Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

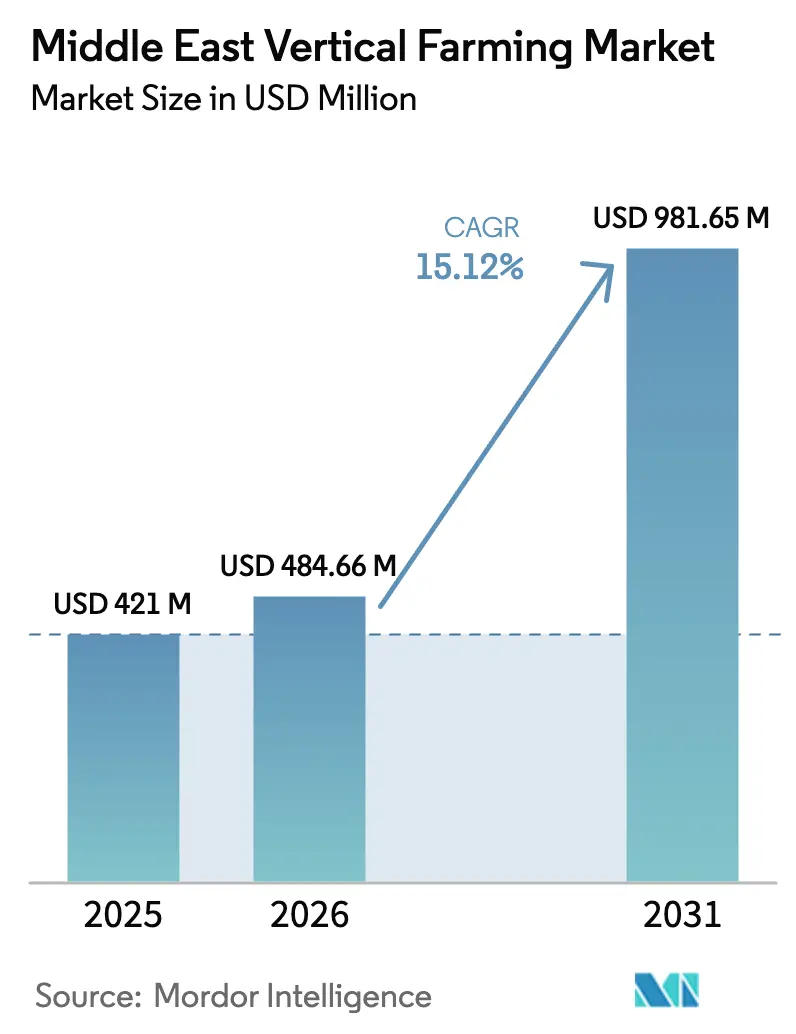

| Base Year Market Size (2025) | USD 421.0 Million |

| Market Size (2026) | USD 484.66 Million |

| Market Size (2031) | USD 981.65 Million |

| Growth Rate (2026 - 2031) | 15.12% CAGR |

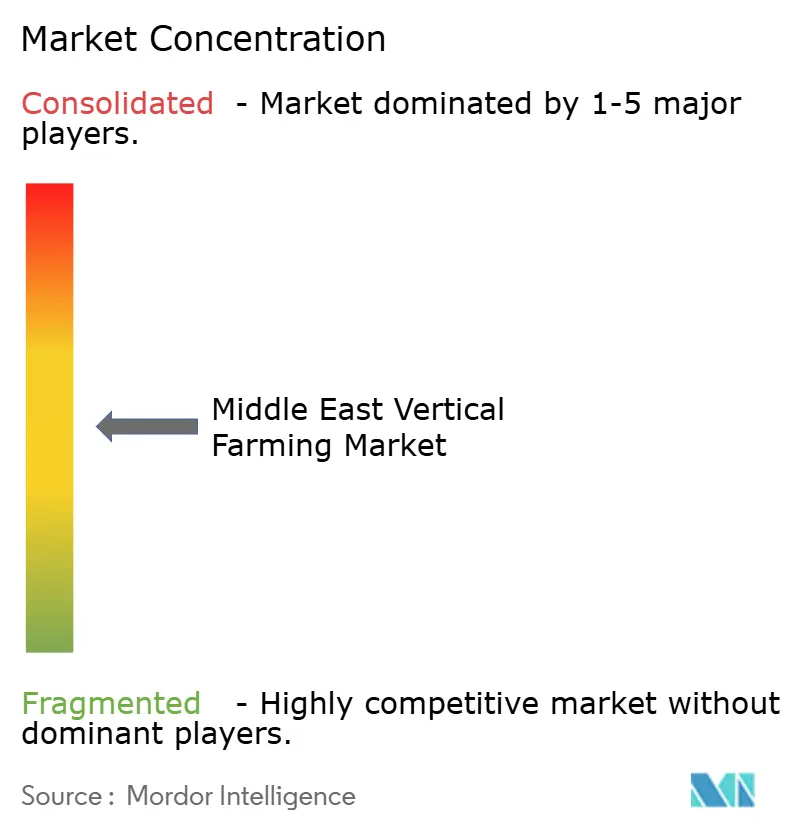

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Vertical Farming Market Analysis by Mordor Intelligence

The Middle East vertical farming market size in 2026 is estimated at USD 484.66 million, growing from 2025 value of USD 421.0 million with 2031 projections showing USD 981.65 million, growing at 15.12% CAGR over 2026-2031. Government support, sovereign wealth investments, and increasing consumer demand for traceable produce drive the market growth in the region. The Gulf Cooperation Council (GCC) states recognize water scarcity as a critical challenge, making indoor hydroponic systems an essential solution as they consume 95% less water compared to traditional farming methods. The region's economic diversification initiatives direct both public and private investments toward agricultural technology, establishing vertical farming as a key component of national food security plans. Sovereign wealth funds are investing through minority stakes and acquisitions to acquire operational expertise, while retailers allocate space for premium locally-grown produce. The market's increasing competition drives operators to focus on automation and energy-efficient solutions to reduce operational costs and counter high capital expenditure and electricity costs.

Key Report Takeaways

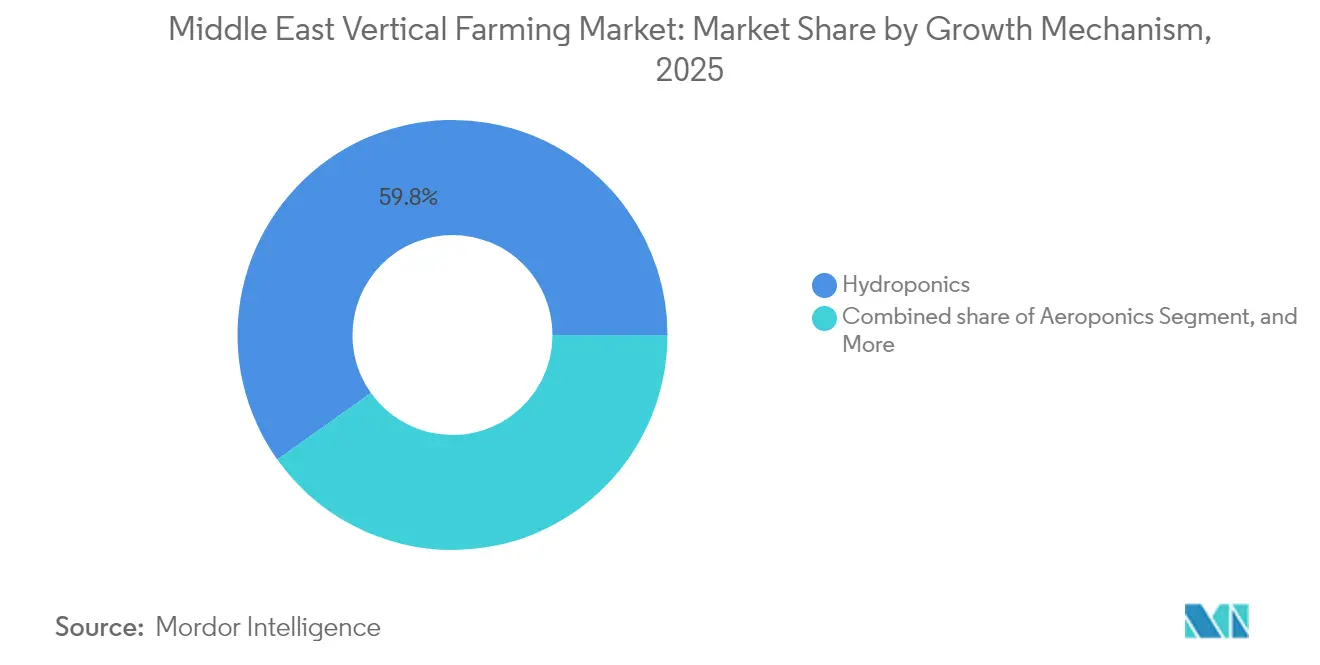

- By growth mechanism, hydroponics held 59.84% of the Middle East vertical farming market share in 2025, whereas aeroponics is advancing at a 15.55% CAGR through 2031.

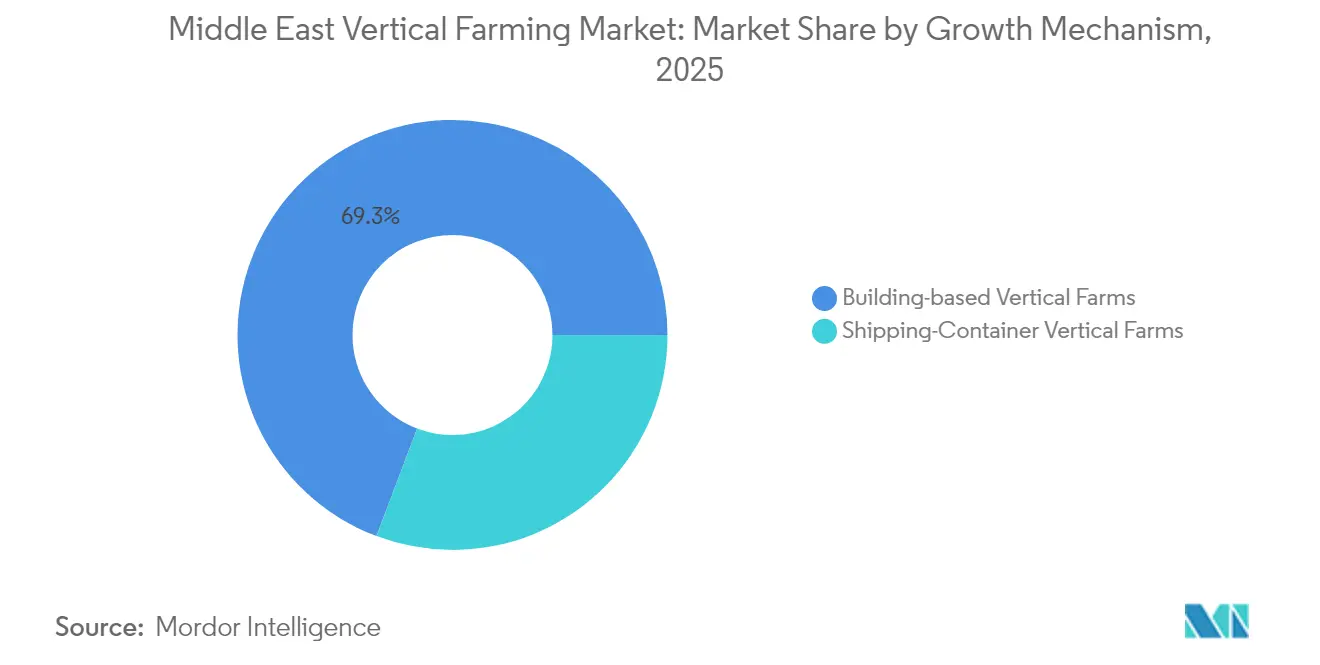

- By Structure, building-based vertical farms accounted for 69.25% of the Middle East vertical farming market size in 2025, yet shipping-container systems are moving ahead at a 12.76% CAGR on the back of hospitality and campus demand.

- By crop type, vegetables led with 47.35% revenue share in 2025, and herbs and micro-greens are rising at an 11.62% CAGR to 2031.

- Geographically, Saudi Arabia captured a 40.42% share of the market in 2025, while the United Arab Emirates recorded the fastest trajectory at 13.23% CAGR.

- The top five companies, such as Pure Harvest Smart Farms Ltd., Bustanica (Emirates Crop One LLC), AeroFarms, Madar Farms, and VeggiTech Hydroponic Technologies Private Limited (SNASCO Holding Company), together commanded 45.9% revenue in 2024, signaling moderate consolidation and leaving room for scale-driven mergers.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East Vertical Farming Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Favorable Food-security Mandates by Governments | +3.2% | UAE, Saudi Arabia, Qatar core with spillover to Kuwait, and Oman | Medium term (2-4 years) |

| Water-saving Potential | +2.8% | Global across all Middle East markets | Long term (≥ 4 years) |

| Rapid Retail Adoption of Locally Branded “Zero-mile” Produce | +2.1% | UAE, Saudi Arabia with early gains in Dubai, Riyadh, and Jeddah | Short term (≤ 2 years) |

| Integration of IoT-driven Climate Control Platforms | +1.9% | UAE, Saudi Arabia, and Qatar with technology transfer to other markets | Medium term (2-4 years) |

| Expansion of Public–private Mega Farm Projects | +2.4% | Saudi Arabia, UAE core with expansion to Egypt, and Jordan | Long term (≥ 4 years) |

| Modular Farm-as-a-service Models for Hotels and Campuses | +1.7% | UAE, Qatar, and Bahrain with hospitality sector concentration | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Favorable Food-security Mandates by Governments

Middle Eastern governments are integrating vertical farming into national food strategies to reduce import dependence and protect food systems from geopolitical disruptions. The United Arab Emirates' food security plan includes specific targets for controlled-environment agriculture, while Saudi Arabia's development vision allocates public investment to indoor farming projects. Egypt's agricultural plan incorporates vertical farms to address land loss in the Nile Delta. These policies simplify licensing and customs procedures for farm inputs while providing concessional financing through agricultural banks. Regional climate initiatives have increased funding for sustainable farming systems. Regulatory authorities now provide expedited certification for nutrient solutions meeting sustainability standards.

Water-saving Potential

Water scarcity in the Gulf region has positioned vertical farming as a practical solution for sustainable agriculture. These systems utilize recirculating hydroponics and closed-loop nutrient systems to reduce water consumption and eliminate runoff, meeting environmental regulations. With traditional methods like cloud seeding showing limited effectiveness, policymakers are prioritizing hydroponic technologies for consistent water conservation. New developments, such as renewable energy-powered root-zone cooling systems, are being tested to decrease water usage in high-value crops. These methods demonstrate both resource efficiency and commercial feasibility in arid environments.

Rapid Retail Adoption of Locally Branded “Zero-mile” Produce

Middle Eastern retailers are incorporating vertical farming to provide fresh, traceable produce that appeals to consumers. Supermarkets include harvest time information on products, increasing transparency and enabling premium pricing while maintaining sales. Airline catering operations use pesticide-free greens, introducing travelers to local produce options. Hotel groups are implementing modular farming systems to ensure a consistent supply and quick delivery. Market research shows consumers prefer locally grown vertical farm produce, influenced by environmental considerations and product freshness. This retail adoption is establishing vertical farming as an essential component of urban food supply chains.

Expansion of Public–private Mega Farm Projects

Major vertical farming facilities are developing as key projects supporting national food production objectives. The Saudi Ministry of Environment, Water, and Agriculture has implemented a vertical farming program in Riyadh to support sustainable agriculture goals.[1]Ministry of Environment, Water and Agriculture, “Urban Vertical Farm Project Launched in Riyadh,” MEWA, SPA.GOV.SA These operations combine waste recycling, modern cultivation methods, and educational programs to develop regional expertise. Saudi Arabia's Public Investment Fund works with international agricultural technology companies to establish indoor farms across various regions, with government support through land allocation and energy subsidies. NEOM's technology center provides testing facilities for new companies to evaluate technologies in desert environments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex per Meter Square Relative to Greenhouse Alternatives | -2.1% | Across all Middle East markets | Medium term (2-4 years) |

| Scarce Regional Skill for Controlled-environment Agronomy | -1.8% | Saudi Arabia, Egypt, Jordan with limited impact in UAE, and Qatar | Long term (≥ 4 years) |

| Import Dependence on Nutrient Solutions and Substrates | -1.4% | Across all Middle East markets with particular impact on smaller markets | Short term (≤ 2 years) |

| Fragmented Cold-chain Logistics for Micro-greens | -1.2% | UAE, and Saudi Arabia core markets with distribution challenges | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarce Regional Skill for Controlled-environment Agronomy

The Middle East faces a significant talent shortage in controlled-environment agriculture, despite recent capacity-building efforts.[2]ICARDA, “Water for Dryland Peace,” icarda.org Academic institutions lack specialized curricula, forcing operators to rely on foreign consultants for managing advanced systems. This dependence increases operational costs and impedes long-term sustainability. Training effectiveness suffers due to language barriers, while immigration policies restrict skilled growers from long-term residency and contribution. Vertical farming ventures struggle to scale efficiently without a robust local talent pipeline. The region requires coordinated investments in education, vocational training, and policy reform to develop local expertise in agricultural innovation.

Fragmented Cold-chain Logistics for Micro-greens

The regional logistics systems lack optimization for delicate produce like micro-greens, which require specific delivery conditions to maintain freshness. Third-party networks primarily serve bulk commodities, leading to temperature variations that reduce shelf life. Farms must operate their own refrigerated vehicles, increasing last-mile delivery costs and limiting growth potential. Cross-border trade faces restrictions due to inconsistent food-safety documentation requirements among neighboring countries, reducing market access.[3]UAE Legislations, “Federal Law Concerning the Food Safety,” uaelegislation.gov.ae The development of the vertical farming market requires standardization of regulations and improvements in cold-chain infrastructure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Growth Mechanism: Hydroponics Leads Despite Aeroponic Innovation

Hydroponics accounted for 59.84% of the Middle East vertical farming market share in 2025, driven by its operational predictability and established nutrient solutions. The method benefits from developed supply chains and widespread technical expertise, particularly in Saudi Arabia and the United Arab Emirates. The segment attracts investment due to shorter payback periods and reliable yields. The scalability of hydroponic systems appeals to commercial and institutional stakeholders focused on food security.

The aeroponic segment is projected to grow at a 15.55% CAGR through 2031. Its misting technique improves oxygen absorption, resulting in faster plant growth and higher yields. The method uses approximately 10% less water than hydroponics, addressing regional water scarcity concerns. Research institutions and restaurants are testing aeroponic systems with desert-adapted crops. Aquaponics remains a small segment but is growing among premium market consumers due to its circular system benefits.

By Structure: Building-based Dominance Faces Container Disruption

Building-based vertical farms facilities represented 69.25% of the Middle East vertical farming market size in 2025, reflecting the advantages of large-scale operations. These facilities incorporate nutrient mixing systems, automation, and renewable energy infrastructure, enabling consistent production costs and efficient operations. The facilities support centralized distribution and food safety compliance, making them suitable for supermarket chains and institutional customers. The prevalence of building-based farms indicates market confidence in permanent infrastructure investments.

Shipping-container vertical farms are growing at a 12.76% CAGR, providing flexibility in deployment. Their modular design reduces regulatory requirements and enables quick installation in urban areas. Hotels and specialty retailers are installing container units for direct cultivation, reducing transport costs. These systems include remote monitoring capabilities and data analytics features, attracting technology-focused operators. The mobility of container farms provides operational flexibility in regions with uncertain property markets and infrastructure limitations.

By Crop Type: Vegetables Lead While Herbs Show Premium Growth

Fruits and Vegetables generated 47.35% of revenue in 2025, establishing their position as the primary vertical farming crop category. Lettuce, kale, and arugula are preferred for their quick-growing cycles, allowing multiple harvests per year. This production pattern ensures a consistent supply to retail and food service customers, building market stability. The segment provides operators with predictable income streams and efficient production processes.

Herbs and micro-greens are experiencing growth due to higher price points and culinary demand. These products are popular among restaurants and luxury hospitality venues for their intense flavors and freshness guarantees. The segment's 11.62% CAGR through 2031 reflects increasing demand for local, traceable produce that meets sustainability requirements. Flower and ornamental cultivation provides seasonal revenue opportunities, particularly during cultural events, while adherence to traceability standards enables regional export opportunities.

Geography Analysis

Saudi Arabia accounts for 40.42% of the Middle East vertical farming market size in 2025, supported by comprehensive government policies. The development of vertical farms in Riyadh and Jeddah benefits from government subsidies on land and utilities, facilitating rapid expansion. The partnerships between government-affiliated food companies and private operators ensure financial stability and guaranteed demand. The regulatory framework, including resource-efficiency certifications and agricultural incentives, strengthens investor confidence and promotes foreign technology adoption in the country's agritech sector.

The United Arab Emirates demonstrates the highest growth rate at 13.23% CAGR through 2031, driven by innovation policies and startup development. Government programs facilitate integration between farms, technology providers, and logistics centers. Efficient licensing and import procedures minimize operational barriers, while dedicated funding initiatives address early-stage financing needs. The United Arab Emirates' focus on sustainability and circular economy principles, including food waste composting, establishes it as a regional pioneer in agricultural technology and urban farming.

Other Middle Eastern countries display varying degrees of market development. Egypt integrates vertical farming into its land-reclamation strategy to decrease dependence on food imports. Qatar implements smart-farm systems combining data analytics with efficient climate control. Bahrain and Oman work to overcome logistics challenges by using free-trade zones to access South Asian and East African markets. The expansion of expertise and infrastructure in Gulf Cooperation Council centers is anticipated to accelerate regional adoption through knowledge transfer and collaborative initiatives.

Competitive Landscape

Pure Harvest Smart Farms Ltd., Bustanica (Emirates Crop One LLC), AeroFarms, Madar Farms, and VeggiTech Hydroponic Technologies Private Limited (SNASCO Holding Company) collectively held 45.9% market revenue in 2024. The Middle East vertical farming market maintains moderate concentration, with Pure Harvest Smart Farms and Bustanica as primary market leaders. Pure Harvest's adoption of a farm-as-a-service model has expanded its market presence and established recurring revenue streams, reducing its reliance on infrastructure projects. Bustanica utilizes its parent company's logistics network for broad retail distribution, demonstrating the benefits of integrated supply chains.

AeroFarms AgX in Abu Dhabi functions as a regional research and development center, performing cultivar trials to enhance commercial farm operations. iFarm's strategic move to the United Arab Emirates highlights the region's strong intellectual property protection and favorable funding environment. Crysp Farms has developed a specialized market position in hospitality through container farms combined with chef training programs, improving customer retention and product freshness.

Small-scale operators encounter difficulties with expansion and increasing operational expenses. This has resulted in increased merger and acquisition activity, while investors prefer revenue-linked financing structures. Companies distinguish themselves through energy-efficient systems, automated harvesting technologies, and climate-adapted seed varieties. Blockchain-based traceability systems are increasing in adoption, providing product recall capabilities and supporting premium positioning for health-conscious consumers.

Middle East Vertical Farming Industry Leaders

Pure Harvest Smart Farms Ltd.

Bustanica (Emirates Crop One LLC)

AeroFarms

Madar Farms

VeggiTech Hydroponic Technologies Private Limited (SNASCO Holding Company)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2024: The Ministry of Environment, Water, and Agriculture in Saudi Arabia launched a vertical farming project in Riyadh to enhance domestic food production and sustainability. This development aligns with Vision 2030 objectives by implementing advanced agricultural technologies that optimize water usage and crop yields in urban settings.

- February 2024: Masdar City partnered with Alesca Technologies to establish its first indoor vertical smart farm in Abu Dhabi, utilizing repurposed shipping containers near Eco-Plaza. The facility employs AI-driven automation to cultivate leafy greens throughout the year, reducing water consumption by 90-95% compared to traditional farming methods.

- December 2023: Pure Harvest Smart Farms Ltd. acquired RedSea, a Saudi Arabian player that deals with climate-smart technology solutions. According to the acquisition terms, Pure Harvest took over RedSea’s existing six-hectare controlled-environment agriculture (CEA) production facility near Riyadh, Saudi Arabia. Through this acquisition, the company aimed to increase its production of fresh produce in the Saudi Arabian market.

Middle East Vertical Farming Market Report Scope

Vertical farming, an innovative agricultural approach, cultivates crops in vertically stacked layers. This method employs soil-less techniques like aquaponics, hydroponics, and aeroponics, all within a meticulously controlled environment.

The Middle East vertical farming market is segmented by growth mechanism (aeroponics, hydroponics, and aquaponics), structure (building-based vertical farms and shipping container vertical farms), crop type (fruits and vegetables, herbs and micro-greens, flowers and ornamentals, and other crop types), and geography (Saudi Arabia, United Arab Emirates, Egypt, and Rest of Middle East).

The report offers market sizing and forecasts in value (USD) for all the above segments.

By Growth Mechanism

| Aeroponics |

| Hydroponics |

| Aquaponics |

By Structure

| Building-based Vertical Farms |

| Shipping-Container Vertical Farms |

By Crop Type

| Fruits and Vegetables |

| Herbs and Micro-greens |

| Flowers and Ornamentals |

By Geography

| Saudi Arabia |

| United Arab Emirates |

| Egypt |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| Jordan |

| Rest of Middle East |

| By Growth Mechanism | Aeroponics |

| Hydroponics | |

| Aquaponics | |

| By Structure | Building-based Vertical Farms |

| Shipping-Container Vertical Farms | |

| By Crop Type | Fruits and Vegetables |

| Herbs and Micro-greens | |

| Flowers and Ornamentals | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Egypt | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain | |

| Jordan | |

| Rest of Middle East |

Key Questions Answered in the Report

What is the current value of the Middle East vertical farming market?

The market stands at USD 484.66 million in 2026 and is projected to reach USD 981.65 million in 2031.

Which cultivation method holds the largest share?

Hydroponics leads with 59.84% share in 2025, given its operational reliability and mature supply chains.

Which country is the fastest grower?

The United Arab Emirates records the highest CAGR at 13.23% through 2031, propelled by innovation policies and startup development.

How much water can vertical farms save compared with open-field farming?

Modern vertical farms in the region report 90-95% water savings by using closed-loop hydroponic and aeroponic systems.

Page last updated on: