China Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 24.90 Billion |

| Market Size (2026) | USD 25.83 Billion |

| Market Size (2031) | USD 31.82 Billion |

| Growth Rate (2026 - 2031) | 4.26% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Containerboard Market Analysis by Mordor Intelligence

The China containerboard market size is projected to be USD 24.9 billion in 2025, USD 25.83 billion in 2026, and reach USD 31.82 billion by 2031, growing at a CAGR of 4.26% from 2026 to 2031. The China containerboard market is holding steady amid growth, as parcel shipping volumes remain very large and paper-based packaging is gaining policy support across the express and consumer goods channels. Demand is also staying resilient because logistics-led box consumption creates a volume base that helps the China containerboard market absorb weak pricing periods better than many other paper categories. Large producers are responding through inland expansion, higher-grade kraftliner output, and deeper control over fiber supply, which is changing the structure of competition in the China containerboard market. At the same time, persistent overcapacity and raw material cost swings are limiting margin recovery, so growth in the China containerboard market is likely to remain measured rather than rapid. That balance between structural demand support and margin pressure will continue to shape investment, product upgrades, and regional capacity decisions across the China containerboard market through 2031.

Key Report Takeaways

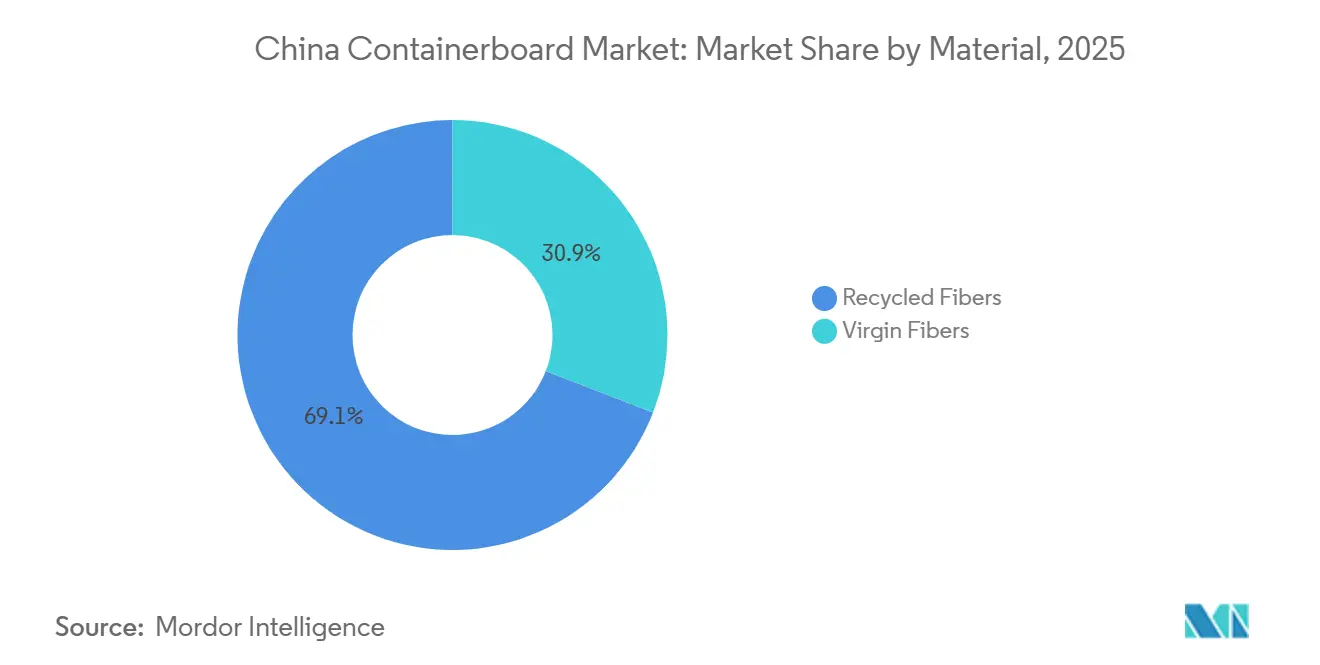

- By material, recycled fibers captured 69.14% of the China containerboard market share in 2025.

- By product type, the China containerboard market size for the kraftliners segment is forecast to advance at a 4.81% CAGR through 2031.

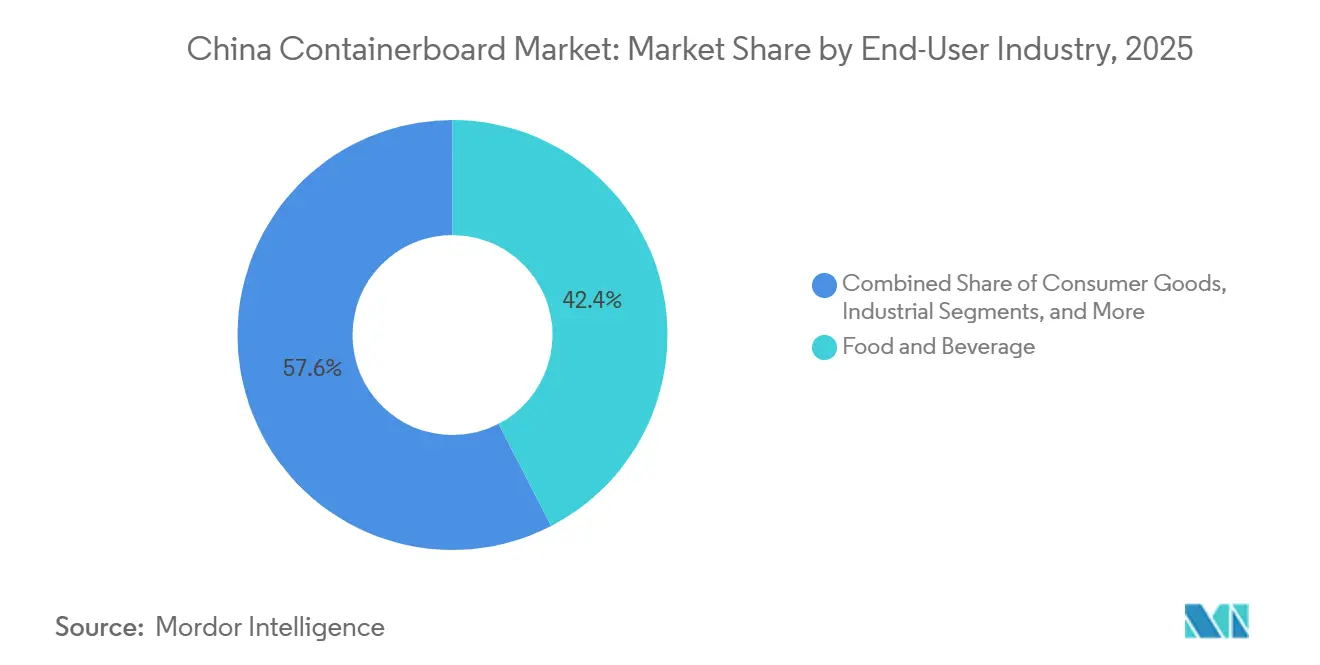

- By end-user industry, food and beverage captured 42.41% of the China containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce And Parcel Delivery Expansion | +1.4% | National, concentrated in East and South China logistics hubs | Short term (≤ 2 years) |

| Food And Beverage Packaging Intensity | +0.8% | National, strongest in Yangtze River Delta and Pearl River Delta consumption zones | Medium term (2-4 years) |

| Plastic-Substitution And Green Packaging Regulation | +0.6% | National, leading in coastal provinces with established green certification infrastructure | Medium term (2-4 years) |

| Premiumization Toward Higher-Performance Containerboard | +0.4% | East and South China export-manufacturing clusters, with spillover into inland markets | Medium term (2-4 years) |

| Direct-From-Origin Shipping Needs Stronger Board | +0.2% | Inland and agricultural-origin provinces including Henan, Sichuan, and Yunnan | Long term (≥ 4 years) |

| Inland Parcel Growth Rebalances Mill Footprints | +0.2% | Central and Western China including Chongqing, Henan, and Hubei | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce And Parcel Delivery Expansion

E-commerce remains the single strongest driver of demand for the China containerboard market because parcel movement is now embedded in daily consumption across urban and rural China. China’s express network handled 175 billion parcels in 2024, making it the world's first for the 11th straight year.[1]State Council of the People’s Republic of China, “State Council Order No. 806, Amended Provisional Regulations on Express Delivery,” State Council of the People’s Republic of China, gov.cn The amended Provisional Regulations on Express Delivery took effect on June 1, 2025, and pushed service quality and packaging durability into a firmer regulatory framework. That policy direction favors sturdier corrugated formats and supports a more reliable base of box demand for the China containerboard market. Corrugated demand from the express sector is on track to exceed 9 million tons in 2026, indicating that logistics demand is still rising even as mill pricing remains under pressure. The demand base is also spreading into lower-tier counties, widening the reach of the China containerboard market beyond traditional coastal manufacturing centers.

Food And Beverage Packaging Intensity

Food and beverage remains the largest demand center in the China containerboard market, accounting for 42.41% of end-user share in 2025 and still serving the broadest mix of packaging needs. The category is no longer driven only by shipment volume, because fresh produce, prepared meals, dairy, and beverage distribution all require more stable box performance than standard low-specification transport packaging. Cold-chain distribution is driving higher moisture resistance, stacking strength, and surface quality, raising the value profile of the board used in the Chinese containerboard market. China’s GB 4806.8 food safety framework limits the use of recycled fiber in certain primary food-contact applications, redirecting part of premium food packaging demand toward virgin-fiber and coated grades.[2]Ministry of Justice of the People’s Republic of China, “GB 45186-2024, Mandatory Standard on Excessive Express Packaging,” Ministry of Justice of the People’s Republic of China, moj.gov.cn That shift is helping mills with certified material and compliance-ready product lines win stronger positions with major food brands in the China containerboard market. It also means that product mix improvement is being driven by compliance and performance needs, not just by higher shipment counts.

Plastic-Substitution And Green Packaging Regulation

The move from plastic to paper-based formats has become a durable policy driver for the China containerboard market, as it is now tied to formal compliance rather than broad policy messaging. GB 45186-2024, the mandatory national standard on excessive express packaging, will take effect on July 1, 2026, and raises the pressure to reduce wasteful formats and improve recoverability. The National Development and Reform Commission’s action plan for greener express packaging also supports recyclable designs and discourages mixed-material structures that make fiber recovery harder.[3]National Development and Reform Commission, “Action Plan for Green Transformation of Express Packaging,” National Development and Reform Commission, ndrc.gov.cn By the end of 2025, 248 packaging products had received green certification, indicating that commercial adoption is already ahead of full implementation timelines. That matters for the China containerboard market because brand owners now have a clearer route to shift toward fiber-based secondary packaging without waiting for another policy cycle. The result is a steadier demand pull across express, FMCG, and retail chains in the China containerboard market.

Premiumization Toward Higher-Performance Containerboard

Premiumization is becoming one of the clearest strategic responses to margin pressure in the China containerboard market. Nine Dragons Paper reported kraftliner revenue of RMB 18.93 billion (USD 2.63 billion) in FY2026 H1, a 5.5% increase from the prior period.[4]Nine Dragons Paper (Holdings) Limited, “Interim Results Announcement for the Six Months Ended 31 December 2025,” Nine Dragons Paper, ndpaper.com That performance shows that a higher-grade board is still finding demand even in a market where commodity pricing remains volatile. Export-oriented consumer goods makers continue to ask for stronger burst strength, better print surfaces, and more consistent performance, which keeps lifting quality expectations across the China containerboard market. Cold-chain shipping and cross-border fulfillment add to that demand because box failure in transit creates direct return costs for brands and platforms. Mills that cannot upgrade forming, pressing, coating, or fiber quality are therefore losing ground to scale producers that can offer premium grades more reliably in the China containerboard market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Overcapacity And Price Competition | -0.7% | National, most acute in East and South China capacity clusters | Short term (≤ 2 years) |

| Fiber And Energy Cost Volatility | -0.6% | National, with stronger exposure at coal-dependent inland mills and OCC-dependent coastal mills | Medium term (2-4 years) |

| Dry-Pulp Import Scrutiny Disrupts Low-Cost Fiber | -0.3% | Coastal import-dependent mills and major South and East China ports | Short term (≤ 2 years) |

| Packaging Reduction Lowers Fiber Intensity Per Parcel | -0.2% | National, concentrated in express channels and modern retail packaging | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Overcapacity And Price Competition

Persistent overcapacity remains the main structural restraint on the China containerboard market because supply additions have continued to outpace real demand absorption. Capacity reached 38.19 million tons in 2025, while output stood at 28.2 million tons, which kept utilization in the 70-80% range across the sector. That mismatch left average industry net margins at 2.3% and kept many producers under pressure even when shipment volumes were stable. Around 140 small and medium production lines were shut or converted in 2025, but that still represented only a partial response to the scale of excess supply in the China containerboard market. Beijing’s anti-innovation language points to a policy desire to curb destructive price competition, but pricing relief in the China containerboard market will still depend on slower new capacity additions over multiple investment cycles. Until that happens, the China containerboard market is likely to remain volume-supported but margin-constrained.

Fiber And Energy Cost Volatility

Fiber and energy volatility continue to weigh on the China containerboard market because recycled-fiber mills still depend heavily on OCC and remain exposed to sudden procurement changes. OCC accounts for 60-70% of production costs at most recycled-fiber mills, meaning even short-lived cost spikes can quickly shift mill economics. The benchmark OCC price reached CNY 1,668 per ton (USD 230 per ton) on May 18, 2026, and multiple mills raised procurement prices by CNY 20-30 per ton (USD 2.8-4.2 per ton) within a single week. China’s tighter scrutiny of dry-milled recycled pulp imports in October 2025 also stranded 3,000-4,000 containers at ports, which showed how quickly fiber disruptions can hit coastal producers in the China containerboard market. On the energy side, mills with cleaner power sourcing or stronger internal efficiency are in a better position than mills that still rely on higher-cost, more volatile inputs. The result is a widening cost gap across the China containerboard market, especially between large integrated producers and smaller spot-fiber buyers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fiber Leads, While Virgin Fiber Gains Strategic Weight

Recycled fibers held 69.14% of the China containerboard market share in 2025, which kept this material base clearly in the lead. That position came from China’s deep OCC collection system and the long-established production infrastructure built around recycled fiber processing. Large mills in the Yangtze River Delta and Pearl River Delta still benefit from scale, converter proximity, and lower transport complexity for recovered paper flows, which supports the cost logic of this part of the China containerboard market. The recycled segment also fits the needs of high-volume testliner and fluting output, where consistent throughput matters more than premium pricing. This explains why recycled fiber remains the backbone of the China containerboard industry, even as margins in commodity grades stay under pressure.

Virgin fibers are projected to grow at a 4.68% CAGR through 2031, making them the fastest-growing material category in the China containerboard market. Food-contact rules, export-grade packaging requirements, and stronger specifications in cold-chain distribution are all lifting the role of virgin-based grades across the China containerboard market. China’s GB 4806.8 framework supports that shift because it limits the use of recycled fiber in certain primary food-contact applications. Nine Dragons Paper is also targeting an additional 2.5 million tons of chemical pulp capacity across Chongqing, Tianjin, Beihai, and Dongguan, which shows how major players are building upstream support for this higher-value material mix. The result is a more divided China containerboard industry, where one tier focuses on scale-driven recycled grades and another moves toward virgin-fiber kraftliners and coated products with better pricing power.

By Product Type: Testliners Hold Scale, While Kraftliners Lift Value Growth

Testliners captured 45.43% of the China containerboard market in 2025, making them the leading product type by volume. Their position is tied to the economics of OCC-based production and to China’s very large corrugated-box converting network, which still consumes standard containerboard grades at scale. Flutings remain closely linked to the same supply chain because they serve as the corrugating medium and are often produced at the same mills. This leaves both product groups highly exposed to the overcapacity cycle in the China containerboard market, especially where mills compete mainly on price. Smaller producers that remain concentrated in commodity testliners and flutings have fewer tools to improve margins without fresh capital spending.

Kraftliners are forecast to grow at a 4.81% CAGR through 2031, which gives them the strongest growth profile among product types in the China containerboard market. Buyers are shifting toward kraftliners because cold-chain, branded-goods shipping, and cross-border fulfillment all place greater weight on burst strength, printability, and consistency. Premium board, therefore, carries a more visible commercial case in the Chinese containerboard market, especially when damaged packaging leads to returns, waste, and reputational cost for brand owners. This change also affects procurement behavior because large customers increasingly want stable grade performance at scale rather than the lowest possible ton price. Over time, that will keep pulling growth within the China containerboard market toward producers that can meet specification-heavy demand more reliably.

By End-User Industry: Food And Beverage Anchors Volumes, While Consumer Goods Advances Faster

Food and beverage retained a 42.41% share in 2025, making it the largest end-user segment in the China containerboard market. The segment draws on a broad mix of demand, including fresh produce, processed foods, dairy, beverages, and prepared meals, giving it a broader customer base than any other customer group. That diversity helps stabilize shipments in the China containerboard market because demand is not dependent on a single product category. It also underscores the value of grade consistency, as cold-chain and moisture-sensitive applications require stronger board performance. As food distribution models become more specialized, the largest end-user pool in the Chinese containerboard market is also becoming more specification-led.

Consumer goods are projected to expand at a 4.89% CAGR through 2031, making it the fastest-growing end-user category in the China containerboard market. Personal care, apparel accessories, electronics accessories, and home goods are all shifting more of their outer packaging toward paper-based formats for direct-to-consumer distribution. Platform standards and brand sustainability commitments are reinforcing that change, which means volume growth and material substitution are working together in this part of the China containerboard market. Producers that can supply print-ready, stronger, and more uniform board are better placed to serve these branded channels. This growth path also supports the wider move in the China containerboard market toward better-grade packaging rather than simple tonnage expansion.

Geography Analysis

East China accounted for 53.4% of national output in 2025, giving the region the largest geographic position in the China containerboard market. Jiangsu, Zhejiang, and Shanghai benefit from a dense chain of converters, packaging manufacturers, and downstream consumer brands, which keeps sourcing and delivery distances relatively short within this part of the China containerboard market. The Yangtze River Delta remained under-utilized in 2025, with utilization reported at 68.5%, highlighting the strong concentration of national overcapacity in this region. Energy and environmental enforcement also tightened operating conditions, and mill shutdowns in eastern provinces began to serve as a slow capacity filter, even if they did not yet solve the broader balance-of-power problem. That means East China still sits at the center of the China containerboard market, but it is also where competitive and regulatory pressure is felt most directly.

South China held 25% of national containerboard capacity and accounted for 15% of corrugated paper output, making it the second-largest production center in the China containerboard market. The Pearl River Delta’s export-heavy manufacturing base continues to support demand for kraftliner and higher-performance testliner grades, which makes South China one of the clearest premium segments in the China containerboard market. Lee and Man Paper filed for a CNY 720 million (USD 99.3 million) technical upgrade at its Guangdong facility, which shows that leading producers still see value in upgrading South China capacity. Nine Dragons’ Dongguan site also received approval for a wood-fiber substitution and kraft liner expansion plan, which reinforces South China’s role in the higher-grade side of the China containerboard market.

Inland China is the fastest-changing regional pocket in the China containerboard market, as Henan, Sichuan, Chongqing, and Hubei are attracting new investment tied to rising consumption and agricultural e-commerce. Henan attracted CNY 4.2 billion (USD 592 million) in containerboard investment during 2025. Nine Dragons also announced a CNY 6 billion (USD 834 million) Chongqing smart-factory containerboard complex in August 2025, which marked one of the clearest inland commitments in the China containerboard market. Better access to consumption clusters, farm-origin shipping flows, and local raw materials is slowly reshaping mill location logic across the China containerboard market.

Competitive Landscape

The China containerboard market remained structurally fragmented in 2025, with the top 5 producers accounting for around 25-30% of total capacity, leaving more than 70% of supply with small- and medium-sized mills. Even so, Nine Dragons Paper remained the clear scale leader in the China containerboard market with total paper capacity exceeding 25 million tons. Nine Dragons reported FY2026 H1 revenue of RMB 37.22 billion (USD 5.18 billion) and net profit of RMB 2.21 billion (USD 307 million), which showed how strongly a premium-grade mix can support earnings in the China containerboard market. The leading group is largely following the same playbook, with deeper pulp integration, more inland diversification, and greater focus on kraftliners and specialty grades. The main open opportunity in the China containerboard market remains in higher-precision and functional-coated formats, where capability is still limited relative to commodity testliner supply.

Mid-tier and smaller mills face a narrower strategic path in the China containerboard market because cost gaps are widening and commodity grades offer little room for pricing recovery. Technology and process control are becoming more important, since better OCC sorting, fiber utilization, and basis-weight control can make a visible cost difference even when selling prices are soft. Nine Dragons’ April 2026 environmental filing for Phase 1 of its Chongqing green-pulp project showed that the company is still making long-cycle upstream investments rather than relying only on short-term price recovery in the China containerboard market. Its Dongguan wood-fiber substitution upgrade follows the same logic and deepens its premium product position in South China.

Compliance is also likely to push the China containerboard market toward stronger players, as GB 45186-2024 imposes greater burdens on mills that cannot support recyclable, specification-ready packaging formats. Lee and Man Paper’s Guangdong PM7 upgrade filing and Chongqing fiber-sorting plan show that established producers are still investing in quality improvement and fiber resilience rather than standing still. Shanying International’s 3.6 million ton packaging paper project in Suzhou shows that capacity competition has not disappeared, even among mid-tier players. The result is that the China containerboard market is likely to remain fragmented in volume terms, even as a smaller group of scale producers captures a larger share of premium and compliance-led demand.

China Containerboard Industry Leaders

Nine Dragons Paper (Holdings) Limited

Lee & Man Paper Manufacturing Limited

Shanying International Holdings Co., Ltd.

Shandong Sun Paper Industry Joint Stock Co., Ltd.

Zhejiang Jingxing Paper Joint Stock Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: OCC procurement prices at multiple Chinese mills rose CNY 20-30 per ton in a single week, with the benchmark OCC price reaching CNY 1,668 per ton (USD 230 per ton) on May 18, 2026, reflecting tightening domestic secondary-fiber supply amid import restrictions and higher logistics costs.

- April 2026: Nine Dragons Paper published the Environmental Impact Assessment for Phase 1 of its Chongqing green-pulp project, CNY 3.5 billion (USD 483 million) in capital expenditure for 700,000 tons per year of green chemical pulp, advancing the company's fiber self-sufficiency strategy.

- April 2026: Nine Dragons' Dongguan facility received EIA approval for a wood-fiber substitution upgrade incorporating 500,000 tons of natural wood fiber, 250,000 tons of mechanical fiber, and 620,000 tons of kraft liner capacity, deepening the company's premium product portfolio in South China.

- March 2026: Shanying International Holdings announced a 3.6 million ton packaging paper project in Suzhou, representing one of the largest single capacity-addition commitments by a mid-tier producer in 2026, targeting growing demand in East China corrugated conversion.

China Containerboard Market Report Scope

The China Containerboard Market encompasses the production, distribution, and consumption of containerboard materials used in manufacturing corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The market is driven by the increasing demand for sustainable, lightweight, and durable packaging solutions.

The China Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current and forecast value of the China containerboard market?

The China containerboard market was valued at USD 24.9 billion in 2025, reached USD 25.83 billion in 2026, and is forecast to reach USD 31.82 billion by 2031 at a 4.26% CAGR.

Which material type leads demand in China containerboard?

Recycled fibers led with a 69.14% share in 2025 because China has a deep OCC collection and recycled-board production base.

Which product category is growing the fastest through 2031?

Kraftliners are the fastest-growing product type with a 4.81% CAGR, supported by cold-chain shipping, cross-border fulfillment, and better print and strength requirements.

Which end-user segment contributes the most demand?

Food and beverage held the largest end-user share at 42.41% in 2025 because it spans fresh produce, processed foods, dairy, beverages, and prepared meals.

Why does overcapacity remain a major issue for producers?

Capacity reached 38.19 million tons in 2025 against output of 28.2 million tons, which kept utilization in the 70-80% range and held margins down across many mills.

Which regions matter most for production and investment?

East China remains the largest production base, South China stays central for premium export-linked grades, and inland provinces such as Henan and Chongqing are attracting new capital and capacity.

Page last updated on: