Dyspnea Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

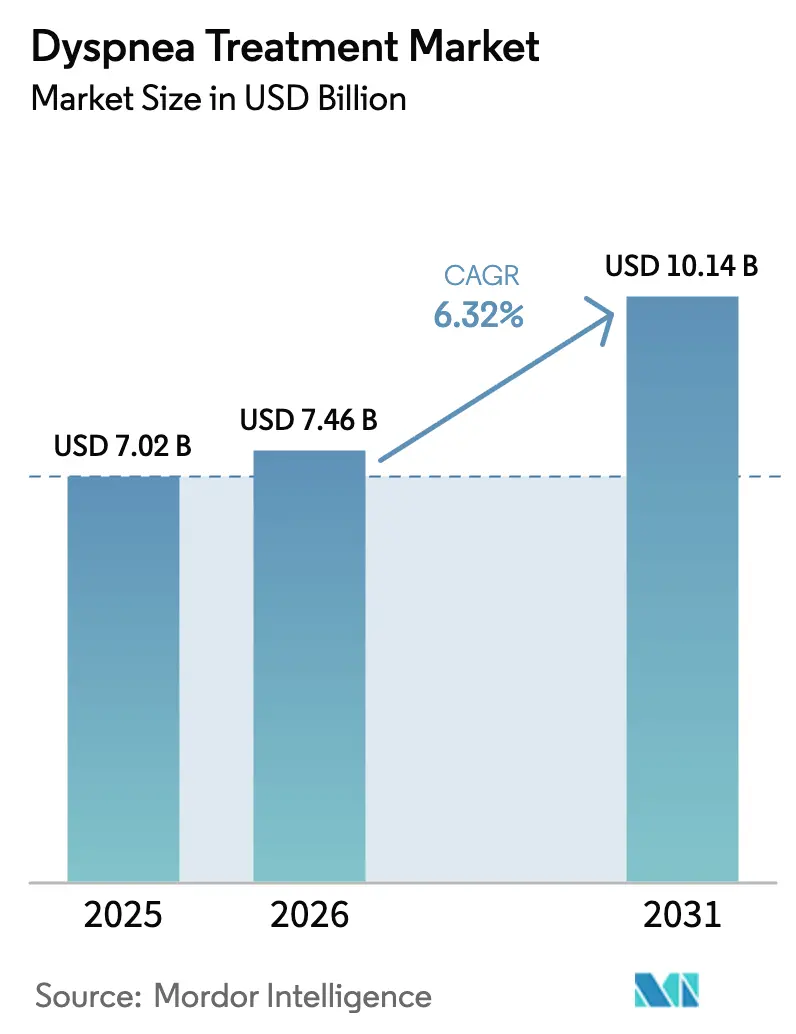

| Market Size (2026) | USD 7.46 Billion |

| Market Size (2031) | USD 10.14 Billion |

| Growth Rate (2026 - 2031) | 6.32% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dyspnea Treatment Market Analysis by Mordor Intelligence

The Dyspnea Treatment Market size was valued at USD 7.02 billion in 2025 and estimated to grow from USD 7.46 billion in 2026 to reach USD 10.14 billion by 2031, at a CAGR of 6.32% during the forecast period (2026-2031). Growth is powered by the rising global prevalence of chronic obstructive pulmonary disease (COPD) and lingering post-COVID-19 respiratory complications that have expanded the treated patient pool. Product innovation is accelerating, highlighted by the US FDA’s June 2024 approval of OHTUVAYRE (ensifentrine), the first COPD inhaler with a new mechanism of action in two decades.[1]Source: US Food and Drug Administration, “Drug Trials Snapshots: OHTUVAYRE,” fda.gov Adoption of home-based oxygen technologies is increasing as Medicare now reimburses virtual pulmonary rehabilitation and as portable concentrators become widely available in middle-income countries. Strategic acquisitions by leading pharmaceutical manufacturers are broadening respiratory portfolios, while biologics targeting eosinophilic COPD subtypes are redefining precision care. Costly high-flow oxygen systems in low-resource hospitals, regulatory complexity for drug-device combinations, and uneven clinician uptake of non-pharmacological tools temper market momentum.

Key Report Takeaways

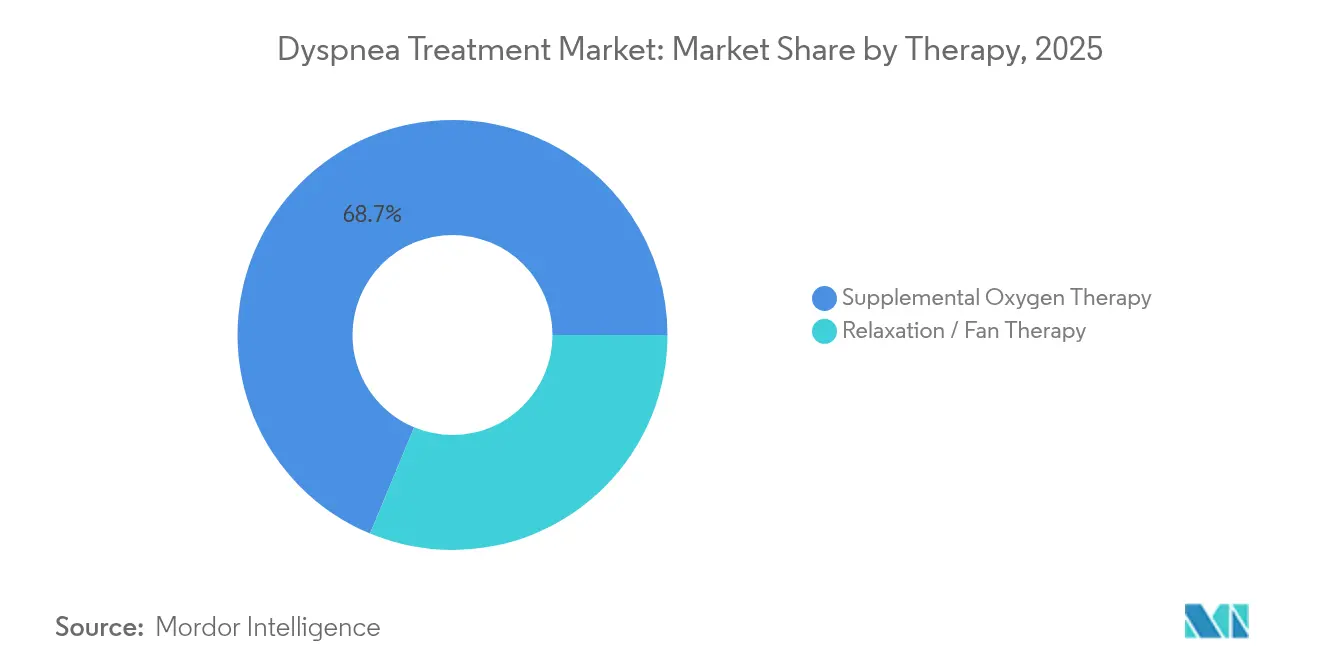

- By treatment type, supplemental oxygen therapy led with 68.74% revenue share in 2025, whereas relaxation and fan therapy is projected to expand at a 5.98% CAGR to 2031.

- By route of administration, inhalation commanded 58.63% of the dyspnea treatment market share in 2025, while oral delivery is poised for the fastest growth at 7.1% CAGR through 2031.

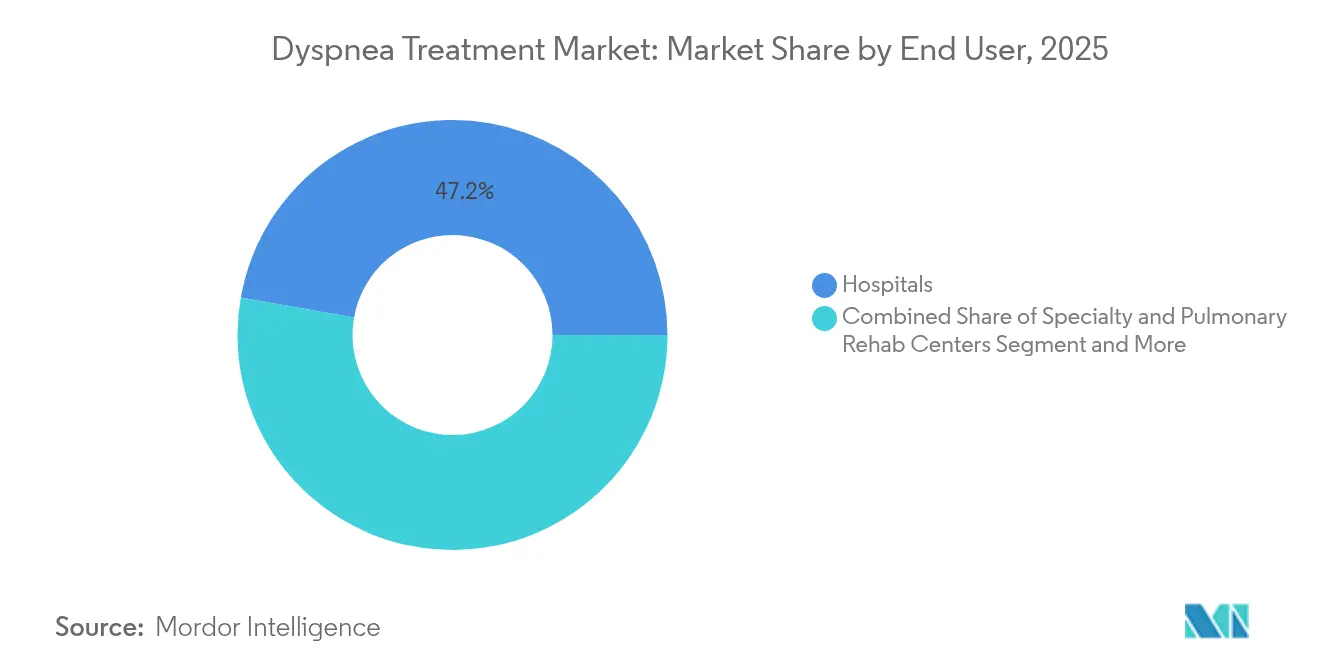

- By end user, hospitals held 47.21% share of the dyspnea treatment market size in 2025; home-care settings are advancing at a 7.48% CAGR between 2026-2031.

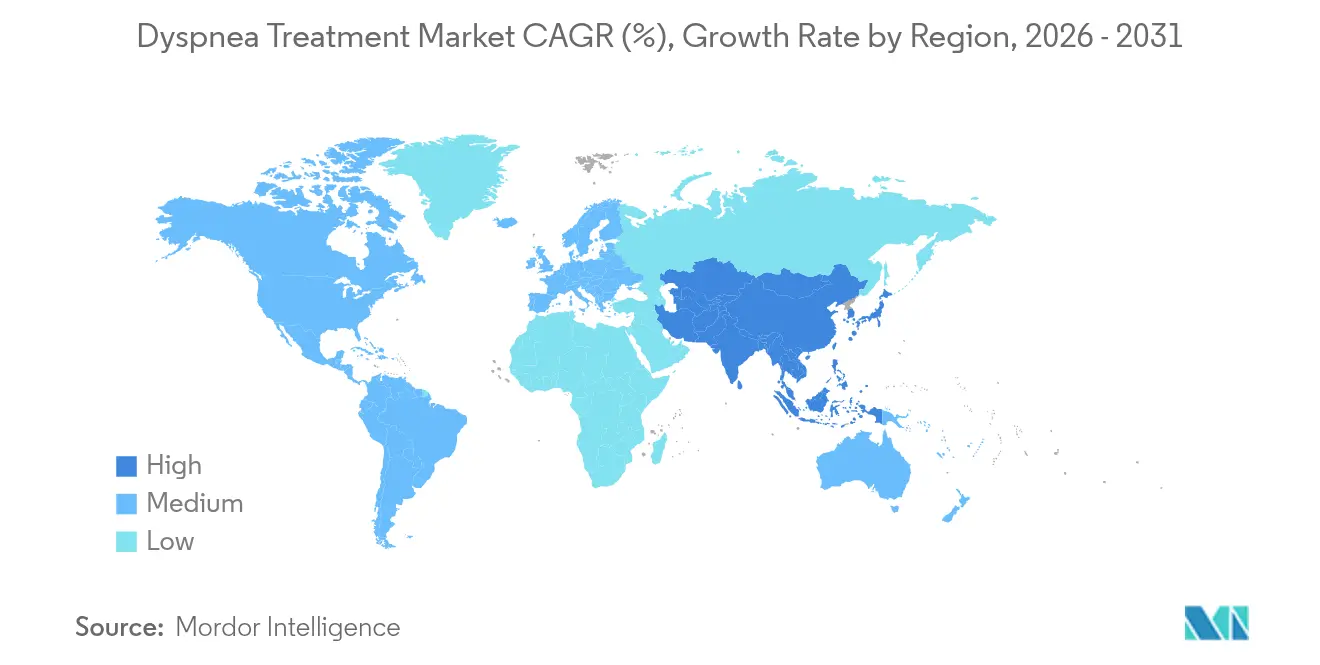

- By geography, North America accounted for 37.66% of the dyspnea treatment market in 2025, whereas Asia-Pacific is forecast to grow at an 7.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dyspnea Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Prevalence of COPD and Post-COVID Breathlessness | +1.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Rapid Uptake of Home Oxygen Concentrators in Middle-Income Countries | +1.2% | APAC core, spill-over to Latin America | Long term (≥ 4 years) |

| Pipeline Arrival of Once-Daily Triple-Combo Inhalers | +0.9% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| AI-Enabled Early-Warning Wearables Reducing ER Dyspnea Admissions | +0.7% | North America & EU pilot markets | Medium term (2-4 years) |

| Reimbursement Expansion for Remote Pulmonary Rehab | +0.6% | North America, selective EU markets | Short term (≤ 2 years) |

| Breakthrough Biologics for Eosinophilic COPD Phenotypes | +0.5% | Global, premium healthcare markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Prevalence of COPD and Post-COVID Breathlessness

Post-COVID-19 cough persists in 48.1% of patients with dyspnea, generating a sizeable new cohort that now enters clinical pathways for chronic breathlessness management. Virtual pulmonary rehabilitation programs demonstrate 99% safe engagement among COPD patients who need supplemental oxygen, proving the viability of tech-enabled interventions. Asia-Pacific markets face an alarming rise in COPD among adults aged 15-49 linked to particulate pollution, underscoring future demand for cost-effective dyspnea therapies. Economic modelling estimates COPD-linked direct and indirect costs could total USD 4.326 trillion from 2020-2050, reinforcing investment urgency.

Rapid Uptake of Home Oxygen Concentrators in Middle-Income Countries

Portable and solar-powered concentrators are proliferating where piped oxygen and cylinder logistics remain weak. Solar systems deliver oxygen at an incremental USD 20 per disability-adjusted life-year saved, a highly cost-effective ratio for resource-constrained hospitals.[2]Source: Nicholas Long et al., “Solar-Powered Oxygen Delivery Systems,” JAMA Network Open, jamanetwork.com The OXFO valve conserved 92.3% oxygen without compromising saturation levels in clinical testing, directly lowering operating costs. Comprehensive oxygen ecosystem programs in Kenya, Rwanda, and Ethiopia boosted procurement volumes by up to 220% at USD 7.34 per patient treated, validating scalable supply-hub models. Patient-controlled flow devices such as FlexO2 raised self-management scores from 14 to 92 points, highlighting empowerment benefits.

Pipeline Arrival of Once-Daily Triple-Combo Inhalers

Ultra-long-acting triple therapies improve adherence and aim to modify disease activity. Depemokimab achieved a 26% reduction in rescue interventions versus placebo in Phase 3 trials, supporting twice-yearly dosing. AstraZeneca completed studies enabling Breztri’s switch to next-generation propellants with 99.9% lower global-warming potential while retaining efficacy. The THARROS trial will evaluate triple therapy impact on severe cardiopulmonary outcomes in 5,000 COPD patients, reflecting a shift to outcome-driven endpoints.

AI-Enabled Early-Warning Wearables Reducing ER Dyspnea Admissions

Respira Labs’ Sylvee device uses acoustic algorithms to detect lung deterioration and seeks FDA clearance within 18 months, with Medicare coverage already in place. The EBCare smart mask from Caltech captures exhaled biomarkers to track airway inflammation in real time, demonstrating how sensor fusion supports proactive care. Wellinks integrated Spire360 analytics to predict decline 10 days in advance, reducing readmissions in pilot programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost of High-Flow Oxygen Systems in LMIC Hospitals | -0.8% | Sub-Saharan Africa, South Asia | Long term (≥ 4 years) |

| Drug-Device Regulatory Mismatches Delaying Combo Launches | -0.6% | Global, particularly EU & US | Medium term (2-4 years) |

| Low Clinician Adoption of Non-Pharma Dyspnea Scoring Tools | -0.4% | Global, rural healthcare settings | Medium term (2-4 years) |

| Patent Expiration Pressures on Established Therapies | -0.3% | North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of High-Flow Oxygen Systems in LMIC Hospitals

The substantial capital requirements for advanced oxygen delivery infrastructure create significant barriers to market penetration in resource-constrained healthcare systems. Sophisticated high-flow units cost more than USD 50,000 each, exceeding budgets in low-resource facilities.[3]Source: George R. Ochieng et al., “High-Flow Oxygen Therapy Systems in Low-Resource Hospitals,” Frontiers in Medicine, frontiersin.org Pulse-oximetry rollouts also struggle with procurement, training, and maintenance costs, limiting guideline uptake. Although solar concentrators show favourable cost-effectiveness, initial financing remains a hurdle. Alternative approaches like the low-cost SpO2 integrated neonatal CPAP device, costing under USD 200, show promise but require extensive validation and regulatory approval processes that further delay implementation.

Drug-Device Regulatory Mismatches Delaying Combo Launches

The FDA’s draft bioequivalence guidance for triple fixed-dose sprays requires seven in-vitro and multiple in-vivo studies, extending timelines and raising costs for developers. Divergent EMA requirements further complicate synchronization, despite parallel advice programs designed to streamline rare-disease products. These regulatory mismatches create uncertainty for investors and developers, potentially delaying breakthrough innovations that could significantly improve dyspnea management outcomes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy: Supplemental Oxygen Therapy Dominance Challenged by Innovation

Supplemental oxygen therapy represented 68.74% of 2025 revenue, reflecting entrenched clinical protocols and dependable reimbursement. Evidence from large COPD cohorts confirms sustained demand, particularly for ambulatory and nocturnal hypoxemia management. Yet relaxation and fan therapy is expanding at a 5.98% CAGR as randomized studies validate symptom relief and as value-based care incentivizes non-pharmacological tools. The dyspnea treatment market size for relaxation and fan modalities is on course to widen steadily, aided by cost-conservation devices such as OXFO that save 92.3% oxygen while maintaining target saturation levels.

Drug classes pivot toward precision medicine and environmental sustainability. Long-standing corticosteroid and anticholinergic categories retain broad utility, but biologics like depemokimab offer twice-yearly dosing and possible disease modification. Handheld fan trials reveal meaningful Visual Analogue Scale improvements, accelerating institutional acceptance. These dynamics suggest the dyspnea treatment market will witness gradual erosion of oxygen therapy’s share as low-cost, evidence-backed alternatives scale globally.

By Route of Administration: Inhalation Leadership Faces Oral Challenge

Inhalation held 58.63% of the dyspnea treatment market share in 2025 as direct pulmonary delivery ensures rapid relief and lower systemic exposure. Environmental compliance is now pivotal; Breztri’s near-zero GWP propellant exemplifies how inhaler innovation must align with climate policy. The FDA approval of OHTUVAYRE underscores ongoing room for breakthrough inhaled mechanisms despite maturity.

Oral delivery is the fastest growing at 7.1% CAGR, reflecting patient preference and emerging agents such as nerandomilast that demonstrate forced vital capacity gains in idiopathic pulmonary fibrosis. Formulation advances that enhance bioavailability are eroding historical efficacy gaps versus inhaled routes. As adherence data accumulate, the dyspnea treatment market size for oral products is projected to expand, challenging inhalation’s dominance while fostering multimodal regimens.

By End User: Hospital Dominance Shifts Toward Home Care

Hospitals retained 47.21% revenue share in 2025 through management of acute respiratory distress, invasive monitoring, and high-risk interventions. The segment benefits from multidisciplinary teams and reimbursement structures that favour inpatient care for severe exacerbations.

Home-care settings are growing at 7.48% CAGR as payers encourage decentralised models. Medicare’s coverage of remote rehabilitation and the widespread rollout of patient-controlled oxygen devices have enabled complex care outside institutional walls. Visual Analogue Scale improvements from 14 to 92 points with FlexO2 confirm strong patient acceptance. The dyspnea treatment market size for home-care solutions is set to climb steadily as remote monitoring platforms prove cost-effective and as chronic disease management policies shift risk to community settings.

Geography Analysis

North America generated 37.66% of 2025 revenue on the back of robust insurance coverage, established rehabilitation networks, and rapid regulatory clearance for novel therapeutics. CPT 94625 and 94626 improved pulmonary rehabilitation payment parity, fueling virtual program adoption. OHTUVAYRE’s FDA approval confirms the region’s innovation leadership. Pharmaceutical copay caps, such as Boehringer Ingelheim’s USD 35 ceiling, address affordability gaps that could otherwise constrain uptake.

Asia-Pacific is the fastest growing with an 7.78% CAGR. COPD underdiagnosis in Japan, where only 8.4% of airflow-obstructed individuals receive a formal diagnosis, highlights latent demand. Solar-powered concentrators and PSA plants deliver oxygen at favourable DALY-based cost ratios suitable for emerging economies. Workforce initiatives in China that pair academic respiratory therapy programs with tertiary hospitals aim to meet escalating service needs.

Europe maintains steady progress owing to universal health systems and strict evidence thresholds. The European Respiratory Society’s guidelines expedite uniform adoption of validated interventions. Environmental regulations advance propellant reforms, positioning the region as a catalyst for low-GWP inhaler transitions. Latin America, Africa, and the Middle East remain smaller but strategic, leveraging innovations such as solar concentrators and regional oxygen hubs to bypass legacy infrastructure barriers.

Competitive Landscape

Market competition is moderate yet intensifying. GSK acquired Aiolos Bio for USD 1 billion to secure a TSLP-targeting asset, while AstraZeneca bought Almirall’s respiratory franchise for USD 2 billion to deepen speciality focus. These moves consolidate late-stage pipelines and widen global reach. FDA clearance of OHTUVAYRE and approval of Nucala for eosinophilic COPD reshape therapeutic classes, raising entry thresholds for entrants that lack biologic or novel inhaler platforms.

Patent expirations accelerate innovation cycles. Boehringer Ingelheim’s push into PDE4B inhibition anticipates Ofev’s loss of exclusivity. Developers are also investing in low-GWP propellants; DevPro Biopharma’s DP007 is on track for mid-2027 launch with 99.9% lower climate impact.

Digital health disruptors such as Respira Labs and Wellinks cultivate predictive analytics ecosystems that integrate wearables, cloud analytics, and reimbursement-grade reporting. Partnerships between sensor firms and spirometry vendors signal convergence toward closed-loop management solutions. Competitive advantage now hinges on technology differentiation, environmental stewardship, and precision-guided biologics rather than sheer scale.

Dyspnea Treatment Industry Leaders

Mayne Pharma Group Limited

Hikma Pharmaceuticals plc

Lannett Company, Inc.

GlaxoSmithKline

Teva Pharmaceutical Industries Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: DevPro Biopharma and Bespak finished feasibility studies for DP007, a low-GWP albuterol inhaler, with clinical trials slated for late 2025

- December 2024: Teva launched a patient-access program with Direct Relief to supply inhalers free of charge to uninsured US residents.

- June 2024: BARDA selected multiple candidates for platform trials in acute respiratory distress syndrome, expanding federal support for dyspnea therapeutics.

Global Dyspnea Treatment Market Report Scope

As per the scope of the report, dyspnea, also referred to as air hunger, is characterized as shortness of breath. Mild, transient, serious, and persistent shortness of breath is all possible. Dyspnea can be brought on by excessive exertion, spending time at high altitudes, and a variety of other conditions. Dyspnea Treatment Market is segmented By Treatment Type (Therapy (Supplemental Oxygen Therapy, Relaxation Therapy), Drugs (Antianxiety Drugs, Antibiotics, Anticholinergic Agents, Corticosteroids, Others), End-user (Hospitals, Home Care, Specialty Centers, Others), and Geography (North America, Europe, Asia-Pacific, and Rest of the World). The report offers the value (in USD million) for the above segments.

| Therapy | Supplemental Oxygen Therapy |

| Relaxation / Fan Therapy | |

| Drug Class | Antianxiety Agents |

| Antibiotics | |

| Anticholinergic Agents | |

| Corticosteroids | |

| Others |

| Oral |

| Inhalation |

| Others |

| Hospitals |

| Home Care Settings |

| Specialty and Pulmonary Rehab Centers |

| Ambulatory Surgical Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Therapy | Supplemental Oxygen Therapy |

| Relaxation / Fan Therapy | ||

| Drug Class | Antianxiety Agents | |

| Antibiotics | ||

| Anticholinergic Agents | ||

| Corticosteroids | ||

| Others | ||

| By Route of Administration | Oral | |

| Inhalation | ||

| Others | ||

| By End User | Hospitals | |

| Home Care Settings | ||

| Specialty and Pulmonary Rehab Centers | ||

| Ambulatory Surgical Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the dyspnea treatment market?

The market stands at USD 7.46 billion in 2026 and is forecast to reach USD 10.14 billion by 2031.

Which treatment type holds the largest market share?

Supplemental oxygen therapy leads with 68.74% share in 2025, remaining the cornerstone intervention across care settings.

Why is Asia-Pacific the fastest growing region?

Rapidly aging populations, rising COPD prevalence, and adoption of cost-effective oxygen technologies drive an 7.78% CAGR through 2031.

How are reimbursement changes influencing home-based care?

New Medicare billing codes and virtual rehabilitation coverage have accelerated the shift toward home-care settings, which now grow at 7.48% CAGR.

What technological trends will shape future market growth?

Low-GWP inhalers, precision biologics for eosinophilic COPD, and AI-enabled wearables that predict exacerbations are set to redefine competitive advantage.

What are the main barriers to wider adoption of non-pharmacological dyspnea therapies?

High equipment costs in low-resource hospitals, regulatory complexities for combination products, and limited clinician familiarity with evidence-based scoring tools slow uptake.

Page last updated on: