Canada Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

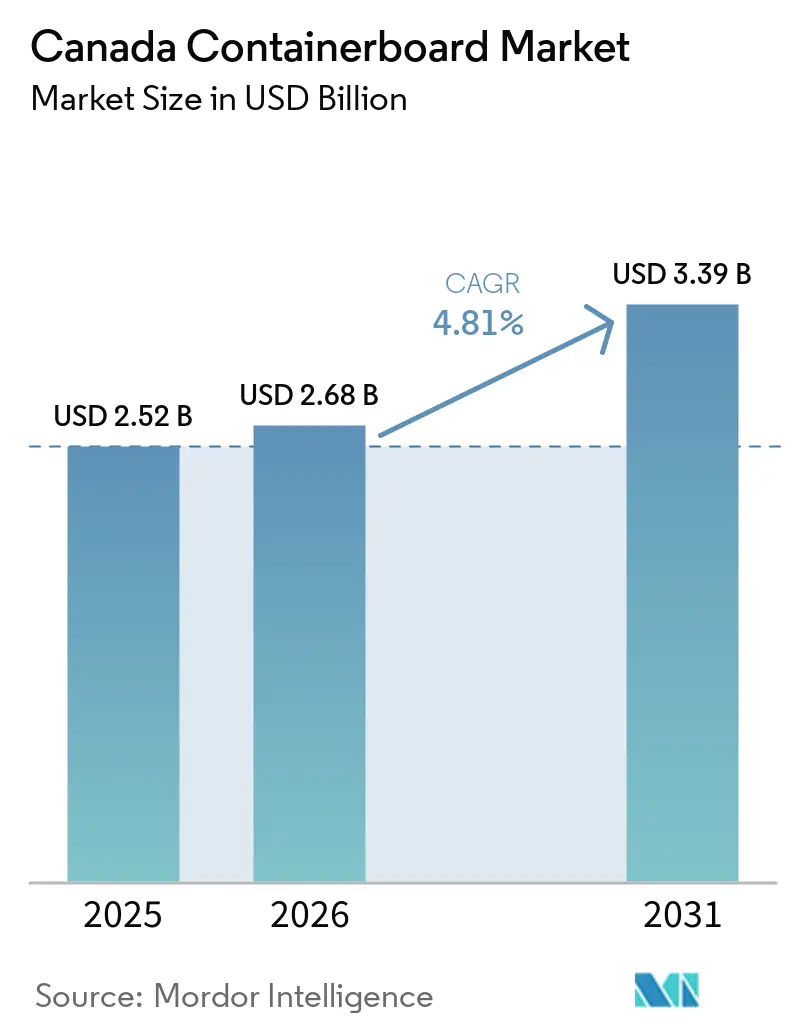

| Base Year Market Size (2025) | USD 2.52 Billion |

| Market Size (2026) | USD 2.68 Billion |

| Market Size (2031) | USD 3.39 Billion |

| Growth Rate (2026 - 2031) | 4.81% CAGR |

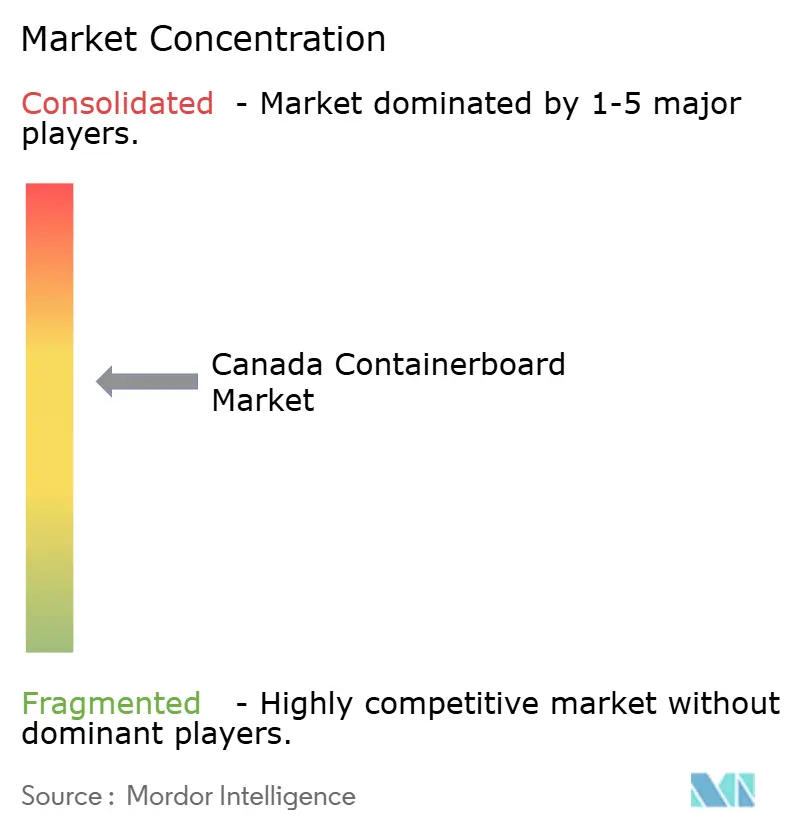

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Containerboard Market Analysis by Mordor Intelligence

The Canada containerboard market is projected to be USD 2.5 billion in 2025, USD 2.7 billion in 2026, and USD 3.4 billion by 2031, reflecting a 4.81% CAGR from 2026 to 2031. The market is supported by parcel demand linked to e-commerce, stable packaging needs in food processing, and broader shifts away from plastics. Mill integration across Quebec, Ontario, and British Columbia gives domestic producers control over fiber, converting, and distribution, supporting supply reliability and export reach. The United States remains the main export outlet for Canadian kraft linerboard, keeping cross-border trade conditions important for pricing and operating decisions. Capacity closures across North America through 2025 tightened supply conditions, improving the pricing backdrop entering 2026. This setup leaves the Canada containerboard market positioned for steady expansion, while profit performance still depends on fiber access, transport reliability, and the ability to meet stricter environmental claim standards.

Key Report Takeaways

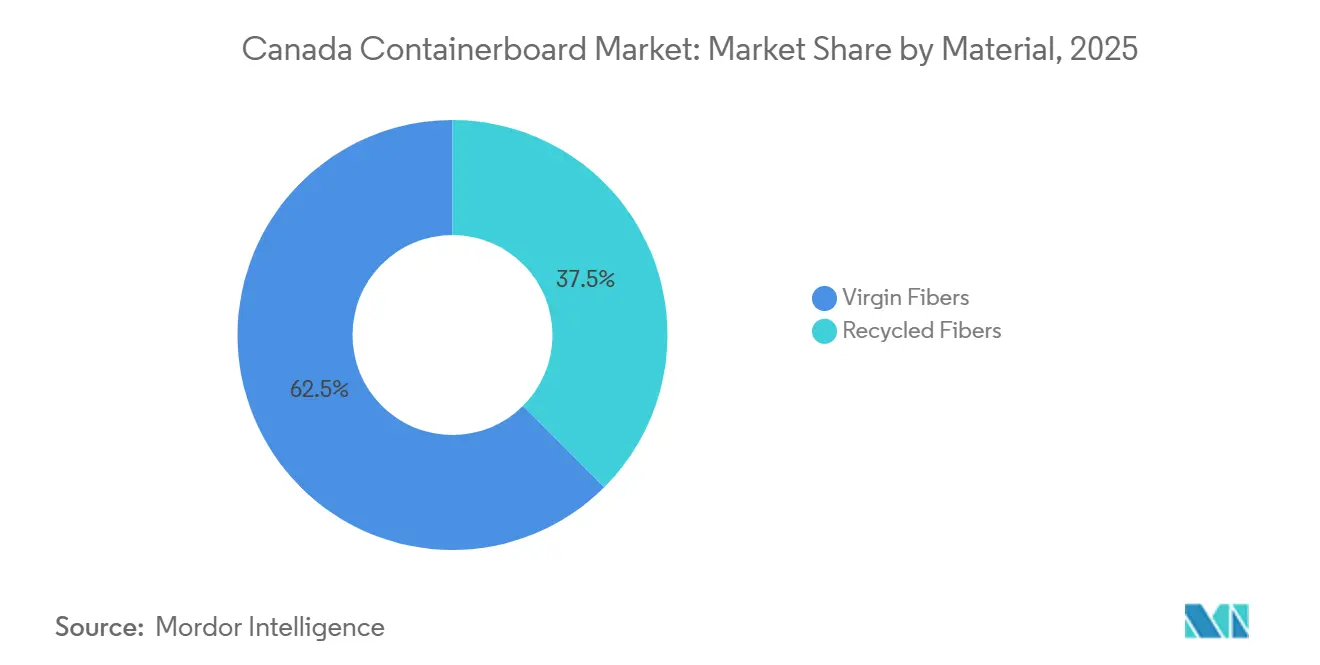

- By material, virgin fibers captured 62.47% of the Canada containerboard market share in 2025.

- By product type, the Canada containerboard market size for flutings is projected to grow at a 5.68% CAGR to 2031.

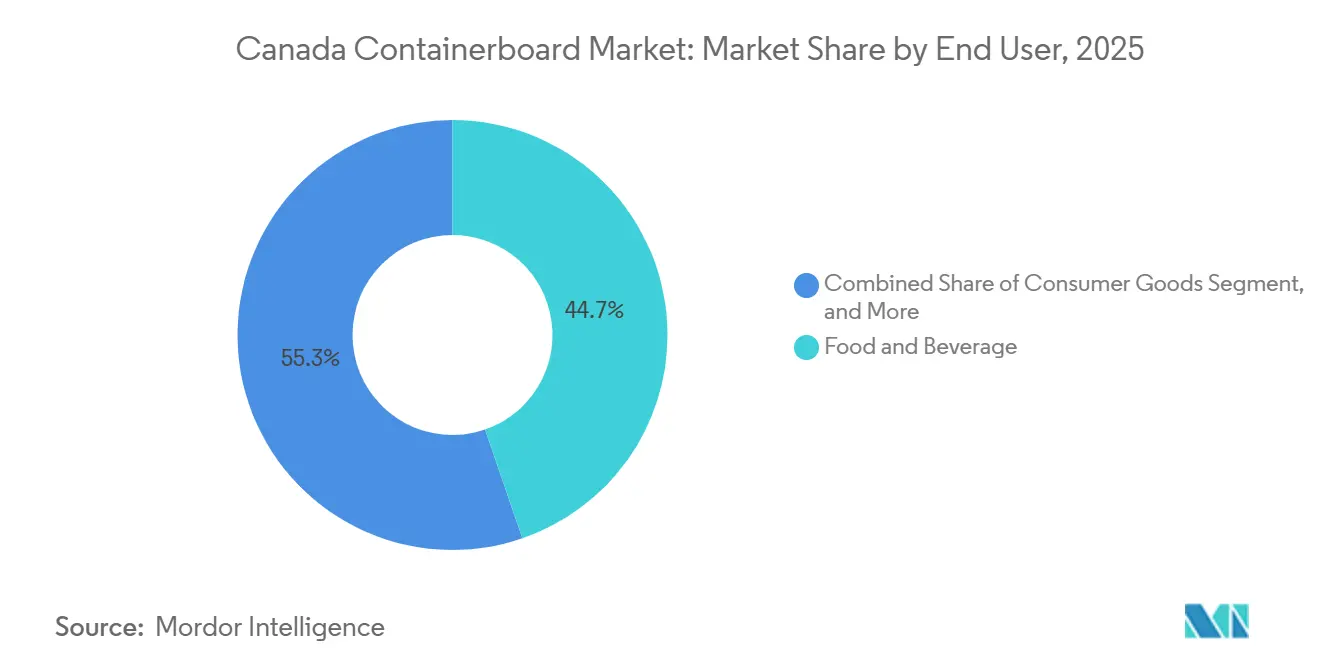

- By end user, food and beverage captured with 44.73% of the Canada containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce And Home Delivery Demand | +1.4% | Ontario, British Columbia, and Quebec, primary urban centers | Medium term (2-4 years) |

| Food Processing and Grocery Distribution Expansion | +0.9% | Ontario, Quebec, and the Prairie provinces | Medium term (2-4 years) |

| Plastic Substitution and Corporate Fiber Targets | +0.7% | National | Long term (≥ 4 years) |

| Ontario And Quebec EPR-Driven Paper Recovery | +0.5% | Ontario and Quebec, with spillover to all provinces | Medium term (2-4 years) |

| Anti-Greenwashing Compliance Favoring Fiber Claims | +0.3% | National | Medium term (2-4 years) |

| Cold-Chain and Export Packaging Performance Needs | +0.2% | National, with early gains in Ontario, Quebec, and British Columbia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce and Home Delivery Demand

Canada’s e-commerce activity has lifted corrugated box demand to a higher base, with the effect strongest in the Greater Toronto Area, the Lower Mainland, and the Montreal corridor. Statistics Canada tracked continued double-digit retail e-commerce growth across major urban centers, a pattern that supports higher use of crush-resistant single-wall and double-wall boxes for delivery volumes in the Canada containerboard market. Corrugated formats remain central to paper packaging for direct-to-consumer shipping because they support right-sized box design, graphics, and stacking strength during transport. As smaller parcels move into paper mailers, containerboard demand becomes more concentrated in larger, heavier-duty formats, preserving volume while shifting the grade mix toward stronger constructions. Cascades said in its first-quarter 2026 results that new packaging volumes in food and beverage are a strategic priority, which ties e-commerce demand to more resilient consumer end markets.

Food Processing and Grocery Distribution Expansion

Food and beverage processing remained Canada’s largest manufacturing sector, and that scale gives the Canada containerboard market a stable source of recurring packaging demand. Agriculture and Agri-Food Canada said the sector generated CAD 115.6 billion (USD 84.7 billion) in goods and accounted for 18.2% of total manufacturing sales.[1]Agriculture and Agri-Food Canada, “Overview of Canada’s Agriculture and Agri-Food System,” Agriculture and Agri-Food Canada, agriculture.canada.ca That production base supports steady demand for transit boxes, shelf-ready packaging, and export corrugated across grocery, produce, protein, and packaged foods. Export-oriented shipments of agricultural and processed foods also require packaging that meets transit and handling standards, which keeps demand strong for stronger virgin-fiber linerboard grades. Grocery distribution adds another layer of demand, as retailers increasingly use retail-ready and display-ready corrugated formats to improve store replenishment and handling efficiency. Improvements in high-burst single-wall packaging for produce and refrigerated goods are also increasing the board content used in some food shipping formats.

Plastic Substitution and Corporate Fiber Targets

Corporate packaging targets are pushing more outer packaging away from plastics and toward corrugated and kraft-paper formats, which extends the addressable demand base for the Canada containerboard market. The Canada Plastics Pact said that 50% of plastic packaging placed on the market by signatories was designed as reusable, recyclable, or compostable by 2023, up 7% in 2 years. That shift matters because fiber preferences are increasingly baked into procurement decisions, making the demand signal less dependent on short-term price swings. RYAM expanded its Kallima folding carton board line in Temiscaming in October 2025 with a freezer application that can withstand minus 18°C without plastic coatings, demonstrating that fiber substitution is moving into colder, more demanding packaging applications. This broadens the substitution opportunity beyond ambient consumer goods and into frozen foods, proteins, and other uses where plastic barriers had long held an advantage.

Ontario and Quebec EPR-Driven Paper Recovery

Ontario’s Blue Box system moved to 100% producer responsibility on January 1, 2026, which gives the Canada containerboard market a stronger domestic recovered-fiber base. The program covers 383 municipalities and 12 First Nations communities, and Circular Materials said it serves more than 5 million households, supported by new material recovery facilities in Cambridge and Greater Napanee. In Quebec, Éco Entreprises Québec collected 791,000 tonnes of materials in 2025 and reported a 87% residential collection rate, indicating a larger, more predictable recovery system. Its 2026 producer financial participation schedule set corrugated cardboard recovery at CAD 539.67 per ton (USD 396.50), up 7.5% year over year, indicating rising system costs but also confirming continued scaling of paper recovery. For mills that rely on recycled inputs, this larger domestic OCC stream reduces dependence on export-sensitive spot markets and helps smooth procurement conditions. Cascades said OCC prices had risen 245% above January 2023 levels in mid-2024, before falling 37% year over year by December 2025, underscoring why a more local supply base carries strategic value.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Virgin Fiber, OCC, And Energy Cost Volatility | -0.4% | British Columbia, Ontario, and Quebec for fiber, national for energy, and OCC | Medium term (2-4 years) |

| Competition From Reusable Plastic Totes and Flexible Formats | -0.3% | National, with a stronger concentration in Ontario and Quebec urban markets | Medium term (2-4 years) |

| Rail And Port Disruptions Across Canada | -0.2% | British Columbia through Vancouver, Ontario, and Quebec through Montreal, with national spillover | Short term (≤ 2 years) |

| Wildfire-Driven Fiber Access Tightness | -0.2% | British Columbia, Alberta, and northern Quebec | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Virgin Fiber, OCC, And Energy Cost Volatility

Input cost swings remain the most persistent operational restraint for the Canada containerboard market because virgin fiber, recovered fiber, and energy each move through different cost cycles. Canfor Pulp said in March 2026 that its British Columbia operations were facing persistent challenges in accessing economically viable fiber, and the company recorded an impairment charge of CAD 106.5 million (USD 78 million) in its fourth-quarter 2025 results. OCC prices eased by December 2025 after the earlier spike, but the swing from extreme highs to sharp year-over-year declines still highlights the planning risk for mills that buy into spot markets. Energy remains another major pressure point because mill economics can change quickly when electricity costs are less competitive. Irving Paper closed half of its Saint John operations in February 2025, citing uncompetitive industrial electricity rates, underscoring how energy pricing can reshape regional capacity decisions. Producers with self-generation or long-term power advantages are better placed to absorb volatility than mills that rely more heavily on external energy supply.

Competition From Reusable Plastic Totes and Flexible Formats

The Canada containerboard market also faces substitution pressure from reusable plastic container systems and from lighter flexible mailer formats in selected use cases. Returnable plastic container programs are expanding in grocery and fresh produce distribution because retailers can reduce dunnage use and lower spoilage rates in some routes. In e-commerce, paper mailers, padded kraft envelopes, and thin-wall protective formats are taking a portion of the small-parcel volume that once defaulted to corrugated boxes. The Canada Plastics Pact said flexible mono-material structures are advancing into uses previously served by rigid plastics and corrugated, confirming that format competition is widening rather than narrowing. That means producers need to compete on total performance, including burst strength, print quality, moisture resistance, and logistics efficiency, instead of relying on price alone. Mills that keep investing in lightweight, high-strength linerboard and fluting grades are more likely to defend their share than suppliers focused on heavier commodity grades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Virgin Fiber Held the Lead While Recycled Fiber Scaled Faster

Virgin fibers held 62.5% of Canada's containerboard market share in 2025, and that leadership reflected the technical demands of export-grade kraft linerboard and industrial corrugated uses. These applications often require higher burst strength, ring crush, and edge-crush performance than single-pass recycled grades can consistently deliver. Canada’s softwood resource base in British Columbia, Quebec, and New Brunswick gives mills a long-fiber advantage that remains important for fresh produce, protein export, and automotive parts packaging. That performance profile kept virgin-fiber grades central to the Canada containerboard market, where load-bearing and transit protection remain the first buying criteria.

At the same time, recycled fibers are projected to grow at a 5.3% CAGR from 2026 to 2031, making them the fastest-expanding material segment in the Canada containerboard market. Ontario and Quebec recovery systems are improving local OCC availability, giving recycled-fiber mills a more stable sourcing base than they had under more export-sensitive collection patterns. Kruger announced a CAD 16 million (USD 11.7 million) recycling hub in Trois-Rivières in October 2025 to secure an annual supply of 450,000 tonnes of OCC for its containerboard operations.[2]Kruger Inc., “Kruger Invests USD 16M in Trois-Rivières to Consolidate Its Recycling Operations and Make Mauricie a Circular Economy Hub,” Kruger Inc., kruger.com Its Wayagamack carbon capture project also became operational from 2026 and captures up to 5 tonnes of CO2 per day for reuse in paper manufacturing, which adds an efficiency and sustainability advantage for buyers seeking lower-emission packaging inputs.

By Product Type: Kraftliners Led on Performance While Flutings Advanced on Lightweighting

Kraftliners accounted for 55.4% of the Canada containerboard market in 2025, making them the largest segment. Their position rests on heavy-duty export corrugated, cold-chain food packaging, and industrial shipping formats where outer-layer strength is critical. Canadian uncoated kraft liner exports to the United States reached USD 298 million in 2024, indicating that premium-performance grades continued to enjoy stable demand in cross-border converting markets. Testliners occupied a broad middle position between premium virgin grades and more recycled-heavy formats, especially in consumer goods, retail-ready packaging, and foodservice corrugated.

Flutings are forecast to expand at a 5.7% CAGR through 2031, making them the fastest-growing type segment in the Canada containerboard market. Lightweighting is increasing the proportion of fluting in each corrugated design to reduce fiber use without sacrificing box strength. E-commerce box optimization also supports faster fluting demand because right-sized parcel formats rely on efficient single-wall and single-face constructions that need strong medium performance. Domtar’s 2025 sustainability report said its capital choices will increasingly include sustainability-focused R&D criteria by 2026, pointing to more formal investment in grade development rather than commodity-only production logic. That shift gives fluting a stronger long-term role in the Canada containerboard market as converters seek lower basis weights with stable flat crush performance.

By End User: Food And Beverage Anchored Demand While Industrial Usage Rose Faster

Food and beverage accounted for 44.7% of the Canadian containerboard market in 2025, making it the largest end-user segment by a clear margin. The main support came from Canada’s large food processing base, export-oriented agriculture, and the widespread use of retail-ready corrugated display formats across grocery channels. Agriculture and Agri-Food Canada said food and beverage processing generated 18.2% of total manufacturing sales, which helps explain why this segment provides a durable volume foundation. Food safety and traceability requirements also keep virgin-fiber kraftliner important in packaging for meat, produce, dairy, and other regulated shipments.

Industrial end use is projected to grow at a 5.3% CAGR from 2026 to 2031, making it the fastest-rising demand block in the Canada containerboard market. Growth is tied to manufacturing packaging for automotive parts, machinery, electronics, construction materials, and resource-linked shipments, all of which need durable corrugated protection. As supply chains move closer to Canadian end markets, some packaging efficiencies tied to overseas pallet formats become less relevant, potentially increasing corrugated use per shipped unit. Consumer goods remain another large channel through retail distribution and e-commerce fulfillment, while healthcare and specialty shipping add smaller but rising volumes.

Geography Analysis

Ontario and Quebec together accounted for around 75% of corrugated output, placing the center of Canada's containerboard market share in the country’s main manufacturing and consumer corridors. Ontario benefits from dense industrial activity around Greater Toronto and Hamilton, where automotive, electronics, and food processing create steady demand for corrugated products. Ontario also completed its Blue Box EPR transition on January 1, 2026, and Circular Materials said the system now serves 383 municipalities and 12 First Nations communities, supported by new facilities in Cambridge and Greater Napanee. Those facilities can handle close to 30% of Ontario’s blue box volume and separately sort corrugated fiber, improving local feedstock access for recycled mills. This local fiber base reduces exposure to export-driven OCC swings and supports a more stable operating environment within the Canada containerboard market.

Quebec remains the other major production center because it combines strong mill infrastructure with lower hydroelectric power costs than many other provinces. Vancouver port and rail congestion added another constraint in 2025, with on-dock footage reports showing more than 185,000 feet of import rail containers at Centerm and Deltaport and some containers idle for more than 7 days.[3]Vancouver Fraser Port Authority, “Daily Import Rail On-Dock Footage Reports,” Vancouver Fraser Port Authority, portvancouver.com Kruger’s Trois-Rivières mill and Cascades’ facilities in Kingsey Falls, Lachute, and other locations give the province a broad operating base across recycled and virgin grades. British Columbia remains critical for fiber origin and export-grade production, but supply conditions have tightened as sawmill curtailments reduced chip availability and pushed up fiber costs.

Atlantic Canada and the Prairie provinces play different roles in the Canada containerboard market size structure. The project is expected to lift annual kraft pulp capacity from 335,000 tonnes to 575,000 tonnes and make the mill energy self-sufficient at up to 145 MW. The Prairie provinces are more important as demand centers because agricultural exports, food processing, and resource activity generate corrugated demand without matching local mill concentration. Alberta’s EPR system is expected to enter Phase 2 in October 2026, which should widen recovered-fiber collection and gradually improve OCC availability in a region that long depended on westbound supply flows.

Competitive Landscape

The Canada containerboard market is moderately concentrated at the mill level because a small group of vertically integrated producers controls most domestic capacity, while converting and box-making remain far more fragmented. Cascades, Kruger, and Irving Pulp and Paper together form the core of domestic mill supply, but downstream corrugators and regional box makers include a wider field of operators across Ontario, Quebec, and Atlantic Canada. That split means pricing power is stronger upstream than downstream, especially when supply conditions tighten after mill closures or transport disruptions. The resulting structure gives the Canada containerboard market a concentrated production base without producing the kind of near-monopoly conditions seen in more consolidated materials categories. It also means converters have less room to absorb cost moves when mills become more disciplined on pricing and asset use.

Cascades has focused on portfolio simplification and balance-sheet repair rather than broad capacity addition. In early 2026, the company agreed to sell its Richmond, British Columbia, corrugated packaging facility to Crown Paper Group for CAD 65.5 million (USD 48.0 million) and said the proceeds would support debt reduction.[4]Cascades Inc., “Cascades Reports Results for the Fourth Quarter and Full Year 2025,” Cascades Inc., newswire.ca It also entered into a long-term strategic partnership with Solifor on April 1, 2026, to optimize forest assets in Quebec and improve the economics of fiber supply. Kruger has taken a different route through continued capital deployment, including the Trois-Rivières recycling hub and a government-backed CAD 333 million (USD 243.8 million) investment linked to its Wayagamack diversification project in May 2026. These moves show that the Canada containerboard market is being shaped by stronger asset discipline at one end and targeted reinvestment at the other.

Technology and sustainability credentials are also becoming more visible points of competition in the Canada containerboard market. Kruger’s Wayagamack carbon capture system, operational from 2026, is the first in North American paper manufacturing to capture CO2 for reuse in the production process. Atlantic Packaging’s New Forest Mill said in April 2026 that it had reached close to 85% overall equipment effectiveness and used an anaerobic digester to convert wastewater byproducts into methane for on-site energy reuse. Irving’s Project NextGen adds another strategic example because it combines production expansion with renewable energy self-sufficiency, which can strengthen long-run operating resilience.

Canada Containerboard Industry Leaders

Mondi plc

Cascades Inc.

Kruger Inc.

Smurfit Westrock plc

Canadian Kraft Paper, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: The Government of Canada announced a CAD 35 million (USD 25.6 million) Strategic Response Fund investment in Kruger Inc.'s Wayagamack Mill in Trois-Rivières, Quebec, supporting the first plastic-free, chemical-free, biodegradable paper material production line for finished wipe products in North America.

- April 2026: Cascades Inc. entered a long-term strategic partnership with Solifor on April 1, 2026, to optimize its forest assets in Quebec, strengthening its fiber supply base as part of ongoing efforts to improve operational cost structure and reduce exposure to spot-market fiber volatility.

- February 2026: Kruger Energy began construction of the Saint-Paul-de-Montminy wind farm in Quebec as part of its plan to expand aggregate renewable energy capacity from 650 MW to 993 MW by 2028, further reducing the carbon intensity of its containerboard manufacturing operations.

- October 2025: Kruger Inc. announced a CAD 16 million (USD 11.7 million) investment in a new 1-million-square-foot recycling facility in Trois-Rivières, Quebec, to consolidate its OCC collection and storage operations.

Canada Containerboard Market Report Scope

The scope of the report includes an analysis of the Canada containerboard market, covering production, consumption, and trade. Containerboard is the paperboard used primarily for the manufacture of corrugated boxes and packaging materials. The study examines market trends, key drivers, challenges, and opportunities within the industry, providing insights into the supply chain, competitive landscape, and forecasted growth during the study period.

The Canada Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End User (Food and Beverage, Consumer Goods, Industrial, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End Users |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End User | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End Users |

Key Questions Answered in the Report

What is the current and forecast value of the Canada containerboard sector?

The Canada containerboard market size was USD 2.5 billion in 2025 and is estimated at USD 2.7 billion in 2026. It is forecast to reach USD 3.4 billion by 2031 at a 4.81% CAGR.

Which material segment leads demand in Canada?

Virgin fibers led with 62.5% share in 2025 because export-grade kraft linerboard and industrial corrugated formats still require stronger burst and edge-crush performance.

Which product type is growing the fastest in corrugated packaging in Canada?

Flutings are projected to grow at a 5.7% CAGR through 2031. Lightweighting and box optimization for e-commerce are raising the share of fluting in right-sized corrugated designs.

Why do food and beverages remain the biggest end-user category?

Food and beverage held 44.7% share in 2025 because Canada’s food processing sector is large, export oriented, and dependent on transit-ready and retail-ready corrugated packaging.

How are EPR systems changing the recovered fiber supply in Canada?

Ontario’s full producer responsibility model in 2026 and Quebec’s high collection rates are making the domestic OCC supply larger and more predictable. That lowers exposure to volatile export-sensitive spot markets.

What are the main risks producers are facing over the next few years?

The main risks are fiber and energy cost volatility, substitution from reusable plastic totes and flexible formats, and logistics disruption across rail and port corridors, especially in British Columbia and central Canada.

Page last updated on: