Huntington's Disease Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

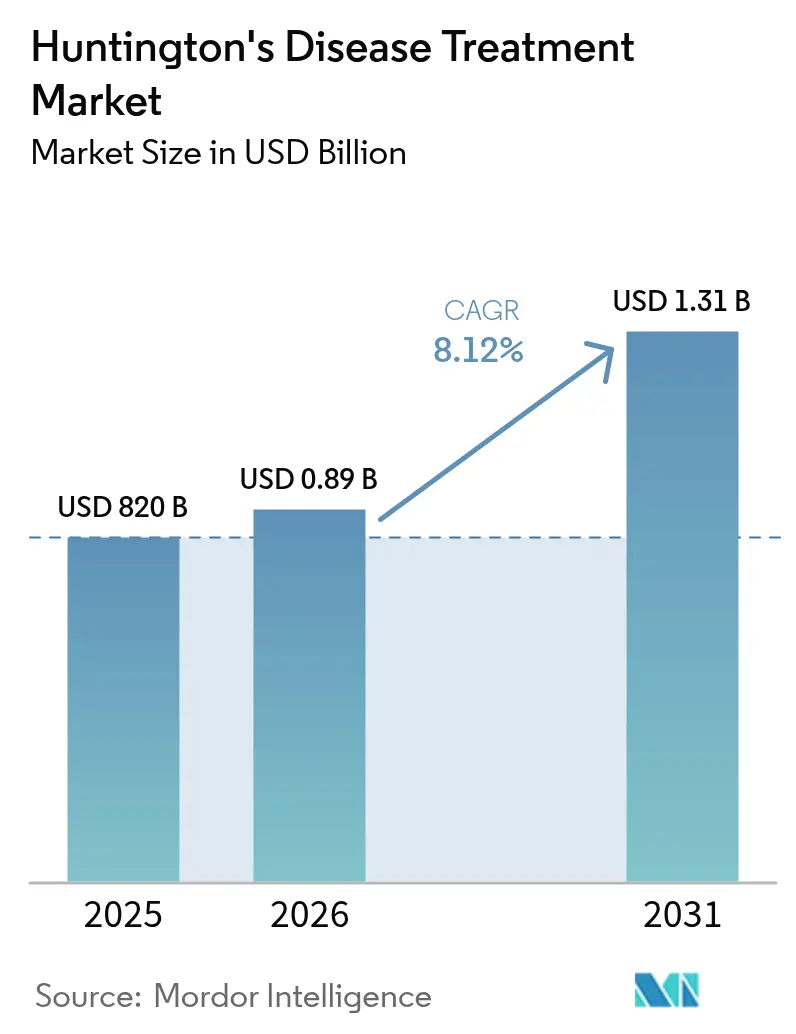

| Market Size (2026) | USD 0.89 Billion |

| Market Size (2031) | USD 1.31 Billion |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

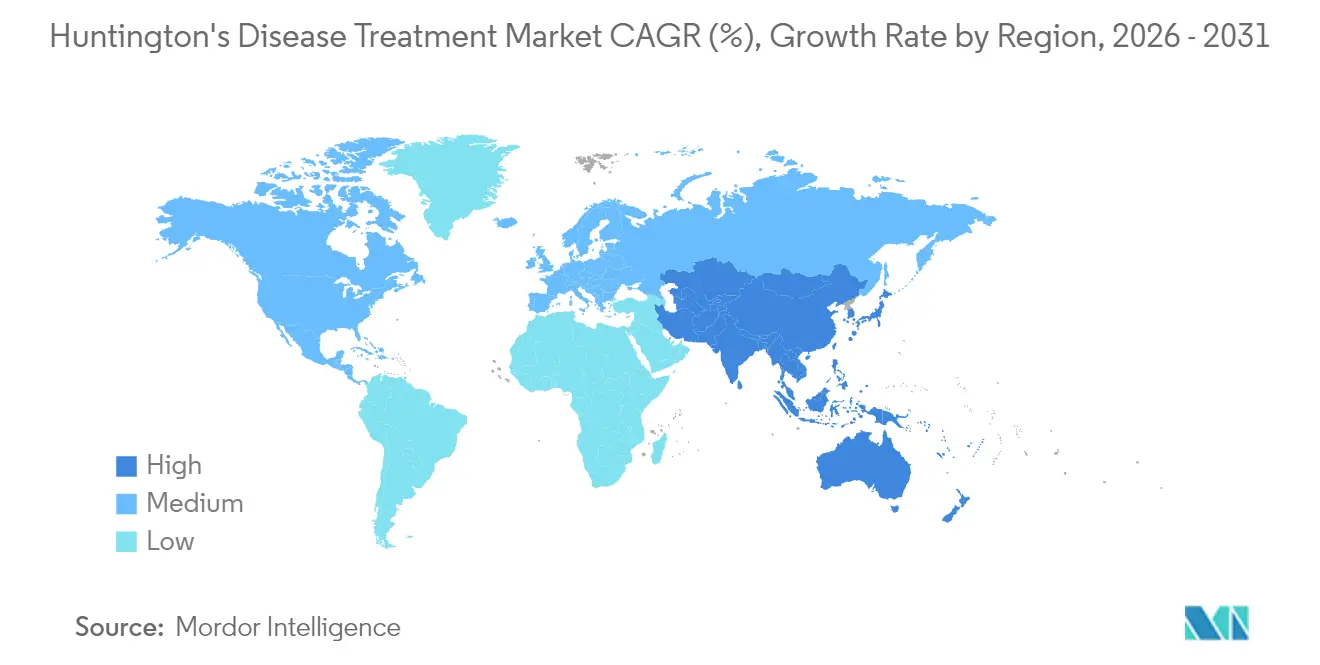

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Huntington's Disease Treatment Market Analysis by Mordor Intelligence

The Huntington's disease treatment market size was valued at USD 820 million in 2025 and estimated to grow from USD 890 million in 2026 to reach USD 1.31 billion by 2031, at a CAGR of 8.12% during the forecast period (2026-2031). This expansion signals a structural pivot from symptomatic relief toward disease-modifying solutions, fueled by breakthrough gene-therapy milestones, accelerated regulatory pathways, and heightened investor confidence. Large-cap transactions such as Novartis’ USD 2.9 billion purchase of PTC 518 underscore the transition of huntingtin-lowering modalities from experimental promise to commercial reality. Concurrently, VMAT2 inhibitor revenues continue to grow, digital biomarkers improve trial design, and innovative financing models emerge to temper gene-therapy costs. Forward momentum is likely to remain strong as platforms achieve surrogate endpoint validation, specialist centers proliferate, and combination regimens linking symptomatic and disease-altering benefits take shape.

Key Report Takeaways

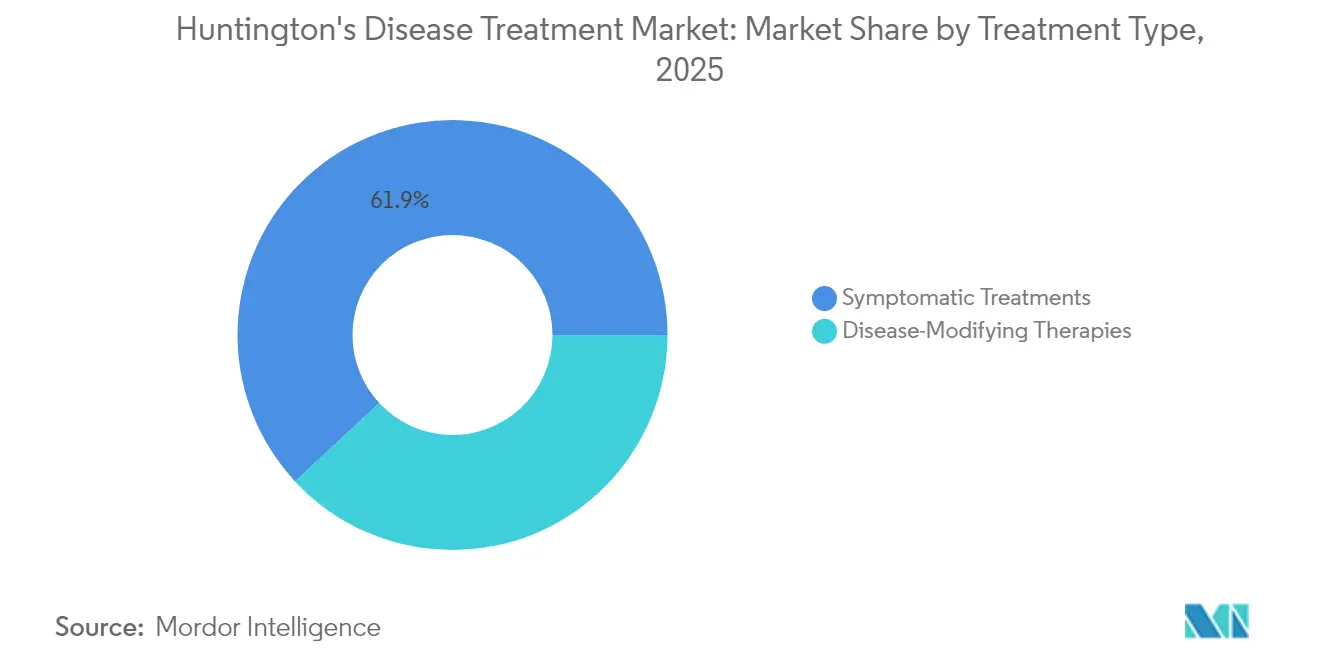

- By treatment type, symptomatic therapy led with 61.92% of the Huntington's disease treatment market share in 2025, while disease-modifying approaches are forecast to grow at a 15.84% CAGR to 2031.

- By route of administration, oral products held 54.05% of the Huntington's disease treatment market size in 2025; intravenous delivery is projected to expand at 11.73% CAGR during 2026-2031.

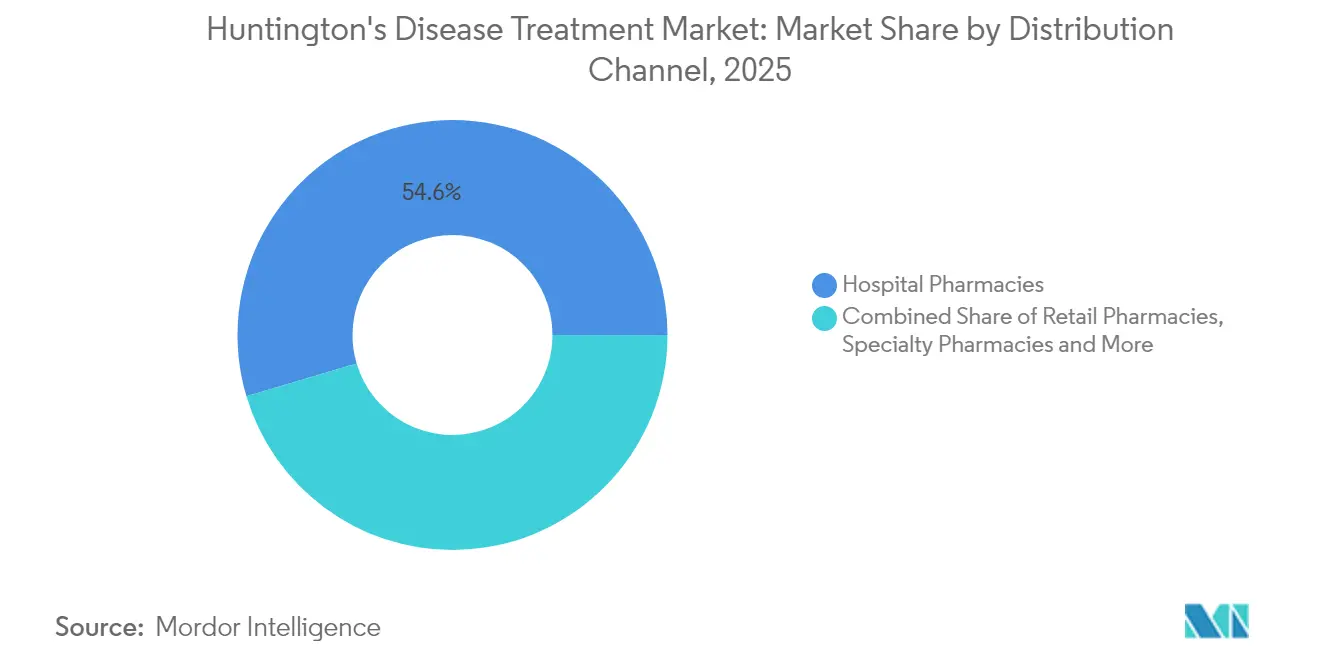

- By distribution channel, hospital pharmacies retained 54.60% revenue share in 2025; specialty and online pharmacies are poised for the fastest 14.92% CAGR through 2031.

- By stage of disease, early-stage patients accounted for 40.25% of the Huntington's disease treatment market size in 2025, whereas the pre-symptomatic cohort is projected to surge at 16.25% CAGR to 2031.

- By geography, North America commanded 38.20% of the Huntington's disease treatment market share in 2025; Asia-Pacific is set to grow at 14.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Huntington's Disease Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence In Ageing-Cohort Populations | +1.2% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Accelerating HTT-Lowering Clinical Pipeline Breakthroughs | +2.8% | Global, led by North America & EU regulatory pathways | Medium term (2-4 years) |

| Commercial Launch Of Once-Daily VMAT2 Inhibitors In Asia | +1.5% | Asia-Pacific core, spill-over to emerging markets | Short term (≤ 2 years) |

| Fast-Track & Orphan Designations In US / EU | +1.8% | North America & EU, with global implications | Medium term (2-4 years) |

| AI-Enabled Biomarker Discovery Improving Trial Success | +0.9% | Global, with early adoption in North America | Long term (≥ 4 years) |

| Beta-Blocker Repurposing Showing Disease-Modifying Signal | +0.6% | Global, with initial focus in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

HTT-lowering clinical pipeline breakthroughs

Multiple platforms now show meaningful mutant huntingtin reductions. WVE-003 produced a 46% cerebrospinal-fluid decrease while sparing wild-type protein, addressing earlier safety concerns[1]Wave Life Sciences, “Positive Results From Phase 1b/2a SELECT-HD Trial,” wavelifesciences.com. Oral PTC 518 delivered up to 43% blood reductions and slowed Total Motor Score progression by more than 70% at 12 months. Investor confidence surged when Novartis paid USD 2.9 billion for PTC 518, crystallising the therapy’s perceived commercial potential. The US FDA’s readiness to accept huntingtin lowering as a surrogate endpoint compresses timelines and mitigates single-platform risk, accelerating the Huntington's disease treatment market trajectory.

Once-daily VMAT2 launches in Asia

Teva’s alliance with Jiangsu Nhwa earned the first deuterated-drug approval in China for AUSTEDO, broadening access to chorea management and creating a springboard for future disease-modifying entries. INGREZZA generated USD 2.3 billion in 2024, with sprinkle formulations easing administration for dysphagic patients. Prevalence disparity—0.40 per 100,000 in Asia versus 5.70 per 100,000 in Europe—necessitates physician-education heavy models rather than mass-market campaigns. Strategic Asian launches therefore extend the Huntington's disease treatment market footprint beyond Western strongholds.

Fast-track and orphan designations in US / EU

AMT-130 gained Breakthrough Therapy status in 2025 after earlier RMAT and Orphan tags, establishing an unprecedented regulatory suite[2]uniQure, “FDA Breakthrough Therapy Designation Granted to AMT-130,” uniqure.com. PTC 518 secured Fast Track classification, and pridopidine entered European marketing review, reflecting agency willingness to accept biomarker-based dossiers. Alignment on using ENROLL-HD external-control data marks a regulatory paradigm shift that favours companies deploying robust real-world evidence frameworks.

Rising incidence in ageing cohorts

Improving diagnostic coverage uncovers more late-onset cases, while global life expectancy gains expand the patient pool. Cohort studies in North America and Europe project prevalence to rise steadily through 2030, giving the Huntington's disease treatment market sustained volume momentum.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ultra-High Cost Of Gene & Cell Therapies | -1.8% | Global, with acute impact in emerging markets | Short term (≤ 2 years) |

| Limited Specialist Centres Outside North America & EU | -1.2% | Asia-Pacific, Latin America, Middle East & Africa | Medium term (2-4 years) |

| Sub-Optimal Adherence To Symptomatic Poly-Pharmacy | -0.7% | Global, with variation by healthcare system | Long term (≥ 4 years) |

| Data-Safety Concerns For CRISPR In Neuronal Tissue | -0.9% | Global, with regulatory focus in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ultra-high cost of gene and cell therapies

List prices eclipsing USD 1 million per patient threaten equitable access. Less than 5% of 10,000 rare diseases have FDA-cleared therapies, underscoring reimbursement hurdles[3]American Society of Gene & Cell Therapy, “Ensuring Patient Access to Gene Therapies,” asgct.org. Payors explore value-based models and reinsurance, yet fragmented adoption keeps many markets out of reach and slows early uptake within the Huntington's disease treatment market.

Limited specialist centres outside US/EU

Black participants in North America experience diagnosis delays approaching 12 months, spotlighting systemic inequities even in advanced systems. Emerging regions often lack intrathecal or gene-therapy facilities, making telemedicine stopgaps rather than substitutes. Infrastructure investment and clinician training therefore remain pre-requisites for global market maturation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Disease-modifying Therapies Drive Innovation

Symptomatic drugs retained 61.92% of the Huntington's disease treatment market share in 2025, yet disease-modifying agents are scaling faster at a 15.84% CAGR through 2031. This pivot enlarges the Huntington's disease treatment market as oral small molecules, antisense oligonucleotides, RNA interference constructs, and AAV gene therapies converge. INGREZZA’s USD 2.3 billion 2024 revenue underscores robust demand for chorea control, while AMT-130’s 80% slowing of disease progression versus external controls illustrates gene therapy’s disruptive promise. Beta-blocker repurposing introduced 34% motor-symptom risk reduction in pre-manifest carriers, bridging symptomatic and modifying paradigms. As combination regimens coalesce, developers will need to optimise sequencing, safety monitoring, and payor evidence packages.

Integrated care models may soon pair once-daily VMAT2 inhibitors with periodic huntingtin-lowering infusions to synchronise acute symptom relief and long-range neuroprotection. The Huntington's disease treatment market size for disease-modifying products is projected to reach USD 590 million by 2031, accounting for nearly 45.00% of incremental revenue growth. Uptake hinges on selective lowering approaches that spare wild-type huntingtin and offer outpatient dosing. Regulatory flexibility around biomarker-driven approvals further lowers market-entry barriers for next-wave candidates targeting DNA-repair pathways and somatic CAG expansion.

By Route of Administration: Intravenous Delivery Gains Momentum

Oral formulations secured 54.05% of the Huntington's disease treatment market size in 2025, aligned with strong adherence and primary-care prescription patterns. Intravenous segment growth at 11.73% CAGR is catalysed by one-time gene therapies and recurrent antisense infusions demanding precise central-nervous-system distribution. Intrathecal delivery remains niche yet essential for allele-selective oligonucleotides that require cerebrospinal-fluid access without systemic exposure.

Drug-delivery engineering now focuses on patient-friendly packaging such as pre-filled syringes and lyophilised powder kits. Hospitals invest in infusion suites with real-time neuro-monitoring, while specialty pharmacies manage cold chain and long-term follow-up. As post-marketing data confirm durability and safety, intravenous share is forecast to approach 29.40% of the Huntington's disease treatment market by 2031. Subcutaneous-to-intravenous switching studies will further refine cost-effectiveness boundaries.

By Distribution Channel: Specialty Pharmacies Capture Growth

Hospital pharmacies held 54.60% revenue in 2025, reflecting initiation of gene therapies and management of acute neuropsychiatric events. Specialty and online outlets are projected to deliver the strongest 14.92% CAGR, supported by direct-to-patient logistics, adherence analytics, and outcomes-based reimbursement administration. Retail pharmacies continue supplying oral symptomatic scripts but are integrating digital tools to flag non-adherence and side-effect patterns.

Pharmaceutical firms co-locate nurse educators within specialty networks to streamline genetic counselling, remote monitoring, and logistical coordination for once-in-a-lifetime infusions. This expansion tightens feedback loops, providing real-world data feeds that regulators increasingly reward. As a result, specialty channels could manage nearly half of Huntington's disease treatment market prescriptions by 2031, shifting bargaining power toward integrated dispensing ecosystems.

By Stage of Disease: Pre-symptomatic Segment Drives Innovation

Early-stage presentations dominated 40.25% of 2025 revenue, yet the pre-symptomatic segment is on track for a 16.25% CAGR through 2031 as biomarker-driven screening identifies carriers long before onset. The Huntington's disease treatment market size for preventive interventions is expected to surpass USD 280 million by 2031. Somatic CAG-repeat assays, neurofilament-light elevations, and digital motor-sensor readouts enrich trial enrolment and validate earlier therapeutic windows.

Mid-stage and late-stage care still absorbs significant resource intensity, with 4.1-year median nursing-home stays and multifaceted palliative requirements. Future pipelines therefore stratify indications: disease-modifying products target prodromal phases, whereas multidrug chorea cocktails and pain-control regimens dominate advanced stages. Telemedicine platforms will coordinate multidisciplinary teams, ensuring longitudinal oversight across disease milestones.

Geography Analysis

North America generated 38.20% of global revenue in 2025, underpinned by FDA leadership on expedited pathways, concentrated specialist clinics, and strong payer adoption of VMAT2 inhibitors. Nevertheless, diagnosis delays in Black populations highlight systemic inequities that temper absolute growth potential. Canada and Mexico collaborate with US centres to widen access to gene therapy trials, fostering cross-border referral channels that steadily enlarge the Huntington's disease treatment market.

Europe leverages regulatory harmonisation to fast-track disease-modifying dossiers, with the EMA reviewing pridopidine for potential H2 2025 launch. Multi-country consortia developed the Huntington Support App, exemplifying cost-efficient digital outreach that offsets uneven clinic density. Germany, United Kingdom, and France lead on trial sponsorship, while Eastern Europe’s modernising neurologic infrastructure promises double-digit gains. Diverse reimbursement systems foster pilot outcomes-based contracts that could migrate to other regions once validated.

Asia-Pacific is the fastest-growing cluster at 14.55% CAGR through 2031, spearheaded by China’s first deuterated-drug approval and Japan’s sophisticated rare-disease registries Teva. South Korea’s dedicated society advances local clinician training, and Australia’s regulatory parallel-processing accelerates international studies. Lower prevalence forces high-touch engagement: physician-led patient mapping, centre-of-excellence accreditation, and remote monitoring fill gaps where infrastructure lags. These initiatives collectively elevate the Huntington's disease treatment market presence across emerging economies. Latin America, the Middle East, and Africa remain nascent yet display improving diagnostic rates and advocacy-driven policy discussions that foreshadow gradual uptake once cost barriers recede.

Competitive Landscape

Competition blends big-pharma scale with biotech specialisation. Teva capitalises on an entrenched VMAT2 franchise, Neurocrine augments its dominance with sprinkle formulations for ingestion-challenged patients, and uniQure spearheads gene-therapy validation via successive FDA designations. PTC 518’s USD 2.9 billion handoff to Novartis illustrates large-cap appetite for de-risked phase-2 assets over first-principles research.

Allele-selective lowering, small-molecule penetrance, and durable AAV payloads form the primary technology races. Delivery differentiates portfolios: intrathecal oligonucleotides contrast with one-time intravenous vectors and daily oral modulators. Competitive edges increasingly arise from biomarker sophistication, real-world evidence strategies, and patient-centric service models that anchor reimbursement negotiations.

White-space opportunities include pain-management combinations, beta-blocker repurposing, and digital-therapeutic adjuncts. Biogen’s new splicing-modulator patents suggest ongoing pursuit of next-generation targeting. Despite escalating pipeline crowding, the Huntington's disease treatment market rewards companies that couple breakthrough biology with pragmatic distribution and evidence frameworks.

Huntington's Disease Treatment Industry Leaders

Pfizer, Inc.

Alnylam Pharmaceuticals Inc.

Teva Pharmaceutical Industries Ltd.

Neurocrine Biosciences, Inc.

Ionis Pharmaceuticals

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: PTC Therapeutics reported PIVOT-HD phase 2 success, achieving significant huntingtin reduction and a favourable safety profile.

- April 2025: uniQure received FDA Breakthrough Therapy designation for AMT-130 following 80% disease-progression slowing versus external controls.

Global Huntington's Disease Treatment Market Report Scope

As per the scope of this report, Huntington's disease treatment covers various treatment modalities that are commercially available. It is a genetic disorder that mostly occurs between 30 and 50 years, leading to the degeneration of nerve cells in the brain.

The Huntington's disease treatment market is segmented by type and end user. By type, the market is segmented as symptomatic treatment and disease-modifying therapies. By end user, the market is segmented as hospital pharmacies, retail pharmacies, and online pharmacies. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America.

| Symptomatic Treatments | VMAT2 Inhibitors |

| Antidopaminergics (Antipsychotics) | |

| Antidepressants & Anxiolytics | |

| Anticonvulsants / Others | |

| Disease-Modifying Therapies | Gene Silencing / ASO |

| Gene Therapy (AAV, LNP etc.) | |

| Stem-Cell Therapy | |

| Small-Molecule HTT Modifiers |

| Oral |

| Intravenous |

| Intrathecal |

| Subcutaneous |

| Hospital Pharmacies |

| Retail Pharmacies |

| Specialty & Online Pharmacies |

| Pre-symptomatic / Prodromal |

| Early-Stage |

| Mid-Stage |

| Late-Stage |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Symptomatic Treatments | VMAT2 Inhibitors |

| Antidopaminergics (Antipsychotics) | ||

| Antidepressants & Anxiolytics | ||

| Anticonvulsants / Others | ||

| Disease-Modifying Therapies | Gene Silencing / ASO | |

| Gene Therapy (AAV, LNP etc.) | ||

| Stem-Cell Therapy | ||

| Small-Molecule HTT Modifiers | ||

| By Route of Administration | Oral | |

| Intravenous | ||

| Intrathecal | ||

| Subcutaneous | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Specialty & Online Pharmacies | ||

| By Stage of Disease | Pre-symptomatic / Prodromal | |

| Early-Stage | ||

| Mid-Stage | ||

| Late-Stage | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the Huntington's disease treatment market?

The market is valued at USD 890 million in 2026 and is on course to reach USD 1.31 billion by 2031

Which therapy segment is growing the fastest?

Disease-modifying therapies are expanding at a 15.84% CAGR through 2031, outpacing symptomatic categories

Why are intravenous therapies gaining traction?

Gene therapies and antisense oligonucleotides require controlled systemic or cerebrospinal delivery, driving 11.73% CAGR for the intravenous segment

Which region offers the highest growth potential?

Asia-Pacific leads in growth with a projected 14.55% CAGR through 2031, propelled by strategic partnerships and regulatory harmonisation

How are high gene-therapy prices being addressed?

Stakeholders explore value-based payment models, reinsurance, and instalment plans to improve affordability for one-time treatments

Page last updated on: