Europe Agricultural Drones Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

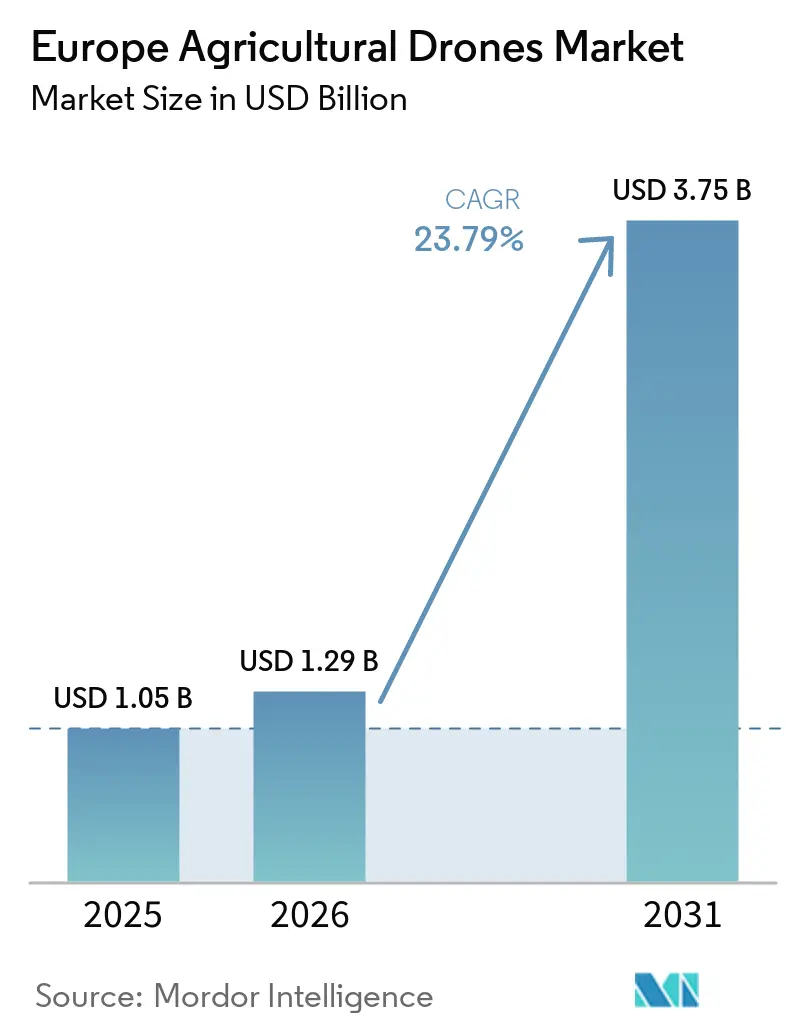

| Base Year Market Size (2025) | USD 1.05 Billion |

| Market Size (2026) | USD 1.29 Billion |

| Market Size (2031) | USD 3.75 Billion |

| Growth Rate (2026 - 2031) | 23.79% CAGR |

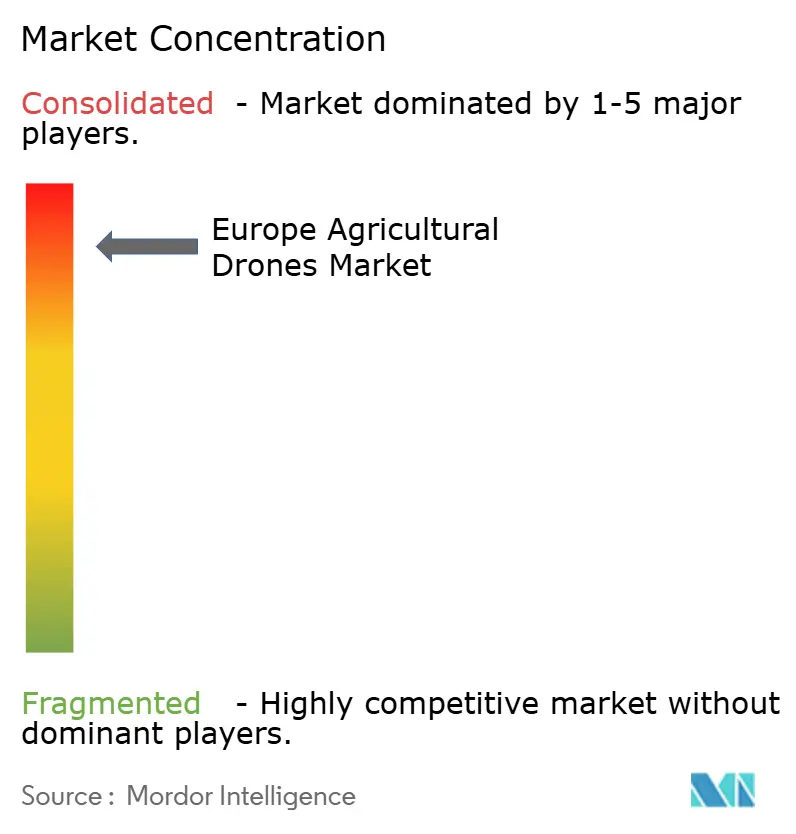

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Agricultural Drones Market Analysis by Mordor Intelligence

The Europe agricultural drones market size is projected to grow from USD 1.05 billion in 2025 and USD 1.29 billion in 2026 to USD 3.75 billion by 2031, registering a CAGR of 23.79% between 2026 and 2031. The Europe agricultural drones market is being reshaped by synchronized policy reforms, falling hardware prices, and an acute shortage of seasonal labor across the continent. The December 2025 Food and Feed Safety Omnibus proposal to exempt low-drift unmanned systems from the blanket aerial-spraying ban signals a regulatory pivot that favors the market. Hardware advances, especially multispectral sensors bundled with cloud analytics, shorten feedback loops between scouting flights and agronomic action, while venture capital keeps service pricing competitive. Persistent rural labor deficits, particularly in Germany, France, and Spain, further strengthen the case for autonomous spraying and variable-rate application.

Key Report Takeaways

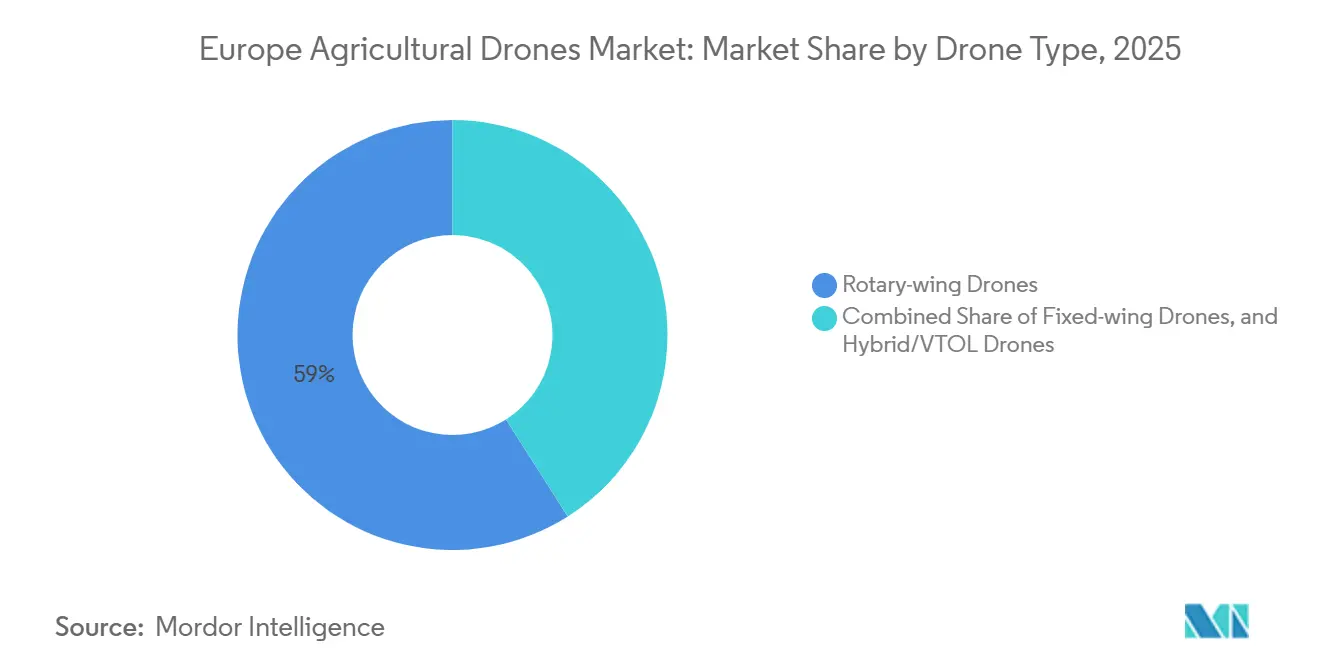

- By drone type, rotary-wing drones are projected to account for 59% of the Europe agricultural drones market share in 2025. Hybrid/VTOL drones are anticipated to be the fastest-growing category, with a compound annual growth rate (CAGR) of 29.0% from 2026 to 2031.

- By component, hardware is anticipated to be the largest segment, accounting for 48% of the Europe agricultural drones market in 2025. Meanwhile, services are forecast to be the fastest-growing segment, with a CAGR of 31.0% from 2026 to 2031.

- By application, crop spraying is projected to remain the largest segment, contributing 36% of the market size in 2025. Variable-rate application is projected to grow the fastest, with a CAGR of 32.5% from 2026 to 2031.

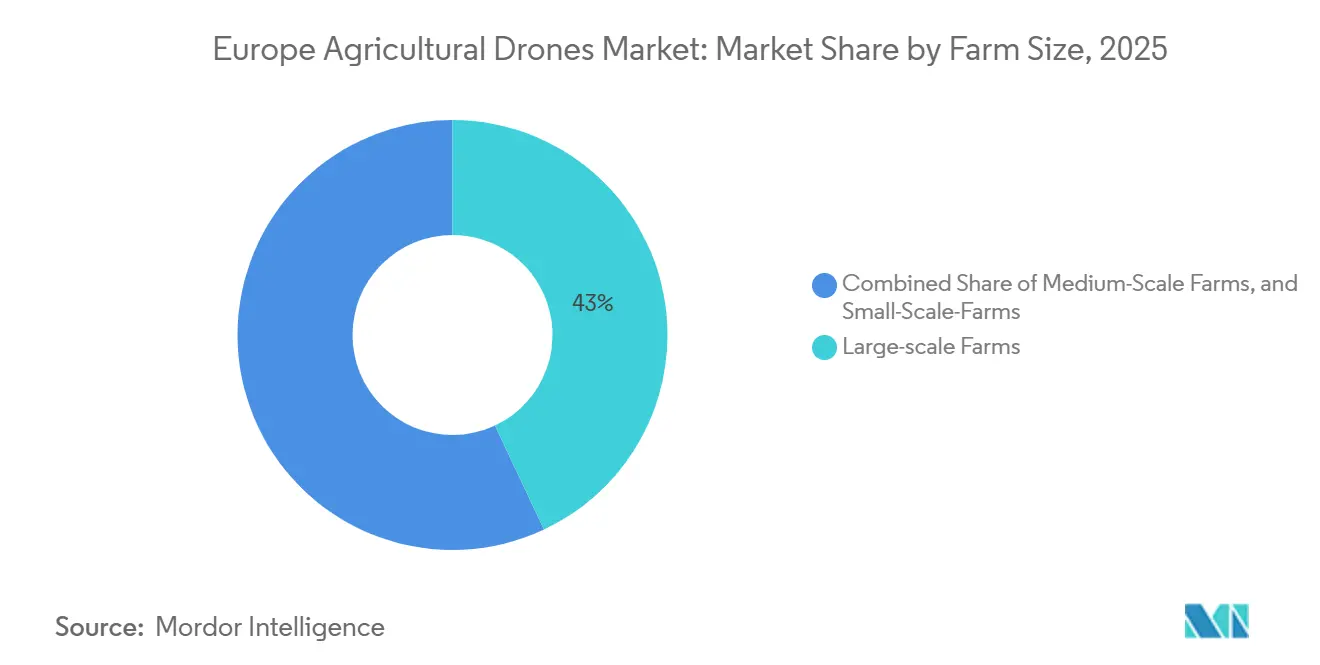

- By farm size, large-scale farms are estimated to dominate the market, capturing 43% share of the market in 2025. Small-scale farms are predicted to be the fastest-growing segment, with a CAGR of 28.0% from 2026 to 2031.

- By country, France is projected to hold the largest share, accounting for 24% of the Europe agricultural drones market size in 2025. Spain is projected to be the fastest-growing market, with a CAGR of 27.0% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Agricultural Drones Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Subsidy programs under the European Union Common Agricultural Policy | +4.2% | European Union-wide, strongest in France, Spain, and Italy | Medium term (2-4 years) |

| Growing labor shortages accelerating farm automation | +5.1% | European Union-wide, acute in Germany, France, Spain, Italy, and the United Kingdom | Short term (≤ 2 years) |

| Availability of low-cost rotary-wing platforms | +3.8% | European Union-wide, the highest uptake in Eastern Europe, Spain, and Italy | Short term (≤ 2 years) |

| Integration of multispectral imaging and AI analytics | +4.5% | European Union-wide, early adoption in the Netherlands, Germany, and France | Medium term (2-4 years) |

| Carbon-credit-linked eco-drone service models | +2.9% | European Union-wide, concentrated in France, Germany, and Denmark | Long term (≥ 4 years) |

| Vineyard-specific pest scouting requirements | +2.7% | France, Spain, Italy, and Germany | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Subsidy Programs Under the European Union Common Agricultural Policy

Eco-schemes introduced for 2023-2027 reimburse up to 25% of precision agriculture hardware, lowering capital barriers for cooperatives and small farms[1]Source: European Commission, “Common Agricultural Policy 2023-27,” EUROPA.EU. In 2025, the French Parliament adopted a bill focused on "improving the treatment of diseases affecting plant crops using remotely piloted aircraft," enabling the use of drones to spray specific pesticides on certain crops. Similarly, in 2025, the Italian Senate approved an amendment to the "Simplifications" Bill (DDL) that allows the use of drones in agriculture under a regulated trial framework. This development, emphasized by Coldiretti as a result of collaborative efforts with Parliament and the Government, aligns with Italy's strategy to promote innovation and sustainability in agriculture.

Growing Labor Shortages Accelerating Farm Automation

Labor shortages are a significant growth driver for the European agricultural drones market, as the declining availability of farm workers is encouraging farmers to automate tasks such as spraying, scouting, and crop monitoring using drones. This trend is particularly pronounced in countries experiencing seasonal labor shortages and increasing labor costs, where drones enable farms to sustain productivity with reduced reliance on manual labor. By 2025, Europe’s agricultural sector continues to face acute labor shortages, marked by an aging workforce and limited interest among younger generations, resulting in a net loss of 3.5 million workers between 2009 and 2024. To address this challenge, the European Union has achieved a 9.2% increase in agricultural labor productivity in 2025 through automation and structural reforms, although dependence on non-EU, seasonal, and migrant labor remains insufficient to fully bridge the gap. For instance, Dutch tulip growers have utilized DJI Agras T50 units for overnight slug control, effectively replacing unavailable manual scouts.

Availability of Low-Cost Rotary-Wing Platforms

The availability of low-cost rotary-wing platforms is driving the growth of the Europe agricultural drone market. These multirotor systems are affordable, maneuverable, and well-suited to the fragmented and irregular field patterns prevalent across Europe. Their ability to hover enables precise spot spraying and low-altitude crop imaging, making them a practical choice for farms aiming to adopt precision agriculture without incurring the higher costs associated with larger aircraft. In 2026, DJI introduced a new lineup of entry-level drones, including the Lito X1 and Lito 1, designed for high-altitude aerial photography applications, including agriculture. These drones offer high performance at an affordable price, enabling new users to explore aerial imaging for various purposes.

Integration of Multispectral Imaging and AI Analytics

An example of precision crop scouting involves the use of drones equipped with multispectral cameras on wheat or vineyard farms. These drones capture Normalized Difference Vegetation Index (NDVI) or red-edge imagery, and AI software identifies stress or disease hotspots for targeted treatment. This approach enables farmers to apply treatments only to the affected areas rather than the entire field, reducing input usage and improving response times. For instance, the MicaSense Altum-PT combines thermal and multispectral data in a single flight, providing comprehensive insights into crop health. Additionally, Pix4D’s cloud photogrammetry processes imagery into centimeter-accurate orthomosaics within minutes, facilitating precise analysis and decision-making.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented airspace regulations across member states | -3.6% | European Union-wide, most acute in cross-border operations | Medium term (2-4 years) |

| High upfront hardware and software costs | -2.8% | European Union-wide, disproportionate impact on small farms | Short term (≤ 2 years) |

| Limited rural 5G coverage for real-time analytics | -2.1% | Eastern Europe, rural France, Spain, Italy | Medium term (2-4 years) |

| Public concerns over chemical drift from drone spraying | -1.9% | Germany, Austria, organic wine regions in France, Italy | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Hardware and Software Costs

High upfront hardware and software costs pose a restraint on the Europe agricultural drone market. Advanced drones often require costly components such as sensors, spraying systems, flight software, and data analytics tools, which many small and medium-sized farms find difficult to justify. These expenses can lengthen the payback period, particularly when additional costs for training, maintenance, and integration with existing farm systems are factored in. For example, professional-grade drone systems, such as the senseFly eBee X with a Sequoia+ sensor and Pix4D license, cost approximately EUR 25,000 (USD 26,500). Similarly, the DJI nuWay DJI T50 Complete Generator Kit is priced at around USD 23,999[2]Source: DJI, “Agras Agricultural Drone Series,” DJI.COM. Leasing and per-flight models are emerging, but price wars in French viticulture have already pushed hectare fees near breakeven.

Limited Rural 5G Coverage for Real-Time Analytics

Limited rural 5G coverage poses a challenge to the Europe agricultural drone market, as real-time analytics rely on fast and reliable data transfer between drones and cloud or edge platforms. In regions with weak network coverage, farmers may face delays in streaming multispectral video, AI processing, and live decision-making, diminishing the effectiveness of advanced drone services for precision spraying and crop monitoring. A 2024 study by the Institute of Electrical and Electronics Engineers (IEEE) highlighted the issue of inconsistent rural 5G coverage, which restricts beyond-visual-line-of-sight (BVLOS) telemetry. Parrot’s ANAFI Ai addresses this limitation with onboard AI and a 4G fallback system. Similarly, WingtraRAY stores data locally for post-flight uploads, delayed analytics reduce the utility of real-time decision-making capabilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drone Type: Hybrid Platforms Gain Altitude

Rotary-wing drones led with 59% of Europe agricultural drones market share in 2025, owing to vertical take-off simplifying spraying in narrow vineyards and orchards. Fixed-wing units remain essential for 90-minute endurance over 200-ha wheat lots. Spain’s PDRA-S01 favors long-endurance fixed wings for olive estates, while line-of-sight limits in Burgundy make rotary craft the default.

Hybrid/VTOL drones are the fastest-growing, projected to expand at a 29.0% CAGR through 2026 to 2031, combining fixed-wing range with vertical takeoff and landing. Growers now seek fleet consolidation to minimize pilot training and spares inventory. Payload modularity, exemplified by MicaSense Altum-PT clip-on sensors, enables a single airframe to map at dawn and spray at dusk, boosting utilization. The Europe agricultural drones market share shift toward hybrid designs underscores a demand for operational flexibility rather than platform purity.

By Component: Services Layer Captures Margin

Hardware was the largest segment, commanding 48% of the Europe agricultural drones market size in 2025. This dominance is attributed to the rising demand for drone platforms, multispectral cameras, GPS modules, sensors, and spraying systems that facilitate precision agriculture practices. For instance, farmers in countries such as Germany and France are increasingly adopting advanced drones for applications like crop health monitoring, irrigation management, and pesticide spraying to enhance productivity and lower operational costs.

Services are the fastest-growing segment, with a 31.0% CAGR through 2026 to 2031, as farms outsource flying, data, and compliance. This growth is driven by farms increasingly outsourcing drone operations, including aerial surveying, data analytics, pilot training, maintenance, and regulatory compliance. For instance, many medium-sized farms are opting to hire specialized drone service providers for seasonal crop assessments and AI-based field reports, enabling them to reduce upfront investments and gain access to technical expertise more effectively.

By Application: Variable-Rate Prescriptions Overtake Blanket Treatments

Crop spraying was the largest segment, accounting for 36% of the Europe Agricultural Drones Market share in 2025. Regulatory stringency confines spraying to slopes and nurseries in France, whereas mapping faces no such barriers, allowing quick wins in arable cereal belts. The adoption of spraying drones is primarily driven by the growing demand for precision agriculture, reduced chemical wastage, and enhanced operational efficiency on farms across Europe. Agricultural drones enable farmers to apply fertilizers, pesticides, and herbicides with greater accuracy and speed than traditional methods, while reducing labor costs and environmental impact.

Variable-rate application is the fastest-growing, advancing at a 32.5% CAGR from 2026 to 2031, as multispectral analytics guide intra-field input modulation. The GO_PhytoDron project proved 20-30% fungicide savings in Rioja vineyards without yield loss. Variable-rate adoption reflects the maturation of precision farming from reactive blanket treatments to predictive, event-driven interventions, a transition that the Europe agricultural drones market is well placed to enable.

By Farm Size: Cooperatives Bridge the Small-Scale Gap

Large-scale farms were the largest, captured 43% of Europe agricultural drones market size in 2025. This dominance is attributed to their greater financial capacity, larger cultivation areas, and greater adoption of precision agriculture technologies to enhance productivity and operational efficiency. Large-scale farms extensively use drones for applications such as crop monitoring, spraying, mapping, and livestock management, reducing labor dependency and optimizing resource use. Commercial grain farms in France and extensive agricultural estates in Germany are increasingly employing drone fleets to monitor crop health and automate spraying operations across vast farmland.

Small-scale farms are projected to be the fastest-growing segment, registering a CAGR of 28.0% during 2026-2031, as eco-scheme reimbursements and per-flight service models lower barriers. This growth is driven by declining drone costs, the emergence of drone-as-a-service providers, and growing awareness of precision farming's benefits among smaller agricultural businesses. Small fruit and vegetable growers in Spain are adopting cost-effective drone services for targeted pesticide application and irrigation monitoring, enabling them to enhance yields without significant upfront technology investments.

Geography Analysis

France held the largest share, accounting for 24% of the Europe Agricultural Drones Market share in 2025, owing to slope exemptions and 2025 emergency mildew authorizations. This leadership is attributed to its well-established precision farming ecosystem, extensive vineyard cultivation, and growing government support for smart agriculture technologies in 2025, the French Parliament approved legislation allowing drone-based spraying of low-risk pesticides and biocontrol products on steep vineyards and banana plantations. This measure enhanced efficiency and worker safety in challenging terrains.

Spain is projected to record the fastest growth, at a 27.0% CAGR through 2026-2031. The country is experiencing rapid adoption of agricultural drones driven by increased investments in smart farming, water-efficient agriculture, and favorable drone regulations. In 2025, Spain surpassed 119,000 registered drone operators, highlighting the professionalization of its drone ecosystem and the expansion of agricultural applications[3]Source: Agencia Estatal de Seguridad Aérea, “Spain Exceeds 119,000 Drone Operators Registered with the Spanish Aviation Safety Agency (AESA),” seguridadaerea.gob.es. These advancements are encouraging Spanish farmers to adopt drones for crop monitoring, precision spraying, irrigation optimization, and soil health management.

The Netherlands is becoming a significant market for agricultural and commercial drones, supported by its emphasis on precision farming, smart agriculture, and drone-enabled digital infrastructure. Farmers in the Netherlands are increasingly utilizing drones for applications such as crop monitoring, greenhouse management, and precision spraying to enhance productivity and sustainability. The country has launched various initiatives to promote drone innovation and establish regulatory frameworks. Germany remains one of Europe’s most advanced drone markets, driven by robust industrial capabilities, the adoption of smart farming practices, and government-supported drone innovation programs.

Competitive Landscape

The Europe agricultural drones market remains highly concentrated among leading manufacturers, although emerging service providers and startups are gradually increasing fragmentation within niche application areas. The top five players, including SZ DJI Technology Co., Ltd., Parrot Drones SAS, senseFly SA (AgEagle Aerial Systems Inc.), Delair SAS, and Guangzhou XAircraft Technology Co., Ltd., hold significant market share in 2025. The market is also witnessing increased activity from smaller players and startups, which are leveraging innovative technologies and targeting underserved areas to gain a foothold.

Technological advancements are primarily centered on sensor fusion, where platforms capable of integrating multispectral, thermal, and LiDAR data within a single flight command command higher pricing. Additionally, advancements in autonomy, such as beyond-visual-line-of-sight capabilities, allow service providers to cover larger areas with fewer pilots. The market is witnessing a shift from hardware-centric business models to service-oriented approaches, as profit margins increasingly move toward analytics and managed services. This transition benefits companies with agronomic expertise and strong regulatory compliance capabilities over those focused solely on hardware. The integration of advanced AI and machine learning algorithms is enhancing the precision and efficiency of data analysis, enabling more actionable insights for end-users.

Strategic collaborations among drone manufacturers, agritech firms, and research institutions are intensifying competition across the European market. Companies are increasingly partnering with software providers and precision agriculture platforms to offer integrated farm management solutions that combine aerial imaging, AI-driven analytics, and real-time crop monitoring. These partnerships are also fostering innovation in drone design and functionality, ensuring compatibility with evolving agricultural practices and regulatory frameworks.

Europe Agricultural Drones Industry Leaders

SZ DJI Technology Co., Ltd.

Parrot Drones SAS

senseFly SA (AgEagle Aerial Systems Inc.)

Delair SAS

Guangzhou XAircraft Technology Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Wingtra received the European Union Aviation Safety Agency (EASA) C6 certification for its WingtraRAY vertical take-off and landing mapping drone. This certification enables commercial operations across Europe Union Member States and positions the platform for large-scale surveying contracts in agriculture and infrastructure.

- December 2025: Agreenculture, a French agricultural robotics company, secured EUR 6 million (USD 6.4 million) in a Series A funding round. The funding aims to commercialize its AGC Autonomy Kit, which retrofits existing tractors and integrates drone scouting data for autonomous field operations.

- April 2024: DJI introduced the Agras T50 and Agras T25 drones in Europe. Building on the established Agras drone line, the T50 is designed for enhanced efficiency in larger-scale growing operations, while the lightweight T25 is tailored for portability in smaller fields. Both drones are compatible with the upgraded SmartFarm app, which provides advanced features for comprehensive aerial application management.

Europe Agricultural Drones Market Report Scope

An agricultural drone is an unmanned aerial vehicle utilized in farming for crop monitoring, field mapping, and tasks such as spraying, seeding, and fertilizing.

The Europe agricultural drones market report is segmented by drone type into fixed-wing drones, rotary-wing drones, and hybrid/VTOL drones; by component into hardware, software, and services; by application into crop spraying, field mapping and surveying, variable rate application, livestock monitoring, and others; by farm size into small-scale farms, medium-scale farms, and large-scale farms; and by geography into Germany, France, United Kingdom, Italy, Spain, Netherlands, and the Rest of Europe. The market forecasts are provided in terms of value in USD.

| Fixed-wing Drones |

| Rotary-wing Drones |

| Hybrid/VTOL Drones |

| Hardware |

| Software |

| Services |

| Crop Spraying |

| Field Mapping and Surveying |

| Variable Rate Application |

| Livestock Monitoring |

| Others |

| Small-scale Farms |

| Medium-scale Farms |

| Large-scale Farms |

| Germany |

| France |

| United Kingdom |

| Italy |

| Spain |

| Netherlands |

| Rest of Europe |

| By Drone Type | Fixed-wing Drones |

| Rotary-wing Drones | |

| Hybrid/VTOL Drones | |

| By Component | Hardware |

| Software | |

| Services | |

| By Application | Crop Spraying |

| Field Mapping and Surveying | |

| Variable Rate Application | |

| Livestock Monitoring | |

| Others | |

| By Farm Size | Small-scale Farms |

| Medium-scale Farms | |

| Large-scale Farms | |

| By Geography | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Netherlands | |

| Rest of Europe |

Key Questions Answered in the Report

What is the 2031 value forecast for the Europe agricultural drones market?

The Europe agricultural drones market size is projected to reach USD 3.75 billion by 2031.

How fast is the market growing after 2026?

The market is anticipated to post a 23.79% CAGR between 2026 to 2031.

Which drone type will expand the fastest?

Hybrid and VTOL platforms are forecast to grow at a 29.0% CAGR through 2026 to 2031 as farms seek fixed-wing range with rotary-wing agility.

Why are services outpacing hardware sales?

Regulatory complexity and data-analytics gaps are prompting farms to outsource flights and mapping, driving services to a 31.0% CAGR 2026 to 2031.

Page last updated on: