Argentina Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

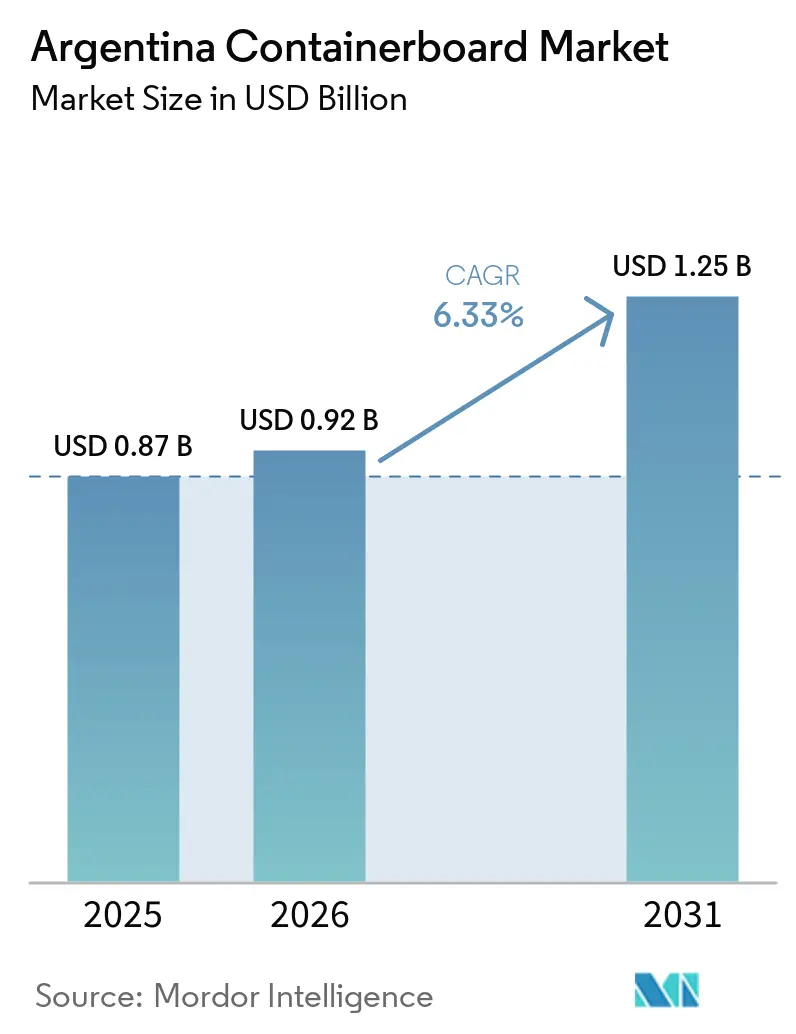

| Base Year Market Size (2025) | USD 0.87 Billion |

| Market Size (2026) | USD 0.92 Billion |

| Market Size (2031) | USD 1.25 Billion |

| Growth Rate (2026 - 2031) | 6.33% CAGR |

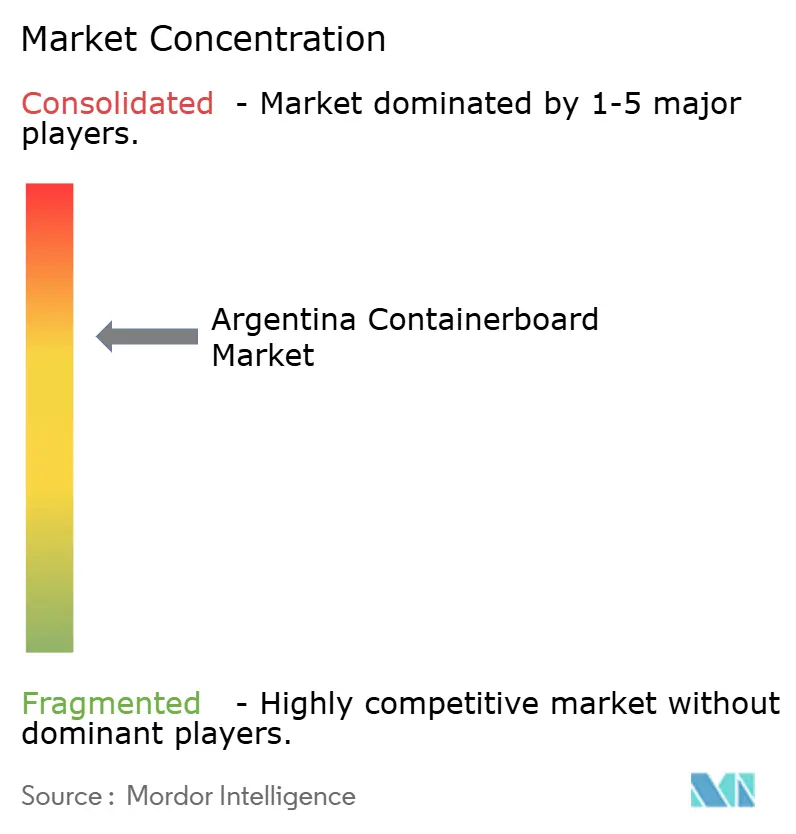

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Argentina Containerboard Market Analysis by Mordor Intelligence

The Argentina containerboard market was valued at USD 0.87 billion in 2025 and is forecast to reach USD 1.25 billion by 2031, at a CAGR of 6.33% over 2026-2031. The Argentina containerboard market is emerging from the deep contraction seen in 2023 and 2024, when fiscal tightening, peso depreciation, and lower real wages reduced packaging demand and kept mill utilization well below installed capacity. The current recovery matters because it is tied to broader macroeconomic stabilization, which is gradually restoring purchasing power for both households and companies. At the same time, the market's operating model has changed, with import liberalization, weaker urban recycling flows, and a wider e-commerce footprint altering both supply conditions and demand patterns. Competitive positioning now depends more clearly on fiber security, mill-converter integration, and service reliability than it did during the downturn. These conditions are creating room for growth, but they are also keeping pressure on commodity grades where imported board continues to set a firm price reference.

Key Report Takeaways

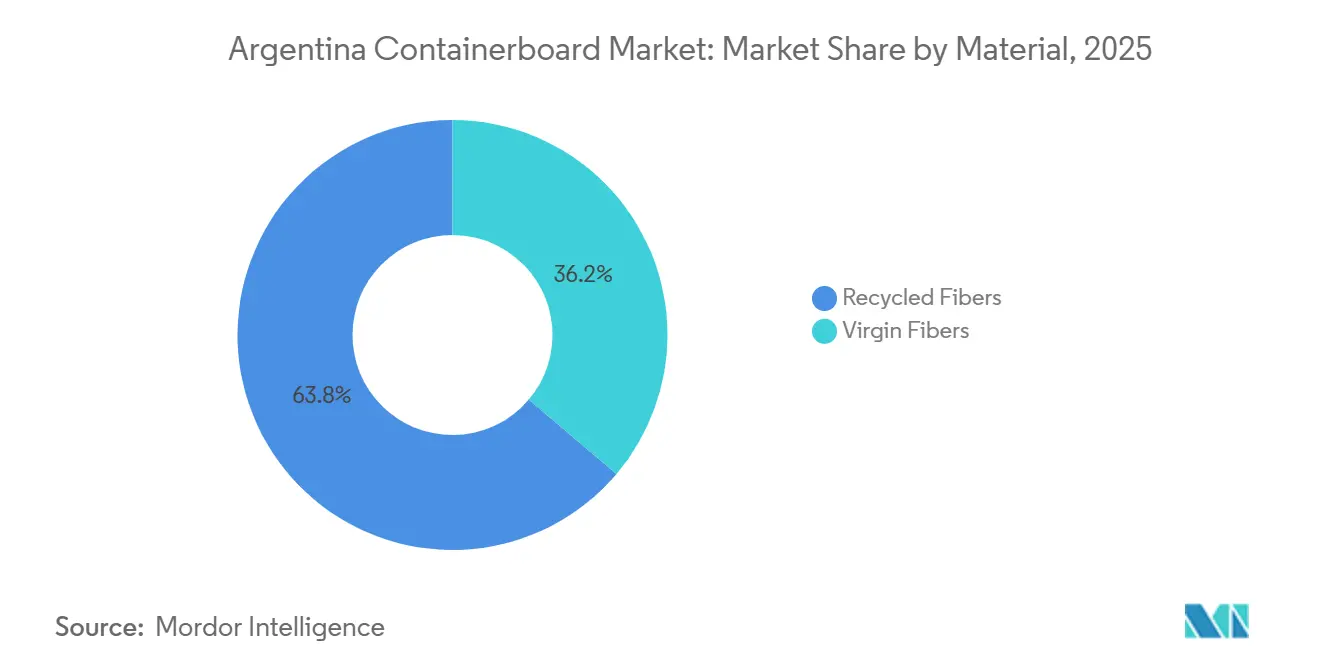

- By material, recycled fibers captured 63.82% of the Argentina containerboard market share in 2025.

- By product type, the Argentina containerboard market size for the kraftliners segment is forecast to advance at a 6.92% CAGR through 2031.

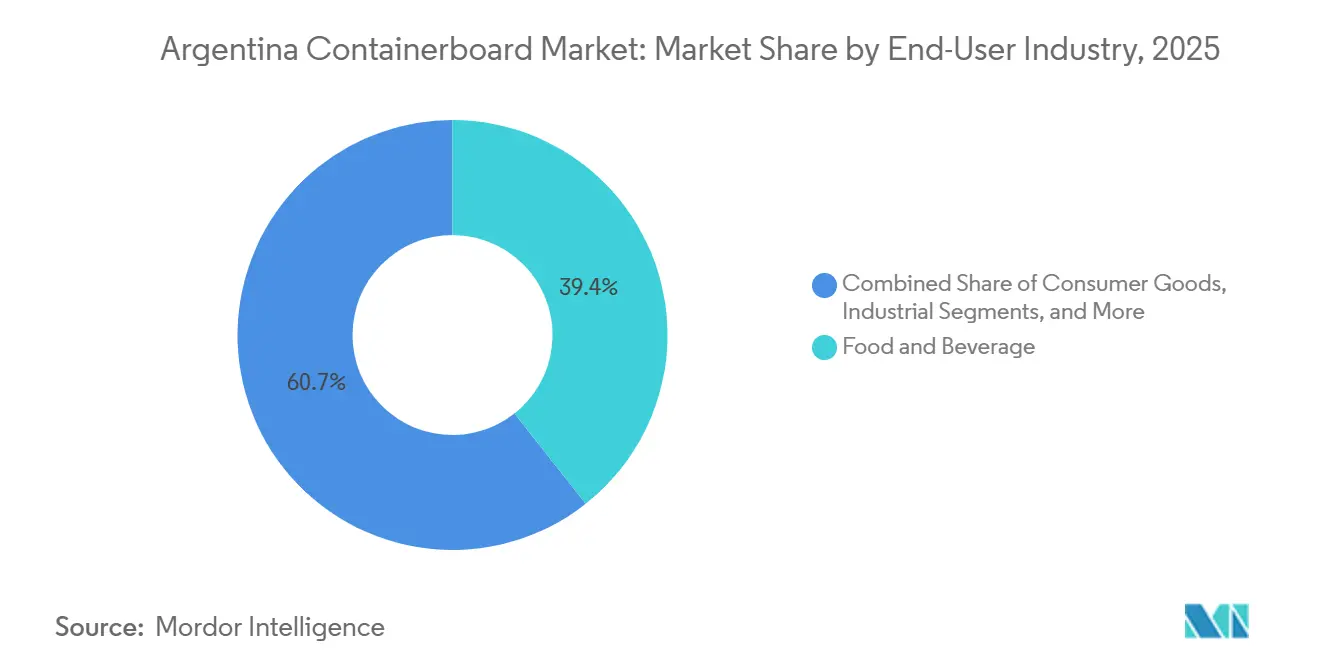

- By end-user industry, food and beverage captured 39.35% of the Argentina containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Argentina Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recovery In Domestic Containerboard Demand | +1.8% | National, with early gains in Greater Buenos Aires, Córdoba, and Santa Fe | Short term (≤ 2 years) |

| Food And Beverage Packaging Resilience | +1.4% | National, with concentration in Buenos Aires province and NOA agro-industrial corridors | Medium term (2-4 years) |

| Expansion Of E-Commerce Fulfillment Networks | +1.1% | AMBA core, with spill-over to Patagonia and Cuyo via air and road logistics | Medium term (2-4 years) |

| Shift Toward Recycled And Circular Packaging | +0.9% | National, with early intensity in Buenos Aires Metropolitan Area cooperatives | Long term (≥ 4 years) |

| OCC Processing Capacity Additions | +0.6% | Greater Buenos Aires and Littoral provinces | Medium term (2-4 years) |

| Remote-Corridor Parcelization From Air Logistics Expansion | +0.3% | Patagonia, NOA, and Cuyo - historically underserved delivery corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Recovery In Domestic Containerboard Demand

Argentina's demand cycle for containerboard reached its low point in 2024, when fiscal austerity and weak spending reduced activity across converters, retailers, and industrial customers.[1]Asociación Argentina de Agentes de Carga Internacional, “El Gobierno Desplegó 138 Medidas Para Abrir Importaciones Y Redefinir El Esquema Comercial,” AAACI, aaaci.org.ar The rebound in 2025 was tied to the return of deferred purchasing by food processors, retailers, and consumer goods companies as inventories began to normalize. The recovery has not been uniform across grades because commodity testliner still faces firm price competition from Brazilian and regional imports entering through more open trade channels. In contrast, domestically integrated virgin-fiber grades have recovered faster because Arcor's Cartocor division combines forestry assets, linerboard capacity, and converter reach, thereby reducing exposure to imported supply. Export duty removal for the paper and cardboard value chain from January 2025 also supported the Argentina containerboard market by lowering tax friction for export-facing converters and improving cost conditions across the packaging chain.[2]Diario La Opinión de Rafaela, “Smurfit Westrock Argentina Alcanzó El 100% De Energía Renovable En Sus Operaciones Durante Diciembre De 2025,” Diario La Opinión de Rafaela, diariolaopinion.com.ar

Food And Beverage Packaging Resilience

Food and beverage remains the most stable demand base in the Argentina containerboard market because a large part of Argentine output moves through export channels where corrugated packaging is a required logistics input. That stability is stronger than domestic consumer sentiment because shipments of fresh produce, proteins, dairy, wine, and commodity crops still require dependable secondary packaging. The provisional Mercosur-EU trade arrangement that took effect in February 2026 widened the export pipeline for Argentine agro-industrial goods and strengthened the need for export-grade corrugated formats. Argentina's Decree 35/2025 also reduced domestic certification barriers for food imports and exports from countries with equivalent sanitary standards, which broadened product flows that depend on corrugated secondary packaging. This matters for grade mix because food-contact compliance is easier to document with virgin-fiber kraftliner than with OCC-derived alternatives, which supports faster growth for kraft grades in the Argentina containerboard market.

Expansion Of E-Commerce Fulfillment Networks

E-commerce has become a structural demand engine for the Argentina containerboard market because it is increasing both packaging volumes and the number of delivery points that require corrugated formats.[3]Cámara Argentina de Comercio Electrónico, “Estudio Anual de Comercio Electrónico 2025,” cited by María Julieta Rumi in La Nacion, lanacion.com.ar Argentina's online retail billings reached USD 24 billion in 2025, while units sold rose 28% and the buyer base reached 25.1 million, which directly lifted demand for shipping cases and secondary boxes. The regional pattern is especially important because AMBA still leads, but Patagonia, NOA, Cuyo, and the Littoral are contributing a rising share of new order flows. Mercado Libre, Mirgor's Innova Logistic, and Aerolíneas Argentinas launched commercial air cargo services to Ushuaia, Bariloche, Neuquén, and Trelew in May 2026, with daily route capacity of 15,000 to 16,000 shipments and delivery windows cut to under 48 hours. That new corridor is creating demand for small-format corrugated cases that can withstand the stresses of air transport and support faster parcel handling. Mercado Libre's USD 3.4 billion logistics plan for Argentina in 2026 further supports this wider packaging footprint through storage centers, last-mile stations, and intermediate cargo nodes.

Shift Toward Recycled And Circular Packaging

Sustainability programs are driving demand for recycled-content packaging in Argentina's containerboard market, which already relies heavily on recovered fiber.[4]Smurfit Westrock, “Liners, South America,” Smurfit Westrock, us.smurfitwestrock.com Smurfit Westrock reported that 85% of its packaging solutions in Argentina use post-consumer recycled fibers, demonstrating how deeply recycled inputs are already embedded in commercial packaging offerings. The company also reached 100% renewable electricity coverage across its Argentine operations in December 2025 through agreements with 360Energy, Energeia, and DQD Energy, which strengthens the link between recycled packaging and lower-emission operations. The main limitation is not customer interest, but feedstock quality and supply consistency, because Argentina recovered only 6% of the recyclable waste stream in 2025, according to Conarcoop. This gap between sustainability targets and OCC availability gives mills an advantage, allowing them to invest in sorting and pre-processing rather than depend on spot collection volumes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy Tariff Normalization And Utility Cost Inflation | -0.9% | National, most acute in energy-intensive mill operations in Buenos Aires province and Santa Fe | Short term (≤ 2 years) |

| Weak Mass-Market Consumption Recovery | -0.7% | National, with greatest drag in interior provinces lagging Buenos Aires metro recovery | Short term (≤ 2 years) |

| Cartonero Network Contraction And OCC Collection Dislocation | -0.5% | Greater Buenos Aires, Córdoba, and Rosario - cities with highest cooperative density | Medium term (2-4 years) |

| Import Liberalization And Price Pressure On Domestic Mills | -0.4% | National, concentrated among commodity testliner and fluting producers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Energy Tariff Normalization And Utility Cost Inflation

Electricity cost normalization is a direct cost restraint for the Argentina containerboard market because paper machines run with continuous drying and pressing loads. ENRE resolutions finalized in April and May 2025 approved an initial 20% transport tariff increase for multiple transmission companies and then set up monthly real adjustments through December 2025. Distribution tariff adjustments for EDENOR and EDESUR were also structured to continue through November 2027, extending the effect well beyond the first recovery phase. The framework uses an index with 67% weighting to IPIM and 33% to IPC, which preserves real utility costs even when broader inflation slows. That matters because mills are facing higher energy bills at the same time that imported board is limiting how much domestic producers can pass through to customers. The five-year investment schedules approved through April 2030 show that this is a structural shift in operating costs rather than a short-lived adjustment.

Weak Mass-Market Consumption Recovery

Consumer purchasing power has improved more slowly than macro stabilization, which is limiting the pace of recovery in packaging demand tied to mass-market goods. An INDEC industrial survey cited in AAACI's February 2026 trade analysis found that 53.5% of industrial firms still saw insufficient domestic demand as their main production constraint. The slowdown is not evenly spread because Buenos Aires metro chains are recovering faster than interior provinces where income repair has been weaker. E-commerce helps offset part of that weakness, but it tends to favor smaller and lighter boxes rather than the bulk transit formats that lift tonnage more quickly. As a result, order growth is supporting the Argentina containerboard market, but the product mix is keeping the recovery more gradual than headline parcel counts might suggest.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fiber Dominates, Virgin Grades Gain Pace

Recycled fibers accounted for 63.82% of the Argentina containerboard market in 2025, reflecting a production base built around urban OCC recovery and recycled pulp processing rather than plantation forestry at the national scale. Smurfit WestRock said that 85% of its local packaging solutions used post-consumer recycled fibers, confirming the central role of recovered paper in the commercial packaging supply. Arcor's Cartocor also remains one of South America's largest recycled paper producers by volume, reinforcing the depth of recycled integration in Argentina's containerboard industry. This recycled base gives the Argentina containerboard market scale and cost familiarity, but it also ties producers to the quality and consistency of local collection systems.

Virgin fibers are projected to be the fastest-growing material segment, with a 6.79% CAGR from 2026 to 2031, despite starting from a smaller base. Arcor-Cartocor leads domestic virgin-fiber capacity through 23,000 hectares of forestry assets and integrated kraft linerboard manufacturing, which gives it a different cost and availability profile from pure recycled players. Dependence on imported pulp for complementary virgin grades has also become easier to manage following Resolution 5730/2025, which streamlined digital import procedures under the VUCEA framework. The core tension in the Argentina containerboard market is that recycled fibers still dominate current output, while export-oriented packaging and compliance-heavy applications are driving demand toward virgin grades faster.

By Product Type: Testliner Leads, Kraftliner Gains Export Momentum

Testliner held 42.61% of the Argentina containerboard market in 2025, underscoring the continued dominance of OCC-based grades in domestic retail and consumer goods packaging. Delivered cost still drives a large share of converter decisions in these domestic applications, which is why testliner remains the leading grade in the current mix. Fluting also remains an important layer in corrugated structures, and Smurfit Westrock's South American production network supports both testliner and fluting supply into its converting system. This keeps the Argentina containerboard market anchored in a broad recycled-grade base even as the mix begins to shift at the margin.

Kraftliners are the fastest-growing product type, with a projected 6.92% CAGR from 2026 to 2031, as export packaging and multinational FMCG requirements favor higher burst strength and better moisture resistance. Those technical advantages matter for fresh produce, protein, and dairy shipments where handling stress and humidity control are more demanding. Arcor-Cartocor is well-positioned in this part of Argentina's containerboard industry because its forestry and linerboard assets support supply security for virgin-fiber grades. The premium growth rate for kraftliner suggests that the Argentina containerboard market is gradually moving toward higher-value export-serving grades rather than away from recycled grades altogether.

By End-User Industry: Food And Beverage Anchors, Consumer Goods Accelerates

Food and beverage accounted for 39.35% of the Argentina containerboard market in 2025, providing the market with a stable demand floor linked to agricultural and food export flows. Corrugated packaging in this end-user base is less sensitive to household spending because it sits inside non-discretionary transit and handling requirements. That structural stability is one reason the Argentina containerboard market began recovering even as parts of mass consumption remained weak. Food-contact requirements also keep a floor under virgin-fiber demand because documentation and purity control are easier to maintain than with unverified recycled grades.

Consumer goods are the fastest-growing end-user segment, with a 7.04% CAGR from 2026 to 2031, supported by the continued expansion of e-commerce fulfillment in the Argentine containerboard market. CACE's 2025 annual report recorded 253 million purchase orders, unit sales growth of 28%, and 25.1 million active buyers, all of which directly support demand for small-format corrugated shippers and mailer-style boxes. Industrial and other end-user segments remain more stable and are supported by the large-investment framework introduced in 2024, which is drawing capital toward extractive, energy, and manufacturing activities with industrial packaging needs. The result is that the Argentina containerboard market is seeing its fastest end-user growth in consumer-oriented shipping formats, while food and beverage continues to carry the largest absolute share of demand.

Geography Analysis

AMBA accounted for 52% of Argentina's total e-commerce billing in 2025, which made it the strongest demand center for corrugated shipping activity and a major anchor for the Argentina containerboard market. The Buenos Aires Metropolitan Area and the Buenos Aires province-Santa Fe corridor also host the main integrated production assets, including Smurfit Westrock's facilities in Bernal, Coronel Suárez, Laferrere, and Sunchales, and Celulosa Argentina's mills in Capitán Bermúdez and Zárate. That concentration creates a self-reinforcing packaging corridor with dense end-user demand, better access to recovered paper, and shorter service distances to the largest retail and consumer goods networks. Celulosa Argentina's disruptions through 2024 and into much of 2025 tightened domestic supply in this corridor and increased reliance on imports.

Outside the AMBA-Littoral axis, the Argentina containerboard market is supported by several regional demand pockets with different packaging needs. NOA relies on citrus, sugarcane, tobacco, and mining, which create a steady demand for functional, cost-competitive corrugated formats. Cuyo is shaped by wine and olive oil exports, where wet-strength performance and print quality can justify a higher grade mix. Patagonia has historically been the most supply-constrained corridor because road transport from Buenos Aires-area mills added both cost and lead time to each shipment. The pilot launched in September 2025 and the commercial air cargo rollout in May 2026 changed that pattern by creating a new regional need for small, light, fast-turn packaging formats that were previously limited.

Within South America, Argentina remains secondary to Brazil in containerboard production volume, which matters because Brazilian supply now exerts stronger pricing pressure across the region. Smurfit Westrock's February 2026 medium-term plan still identified Argentina as 1 of its 3 primary corrugated markets in South America, which confirms the country's strategic value despite macro volatility. The provisional Mercosur-EU arrangement improves the medium-term export backdrop for Argentine agro-industrial goods, which supports packaging demand across export corridors. In the near term, the 138-measure trade liberalization program leaves domestic mills more exposed to lower-cost imported board, especially in commodity testliner and fluting grades.

Competitive Landscape

The Argentina containerboard market is led by 2 integrated mill-converter groups, Arcor through Cartocor and Smurfit Westrock, while the rest of the field is made up of regional converters that compete mainly on location, customer service, and delivery speed. Smurfit Westrock's February 2026 medium-term plan described South America as its fastest-growing and highest-margin region and named Argentina among its 3 leading corrugated markets there. The company is also raising switching costs with packaging design tools such as ShelfSmart.AI and SupplySmart Analyzer, which smaller domestic converters are unlikely to match at the same scale. In May 2026, Smurfit Westrock added another competitive layer by opening its first Experience Center for Argentina and Chile in Buenos Aires with ISTA testing and co-creation capabilities for food, agro, retail, and e-commerce customers. It also confirmed 100% renewable electricity coverage across its Argentine operations in December 2025, which strengthens its sustainability offer for multinational clients.

Arcor-Cartocor competes from a different position in the Argentina containerboard market by combining eucalyptus and pine forestry, kraft linerboard production, and 18 converting plants certified to ISO 9001 and ISO 14001. That level of vertical integration gives it strong supply security for domestic food manufacturers and export customers that need consistent board quality. In March 2026, Arcor's Papel Misionero plant added new effluent containment infrastructure with a capacity of 20,000 m³, indicating that compliance investment is becoming part of competitive positioning as well. The most visible disruption came from Celulosa Argentina's preventive insolvency filing in September 2025 and the later acquisition by a new ownership group, which removed a key domestic paper supplier from normal operations before capacity restarted.

This operating gap created room in the Argentina containerboard market for both established converters and imported Brazilian supply to contest displaced volumes. Regional independents such as Papelera del NOA, Papelera Entre Ríos, and Corrugadora Centro remain present, but higher energy costs and weaker scale economics are making their position harder to defend. Smurfit Westrock's FSC chain-of-custody coverage across South American mills also raises the sustainability bar for customers with stricter procurement audits. The result is a market where concentration is strongest at the integration level, and where the next round of competition is likely to center on fiber access, compliance credentials, and high-service packaging formats rather than on commodity volume alone.

Argentina Containerboard Industry Leaders

Arcor S.A.I.C.

Smurfit Westrock plc

Celulosa Argentina S.A.

Converpack de SPC S.A.

Corupel S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Mercado Libre, in partnership with Mirgor's Innova Logistic and Aerolíneas Argentinas, commercially launched air cargo delivery services to Patagonian destinations, Ushuaia, Bariloche, Neuquén, and Trelew, as part of a USD 3.4 billion logistics investment plan for Argentina in 2026. The service targets daily processing of 15,000 to 16,000 shipments per route, reducing delivery times from 1 week to under 48 hours and opening a new demand corridor for corrugated secondary packaging in a historically road-constrained region.

- May 2026: Smurfit Westrock inaugurated its first Experience Center for Argentina and Chile in Buenos Aires, joining a global network of over 25 such facilities. The center integrates AI-enabled ShelfSmart and SupplySmart packaging design tools, ISTA-certified laboratory testing, and co-creation environments to develop advanced corrugated packaging solutions with local customers across food and beverage, agro, retail, and e-commerce sectors.

- March 2026: Arcor Group's Papel Misionero plant in Puerto Leoni, Misiones, commissioned new environmental infrastructure, including effluent containment pools with a 20,000 m³ capacity, responding to an environmental compliance finding from 2024 related to Paraná River contamination. The investment reflects Arcor's commitment to ISO 14001-aligned environmental management across its packaging operations.

- February 2026: Smurfit Westrock published its Medium-Term Plan, classifying Argentina among the 3 primary corrugated markets in South America and targeting South American Adjusted EBITDA of USD 0.8 billion at a 28% margin by 2030 through organic growth and selective acquisitions. The filing confirms the company's position as the 1 corrugated supplier across the region.

Argentina Containerboard Market Report Scope

The Argentina Containerboard Market encompasses the production, distribution, and consumption of containerboard materials used in manufacturing corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The market is driven by the increasing demand for sustainable, lightweight, and durable packaging solutions.

The Argentina Containerboard Market Report is Segmented by Material (Virgin Fibers and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current size and future value of the Argentina containerboard market?

The Argentina containerboard market was valued at USD 0.87 billion in 2025 and is forecast to reach USD 1.25 billion by 2031, growing at a 6.33% CAGR over 2026-2031.

Which material segment leads demand in Argentina?

Recycled fibers led the market with a 63.82% share in 2025, reflecting the country's long-standing reliance on OCC collection and recycled pulp processing.

Which product grade is growing the fastest in containerboard demand?

Kraftliners are projected to grow at a 6.92% CAGR through 2031, supported by export packaging needs and stronger performance requirements in food and FMCG applications.

Why does food and beverage remain so important for packaging demand?

Food and beverage held 39.35% of demand in 2025 because agricultural and food exports require corrugated packaging regardless of swings in domestic consumer sentiment.

How is e-commerce changing corrugated packaging demand across Argentina?

E-commerce is expanding both volumes and geography, with 25.1 million buyers and strong unit growth in 2025 driving demand for small-format shipping boxes and broader last-mile packaging needs.

What are the main risks facing domestic mills through the forecast period?

The main risks are rising electricity costs under tariff normalization, uneven mass-market consumption recovery, weaker OCC collection quality, and stronger import pressure on commodity grades.

Page last updated on: