Mexico Container Glass Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

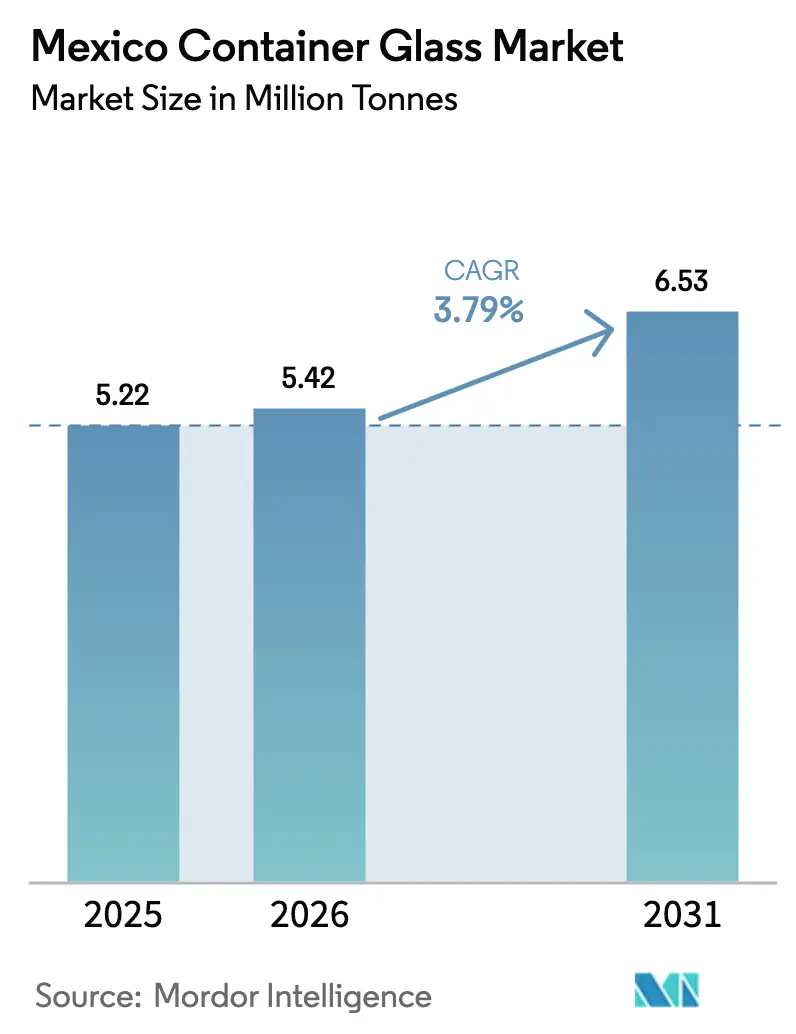

| Base Year Market Size (2025) | 5.22 Million tonnes |

| Market Volume (2026) | 5.42 Million tonnes |

| Market Volume (2031) | 6.53 Million tonnes |

| Growth Rate (2026 - 2031) | 3.79% CAGR |

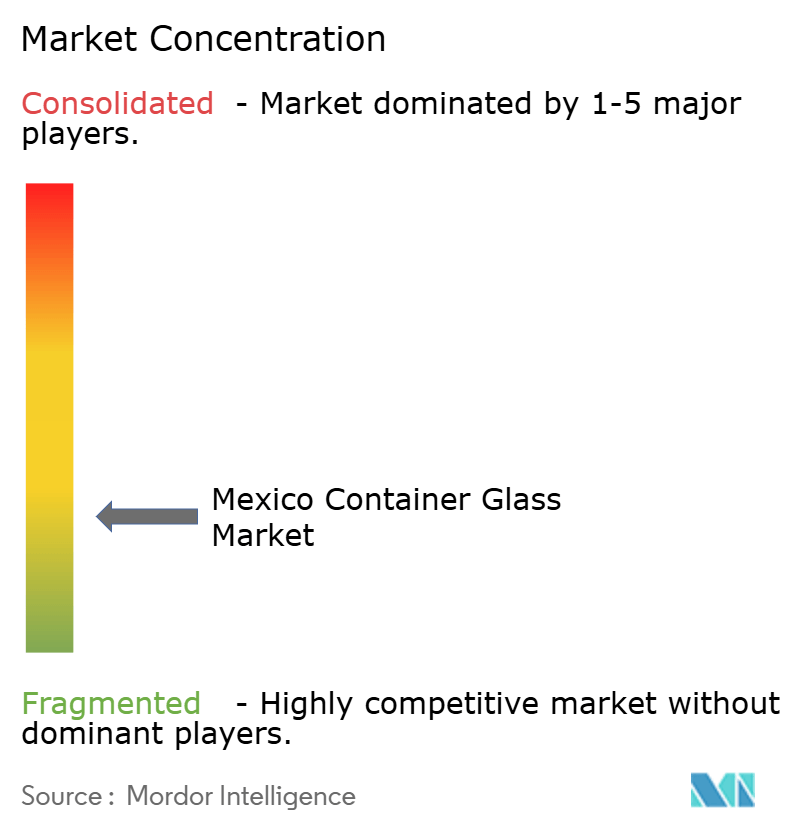

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Container Glass Market Analysis by Mordor Intelligence

Mexico Container Glass Market size in 2026 is estimated at 5.42 million tonnes, growing from 2025 value of 5.22 million tonnes with 2031 projections showing 6.53 million tonnes, growing at 3.79% CAGR over 2026-2031. Near-shoring by beverage and pharmaceutical brand owners, sustained momentum in tequila exports, and government-backed decarbonization financing collectively underpin this growth trajectory. Mexico is already the largest glass-bottle supplier to the United States, shipping containers worth USD 550 million in 2023, while domestic spirits producers generated 495.8 million liters of tequila and exported 400.3 million liters in 2024, keeping furnace lines running close to nameplate capacity. The Mexico container glass market benefits from a dual demand base: sizeable local consumption and a robust export pipeline that absorbs premium bottles for agave-based spirits, craft beer, and high-value pharmaceuticals. Competitive pressures center on energy-efficiency upgrades, cullet availability, and the ability to offer short production runs for artisanal beverages, all of which shape near-term capital spending priorities.

Key Report Takeaways

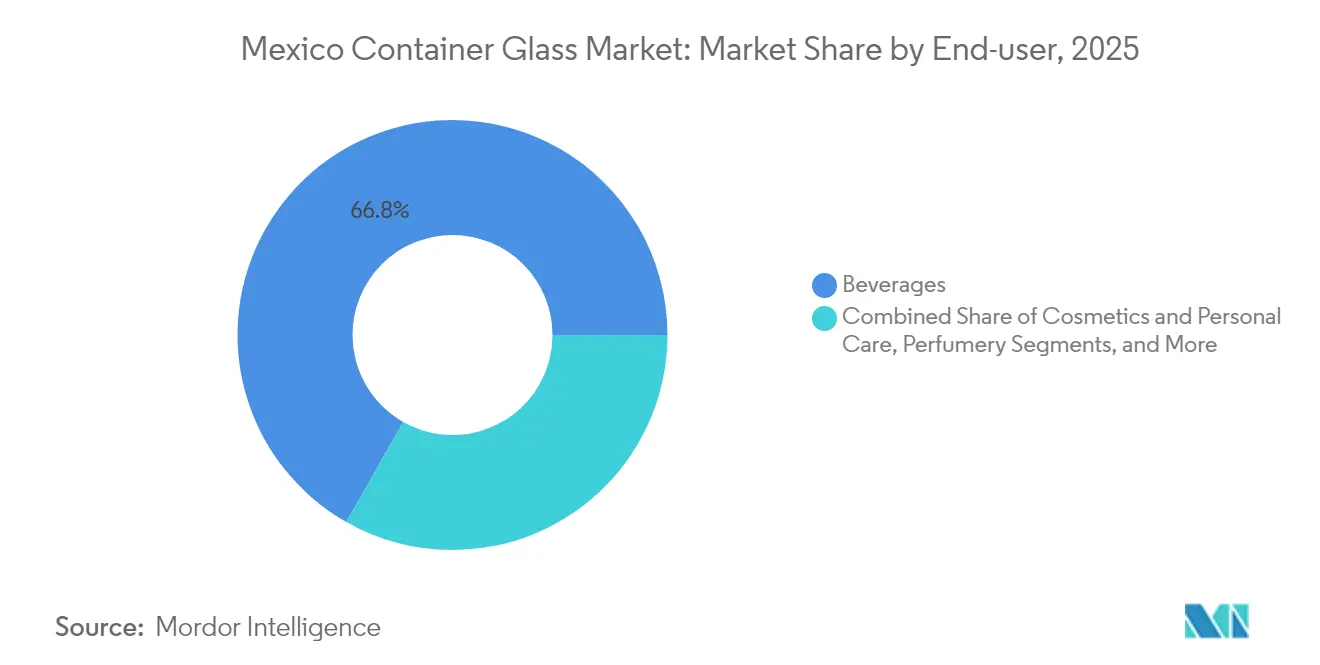

- By end-user, beverages accounted for 66.78% of the Mexico container glass market share in 2025.

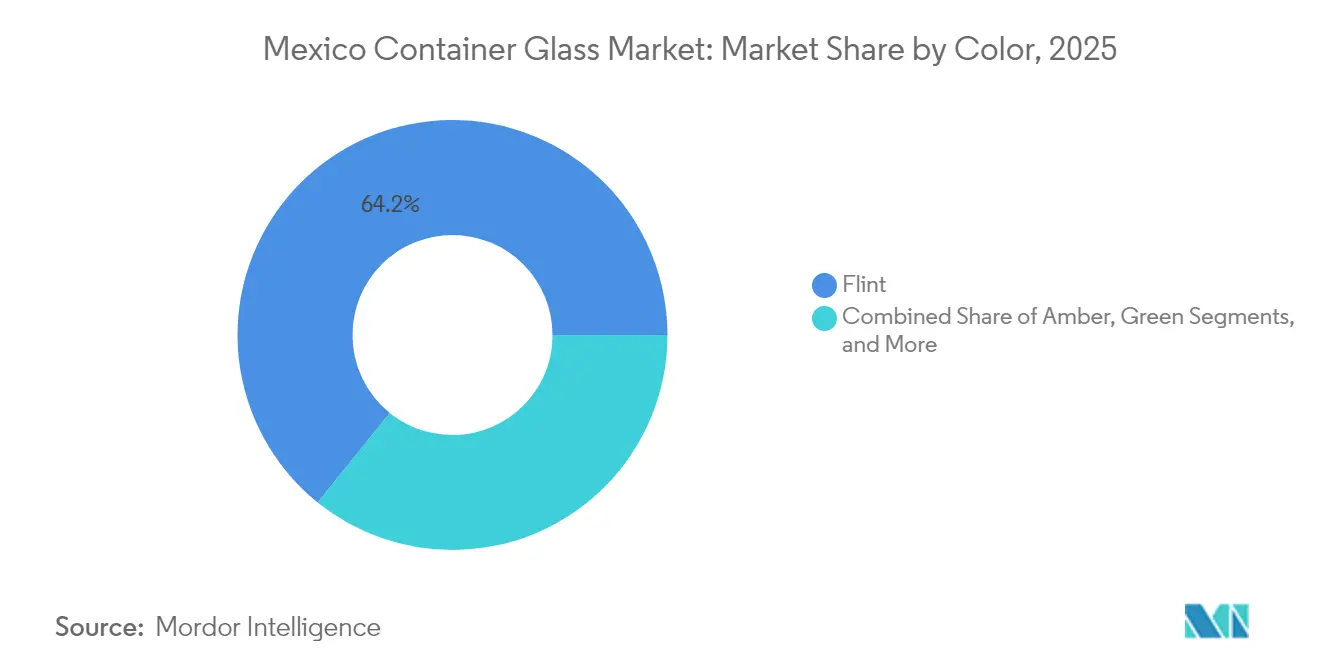

- By color, the Mexico container glass market for amber glass is projected to grow at a 4.88% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium-packaging demand from beverages | +0.8% | National; Jalisco, Guanajuato, Michoacán | Medium term (2–4 years) |

| Sustainability and recyclability push | +0.6% | National; Mexico City, Monterrey, Guadalajara | Long term (≥ 4 years) |

| Craft beer and artisan spirits boom | +0.5% | National; central and northern Mexico | Short term (≤ 2 years) |

| Agave-based spirit export surge | +0.7% | Jalisco, Nayarit, Michoacán, Guanajuato, Tamaulipas | Medium term (2–4 years) |

| Government incentives for recycled glass | +0.4% | National | Long term (≥ 4 years) |

| Near-shoring of pharma filling lines | +0.3% | Northern Mexico, Bajío, Mexico City | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Premium-packaging demand from beverages

The record tequila output of 495.8 million liters and exports of 400.3 million liters in 2024 have heightened the demand for heavier, custom flint bottles that signal authenticity on U.S. shelves. Craft breweries echo the trend, commissioning embossed containers to stand apart in crowded retail sets and are willing to pay a premium for design exclusivity. Export-oriented spirits producers now treat bottle aesthetics as a core marketing lever, prompting glassmakers to install flexible IS machines capable of shorter runs. The willingness of consumers to pay higher unit prices for distinctive packaging boosts the average revenue per ton, thereby cushioning producers against energy price volatility. With the United States absorbing roughly 80% of agave-spirit exports, Mexico's container glass market participants enjoy steady offtake for premium formats despite tariff overhang.

Sustainability and recyclability push

Corporate mandates favor infinitely recyclable glass, yet Mexico’s cullet utilization rate lags at around 12% of the 2.5 million tons generated annually. Beverage majors have responded by building closed-loop logistics, exemplified by O-I’s Chihuahua hub that upgrades post-consumer glass for furnace feedstock. SEMARNAT’s circular-economy guidelines and the USD 100 million Iniciativa Industria Sustentable 2025 further tilt capital toward oxy-fuel furnaces and alternative energy systems that can trim power costs by up to 40%. As environmental scrutiny tightens, brand owners are increasingly tying bottle procurement to suppliers’ carbon-reduction roadmaps, pushing the Mexico container glass market toward higher recycled content and lower-emission melting technologies.

Craft beer and artisan spirit's boom

Rising disposable incomes and shifting tastes have lifted craft beer output and sparked a mezcal renaissance, with the latter logging 12.2 million liters of production and 7.8 million liters of exports in 2023. Both niches lean on glass to convey craftsmanship, favoring amber for UV protection and intricate mold features for shelf differentiation. Smaller batch sizes pressure producers to refine job-change agility and invest in digital inspection to minimize wastage on complex geometries. Regional breweries form tight supply loops with nearby glass plants, reducing freight emissions and turnaround times. The artisanal surge therefore rewards plants capable of multi-color, quick-switch operations within the Mexico container glass market.

Agave-based spirit export surge

With tequila exports exceeding 400.3 million liters in 2024 and mezcal shipments skewing heavily toward the United States, export-grade bottles must comply with stringent ASTM impact and top-load criteria. Producers increasingly specify deeper punts, thicker heels, and refined neck finishes to ensure freight resilience over multi-modal routes. International demand for distinctive shapes prompts mold workshops to expand their design services, thereby embedding intellectual property into packaging. Although proposed U.S. tariffs of up to 25% could reshape price ladders, Mexico remains the sole legitimate source of tequila and mezcal, anchoring baseline demand for compliant glass containers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PET and aluminum substitution | -0.9% | National; beverage and food | Short term (≤ 2 years) |

| High furnace energy costs | -0.7% | National; energy-intensive regions | Medium term (2–4 years) |

| Furnace-upgrade capex for gas transition | -0.5% | National | Medium term (2–4 years) |

| Domestic cullet shortage | -0.4% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

PET and aluminum substitution

Cost-sensitive beverage lines are continuing to migrate toward lightweight PET and aluminum, especially as fuel surcharges magnify the logistics savings offered by lower-mass formats. The food-delivery boom alone adds 300,000 tonnes of plastic waste annually, signaling consumer acceptance of non-glass containers in convenience channels. During economic slowdowns, brand owners prioritize unit cost over premium cues, temporarily ceding market share to the Mexico container glass market. Yet regulatory momentum for recyclable packaging and consumer loyalty in premium categories buffers long-run volume.

High furnace energy costs

Glass melting in Mexico relies on electricity and natural gas, which, on average, cost nearly double the U.S. benchmarks, eroding margin headroom. Utilities in northern states face intermittent drought-driven hydro deficits, heightening exposure to higher-priced thermal generation. Producers are accelerating oxy-fuel conversions, waste-heat recovery, and alternative feedstock trials to counterbalance the penalty. Government credit under the Iniciativa Industria Sustentable 2025 is available, but application cycles and project-finance hurdles delay immediate relief.[1]MexicoIndustry, “Iniciativa Industria Sustentable 2025,” MEXICOINDUSTRY.COM Consequently, energy intensity remains a strategic bottleneck for Mexico's competitiveness in the container glass market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-user: Beverages Sustain Volume Leadership

Beverages accounted for 66.78% of the Mexican container glass market share in 2025, as distillers, brewers, and soft drink bottlers kept their lines running at near full capacity. Tequila’s 495.8 million-liter run generated extraordinary pull for heavyweight flint bottles, while Coca-Cola FEMSA moved 2,052.9 million unit cases of soft drinks, sustaining demand for both returnable and one-way glass packages. Constellation Brands secures around 60% of its Mexican beer-bottle needs through a joint venture with O-I Glass, illustrating the scale of locked-in beverage contracts that stabilize furnace utilization.

Beyond alcohol, mineral-water and premium-juice brands adopt glass to differentiate on quality and recyclability, deepening the segment’s moat. Cosmetics and personal care are the fastest-growing applications, expanding at a 5.07% CAGR as luxury skin-care labels transition from plastic to glass jars for product preservation. Pharmaceutical vials and injectable formats represent a smaller slice, but near-shoring of filling lines in Monterrey and the Bajío is widening the addressable tonnage, sharpening producers’ focus on Type I borosilicate and coated flint containers.

By Color: Flint Dominates, Amber Accelerates

Flint retained a commanding 64.21% market share in the Mexican container glass market in 2025, underpinned by export standards that favor transparency for tequila and sterile drugs. Spirits marketers leverage clarity to showcase liquid hues and entrust brand storytelling to embossed ornaments and shoulder etchings. Pharmaceutical regulators likewise stipulate clear vials for visual inspection, reinforcing baseline flint tonnage.

Amber is the pace-setter, growing at 4.88% CAGR through 2031 on craft beer’s need for UV shielding and pharma’s light-sensitive formulations. Brewers in Baja and the central corridor have standardized on amber long-necks, credits to expanding cold-chain reach that tolerates return cycles. Green and specialty tones remain niche, favored by boutique wineries or premium mezcal labels seeking signature visuals, but represent incremental margin in the Mexico container glass industry.

Geography Analysis

Production capacity is concentrated in Jalisco, Mexico State, Nuevo León, and Guanajuato, locations that combine skilled labor pools, access to silica sand, and proximity to highways or rail links to U.S. ports of entry. Plants in central Mexico benefit from proximity to agave-spirit bottlers, which reduces inbound freight on raw materials and outbound logistics on finished goods. Northern furnaces leverage shorter haul distances to U.S. buyers, an advantage accentuated by the United States-Mexico-Canada Agreement’s rules of origin for packaging inputs.

Energy tariffs diverge across regions; northern industrial hubs often secure marginally cheaper electricity yet face water-scarcity risk, while central sites profit from denser natural-gas grids. Recycling hubs are scarce, with O-I’s Chihuahua facility standing out as a dedicated cullet processor that feeds multiple furnaces. Expanding cullet collection networks would reduce dependence on virgin raw materials and lower melting temperatures, a strategic imperative flagged by every major producer.

Ongoing highway expansions and port deep-water projects augment the Mexico container glass market’s export edge. As the Bajío develops into a life-sciences manufacturing hub, glassmakers weigh the benefits of brownfield upgrades against greenfield builds to meet pharmaceutical-grade container demand. Each locale contends with differing timelines for permitting, utility hookups, and environmental clearances, influencing capital-allocation sequencing across producers.

Competitive Landscape

The Mexican container glass market is characterized by a moderately concentrated field, where the top five suppliers collectively hold an estimated 55-60% share. Vitro, O-I Glass, Saverglass, BA Glass-Vidrio Formas, and Fevisa leverage multi-furnace networks, in-house mold shops, and long-term offtake contracts to protect the installed base. O-I’s Nava joint venture supplies roughly 60% of Constellation Brands’ beer-bottle needs, highlighting the effectiveness of captive agreements.

Consolidation persists: BA Glass acquired 60% of Vidrio Formas for EUR 125 million (USD 133 million) in 2023, jumping into the North American arena with 320 tons-per-day capacity. Strategic investments center on furnace rebuilds, IS machine automation, and hot-end inspection systems that reduce defect rates. Emerging disruptors cater to craft producers with short-run capabilities, exploiting gaps left by high-volume incumbents.

Trade frictions introduce complexity: the U.S. antidumping duty matrix ranges from 13.95% for Fevisa to 96.95% for smaller exporters, tilting competitiveness toward domestic supply for American buyers. High energy costs pressure margins, but government grants of up to USD 2 million per project under the Iniciativa Industria Sustentable 2025 entice firms to retrofit oxy-fuel burners and waste-heat recovery systems. Ultimately, success leans on balancing cost discipline with the design flexibility demanded by premium beverage and pharma customers.

Mexico Container Glass Industry Leaders

O-I Glass, Inc.

Gerresheimer AG

Tecnoglass S.A.

Vitro, S.A.B. de C.V.

Saverglass SAS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: AB InBev pledged a USD 3.6 billion capital program through Grupo Modelo, signaling its enduring confidence in the Mexican brewing and bottling supply chains.

- March 2025: Stevanato Group booked record EUR 1,104 million (USD 1,179 million) revenue in fiscal 2024 and highlighted expanded syringe output at its Monterrey site.

- March 2025: The second round of Iniciativa Industria Sustentable 2025 opened USD 100 million for industrial decarbonization, with glassmakers among eligible applicants.

- January 2025: Libbey confirmed that ongoing operations at its Monterrey plant will keep Latin American supply insulated from U.S. restructuring.

Mexico Container Glass Market Report Scope

Glass Containers refer to clean bottles and jars made from glass. The scope excludes windows and other non-container glass products. Container glass is used in the alcoholic and non-alcoholic beverage industries due to its ability to maintain chemical inertness, sterility, and non-permeability. Glass packaging is valued for its unique properties, including its transparency, inertness, and ability to preserve the quality and integrity of its contents.

Mexico container glass market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery, by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments.

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

What is the size of the Mexican container glass market in 2026?

The Mexico container glass market size stands at 5.42 million tonnes in 2026 and is on track for 6.53 million tonnes by 2031.

What is the primary end-user of container glass in Mexico?

Beverages dominate with 66.78% of Mexico container glass market share in 2025, driven mainly by tequila, mezcal, and beer bottling.

Which color segment is growing fastest?

Amber bottles, favored by craft beer and light-sensitive pharmaceuticals, are expanding at a 4.88% CAGR through 2031.

How are energy costs impacting producers?

Mexican furnaces pay nearly double U.S. energy rates, prompting investments in efficiency and participation in the Iniciativa Industria Sustentable 2025 financing program.

What role does near-shoring play for pharmaceutical glass?

Drug makers relocating filling lines to northern Mexico and the Bajío are boosting demand for Type I and coated flint vials and syringes sourced locally.

Page last updated on: