Africa Agricultural Tractor Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

| Market Size (2025) | USD 1.9 Billion |

| Market Size (2030) | USD 2.60 Billion |

| Growth Rate (2025 - 2030) | 6.50% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Agricultural Tractor Market Analysis by Mordor Intelligence

The Africa agricultural tractor market size is USD 1.9 billion in 2025 and is projected to reach USD 2.6 billion by 2030, growing at a CAGR of 6.5%. The market growth is driven by increasing mechanization, expansion of commercial farming estates, and government support programs. The introduction of innovative financing options has reduced barriers to equipment ownership, while advancements in precision guidance and connectivity technologies encourage farmers to upgrade to higher-horsepower tractors. Digital platforms for equipment rental have improved access for smallholder farmers by increasing utilization rates. Currency fluctuations and fragmented landholdings constrain market growth, while addressing the shortage of skilled operators and maintenance personnel remains a key challenge.

Key Report Takeaways

- By engine power, the 35-50 HP range accounted for 35.2% of the Africa agricultural tractor market size in 2024, and the 76-100 HP range is forecast to grow at 8.2% CAGR to 2030.

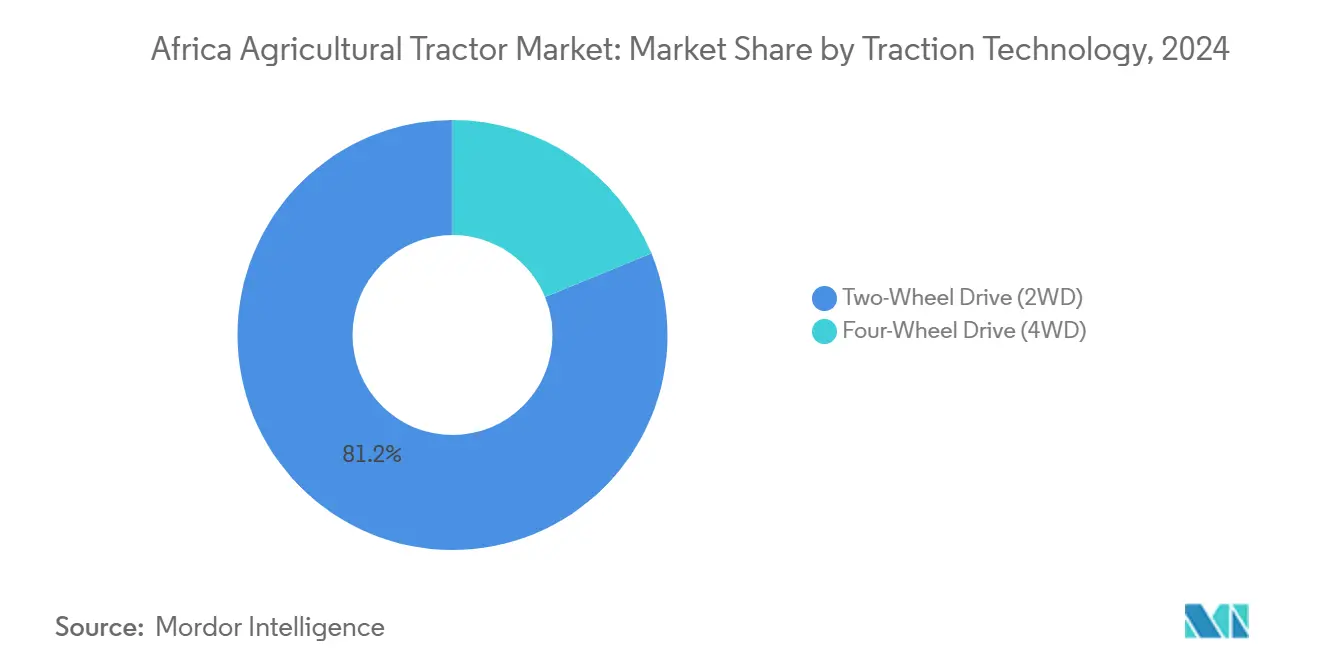

- By traction technology, 2-wheel drive (2WD) units held 81.2% share of the Africa agricultural tractor market in 2024, with 4-wheel drive (4WD) models advancing at a 10.1% CAGR through 2030.

- By application, row-crop farming captured 44% of the market share in 2024, and the plantation and estate crops recorded the fastest CAGR at 9.1% through 2030.

- By geography, South Africa led with a 34.7% of the market share in 2024, while Egypt is projected to expand at a 10.4% CAGR through 2030.

- The top five companies - Deere & Company, AGCO Corporation, CNH Industrial N.V., Mahindra & Mahindra Ltd., and Kubota Corporation accounted for 76% of the market share in 2024.

Africa Agricultural Tractor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing adoption of farm mechanization and precision agriculture | +1.8% | South Africa and Kenya | Medium term (2-4 years) |

| Government subsidies and mechanization programs | +1.2% | Nigeria, Kenya, South Africa, and Egypt | Short term (≤ 2 years) |

| Growth in commercial horticulture and export-oriented cash crops | +0.9% | Egypt, South Africa, and Kenya | Medium term (2-4 years) |

| Expansion of agricultural credit and tractor financing facilities | +0.8% | Nigeria and Kenya | Short term (≤ 2 years) |

| Pay-as-you-go tractor leasing via mobile platforms | +0.6% | Sub-Saharan core, spill-over to North Africa | Long term (≥ 4 years) |

| Uptake of low-horsepower autonomous electric tractors on large estates | +0.4% | South Africa and Egypt | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption of Farm Mechanization and Precision Agriculture

Africa currently operates fewer than two tractors per 1,000 hectares, indicating significant potential for equipment adoption. Nigeria aims to deploy tractors across 9 million hectares of new production through a public-private partnership with Hello Tractor over five years. South African commercial farmers are implementing GPS guidance and telematics systems, while Case IH eliminated subscription fees for its FieldOps application on machines purchased after October 2024 to increase usage. Kenya's Big Four Agenda supports automation trials combining mechatronics with data-driven crop management[1]Source: European Journal of Electrical Engineering and Computer Science, “Integration of Mechatronic and Automation Technology in Sustainable Farming for Achieving Food Security in Kenya,” ejece.org. The improved yields and reduced waste from these technologies encourage farmers to invest in higher horsepower and advanced machinery in the Africa agricultural tractor market.

Government Subsidies and Mechanization Programs

Government subsidies are reducing initial costs for farmers. Kenya's National Fertilizer Subsidy Program allocated 3.55 billion Kenyan shillings (USD 23 million) in September 2022 and distributed 3.5 million 50 kg bags by July 2023, driving demand for agricultural equipment[2]Source: CGIAR, “How is Kenya's National Fertilizer Subsidy Program working?” cgiar.org. Nigeria has shifted from government-operated rental programs to mixed models combining private operators and pay-as-you-go leasing, which has improved equipment utilization. South Africa uses blended financing mechanisms in its agricultural master plan to provide credit to farmers, supporting export earnings that reached USD 13.7 billion in 2024[3]Source: South African Government, “Agriculture is a Vital Part of Our Growth Story,” stateofthenation.gov.za. Egypt's climate-smart strategy emphasizes mechanization to address projected yield reductions by 2050. Success depends on combining financial support with private service providers and farmer training programs.

Growth in Commercial Horticulture and Export-Oriented Cash Crops

The demand for specialized tractors and attachments is increasing due to the cultivation of high-value fruits, vegetables, and estate crops. Egypt's agricultural exports are growing due to improved mechanization and quality control measures. South African vineyards are investing in new equipment following drought-related production declines, with expectations of harvest recovery by 2025. In Kenya, horticultural producers are adopting mid-range horsepower tractors to maintain consistent yields. Similar transitions are occurring in Malawi through United States Agency for International Development (USAID) initiatives as exporters upgrade their operations. This shift toward premium crop production is driving demand for versatile 51-75 HP tractors and specialty implements across the Africa agricultural tractor market.

Expansion of Agricultural Credit and Tractor Financing Facilities

Blended finance mechanisms are improving access to agricultural tractors in Africa. Hello Tractor and John Deere received USD 4.5 million in philanthropic funding from Heifer International to expand their equipment leasing programs. The Agricultural Credit Facility in Uganda provides machinery loans, though limited agricultural extension services affect adoption rates. In South Africa, favorable rainfall patterns have improved revenue forecasts, increasing commercial banks' willingness to provide financing. In Kenya, asset-backed lending supported by telematics data and mobile payment systems has reduced default risks. CNH Industrial maintains steady unit sales through integrated financing options. These financing approaches are increasing purchasing capacity across the Africa agricultural tractor market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented land holdings limiting tractor utilization rates | -1.4% | Kenya and Nigeria | Long term (≥ 4 years) |

| Shortage of skilled operators and maintenance technicians | -0.9% | Rural regions continent-wide | Medium term (2-4 years) |

| Volatile foreign-exchange rates and import duties inflating tractor purchase prices | -1.1% | Kenya, Nigeria, and Ghana | Short term (≤ 2 years) |

| Grey-market spare-parts supply-chain disruptions | -0.6% | West Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Land Holdings Limiting Tractor Utilization Rates

Farm plot sizes continue to decrease as families subdivide their agricultural holdings, reducing equipment efficiency. Studies in Kenya show increased transportation costs and equipment downtime due to movement between scattered land parcels. Labor assessments in Eastern and Southern Africa indicate that demand surpasses supply, emphasizing access limitations rather than lack of need. While Rwanda's Land Use Consolidation program demonstrates promise, it primarily benefits farmers with adjacent plots. Though custom-hire services help address land fragmentation issues, significant fleet management costs remain. Land parcel exchanges and intensive cropping practices may enhance equipment utilization, but broad implementation requires time.

Shortage of Skilled Operators and Maintenance Technicians

The growth in agricultural equipment outpaces technical training availability, particularly in remote regions. While women tractor operators in Ghana show potential to expand the workforce, cultural barriers and insufficient training programs limit advancement. Surveys in Nigeria indicate that a small percentage of smallholder farmers access tractor services, with education levels and prior experience significantly affecting adoption rates. The prevalence of unofficial spare parts hampers proper maintenance and reduces equipment lifespan. In Kenya, the 16% VAT on components, despite duty-free tractor imports, increases operational costs[4]Source: The World Bank, “Agribusiness Indicators: Kenya,” worldbank.org. The expansion of vocational training facilities and manufacturer-supported training centers is essential to enhance the long-term value of Africa's agricultural tractor fleet.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Engine Power: 35 – 50 HP Dominance with High-Power Growth

The 35-50 HP segment holds 35.2% of the Africa agricultural tractor market share in 2024, providing an optimal cost-to-performance ratio for diverse smallholder operations. Farmers access these units through financing programs for land preparation, seeding, and transport activities. The 76-100 HP tractor segment grows at 8.2% CAGR, driven by farm consolidation and expansion of export crops. This market evolution toward higher-powered models increases revenue growth beyond unit sales volumes.

Manufacturers develop modular platforms across power segments. In 2024, Mahindra introduced the OJA series in Cape Town, featuring 20-70 HP four-wheel-drive models with digital intelligence systems, emphasizing adaptability. While below-35 HP tractors remain crucial for orchards and small plots, their growth is limited as rental fleets prefer mid-range machines. Over 100 HP tractors represent a small but growing segment, particularly in South African grain-producing regions where productivity requirements support higher investments. The varying demand across horsepower ranges reflects the correlation between mechanization adoption, farm size, and economic capacity.

By Traction Technology: 2WD Foundation with 4WD Acceleration

Two-wheel drive (2WD) tractors account for 81.2% of the Africa agricultural tractor market size in 2024. The dominance stems from the region's predominantly flat terrain and cost considerations. Four-wheel drive (4WD) tractors are projected to grow at a 10.1% CAGR as farmers expand operations into sloped and uncultivated areas while implementing precision agriculture. This growth trend is particularly evident in South Africa, where improved rainfall patterns support agricultural expansion.

Four-wheel drive (4WD) tractors reduce soil compaction and enable the use of heavier implements required for conservation tillage practices. The Kenyan government's focus on food security supports increased adoption of 4WD tractors, which offer greater versatility for multiple field operations throughout the growing season. Telematics data demonstrating operational efficiency has prompted agricultural contractors to invest in 4WD models to enhance service reliability. This ongoing transition toward performance-focused equipment is anticipated to gradually reduce the two-wheel-drive market share.

By Application: Row-Crop Leadership with Plantation Growth

Row-crop farming accounts for 44% of 2024 revenue, as cereals and grains occupy the majority of continental acreage under government food-security programs. Consistent subsidies for staple production maintain mechanization in this segment. Plantation and estate crops demonstrate the highest growth rate at 9.1% CAGR, driven by export-oriented horticulture, viticulture, and nut orchards. Egypt depends on mechanized horticulture to maintain export competitiveness, as agrifood contributes a significant percentage to the gross domestic product.

Kenyan mid-scale producers are transitioning to avocados and macadamia cultivation, which requires specialized implements and reliable mid-horsepower tractors. South African wine estates are recovering from droughts and implementing precision sprayers that integrate with 4WD units. This diversification drives the Africa agricultural tractor market toward versatile machines that can adapt to changing crop mixes.

Geography Analysis

South Africa maintained its market leadership with a 34.7% share of the Africa agricultural tractor market in 2024. The country's agricultural machinery market benefits from established financing systems and an experienced dealer network. Favorable rainfall conditions in 2025 and major agricultural events like NAMPO Harvest Day support the demand for medium to high-horsepower tractors. Large-scale producers focusing on export markets increasingly adopt precision agriculture-enabled models.

Egypt shows the highest growth potential with a projected CAGR of 10.4% through 2030. Government modernization initiatives, including lower import duties and environmental sustainability programs, drive capital investment in the market. The agricultural sector's significant employment contribution ensures continued political support for mechanization efforts. The well-developed infrastructure in the Nile valley region facilitates equipment distribution, enhancing market growth.

Kenya continues to drive growth in the Rest of Africa segment. While mechanization supports the country's Big Four Agenda food security goals, the 2025 Finance Bill's increased VAT (Value Added Tax) on agricultural inputs may impact market growth. Nigeria's procurement of 3,000 machinery units through Zimbabwe demonstrates regional cooperation in addressing supply constraints. Ghana, Tanzania, and Côte d'Ivoire demonstrate growth potential as financing options expand. Despite regional variations, increasing commodity prices and digital equipment rental platforms improve mechanization returns across different agricultural zones, supporting consistent demand in the Africa agricultural tractor market.

Competitive Landscape

The Africa agricultural tractor market shows moderate consolidation, with five major manufacturers - Deere & Company, AGCO Corporation, CNH Industrial N.V., Mahindra & Mahindra Ltd., and Kubota Corporation - accounting for 76% of market revenue in 2024. Deere & Company maintains market leadership, followed by AGCO Corporation and CNH Industrial N.V. Deere's competitive advantage stems from its precision software ecosystems that generate recurring revenue. AGCO strengthens its regional presence through a USD 100 million investment in local Massey Ferguson production in Algeria, reducing import costs and enhancing after-sales service.

CNH Industrial enhances its offering through a partnership with Intelsat for satellite connectivity, providing improved performance analytics for operators, and showcases the importance of connectivity solutions in agricultural mechanization. Asian manufacturers TAFE and Sonalika gain market share in low and mid-range horsepower segments through competitive pricing and expanding dealer networks.

The electric and autonomous tractor segments present significant growth opportunities, where traditional manufacturers face competition from emerging specialized manufacturers and technology companies. The market structure indicates potential consolidation, particularly among smaller regional players who lack resources for technology development and service network expansion necessary for long-term market success.

Africa Agricultural Tractor Industry Leaders

Deere & Company

AGCO Corporation

CNH Industrial N.V.

Mahindra & Mahindra Ltd.

Kubota Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Massey Ferguson’s MF 8S Dyna E-Power completed the Morocco Desert Challenge, finishing 75th out of 144 competitors, underscoring AGCO engineering resilience.

- February 2025: AGCO partnered with SDF to broaden Massey Ferguson’s low to mid-horsepower portfolio for global markets, including Africa.

- October 2024: Volkswagen Group Africa began the GenFarm e-tractor pilot in Rwanda, pairing battery units with renewable power hubs.

- June 2024: Case IH introduced the Case IH Optum tractor at NAMPO Harvest Day in Bothaville, South Africa. The tractor comes in 270 and 300 models and features a 6.7-FPT six-cylinder engine that delivers 202 to 225kW.

Africa Agricultural Tractor Market Report Scope

Agricultural tractors are types of machinery used in farming or other agriculture operations such as plowing, tilling, planting, and harvesting. They are equipped with a variety of attachments and implements, allowing them to perform a wide range of functions on farms. The report defines the market in terms of end users that only procure tractors for agricultural operations. The end users include farmers and institutional buyers operating in agriculture and allied production. The corporations in the tractor industry operate in the B2B and B2C formats. However, bulk buyers procuring tractors for retail sales are not considered in this market to eliminate any 'double-count' error in market estimations.

The African agricultural tractor market is segmented by engine power (less than 35 HP, 35 to 50 HP, 51 to 75 HP, 76 to 100 HP, and above 100 HP), and Geography (South Africa, Kenya, and the Rest of Africa). The report offers the market size and forecasts in terms of volume (Units) and value (USD) for all the above segments.

| Less than 35 HP |

| 35 - 50 HP |

| 51 - 75 HP |

| 76 - 100 HP |

| Above 100 HP |

| 2-Wheel Drive (2WD) |

| 4-Wheel Drive (4WD) |

| Row-Crop Farming |

| Horticulture and Viticulture |

| Plantation and Estate Crops |

| South Africa |

| Kenya |

| Egypt |

| Rest of Africa |

| By Engine Power | Less than 35 HP |

| 35 - 50 HP | |

| 51 - 75 HP | |

| 76 - 100 HP | |

| Above 100 HP | |

| By Traction Technology | 2-Wheel Drive (2WD) |

| 4-Wheel Drive (4WD) | |

| By Application | Row-Crop Farming |

| Horticulture and Viticulture | |

| Plantation and Estate Crops | |

| By Geography | South Africa |

| Kenya | |

| Egypt | |

| Rest of Africa |

Key Questions Answered in the Report

What is the projected value of the Africa agricultural tractor market by 2030?

The market is forecast to reach USD 2.6 billion by 2030, growing at a 6.5% CAGR.

Which horsepower segment currently holds the largest share?

Tractors in the 35-50 HP range led with 35.2% of 2024 revenue.

Which country is projected to post the fastest growth?

Egypt is projected to advance at a 10.4% CAGR through 2030 due to modernization programs and export ambitions.

How dominant are diesel engines in the propulsion mix?

Diesel units accounted for 94.5% of 2024 sales, although hybrids and electrics are growing the fastest.

What role do digital rental platforms play?

Platforms such as Hello Tractor increase utilization and access, and are forecast to grow at a 13.7% CAGR over the forecast period.

Who are the leading manufacturers?

Deere & Company, AGCO Corporation, CNH Industrial N.V., Mahindra & Mahindra Ltd., and Kubota Corporation accounted for 76% of the market share in 2024.

Page last updated on: