South America Agricultural Drones Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

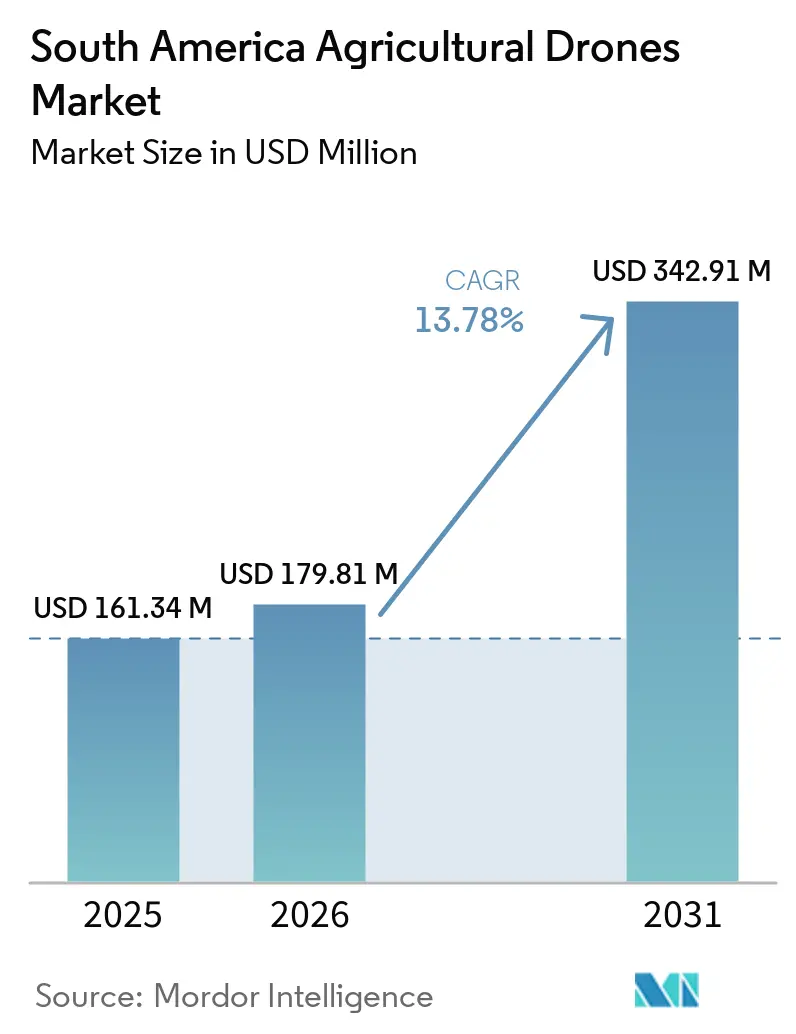

| Base Year Market Size (2025) | USD 161.34 Million |

| Market Size (2026) | USD 179.81 Million |

| Market Size (2031) | USD 342.91 Million |

| Growth Rate (2026 - 2031) | 13.78% CAGR |

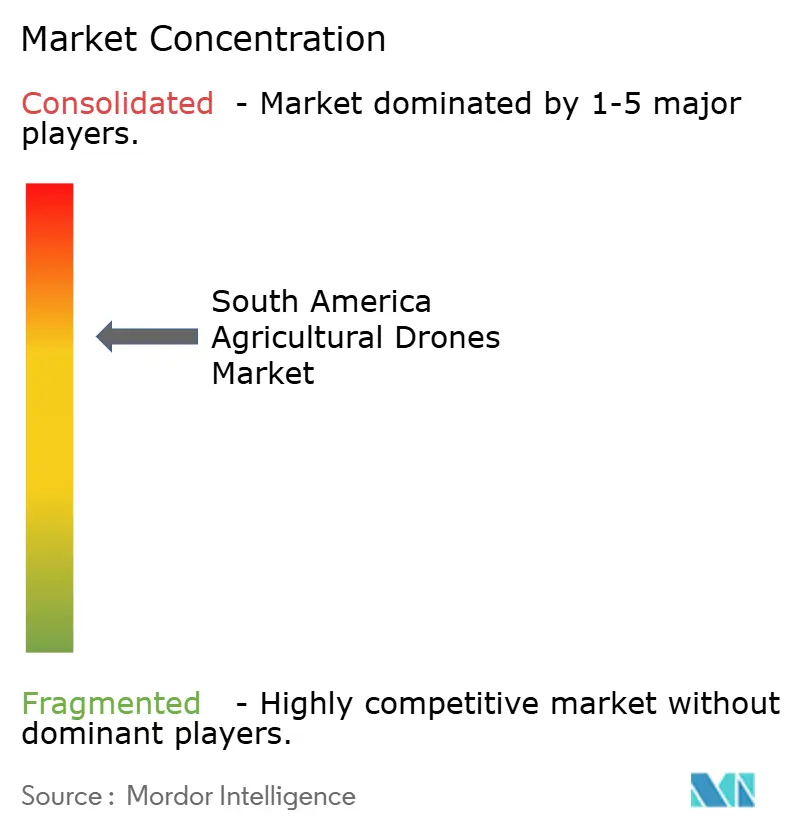

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Agricultural Drones Market Analysis by Mordor Intelligence

The South America agricultural drones market size was valued at USD 161.34 million in 2025 and is estimated to grow from USD 179.81 million in 2026 to USD 342.91 million by 2031, at a CAGR of 13.78% during the forecast period (2026-2031). The market is being shaped by large soybean and sugarcane farming systems, which allow operators to cover wide, contiguous fields with better flight economics than smaller, fragmented farm structures. Brazil remains the center of regional adoption, as the Ministry of Agriculture and Livestock (MAPA) reported that the country's operational fleet expanded from 3,000 units in 2021 to 35,000 units by 2025 [1]Source: Ministerio da Agricultura e Pecuaria, “Mercado de Drones Agricolas Dispara Apos Regulamentacao do Mapa,” Gov.br, gov.br. The market is also moving away from early hardware purchases toward more formal service models, as growers increasingly need training, reporting, compliance support, and field documentation alongside the aircraft itself. At the same time, the industry still faces friction from low formal registration rates in Brazil and varying certification requirements across countries, which slow insurance-backed scaling and broader enterprise procurement.

Key Report Takeaways

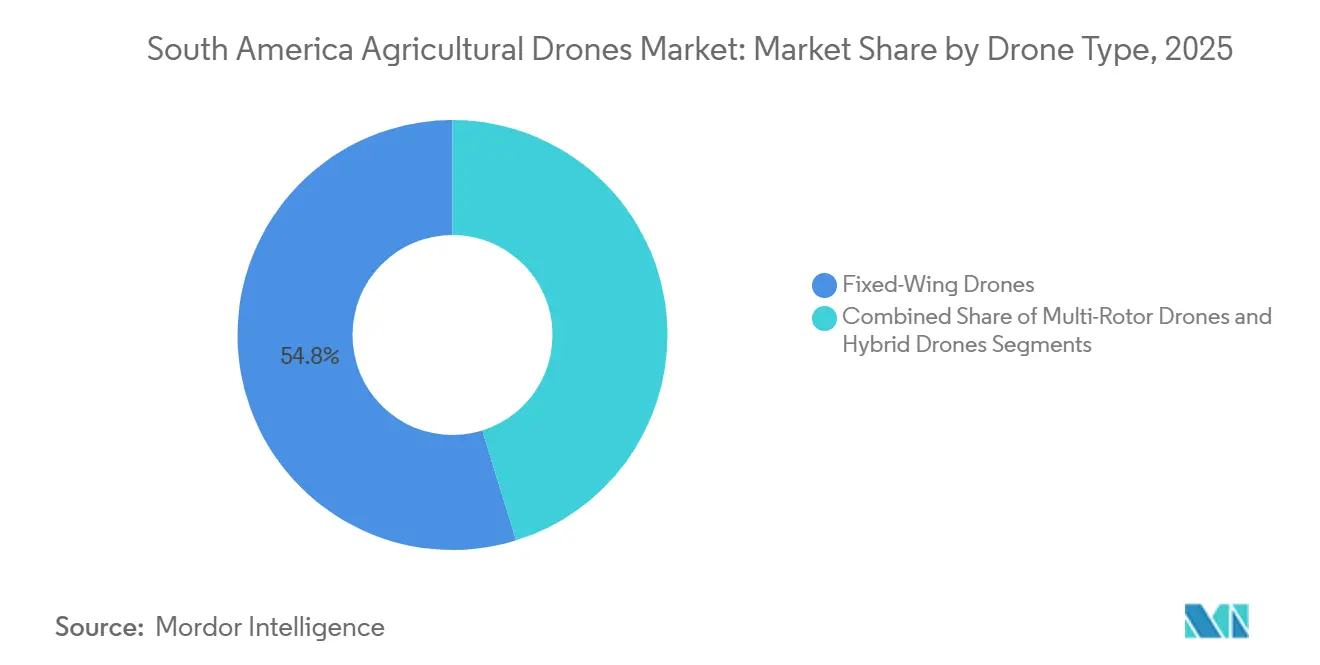

- By drone type, fixed-wing drones were the largest segment, accounting for 54.8% of the South America agricultural drones market share in 2025, while multi-rotor drones are anticipated to grow the fastest with a CAGR of 14.8% during 2026-2031.

- By component, hardware was the largest segment with a 65.7% share in 2025, while services are the fastest-growing segment, forecast to expand at a 15.1% CAGR during 2026-2031.

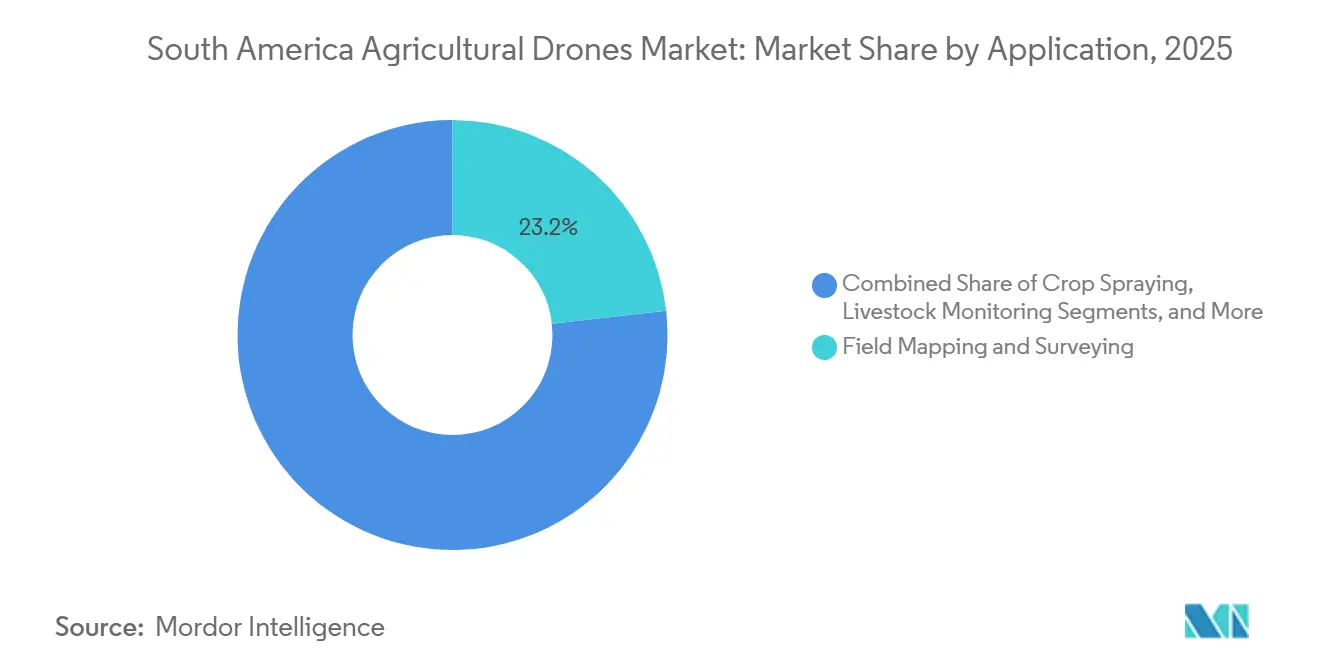

- By application, field mapping and surveying was the largest segment, accounting for 23.2% of the South America agricultural drones market size in 2025, while crop spraying is the fastest-growing segment and is forecast to grow at a 15.6% CAGR during 2026-2031.

- By farm size, large-scale commercial farms captured 66.8% share of the market in 2025, while small and medium farms are anticipated to grow at a 14.6% CAGR to 2031.

- By geography, Brazil was the largest country with 35.6% share in 2025, while Argentina was the fastest country and is projected to record a 15.9% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Agricultural Drones Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Large Soybean and Sugarcane Acreage Supports Drone Economics | +3.50% | Strongest in Brazil, Argentina, and Paraguay due to large-scale row-crop and plantation farming systems | Short term (≤ 2 years) |

| Precision Agriculture Adoption and Input Optimization Push | +2.80% | Most relevant in Brazil, Argentina, and Colombia, with increasing adoption in Chile and Peru | Medium term (2-4 years) |

| Brazil Regulatory Formalization Improves Legal Spraying Adoption | +2.20% | Highest impact in Brazil, with broader influence across other South American countries | Short term (≤ 2 years) |

| Large-Farm Labor Scarcity Increases Demand for High-Output Aerial Application | +2.00% | Concentrated in Brazil and Argentina, with added relevance in Chilean estate agriculture | Long term (≥ 4 years) |

| Wet-Season Field Access Constraints Favor Drones Over Ground Sprayers | +1.40% | Relevant across wet-prone agricultural zones in Brazil and Colombia, and uneven terrain areas in Peru | Short term (≤ 2 years) |

| Financing, Training, and Turnkey Service Models Reduce Adoption Friction | +1.60% | Most visible in Brazil and Argentina through dealer-backed financing and operator training ecosystems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Large Soybean and Sugarcane Acreage Supports Drone Economics

Large-scale farm structures across Brazil, Argentina, and Paraguay provide agricultural drone fleets with more productive flight hours than in many smaller, fragmented farming regions. Broad row-crop and plantation areas allow long straight passes and larger operating blocks, improving route planning and payload efficiency. AgEagle Aerial Systems Inc. demonstrated this scale in July 2025 when it deployed 5 eBee X drones with MicaSense S.O.D.A. 3D cameras across 1.2 million acres of Atvos Agroindustrial S.A. sugarcane operations in Brazil. The same deployment produced 3-centimeter-resolution maps that fed machinery autopilot systems, improving travel accuracy to within 15 centimeters, demonstrating how large estates can connect mapping data directly to field operations. In this setting, adoption is less dependent on experimental use and more dependent on whether operators can capture enough hectares per mission to justify the service or equipment cost.

Precision Agriculture Adoption and Input Optimization Push

Growers across South America are increasingly using drones to improve control over water, agrochemicals, and labor at the field level. A peer-reviewed study in Peru showed that drone imagery and machine learning models achieved yield-prediction accuracy above R² = 0.74 in potato trials, supporting the value of drone-led crop intelligence beyond simple field observation [2]Source: Dennis Ccopi et al., “Using UAV Images and Phenotypic Traits to Predict Potato Morphology and Yield in Peru,” Agriculture, mdpi.com. A second peer-reviewed study in central Peru mapped nitrogen, phosphorus, potassium, organic matter, and electrical conductivity across 49.83 hectares with strong model performance, reinforcing the role of drones in precision input management. Company releases also point in the same direction, as XAG Co., Ltd. reported that its Brazilian farm deployment reduced water application from 15 liters per hectare to 10 liters per hectare in 2025, although that figure remains a company claim. SZ DJI Technology Co., Ltd. further stated in its 2026 report that spot spraying can reduce herbicide use by up to 35%, thereby keeping the value case active even as crop price cycles change.

Brazil Regulatory Formalization Improves Legal Spraying Adoption

Clearer and more enforceable agricultural drone regulations in Brazil are improving confidence among commercial operators and enterprise farm buyers. MAPA confirmed that Portaria 298 from 2021 created the initial structure for training and registration, and the ministry opened a formal public consultation in October 2024 to replace older drone and manned aviation rules with a more updated framework [3]Source: Ministerio da Agricultura e Pecuaria, “Mapa Lanca Consulta Publica Para Revisao Das Regras Para Operacoes Aeroagricolas Com Drones e Tripulados,” Gov.br, gov.br. This matters because enterprise buyers are more willing to hire service providers when operator qualification, reporting, and registration are easier to verify. SZ DJI Technology Co., Ltd. also stated in its 2026 industry report that Brazil's National Civil Aviation Agency (ANAC) introduced standard scenarios for recurring agricultural operations, which suggests lower administrative friction for repetitive missions. Argentina has followed up with its own 2024 deregulation measures to simplify the use of unmanned civil aviation in agricultural areas, showing that regulatory modernization is spreading across the region. The commercial effect is that legally compliant operators are likely to gain share as more buyers prioritize insurance, traceability, and contract certainty.

Large-Farm Labor Scarcity Increases Demand for High-Output Aerial Application

Labor shortages during narrow crop treatment windows are increasing the value of high-output aerial application systems across large South American farms. XMobots Aeroespacial e Defesa S.A. launched the SPAD 200B in 2025 and stated that 1 pilot and 1 assistant can support 4 continuous hours of work with 2 drones, which shows the direction of labor-saving field logistics. That operating structure is important in Brazil and Argentina, where broad commercial farms cannot always rely on large seasonal crews for every crop protection cycle. Jacto has also built training, financing, and technical support around its agricultural drone line, reducing the operational burden on growers who do not want to build a full in-house aviation capability. The labor argument becomes stronger when farms need fast treatment over large acreage without the downtime of repeated vehicle entry into the field. As a result, aerial application is moving from a niche option toward a practical operating model in parts of the South America agricultural drones market where scale is already present.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront System and Charging Infrastructure Cost for Smaller Farms | -1.60% | Broad regional impact, especially in Peru, Bolivia, Ecuador, and smaller Colombian farming operations | Long term (≥ 4 years) |

| Cross-Country Compliance Complexity for Pilots, Spraying, and Airspace Use | -1.20% | High friction across South America for operators managing multi-country certifications and airspace rules | Medium term (2-4 years) |

| Drift Liability and Contamination Disputes Can Slow Enterprise Rollout | -0.80% | Most relevant near sensitive crop zones, residential areas, and regulated spraying regions | Short term (≤ 2 years) |

| Registration and Pilot-Certification Lag Limits Insurance and Financing Access | -0.90% | Strongest in Brazil, with additional impact in markets facing rapidly evolving drone regulations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront System and Charging Infrastructure Cost for Smaller Farms

Smaller farms across South America continue to face adoption barriers because a viable agricultural drone setup requires more than just the aircraft itself. Colombia's 2025 ADR procurement document showed that a working package can include the drone, multiple intelligent batteries, a generator, a portable charger, and a supporting kit with additional accessories and training requirements [4]Source: Aeronautica Civil de Colombia, “Informacion Importante Sobre la Regulacion de la Aviacion No Tripulada UAS,” Aerocivil, aerocivil.gov.co. That full package makes economic sense for large operators or shared-use models, but it is harder for smaller farms that cannot spread the cost over enough hectares. This is why financing programs and leasing mechanisms are emerging in Argentina, and why dealer-backed service models remain important for the South America agricultural drones market. Until service density improves in smaller agricultural regions, direct ownership will remain difficult for many farms.

Cross-Country Compliance Complexity for Pilots, Spraying, and Airspace Use

The lack of a common regional operating framework constrains the South America agricultural drone market. Brazil's system is built around MAPA registration and training, while Colombia's RAC 100 places clear limits on airspace, no-fly areas, and the dropping of objects without authorization. Argentina's 2024 deregulation path reduces bureaucracy for agricultural use, but it does not automatically make the country's rules transferable across borders. A service provider that wants to work across Brazil, Argentina, Colombia, Chile, and Peru, therefore, faces separate certification, documentation, and airspace procedures. That raises overhead and favors larger operators that can spread compliance costs across wider service territories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drone Type: Fixed-Wing Systems Command Extensive-Crop Economics

Fixed-wing drones were the largest segment, accounting for 54.8% of the South America agricultural drones market share in 2025. Their position reflects the farm structure of Brazil, Argentina, and Paraguay, where wide commercial estates reward flight endurance and large-area coverage more than short-range maneuverability. AgEagle Aerial Systems Inc. strengthened that case in July 2025 when its eBee X system was deployed across 1.2 million acres of sugarcane at Atvos Agroindustrial S.A. in Brazil. The company also noted that the system holds beyond-visual-line-of-sight certification in Brazil, which matters for large-estate mapping contracts that require greater operating range and formal approval. In the South America agricultural drones market, this makes fixed-wing platforms especially hard to displace in mapping and surveying work over extensive crop areas.

Multi-rotor drones are the fastest-growing segment and are projected to expand at a CAGR of 14.8% during 2026-2031, as their maneuverability, precision spraying capability, and suitability for uneven terrain make them increasingly valuable for specialty crops, targeted applications, and smaller field operations. Summit Agro Chile launched the DJI Agras T70P and T100 in August 2025, demonstrating that larger-payload multirotor systems are now being positioned for Chilean fruit, citrus, and vineyard operations. XAG Co., Ltd. also launched the P150 and P60 in Brazil in 2025, with one model aimed at large farms and the other aimed at smaller and medium-scale users. Hybrid drones remain at an early commercial stage because heavier unmanned systems still need clearer operating rules and wider field proof before scale adoption. The South America agricultural drone industry is therefore likely to remain led by fixed-wing mapping systems and multi-rotor spraying systems in the near term.

By Component: Hardware Anchors Revenue While Services Accelerate

Hardware was the largest component, accounting for 65.7% of the South America agricultural drones market size in 2025. That result fits a market that is still building out fleets, payload systems, charging assets, and field support equipment. XMobots Aeroespacial e Defesa S.A. illustrated this trend with the SPAD 75, which bundled the drone, mixer, charging, weather station, connectivity, and transport structure into a single operating system. Jacto Inc. followed a similar practical model by combining equipment sales with technical support, parts, training, and financing rather than selling isolated units, thereby keeping hardware spending high, as buyers often need a full operating package rather than a single aircraft.

Services are the fastest-growing segment, and are projected to expand at a 15.1% CAGR during 2026-2031. The shift is being driven by growers who prefer contracted spraying, fleet support, and data reporting without direct asset ownership. XMobots Aeroespacial e Defesa S.A. launched DAASFY in 2025 to provide mobile spraying management, climatic monitoring, and automated technical reports, which show how service revenue is moving beyond field labor alone. Software remains the smallest revenue pool, but it is gaining weight because regulators and larger farm buyers increasingly expect traceability and post-operation documentation. The industry is therefore shifting from pure equipment sales toward recurring revenue models tied to compliance, analytics, and operational support.

By Application: Mapping Leads Current Demand While Spraying Drives Growth

Field mapping and surveying was the largest application, accounting for 23.2% of the market in 2025. It remains a natural entry point because growers can adopt it before moving into more regulated spraying work. Mapping outputs also fit directly into farm management through stand counts, crop condition checks, topography, and prescription planning. In Peru, peer-reviewed research showed that drone imagery and machine learning could predict potato yield, with test-set R2 values above 0.74, supporting the practical agronomic value of this use case. This makes mapping both a lower-friction starting point and a continuing demand center for large farms.

Crop spraying is the fastest-growing segment, projected to grow at a 15.6% CAGR during 2026-2031. Weather-related access problems, labor efficiency needs, and the rising payload of commercial multi-rotor systems are pushing growth. In 2026, SZ DJI Technology Co., Ltd. stated that drone spot spraying can reduce herbicide use by up to 35%, which supports the cost case for high-value, chemically intensive crops, although the figure is company-reported. Crop monitoring/field surveillance, irrigation management, livestock monitoring, and soil and field analysis are also expanding, but they remain more selective in geography and crop fit than spraying and mapping. The industry is therefore developing around 2 strong anchors, which include mapping current demand and faster adoption of spraying.

By Farm Size: Estate Economics Lead as Service Models Unlock Small-Farm Reach

Large-scale commercial farms were the largest segment and accounted for 66.8% of the South America agricultural drones market share in 2025. At this farm tier, many growers are moving from contracted spraying toward owned multi-drone fleets because scale makes direct ownership more practical during narrow treatment windows. For these estates, the main advantage is operational control, since soybean and sugarcane operations often require rapid phytosanitary action within 4-6-hour weather windows that outside providers cannot always guarantee across very large areas. SZ DJI Technology Co., Ltd. highlighted its Dock 3 autonomous system in its Brazil portfolio at Agrishow 2026, reflecting demand for continuous, weather-responsive aerial coverage across large properties. Large commercial operators also face tighter pesticide traceability requirements from processors and grain traders, so fleet management systems that generate GPS-tagged, time-stamped records are becoming part of routine compliance, while heavy-lift platform options remain relevant in Brazil's most intensive production corridors.

Small and medium farms are the fastest segment, and the South America agricultural drones market size for this group is projected to grow at a 14.6% CAGR during 2026-2031. Growth is strongest in specialty and high-value crops where slopes, fragile plants, or limited field access make drones economical even on 5-15 hectares of planted area. This pattern is especially clear in coffee regions across Brazil and Colombia and in higher-altitude plots in Peru, where drone application can compete well with manual labor and ground equipment because it reduces access problems and crop disturbance. XAG Co., Ltd. positioned the P60 in 2025 as a flexible, cost-effective option for small- to medium-sized farms, while SZ DJI Technology Co., Ltd. launched the T25P in Brazil in 2025 for compact operations and independent users. Colombia’s Agencia de Desarrollo Rural procured agricultural drone systems in 2025 for the COAFROSAVI rice cooperative under PIDAR 280, helping expand operator familiarity, cooperative-based usage models, and regional adoption among medium-scale farms.

Geography Analysis

Brazil was the largest country and accounted for a 35.6% share of the South America agricultural drones market in 2025. MAPA stated that Brazil's operational agricultural drone fleet rose from 3,000 units in 2021 to 35,000 units by 2025, making the country the clearest reference point for regional commercial adoption. The Brazilian ecosystem is also deeper than elsewhere because players such as XMobots Aeroespacial e Defesa S.A. and Jacto built dealer, service, training, and financing capacity around the aircraft. At the same time, formalization remains incomplete, as MAPA reported that only 2,618 aircraft were formally registered for spraying in 2025. This means Brazil combines the strongest scale advantage in the South America agricultural drones market with one of its most visible compliance gaps.

Argentina is the fastest-growing country, and is projected to grow at a 15.9% CAGR during 2026-2031 in the South America agricultural drones market. The country's growth case improved after 2024, when deregulation measures aimed to simplify the use of unmanned civil aviation and explicitly support applications such as soil control, fumigation, and seeding in agricultural zones. Government messaging in 2026 also showed that Argentina is trying to build a more coordinated drone technology ecosystem linked to productive sectors. Financing support is improving as well, with Rio Negro adding agricultural drones to its leasing program in 2025. As a result, Argentina stands out in the South America agricultural drones market as the strongest growth story outside Brazil.

Colombia, Chile, and Peru represent medium-growth positions within the South America agricultural drones market, each supported by a different adoption route. In Colombia, Aerocivil provides a defined regulatory base under RAC 100, and the ADR issued a 2025 procurement process for agricultural fumigation and fertilization drones with a budget of USD 38,000 (COP 156,364,918). In Chile, Summit Agro Chile introduced the DJI Agras T70P and T100 in 2025, aimed at export-oriented fruit and vineyard operations that value payload, precision, and night operation. In Peru, peer-reviewed work funded by the Ministry of Agrarian Development and Irrigation supports the use of drone imagery for yield prediction and soil fertility mapping, strengthening the technical foundation for later commercial adoption. The rest of the region, including Paraguay and other neighboring countries, remains a future expansion zone, with its pace likely to follow Brazil-led commercial and service models.

Competitive Landscape

The South America agricultural drone market is moderately concentrated among a small group of leading brands and regionally embedded commercial partners. The top 5 companies by market rank are SZ DJI Technology Co., Ltd., XAG Co., Ltd., XMobots Aeroespacial e Defesa S.A., Hylio, Inc., and AgEagle Aerial Systems Inc. In practice, SZ DJI Technology Co., Ltd. has built reach through local distribution and service structures rather than through a standalone sales push in each country. XAG Co., Ltd. has taken a similar scale approach through dealer-backed commercialization in Brazil and South America. AgEagle Aerial Systems Inc. remains more specialized, with a stronger fit in fixed-wing mapping work that requires large-area coverage and formal flight approval.

XMobots Aeroespacial e Defesa S.A. launched Xmobots Agriculture in 2025 and added DAASFY, SPAD 200B, and the XGen generator line to tie hardware, logistics, and reporting into one field offer. Jacto used Expointer 2025 to push the DJI Agras T100, offering a 24-month warranty, insurance, and financing support, which shows how local commercial execution matters in the South America agricultural drones market. Ceres Air entered Brazil in 2026 through a partnership with Timber Agriculture, combining a new platform launch with a national technical center, pilot training, and a parts network. XAG Co., Ltd. also expanded its position in 2025 by launching the P150 and P60 for distribution in Brazil and across wider South America.

The South America agricultural drones market is therefore competing on compliance support, service depth, and agronomic workflow integration as much as on payload and endurance. Hardware capabilities have advanced quickly, but many leading platforms now sit close enough in specification that commercial support can decide the purchase. Vendors with strong dealer networks and traceability tools are better positioned, as formal buyers increasingly want documentation, training, and post-sale support. Brazil remains the main proving ground for these models because it has the largest installed base and is where formalization pressure is most visible. That leaves room for new entrants and local service providers, but they will need stronger operating systems to challenge the established leaders at scale.

South America Agricultural Drones Industry Leaders

SZ DJI Technology Co., Ltd.

XAG Co., Ltd.

XMobots Aeroespacial e Defesa S.A.

Hylio, Inc.

AgEagle Aerial Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Ceres Air established a strategic partnership with Timber Agriculture to enter Brazil's commercial agricultural drone space. Timber Agriculture introduced the C31 Black Betty platform under the Timber AT150 name, established a national technical center, launched pilot training programs, and built a dedicated parts logistics network for soybeans, corn, sugarcane, coffee, cotton, and forestry users.

- March 2026: The Ministry of Agriculture, Livestock and Food Supply (MAPA) conducted an enforcement operation in Maranhão, Brazil, focused on agricultural aviation and the use of agrochemicals. The action highlighted the ministry's tighter compliance posture toward irregular operators and reinforced the need for registration and qualified technical oversight in drone spraying activity.

- July 2025: AgEagle Aerial Systems Inc. sold and deployed 5 eBee X drones with MicaSense S.O.D.A. 3D cameras to Atvos Agroindustrial S.A. for use across 1.2 million acres of sugarcane in Brazil. The company stated that the deployment could support a 5% yield increase and improve mapping for targeted field operations.

South America Agricultural Drones Market Report Scope

The South America agricultural drones market covers unmanned aerial systems used in farming for spraying, mapping, surveying, crop monitoring/field surveillance, irrigation support, livestock monitoring, and soil analysis. It includes revenue from hardware, software, and services sold across Brazil, Argentina, Colombia, Chile, Peru, and the rest of South America. The South America Agricultural Drones Market Report is Segmented by Drone Type (Fixed-Wing, Multi-Rotor, and Hybrid Drones), by Component (Hardware, Software, and Services), by Application (Crop Spraying, Field Mapping and Surveying, and More), by Farm Size (Large-Scale Commercial Farms and Small and Medium Farms), and by Geography (Brazil, Argentina, Colombia, Chile, Peru, and Rest of South America). Market Forecasts are Provided in Value (USD).

| Fixed-Wing Drones |

| Multi-Rotor Drones |

| Hybrid Drones |

| Hardware |

| Software |

| Services |

| Field Mapping and Surveying |

| Crop Spraying |

| Crop Monitoring/Field Surveillance |

| Livestock Monitoring |

| Irrigation Management |

| Soil and Field Analysis |

| Large-scale Commercial Farms |

| Small and Medium Farms |

| Brazil |

| Argentina |

| Colombia |

| Chile |

| Peru |

| Rest of South America |

| By Drone Type | Fixed-Wing Drones |

| Multi-Rotor Drones | |

| Hybrid Drones | |

| By Component | Hardware |

| Software | |

| Services | |

| By Application | Field Mapping and Surveying |

| Crop Spraying | |

| Crop Monitoring/Field Surveillance | |

| Livestock Monitoring | |

| Irrigation Management | |

| Soil and Field Analysis | |

| By Farm Size | Large-scale Commercial Farms |

| Small and Medium Farms | |

| By Geography | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

What is the projected value of the South America agricultural drones market by 2031?

The South America agricultural drones market is forecast to reach USD 342.91 million by 2031 from USD 179.81 million in 2026, growing at a 13.78% CAGR during 2026-2031.

Which country leads regional demand for agricultural drones?

Brazil is the largest country in 2025 with a 35.6% share, supported by a large installed fleet, stronger dealer networks, and a more developed compliance framework.

Which application is growing the fastest in South America?

Crop Spraying is the fastest application, with a projected 15.6% CAGR during 2026-2031, driven by wet-field access issues and the need for faster aerial treatment.

What is holding back wider adoption across the region?

The main constraints are high full-system ownership costs for smaller farms, uneven registration and certification rates, and different compliance rules across South American countries.

How are vendors differentiating beyond aircraft hardware?

Leading companies are adding financing, pilot training, service networks, reporting tools, and integrated logistics systems, which are becoming as important as payload and flight range.

Page last updated on: