Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

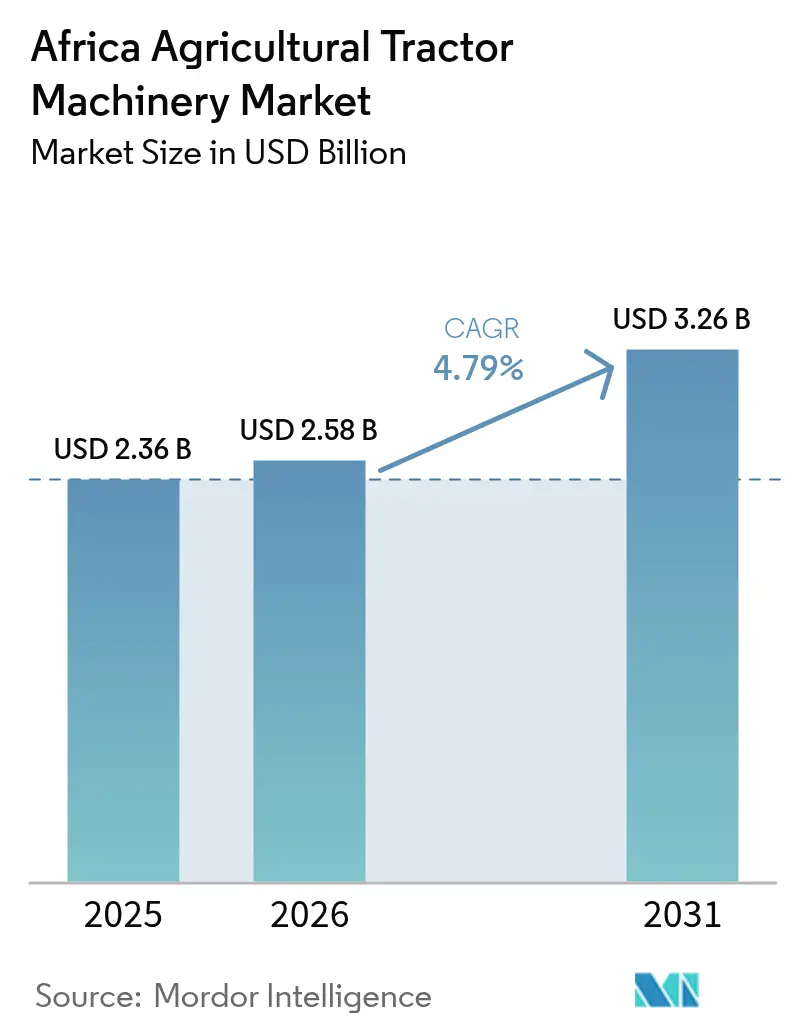

| Base Year Market Size (2025) | USD 2.36 Billion |

| Market Size (2026) | USD 2.58 Billion |

| Market Size (2031) | USD 3.26 Billion |

| Growth Rate (2026 - 2031) | 4.79% CAGR |

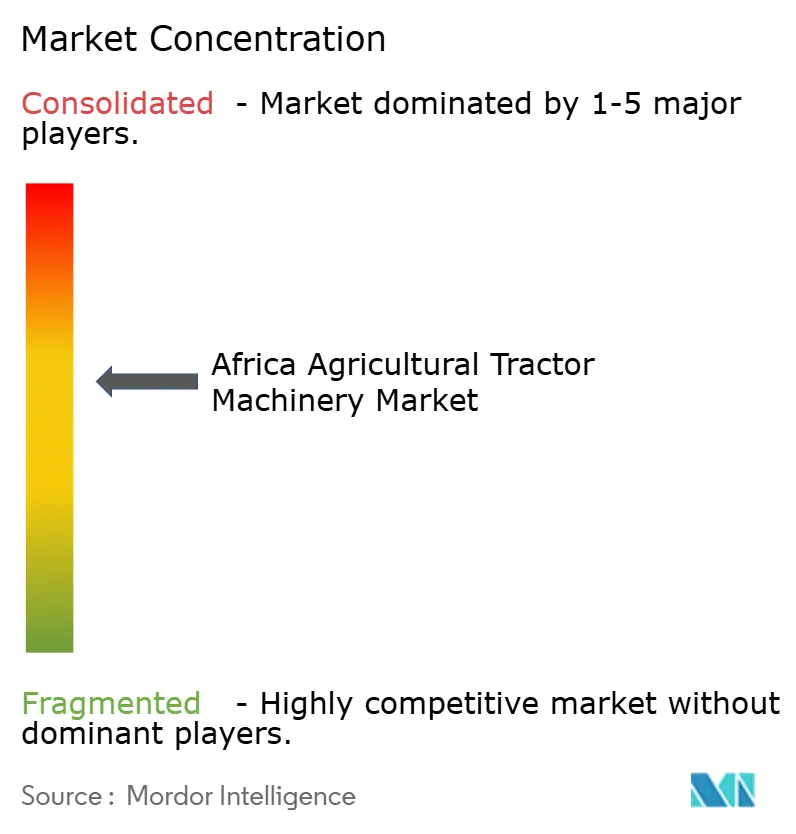

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Africa Agricultural Tractor Machinery Market Analysis by Mordor Intelligence

The Africa agricultural tractor machinery market size is projected to grow from USD 2.36 billion in 2025 to USD 2.58 billion in 2026 and is forecast to reach USD 3.26 billion by 2031 at a 4.79% CAGR over 2026-2031. Rising mechanization subsidies, the spread of pay-per-use digital tractor-hire platforms, and the establishment of completely knocked-down assembly lines are converting latent demand into realized sales. Medium commercial farms are scaling up their fleets to support double-cropping, while county-level cooperatives in Kenya and Tanzania are lowering rental costs for smallholders. Nigeria anchors demand due to federal-subsidized loan programs, but Kenya records the fastest expansion as horticulture exporters standardize precision implements. Moderate competitive intensity prevails, with Western, Asian, and regional manufacturers adopting local assembly, embedded finance, and service-driven differentiation.

Key Report Takeaways

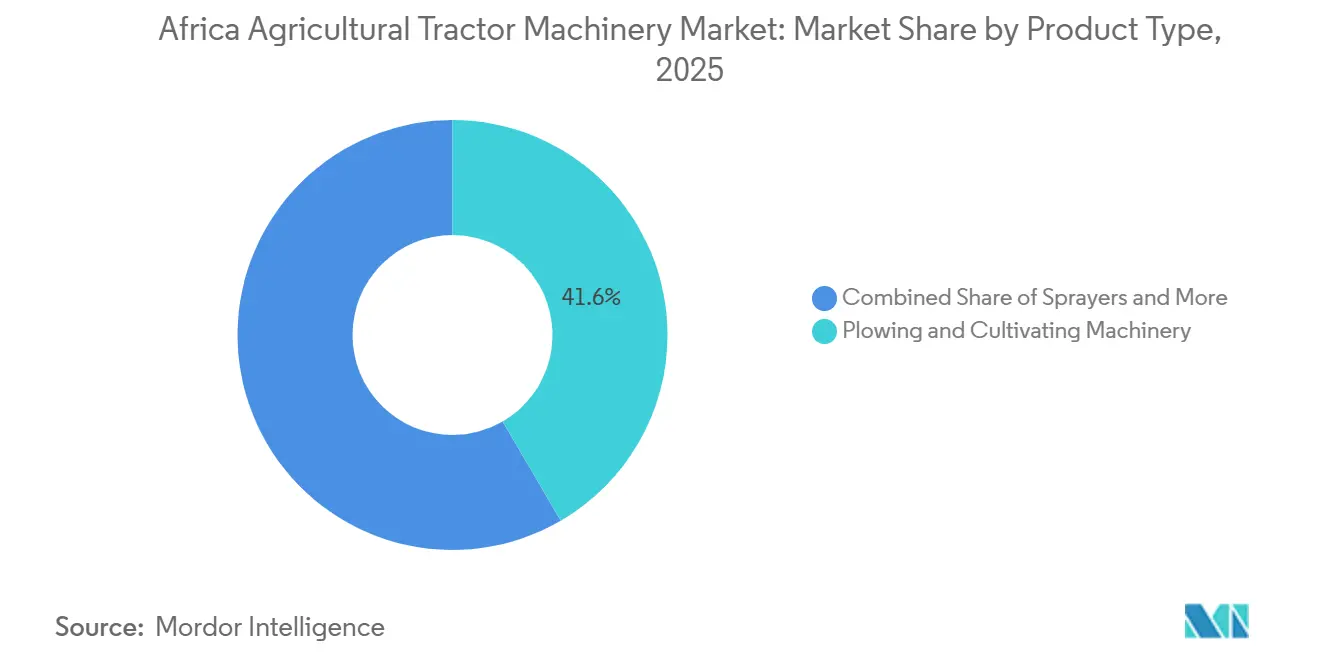

- By product type, plowing and cultivating machinery led with 41.6% of the Africa agricultural tractor machinery market share in 2025, and sprayers are projected to advance at a 5.9% CAGR through 2031.

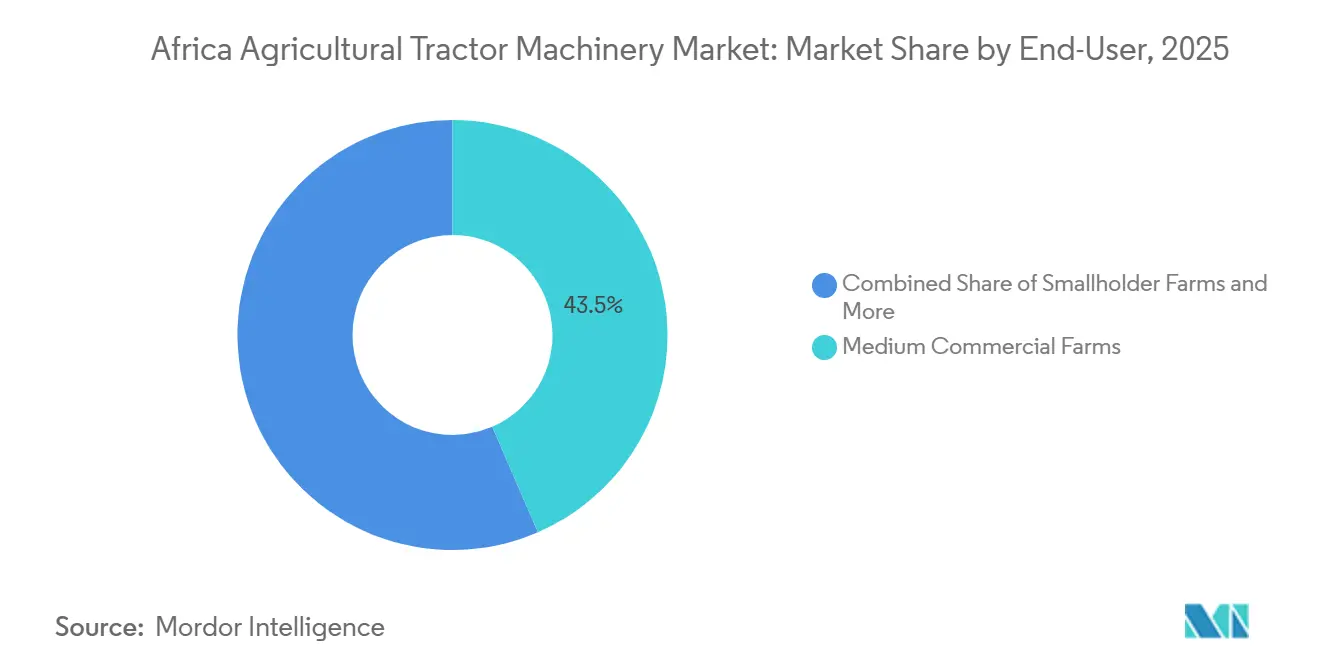

- By end-user, medium commercial farms accounted for 43.5% of the Africa agricultural tractor machinery market size in 2025, whereas contract-hire and rental fleets are forecast to post the highest growth at a 4.9% CAGR to 2031.

- By geography, Nigeria accounted for 38.6% of 2025 sales, but Kenya is set to grow at a 5.4% CAGR through 2031, the fastest among tracked countries.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Agricultural Tractor Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising mechanization subsidies and pan-African finance programs | +0.9% | Nigeria, Tanzania, Ethiopia, and Kenya | Medium term (2-4 years) |

| Expansion of large-scale commercial farming | +0.6% | Sudan, Zambia, Mozambique, and Zimbabwe | Long term (≥4 years) |

| Growth of pay-per-use digital equipment hire platforms | +0.8% | Nigeria, Kenya, Ethiopia, Uganda, and Rwanda | Short term (≤2 years) |

| Climate-smart agriculture incentives boosting demand for precision implements | +0.5% | Kenya, South Africa, and Egypt | Medium term (2-4 years) |

| China-Africa industrial parks enabling low-cost completely knocked down tractor assembly | +0.4% | Ethiopia, Kenya, and Nigeria | Medium term (2-4 years) |

| Emergence of renewable-powered autonomous equipment in high-solar belts | +0.2% | Kenya, South Africa, and Egypt | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Mechanization Subsidies and Pan-African Finance Programs

Soft-loan schemes and subsidized leases lower initial capital requirements and shorten payback periods for farms as small as 5 hectares. National subsidy schemes are shifting machinery procurement from individual ownership to cooperative pools and publicly managed hiring centers. In February 2025, the Federal Government launched the largest agricultural mechanization initiative in Africa, deploying 2,000 tractors and over 9,000 precision implements nationwide. This initiative aims to enhance productivity, expand cultivated land, and improve food security. The Kenyan Ministry of Agriculture and Livestock Development launched the National Mechanization Program in 2023 to enhance food and nutritional security by increasing farm mechanization from the current 30% to 50%. This program aims to supply farm machinery, equipment, and related implements to transform underutilized government-owned land into mechanized farming operations[1]Source: The International Trade Administration, " Kenya Agribusiness: Announcement of Interest to Procure Agricultural Machinery and Equipment," trade.gov. Such initiatives assure predictable demand while concentrating price negotiations, pushing manufacturers to localize parts content and to agree to extended payment terms. Collectively, these schemes shift ownership economics from a decade-long commitment to manageable operating leases, accelerate fleet renewal cycles, and bolster the Africa agricultural tractor machinery market.

Expansion of Large-Scale Commercial Farming

Large estates, averaging 5,000 hectares, attract foreign direct investment, generate bulk tractor orders, and serve as demonstration models for neighboring smallholders. Kenya's agricultural sector experienced a notable recovery, with the cereal harvested area increasing to 2.94 million hectares in 2024, up from 2.68 million hectares in 2021. This growth necessitated additional plowing, planting, and harvesting capacity. Kenya’s export horticulture, worth USD 195.6 million between July and September 2025, relies on narrow-track tractors that deliver centimeter-level accuracy for irrigation and orchard pruning[2]Source: Floriculture, "Kenya’s Horticultural Exports Thrive in Last Year’s Q3 Amid Global Demand," floriculture.co.ke. Sudan's agricultural recovery following the conflict has focused on the Gezira Scheme. The rehabilitation of irrigation infrastructure in 2025 facilitated the return of hectares to production, driving demand for tractors and related machinery. Mega-farms anchor dealership footprints, reduce logistical costs for after-sales parts, and stabilize demand across cropping seasons.

Growth of Pay-Per-Use Digital Equipment Hire Platforms

Asset-light farming is scaling as telematics platforms match idle tractors with underserved plots. Machinery financing and leasing in Africa are undergoing significant changes, driven by technology-driven models such as Pay-As-You-Go (PAYG) and customized seasonal loan repayment plans. These initiatives typically offer 90-95% financing with repayment terms of up to five years, aiming to support smallholder farmers and young agripreneurs. The African Development Bank’s USD 500 million mechanization facility in 2025 provides risk-sharing features that allow local banks to price seven-year loans at single-digit interest rates, provided borrowers choose low-emission or precision-ready equipment[3]Source: African Development Bank, “Mechanization Facility 2025,” afdb.org. Hello Tractor’s mobile platform lets farmers book services and pay per hectare through mobile money, reducing default risk for equipment owners. Mahindra & Mahindra Limited and Simba Corporation added 36-month installment plans with 20% down payments and six Kenyan branches in 2024. Ethiopia’s state platform enrolled tractors and is layering agronomic data to optimize tillage depth. By converting machinery from a fixed asset to a variable expense, digital hire lowers entry thresholds and expands the Africa agricultural tractor machinery market.

Climate-Smart Agriculture Incentives Boosting Demand for Precision Implements

Subsidies aligned with adaptation objectives are influencing buyers to shift from traditional farming practices to advanced agricultural techniques such as GPS-guided planting and variable-rate spraying. Kenya's Climate-Smart Agriculture Project (KCSAP), running from 2017 to 2026, offers substantial subsidies to farmers in arid regions, promoting the use of modern agricultural practices and enhancing resilience to climate change. In South Africa, carbon credits are offered to conservation-tillage adopters, reducing the financial burden of transitioning to sustainable farming practices and promoting soil health. Trials in Ghana and Senegal have demonstrated that precision planting techniques result in significant reductions in seed use, underscoring the efficiency and cost-saving potential of adopting advanced farming solutions. These policies are fostering a shift toward higher-value agricultural practices, increasing productivity, and driving greater investment in the Africa agricultural tractor machinery sector.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented after-sales networks limiting machinery uptime | -0.6% | Rest of Africa, rural Nigeria and Ethiopia | Medium term (2-4 years) |

| Local-currency depreciation escalating import component costs | -0.8% | Nigeria, Egypt, Ethiopia, and Kenya | Short term (≤ 2 years) |

| Land-tenure uncertainty deterring long-payback investments | -0.5% | Zimbabwe, Sudan, and Kenya | Long term (≥ 4 years) |

| Electronic-control-unit chip shortages prolonging delivery cycles | -0.4% | Global, affecting all African markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented After-Sales Networks Limiting Machinery Uptime

Sparse dealer networks and prolonged parts-delivery times result in a significant number of tractors being out of service during critical agricultural periods. According to Nigeria’s agriculture ministry, a majority of tractors older than several years were non-functional in recent years due to replacement parts requiring extended periods to arrive from coastal warehouses. In Ethiopia, a substantial portion of state-distributed tractors experienced lengthy annual downtimes. Similarly, rural counties in Kenya experienced significant service delays, reducing annual tractor utilization. Hello Tractor addresses this issue by deploying mobile mechanics, who typically restore machines within a few days. While manufacturers are establishing regional hubs and training independent workshops, low machinery densities in remote areas continue to hinder the economic feasibility of dedicated service centers.

Land-Tenure Uncertainty Deterring Long-Payback Investments

Ambiguous ownership reduces collateral value and increases lender risk premiums. Zimbabwe's long-term leases provide weaker security compared to freehold titles, which restricts access to equipment financing. In Kenya, delays in the community land adjudication process are projected to leave a considerable portion of land without registered titles in the coming years. In Sudan, overlapping claims within major agricultural schemes discourage banks from approving tractor loans. Although rental models help address these challenges, persistent uncertainty continues to hinder mechanization across large areas, limiting the growth of the agricultural tractor machinery market in Africa.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Plowing and Cultivating Machinery Dominates While Sprayers Accelerate

Plowing and cultivating machinery is the largest product type and captured 41.6% of the Africa agricultural tractor machinery market share in 2025, as soil preparation remains a precursor for most smallholder and medium farm operations. Government voucher programs in Tanzania allocated mechanization budgets to plows and harrows to offset yield losses from manual tillage. In February 2026, the Federal Government of Nigeria officially commenced the distribution of over 9,000 agricultural implements, which include a significant number of disc harrows, as part of the Renewed Hope National Agricultural Mechanisation Programme (RHAMP). Demand persists across conservation-tillage campaigns because many fields still require initial deep ripping before adopting minimal-disturbance systems.

Sprayers are the fastest-growing product line, advancing at a 5.9% CAGR through 2031 as export markets enforce residue limits and climate projects incentivize precise chemical use. South African wine and citrus producers are adopting smart technologies, such as variable-rate sprayers, to enhance efficiency and sustainability. These efforts address challenges posed by climate change and the growing need for effective water management. As calibrated applications reduce pesticide costs, the Africa agricultural tractor machinery market for sprayers is projected to grow steadily, capturing budget share from generic plows and seeders. Planting machinery, including seed drills, planters, and spreaders, is projected to hold a significant market share in the coming years, driven by the increasing adoption of precision planting techniques in key maize- and soybean-producing regions. Haying and forage machinery, including mowers, conditioners, and balers, is anticipated to play a crucial role, particularly in supporting the livestock industry in South Africa and the dairy sector in Kenya. Other machinery types, including specialized implements such as potato diggers and sugarcane harvesters, are projected to serve niche crop markets, addressing specific agricultural needs.

By End-User: Medium Commercial Farms Lead, Contract-Hire and Rental Fleets Grow Fastest

Medium commercial farms are the largest end-user segment and accounted for 43.5% of the Africa agricultural tractor machinery market size in 2025. These farms integrate tractor ownership with contracted labor to reduce operating costs and benefit from government credit programs, such as Nigeria's Anchor Borrowers Program, which offers loans at a reduced interest rate. In Zambia, a significant increase in cultivated land among medium farms was observed in recent years, leading to a notable rise in tractor purchases to support agricultural activities.

Contract-hire and rental fleets are expanding at a 4.9% CAGR through 2031, the fastest among end users, because pay-per-use models convert capex into a predictable operating expense. Hello Tractor experienced significant growth in 2025, increasing its unit count and serving a vast area of farmland. Collaborative efforts with counties in Kenya led to a substantial reduction in rental costs per hectare, encouraging many smallholders to adopt formal mechanization practices. The Africa agricultural tractor machinery market size attributed to rental fleets is therefore projected to gain share as digital platforms scale across additional provinces and languages.

Geography Analysis

Nigeria is the largest geography and accounted for 38.6% of the Africa agricultural tractor machinery market share in 2025 because Nigeria’s subsidy blueprint requires tractor access in every local government area. The depreciation of Nigeria's naira, from a relatively stable value in early 2024 to a significantly weaker position by 2025, created substantial challenges for importers. These challenges included the necessity to adjust pricing for inventory while it was still in transit. This situation led to a significant decline in machinery registrations compared to the same period the previous year. The cultivation of rice and maize in key agricultural regions such as Kano, Kaduna, and Benue has been a major driver of machinery purchases, supported by policies such as guaranteed minimum prices that stabilize farmers' cash flow. Hello Tractor operates a substantial number of units locally, promoting the adoption of pay-per-use models among small-scale farmers managing relatively modest landholdings.

Kenya is forecast to post the fastest compound growth rate of 5.4% through 2031, driven by county mechanization hubs and export-driven horticulture that relies on GPS-guided tractors to reduce seed waste. The country’s Climate-Smart Agriculture Framework channels funding toward conservation tillage kits, underscoring policy continuity. Tanzania benefits from Vodacom's telemetry, which reduces downtime, and Ghana now hosts Indian maker Captain Tractors, confirming rising investor confidence. South Africa's Agricultural Research Council reported that precision land preparation reduced fertilizer application rates in maize trials conducted in Mpumalanga and North West provinces during 2024-2025. This has led commercial farms to retrofit existing fleets with GPS receivers and yield monitors.

Egypt's New Delta reclamation program, launched in 2021, requires a specific number of tractors per designated farmland area, leading to increased orders. The depreciation of the Egyptian pound led to a temporary suspension of import licenses for several months the following year. Chinese manufacturers have established a strong foothold in cost-sensitive markets such as Angola and Burkina Faso by offering flexible payment terms and ensuring local availability of spare parts. The remainder is sourced from Tanzania, Zambia, Zimbabwe, and other markets, where voucher programs and large-scale farm projects support baseline growth in the Africa agricultural tractor machinery market.

Competitive Landscape

The Africa agricultural tractor machinery market shows moderate concentration. Top players Deere & Company, CNH Industrial N.V., AGCO Corporation, Mahindra & Mahindra Limited, and Kubota Corporation collectively hold a significant share of the market in 2025, offering buyers a wide range of brand options alongside attractive financing plans. Western brands maintain a premium market position but face affordability challenges among smallholders, despite initiatives such as AGCO Corporation’s consignment agreement with Hello Tractor, which bases payments on usage hours rather than upfront costs. Mahindra & Mahindra Limited and Kubota Corporation offer mid-tier models at lower prices compared to Western competitors, gaining market share in Nigeria and Kenya, where loan caps continue to limit purchasing power.

Chinese makers Weichai Lovol Intelligent Agricultural Technology Co., Ltd. (Weichai Power Co., Ltd.), and Zoomlion Heavy Industry Science and Technology Co., Ltd. leverage local assembly hubs to undercut fully built imports and trim lead times. These facilities also create skilled jobs, aligning with the host government's industrialization goals. Regional players such as Rovic & Leers (Pty) Ltd. in South Africa and Agrimont Industrial Group emphasize after-sales responsiveness, deploying mobile workshops that resolve breakdowns within 24 hours, a service differential that multinational dealers struggle to match in remote zones.

Competitive advantage in the Africa agricultural tractor machinery market increasingly favors firms that align technological advancements with customers' willingness to pay, rather than offering uniformly feature-rich platforms across all income tiers. Companies are focusing on tailoring their offerings to meet the specific needs of different customer segments, ensuring affordability and relevance. Midsize companies, such as Yanmar Holdings Co., Ltd., have streamlined their supply chains, lowering production costs and facilitating their expansion into African markets. These firms are leveraging localized strategies and partnerships to strengthen their market presence and meet the growing demand for agricultural tractor machinery in the region.

Africa Agricultural Tractor Machinery Industry Leaders

-

Deere & Company

-

AGCO Corporation

-

CNH Industrial N.V.

-

Mahindra & Mahindra Ltd.

-

Kubota Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: New Holland Agriculture has partnered with Inchcape Kenya, officially appointing the company as its authorized full-range importer and distributor in Kenya. This partnership aims to enhance access to modern agricultural machinery and support the long-term growth of Kenya's farming sector.

- September 2025: New Holland has introduced the next-generation CR10 combine in South Africa to commemorate 50 years of Twin Rotor technology. Equipped with a 635hp 12.9L FPT Cursor 13 engine and a 16,000L grain tank, the combine is designed to lower overall harvesting costs by enhancing productivity, improving grain quality, and enabling automated, low-loss operations.

- June 2025: Yanmar Holdings Co., Ltd. collaborated with Côte d'Ivoire-based ATC Comafrique to enhance its agricultural machinery operations across 16 West African countries. As part of the agreement, ATC will manage the sales and servicing of Yanmar products, including tractors, combine harvesters, tillers, engines, and spare parts.

Africa Agricultural Tractor Machinery Market Report Scope

Agricultural tractor machinery encompasses various equipment designed to be attached to, powered by, or towed behind an agricultural tractor. These implements facilitate the mechanization of farming operations, including tillage, sowing, and harvesting, thereby reducing manual labor and enhancing efficiency and productivity.

The Africa Agricultural Tractor Machinery Market Report delivers a structured analysis of the industry across product categories, end-user groups, and key regional markets. By product type, the market encompasses plowing and cultivating equipment, planting machinery, sprayers, haying and forage machinery, along with other related tractor-mounted implements. From an end-user perspective, the study evaluates demand across smallholder farms, medium-sized commercial operations, large estates and agroholdings, and contract-hire and rental service providers. Regionally, the assessment spans Nigeria, South Africa, Kenya, Egypt, Ethiopia, and the broader Rest of Africa. All market estimates and forecasts are presented in value terms (USD).

By Product Type

| Plowing and Cultivating Machinery | Plows |

| Harrows | |

| Rotovators and Cultivators | |

| Other Equipment | |

| Planting Machinery | Seed Drills |

| Planters | |

| Spreaders | |

| Other Planting Machinery | |

| Sprayers | |

| Haying and Forage Machinery | Mowers and Conditioners |

| Balers | |

| Other Haying and Forage Machinery | |

| Other Types |

By End-User

| Smallholder Farms |

| Medium Commercial Farms |

| Large Estates and Agro-holdings |

| Contract-Hire and Rental Fleets |

By Geography

| Nigeria |

| South Africa |

| Kenya |

| Egypt |

| Ethiopia |

| Rest of Africa |

| By Product Type | Plowing and Cultivating Machinery | Plows |

| Harrows | ||

| Rotovators and Cultivators | ||

| Other Equipment | ||

| Planting Machinery | Seed Drills | |

| Planters | ||

| Spreaders | ||

| Other Planting Machinery | ||

| Sprayers | ||

| Haying and Forage Machinery | Mowers and Conditioners | |

| Balers | ||

| Other Haying and Forage Machinery | ||

| Other Types | ||

| By End-User | Smallholder Farms | |

| Medium Commercial Farms | ||

| Large Estates and Agro-holdings | ||

| Contract-Hire and Rental Fleets | ||

| By Geography | Nigeria | |

| South Africa | ||

| Kenya | ||

| Egypt | ||

| Ethiopia | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the Africa agricultural tractor machinery market in 2031?

The market is forecast to reach USD 3.26 billion by 2031.

How fast will the market grow between 2026 and 2031?

The market is projected to grow at a CAGR of 4.79% over the forecast period from 2026 to 2031.

Which product type currently holds the largest market share?

Plowing and cultivating machinery led with 41.6% share in 2025.

Which end-user segment is expanding most rapidly?

Contract-hire and rental fleets are projected to grow at 4.9% CAGR through 2031.

Page last updated on: