Middle East and North Africa Agriculture Market Analysis by Mordor Intelligence

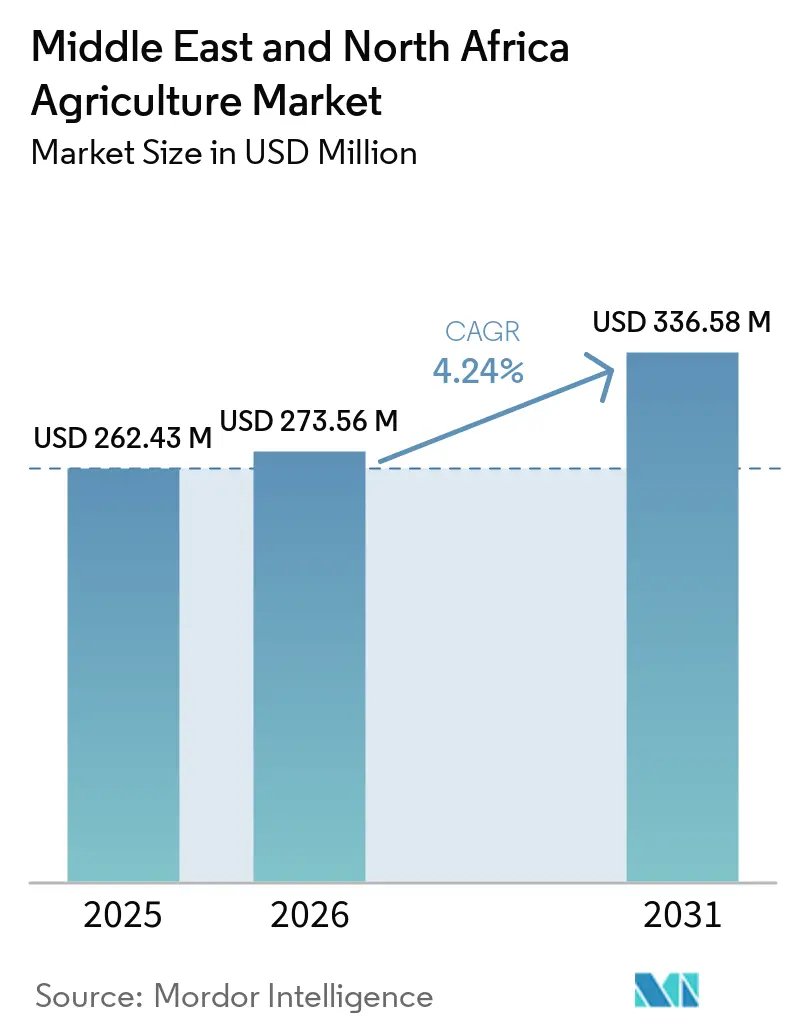

The Middle East and North Africa agriculture market size is expected to grow from USD 262.43 billion in 2025 to USD 273.56 billion in 2026 and is forecast to reach USD 336.58 billion by 2031 at 4.24% CAGR over 2026-2031. The region is shifting from import dependence to regional food production through investments in irrigation infrastructure, desalination-powered hydroponics, and climate-controlled greenhouses. According to the International Center for Agricultural Research in the Dry Areas (ICARDA), date palm cultivation remains significant in the Middle East and North Africa's economy, history, and culture. The region produces 1.9 million metric tons of date palm, accounting for 29% of global production and 33% of global date palm acreage in 2024[1]Source: International Center for Agricultural Research in the Dry Areas (ICARDA), "Date Palm", icarda.org. Government investments in water infrastructure and reduced membrane filtration costs have made desert cultivation economically feasible. The growth of agri-fintech platforms has improved smallholder access to working capital, while bilateral grain agreements have reduced price volatility and encouraged large-scale production. While multinational processors establish regional operations, local companies maintain their market positions through proximity advantages, local expertise, and supportive policies.

Key Report Takeaways

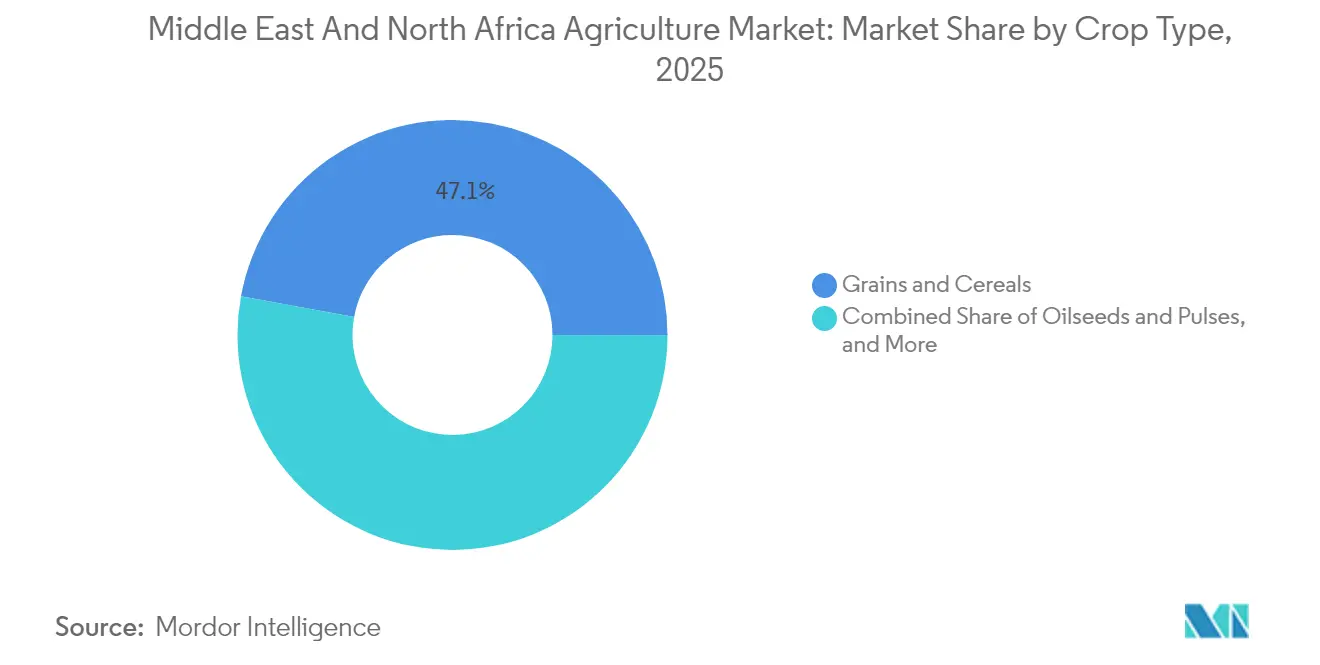

- By crop type, grains and cereals held 47.12% of the Middle East and North Africa agriculture market share in 2025, while oilseeds and pulses are forecast to expand at a 4.86% CAGR through 2031, the fastest among all segments.

- By geography, North Africa accounted for 40.05% of the Middle East and North Africa agriculture market size in 2025, whereas the Middle East is poised to expand at a 4.62% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East and North Africa Agriculture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-backed mega-irrigation expansion programs | +1.2% | Middle East core, North Africa expansion | Medium term (2-4 years) |

| Accelerated adoption of climate-smart greenhouse systems | +0.8% | Gulf Cooperation Council, Egypt, and South Africa | Short term (≤ 2 years) |

| Rapid rise of agri-fintech platforms improving farm liquidity | +0.6% | East Africa, Nigeria, and Egypt | Short term (≤ 2 years) |

| Growing intra-country grain procurement agreements | +0.5% | Egypt, Algeria, and Morocco | Medium term (2-4 years) |

| Scaling desalination-powered hydroponics | +0.4% | United Arab Emirates, Saudi Arabia, and Jordan | Long term (≥ 4 years) |

| Emergence of carbon-credit revenues for conservation tillage | +0.3% | Kenya, Ethiopia, and South Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government-Backed Mega-Irrigation Expansion Programs

Government-funded irrigation projects are transforming agricultural production patterns across the Middle East and North Africa. Jordan's USD 5 billion desalination plant, scheduled for January 2025, will provide fresh water for 300 km of new agricultural zones. Egypt's Mustaqbal Misr project aims to convert 1.5 million feddans of desert into arable land. Saudi Arabian research institutes are developing salt-tolerant crop varieties specifically designed for desalinated water irrigation. Ethiopia's investment forum showcased USD 600 million in domestic irrigation equipment manufacturing capacity, indicating progress toward agricultural self-sufficiency and employment growth. These developments, combined with decreasing desalination costs, are establishing water-secure agricultural corridors that will support the Middle East and North Africa agriculture market's long-term growth[2]Source: International Finance Corporation, “Food Systems Development Program,” ifc.org.

Accelerated Adoption of Climate-Smart Greenhouse Systems

Climate challenges, including heat waves and irregular rainfall patterns, have driven increased adoption of controlled-environment farming in the Middle East and North Africa (MENA) region. The United Arab Emirates uses multi-tiered glasshouses that reduce water consumption by 90% compared to open-field farming while minimizing seasonal yield variations. Saudi Arabian coastal resorts implement advanced heat-blocking covers that maintain temperatures below 30°C inside greenhouses, even when external temperatures exceed 45°C. Government support through subsidized electricity rates and streamlined organic certification processes reduces operational costs. Farmers report investment recovery within four years, supported by premium pricing for consistent year-round supply. The transition to advanced greenhouse technology strengthens the Middle East and North Africa agricultural market's competitive position.

Growing Intra-Country Grain Procurement Agreements

Direct government purchasing agreements are stabilizing producer incomes and national reserves across key markets. Egypt secured 3.5 million metric tons of wheat from Russia through bilateral contracts in 2025, eliminating exchange premiums and providing farmers with fixed reference prices. In 2024, Nigeria implemented a minimum price program covering 250,000 wheat growers, supported by the African Development Bank, enabling reliable cash flow planning. Morocco and Algeria have established comparable systems to shield their markets from global price volatility. These guaranteed purchase agreements enhance financing opportunities for storage and processing infrastructure, strengthening supply chain stability in the Middle East and North Africa agriculture market[3]Source: African Development Bank, “Country Strategy Paper Nigeria 2025-2029,” afdb.org.

Scaling Desalination-Powered Hydroponics

Gulf countries combine solar energy with membrane desalination to operate nutrient-film greenhouses in arid regions. United Arab Emirates demonstration farms achieve lettuce yields of 320 metric tons per hectare while using 15 liters of water per kilogram of produce. Jordan intends to implement desalinated water distribution through gravity-fed drip systems, reducing pumping energy consumption by 35%. Research facilities are developing optimized nutrient solutions to address mineral imbalances in desalinated water. The successful expansion of these systems will enable the cultivation of high-value horticultural crops across thousands of hectares, contributing to the growth of the Middle East and North Africa agriculture market[4]Source: King Abdullah University of Science and Technology, “Desalinated Water for Agriculture,” kaust.edu.sa.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dependence on imported seed genetics and inputs | -0.7% | Region-wide with acute impact in Gulf | Medium term (2-4 years) |

| Pollination inefficiencies in vertical farms | -0.4% | United Arab Emirates, Saudi Arabia, and Egypt | Short term (≤ 2 years) |

| Fragmented land-holding patterns | -0.6% | Sub-Saharan Africa, and Egypt | Long term (≥ 4 years) |

| Limited cold-chain nodes between farmgate and ports | -0.5% | Nigeria, Kenya, and Morocco | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Dependence on Imported Seed Genetics and Inputs

Commercial seed in core markets primarily comes from overseas breeders, which exposes growers to foreign exchange risks and potential export restrictions. Ethiopia's seed audit revealed yield reductions of up to 30% when imported hybrid seeds are planted outside their intended agro-ecological zones. Gulf producers experience similar challenges with fertilizer supply, as shipping disruptions can delay essential top dressings. While national seed-multiplication programs are expanding, the time required for varietal development indicates that import dependency will continue in the medium term, constraining growth in the Middle East and North Africa agriculture market[5]Source: U.S. Department of Agriculture Foreign Agricultural Service, “Seed Sector Assessment Ethiopia,” fas.usda.gov.

Pollination Inefficiencies in Vertical Farms

Indoor vertical farms growing lettuce and strawberries require controlled pollination processes, which increase operational costs. Both manual and robotic pollination methods are labor-intensive and yield inconsistent results, reducing fruit production rates. Research on bumblebee micro-colonies and electrostatic pollen dispensers shows promise, these solutions are not yet commercially viable for large-scale operations. The lack of efficient pollination systems keeps operating margins low in vertical farms, limiting their ability to meet the increasing agricultural demand in the Middle East and North Africa region.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Crop Type: Grains and Cereals anchor food resilience while oilseeds and Pulses capture high-margin expansion

Grains and cereals hold 47.12% of the Middle East and North Africa agriculture market share in 2025, serving as essential components of regional diets and strategic reserves. Egypt's public wheat procurement reached 14.4 million metric tons in 2024 through direct contracts, providing millers with a consistent supply and strengthening domestic food security. Nigeria's irrigation-focused rice production, backed by minimum price guarantees, is increasing average yields to 4.5 metric tons per hectare, reducing import requirements and stabilizing urban market prices. North African barley production meets both human consumption and animal feed needs, creating balanced demand patterns that provide steady income for farmers. The implementation of precision planting technologies and remote sensing improves input efficiency across extensive grain fields, maintaining the segment's dominant position in the Middle East and North Africa agriculture market.

The oilseeds and pulses segment is projected to grow at a 4.86% CAGR through 2031. Nigeria's soybean production region has secured USD 2 billion in processing facility investments, with potential annual export revenues of USD 200 million in the coming decade. Ethiopia and Egypt are expanding chickpea and fava bean production to meet increasing protein demand from urban consumers focused on health. Local processing facilities prefer domestic supply sources to reduce transportation costs associated with imported meals, supporting the expansion of cultivation areas. The development of drought-resistant, short-duration crop varieties improves yields and water efficiency, supporting the continued growth of this rapidly expanding segment in the Middle East and North Africa agriculture market.

Geography Analysis

North Africa accounted for 40.05% of the Middle East and North Africa agriculture market share in 2025, by utilizing its European proximity and Mediterranean climate advantages. Egypt's Suez Canal Economic Zone functions as an export hub with cold-chain connections that reduce transit times to Gulf markets, reinforcing the strategic role of Egypt Agriculture in regional food supply chains. Morocco and Tunisia focus on citrus and olive oil production, benefiting from European Union duty-free quotas. Algeria develops durum wheat and hard-red wheat varieties to fulfill domestic pasta requirements. The implementation of organic certification and traceability regulations increases as producers target higher margins from health-conscious consumers, enhancing revenues in the Middle East and North Africa agriculture market.

The Middle East agricultural market is projected to grow at a CAGR of 4.62% through 2031. The Arabian Peninsula influences agricultural production through capital-intensive, climate-controlled systems to address limited arable land constraints. Saudi Arabia's Vision 2030 food security initiative supports vertical farming facilities that produce 16 metric tons of leafy greens monthly, integrating solar power with liquid-fertilizer recirculation systems. In the United Arab Emirates, producers utilize renewable-powered desalination and AI-controlled climate systems, achieving year-round production while conserving 90% of water resources. Jordan's USD 5 billion desalination canal project, planned for completion in 2025, aims to irrigate newly reclaimed areas for increased staple crop production. These infrastructure developments reduce the region's reliance on maritime imports and support the expansion of the Middle East and North Africa agriculture market.

Sub-Saharan Africa presents significant growth potential through improved smallholder productivity and technology-enabled input access. Nigeria's Special Agro-Industrial Processing Zones establish infrastructure networks including feeder roads, electricity, and storage facilities, drawing investments from milling and oilseed processing companies. Ethiopia's Digital Agriculture Roadmap, launched in June 2025, provides 25 e-service modules, delivering market data, advisory services, and remote diagnostics to over 10 million users. Kenya's carbon-credit initiative rewards regenerative farming practices, providing additional income to rural areas. Infrastructure investments in rail and ports decrease inland transportation costs, expanding market access and supporting growth in the Middle East and North Africa agriculture market.

Recent Industry Developments

- September 2025: Saudi Arabia's Agricultural Development Fund (ADF) approved SAR 473 million (USD 126.1 million) in financing and credit facilities across the Kingdom. The funding includes development loans for farmers and project financing across various sectors, including poultry farming, greenhouse vegetable production, inland fish farming, date purchasing operations, and date manufacturing industries.

- September 2025: The United Arab Emirates Ministry of State for Artificial Intelligence has established a strategic partnership with Abu Dhabi Agriculture and Food Safety Authority (ADAFSA) to enhance AI applications in food security. This collaboration aligns with the United Arab Emirates' National Food Security Strategy 2051, which aims to position the country as the leading nation in the Global Food Security Index by 2051.

- April 2025: The Nigerian Federal Government implemented the National Agribusiness Policy Mechanism (NAPM) to enhance agricultural productivity, regulate food prices, and promote economic growth. The NAPM integrates with existing initiatives to transform the agricultural sector through evidence-based policies and public-private collaborations.

- February 2025: Ethiopia launched its Digital Agriculture Roadmap (DAR) 2025-2032 to modernize its agricultural sector through digital technologies and services. The roadmap aims to support farmers, especially smallholders, by providing real-time market data, mobile credit access, and digital agricultural extension services to improve productivity, resilience, and livelihoods.

Middle East and North Africa Agriculture Market Report Scope

Agriculture is the science or practice of farming, including the cultivation of the soil to grow crops and the rearing of animals to provide food, wool, and other products. The Middle East and North Africa Agriculture Market is Segmented by Crop Type (Food Crops/Cereals, Fruits, Vegetables, and Oilseeds/Non-food Crops). The Report includes Production Analysis (Volume), Consumption Analysis (Value and Volume), Export Analysis (Value and Volume), Import Analysis (Value and Volume), and Price Trend Analysis for each of the abovementioned segments. The market estimation and forecasts are provided in value (USD) and volume (Metric Tons) for the above-mentioned segments.

By Crop Type (Production Analysis (Volume), Consumption Analysis (Volume and Value), Import Analysis (Volume and Value), Export Analysis (Volume and Value), and Price Trend Analysis)

| Grains and Cereals |

| Oilseeds and Pulses |

| Fruits and Vegetables |

| Forage and Fodder Crops |

By Geography

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Bahrain | |

| Kuwait | |

| Oman | |

| Qatar | |

| Rest of Middle East | |

| North Africa | Egypt |

| Libya | |

| Algeria | |

| Morocco | |

| Tunisia | |

| Sudan | |

| Rest of North Africa |

| By Crop Type (Production Analysis (Volume), Consumption Analysis (Volume and Value), Import Analysis (Volume and Value), Export Analysis (Volume and Value), and Price Trend Analysis) | Grains and Cereals | |

| Oilseeds and Pulses | ||

| Fruits and Vegetables | ||

| Forage and Fodder Crops | ||

| By Geography | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Bahrain | ||

| Kuwait | ||

| Oman | ||

| Qatar | ||

| Rest of Middle East | ||

| North Africa | Egypt | |

| Libya | ||

| Algeria | ||

| Morocco | ||

| Tunisia | ||

| Sudan | ||

| Rest of North Africa | ||

Key Questions Answered in the Report

What is the projected value of the Middle East and North Africa agriculture market in 2031?

The market is forecast to reach USD 336.58 billion by 2031, up from USD 262.43 billion in 2025.

Which crop type currently generates the largest revenue?

Grains and cereals hold 47.12% of Middle East and North Africa agriculture market share due to their staple role in regional diets.

Which crop type is expanding the fastest?

Oilseeds and pulses are growing at a 4.86% CAGR through 2031, driven by rising protein demand and processor investment.

How are governments supporting irrigation expansion?

Sovereign-funded megaprojects such as Jordan's USD 5 billion desalination canal and Egypt's Mustaqbal Misr reclamation convert desert land into irrigated farmland.

Why are agri-fintech platforms important?

Digital lenders shorten credit cycles and align repayments with harvest seasons, unlocking capital for inputs and mechanization among smallholders.

What is the main infrastructure gap in the region?

Limited cold-chain capacity between farmgate and ports causes post-harvest losses of up to 35%, constraining export growth.

Page last updated on: