Philippines Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.12 Billion |

| Market Size (2026) | USD 2.21 Billion |

| Market Size (2031) | USD 2.77 Billion |

| Growth Rate (2026 - 2031) | 4.62% CAGR |

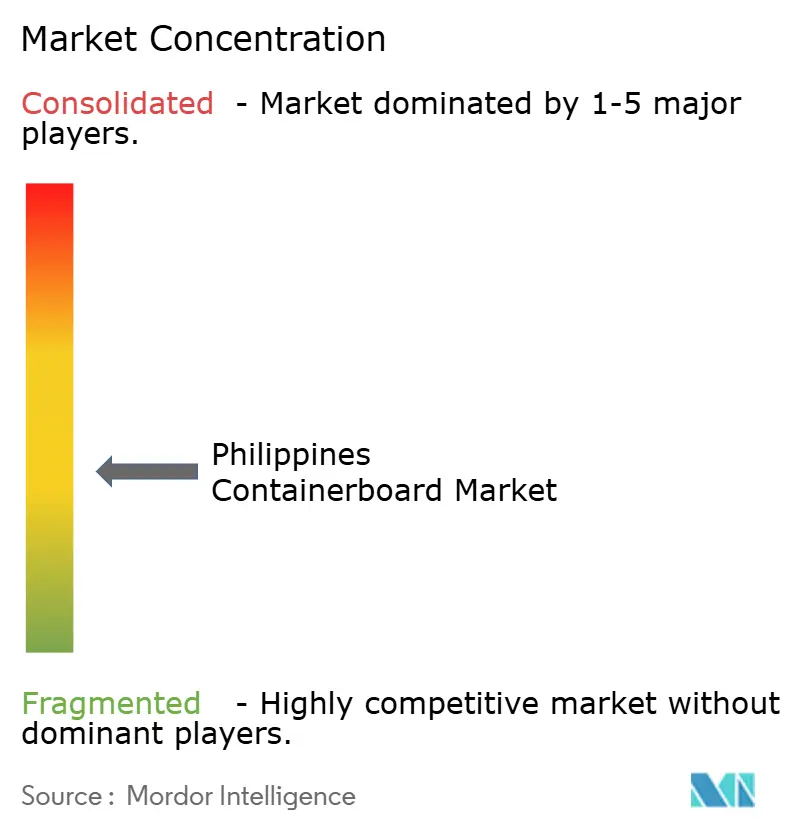

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines Containerboard Market Analysis by Mordor Intelligence

The Philippines Containerboard Market size is projected to expand from USD 2.12 billion in 2025 and USD 2.21 billion in 2026 to USD 2.77 billion by 2031, registering a CAGR of 4.62% between 2026 to 2031.

The Philippines containerboard market is supported by the country’s archipelagic trade structure because corrugated packaging remains the most practical protective format for inter-island movement of food, consumer goods, and industrial products. Domestic supply has some built-in resilience because local demand does not depend on a single end-use stream, and instead draws support from packaged food, online retail fulfillment, export manufacturing, and provincial distribution needs.

The Philippines containerboard market also reflects a structural raw material constraint, as local mills rely heavily on recycled fiber due to the absence of commercial-scale virgin pulp plantations, which makes wastepaper recovery policy and imported feedstock availability central to cost stability. Competition is uneven across the value chain, with upstream mill supply more concentrated than downstream box conversion, so pricing pressure tends to travel back toward converters while domestic mill utilization remains sensitive to import competition and energy costs.

Key Report Takeaways

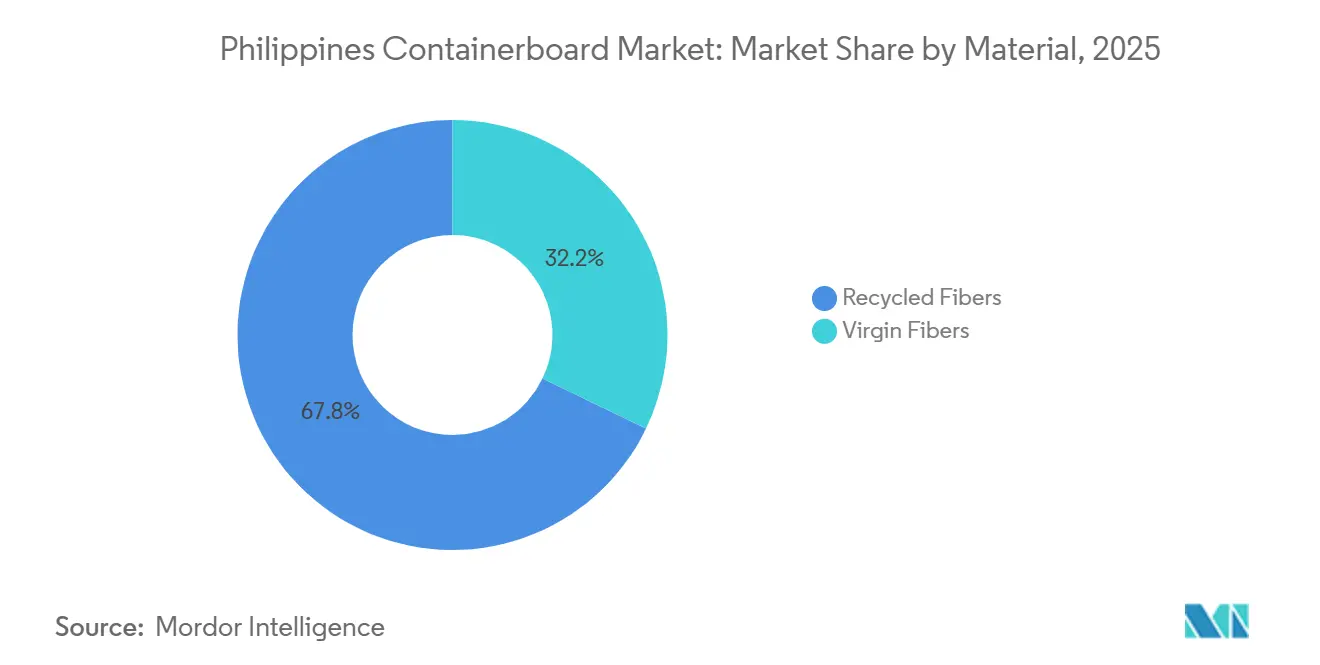

- By material, recycled fibers held 67.83% of the Philippines containerboard market share in 2025, while virgin fibers are projected to expand at a 5.37% CAGR through 2031.

- By product type, kraftliners accounted for 43.79% of the Philippines containerboard market size in 2025, while flutings are forecast to grow at a 5.69% CAGR through 2031.

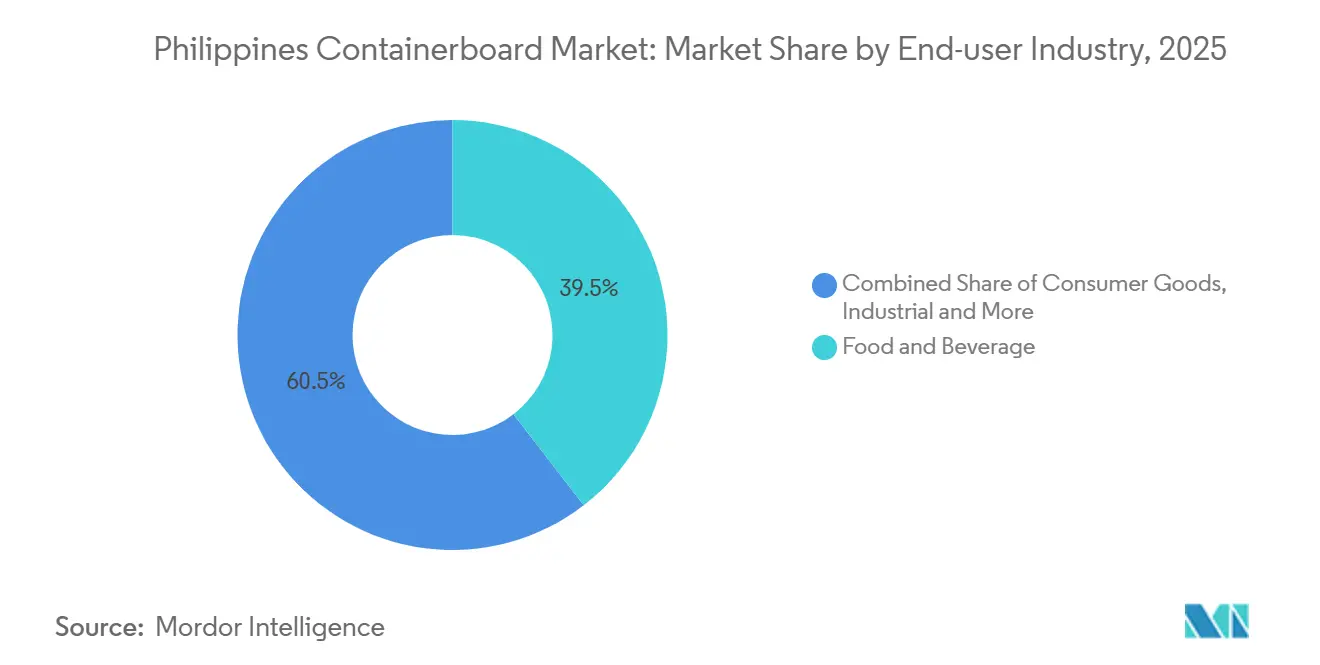

- By end-user industry, food and beverage commanded 39.54% of the Philippines containerboard market in 2025, while industrial applications are expected to advance at a 6.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Philippines Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Packaged Food And Beverage Output Expansion | +1.4% | National, with concentrated activity in Metro Manila, Central Luzon, and CALABARZON | Medium term (2-4 years) |

| E-Commerce Parcel Volume Growth | +1.2% | National, Luzon dominant, spill-over to Cebu and Davao | Medium term (2-4 years) |

| Electronics And Industrial Export Packaging Demand | +0.8% | Luzon, especially Cavite, Laguna, and Batangas ecozones, and CALABARZON | Long term (≥ 4 years) |

| Better Domestic Wastepaper Recovery And Reuse | +0.6% | National, with early gains concentrated in Metro Manila, Region III, and Region IV-A | Long term (≥ 4 years) |

| Corrugating Medium Safeguard Action Supporting Local Utilization | +0.3% | National, with mill-level benefit in Bulacan and Bataan | Short term (≤ 2 years) |

| ISO 14001:2026 Adoption Favoring Traceable Fiber Packaging | +0.2% | Global compliance standards with national implementation focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Packaged Food And Beverage Output Expansion

Packaged food and beverage production remains the strongest demand anchor for the Philippines containerboard market because it creates recurring shipping needs across urban, provincial, and inter-island distribution channels. The Philippine Statistics Authority reported that the volume of production index for food products rose 15.7% year over year in May 2025, then increased 3.4% in February 2026 even as wider industrial activity stayed less even, which shows that food manufacturing has been more defensive than many other factory categories. The USDA Foreign Agricultural Service also projected continued expansion in 2026 and linked part of that support to government efforts aimed at reducing logistics friction for food processors.[1]United States Department of Agriculture Foreign Agricultural Service, “Philippines Food Processing Ingredients Annual,” USDA Foreign Agricultural Service, fas.usda.gov The barangay-led retail model adds another layer of box demand because goods often move in smaller shipment formats and more frequent replenishment cycles than in supermarket-heavy systems, which raises box conversion intensity per unit of product sold. That pattern helps explain why the Philippines containerboard market draws durable support from food applications even when headline industrial production softens and why converters tied to everyday consumer staples tend to operate with a steadier order base than firms exposed mainly to discretionary categories.

E-Commerce Parcel Volume Growth

E-commerce continues to reshape the Philippines containerboard market by shifting more packaging demand toward single-trip corrugated formats used in parcel delivery and return handling. Online retail flows differ from traditional wholesale movement because orders are broken into smaller shipments, which changes box specifications, increases the number of units handled, and creates repeat demand for light but consistent corrugated grades. This has supported demand for recycled testliners and lighter fluting structures that suit parcel shipping without requiring export-grade board in every application. The benefit is strongest for local converters that can handle short production runs, varied dimensions, and quick turnaround times for merchants serving social commerce and marketplace channels. The result is a broader customer base for the Philippines containerboard market because packaging demand is spreading beyond large contract buyers and into a wider pool of domestic sellers, fulfillment operators, and courier-linked accounts.

Electronics And Industrial Export Packaging Demand

Industrial export activity is giving the Philippines containerboard market a premium demand layer that is distinct from mass domestic packaging applications. The Philippine Statistics Authority reported electronics exports of USD 4.82 billion in March 2026, helping lift first-quarter 2026 merchandise exports to USD 22.70 billion, up 12.7% from the prior year and the highest export quarter since the current trade statistics series began. SEIPI also projected electronics exports above USD 50 billion in 2026, supported by demand tied to AI peripherals, automotive semiconductors, and IoT devices. These export flows require higher-specification corrugated packaging, including humidity-resistant cartons, protective inserts, anti-static liners, and multi-layer outer shippers for delicate goods. That keeps part of the Philippines containerboard market less exposed to commodity-style pricing because converters serving electronics and industrial exporters operate in applications where performance, certification, and reliability matter more than the lowest board cost alone.

Better Domestic Wastepaper Recovery And Reuse

Better domestic wastepaper collection is improving the operating base of the Philippines containerboard market because recycled fiber remains the main practical feedstock for local production. The Board of Investments PAPELS study showed the recovery rate improved from 51% in 2021 to 56% in 2022, while 94% of recovered paper was used domestically in paper production in 2022.[2]Board of Investments, “Philippine Pulp and Paper Analysis Promoting Effective Linkages Updates and Supply Chain Mapping PAPELS,” Board of Investments, boi.gov.ph The Department of Trade and Industry, Bureau of Product Standards, also issued Philippine National Standards PNS 2162:2021 and PNS 2163:2021 to align domestic recovered paper quality with industrial acceptance criteria for OCC and mixed recovered grades.[3]Department of Trade and Industry Bureau of Product Standards, “Standards for Recovered Paper Towards Environmental Sustainability and Paper Industry Revitalization,” DTI Bureau of Product Standards, bps.dti.gov.ph The collection network matters beyond raw material quality because BOI linked the broader recovery chain to 1 million indirect livelihoods, which gives policymakers a strong reason to support its expansion and formalization. As recovery quality and coverage improve, the Philippines containerboard market gains a more stable local fiber base, which can reduce exposure to imported OCC swings and ease some price pressure on both mills and box converters over time.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imported Board Price Pressure On Local Mills | -0.9% | National, with highest exposure for mills in Bulacan and Bataan | Medium term (2-4 years) |

| High Electricity Costs Versus ASEAN Peers | -0.7% | National, with the greatest impact on energy-intensive mills in high-tariff distribution zones | Long term (≥ 4 years) |

| Recycling-Center Scarcity Outside Major Urban Hubs | -0.5% | Visayas, Mindanao, and provincial Luzon | Medium term (2-4 years) |

| Port Congestion And Elevated Container Freight Costs | -0.4% | Metro Manila ports, especially MICT and South Harbor, and inter-island domestic routes | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Imported Board Price Pressure On Local Mills

Imported containerboard remains a serious constraint on the Philippines containerboard market because local mills compete against suppliers from larger regional production systems with better economies of scale and lower operating costs. The Board of Investments noted that the domestic paper sector includes 22 non-integrated mills with combined capacity of 1.65 million metric tons per year, which is sizable for the local market but still fragmented compared with regional heavyweights. Trade policy support also weakened after the Tariff Commission’s January 2026 finding that Indonesian corrugating medium imports did not cause serious injury, and the Department of Trade and Industry later rejected the petition for definitive safeguard duties and ordered cash bond refunds to importers. That outcome reopened room for foreign board to compete more freely in commodity grades, especially where domestic producers rely on older machines or face higher operating costs. The pressure is especially relevant in the Philippines containerboard market because converters can use imports as a negotiating check on local mill pricing, which compresses domestic margins even when end-user demand remains healthy.

High Electricity Costs Versus ASEAN Peers

High electricity costs remain a persistent drag on the Philippines containerboard market because paperboard production is energy intensive and runs continuously across core process stages. The industrial power pricing as one of the highest in ASEAN during 2025 and 2026, which limits the ability of domestic mills to close cost gaps with regional suppliers even when freight conditions temporarily favor local production. Company commentary carried in local reporting also tied the issue to taxes on power bills and the lack of deeper system-loss reform, which suggests that the problem is structural rather than temporary. This matters for the Philippines containerboard market because imported board pressure is already strong, and energy inflation directly affects a cost line that converters cannot easily offset through product redesign or short-term sourcing changes. Unless mills secure scale efficiencies, captive energy solutions, or broader power-sector reform, electricity will continue to limit margin recovery and reduce domestic pricing flexibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled-Fiber Dominance Signals Structural Raw Material Dependency

Recycled fibers held 67.83% of the market in 2025, which shows how deeply the Philippines containerboard market depends on OCC and mixed wastepaper as its operating base. The Board of Investments PAPELS study stated that recycled fiber content in Philippine paper production runs at 95-100%, which means this position reflects infrastructure reality more than a simple commercial preference. In practice, the Philippines containerboard industry is built around a feedstock model where local mills work with recovered paper because commercial-scale virgin pulp plantations are not available in the country. That gives recycled board a stable volume role and keeps its demand closely linked to collection efficiency, municipal recovery systems, and the quality of domestically sourced wastepaper rather than only to shifts in end-user packaging choice.

Virgin fibers are projected to grow at a 5.37% CAGR from 2026 to 2031, which makes them the fastest-moving material niche even from a small base. The opportunity comes from applications where recycled content is less favored, including select pharmaceutical packaging, premium consumer goods, and food uses that require cleaner or certified fiber grades. Imports from established virgin kraft suppliers give converters access to these substrates, which means value-added demand can grow even without domestic pulp integration. This creates a two-speed structure in the Philippines containerboard industry, where recycled inputs remain dominant in tonnage while virgin-fiber applications capture incremental value in narrower, specification-driven segments. SCGP’s 2026 investment plan of THB 13,000 million, or USD 354 million, for fiber packaging upgrades across Southeast Asia reinforces that higher-value positioning is becoming more important for regional players that include the Philippines in their network strategy.

By Product Type: Kraftliners Hold The Core Volume Position While Flutings Set The Growth Pace

Kraftliners accounted for 43.79% of the market in 2025, giving them the largest position in the product mix and confirming their role as the main outer facing for many corrugated applications in the Philippines containerboard market size. Their position reflects demand from export shipping, organized food distribution, and retail-ready applications where appearance, surface performance, and structural strength remain important. Kraftliners are especially relevant in end uses such as electronics and packaged food, where converters often need consistent board quality, stronger handling performance, or a better print surface. Testliners remain an important secondary product group because they offer a more economical facing option for domestic distribution and parcel-heavy channels operating under tighter cost control.

Flutings are forecast to expand at a 5.69% CAGR through 2031, which makes them the fastest-growing product category in the Philippines containerboard market. Growth is tied to broader corrugated box demand across food shipments, industrial handling, and e-commerce packaging, where the internal medium determines stacking strength and protection during inter-island transport. The provisional safeguard measure on imported corrugating medium in late 2025 briefly encouraged greater use of domestic fluting, although the later reversal restored import flexibility and reduced the likelihood of lasting policy-based support.

By End-User Industry: Food And Beverage Secures Volume While Industrial Demand Builds Higher-Value Growth

Food and beverage held 39.54% of the market in 2025, which made it the largest end-user block and confirmed its role as the main volume base in the Philippines containerboard market size. The segment benefits from broad manufacturing depth, recurring restocking patterns, and the country’s need to move packaged goods across islands and retail formats with reliable protective packaging. Philippine Statistics Authority data showed food manufacturing volume growth of 15.7% in May 2025 and 3.4% in February 2026, which supports the view that this end use keeps a steady packaging demand floor even when wider factory activity is uneven. Consumer goods form the next major application group because household products, personal care items, and other branded retail goods still rely heavily on corrugated secondary packaging across a fragmented national distribution system.

Industrial applications are expected to grow at a 6.15% CAGR from 2026 to 2031, which makes them the fastest-expanding end-user group. That pace reflects the strength of export-oriented electronics assembly, testing, and packaging activity, where packaging must protect higher-value goods and often meet tighter technical requirements than standard domestic boxes. SEIPI reported electronics exports of USD 49.64 billion in 2025 and projected the figure above USD 50 billion in 2026, which points to a durable base for premium corrugated shippers and protective inserts. Other end users such as pharmaceuticals, agriculture, and construction materials still contribute incremental demand, but their order patterns are more variable because they are tied to crop cycles, project timing, and narrower product streams.

Geography Analysis

The Philippines containerboard market is geographically centered on Luzon because the largest concentration of board supply, corrugated converting capacity, food manufacturing, and export-oriented industrial demand sits around Metro Manila, Bulacan, and the wider CALABARZON corridor. UPPC’s Calumpit mill in Bulacan remains the dominant domestic supply point, and its location near the capital gives it a natural advantage in serving the country’s biggest converting and consumption zone. Metro Manila and nearby provinces also host major food processors, consumer goods manufacturers, and electronics facilities, so the area functions as both the largest demand center and the main distribution base for the Philippines containerboard market. Imported board has historically supplemented domestic supply through Manila gateways, especially when converters needed commodity grades or pricing checks against local mill offers. That pattern keeps Luzon at the center of procurement decisions, inventory buffering, and price formation across the national market.

The Visayas and Mindanao represent a different operating environment because converters there depend on either inter-island shipments from Luzon or imports arranged through regional hubs such as Cebu and Davao. Cebu had only 33% yard utilization in March 2026, far below Manila, which suggests a less congested entry point for board moving into the central Philippines. Mindanao demand is tied more closely to agri-food export cycles, including fruit packing, fish processing, and other seasonal activities that create sharper order swings for local corrugated plants. MARINA’s decision to raise the maximum allowable freight rate increase to 30% in March 2026 and then 40% in April 2026 raised the cost of moving containerboard across islands, which widened the logistics burden for converters outside the main production heartland. This means the Philippines containerboard market does not operate as one fully uniform national space, because freight exposure and access to recovered paper differ sharply by region.

Looking ahead, geographic divergence is likely to deepen because electronics-led premium demand remains concentrated in Cavite, Laguna, and Batangas, while agri-food and provincial consumer demand stays spread across island markets. Electronics export strength supports specification-driven corrugated demand that is less tied to household spending and more tied to manufacturing programs and shipment compliance standards. At the same time, recovery systems and recycling infrastructure remain more developed around major urban zones than in many provincial areas, which leaves regional converters with different raw material and working capital pressures than firms near Metro Manila. The Philippines containerboard market therefore behaves as several linked sub-markets, where performance depends less on national averages and more on how closely capacity, sourcing, and customer mix match the needs of specific island clusters and ecozones.

Competitive Landscape

The Philippines containerboard market has a split competitive structure, with far greater concentration at the upstream mill level than in downstream corrugated conversion. United Pulp and Paper Co., Inc., which sits within SCGP, remains the dominant domestic containerboard manufacturer through its Calumpit, Bulacan operations and therefore has outsized influence over local board availability and lead times. By contrast, the converting base is populated by many small and mid-size operators spread across Metro Manila, Cebu, Davao, and nearby industrial corridors, which keeps box conversion pricing competitive and limits the ability of most converters to dictate terms upstream. Buyers often manage this imbalance by preserving import sourcing options, so local mill pricing power is meaningful but not absolute.

Strategy among local converters is shaped more by regional positioning, customer service, and order responsiveness than by large-scale national consolidation. Companies such as Corbox Corporation, Duraboard Packaging Corp., and Goldrich Industrial Packaging Corporation compete by staying close to customer clusters, turning jobs quickly, and tailoring board conversion to local demand rather than trying to match the scale of the leading mill. Fifth Discipline Packaging Paper Corporation in Pampanga adds another competitive layer because it focuses on 100% recycled-material corrugating medium and linerboard, which gives Central Luzon converters a freight advantage outside the strongest orbit of the Bulacan mill. Technology is also changing the shape of competition in the Philippines containerboard market, especially where efficiency or customization can offset smaller scale. UPPC’s Calumpit site commissioned an Andritz OCC line with capacity of 870 admt per day for processing OCC and mixed wastepaper into corrugated medium, which shows that automation and fiber handling capability remain central to mill-side competitiveness.

Another important strategic move came from SCGP’s 2026 investment budget of THB 13,000 million, or USD 354 million, which targeted fiber packaging expansion, production efficiency, and downstream packaging capabilities across Southeast Asia and supports the company’s broader regional integration strategy that includes the Philippines.[4]SCGP, “Investor Meeting Presentation,” SCGP, scgp.listedcompany.com Digital printing adoption at the converter level is also expanding because shorter runs and higher design variability are becoming more common in e-commerce and retail-ready packaging, and that gives nimble regional players a way to compete without major flexographic plate commitments. Compliance is becoming a competitive issue as well, since multinational buyers are paying closer attention to fiber traceability, supplier documentation, and environmental management transitions linked to ISO 14001:2026.

Philippines Containerboard Industry Leaders

United Pulp and Paper Co., Inc.

San Miguel Yamamura Packaging Corporation

Valenzuela Packaging Container Corporation

Liberty Corrugated Boxes Mfg. Corp.

Hyphoria Philippines Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Philippine merchandise export sales reached USD 8.17 billion in March 2026, a record monthly figure and a 20.4% increase from March 2025, with electronics accounting for USD 4.82 billion, 59% of total, according to Philippine Statistics Authority data reported by Newsbytes.ph. The sustained electronics export surge reinforces premium corrugated packaging demand across ATP facilities in Cavite, Laguna, and Batangas export processing zones.

- May 2026: MARINA lowered the cargo rate surcharge ceiling back to 30% from 40% through MA No. 2026-23, dated May 11, following a three-week downward trend in fuel costs per the Department of Energy oil monitor advisories, according to PortCalls Asia. The rollback provided partial freight cost relief for inter-island containerboard distribution.

- April 2026: International Container Terminal Services Inc. announced port tariff increases at Manila International Container Terminal and affiliated domestic terminals, citing elevated fuel costs driven by Middle East geopolitical tensions. ICTSI's 2026 capital expenditure budget was set at USD 740 million, a 14% increase, with 72%, or USD 532 million, allocated to expansion projects, according to Philstar.com. The tariff increases raise import landed costs for containerboard and add pressure to converter working capital.

- April 2026: ISO published ISO 14001:2026 on April 15, 2026, replacing ISO 14001:2015 and introducing auditable requirements on biodiversity, pollution, and resource availability into environmental management systems for the first time, per ISO.org. With over 670,000 global certifications, the update creates new packaging supply chain due diligence obligations affecting multinational FMCG and electronics buyers procuring from Philippine containerboard converters.

Philippines Containerboard Market Report Scope

The Philippines Containerboard Market encompasses the production, distribution, and consumption of containerboard used in the manufacture of corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The market is driven by the increasing demand for sustainable, lightweight, and durable packaging solutions.

The Philippines Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current and future size of the Philippines containerboard market?

The Philippines containerboard market was valued at USD 2.12 billion in 2025 and stands at USD 2.21 billion in 2026. It is forecast to reach USD 2.77 billion by 2031 at a CAGR of 4.62% over 2026-2031.

Which material type leads demand in the Philippines containerboard space?

Recycled fibers led with a 67.83% share in 2025 because local mills depend heavily on OCC and mixed wastepaper. This position is reinforced by the lack of commercial-scale domestic virgin pulp supply.

Which product category is growing the fastest in the country?

Flutings are projected to post the fastest growth, with a 5.69% CAGR through 2031. Their growth is tied to rising corrugated box demand across food, industrial, and e-commerce shipments.

Which end-user group drives the largest volume of boxboard consumption?

Food and beverage remained the largest end-user segment with 39.54% share in 2025. The segment benefits from recurring shipment needs, broad manufacturing depth, and the country’s inter-island distribution model.

Why does geography matter so much for containerboard demand in the Philippines?

Demand is split across Luzon, Visayas, and Mindanao, and each region has different freight, sourcing, and customer patterns. Luzon leads in mill supply and export manufacturing, while Visayas and Mindanao face higher inter-island logistics exposure and more seasonal agri-food demand.

What are the main risks shaping profitability for local mills and converters?

Imported board pressure and high electricity costs remain the biggest constraints on domestic mill margins. Port congestion, freight rate swings, and uneven recycling access outside major urban hubs add further pressure to working capital and regional operating costs.

Page last updated on: