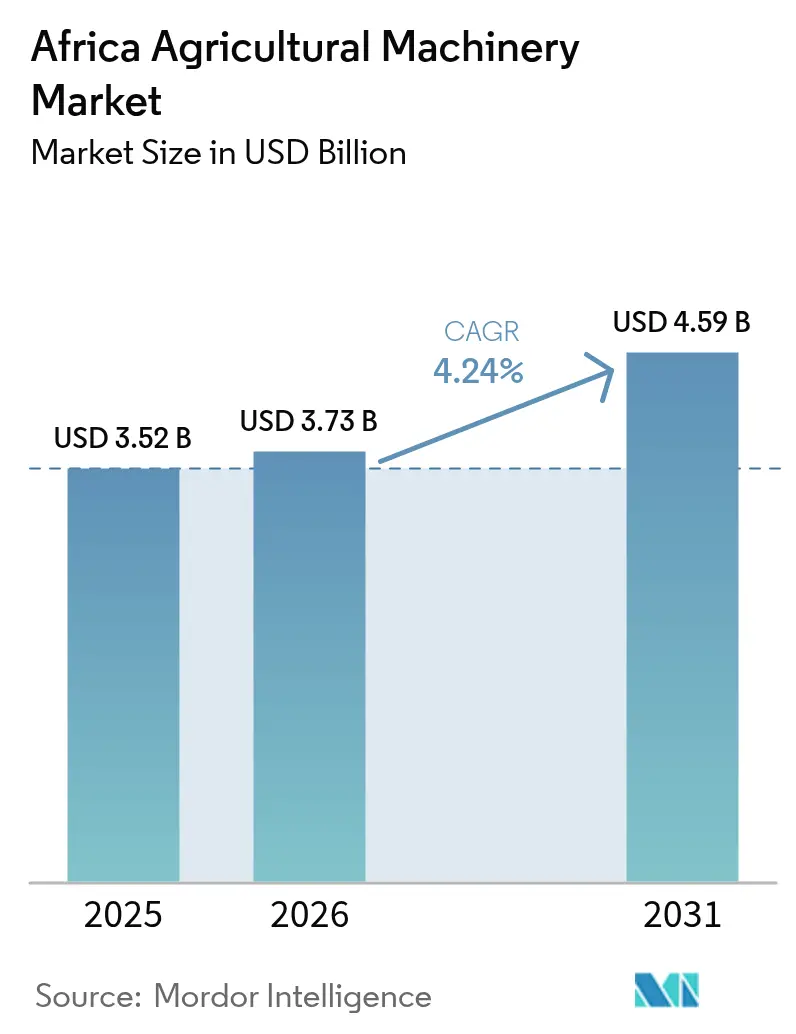

| Base Year Market Size (2025) | USD 3.52 Billion |

| Market Size (2026) | USD 3.73 Billion |

| Market Size (2031) | USD 4.59 Billion |

| Growth Rate (2026 - 2031) | 4.24% CAGR |

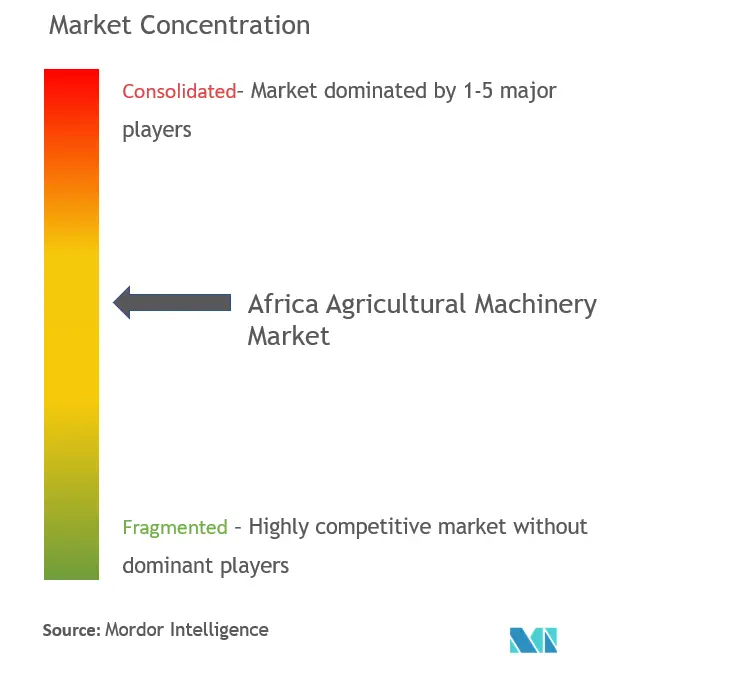

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Africa Agricultural Machinery Market Analysis by Mordor Intelligence

The Africa agricultural machinery market size is projected to grow from USD 3.52 billion in 2025 to USD 3.73 billion in 2026 and is forecast to reach USD 4.59 billion by 2031 at a 4.24% CAGR over 2026-2031. Rising digital financing models, government subsidy schemes, and climate adaptation pressures are driving millions of smallholders to mechanize field operations, opening new demand for compact tractors, sprayers, and irrigation equipment. In February 2026, Nigeria introduced the Renewed Hope National Agricultural Mechanisation Programme, aiming to support 1.2 million farmers and cover 1.5 million hectares annually. The program includes the phased distribution of 2,000 tractors and over 9,000 implements, managed by service providers through lease-to-own arrangements, with financial support from the Bank of Agriculture (BOA) and Heifer International. Kenya’s subsidy on eligible implements and Ethiopia’s pay-as-you-go tractor rentals are accelerating first-time purchases and rental hours, especially for machines below 40 horsepower. Precision agriculture requirements in export-oriented horticulture and stricter pesticide-residue ceilings are fueling rapid uptake of modern sprayers, while persistent rural labor shortages keep tractors at the core of equipment budgets. Manufacturers that wrap hardware with telematics, predictive maintenance, and usage-based credit are gaining an edge in a price-sensitive yet digitally connected customer base.

Key Report Takeaways

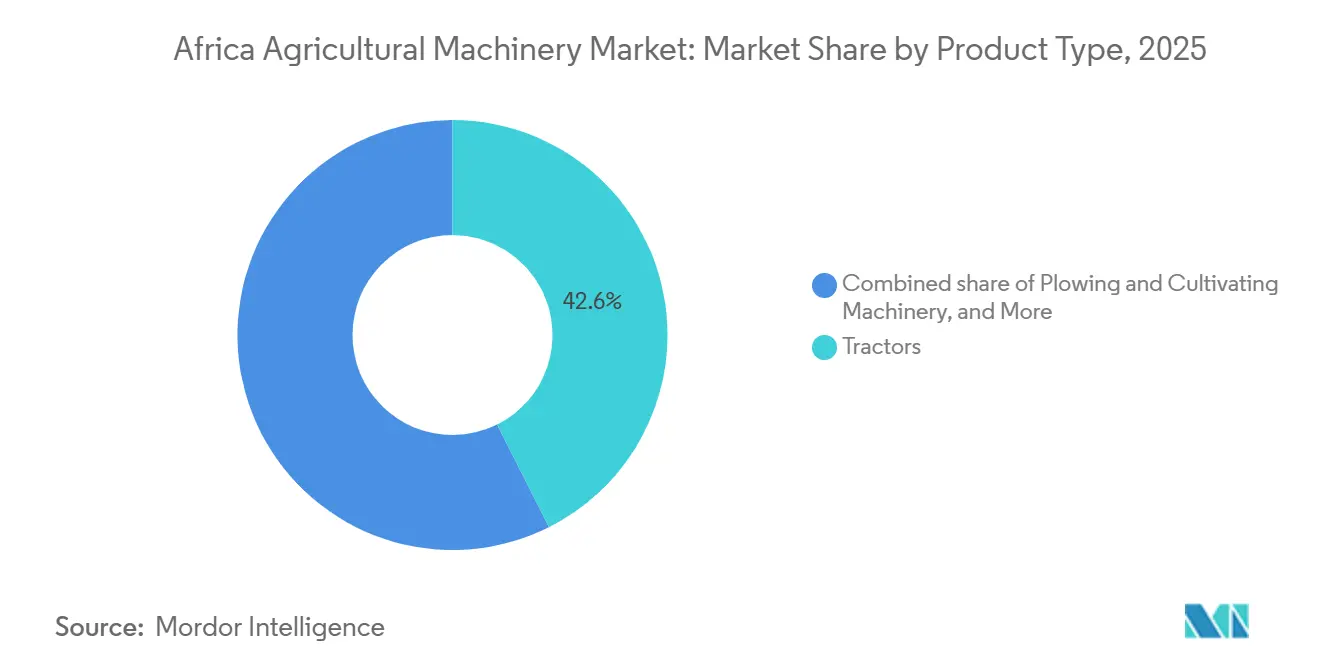

- By product type, tractors led with 42.6% of the Africa agricultural machinery market share in 2025, while sprayers posted the fastest expansion at a 5.1% CAGR through 2031.

- By geography, South Africa accounted for 27.5% of the Africa agricultural machinery market size in 2025, and Kenya recorded the highest projected CAGR of 4.9% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Agricultural Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining agricultural labor | +0.6% | Sub-Saharan centers such as Nigeria, Kenya, and Ethiopia | Medium term (2-4 years) |

| Government mechanization schemes and subsidies | +0.8% | Nigeria, Kenya, Ethiopia, and South Africa | Short term (≤ 2 years) |

| Pay-as-you-go equipment financing platforms | +0.7% | Kenya, Ethiopia, Uganda, expanding to Ghana and Nigeria | Medium term (2-4 years) |

| Digitization and telematics integration | +0.4% | South Africa, Kenya, and Nigeria | Long term (≥ 4 years) |

| Climate volatility accelerating mechanization | +0.5% | Sahel, Horn of Africa, and Southern Africa | Medium term (2-4 years) |

| Carbon-credit–linked mechanization incentives | +0.3% | Pilot zones in Kenya, South Africa, and Ghana | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Declining Agricultural Labor

Rural youth continue to migrate toward service jobs in growing urban centers, shrinking the seasonal workforce available for land preparation and harvest. In Nairobi, the monthly wage for a general laborer increased from USD 105.2 in 2018 to USD 124.9 in 2024, with similar increments observed in other municipalities, squeezing margins for farms under two hectares that traditionally relied on family labor[1]Source: Directorate of Labour Market Research and Analysis, "What Farm workers and Farmers should know about minimum wages and conditions of Employment in Kenya," labourmarket.go.ke. Cooperatives are countering by pooling resources to secure tractor hours through digital rental platforms and shared-ownership schemes that spread fixed costs across many users. According to the World Bank, in 2023, employment in the agricultural sector accounted for 34.3% of total employment in Nigeria [2]Source: World Bank, "Employment in agriculture (% of total employment)," worldbank.org. Between 2021 and 2023, this figure decreased by 7.4%, although the decline was irregular rather than consistent. Growing labor scarcity, therefore, acts as a structural push toward mechanization, even among conservative adopters.

Government Mechanization Schemes and Subsidies

Public programs are now subsidizing acquisition costs, reducing payback periods, and including operator training, significantly improving equipment affordability. These programs aim to make mechanization accessible to a broader range of farmers, including small-scale operators. Nigeria's February 2026 initiative aims to increase national mechanization levels from 12% to 25% by 2028 by providing discounted tractors and implements [3]Source: Federal Ministry of Agriculture and Food Security, Nigeria, “National Agricultural Mechanization Programme Launch,” fmard.gov.ng. This initiative is projected to address the challenges of low productivity and labor shortages in the agricultural sector. In 2023, the Kenyan Ministry of Agriculture introduced a National Agricultural Mechanization Policy and related initiatives to enhance farm mechanization, aiming to increase motorized power use from the current 30% to 50%. These efforts are designed to improve agricultural efficiency and output. These subsidies reduce break-even periods to less than four years, encouraging even small-scale operators to adopt mechanization, thereby fostering greater productivity and economic growth in the agricultural sector.

Pay-As-You-Go Equipment Financing Platforms

Tractor financing and leasing in Africa are undergoing significant changes, driven by technology-driven models such as Pay-As-You-Go (PAYG) and customized seasonal loan repayment plans. Digital platforms such as Hello Tractor, Trotro Tractor, and ETC Agro detach equipment access from outright ownership. Hello Tractor’s mobile platform lets farmers book services and pay per hectare through mobile money, reducing default risk for equipment owners. Smallholders in Ethiopia who utilized such services contributed to the national tractor hours in 2025, alleviating pressure on limited credit channels. The World Bank estimates that usage-based models can halve idle time, pushing owners to maximize operating hours and thereby improve debt service coverage. As rental reliability improves, farmers previously deterred by high down payments begin experimenting with mechanization.

Digitization and Telematics Integration

Embedded sensors now transmit data on fuel consumption, location, and maintenance alerts to cloud-based dashboards, helping to significantly reduce unplanned downtime and minimize theft. Deere & Company’s JDLink and CNH Industrial N.V.’s AFS Connect are increasingly being integrated into new tractors sold in South Africa, with adoption rates anticipated to grow substantially in the coming years. Predictive maintenance routines have proven effective in significantly decreasing emergency repairs on estates that have implemented connected fleets. For rental operators, telematics systems provide accurate verification of the land area serviced, enabling pay-for-use invoicing that ensures transparency and mutual satisfaction for both equipment owners and farmers. However, connectivity challenges in rural areas of Nigeria and Ethiopia continue to hinder widespread adoption, although planned expansions of mobile networks are anticipated to improve coverage and support broader implementation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented after-sales service networks | −0.6% | Rural Nigeria, Ethiopia, and many interior markets | Medium term (2-4 years) |

| High up-front equipment costs | −0.9% | Smallholder-dominated belts across Sub-Saharan Africa | Short term (≤ 2 years) |

| Counterfeit and gray-market imports | −0.4% | Nigeria, Kenya, and secondary ports across West Africa | Medium term (2-4 years) |

| Persistent foreign-exchange volatility | −0.5% | Nigeria, Egypt, and Ethiopia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented After-Sales Service Networks

The limited presence of dealers in rural areas forces tractor owners to wait for extended periods to access certified technicians or genuine parts. A large portion of tractors in Nigeria are situated at considerable distances from authorized workshops, leaving operators with no choice but to rely on informal mechanics. These mechanics often perform repairs that void warranties, creating additional challenges for owners. Manufacturers have introduced initiatives such as mobile service vans and remote diagnostics to address these issues. However, these solutions are heavily dependent on reliable connectivity and adequate technician training, both of which remain inconsistent across the country. In the absence of a robust service infrastructure, tractor utilization rates decline significantly, resulting in lower returns on mechanization investments and discouraging future purchases.

Counterfeit and Gray-Market Imports

Unlicensed clones and counterfeit spare parts are often sold at much lower prices than genuine products, making them appealing to buyers focused on minimizing costs. However, these counterfeit products significantly reduce the operational lifespan of machines, leading to higher long-term expenses for users. Nigerian trade bodies have highlighted that a considerable share of the aftermarket is influenced by counterfeit components. The absence of robust border controls and the inconsistent enforcement of intellectual property regulations discourage original equipment manufacturers from investing in local assembly operations. This reliance on imported products further undermines the reputation and value of established brands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Tractors Remain the Revenue Anchor and Sprayers Post the Fastest Pace

Tractors are the largest product type, accounting for 42.6% of the Africa agricultural machinery market share in 2025, with units under 40 horsepower representing a significant share of sales, as the majority of farms remain below 2 hectares. Compact machines double as transport vehicles and power sources for simple implements, explaining their popularity in Kenya, Ethiopia, and Ghana. The Africa agricultural machinery market size for tractors is projected to grow as financing schemes make ownership viable for cooperatives and contract service providers. Medium-power tractors between 40 and 99 horsepower are gaining ground among estates pooling acreage, while models above 100 horsepower stay concentrated in South Africa and Egypt.

Sprayers expand at a 5.1% CAGR through 2031, the highest among all categories, as export-oriented horticulture faces tighter residue ceilings under European Union safety rules. Precision sprayers that cut chemical volumes are spreading in Kenyan floriculture clusters, aided by subsidies that reimburse half the purchase cost. The Africa agricultural machinery market for sprayers is anticipated to grow significantly, driven by rising pest pressure linked to warmer temperatures. Although starting from a smaller base, growth outpaces every other segment as climate-resilient crop management becomes a policy priority.

Geography Analysis

South Africa is the largest country, accounting for 27.5% of the Africa agricultural machinery market in 2025, driven by a high mechanization rate and robust dealer infrastructure. Load-shedding disruptions in 2024 and 2025 forced some assembly plants to import fully built units, nudging prices upward, yet tax rebates for irrigation gear sustained buyer interest. Export sales into Zambia and Botswana further underpin demand, keeping South Africa a regional supply hub even as domestic growth moderates.

Kenya is the fastest-growing country, advancing at a 4.9% CAGR through 2031 as Vision 2030 targets lifting mechanization from 18% in 2025 to 40% by 2030. Tractor imports saw a significant increase, with a particular emphasis on models designed for smaller agricultural plots. Digital rental platforms, such as Hello Tractor and Trotro Tractor, have deployed thousands of units across the country. These platforms provide services based on the area cultivated, aligning costs with farmers' harvest revenues. Additionally, they generate data trails that help evaluate creditworthiness.

Nigeria, Egypt, and Ethiopia collectively account for a significant share of the Africa agricultural machinery market. Nigeria’s February 2026 subsidy program targets a mechanization leap, yet it still faces sparse service centers and exchange-rate swings. Egypt channels public funds into drip and sprinkler irrigation systems to safeguard yields in water-scarce zones, although smallholders cite limited access to credit as a barrier. Ethiopia’s pay-as-you-go tractor adoption expanded plowed acreage five-fold between 2020 and 2025, proving that usage-based finance can unlock latent demand. Remaining African markets, such as Ghana, Tanzania, and Uganda, show single-digit penetration, constrained by thin dealer networks and smaller capital pools.

Regulatory Landscape

Regulation of agricultural machinery across Africa is largely country-led, with growing emphasis on pre-market testing, registration, and standards compliance to limit gray-market inflows and raise safety and durability. Kenya anchors policy through its National Agricultural Mechanization Policy (2023), which calls for machinery standards enforcement in collaboration with the Kenya Bureau of Standards (KEBS), while Nigeria uses the National Centre for Agricultural Mechanization (NCAM) for testing, evaluation, and certification of tools and equipment used in public programs and procurement. In Tanzania, the Centre for Agricultural Mechanization and Rural Technology (CAMARTEC) sets out compulsory testing for agricultural machinery before importation or use, and Rwanda applies technical regulation requiring registration of agricultural machinery and licensing of manufacturers, importers, and distributors.

Regionally, the African Union Commission has pushed policy convergence through the Framework for Sustainable Agricultural Mechanization in Africa (SAMA), which guides member states on national policies, machinery quality, and testing infrastructure. Broader SPS policy work also intersects with crop protection equipment and residue compliance. Trade facilitation initiatives under the African Continental Free Trade Area (AfCFTA) aim to reduce tariffs and non-tariff barriers, but rules-of-origin and different national conformity processes continue to influence how OEMs structure distribution, local assembly, and after-sales footprints across Africa.

Competitive Landscape

The Africa agricultural machinery market shows moderate concentration. Top players Deere & Company, CNH Industrial N.V., AGCO Corporation, Mahindra & Mahindra Limited, and Kubota Corporation collectively hold a significant share of revenue in 2025. Corporations dominate the premium tier by integrating hardware with telematics, credit programs, and comprehensive parts distribution. Mahindra & Mahindra Limited, Kubota Corporation, and Tractors and Farm Equipment Limited (TAFE) challenge incumbents with tractors priced lower and feature sets tailored to smallholder chores. Chinese suppliers such as Weichai Lovol Intelligent Agricultural Technology Co., Ltd. leverage cost leadership and flexible payment terms to penetrate West African corridors.

Digitization has become a key differentiator. CNH Industrial N.V. established a parts hub in Nairobi in 2024, significantly reducing lead times from four weeks to five days and enhancing after-sales reliability across East Africa. This development has not only improved operational efficiency but also bolstered the company's market presence by enabling faster delivery of parts, thereby effectively addressing critical customer needs. AGCO Corporation's trial of electric tractors on South African horticultural estates highlights how sustainability initiatives can unlock higher-margin micro-segments.

Local assemblers in Nigeria and Kenya source knocked-down kits to bypass import duties, producing competitively priced units but sometimes at the expense of consistent quality. Counterfeit spares erode margins and brand trust, pressing original producers to invest in hologram labels and dealer audits. As emissions rules tighten and ISO 9001 certification becomes a tender prerequisite, smaller unlicensed players may exit, nudging the market toward gradual consolidation.

Africa Agricultural Machinery Industry Leaders

-

Deere & Company

-

CNH Industrial N.V.

-

AGCO Corporation

-

Kubota Corporation

-

Mahindra & Mahindra Limited

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Program-backed procurement and service-model mechanization are creating near-term demand clusters for tractors, implements, and irrigation equipment, particularly where leasing, fleet operations, and maintenance arrangements support sustained utilization. Nigeria launched the Renewed Hope National Agricultural Mechanisation Programme in February 2026, targeting 1.2 million farmers and 1.5 million hectares annually, with phased distribution of 2,000 tractors and over 9,000 implements via service providers and lease-to-own structures supported by the Bank of Agriculture (BOA) and Heifer International. Similar capital formation signals also showed up elsewhere in 2026, including Ethiopia distributing mechanization equipment valued at 2.32 billion Birr to regional states, and sovereign-linked machinery financing packages in Togo that reference multi-thousand-unit tractor and seeding/harvesting line items.

Access models built around payments and compliance are also expanding opportunities beyond basic horsepower, especially for sprayers and connected fleet services. Export-oriented horticulture in East and Southern Africa is pulling adoption toward precision sprayers that manage dosing and documentation, which supports demand for higher-spec tractor-mounted, trailed, and self-propelled systems and raises requirements for genuine parts and calibrated service. As digital platforms and data trails spread across pay-as-you-go and booking models (including Hello Tractor and similar platforms referenced in the market context), vendors can bundle equipment with telematics, usage-based credit, and mobile service. At the same time, policy-linked standardization efforts (SAMA and national testing regimes) create differentiation space for OEMs and dealers through certified products, trained operators, and faster parts availability.

Recent Industry Developments

- June 2026: Tata Africa, a John Deere dealer, opened a new branch in Saint-Louis, Senegal, adding workshop capacity, parts availability, and localized service coverage. The expansion improves after-sales reach in a West African corridor where downtime and parts lead times can deter equipment adoption, and it supports higher utilization for rental and contractor fleets.

- February 2026: CNH Industrial (New Holland) officially launched a strategic partnership with Inchcape Kenya as the authorized full-range importer for Kenya. The arrangement expands distribution and service touchpoints, improving access to tractors and implements for small and mid-sized farms and aligning with Kenya-focused mechanization policy momentum.

- August 2024: AGCO Corporation opened a regional office in Casablanca, Morocco, to serve as a sales hub for West and North Africa and to coordinate its Agri-Parks initiative. Establishing a regional base supports closer dealer management and program execution, helping accelerate bundled offerings that combine equipment access with training and service infrastructure.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the sales value of farm machinery used to prepare land, plant, irrigate, protect crops, and harvest across Africa, counted at the point where equipment is sold into agricultural use through OEMs and distribution channels.

Scope exclusions: We exclude stationary post-harvest processing lines and non-farm construction equipment even when it is sometimes used on farms.

Segmentation Overview

-

By Product Type

-

Tractors

- Less than 40 HP

- 40 - 99 HP

- 100 HP and Above

-

Plowing and Cultivating Machinery

- Plows

- Harrows

- Rotovators and Cultivators

- Other Equipment

-

Planting Machinery

- Seed Drills

- Planters

- Spreaders

- Other Planting Machinery

-

Sprayers

- Handheld/Knapsack

- Tractor-Mounted

- Trailed/Pull-Type

- Self-Propelled

- UAV/Drone Sprayers

-

Irrigation Machinery

- Drip Irrigation Systems

- Sprinkler Irrigation Systems

- Other Irrigation Machinery

-

Harvesting Machinery

- Combine Harvesters

- Other Harvesting Machinery

-

Haying and Forage Machinery

- Mowers and Conditioners

- Balers

- Other Haying and Forage Machinery

-

Tractors

-

By Geography

- Nigeria

- South Africa

- Kenya

- Egypt

- Ethiopia

- Rest of Africa

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by aligning what gets counted as agricultural machinery for Africa, and then mapping the demand signals that can be checked country by country. We used public sources such as FAOSTAT for cropped area and production indicators, World Bank and IMF series for macro variables, UN Comtrade for machinery trade flows, and national agriculture ministry releases for mechanization programs and subsidy schemes.

To keep inputs realistic, secondary reading also included customs and port updates, association websites, and publicly available company filings and investor decks for channel structure and product mix. Where gaps existed on market structure and player coverage, a paid subscription focused on company financials and another covering import and export shipment intelligence were used only to cross-check directional shares and price ranges. The sources listed here are illustrative only, and many other public documents were referred to for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary conversations were done with equipment manufacturers, distributors and dealers, rental and contracting operators, and large farm buyers, and then with local experts close to financing and mechanization schemes. Since this is a regional market, discussions were spread across North, East, West, and Southern Africa so pricing, import dependence, and adoption timing could be compared and then used to refine assumptions that were unclear in desk findings.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 16% | |

| Mid tier: 46% | Functional/Unit leaders: 41% | |

| Smaller Players: 20% | Managers: 43% |

Market-Sizing & Forecasting

Sizing began with a top-down reconstruction where the addressable demand pool was built from mechanized acreage and crop mix by key countries, which was then translated into equipment needs by typical operations (land preparation, planting, crop protection, irrigation, and harvesting). From there, category splits were applied using observed adoption patterns, replacement cycles, and financing access, and the results were converted to value using country-specific price ladders and mix shifts.

To keep the totals grounded, selective bottom-up checks were also run using dealer channel checks, sampled unit volumes for tractors and key implements, and average selling price ranges that were validated through interviews. Inputs that materially moved the model included tractor penetration by farm size, share of imported equipment versus local assembly, diesel and input-cost pressure that affects purchasing timing, subsidy and mechanization program rollouts, and crop intensity that drives utilization. Forecasts were built using scenario analysis, where base, faster mechanization, and slower credit availability cases were tested, and then aligned to what experts expected for financing, rainfall volatility, and policy continuity. When country-level detail was thin, gaps were handled by using proxy indicators like cultivated area, import trends, and peer country adoption ratios, followed by a reasonableness pass with field feedback.

Data Validation & Update Cycle

Outputs were validated through triangulation across independent signals, including trade data direction, policy program announcements, and dealer reported demand changes, before any number was finalized. Where unusual spikes appeared, assumptions were re-checked, and follow-up calls were triggered to confirm whether the change was price-led, volume-led, or driven by one-time tenders.

A multi-step internal review is followed so model logic, unit economics, and country rollups are consistent, and then the final results are signed off. The report is refreshed annually, and interim updates are made when material events occur, such as subsidy resets, FX shocks, or large program tenders. Before delivery, a fresh review pass is completed so the client receives the most current view available.

Mordor Intelligence's Africa Agricultural Machinery Market Estimate Compared With Other Published Estimates

Published values for Africa agricultural machinery often do not match because the included equipment set, the year of pricing, and the way imports and local assembly are treated can differ by publisher. Differences also come from whether estimates lean on trade flows, on-farm adoption, or a mix of both, which can shift totals in markets where credit and programs change year to year.

The main gap comes from what is counted inside the equipment basket and when prices are converted to USD, and in this study Mordor Intelligence counts only farm-use machinery categories like tractors, planting, irrigation, sprayers, and harvesting equipment, and then applies country-level price ladders that are refreshed with dealer feedback instead of using a single regional average.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.52 B (2025) | |

| Regional Consultancy A | USD 4.60 B (2024) | Uses a broader framing that appears to lean heavily on recent import and sales momentum, and the base year is earlier, which can lift totals when FX and pricing shifted afterward. |

| Global Consultancy B | USD 5.50 B (2026) | Presents a forward year value range and likely layers in a faster mechanization scenario, which can overstate near-term demand where financing access and subsidy execution vary by country. |

The table shows that most of the spread is explained by scope breadth, base year choice, and how quickly adoption is assumed to rise in the forecast step. By keeping variables tied to mechanized area, equipment mix, and locally validated pricing, the estimate stays easier to trace and repeat when conditions change.

Key Questions Answered in the Report

What is the projected value of Africa agricultural machinery market in 2031?

The market is forecast to reach USD 4.59 billion by 2031.

Which product category holds the largest revenue share?

Tractors led with 42.6% share in 2025.

Which product type is growing the fastest?

Sprayers show the quickest expansion at a 5.1% CAGR through 2031.

Which country is projected to record the highest growth rate?

Kenya is projected to grow at 4.9% CAGR between 2026 and 2031.

What role do government subsidies play in mechanization?

Programs in Nigeria, Kenya, and Ethiopia lower acquisition costs and shorten payback periods, encouraging smallholders to adopt machinery.

Page last updated on: