Colombia Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.38 Billion |

| Market Size (2026) | USD 1.45 Billion |

| Market Size (2031) | USD 1.98 Billion |

| Growth Rate (2026 - 2031) | 6.43% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Colombia Containerboard Market Analysis by Mordor Intelligence

The Colombia containerboard market size is projected to be USD 1.38 billion in 2025, USD 1.45 billion in 2026, and reach USD 1.98 billion by 2031, growing at a CAGR of 6.43% from 2026 to 2031. Growth in the Colombia containerboard market reflects a durable shift in packaging demand rather than a short-lived rebound in one end-use category. E-commerce is pushing more consumer goods through smaller corrugated parcels, which is raising box throughput across urban logistics networks and tightening converter lead times. Plastic phaseout rules are redirecting secondary and delivery packaging toward fiber, while the recovery in food processing is restoring the steady shipment volumes that support mill and converter utilization. Domestic consumption has also been running ahead of local output, which keeps import dependence relevant and places greater value on producers that can manage fiber sourcing and energy use and deliver service well. Large integrated investments, food-safe certification, and the development of barrier-coated paper are widening the opportunity set in the Colombia containerboard market, even as OCC, pulp, freight, and power costs continue to pressure margins.

Key Report Takeaways

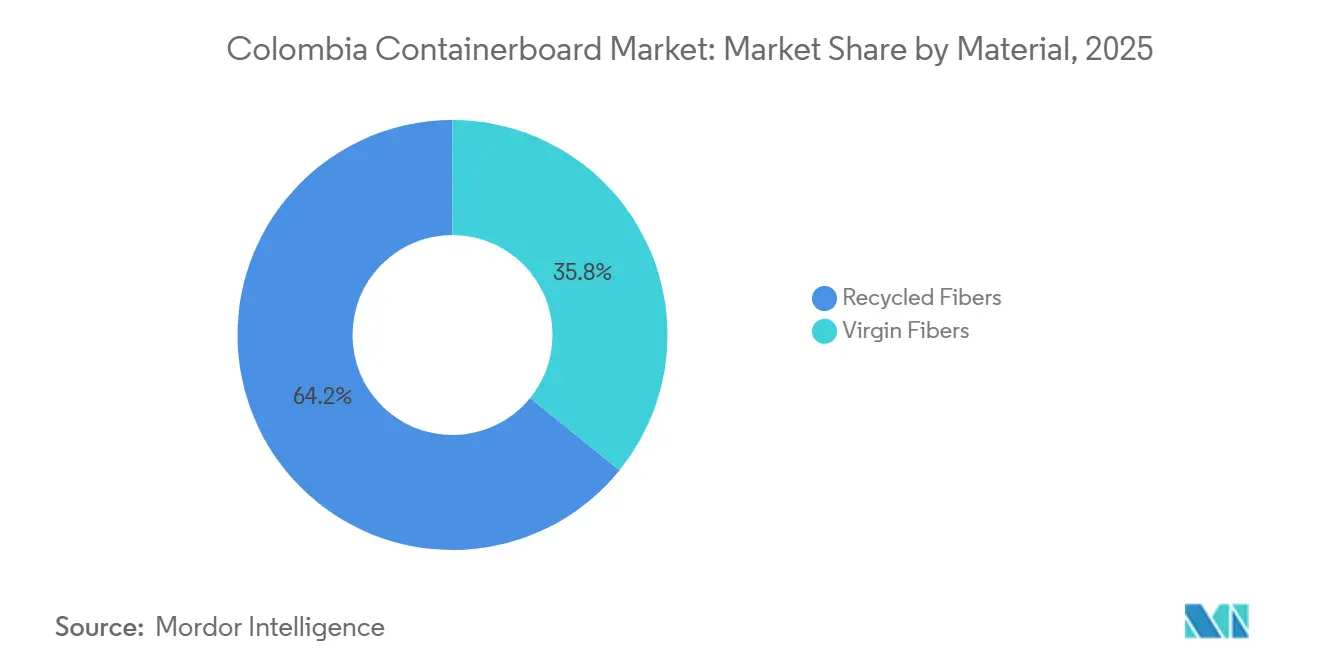

- By material, recycled fibers captured 64.17% of the Colombia containerboard market share in 2025.

- By product type, the Colombia containerboard market size for the kraftliners segment is forecast to advance at a 7.02% CAGR through 2031.

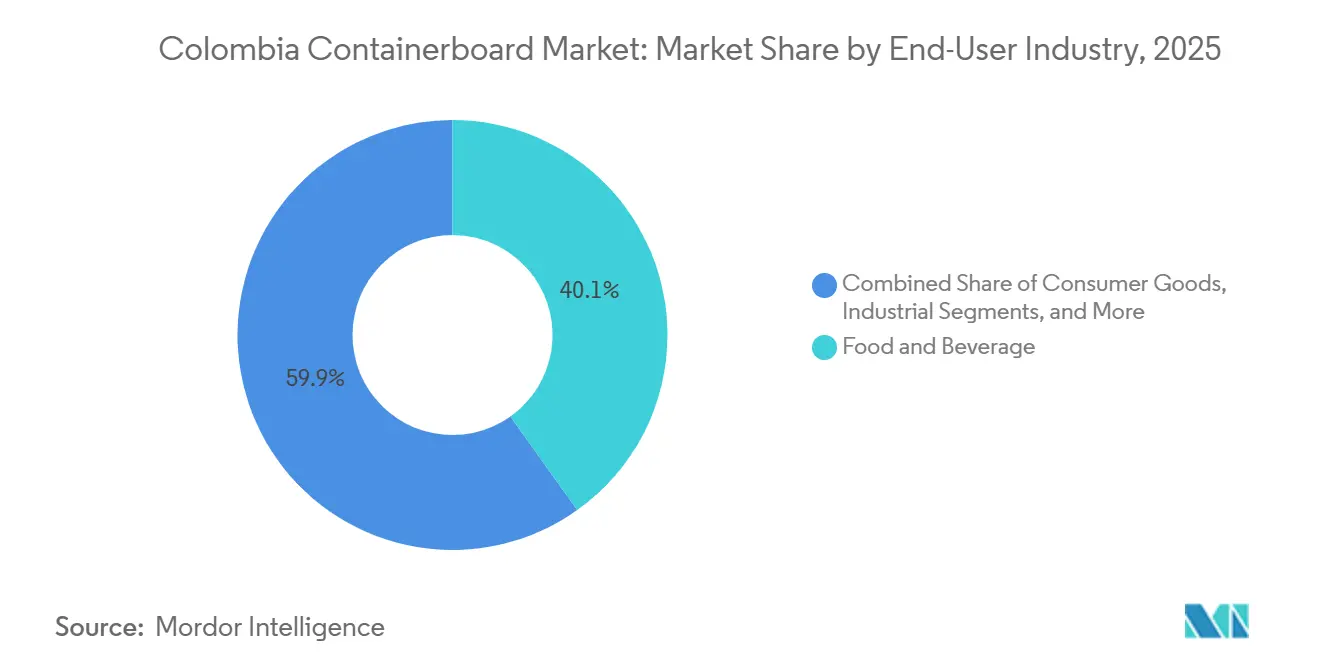

- By end-user industry, food and beverage captured 40.14% of the Colombia containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Colombia Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce Parcel Density Raises Corrugated Box Throughput Needs | +1.4% | National, with early gains in Bogotá, Medellín, Cali, and Barranquilla | Short term (≤ 2 years) |

| Plastic Substitution Rules Redirect Secondary and Delivery Packaging Toward Fiber | +1.2% | National, concentrated in commercial and retail zones across major urban centers | Medium term (2-4 years) |

| Food and Beverage Recovery Sustains Base-Load Carton Demand | +1.0% | National, with Bogotá, Valle del Cauca, and the Atlantic Coast as core consumption zones | Medium term (2-4 years) |

| Recovered-Fiber Ecosystem Lowers Recycled Containerboard Entry Barriers | +0.8% | National, with collection infrastructure concentrated in Bogotá, Medellín, Cali, and Barranquilla | Long term (≥ 4 years) |

| Barrier and Grease-Resistant Paper Innovation Expands Fiber Packaging Use | +0.5% | National, with spillover to export-oriented agricultural packaging in Antioquia and Valle del Cauca | Long term (≥ 4 years) |

| Biomass and Mill Upgrades Improve Domestic Supply Reliability | +0.3% | National, centered in Yumbo, Valle del Cauca, and Barranquilla, Atlántico | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Parcel Density Is Raising Corrugated Box Throughput Requirements

Colombia’s e-commerce channel closed 2025 with a transactional value of COP 145.4 trillion (USD 34.6 billion), an 11.1% year-over-year increase. Lower average ticket values of COP 212,373 (USD 57.69) per transaction indicate smaller, lighter parcels moving through the network. That shift matters because converters in the Colombian containerboard market must handle more box events for the same value of merchandise, which makes box count a tighter operating constraint than total box weight. Retailers and logistics operators are also requesting B-flute and E-flute micro-corrugated formats to reduce void fill and dimensional weight charges in urban delivery channels. This favors converters that can invest in tighter printing and cutting tolerances rather than relying solely on standard brown-box output. ORG It also explains why capacity additions have not fully eased delivery pressure in Bogotá and Medellín, where parcel density is climbing faster than legacy plant layouts were designed to manage.

Plastic Substitution Rules Are Redirecting Secondary And Delivery Packaging Toward Fiber

The Ministry of Environment issued Resolution 0803 in July 2024 and activated the phaseout path under Law 2232, which targets 21 categories of single-use plastics by 2030.[1]Ministerio de Ambiente y Desarrollo Sostenible, “Minambiente Establece Medidas Para La Reducción Gradual De Plásticos De Un Solo Uso En Colombia,” Ministerio de Ambiente y Desarrollo Sostenible, minambiente.gov.co The first restriction took effect on July 7, 2024, when 8 product types were prohibited from the market. The rule also covers products sold through e-commerce channels, which removes an easy path for digital sellers to delay packaging changes. In the Colombian containerboard market, demand extends beyond carry bags into transit-ready secondary packaging for delivery, takeaway, and retail distribution. Smurfit Westrock’s corrugated design for Plásticos Fénix replaced more than 30 tons of single-use plastic each year and helped the client lift regional sales by 20%, which shows that fiber replacement can support both compliance and sell-through. Extended Producer Responsibility rules also require recycled content in bottled-water packaging, which adds more pressure to move away from virgin plastic formats across adjacent packaging categories.[2]Ministerio de Ambiente y Desarrollo Sostenible, “Resolución 803 De 2024 MADS,” Normograma Invima, normograma.invima.gov.co

Food And Beverage Recovery Is Sustaining Base-Load Carton Demand

Colombia’s food-processing sector represented 29% of total manufacturing activity, and consumption reached USD 59 billion in 2024.[3]United States Department of Agriculture, Foreign Agricultural Service, “Food Processing Ingredients Annual, Colombia,” USDA FAS GAIN Report, fas.usda.gov Production in the sector declined 0.7% in 2024, but the pressure came from taxes on some foods, high transport costs, and softer household spending rather than from a structural collapse in packaged-food demand. Retail food sales still rose 12% in 2024, supported by hard-discount chains that depend on frequent corrugated replenishment across compact store networks. Also projected 2025 GDP growth of 2.6%, which supported a firmer consumption backdrop for packaged goods moving through modern retail. That matters for the Colombia containerboard market because food packaging demand is steady, specification driven, and less exposed to abrupt discretionary swings than many industrial uses. Coffee processing, meat and poultry, and sugar all posted positive growth in 2024, and those product flows rely heavily on corrugated cases for domestic distribution and export handling.

Colombia’s Recovered-Fiber Ecosystem Lowers Recycled Containerboard Entry Barriers

The Colombia containerboard market benefits from a secondary-fiber system that is more developed than many peer markets in South America at a similar income level.[4]Smurfit Westrock, “Día Mundial Del Reciclaje, Smurfit Westrock Impulsa Acciones Que Generan Impacto Real,” Smurfit Westrock Newsroom, smurfitkappa.com Smurfit Westrock collected more than 200,000 tons of paper and cardboard each year, covered half of its own fiber needs, and operated compacting plants in Bogotá, Barranquilla, Cartagena, Medellín, and Cali. The company also worked with more than 480 suppliers across 46 municipalities, which shows the scale and geographic reach of the collection already in place. A dense recycler base reduces raw material access risk for mills focused on recycled grades and supports faster response times when domestic box demand rises. It also helps explain why recycled fibers remain the operating foundation of the Colombia containerboard market even as premium virgin grades gain ground in export packaging. Corrugados Andina reports that it recycles 100% of the raw material used in its process, which shows that strict fiber-management discipline is possible beyond the largest integrated producer.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OCC, Pulp, Chemical, and Energy Cost Volatility Compresses Margins | -1.2% | National, with highest exposure at inland mills distant from fiber collection hubs | Short term (≤ 2 years) |

| Inland Freight and Logistics Bottlenecks Raise Delivered Packaging Costs | -0.8% | National, most acute on Bogotá-Buenaventura and Bogotá-Medellín corridors | Medium term (2-4 years) |

| Recovered-Fiber Quality Dispersion Raises Process Losses and Limits Premium Grade Consistency | -0.5% | National, with greater impact in regions outside main collection zones | Long term (≥ 4 years) |

| Domestic Paper Capacity Stress Tightens the Buffer Against Import Shocks | -0.4% | National, with acute stress in Valle del Cauca following the Yumbo plant suspension | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

OCC, Pulp, Chemical, And Energy Cost Volatility Is Compressing Margins

The main cost risk in the Colombia containerboard market is not limited to OCC pricing; pressure also comes from imported pulp, chemicals, and power. Carvajal Pulpa y Papel reported accumulated operating losses of COP 170.957 billion (USD 41.1 million) in 2024 and linked the deterioration in part to artificially low imported paper prices and supply difficulties. Colombia’s Ministry of Commerce also investigated alleged dumping in paper imports from Brazil and documented a weighted-average dumping margin of 45.5%. That leaves domestic mills exposed on both sides of the income statement because imported supply can pressure selling prices while imported inputs can still raise production costs. In this environment, mills with integrated energy systems carry a clear advantage over smaller players that buy a larger share of power and fuel at market rates. Smurfit Westrock’s Yumbo biomass project strengthens that hedge and raises the cost gap between integrated leaders and stand-alone converters in the Colombia containerboard market.

Inland Freight And Logistics Bottlenecks Are Raising Delivered Packaging Costs

Colombia’s national logistics costs stood at 15.6% of gross sales in 2024, down from 2022 but still far above the OECD level of 8%. Transport alone accounted for 44.5% of total logistics costs, which shows how dependent packaging distribution remains on the road network. Between January and September 2025, Colfecar’s Bloqueómetro recorded 700 road blockades, 10,930 hours of disruption, and COP 1.9 trillion (USD 452 million) in losses. That raises the delivered cost of every box and hits smaller converters hardest, since they lack a broad plant network to reroute shipments. It also creates service risk for food customers who run tight replenishment cycles and cannot absorb missed delivery windows during harvest periods or social disruptions. The underdeveloped cold chain worsens this constraint because it limits efficiency in agricultural runs and forces converters to hold more inventory closer to clients.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fibers Lead While Virgin Grades Gain On Quality Needs

Recycled fibers accounted for 64.17% of the Colombia containerboard market share in 2025, reflecting the scale of the country’s OCC collection network and the lower capital burden associated with recycled-grade production. This position was built over time by converters and mills that learned to manage fiber variability through process control rather than relying solely on uniform virgin inputs. That operating model continues to anchor the Colombia containerboard market because access to recovered paper is broader and faster than access to imported premium pulp. Corrugando Digital noted that recycled-fiber corrugated can meet demanding rigidity and compression requirements when starch treatment, COBB values, and pressing are tightly controlled. That point is important because it narrows the quality gap between recycled grades and virgin grades in many agricultural and industrial uses.

Virgin fibers remain the fastest-growing material segment, with a 6.88% CAGR over 2026-2031, as some applications now require higher purity, stronger burst performance, and easier food-safety qualification. Smurfit Westrock’s Cali mill produces bleached eucalyptus pulp and virgin containerboard, which supports that move toward higher-value grades. Export-oriented fresh produce and processed-food customers are a key part of this shift because their packaging specifications are linked to shelf-life risk, stacking performance, and retailer compliance. The June 2025 BRCGS certification at the Guarne corrugated plant reinforces the same pattern, since premium food-safety credentials are easier to support when certified fiber inputs and tighter process controls are in place.

By Product Type: Testliners Hold Scale While Kraftliners Set The Growth Pace

Testliners held 43.61% of the market in 2025, which matches the recycled-fiber orientation of the Colombia containerboard industry and the cost discipline of its largest buyer groups. Food and beverage users, along with many consumer-goods accounts, still value dependable performance at the right delivered cost more than premium liner properties in standard transit applications. That keeps testliners at the center of converter purchasing decisions across everyday shipping formats. Flutings remain essential alongside testliners because recycled medium and corrugating semi-chemical medium are core inputs for the national box-making base. Together, these grades support the broad volume structure of the Colombia containerboard market even before premium export packaging is considered.

Kraftliners are projected to grow at a 7.02% CAGR through 2031, which is faster than any other product type in this market. Agricultural exporters shipping avocado, banana, and tropical fruit increasingly need wet strength and stacking performance that recycled grades do not always match under refrigerated or humid conditions. Smurfit WestRock’s Barranquilla mill focuses on recycled liners and corrugated medium, while its Cali mill produces virgin containerboard, giving the company a workable supply position across both ends of the product range. The shift toward thinner but stronger liner grades also supports kraftliner demand, as eucalyptus-based virgin pulps can help converters reduce basis weight without sacrificing required performance. That combination of export quality, material optimization, and integrated supply is why Kraftliners are outpacing the rest of the product mix in the Colombian containerboard market.

By End-User Industry: Food And Beverage Leads While Consumer Goods Expands Faster

Food and beverage was the largest end-user category with a 40.14% share in 2025, which aligns with the sector’s scale within Colombia’s broader manufacturing base. The USDA reported that food processing accounted for 29% of manufacturing activity, providing converters with a stable flow of recurring box demand across beverages, processed meats, snacks, and bakery items. Those applications matter because they are specification-stable, ship regularly, and are less exposed to abrupt swings than some industrial categories. Industrial end users also contribute meaningful volume, especially in chemicals, construction materials, and consumer durables that need heavier-duty transport packaging. Other end-user industries, including agriculture, floriculture, and e-commerce-native retail, add a smaller but important stream of demand that supports regional converter utilization.

Consumer goods are forecast to grow at a 7.11% CAGR over 2026-2031, making it the fastest-growing end-user segment in the Colombia containerboard market. Personal-care, home-care, and toy brands are shifting more secondary packaging from plastic to corrugated fiber, which is driving demand for cleaner print quality, better shelf presentation, and transit protection. That need supports higher-value formats such as litho-laminated corrugated and retail-ready packaging, not only standard transport cartons. Smurfit Westrock’s GDUSA Package Award 2025 for a plastic-replacement corrugated design used by a Colombian toy manufacturer shows the commercial potential of this move, and the design helped lift the client’s Caribbean regional sales by 20%.

Geography Analysis

The Colombia containerboard market is centered first on the Bogotá Savanna and the wider Cundinamarca region, which form the country’s largest consumption zone for corrugated packaging. This position comes from the concentration of consumer-goods manufacturing, food processing, and Colombia’s main e-commerce distribution base in and around the capital. Bogotá also benefits from stronger OCC availability because its population scale and recycling density support a deeper recovered-paper stream than most other cities. At the same time, intra-urban congestion increases per-delivery costs for smaller orders, which can offset some of the benefits of improved access to raw materials. Antioquia is the second major demand corridor, and Smurfit Kappa’s May 2024 opening of the Guarne corrugated plant, with an investment of over USD 50 million, shows that producers expect sustained growth in that area.

Valle del Cauca, anchored by Cali and the Yumbo industrial belt, remains the highest-value production zone because it combines integrated papermaking with access to virgin-grade and specialty paper capabilities. Smurfit Westrock’s Cali mill and the USD 115.5 million biomass boiler and debarker project at Yumbo reinforced that role in 2025 and strengthened the region’s energy resilience. The April 2025 indefinite suspension of Carvajal Pulpa y Papel’s Yumbo plant also showed that even this industrial core is vulnerable when import pricing falls below domestic cost structures. On the northern coast, Barranquilla, Cartagena, and Santa Marta connect kraftliner demand to fresh-produce export activity, especially where banana and tropical-fruit packing operations require stronger boxes for containerized shipping.

The Andes split Colombia into Atlantic, Pacific, and interior corridors, and that geographic structure increases the logistics burden of serving the Colombia containerboard market on a national basis. The DNP reported logistics costs equal to 15.6% of sales in 2024, and transport alone accounted for 44.5% of that figure. Road disruptions added to that pressure in 2025, when 700 blockades generated 10,930 hours of disruption and COP 1.9 trillion (USD 452 million) in losses. That geography favors integrated players with multi-site converting capacity because they can serve national accounts with shorter haul distances than single-site rivals.

Competitive Landscape

The Colombia containerboard market is moderately consolidated at the mill level and more dispersed at the converting level, which creates a two-speed competitive structure. Smurfit Westrock holds the strongest integrated position through paper mills in Barranquilla and Cali and corrugated converting plants in Bogotá, Medellín, Cali, and Barranquilla. Its SEC-listed subsidiary structure, including Papeles y Cartones S.A. and Carton de Colombia S.A., supports a broader account reach than smaller competitors can match on their own. Also improved its regional position with the November 2025 acquisition of Industria Papelera Indugevi S.A.S., a sign of ongoing consolidation among mid-tier recycled-fiber players. That pattern suggests scale is becoming more important as cost pressures make stand-alone operations harder to defend in the Colombian containerboard market.

The clearest openings now lie in food-safe, direct-contact packaging, as well as in short-run precision converting for e-commerce parcels and branded retail formats. Smurfit Westrock’s June 2025 BRCGS certification at the Guarne plant created a clear food-safety benchmark because it was the first corrugated packaging plant in Colombia to achieve that standard. The same plant also received LEED certification with 46 of 48 possible points, which strengthens its position with multinational consumer-goods customers that screen suppliers on environmental criteria. Those moves show that competition is no longer defined only by tonnage and price, because certification and process capability now matter more in higher-value parts of the Colombia containerboard market.

Smurfit Westrock’s 2024 merger also added international procurement scale that many Colombian mid-tier companies cannot easily replicate. The Guarne plant opening, the Yumbo biomass investment, and the BRCGS and LEED credentials together form a clear sequence of strategic moves centered on capacity, cost control, and qualification depth. By contrast, smaller converters are more exposed to freight inflation, input volatility, and the need to upgrade equipment for short-run and food-safe work. That leaves the Colombia containerboard market open to more mid-tier M&A, but not yet to the point where a few suppliers fully control national converting demand.

Colombia Containerboard Industry Leaders

Smurfit Westrock plc

Papeles y Cartones S.A. Papelsa

EMPACOR S.A.

Empaques Industriales de Colombia S.A.S.

CARTONES AMERICA S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Smurfit Westrock reported Q1 2026 results: Latin America, with Colombia included, achieved net sales of USD 540 million and an Adjusted EBITDA of USD 109 million, marking a ~20% margin. Management highlighted "strong volume growth in Colombia." In Q1, North American containerboard prices increased by USD 20/ton, followed by another USD 30/ton rise in April, indicating a recovery in the pricing cycle. This has implications for Colombia, especially concerning the pass-through of import prices.

- March 2026: Smurfit Westrock finalized its acquisition of Cartomanabí in Ecuador, boasting an annual capacity exceeding 50,000 tons. This move solidifies Smurfit Westrock's status as the leading corrugated supplier in South America and enhances the pan-regional supply chain, benefiting its network in Colombia.

- February 2026: Smurfit Kappa WestRock projected 2.0% growth for the South American market through 2030. The company set ambitious targets of achieving a group EBITDA of USD 7 billion (around a 19% margin) by 2030 and accumulating a cumulative free cash flow of USD 14 billion from 2026 to 2030. Notably, South America, including Colombia, was highlighted as a key engine of above-average growth and margins.

- November 2025: EMPACOR S.A. completed the acquisition of 100% of the shares of Industria Papelera Indugevi S.A.S., a Sabaneta, Antioquia-based recycled-fiber packaging producer with approximately 365 employees. The transaction consolidates 2 recycled-kraft and corrugated-box manufacturers under common ownership and represents one of the significant intra-sector M&A moves in the Colombian market in recent years.

Colombia Containerboard Market Report Scope

The Colombia Containerboard Market encompasses the production, distribution, and consumption of containerboard materials used in manufacturing corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The market is driven by the increasing demand for sustainable, lightweight, and durable packaging solutions.

The Colombia Containerboard Market Report is Segmented by Material (Virgin Fibers and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current size and outlook for the Colombia containerboard market?

The Colombia containerboard market was valued at USD 1.38 billion in 2025, stands at USD 1.45 billion in 2026, and is forecast to reach USD 1.98 billion by 2031 at a 6.43% CAGR.

Which material segment leads demand in Colombia?

Recycled fibers led with a 64.17% share in 2025 because Colombia has an established recovered-paper collection system and a converter base built around recycled grades.

Which product type is growing fastest through 2031?

Kraftliners are the fastest-growing product type, with a 7.02% CAGR, supported by export packaging needs in fresh produce and processed foods.

Why is e-commerce important for box demand in Colombia?

E-commerce reached COP 145.4 trillion (USD 34.6 billion) in 2025, and smaller parcel formats are increasing box throughput faster than revenue growth alone suggests.

What is the main risk facing producers and converters?

The biggest risk is margin pressure from OCC, pulp, chemical, energy, and freight volatility, especially for inland operators without integrated energy or multi-site delivery networks.

Which end-user group is most important and which one is growing fastest?

Food and beverage was the largest end-user segment with 40.14% share in 2025, while consumer goods is expanding fastest at a 7.11% CAGR through 2031.

Page last updated on: