Chile Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.96 Billion |

| Market Size (2026) | USD 1.01 Billion |

| Market Size (2031) | USD 1.38 Billion |

| Growth Rate (2026 - 2031) | 6.44% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chile Containerboard Market Analysis by Mordor Intelligence

The Chile containerboard market size is projected to be USD 0.96 billion in 2025, USD 1.01 billion in 2026, and reach USD 1.38 billion by 2031, growing at a CAGR of 6.44% from 2026 to 2031. The Chile containerboard market is being supported by the country’s export-heavy economy, where fresh fruit and seafood shipments continue to require reliable corrugated packaging at scale. Domestic demand is also rising as e-commerce fulfillment networks expand beyond Santiago and pull more box volume into consumer delivery channels. Chile’s sustainability transition is reinforcing this demand because the EPR framework under Ley REP is pushing brand owners and converters toward fiber-based packaging with documented traceability. The competitive field is split between integrated domestic groups and internationally backed operators, while converting capacity remains concentrated in the central corridor and leaves parts of the south less well served. Input-cost volatility in recovered fiber and competition from flexible plastics still weigh on profitability, but demand tied to perishable exports remains structurally firm because those supply chains have limited packaging substitutes.

Key Report Takeaways

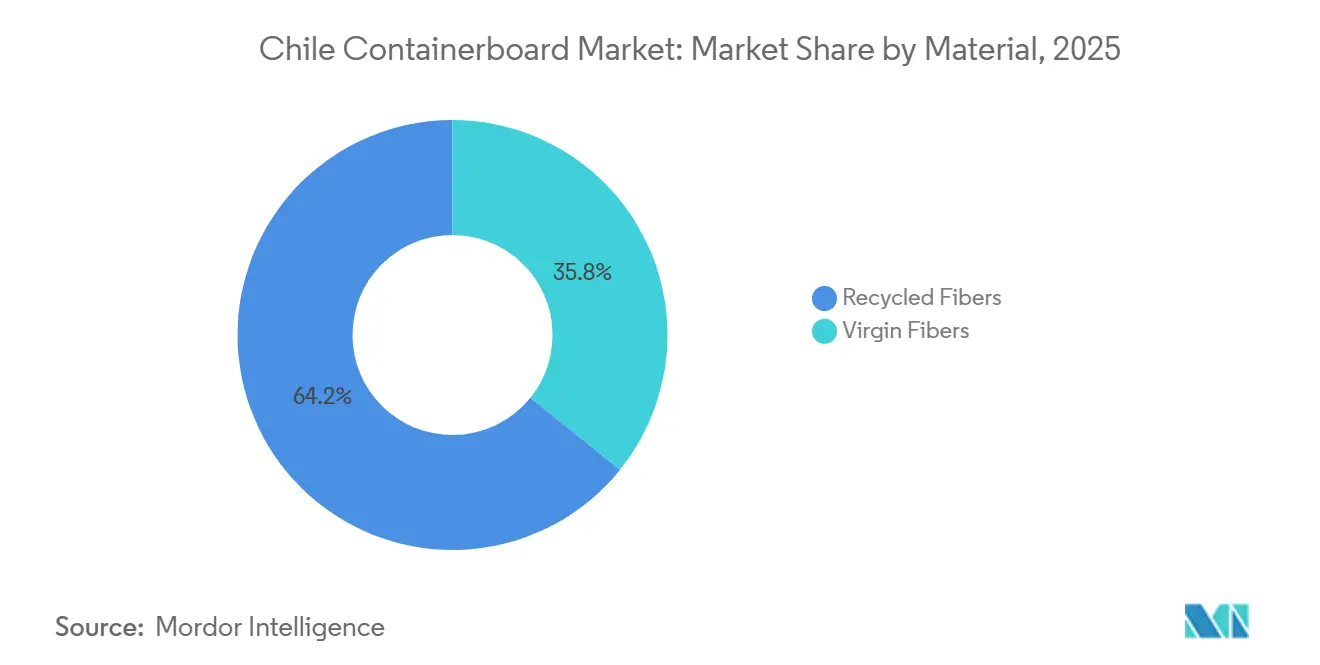

- By material, recycled fibers captured 64.21% of the Chile containerboard market share in 2025.

- By product type, the Chile containerboard market size for the kraftliners segment is forecast to advance at a 7.03% CAGR through 2031.

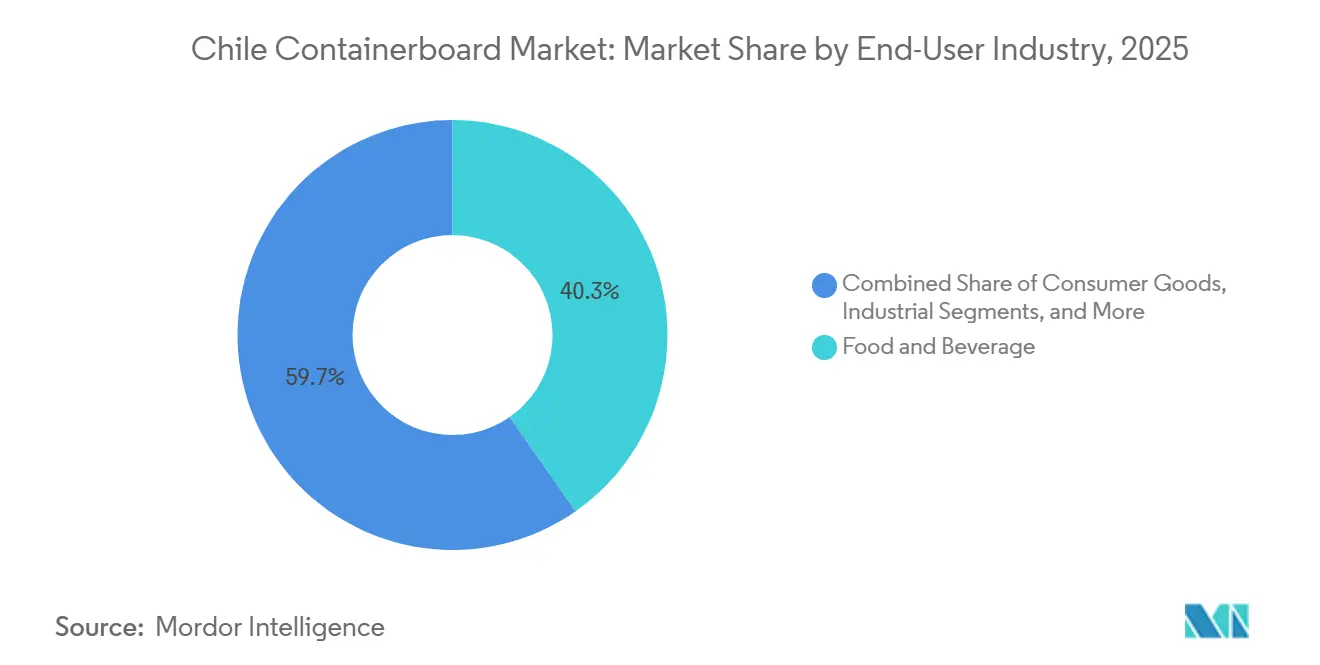

- By end-user industry, food and beverage captured 40.31% of the Chile containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Chile Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Export Demand From Fresh Fruit Shipments | +1.8% | National, core concentration in O'Higgins, Maule, Metropolitana, and Valparaíso | Short term (≤ 2 years) |

| E-Commerce Fulfillment Expansion | +1.5% | National, with early gains in Santiago, Valparaíso, Concepción | Short term (≤ 2 years) |

| EPR-Led Shift Toward Recyclable Fiber Packaging | +1.2% | National, with compliance gains across Metropolitana and Biobío | Medium term (2-4 years) |

| Export Packaging Demand From Salmon and Protein Supply Chains | +1.0% | South-central Chile, Los Lagos, Aysén, Biobío | Medium term (2-4 years) |

| Wax-Replacement Moisture-Resistant Board Innovation | +0.5% | National, with primary uptake in export-oriented converters in Metropolitana and O'Higgins | Long term (≥ 4 years) |

| Regional Fulfillment Decentralization Beyond Santiago | +0.4% | Biobío, Maule, La Araucanía | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Export Demand From Fresh Fruit Shipments

Fresh fruit exports remain the strongest demand driver for the Chile containerboard market, as seasonal produce continues to move in high volumes through corrugated formats. In the 2025-26 season, Chile exported the equivalent of 112 million boxes of cherries, totaling 561,130 tonnes, of which 87% went to China. Agroindustrial fruit and vegetable export value increased 33% in 2025 to USD 3,392 million, and volumes exceeded 1 million tonnes, with hazelnuts and frozen cherries among the strongest performers. China’s traceability requirements are pushing Chilean converters to install inline variable-data print capability, and that requirement is separating compliant, well-capitalized plants from smaller operators that cannot absorb the same investment. Exporters of blueberries and apples are also moving toward hybrid structures that combine recycled liners with starch-based moisture barriers, which is raising value per box without requiring a full shift to virgin fiber.

E-Commerce Fulfillment Expansion

The Chile containerboard market is also being lifted by online retail growth because fulfillment activity directly increases demand for shipping boxes, inserts, and transit-ready corrugated formats. Chile’s e-commerce sales reached USD 10 billion in 2025 and are expected to reach USD 10.6 billion in 2026, indicating that digital purchasing is still expanding within the local retail market.[1]Comité de Comercio Electrónico, “Comercio Electrónico En Chile Alcanzó USD 10 Mil Millones En 2025,” Cámara de Comercio de Santiago, ccs.cl Online sales represented 14% of total retail in Chile, and DHL Express Chile reported a 32% increase in e-commerce shipment volumes during the 2025 peak period compared with the same period in 2024. This pattern favors testliner and fluting consumption in regular-slotted containers and die-cut delivery formats, where unit volumes are high even when board specifications are less demanding than those for export produce packs. Cross-border orders from Chinese marketplaces are also creating a second layer of demand, as many inbound goods are repacked at Chilean fulfillment centers before final delivery to consumers.

EPR-Led Shift Toward Recyclable Fiber Packaging

Chile’s EPR framework has moved from policy design into practical enforcement, and that shift is changing supplier selection across the Chile containerboard market. SISREP became operational from January 2025, requiring monthly digital reporting for packaging producers under the Ley REP framework.[2]Centro de Envases y Embalajes de Chile, “El 1 De Enero De 2025 Entra En Vigencia El Sistema De Reporte De La Responsabilidad Extendida Del Productor (SISREP) En El Marco De La Ley REP,” CENEM, cenem.cl In January 2026, Resolution 2993 EXENTA formally established the environmental audit program for EPR management systems, confirming that the regulator has shifted toward active oversight.[3]Superintendencia del Medio Ambiente, “Resolución Núm. 2993 EXENTA - Fija Programa De Fiscalización Ambiental De Sistemas De Gestión Afectos A La Ley Nº 20.920 Para El Año 2026,” vLex Chile, vlex.cl Large integrated producers can absorb documentation, traceability, and reporting costs inside existing operating systems, while smaller converters face a heavier administrative burden and lose some sourcing relevance with brand owners. A September 2025 study found that more than 50% of Chile’s actual packaging recycling occurred outside the formal REP management system, suggesting that official valorization rates understate the existing recovery base and supporting future investment in auditable fiber loops.

Export Packaging Demand From Salmon and Protein Supply Chains

South-central protein exports provide another strong support line for the Chile containerboard market, as seafood flows require structural packaging that performs well in wet and cold logistics conditions. Chile’s salmon industry exported USD 6,549 million in 2025, up 3% from 2024, and remained the country’s second-largest export product after copper.[4]SalmonChile, “Salmón Chileno Se Consolida Como El Segundo Producto Más Exportado Del País Durante 2025,” SalmonChile, salmonchile.cl In Q1 2026, salmon and trout exports reached USD 1.991 billion, up 8% in value and 19% in volume year over year, while the United States received 70,735 tonnes valued at USD 706 million. Exporters serving maritime routes need corrugated board that can withstand compressive loads in ice-slurry environments during voyages lasting more than 20 days. CMPC Biopackaging presented hydro-repellent corrugated packaging as an EPS alternative at REP Forum 2024, and in 2025, it co-hosted an international design challenge with MITdesignX and Multi X that drew more than 80 designers to develop bio-based salmon packaging solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recovered Fiber Price Volatility | -0.9% | National | Short term (≤ 2 years) |

| Competition From Flexible Plastic Packaging | -0.7% | National, strongest in processed food and personal care | Medium term (2-4 years) |

| REP Traceability and Municipal Collection Gaps | -0.4% | National, with structural gaps outside Metropolitana region | Medium term (2-4 years) |

| Southern Chile Freight and Weather Bottlenecks | -0.2% | Aysén and Magallanes | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Recovered Fiber Price Volatility

Recovered fiber price swings remain the most immediate margin restraint in the Chile containerboard market, as domestic recycled grades closely track global OCC conditions. US OCC prices averaged USD 44 per short ton through most of 2025, declined 16% year over year in December 2025, and export bids to Southeast Asia rose to USD 127-130 per short ton FOB in January 2026. The regional packaging value chain entered 2026 under pressure, with containerboard production in South America up 2% in 2025 and operating rates at 82%, even as cost differences between integrated and non-integrated producers widened. Smaller Chilean converters that lack stable OCC sourcing agreements are more exposed to these swings than integrated groups that manage collection, papermaking, and conversion within a single system. That cost asymmetry is likely to keep new investment centered on larger operators with closed-loop fiber access and better compliance economics.

Competition From Flexible Plastic Packaging

Flexible plastic packaging still competes with containerboard in Chile because it retains cost, barrier, and weight advantages in categories such as snack foods, pet food, and personal care. This substitution risk is highest in domestic ambient-temperature categories, where shelf-ready or transit packaging can shift from corrugated trays to lighter flexible formats. The same pressure is much weaker in seafood exports because salmon transport requires structural performance that flexible solutions cannot provide in cold-chain logistics. The Ley REP framework and brand-owner sustainability programs are reducing this advantage by making recyclable, traceable fiber formats more attractive for compliance and public claims. Chilean converters are responding with fine-flute retail-ready formats that are starting to recover some shelf applications from flexible pouches, but the threat remains real in low-weight consumer packaging.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fibers Hold Scale While Virgin Fibers Lead The Growth Mix

Recycled fibers held 64.21% of the Chile containerboard market share in 2025, which confirms that the country’s collection network and recycled paper infrastructure remain the main scale base for box production. This leading position reflects the economics of EPR-compliant recycled testliner and fluting production in a market where domestic applications often reward affordability and traceability. E-commerce packaging, consumer goods shipments, and many industrial uses can tolerate slightly lower ring-crush performance when the tradeoff is lower cost and better alignment with recycling targets. That is why the Chile containerboard market continues to rely on recycled grades for most domestic volume, especially in applications where moisture exposure and stacking pressure are less severe.

Virgin fibers are projected to record the fastest CAGR at 6.89% through 2031, showing that export-led quality requirements are steadily increasing their role in the product mix. Their growth is tied to Kraftliner and virgin fluting demand in export packaging that must hold compression integrity at high humidity during long Pacific voyages. China’s traceability rules for fruit imports also favor smoother board surfaces that can handle inline variable-data printing with greater consistency, which gives virgin grades an operating advantage in some premium uses. Research published in Cellulose in 2025 showed that cationic starch and carnauba wax coating systems achieved Cobb60 values of 4.5 g/m² with a 12/12 Kit rating, which supports the case for bio-based moisture resistance across paperboard substrates and could narrow the performance gap over time.

By Product Type: Testliners Defend Volume While Kraftliners Gain On Export Performance

Testliners held 42.19% share of the Chile containerboard market size in 2025, which reflects their role as the standard facing material in e-commerce boxes and domestic food and beverage secondary packaging. Their scale comes from cost efficiency inside Chile’s recycled-fiber system and from their fit with high-volume box formats that do not require premium surface or strength properties. Integrated production models, especially those linked to recovered paper collection and local conversion, reinforce that cost advantage in routine domestic shipments. Fluting also remains essential across the product mix because it is used in nearly all corrugated structures, and semi-chemical fluting improvements are helping agricultural pallet loads hold better stacking strength in pack-house operations.

Kraftliners are projected to grow at a 7.03% CAGR through 2031, making them the fastest-rising product type in the Chile containerboard market. That momentum comes from fresh fruit and seafood exports, where moisture resistance and compression strength are non-negotiable. Chile and Norway accounted for 77% of global salmon production in 2025, and Chilean harvest volumes increased 14%, which directly supports demand for high-specification corrugated packaging in export channels. Chilean converters still depend on imported kraftliner from the United States, Brazil, and Finland, but Smurfit Westrock’s USD 150 million investment in its Três Barras mill in Brazil is expected to improve regional supply reliability for Chile-bound export packaging grades.

By End-User Industry: Food And Beverage Leads Demand While Consumer Goods Expands Faster

Food and beverage accounted for 40.31% share of the Chile containerboard market size in 2025, and that leadership is rooted in the country’s export-heavy agrifood base. Fresh cherries, table grapes, blueberries, salmon, and processed fruit and vegetable products all move through corrugated formats that require dependable box supply across seasonal peaks. Cherry exports alone reached the equivalent of 112 million boxes in the 2025-26 season, which shows how large one produce category can be for box demand in a single year. Industrial end users remain important as well, as mining and manufacturing supply chains use heavy-duty corrugated packaging, including triple-wall formats for equipment and spare parts transport.

Consumer goods are projected to expand at a 7.12% CAGR through 2031, making it the fastest-growing end-user segment in the Chile containerboard market. The segment is being supported by e-commerce growth, broader digital purchasing behavior, and the spread of fulfillment activity beyond the Santiago metropolitan area. Imported goods from Chinese marketplaces add another layer, as many arrive in non-retail-ready formats and are repacked locally for final delivery, creating incremental corrugated demand near fulfillment hubs. Healthcare, horticultural inputs, and other smaller end uses remain stable rather than transformative, but they still help widen the demand base beyond export agriculture and seafood.

Geography Analysis

The Chile containerboard market is national in scope, but real demand and converting activity are concentrated in the central corridor that includes Metropolitana, O'Higgins, and Valparaíso. This corridor houses the highest installed corrugating capacity and remains the primary operating base for both domestic fulfillment demand and export packing operations. Santiago’s industrial parks and fulfillment centers account for a large share of domestic box consumption because online retail still centers on the capital region. Valparaíso also remains critical for export-grade demand, and STI handled 14,690 cherry reefer containers in the 2025 season, up 17% year over year, reinforcing seasonal demand for structural corrugated packaging. The O'Higgins region remains strategically important because the former International Paper converting plant in Graneros now sits within the Corrupac-Coipsa platform, strengthening supply coverage for central valley agricultural and industrial users.

The Maule-to-Los Lagos corridor is the most dynamic submarket in Chile's containerboard market because it combines fruit exports, food processing, and aquaculture. Agroindustrial fruit and vegetable exports rose 33% in value in 2025, boosting packaging needs across this production belt. Los Lagos adds another layer because salmon exports remain one of the country’s largest export categories and require moisture-resistant box formats at scale. As of May 2026, 92% of centro-sur fresh fruit was still left through central-zone ports, but Biobío was building cross-docking and intermodal links to capture more of that flow and support new packaging demand nodes. AGUNSA’s new 21,300 m² logistics center in Talcahuano provided additional support for south-central corrugated supply chains and strengthened the case for regional stock points closer to exporters.

Southern Chile, especially Aysén and Magallanes, remains the most difficult operating zone in the Chile containerboard market because freight costs and weather disruptions reduce supply efficiency. Freight in these regions runs near USD 650 per kilometer, which is 40% above Santiago levels, and maritime links face winter delays that keep box users dependent on higher buffer stocks. The government’s Plan de Zonas Extremas includes USD 1.6 billion across 54 projects, but most road and port improvements are not expected to be operational before 2029, leaving the structural logistics gap in place through much of the forecast period. As a result, converters often ship flat blanks from Santiago and rely on on-site erection, which adds handling steps and weakens the economics of specialized board grades even when local demand is present.

Competitive Landscape

The Chile containerboard market shows moderate concentration, with 3 to 4 integrated groups controlling much of the converting and corrugating base, while a wide group of independents still competes on speed, customization, and local service. That independent group includes Celhex Packaging, San Jorge Packaging, WINPACK, P&J Packaging, HSBOX, CartónPro, Box Factory, COMYU, Solucar, Adelpack, La Fábrica de Cajas, and Distribuidora Comercial Saav SpA. The most important competitive move in the current period was Empresas Coipsa SpA’s acquisition, through Corrupac S.A., of International Paper Cartones Limitada’s Chilean assets, a deal notified to the FNE in January 2026. The transaction combined waste management, paper production, and corrugated conversion within a more tightly integrated domestic platform and strengthened coverage across Metropolitana, O'Higgins, and Los Lagos. That move raises scale advantages for larger players and makes it harder for smaller standalone converters to compete on both compliance and procurement.

CMPC remains the technology reference point in the Chile containerboard market through its Biopackaging division and its work on export-oriented salmon packaging. In 2026, CMPC directed USD 658 million in capital expenditures toward operational continuity, signaling a focus on stabilization and system efficiency rather than a near-term greenfield push. Smurfit Westrock also reinforced its regional position by opening an Experience Center for Argentina and Chile in April 2026, giving customers access to packaging design, analytics, and prototyping support for performance-led solutions. Its USD 150 million investment in the Três Barras mill in Brazil further supports kraftliner availability for Chilean converters that serve export-heavy customers.

White-space opportunities are strongest in e-commerce fine-flute applications because Chile still lacks narrow-flute corrugating lines at the scale needed for next-day delivery formats at a highly competitive unit cost. That gap leaves room for regional operators to invest before 2028 if online retail demand continues to spread into secondary cities. Compliance is also becoming a competitive moat, since converters with auditable SISREP documentation are increasingly preferred by brand owners that need defensible fiber traceability under Ley REP. That combination of scale, compliance capability, and regional service keeps the Chile containerboard market moderately concentrated while still leaving openings for specialized converters near agricultural and fulfillment clusters.

Chile Containerboard Industry Leaders

Empresas CMPC S.A.

Corrupac S.A.

Empresas Coipsa SpA

Compania Papelera del Pacífico

Smurfit Westrock plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: CMPC Reports 50% Decline in Q1 2026 Profits Amid Pulp Price Pressure. Empresas CMPC reported Q1 2026 earnings of USD 24.77 million, a 50.2% year-over-year decline, as lower pulp prices and higher energy costs, partly attributed to Middle East supply chain effects, weighed on the Celulosa and Biopackaging segments. CEO Francisco Ruiz-Tagle outlined competitiveness initiatives in a letter to investors, signaling restructuring measures within the packaging division.

- April 2026: Smurfit Westrock Opens Experience Center for Argentina and Chile. Smurfit Westrock inaugurated its Argentina and Chile Experience Center on April 17, 2026, creating a collaborative packaging design facility integrating digital tools, data analytics, and co-creation processes aimed at helping regional customers develop performance-optimized and EPR-compliant packaging solutions.

- March 2026: Chile Salmon Exports Jump 8% in Value in Q1 2026. Chile shipped 260,533 tonnes of salmon and trout valued at USD 1.991 billion in Q1 2026, a 19% volume and 8% value increase over Q1 2025, according to the National Customs Service and SalmonChile. The United States received 70,735 tonnes worth USD 706 million, directly driving demand for export-grade moisture-resistant corrugated packaging from Los Lagos and Biobío converting operations.

- January 2026: Coipsa and Corrupac Acquire International Paper's Chilean Corrugated Assets. Empresas Coipsa SpA, through its subsidiary Corrupac S.A., notified the FNE of its acquisition of International Paper Cartones Limitada from IP México Holdings LLC and Cartonajes Unión S.L. on January 21, 2026. The transaction consolidates Coipsa's corrugated converting network, including International Paper's high-resistance board plant in Graneros, O'Higgins Region, and marks International Paper's full exit from the Chilean market.

Chile Containerboard Market Report Scope

The Chile Containerboard Market encompasses the production, distribution, and consumption of containerboard materials used in manufacturing corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The market is driven by the increasing demand for sustainable, lightweight, and durable packaging solutions.

The Chile Containerboard Market Report is Segmented by Material (Virgin Fibers and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current size of the Chile containerboard market?

The Chile containerboard market was valued at USD 0.96 billion in 2025 and stands at USD 1.01 billion in 2026. It is projected to reach USD 1.38 billion by 2031 at a CAGR of 6.44%.

What is driving demand for containerboard in Chile?

Fresh fruit exports, salmon shipments, e-commerce box demand, and EPR-led packaging shifts are the main growth drivers. Export packaging needs remain especially important because they require structural corrugated board with moisture resistance.

Which material segment leads in Chile?

Recycled fibers led with a 64.21% share in 2025 because Chile has a well-established recovered paper system and strong compliance incentives for recyclable packaging.

Which product type is growing the fastest?

Kraftliners are projected to grow at a 7.03% CAGR through 2031. Their growth is tied to export produce and seafood packaging, where moisture resistance and compression strength matter more.

Which end-user segment is the largest?

Food and beverage led with a 40.31% share in 2025. Chile's export-heavy agrifood and seafood sectors keep this segment dominant in corrugated box consumption.

How is Ley REP affecting packaging suppliers in Chile?

Ley REP and SISREP reporting are pushing brand owners toward converters that can document traceability and fiber recovery. This is increasing the advantage of larger, integrated suppliers with stronger compliance systems.

Page last updated on: