Meniere's Disease Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

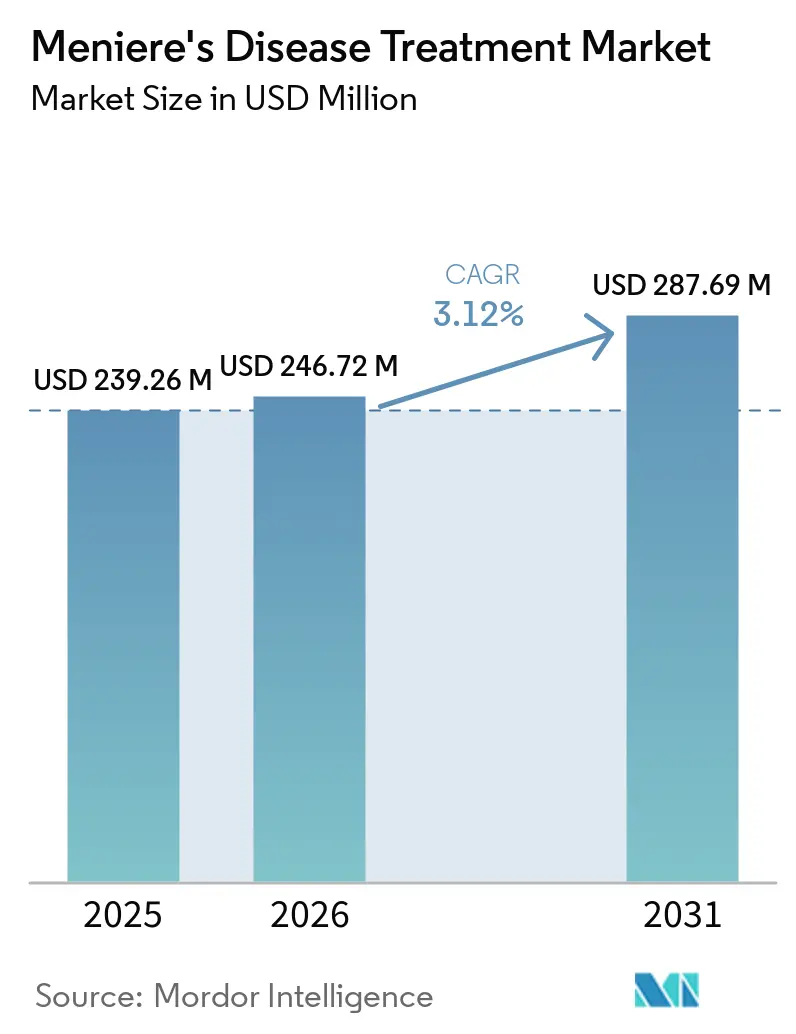

| Market Size (2026) | USD 246.72 Million |

| Market Size (2031) | USD 287.69 Million |

| Growth Rate (2026 - 2031) | 3.12% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Meniere's Disease Treatment Market Analysis by Mordor Intelligence

The Meniere's Disease Treatment Market size is expected to grow from USD 239.26 million in 2025 to USD 246.72 million in 2026 and is forecast to reach USD 287.69 million by 2031 at 3.12% CAGR over 2026-2031.

Growth remains measured because the condition has a relatively fixed patient pool and treatment still centers on symptom control rather than disease modification. Diagnostic adoption is widening the treated pool, with combined caloric testing, vHIT, and cVEMP reaching 78% sensitivity and 92% specificity for definite disease, while MRI sensitivity for cochlear endolymphatic hydrops reaches 95%. A 2025 prospective study also showed that combining cochlear and vestibular hydrops on delayed gadolinium MRI achieved 100% diagnostic accuracy against vestibular migraine, which should reduce one of the main sources of misclassification in the Meniere's disease treatment market. Competition remains split between high-volume generic suppliers and a smaller set of specialty developers pursuing sustained-release intratympanic products and inner-ear targeted therapies, with SPI-1005 standing out as the first investigational drug to meet co-primary endpoints in a pivotal Phase 3 trial and secure FDA Breakthrough Therapy Designation. Even with these advances, the Meniere's disease treatment market still faces limits from diagnostic overlap, low early-stage surgical conversion, and the lack of an approved disease-modifying therapy, although telehealth rehabilitation and greater use of specialty ENT settings are widening access to care.

Key Report Takeaways

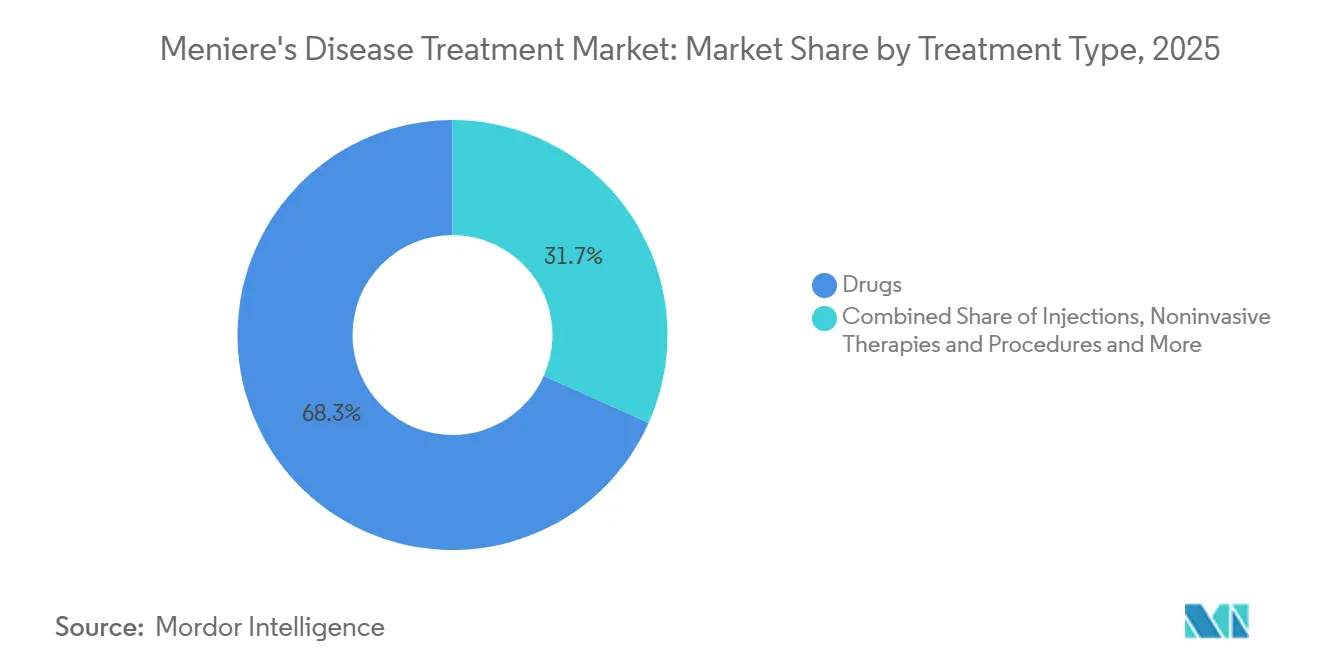

- By treatment type, Drugs held 68.31% share in 2025, while Injections are forecast to expand at a 4.38% CAGR through 2031.

- By symptom type, Vertigo Management accounted for 45.24% share in 2025, while Tinnitus Relief is expected to record the highest CAGR at 5.52% through 2031.

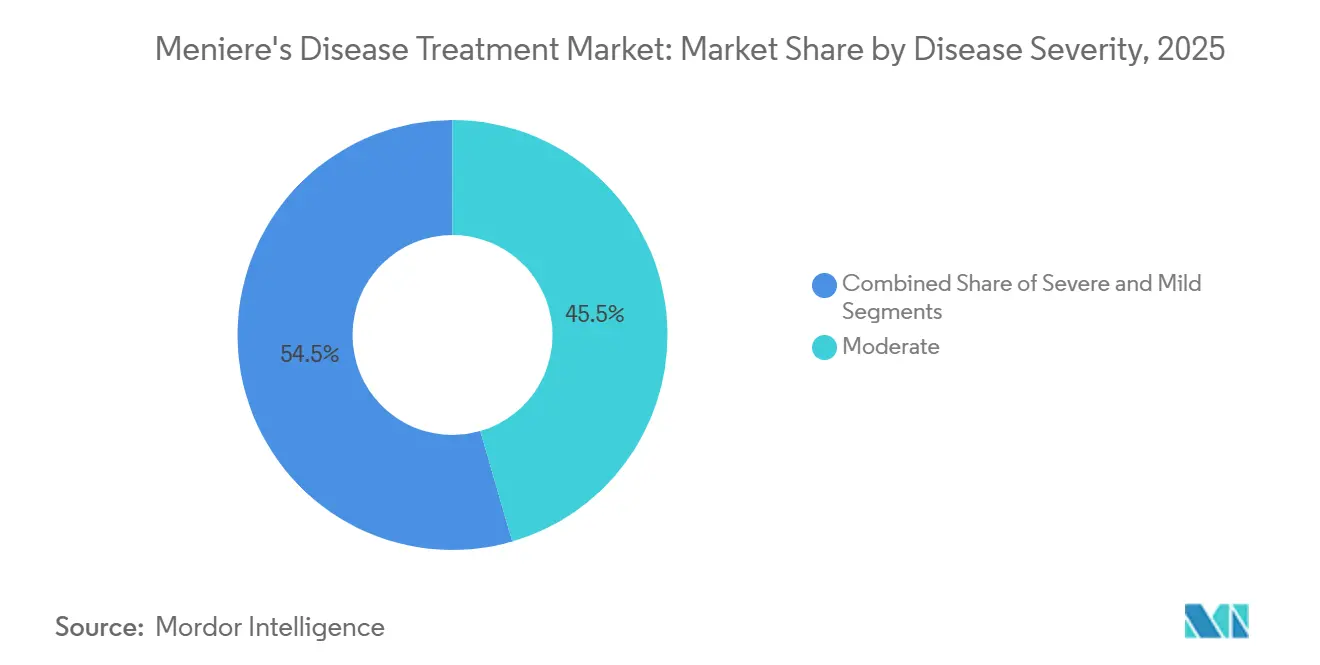

- By disease severity, Moderate cases held 45.52% share in 2025, while Severe cases are projected to grow fastest at a 4.25% CAGR through 2031.

- By end user, Hospitals and Clinics held 60.52% share in 2025, while Specialty ENT Centers are expected to advance at a 5.25% CAGR through 2031.

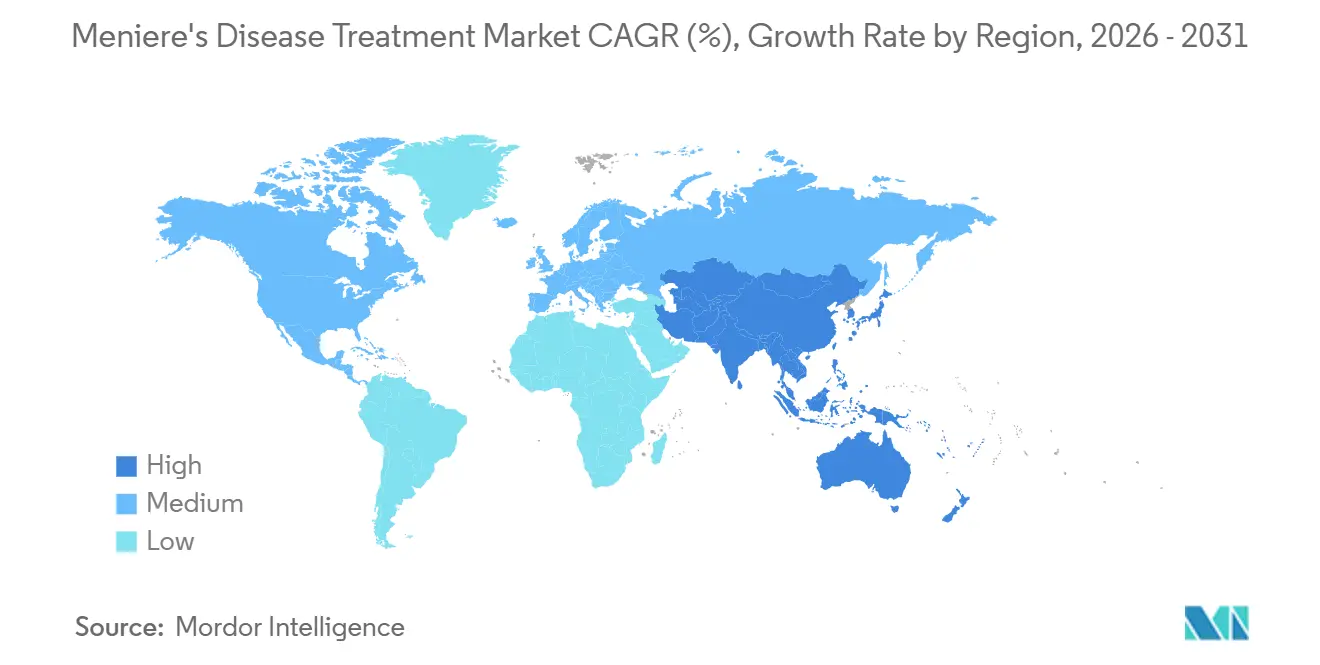

- By geography, North America held 38.22% share in 2025, while Asia-Pacific is forecast to grow fastest at a 5.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Meniere's Disease Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Meniere's Disease Diagnosis Through vHIT, VEMP, and MRI Endolymph Imaging | +0.5% | Global, early gains in North America, Germany, Japan | Short term (≤ 2 years) |

| Expansion of Intratympanic Delivery and Sustained-Release Formulations | +0.7% | North America, Western Europe, Australia | Medium term (2-4 years) |

| Telehealth-Enabled Vestibular Rehabilitation and Home Monitoring | +0.4% | North America, Nordic countries, Australia | Short term (≤ 2 years) |

| Longer Treatment Journeys Driven by Symptom Recurrence and Refractory Cases | +0.6% | Global, most pronounced in high-income markets | Long term (≥ 4 years) |

| Clinical Pipeline Progress in Anti-Inflammatory and Inner-Ear Targeted Therapies | +0.8% | North America, EU core, Japan | Medium term (2-4 years) |

| Shift Toward ENT Specialty Care, Day Procedures, and Outpatient Management | +0.4% | North America, EU, early gains in GCC and APAC urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Meniere's Disease Diagnosis Through vHIT, VEMP, And MRI Endolymph Imaging

Multimodal vestibular testing is expanding the Meniere's disease treatment market by validating patients who were once treated for other vestibular conditions. When at least 2 vestibular function tests are abnormal and MRI confirms hydrops, diagnostic performance rises from 65% with a single test to 88% to 90%. The same review reported 78% sensitivity and 92% specificity for a triple-test approach that combines caloric testing, vHIT, and cVEMP in definite disease. A separate 2025 study showed that delayed gadolinium MRI combining cochlear and vestibular hydrops reached 100% diagnostic accuracy against vestibular migraine, which addresses one of the most common causes of misclassification. Staging is also improving because ECochG, VEMPs, and caloric testing now map hearing decline against vestibular loss more clearly, which supports earlier treatment initiation and more consistent escalation decisions. AI-supported MRI grading lifted inter-rater reliability from 0.61 to 0.89, which should help community centers use the same diagnostic language as academic sites and support more consistent reimbursement pathways in the Meniere's disease treatment market[1]Alessandro Galetti et al., “Multimodal Diagnostic Evaluation in Ménière Disease: A Narrative Review of Vestibular Function Tests and Gadolinium-Enhanced Magnetic Resonance Imaging for Endolymphatic Hydrops,” Revista de Vestibulologia, e-rvs.org.

Expansion Of Intratympanic Delivery And Sustained-Release Formulations

Intratympanic therapy is moving from rescue use toward earlier intervention in the Meniere's disease treatment market because delivery systems now keep drug exposure in the inner ear for much longer. A 2025 systematic review of 6 placebo-controlled randomized trials found that the sustained-release OTO-104 formulation in the AVERTS-2 trial reduced Definite Vertigo Days to 2.04 versus 3.47 for placebo, with p=0.014. This shift matters commercially because thermosensitive hydrogel carriers reduce the burden of repeated injections and improve the economics of specialty ENT treatment visits. The analysis also noted that intratympanic delivery can achieve inner-ear concentrations 100 to 1,000 times higher than systemic administration while reducing systemic side effects, which supports a clearer value case for second-line use. Spiral Therapeutics reported that its 6% dexamethasone sustained-release candidate SPT-2101 showed superior vertigo outcomes versus predecessor OTO-104 across all time points in a Phase 1b/2a trial of 21 patients. As more formulations progress with expedited regulatory support, the premium layer of the Meniere's disease treatment market is likely to shift further toward injectable and sustained-release care pathways.

Telehealth-Enabled Vestibular Rehabilitation And Home Monitoring

Remote vestibular rehabilitation is widening the reach of the Meniere's disease treatment market because it gives patients access to guided therapy without requiring repeated in-clinic visits. A 2026 randomized crossover pilot trial found that smartphone-supported vestibular rehabilitation delivered improvements in Dizziness Handicap Inventory scores and functional mobility comparable with conventional therapy over a 6-week program. A 2025 multicenter randomized trial also supported internet-based vestibular rehabilitation over written instruction-only care in acute vestibular syndrome, which strengthens the evidence base that payers and providers will review for broader use. This matters most in semi-urban and rural areas where patients with dizziness symptoms often do not reach specialist ENT clinics early enough for structured management. The same body of evidence shows that scheduled supervision and structured home exercise plans improve compliance and patient-reported postural control, which addresses a known weakness of unsupervised therapy models. As a result, the noninvasive part of the Meniere's disease treatment market should benefit from better treatment retention and broader follow-up coverage.

Longer Treatment Journeys Driven By Symptom Recurrence And Refractory Cases

Recurring symptoms extend time in treatment and raise the lifetime value of managed patients in the Meniere's disease treatment market. The analysis states that 30% of patients develop bilateral involvement over time, while a meaningful share of unilateral cases progresses to medically refractory disease that requires escalation beyond oral therapy. A 2025 network meta-analysis across 16 studies and 853 participants showed that vestibular nerve section offered the strongest hearing-preservation results in refractory disease, while intratympanic gentamicin outperformed endolymphatic sac surgery and intratympanic steroids for vertigo control. That treatment ladder supports more repeat assessments, more procedural touchpoints, and more formal chronic-disease management in specialty practice. Large ENT groups are increasingly set up around scheduled vestibular testing, audiometric follow-up, and tiered escalation rather than one-time acute vertigo visits, which should raise treatment persistence across the Meniere's disease treatment market. This pattern also explains why refractory and severe patients contribute a disproportionate share of procedural value even though they account for a smaller part of total diagnosed cases.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Symptomatic Treatment Limits Long-Term Disease Modification | -0.9% | Global | Long term (≥ 4 years) |

| Variable Diagnostic Criteria and Overlap With Other Vestibular Disorders | -0.5% | Global, most acute in markets with limited MRI access | Medium term (2-4 years) |

| Betahistine Efficacy Debate and Uneven Reimbursement Acceptance | -0.5% | Europe, including France, the UK, and Switzerland, moderate in North America | Medium term (2-4 years) |

| Small Patient Pool and Low Surgical Conversion Rates in Earlier Disease Stages | -0.3% | Global, most constraining in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Symptomatic Treatment Limits Long-Term Disease Modification

The biggest structural limit on the Meniere's disease treatment market is that current therapies mainly manage symptoms instead of changing the course of the disease. Diuretics, betahistine, vestibular suppressants, and intratympanic corticosteroids can reduce vertigo burden, but they do not stop progressive cochlear decline or reverse endolymphatic hydrops. This caps long-term value because treatment goals often settle at symptom stabilization once attacks are controlled. The strongest late-stage attempt to change that pattern is SPI-1005, which targets glutathione peroxidase-2 activity in the inner ear and showed a 57.9% improvement rate in low-frequency hearing loss versus 36.5% for placebo in the Phase 3 STOPMD-3 trial, with p=0.0037[2]“Sound Pharmaceuticals Receives FDA Breakthrough Therapy Designation for SPI-1005 to Treat Meniere's Disease,” Sound Pharmaceuticals, soundpharma.com. Until an approved disease-modifying therapy reaches commercial use, the Meniere's disease treatment market will remain tied to adherence patterns for symptomatic regimens and procedural escalation in refractory patients. That limitation is one reason premium growth opportunities still depend more on delivery innovation and diagnosis expansion than on a broad reset of clinical practice.

Variable Diagnostic Criteria And Overlap With Other Vestibular Disorders

Diagnostic inconsistency continues to suppress conversion into the Meniere's disease treatment market because many patients are still classified under other vestibular conditions for long periods. The analysis states that single-modality testing reaches only 65% diagnostic accuracy, which leaves many patients undertreated when MRI and multimodal vestibular testing are not available. The challenge is more severe in regions where gadolinium-enhanced MRI is limited to tertiary centers, since treatment initiation is then delayed or routed through less specific symptom labels. The Bárány Society criteria also require at least 2 definite vertigo attacks over a 20-minute to 12-hour window, documented audiometric change, and tinnitus or aural fullness, which can exclude earlier-stage patients from formal classification in routine ENT practice. Europe also faces a separate friction point because betahistine efficacy and reimbursement remain under review in some systems, including a formal Swiss health technology assessment of betahistine and cinnarizine. Together, these issues keep the Meniere's disease treatment market below its potential diagnosed volume even where general awareness of vestibular disorders is improving.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Generic Drugs Anchor Volume While Injections Define Premium Growth

Drugs held 68.31% of the Meniere's disease treatment market share in 2025, so oral therapy remained the commercial base for this segment. That position reflects the wide prescriber base for betahistine, diuretics, vestibular suppressants, and corticosteroids, which still define first-line management in most care settings. The segment also benefits from familiar dosing pathways and lower upfront cost, which keep oral therapy in place even where advanced vestibular testing remains limited. Growth is more restrained because reimbursement scrutiny persists in parts of Europe and no new branded oral therapy has reset pricing or treatment standards.

Injections carry the highest CAGR at 4.38%, and that pace reflects better local drug exposure and lower systemic side effects than oral dosing in appropriate patients. The analysis noted that intratympanic delivery can achieve inner-ear concentrations 100 to 1,000 times higher than systemic administration, which supports its use before surgery in treatment-resistant cases. Intratympanic steroids benefit from a favorable safety profile and a growing randomized evidence base, while intratympanic gentamicin remains more selective because of ototoxicity risk. Noninvasive therapies and procedures are also gaining steadier use as telehealth expands vestibular rehabilitation access and lowers the practical burden of follow-up. Surgery remains a small but important end point in the treatment cascade, with endolymphatic sac surgery controlling vertigo in around 70% of medically refractory cases with minimal morbidity, though practice patterns remain uneven by country.

By Symptom Type: Vertigo Leads Today While Tinnitus Relief Gains More Speed

Vertigo Management accounted for 45.24% share in 2025, which kept it as the largest symptom-focused revenue pool in the Meniere's disease treatment market. This lead reflects the fact that vertigo attacks drive most first specialist visits, urgent care use, and early treatment decisions. Vertigo also acts as the main entry point into the wider care pathway, since patients who first seek relief for severe attacks often stay in treatment for hearing, tinnitus, and balance follow-up later on. Hearing Loss Treatment is becoming more relevant as cochlear damage progresses in moderate and severe disease, especially as newer pipeline agents try to address low-frequency hearing decline. The current structure still leaves Vertigo Management as the most established and most routinely reimbursed part of the Meniere's disease treatment market.

Tinnitus Relief is projected to expand at a 5.52% CAGR through 2031, making it the fastest-growing symptom segment. That pace reflects greater clinical recognition of tinnitus as a distinct quality-of-life burden and the continued lack of any approved pharmacological therapy designed specifically for it. SPI-1005 also matters here because its Phase 3 data created a more credible discussion around pharmacologic improvement in hearing-related manifestations, which could eventually support adjacent positioning in this segment if approvals follow. Balance Disorder Therapy remains the smallest of the 4 symptom groups, but it is gaining more structure as app-based and home-based vestibular rehabilitation lowers access barriers and improves adherence. Over time, integrated audiology and vestibular programs should make symptom bundles more common, which can improve treatment retention across the Meniere's disease treatment market.

By Disease Severity: Moderate Cases Dominate Volume While Severe Cases Lift Care Intensity

Moderate cases held 45.52% share in 2025, which made them the largest severity cohort in the Meniere's disease treatment market. This segment sits at the center of routine maintenance care because it includes the largest group of patients using betahistine-based regimens, diuretics, and periodic vestibular follow-up. It also contains many patients whose symptoms are serious enough to require sustained management, but not yet severe enough to move quickly into repeated injections or surgery. Mild cases are common earlier in the disease course, yet they generate less revenue because watchful waiting, diet modification, and symptom observation still precede active drug use in many practices. That leaves the moderate pool as the main source of recurring prescription and monitoring demand in the Meniere's disease treatment market.

Severe cases are projected to grow at a 4.25% CAGR through 2031, which is the fastest pace across severity categories. This pattern reflects the high cost of care once patients move into refractory disease and require repeated intratympanic treatment, intensive vestibular rehabilitation, or surgery. The 2025 network meta-analysis showed that refractory cases who fail simpler options can benefit from premium interventions such as vestibular nerve section, which raises procedural value even in a smaller cohort. Germany's AWMF stepwise treatment framework also supports orderly escalation because patients must document failure at each tier before moving to the next, which can gradually shift more severe patients into higher-value care settings[3]“Prospective Multicentric Registry Study, SEMM, Meniere's Disease Therapy,” Laryngo-Rhino-Otologie, thieme-connect.com. The result is a severity mix in which moderate cases supply most volume while severe cases contribute more of the procedural upside in the Meniere's disease treatment market.

By End User: Hospitals Lead Today While Specialty ENT Centers Gain More Procedure Flow

Hospitals and Clinics held 60.52% share in 2025, which kept them as the largest end-user category in the Meniere's disease treatment market. Their lead comes from control over surgery, inpatient vestibular assessment capacity, and emergency management of acute vertigo episodes. They also remain important when diagnosis is uncertain and patients need access to broader imaging, audiology, and multidisciplinary review. In many countries, hospitals are still the first organized point of referral for patients whose symptoms overlap with migraine, neurological disorders, or other inner-ear conditions. This makes the hospital channel the largest installed care base in the Meniere's disease treatment market even as procedure migration begins to change the mix.

Specialty ENT Centers are forecast to expand at a 5.25% CAGR through 2031, which makes them the fastest-growing end-user segment. Their growth is tied to the outpatient shift in intratympanic procedures, diagnostic audiology, and vestibular rehabilitation, all of which can now be delivered without full hospital infrastructure. These centers also build more revenue around testing, hearing support, and repeat follow-up, which increases patient value beyond the core treatment visit. Ambulatory Surgical Centers benefit from the same migration when ENT procedures move out of hospital outpatient departments, especially in systems that reward lower-cost sites of care. As a result, the Meniere's disease treatment market is moving toward a more specialized delivery model even though hospitals still control the largest share today.

Geography Analysis

North America held 38.22% share in 2025, which made it the largest regional block in the Meniere's disease treatment market. The United States drives this lead through higher diagnosis rates, broader reimbursement for ENT procedures, and deeper clinical trial activity in inner-ear disorders. The region also contains the most visible late-stage pipeline assets in this space, including SPI-1005 and SPT-2101, which means first commercial launches would likely reach the United States before other regions. Canada adds support through more standardized provincial specialty ENT pathways and a growing base of intratympanic procedures. Mexico remains an emerging opportunity, but diagnostic access, specialist density, and reimbursement limits still keep the regional mix tilted toward the United States and Canada.

Asia-Pacific is projected to grow at a 5.15% CAGR through 2031, which makes it the fastest-growing geography in the Meniere's disease treatment market. Aging populations, urban ENT infrastructure expansion, and better access to vestibular testing are the main reasons for this faster pace. China and Japan are the main demand anchors because they combine large older populations with meaningful specialist capacity in major cities. India remains underpenetrated because gadolinium MRI and vestibular testing are still limited outside large metro areas, so more patients remain in basic drug management instead of moving into premium injectable or procedural care. South Korea and Australia stand out for earlier adoption of app-based vestibular rehabilitation models that can extend treatment continuity beyond the clinic.

Europe was the second-largest regional block in the Meniere's disease treatment market, with Germany, France, the UK, and Italy as core contributors. Regional growth is shaped by strong ENT networks, but it is also tempered by reimbursement scrutiny around established therapies, especially betahistine. The Swiss Federal Office of Public Health is reviewing the use of betahistine and cinnarizine in Meniere's disease, vertigo disorders, and tinnitus, which shows that value assessment remains active in Europe. Germany differs from this pattern because its AWMF stepwise framework preserves first-line use while guiding patients toward higher-tier intervention only after documented failure, which gives the region a more structured escalation pathway. The Middle East and Africa remain smaller, but GCC investment in urban diagnostic and specialty ENT capacity is gradually improving access, while South America continues to face infrastructure and reimbursement limits even as specialist training supports slower adoption of intratympanic procedures.

Competitive Landscape

The Meniere's disease treatment market is moderately fragmented, and no single company controls more than a low double-digit share of total revenue. Generic pharmaceutical manufacturers such as Teva, Viatris, Hikma, Cipla, Sun Pharmaceutical, and Intas dominate day-to-day commercial volume through betahistine, diuretics, and off-patent corticosteroid products. Large pharmaceutical companies including Pfizer, Novartis, Merck, and Sanofi are present mainly through older portfolios rather than through broad proprietary pipelines built specifically for this indication. This creates a split structure in which generic players compete on manufacturing scale, supply continuity, and price, while specialty companies compete on delivery technology, regulatory timing, and clinical differentiation. That structure keeps oral therapy crowded and price sensitive, while the more defensible value pool in the Meniere's disease treatment market sits in injections, sustained-release delivery, and potential inner-ear targeted therapies.

Several strategic moves show where competition is shifting. Sound Pharmaceuticals advanced SPI-1005 to the front of the pipeline after it became the first investigational drug to meet co-primary endpoints in a pivotal Phase 3 Meniere's trial and secure FDA Breakthrough Therapy Designation. Spiral Therapeutics reported that SPT-2101 delivered superior vertigo outcomes versus predecessor OTO-104 across all time points in a Phase 1b/2a study of 21 patients, which strengthens the sustained-release intratympanic case. Shionogi also signaled renewed large-pharma interest in inner-ear disorders through its June 2024 option agreement with Cilcare, paying EUR 15 million (USD 16.1 million) upfront with potential milestones up to EUR 400 million (USD 428.5 million). Together, these moves show that the Meniere's disease treatment market is still open to share capture by focused innovators rather than locked into a mature branded hierarchy.

Open opportunities remain strongest in disease-modifying anti-inflammatory or aquaporin-targeted approaches and in bilateral disease, where current procedural choices carry greater risk and fewer targeted study data. Diagnostics are also becoming a competitive tool, since AI-assisted MRI segmentation raised inter-rater reliability from 0.61 to 0.89 and can support more standardized patient identification across treatment centers. Companies that combine drug development with diagnostic pathway support and deeper specialty ENT relationships are likely to be better positioned than companies that rely only on broad primary-care reach. Overall, the Meniere's disease treatment market remains fragmented enough that a well-supported new entrant can build position through targeted specialty channels instead of mass-market scale alone.

Meniere's Disease Treatment Industry Leaders

Pfizer Inc.

GlaxoSmithKline plc

Teva Pharmaceutical Industries Ltd.

Viatris Inc.

Sun Pharmaceutical Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Spiral Therapeutics raised USD 27 million in Series B funding. Advanced Bionics and a global pharmaceutical company joined as strategic investors, combining cochlear implant delivery expertise with Spiral's SPT-2101 platform for Meniere's disease.

- December 2025: Sound Pharmaceuticals (SPI) announced that the FDA granted Breakthrough Therapy Designation (BTD) to its drug SPI-1005 for treating hearing loss in Meniere’s disease patients.

Global Meniere's Disease Treatment Market Report Scope

As per the scope of the report, Meniere's disease is a disorder of the inner ear that causes episodes of vertigo, hearing loss, tinnitus, and a sensation of fullness or pressure in the affected ear. Treatment aims to manage symptoms, reduce the frequency and severity of episodes, and improve quality of life.

The Meniere's disease treatment market is segmented by treatment type, symptom type, disease severity, end user, and geography. By treatment type, the market includes drugs such as diuretics, betahistine, vestibular suppressants, and corticosteroids. It also covers injections, including intratympanic steroid injections and intratympanic gentamicin injections, along with noninvasive therapies and procedures like vestibular rehabilitation therapy, positive pressure therapy, dietary and lifestyle management, and surgery. By symptom type, the segmentation includes vertigo management, tinnitus relief, hearing loss treatment, and balance disorder therapy. Based on disease severity, the market is categorized into mild, moderate, and severe cases. By end user, the market is divided into hospitals and clinics, specialty ENT centers, ambulatory surgical centers, and other end users. Geographically, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Drugs | Diuretics |

| Betahistine | |

| Vestibular Suppressants | |

| Corticosteroids | |

| Injections | Intratympanic Steroid Injections |

| Intratympanic Gentamicin Injections | |

| Noninvasive Therapies and Procedures | Vestibular Rehabilitation Therapy |

| Positive Pressure Therapy | |

| Dietary and Lifestyle Management | |

| Surgery |

| Vertigo Management |

| Tinnitus Relief |

| Hearing Loss Treatment |

| Balance Disorder Therapy |

| Mild |

| Moderate |

| Severe |

| Hospitals and Clinics |

| Specialty ENT Centers |

| Ambulatory Surgical Centers |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Drugs | Diuretics |

| Betahistine | ||

| Vestibular Suppressants | ||

| Corticosteroids | ||

| Injections | Intratympanic Steroid Injections | |

| Intratympanic Gentamicin Injections | ||

| Noninvasive Therapies and Procedures | Vestibular Rehabilitation Therapy | |

| Positive Pressure Therapy | ||

| Dietary and Lifestyle Management | ||

| Surgery | ||

| By Symptom Type | Vertigo Management | |

| Tinnitus Relief | ||

| Hearing Loss Treatment | ||

| Balance Disorder Therapy | ||

| By Disease Severity | Mild | |

| Moderate | ||

| Severe | ||

| By End User | Hospitals and Clinics | |

| Specialty ENT Centers | ||

| Ambulatory Surgical Centers | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current outlook for Meniere's disease treatment through 2031?

The Meniere's disease treatment market is projected to move from USD 246.72 million in 2026 to USD 287.69 million by 2031 at a 3.12% CAGR, which points to steady but not rapid expansion.

Which treatment category is growing the fastest in Meniere's disease care?

Injections are the fastest-growing treatment type at a 4.38% CAGR through 2031, supported by better local drug delivery and rising use of sustained-release intratympanic formulations.

Why does North America lead revenue in Meniere's disease treatment?

North America held 38.22% share in 2025 because the region combines stronger diagnosis rates, broader reimbursement for ENT procedures, and deeper late-stage pipeline activity.

What is driving faster growth in Asia-Pacific for Meniere's disease treatment?

Asia-Pacific is forecast to grow at a 5.15% CAGR through 2031 as aging populations, urban ENT infrastructure expansion, and wider access to vestibular testing increase diagnosed demand.

Which symptom area is seeing the strongest growth in Meniere's disease management?

Tinnitus Relief is projected to grow at a 5.52% CAGR through 2031, reflecting higher clinical attention to tinnitus and the lack of approved drug options designed specifically for this burden.

How concentrated is competition in Meniere's disease treatment?

Competition is relatively fragmented, with generic manufacturers controlling much of routine volume and specialty firms competing through delivery innovation, trial progress, and targeted inner-ear therapies.

Page last updated on: