United States Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

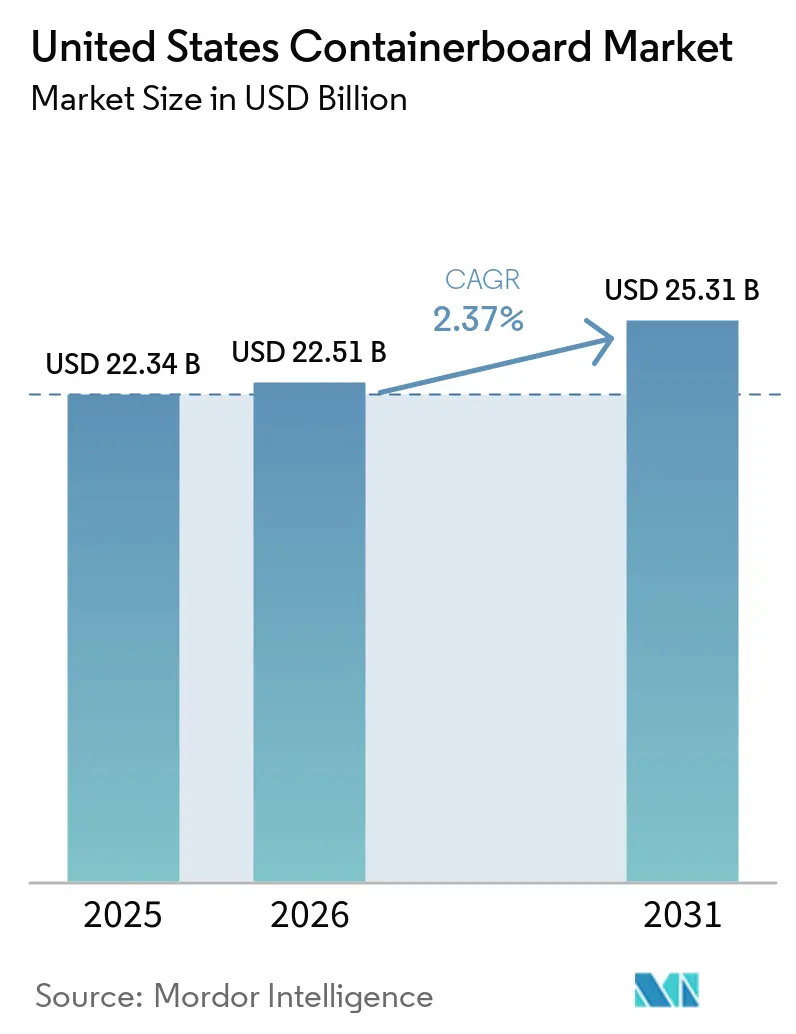

| Base Year Market Size (2025) | USD 22.34 Billion |

| Market Size (2026) | USD 22.51 Billion |

| Market Size (2031) | USD 25.31 Billion |

| Growth Rate (2026 - 2031) | 2.37% CAGR |

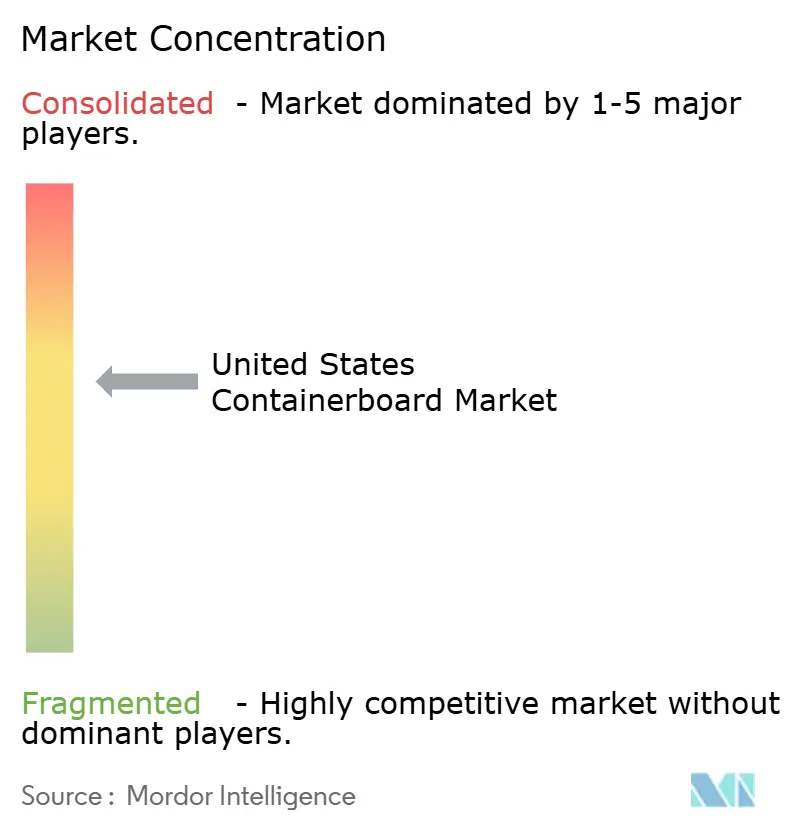

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Containerboard Market Analysis by Mordor Intelligence

The United States containerboard market size was valued at USD 22.34 billion in 2025 and estimated to grow from USD 22.51 billion in 2026 to reach USD 25.31 billion by 2031, at a CAGR of 2.37% during the forecast period 2026-2031. The United States containerboard market is entering a phase in which pricing power matters more than raw volume expansion. Capacity removals in 2025 tightened supply and pushed operating rates higher, improving the balance between mills and buyers. Corrugated packaging remains essential to domestic goods movement, so demand has held broadly even as some end uses have moved unevenly. The United States containerboard market is also being reshaped by recycled-content mandates, packaging redesign, and a steady shift toward lighter but stronger board grades. At the same time, larger integrated producers are gaining an advantage because they can manage fiber sourcing, compliance costs, and mill optimization more effectively than smaller converters.

Key Report Takeaways

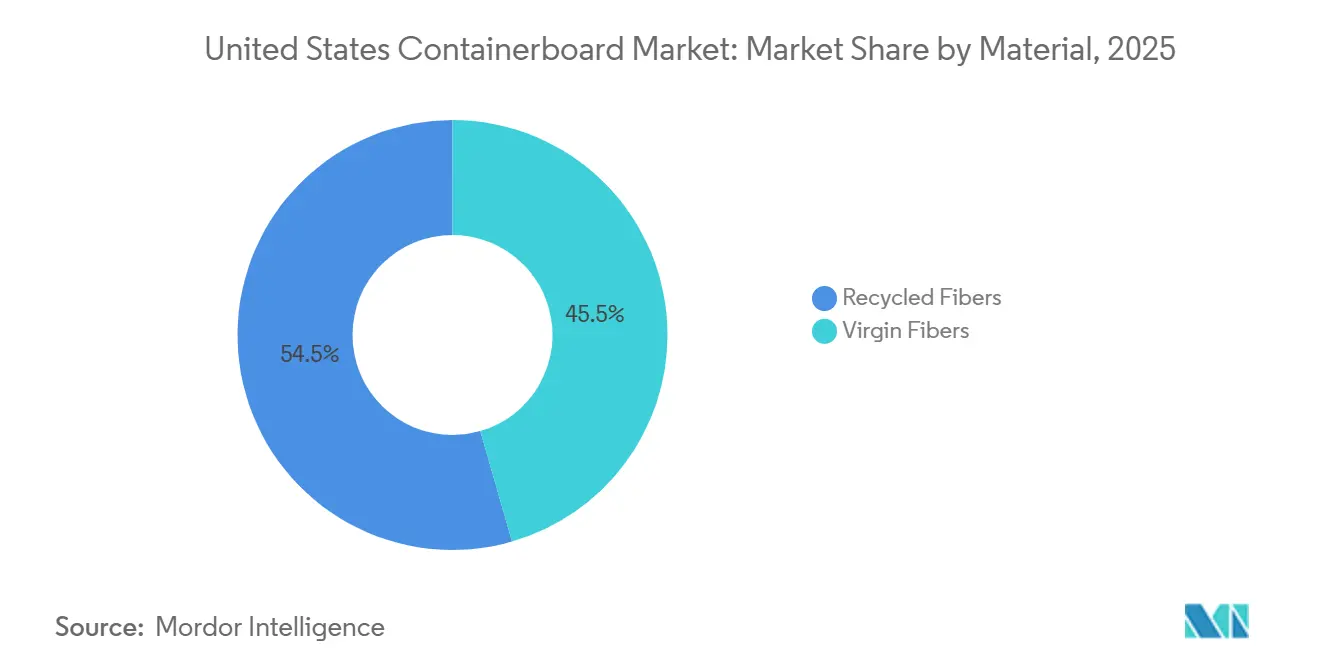

- By material, recycled fibers captured with 54.47% of the United States containerboard market share in 2025.

- By product type, the United States containerboard market size for flutings is projected to grow at a 3.24% CAGR to 2031.

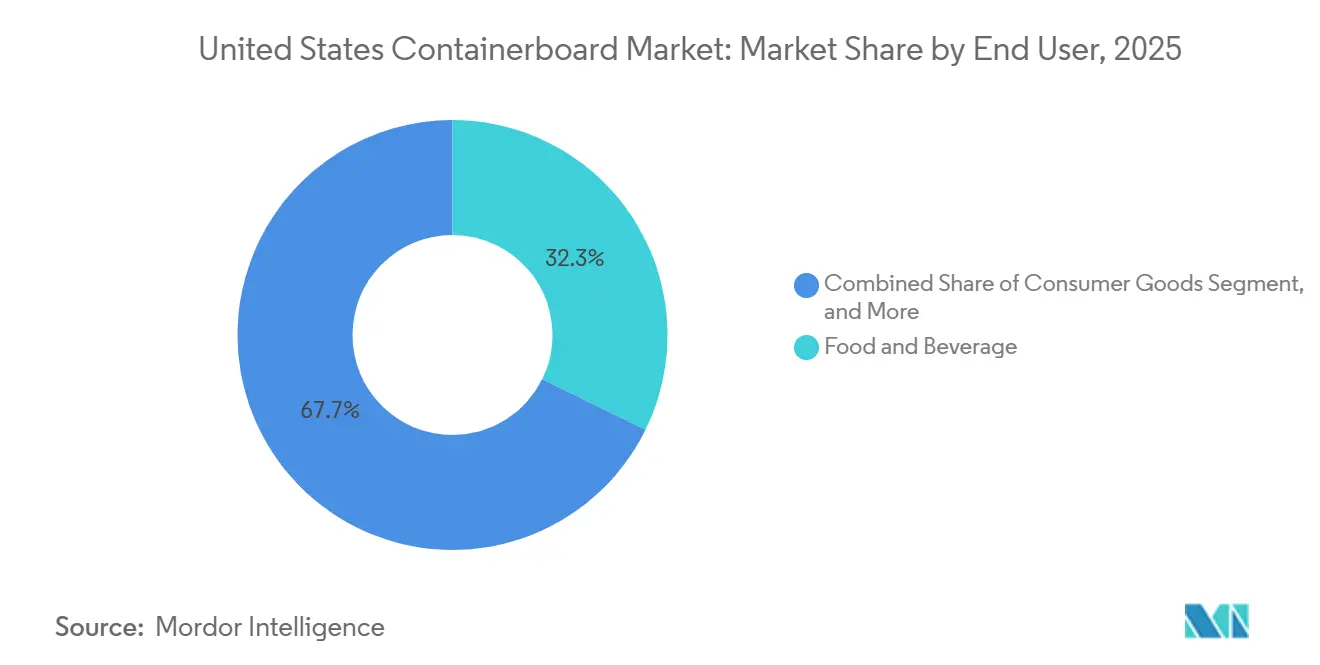

- By end user, food and beverage captured with 32.26% of the United States containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising E-commerce and Omnichannel Box Demand | +0.7% | National, with early gains concentrated in the Southeast, Southwest, and Pacific coastal fulfillment corridors | Medium term (2-4 years) |

| Growing Recycled-Content and Pauperization Mandates | +0.5% | California, Oregon, Colorado, the Northeast corridor, with spillover to national CPG supply chains | Medium term (2-4 years) |

| Stable Food and Beverage Shipment Demand | +0.4% | National, strongest in the Southeast, the Midwest agricultural belts, and the Gulf Coast processing hubs | Long term (≥ 4 years) |

| Capacity Rationalization: Tightening Industry Utilization | +0.3% | National, concentrated where legacy mills closed, including Georgia, Louisiana, and Washington | Short term (≤ 2 years) |

| Eco-Modulated EPR Fees Favoring Recyclable Corrugated Formats | +0.2% | California, Oregon, Colorado, Maine, Maryland, Minnesota, Washington, with multi-state spillover | Medium term (2-4 years) |

| Lightweight Recycled Liner Innovation Expanding Substitution | +0.2% | National, with early adoption in e-commerce hubs and automated fulfillment centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising E-Commerce and Omnichannel Box Demand

Online retail continues to support a broad demand floor for the United States containerboard market, even though parcel growth no longer converts into box demand on a one-to-one basis. Corrugated boxes still account for more than 90% of goods shipped in the country, keeping fiber-based transport packaging central to domestic commerce. The mix inside fulfillment networks is changing, with more die-cut formats, single-wall structures, and microflute designs replacing simpler runs. That shift favors producers who can supply stronger and lighter grades rather than just the commodity-grade medium. Rabobank noted in early 2026 that demand should remain broadly flat through late 2027, with e-commerce gains partly offset by parcel-level lightweighting.[1]Rabobank, “North America Containerboard Quarterly Q1 2026,” Rabobank, rabobank.com In the United States containerboard market, that means omnichannel demand is supporting plant utilization, while product mix is doing more of the work on margins.

Growing Recycled-Content and Pauperization Mandates

Brand owners are directing more packaging specifications toward paper-based formats, which is reinforcing demand for the United States containerboard market. Amazon removed 95% of plastic air pillows from North American fulfillment centers and replaced them with paper filler made from 100% recycled content, avoiding 15 billion plastic air pillows each year. That move shows how packaging redesign at one large shipper can alter fiber demand across broad supply chains. It also supports recycled-fiber grades, as post-consumer content is increasingly part of procurement requirements rather than a branding option. The United States containerboard market benefits from this shift because corrugated packaging already fits existing recovery systems and can more easily meet recyclability expectations than many competing materials. A related effect is that more paper-based packaging eventually returns to the OCC stream, which helps replenish recycled feedstock even as demand for recovered fiber rises.

Stable Food and Beverage Shipment Demand

Food and beverage remains the steadiest demand base in the United States containerboard market because shipment needs do not move closely with discretionary spending cycles. This end use supplies a dependable volume floor for mills and converters when industrial and consumer goods orders soften. Same-day grocery delivery and direct-to-consumer food distribution are also adding packaging needs that differ from traditional shelf-ready formats. That packaging requirement tends to favor heavier or coated board grades, which can improve the revenue mix even as tonnage grows slowly. In the United States containerboard market, this stable end use helps producers maintain firmer asset loading than the headline growth rate alone would suggest.

Capacity Rationalization Tightening Industry Utilization

Supply reduction became one of the clearest forces shaping the United States containerboard market during 2025 and into 2026. AF&PA reported that U.S. containerboard production declined 4% in 2025 versus 2024, while operating rates finished the year above 91%. That combination shows that mill closures and conversions tightened supply faster than demand weakened. Packaging Dive described the 2025 capacity pullback as the steepest single-year reduction on record in North America, which helped support new price hike announcements for 2026. For buyers, this means availability has become more disciplined and less dependent on broad macro conditions alone. In the United States containerboard market, tighter utilization has widened the gap between companies with efficient integrated systems and those with narrower regional footprints.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Flexible Mailers and Ships-in-Own-Container Substitution | -0.5% | National, concentrated in the West Coast, Northeast, and Southeast fulfillment corridors | Medium term (2-4 years) |

| OCC and Energy Cost Volatility | -0.4% | National, most acute for recycled fiber mills in the Southeast, the Midwest, and the Pacific Northwest | Short term (≤ 2 years) |

| PFAS-Free Barrier Qualification Costs in Food Applications | -0.3% | National, with early compliance requirements in California, Oregon, Colorado, Maine, and Minnesota | Medium term (2-4 years) |

| State-by-State EPR and Compliance Complexity | -0.2% | California, Oregon, Colorado, Maine, Maryland, Minnesota, Washington, phasing toward wider reach by 2029-2030 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Flexible Mailers and Ships-In-Own-Container Substitution

Flexible mailers and ship-in-own-container programs are reducing part of the box demand that would otherwise support the United States containerboard market. Amazon reported that corrugated boxes fell from 43% to 40% of deliveries while ship-in-own-container participation increased from 8% to 11%. The effect is most visible in small-parcel e-commerce, where padded mailers and product-ready packs can bypass the need for an additional corrugated box. This does not remove parcel demand from the system, but it does reduce the square footage per shipment. At the same time, the remaining corrugated shipments often require stronger, more specialized board, which partly offsets the lost volumes from the mix. Even so, the United States containerboard market faces a real ceiling on growth if major platforms continue shifting more qualified items into non-box or no-overbox formats.

OCC and Energy Cost Volatility

Cost instability remains a major operating restraint for the United States containerboard market, especially for recycled-fiber mills. Domestic OCC prices fell from USD 106 per short ton in June 2024 to USD 44 per short ton in November 2025 before stabilizing near USD 45 per short ton in January 2026. Recycling Today also highlighted sharp swings in the OCC and mixed paper markets in 2025, which disrupted margin assumptions across recovered fiber operations. On the energy side, the U.S. Energy Information Administration stated that Henry Hub natural gas prices averaged USD 3.52 per MMBtu in 2025, up 56% from 2024, and wholesale electricity prices also climbed across most trading hubs. Mills that depend on both purchased OCC and purchased power are subject to pressure from two volatile inputs at once. In the United States containerboard market, this cost pattern strengthens the relative position of integrated producers that can manage energy geography, recovered fiber access, and mill efficiency more tightly.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fibers Anchor Demand While Virgin Grades Hold Premium Roles

Recycled fibers held 54.5% of the United States containerboard market share in 2025 and are also projected to post the fastest CAGR of 3.4% through 2031. This position reflects the long build-out of OCC recovery, sorting, and mill systems across the country. The United States containerboard market has relied on that infrastructure for years, and recent brand-owner requirements for post-consumer content have further reinforced it. Capacity closures at older virgin-fiber assets also tightened the supply base for unbleached kraft grades and increased the relative weight of recycled production in the system. Producers such as Cascades, Kruger, Pratt Industries, and ND Paper have been investing in stronger recycled liner and medium offerings rather than staying confined to commodity grades. Cascades said its extra-high-performance linerboard uses 100% recycled fiber, including 90% post-consumer content, and is designed for lightweight, high-speed corrugating.[2]Cascades Inc., “Extra High-Performance Linerboard,” Cascades, cascades.com That product direction shows how the United States containerboard industry is pushing recycled material deeper into performance-sensitive uses.

Virgin fibers still matter in applications where surface quality, burst strength, and food-contact assurance remain harder to meet with recycled furnish alone. Premium kraftliner, export packaging, and some retail-ready formats continue to support a functional premium for virgin grades. The United States containerboard market still relies on virgin output for parts of the packaging mix where reliability and branding requirements are strict. Mordor Intelligence noted that 89% of North American corrugated output carried chain-of-custody certifications in 2024, up from 76% in 2023, which points to continued investment in certified virgin inputs as well as broader sustainability documentation. Georgia-Pacific also announced an USD 83 million expansion at its Palatka, Florida mill in 2025, which underlined ongoing capital support for kraft-based paper output. The result is a market where recycled fiber leads on scale and growth, while virgin fiber remains important in the premium end of the grade spectrum.

By Product Type: Kraftliners Keep the Largest Base While Flutings Gain from Lightweighting

Kraftliners accounted for 45.6% of the United States containerboard market in 2025, making them the largest segment. Their position comes from the steady need for strong outer liners with good printability and moisture performance. TAPPI noted that corrugated boxes underpin more than 90% of all goods shipped within the United States, which helps explain why liner demand stays central to box production. Testliners remain relevant as a lower-cost recycled option, but they face greater pricing pressure when new or converted recycled capacity enters the system. The United States containerboard market is therefore seeing a split between volume leadership in linerboard and faster technical evolution in lighter specialty grades. Mordor Intelligence stated that microflute grades accounted for 8% of International Paper's North American containerboard shipments in 2025, double the 2023 share, indicating that product diversification is moving beyond niche adoption. That shift supports higher-value liner and fluting combinations inside increasingly automated corrugating systems.

Flutings are forecast to expand at a 3.2% CAGR through 2031, making them the fastest-growing type segment in the United States containerboard market. Their growth is linked to single-wall e-commerce formats that depend on flute-profile efficiency to maintain stacking strength while reducing board weight. The Sustainable Packaging Coalition identified lightweighting as a key route for meeting both eco-modulated packaging fees and dimensional-weight shipping penalties. That trend pulls demand toward thinner but better-performing fluting grades and favors producers that can run lower basis weights at commercial scale. The United States containerboard industry is responding by moving beyond standard corrugating medium and toward engineered fluting that supports automated fulfillment and lower material use. EPA-linked waste reduction goals in the user draft also point to continued interest in lower basis-weight structures, which strengthens the long-run case for advanced fluting formats even when overall tonnage growth stays modest.

By End User: Food And Beverage Provides Stability While Industrial Builds Momentum

Food and beverage accounted for 32.3% of the United States containerboard market in 2025, making it the largest end-user segment. Its lead reflects the basic shipment needs for processed food, beverages, and produce, which persist even in weaker economic phases. The United States containerboard market depends on this segment as a reliable volume base because it is less exposed to discretionary demand shifts than industrial or general consumer goods. A 2025 comparative life-cycle analysis released by the Corrugated Packaging Alliance found that corrugated packaging performed 57-110% better than reusable plastic containers across several environmental measures, supporting continued adoption in food distribution systems. Certification requirements are also becoming more important, and that favors producers with documented fiber sourcing and established food-grade packaging capabilities. These conditions help explain why food and beverage remains the demand anchor of the United States containerboard market.

Industrial is projected to grow at a 2.9% CAGR through 2031, which makes it the fastest-growing end-user segment. That momentum is tied to manufacturing nearshoring, broader domestic distribution requirements, and the movement of heavier goods that often need stronger box formats. The United States containerboard market is benefiting from this pattern because industrial shipments usually require double-wall or triple-wall structures that support heavier loads and longer domestic transport routes. Consumer goods remain an important middle segment, but they face both an e-commerce tailwind and some substitution risk from ship-in-own-container models. Other end users, including agriculture, chemicals, and pharmaceuticals, contribute useful tonnage but do not match the growth pace of industrial demand. This leaves the United States containerboard market with a balanced end-user mix where food and beverage protects the base and industrial demand supplies the main incremental lift.

Geography Analysis

The United States containerboard market is organized around regions that combine mill capacity, converting assets, and dense freight activity. The Southeast, including Georgia, Alabama, Florida, Louisiana, and the Carolinas, has remained the core production zone because it combines integrated mills with a large corrugated converting base. The Gulf Coast and South Central states, including Texas, Arkansas, and Mississippi, form a second major supply node for retail and food distribution across the southern interior. AF&PA reported that national production fell 4% in 2025 while operating rates ended above 91%, and those tighter conditions were shaped in part by closures in Georgia and Louisiana.

The Pacific Northwest has seen one of the clearest structural changes in the United States containerboard market during 2026. Packaging Corporation of America reconfigured its Wallula, Washington, mill to a fully recycled linerboard and medium operation by the end of the first quarter of 2026, reflecting the region's high wood fiber and purchased power costs. International Paper then announced the acquisition of NORPAC in April 2026 for USD 360 million, adding West Coast containerboard capacity to address tighter paper availability in the region.[3]International Paper to Expand Containerboard Capacity with NORPAC Acquisition,” Packaging Insights, packaginginsights.comCalifornia is also becoming more influential because draft SB 54 rules published in May 2026 required producers to register with the Circular Action Alliance by June 1, 2026, which added another policy reason to favor recyclable fiber-based packaging.

The Midwest and Northeast play a different role in the United States containerboard market because they are larger as converting and consumption centers than as primary mill regions. The Midwest supports food processing, automotive flows, and general goods distribution, while the Northeast depends on dense urban delivery networks that sustain corrugated demand. EIA reported that regional natural gas prices in the Northeast rose sharply in 2025, which left energy-intensive mills there facing some of the highest cost pressure in the country. Pratt Industries' USD 92.5 million expansion in Rock Hill, South Carolina, announced in October 2025, also showed how the Mid-Atlantic and Southeast corridor remains attractive for recycled-fiber converting capacity close to OCC generation and major end users.

Competitive Landscape

The United States containerboard market is moderately concentrated at the production level, even though converting remains more fragmented. International Paper Company, Packaging Corporation of America, Georgia-Pacific, and Pratt Industries account for 60-65% of domestic containerboard capacity, giving the top tier clear influence over pricing and capacity discipline. That structure means competitive advantage comes from mill footprint quality, integration into corrugated conversion, and the ability to absorb compliance and fiber volatility. The United States containerboard market has become more consolidated after the Smurfit Kappa-WestRock combination and International Paper's acquisition of DS Smith reshaped the leading group within a short period. At the same time, mid-tier operators such as Pratt Industries, Cascades, Hood Container, New-Indy Containerboard, ND Paper, and Kruger remain relevant through regional positions and recycled-grade specialization.

Large integrated producers are following a value-over-volume approach in the United States containerboard market. They have focused on closing weaker assets, concentrating output in more efficient mills, and pursuing price increases where tighter supply supports them. Smurfit Westrock said in February 2026 that it was targeting adjusted EBITDA of USD 7 billion by 2030 and discretionary free cash flow of USD 14 billion over 2026-2030, based partly on a 1.6% annual North American growth assumption.[4]Katie Pyzyk, “Smurfit Westrock Unveils Medium-Term Plan to Accelerate Growth,” Packaging Dive, packagingdive.com Pratt Industries has taken a different route, expanding recycled-fiber capacity and corrugating assets to capture room created by legacy mill closures. That split in strategy shows how the United States containerboard market now rewards both scale discipline and selective expansion, depending on grade focus and geography.

White-space opportunity in the United States containerboard market is strongest in advanced barrier-coated board, lighter performance grades, and faster packaging design services. Smurfit Westrock has used AI-supported design tools and customer experience centers to shorten packaging development timelines and build more service-led relationships. Cascades and other recycled-grade suppliers are also pushing higher-performance linerboard, which narrows the historic gap between recycled and virgin offerings. Certification is now more of a baseline requirement than a selling point, because large consumer packaged goods buyers increasingly expect documented chain-of-custody coverage. Smaller digital and regional converters still have space in short-run and SKU-diverse work, but the overall direction of the United States containerboard market favors well-capitalized players with integrated systems and clearer access to recycled feedstock.

United States Containerboard Industry Leaders

International Paper Company

Smurfit Westrock plc

Packaging Corporation of America

Georgia-Pacific LLC

Graphic Packaging International LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Smurfit Westrock announced an additional USD 50 per ton containerboard price increase, effective June 2026, following a net USD 20 per ton first-quarter 2026 realization.

- April 2026: Packaging Corporation of America reported first quarter 2026 net sales of USD 2.4 billion, up from USD 2.1 billion in the first quarter of 2025, with total corrugated product shipments in the packaging segment rising 19.9%, including legacy corrugated operations achieving record daily shipment levels.

- March 2026: International Paper announced a USD 225 million greenfield box plant in Mississippi, scheduled for late-2027 startup, designed to serve same-day delivery infrastructure in the Southeast region.

- January 2026: Pratt Industries officially opened its 496,000-square-foot corrugating facility in Warner Robins, Peach County, Georgia, a USD 120 million investment producing corrugated boxes from 100% recycled containerboard sourced from Pratt's Conyers, Georgia mill.

United States Containerboard Market Report Scope

The scope of this report covers the United States containerboard market, including analyses of production, consumption, and trade of containerboard materials. Containerboard is the paperboard used primarily for the manufacture of corrugated boxes and packaging materials. The study examines market trends, drivers, challenges, and opportunities, providing insights into the industry's current state and future prospects.

The United States Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End User (Food and Beverage, Consumer Goods, Industrial, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End Users |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End User | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End Users |

Key Questions Answered in the Report

What is the current size of the United States containerboard market?

The United States containerboard market was valued at USD 22.34 billion in 2025 and stands at USD 22.51 billion in 2026, with a forecast of USD 25.31 billion by 2031.

What is driving growth in United States containerboard demand through 2031?

Growth is being supported by e-commerce demand, recycled-content mandates, stable food and beverage shipments, and tighter industry utilization after major capacity reductions.

Which material segment leads containerboard demand in the United States?

Recycled fibers lead with a 54.5% share in 2025 and are also the fastest-growing material segment, supported by established OCC recovery and stronger recycled liner innovation.

Which product type is growing fastest in United States containerboard?

Flutings are projected to grow at a 3.2% CAGR through 2031, as lightweight corrugated structures become increasingly important for automated fulfillment and parcel shipping.

Why are food and beverages so important to containerboard suppliers?

Food and beverage accounted for 32.3% of demand in 2025 and serves as the most stable shipment base because everyday consumption keeps box usage more consistent than cyclical end uses.

What are the main risks facing United States containerboard producers?

The main risks are substitution from flexible mailers and ship-in-own-container programs, along with sharp swings in OCC and energy costs that pressure recycled-fiber mill margins.

Page last updated on: