India Agricultural Drones Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

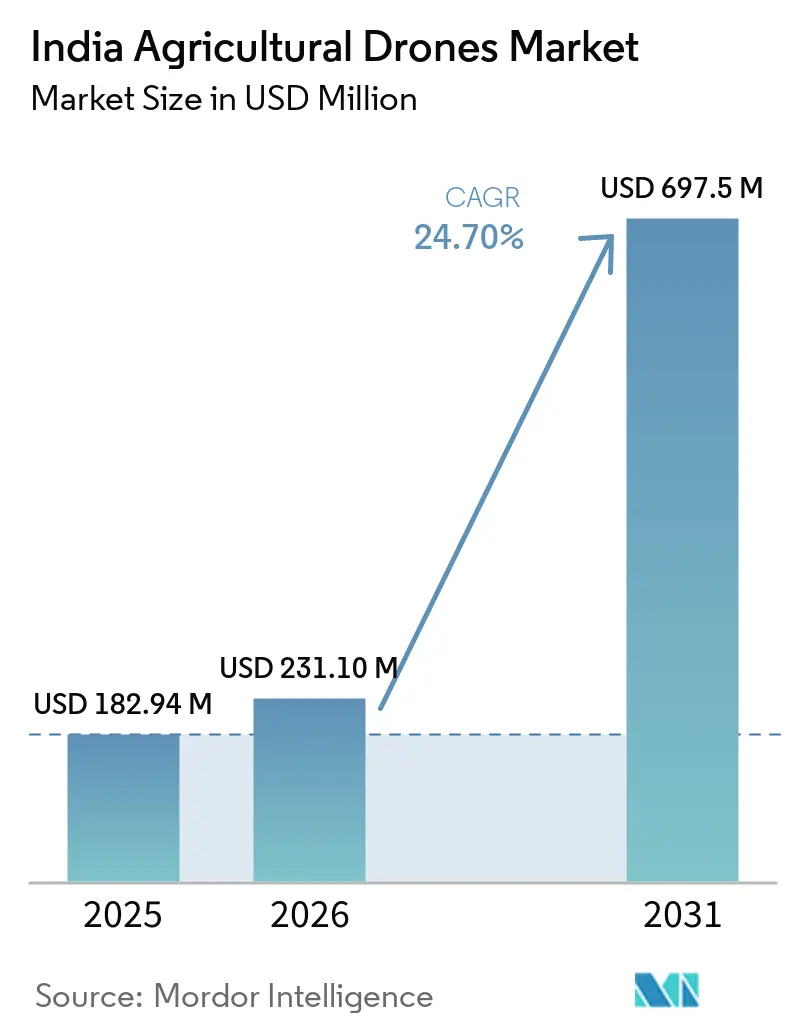

| Base Year Market Size (2025) | USD 182.94 Million |

| Market Size (2026) | USD 231.10 Million |

| Market Size (2031) | USD 697.5 Million |

| Growth Rate (2026 - 2031) | 24.70% CAGR |

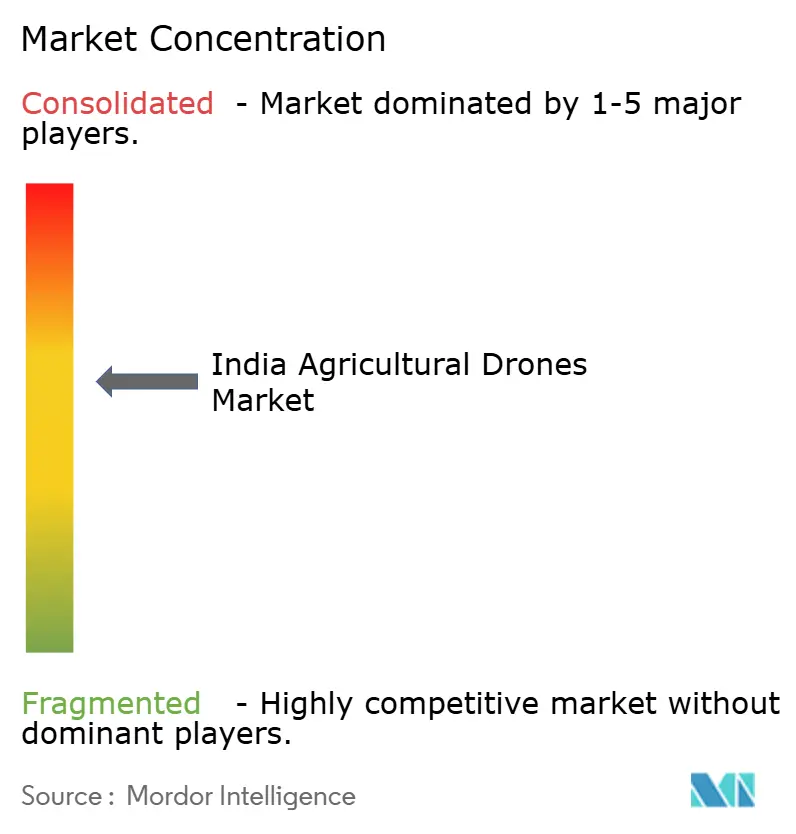

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Agricultural Drones Market Analysis by Mordor Intelligence

The India agricultural drones market size is projected to grow from USD 182.94 million in 2025 to USD 231.10 million in 2026 and further to USD 697.50 million by 2031, registering a CAGR of 24.70% between 2026 and 2031. The market is scaling quickly because subsidy support, tighter availability of field labor, and broader commercial acceptance are now moving together rather than acting as isolated demand factors. The 2022 ban on complete build-up drone imports continues to favor locally assembled platforms, making domestic pricing more responsive to local manufacturing gains than in many other countries. The market is also becoming more service-led, as battery handling, spray planning, pilot availability, and farmer-facing applications now play a larger role in contract renewal than pure airframe features. Rotary-wing platforms still dominate current deployment because they suit spray-intensive crop systems and irregular plots, while fixed-wing systems are gaining ground where larger plantation formats make longer coverage worthwhile. The main constraint remains operational readiness, as the sector continues to face pressure from pilot shortages, uneven compliance execution, and rising caution about how field data and spray records are stored and shared.

Key Report Takeaways

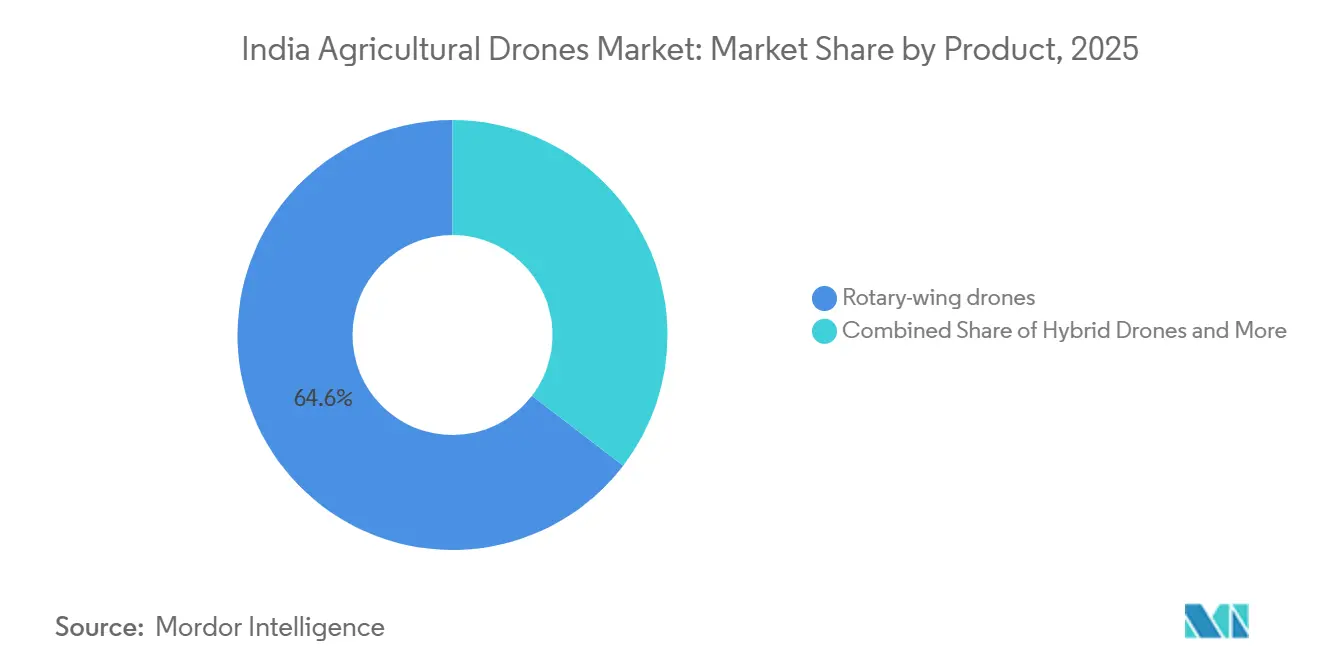

- By product, rotary-wing drones led with 64.6% of the India agricultural drones market share in 2025. Hybrid drones are forecast to expand at a 24.5% CAGR through 2031, the fastest among product categories.

- By component, hardware accounted for 53.2% share of the India agricultural drones market size in 2025. Services are projected to register the quickest growth at a 23.1% CAGR through 2031.

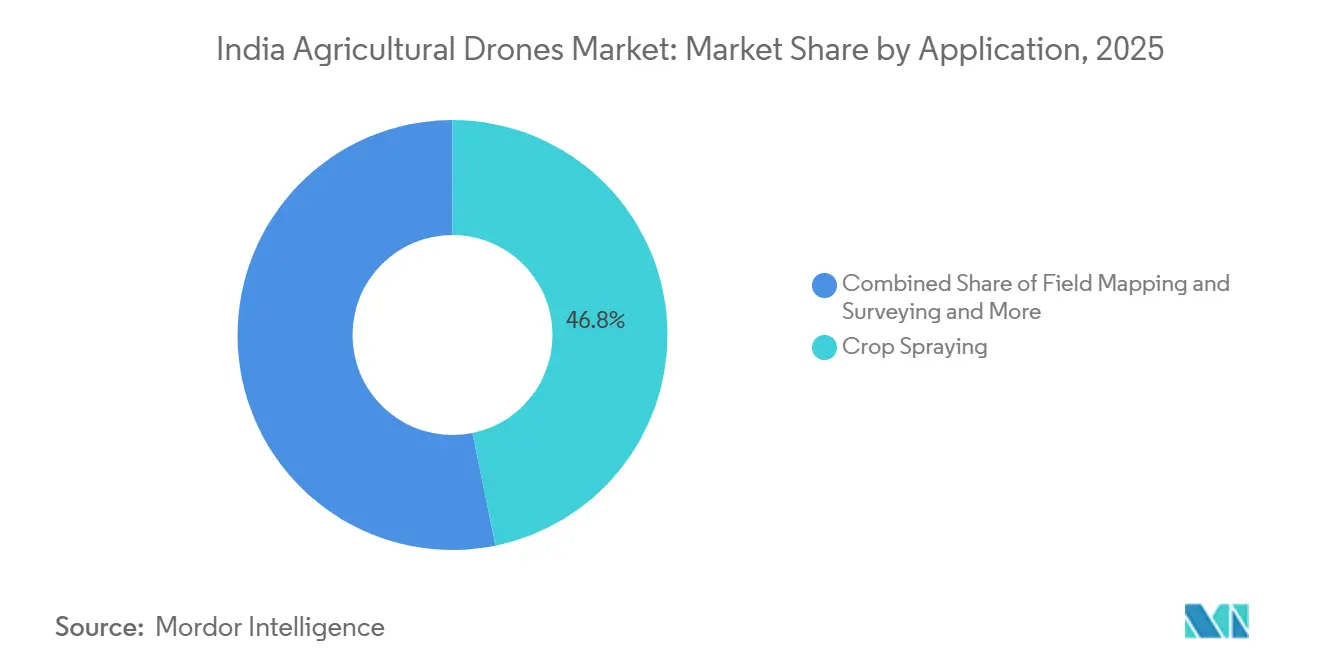

- By application, crop spraying accounted for 46.8% of the market in 2025. Field mapping and surveying are anticipated to grow at the fastest pace, with a 25.4% CAGR through 2031.

- By farm size, large-scale commercial farms accounted for 66.1% of market revenue in 2025. Small and medium farms are projected to record the highest 24.5% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Agricultural Drones Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Farm-Labor Costs and Shortages | +4.8% | India-wide, with the sharpest pressure in Punjab, Haryana, and Tamil Nadu during peak crop cycles | Medium term (2-4 years) |

| Government Subsidies | +4.2% | India-wide, with strong subsidy pull in Uttar Pradesh, Bihar, Madhya Pradesh, and Rajasthan | Short term (≤ 2 years) |

| Falling Drone Hardware Prices | +3.5% | India-wide, with strong purchase response in Punjab, Haryana, Andhra Pradesh, and Maharashtra | Short term (≤ 2 years) |

| Input-Chemical Inflation Boosting Variable-Rate Spraying | +3.2% | India-wide, with early uptake in Maharashtra and Madhya Pradesh cotton and soybean belts | Medium term (2-4 years) |

| Carbon-Credit Revenue for Low-Input Farming | +1.8% | Early activity in Maharashtra, Karnataka, and export-oriented plantation zones | Long term (≥ 4 years) |

| Women-Led Cooperative Models Accelerating Adoption | +2.1% | India-wide, with strongest near-term effect in Uttar Pradesh, Bihar, Odisha, and Chhattisgarh | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Farm-Labor Costs and Shortages

Labor scarcity during narrow spray windows has become one of the clearest commercial triggers for drone deployment across Indian farming systems. Paddy blast and cotton bollworm treatment windows are time-sensitive, and delayed spraying is costly for both farmers and input companies. Contract labor availability has tightened during peak Kharif and Rabi periods, especially in states that already face strong rural-to-urban migration. The supplied draft noted that agricultural labor rates in Punjab and Haryana rose by an estimated 8% to 12% annually between 2022 and 2025, with average farm labor wages reaching nearly USD 4.5 to USD 6.0 per day, thereby raising the relative appeal of mechanized application methods. A drone that can cover 20 to 30 acres per hour narrows the operating window, a feature manual backpack crews cannot match, especially when treatment timing matters more than unit labor cost alone. Agrochemical companies are also supporting drone deployment because more accurate application improves product performance and helps field teams manage larger territories with better consistency. This labor-driven shift is broadening the agriculture drones industry beyond equipment sales into repeat-service contracts that depend on seasonal execution quality.

Government Subsidies

Government support remains one of the strongest near-term demand anchors for the agricultural drones industry because it lowers entry costs across several user groups at the same time. The subsidy structure is layered, and that matters because it supports direct buyers, community operators, and organized rural groups rather than only individual farm owners. The Sub-Mission on Agricultural Mechanization supports drone acquisition for selected beneficiary groups, and the Namo Drone Didi scheme adds a separate route for women-led Self-Help Groups. Under the scheme, support reaches up to 80% of the drone cost, with a cap of USD 9,524 for each eligible Self-Help Group, while the broader program outlay for 2023-24 to 2025-26 stood at USD 150.1 million[1]Source: Ministry of Agriculture and Farmers Welfare, “About Scheme,” namodronedidi.php-staging.com. This framework reduces ownership risk and helps local groups treat the drone as a village service asset instead of a single-farm machine. It also links drone access with fertilizer and crop-protection distribution channels, since organized service delivery makes it easier to push standardized input programs in the field. That combination gives the market a more durable policy base than a one-time capital subsidy program would normally provide.

Falling Drone Hardware Prices

Lower upfront cost continues to widen the addressable user base for the agricultural drones industry, especially among Farmer-Producer Organizations and Custom Hiring Centers. The supplied draft noted that entry-level agricultural spray drones in India were available at around USD 3,571 in 2026 after subsidy adjustment, which brings payback within reach for operators serving 80 to 100 acres each month[2]Source: Kodainya, “Drones in Agriculture in India: The Operator's Guide,” kodainya.com. The domestic production-linked incentive program has also supported local assembly of frames, propulsion units, and spray systems, which is gradually reducing reliance on imported subsystems. The September 2025 move to a uniform 5% goods and services tax on commercial drones further lowered the cost burden for smaller service operators and organized farm groups. The benefit is not limited to cheaper ownership. Lower platform cost also makes it easier for operators to expand fleets, hold spare units, and replace batteries without weakening monthly service economics. That is why declining equipment cost is supporting both first-time purchases and repeat deployment in the market.

Input-Chemical Inflation Boosting Variable-Rate Spraying

Higher crop-protection costs have strengthened the value case for drones because the savings come from better application control rather than from ownership alone. The supplied draft noted that chemical prices remained elevated through 2024 and 2025, and that increased pressure on farm input budgets. In that setting, drone spraying becomes more attractive because precise delivery and optimized flight paths can reduce chemical use per acre by 20% to 40% compared with manual application. That saving matters most in cotton and soybean systems where treatment frequency, acreage, and product cost all raise the importance of avoiding waste. Variable-rate systems push this advantage further by adjusting nozzle output based on crop condition data from onboard sensors, which turns spraying into a data-linked field operation rather than a uniform coverage exercise. As these spray records accumulate, operators begin to hold farm-level application history that can also support crop advice and insurance workflows. This makes input inflation a persistent driver for the India agricultural drones market, because the economic benefit remains relevant even when subsidy intensity changes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Drone and Pesticide Regulations | -2.8% | India-wide, with friction strongest in cross-state deployments and crop-specific approval processes | Medium term (2-4 years) |

| Limited Skilled Pilots and Training Capacity | -2.4% | India-wide, with the widest shortage in Bihar, Odisha, Chhattisgarh, and Northeast India | Medium term (2-4 years) |

| Patchy Rural 4G and 5G Connectivity | -1.6% | India-wide, with heavier exposure in hilly, tribal, and flood-prone districts | Long term (≥ 4 years) |

| Data Sovereignty Concerns Among FPOs | -1.0% | India-wide, with early sensitivity in Maharashtra, Punjab, and Karnataka | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Drone and Pesticide Regulations

Regulation remains one of the most important constraints because the operating burden is split across aviation compliance and pesticide-use approval. The aviation side runs through the Digital Sky system, which covers unique identification, pilot certification, and permission-linked operations. Separate crop and chemical approvals add another layer, since drone application rules can vary by product, formulation, and local advisory practice[3]Source: FarmToPlot, “Agricultural Drone Regulations in India: Directorate General of Civil Aviation Rules Every Farmer Must Know,” farmtoplot.com. A service operator may be technically ready to fly but still face delays before a specific spray program can begin in a new area. Cross-state expansion becomes slower because each new operating geography can bring another round of procedural checks and local alignment. Smaller providers are affected the most because compliance work consumes working capital and management time that larger operators can spread across bigger fleets. This regulatory fragmentation keeps the market from scaling as quickly as the demand picture alone would suggest.

Limited Skilled Pilots and Training Capacity

Pilot availability remains a practical bottleneck because drone fleet growth is moving faster than specialized agri-operation capability in many districts. As of February 2026, India had 39,800 certified remote pilots and 240 approved Remote Pilot Training Organizations, against a registered fleet of more than 38,500 drones[4]Source: Press Information Bureau, “India's Drone Ecosystem: From Policy to Public Service Transformation,” pib.gov.in. On paper, that looks close to balance, but the ratio leaves little room for seasonal peaks, regional gaps, multi-shift use, or pilot attrition. Agricultural flying also requires more than licensing. Effective operators need to understand nozzle calibration, canopy variation, spray timing, and how formulation changes affect field execution. Companies that built their own training networks have a clear advantage because trained pilots also become deployment infrastructure. Until training quality and district-level availability improve further, pilot scarcity will remain a real drag on the India agricultural drones market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Rotary-Wing Platforms Sustain Revenue Leadership

Rotary-wing drones held 64.6% of product revenue in 2025, leading the India agricultural drones market share among platform types. Their lead came from spray-intensive crop patterns, irregular plot geometry, and hover control in narrow fields across fragmented agricultural landholdings and smallholder-dominated cultivation environments. Subsidy-backed purchases by Farmer-Producer Organizations and service operators kept multirotors in the lead.

Hybrid drones are forecast to expand at a 24.5% CAGR through 2031, the fastest among product categories, as plantation estates and larger field blocks seek longer-range coverage with Vertical Take-Off and Landing (VTOL) flexibility and improved mapping efficiency. Their use is rising in grapes, bananas, and orchard belts where contiguous acreage supports longer sorties and precision monitoring applications. Fixed-wing drones remain relevant for large-area surveying operations, while hybrid platforms are increasingly preferred for balancing endurance and operational flexibility. Product improvements are still evident in stronger weather protection, better connectivity, and smarter path planning in newer launches. This mix keeps rotary-wing systems dominant today while widening the future role of fixed-wing and hybrid platforms in the market.

By Component: Hardware Anchors Value and Services Accelerate Fastest

Hardware accounted for 53.2% of component revenue in 2025, giving it the largest position in the India agricultural drones market size across components. Spending remained focused on spray systems, batteries, sensors, and charging support as agricultural drone deployment networks nationwide expanded. This reflected a deployment phase in which asset purchases still materially outweighed software subscriptions and service fees.

Services are projected to register the quickest growth at a 23.1% CAGR through 2031 as cooperatives, state programs, and commercial operators shift spending from ownership to recurring-use models. Software is also gaining relevance because flight management, prescription mapping, crop analytics, and fleet-management tools are becoming increasingly integrated into daily farm operations. The India agriculture drones industry is therefore moving from hardware-first adoption toward a more balanced mix of equipment, software, and recurring service value. Time-stamped spray logs further strengthen software adoption by supporting insurance documentation, regulatory compliance, and agronomic advisory workflows. As hardware prices decline, the overall revenue mix is estimated to tilt further toward services and software across the market.

By Application: Crop Spraying Anchors Share and Field Mapping Scales Fastest

Crop spraying accounted for 46.8% of application revenue in 2025, making it the largest use case in the Indian agriculture drones market. Its lead rested on paddy, cotton, sugarcane, and vegetable cultivation, where precision delivery can replace manual backpack spraying. Rising agrochemical costs reinforced this operating case across states further, while labor shortages and exposure risks accelerated farmer preference for drone-based spraying solutions nationwide.

Field mapping and surveying are anticipated to grow at the fastest pace, with a 25.4% CAGR through 2031, as drone-generated imagery increasingly supports land records, farm planning, precision agriculture workflows, and organized lending use cases. The Survey of Villages and Mapping with Improvised Technology in Village Areas program completed drone surveys across 3.28 lakh villages by December 2025, demonstrating that mapping workflows are already gaining national operational relevance. Crop monitoring remains another important growth lane because imagery is becoming easier to interpret for crop health through software overlays. Soil analysis, livestock monitoring, and irrigation uses are smaller today, but they have room to scale as agronomic data services mature. That widening mix keeps the market from depending only on spraying demand.

By Farm Size: Large Farms Hold Revenue While Smallholders Drive Growth

Large-scale commercial farms accounted for 66.1% of segment revenue in 2025, giving them the largest share across farm-size groups. Their advantage came from contiguous fields, better mobilization economics, and higher spray hours per deployment. These conditions let service operators sustain margins while offering competitive rates to large farms at scale.

Small and medium farms are projected to record the highest 24.5% CAGR through 2031 because Drone-as-a-Service models reduce the need for direct ownership. Group-based access through Self-Help Groups and Farmer-Producer Organizations is transforming drones into shared rural utility assets rather than individually owned equipment. The India agriculture drones industry is therefore expanding into smaller landholdings through service aggregation models instead of one-to-one equipment sales. As cluster-based demand increases, procurement decisions are becoming more dependent on operational outcomes, spraying efficiency, and service reliability than on hardware specifications alone. This shift is estimated to remain a defining trend for the agricultural drones industry throughout the forecast period.

Geography Analysis

North India remains the highest-density adoption zone in the India agricultural drones market because Punjab, Haryana, and Uttar Pradesh combine labor pressure, organized procurement channels, and strong crop-treatment intensity. Punjab and Haryana continue to generate a large share of active spray hours through paddy and wheat systems, where treatment timing is highly structured. Uttar Pradesh adds scale through broad rural group networks and strong scheme visibility under women-led deployment programs. This gives the northern belt a lead in both commercial utilization and institutional familiarity with drone services.

South and West India form the second major operating cluster in the market because horticulture, plantation crops, and commercial field layouts improve service economics. Andhra Pradesh, Telangana, Karnataka, and Maharashtra support use cases in grapes, bananas, cotton, and soybean systems where spray frequency and field geometry favor repeated deployment. These states also benefit from a more diverse mix of spraying, mapping, and monitoring demand than regions that depend on only one crop system. That diversity gives operators better asset use throughout the year and reduces dependence on a single treatment cycle.

Eastern and Central India remain the emerging frontier because lower current penetration sits beside strong future access potential. Bihar, Odisha, West Bengal, Jharkhand, and Chhattisgarh are important because smaller holdings can still become viable through cooperative service structures and cluster-based deployment. The February 2026 partnership between the National Council for Cooperative Training and AVPL International targeted more than 63,000 Primary Agricultural Credit Societies, which could materially widen district-level skilling and drone familiarity in these regions. This matters because these states need more local operators and support infrastructure before demand can scale smoothly. As training and shared access improve, Eastern and Central India are likely to contribute more meaningfully to the agricultural drones market through the rest of the forecast period.

Competitive Landscape

The India agricultural drones market remains moderately concentrated, with DJI, XAG Co., Ltd., Garuda Aerospace Pvt. Ltd., Marut Drones, and General Aeronautics Pvt. Ltd. representing some of the most visible participants across hardware, spraying, and field-service operations. Garuda Aerospace Pvt. Ltd. has strengthened its position through integrated capabilities spanning drone manufacturing, pilot training, and deployment services, while DJI continues to maintain a strong benchmark status in spraying and imaging platforms. At the same time, increased government support and rising investments in service networks are steadily strengthening organized competition across India’s agricultural drone ecosystem.

Competition is increasingly shaped by service depth rather than airframe design alone. Operators capable of managing battery ecosystems, pilot networks, agronomy-linked spray planning, and farmer-facing digital workflows are better positioned to secure repeat business and long-term deployment contracts. General Aeronautics Pvt. Ltd. reflects this trend through collaborations with crop-input and agricultural ecosystem partners that extend deployment reach and strengthen field integration capabilities. Import restrictions on complete drone build-up units continue supporting domestic assemblers and local manufacturing activity, while also encouraging indigenous technology development across the market.

Strategic positioning across the market broadly falls into three models. Vertically integrated operators such as Garuda Aerospace Pvt. Ltd. and Marut Drones emphasize pilot training, fleet ownership, manufacturing, and government-linked deployments to build distribution advantages. Hardware-oriented companies such as XAG Co., Ltd., General Aeronautics Pvt. Ltd., Hylio Inc., and iotechworld.com focus on platform capability, crop-use optimization, and channel-based market expansion. Software and analytics players such as DroneDeploy and Trimble Inc. concentrate on mapping, analytics, precision agriculture workflows, and fleet-management layers rather than direct farmer equipment sales. Companies including Parrot Drones SAS., Terra Drone Corporation, EagleNXT, Kray Technologies, Yamaha Motor Co., Ltd., and Rattanindia Group are also expanding their presence through autonomous technologies, spraying systems, analytics integration, and strategic partnerships. These developments indicate that long-term scale in the market will increasingly depend on manufacturing capability, field execution, software integration, and training infrastructure rather than product sales alone.

India Agricultural Drones Industry Leaders

Garuda Aerospace Pvt. Ltd.

DJI

iotechworld.com

Marut Drones

General Aeronautics Pvt. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: EFT and Bharat Skytech have launched "EFT BHARAT," a co-branded manufacturing initiative aimed at producing EFT's E610P agricultural drone domestically. This includes transferring production molds for the tank and canopy to an Indian facility in alignment with Make in India protocols.

- January 2026: Garuda Aerospace Pvt. Ltd. has inaugurated a Drone Battery Manufacturing Facility and an Academic Block for its Directorate General of Civil Aviation-approved Remote Pilot Training Organization in Chennai. This facility enhances India's domestic drone battery supply chain and expands Garuda's end-to-end manufacturing integration beyond airframes.

- September 2025: The Government of India reduced the goods and services tax on commercial drones to a uniform 5%, down from the previous range of 18% to 28%. This policy change has lowered entry costs for small and medium drone service operators and enhanced the affordability of drone purchases for Farmer-Producer Organizations.

India Agricultural Drones Market Report Scope

Agricultural drones are unmanned aerial systems used for crop spraying, monitoring, mapping, surveying, and precision farming operations in agriculture. The India Agricultural Drones Market Report is Segmented by Product (Fixed-Wing Drones, Rotary-Wing Drones, and Hybrid Drones), by Component (Hardware, Software, and Services), by Application (Field Mapping and Surveying, Crop Spraying, Crop Monitoring/Field Surveillance, Livestock Monitoring, Irrigation Management, and Soil and Field Analysis), and by Farm Size (Large-Scale Commercial Farms and Small and Medium Farms). The Market Forecasts are Provided in Terms of Value (USD).

| Fixed-wing Drones |

| Rotary-wing Drones |

| Hybrid Drones |

| Hardware |

| Software |

| Services |

| Field Mapping and Surveying |

| Crop Spraying |

| Crop Monitoring/Field Surveillance |

| Livestock Monitoring |

| Irrigation Management |

| Soil and Field Analysis |

| Large-scale Commercial Farms |

| Small and Medium Farms |

| By Product | Fixed-wing Drones |

| Rotary-wing Drones | |

| Hybrid Drones | |

| By Component | Hardware |

| Software | |

| Services | |

| By Application | Field Mapping and Surveying |

| Crop Spraying | |

| Crop Monitoring/Field Surveillance | |

| Livestock Monitoring | |

| Irrigation Management | |

| Soil and Field Analysis | |

| By Farm Size | Large-scale Commercial Farms |

| Small and Medium Farms |

Key Questions Answered in the Report

What is the current value of agriculture drones in India in 2026?

The India agricultural drones market size is projected to grow from USD 182.94 million in 2025 and USD 231.10 million in 2026 to USD 697.50 million by 2031, registering a CAGR of 24.70% between 2026 and 2031.

Which product type leads drone adoption in Indian farming?

Rotary-wing drones led product revenue with 64.6% in 2025 because they fit irregular plots, spray-intensive crops, and short-range precision work.

Why are small and medium farms becoming important users?

Growth is shifting toward smaller holdings because Drone-as-a-Service, Self-Help Group models, and Farmer Producer Organization access reduce the need for direct ownership.

Which application drives the largest demand today?

Crop spraying held 46.8% of application revenue in 2025, supported by chemical-intensive cultivation and the push to replace manual backpack spraying.

Page last updated on: