Ear Infection Treatment Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Market Size (2026) | USD 13.39 Billion |

| Market Size (2031) | USD 17.12 Billion |

| Growth Rate (2026 - 2031) | 5.05% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

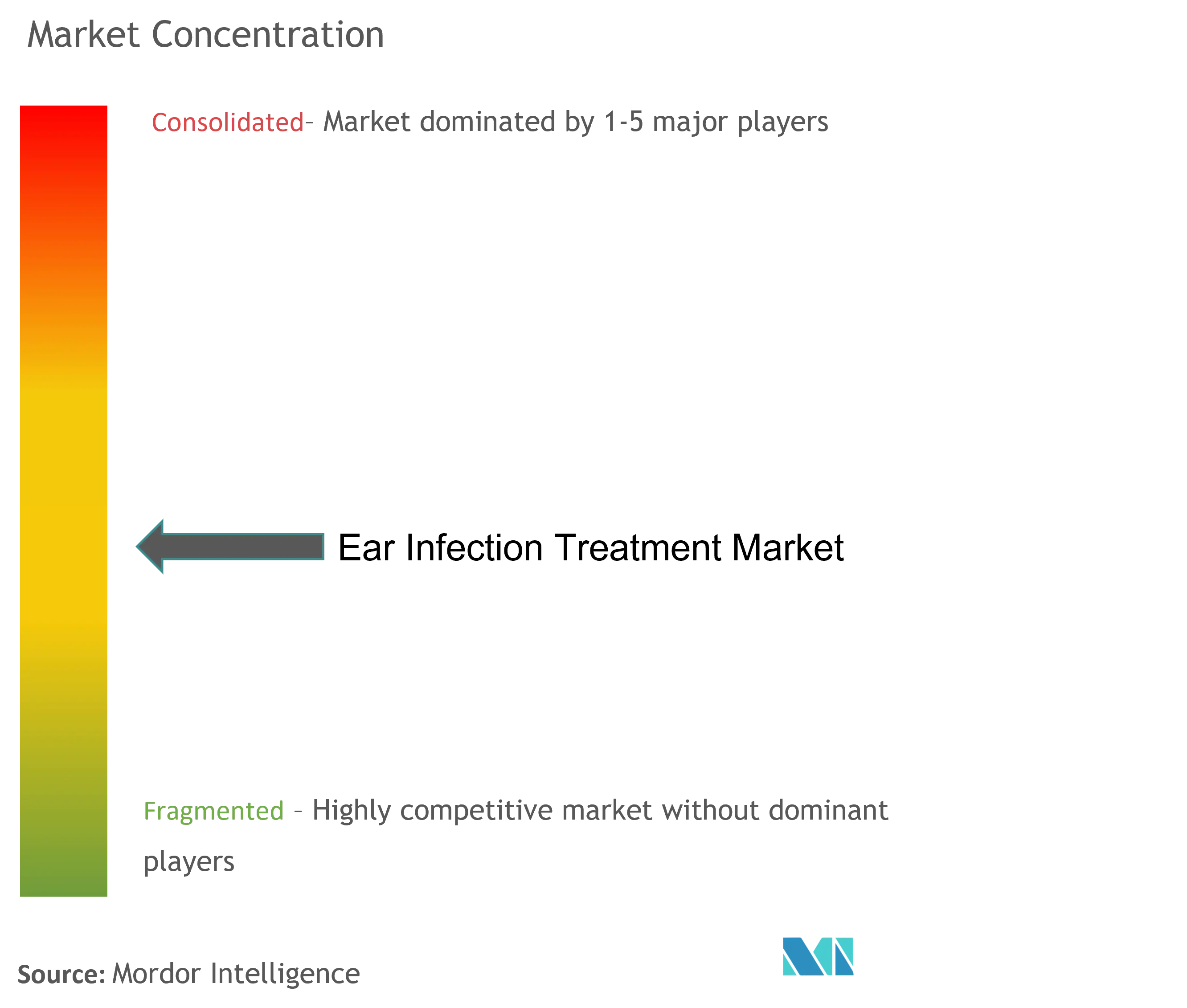

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ear Infection Treatment Market Analysis by Mordor Intelligence

The Ear Infection Treatment Market size was valued at USD 12.75 billion in 2025 and estimated to grow from USD 13.39 billion in 2026 to reach USD 17.12 billion by 2031, at a CAGR of 5.05% during the forecast period (2026-2031). Growth is underpinned by rising antimicrobial resistance, the broad pediatric disease burden, and sustained product innovation across drugs, diagnostics, and minimally invasive devices. Recent genomic surveillance confirms that 30% of Streptococcus pneumoniae isolates are penicillin-resistant and that 30% of Haemophilus influenzae strains contain beta-lactamase genes, prompting clinicians to adopt targeted therapies that preserve antibiotic efficacy.[1]Source: Briallen Lobb et al., “Genomic Classification and Antimicrobial Resistance Profiling of Streptococcus pneumoniae and Haemophilus influenzae,” BioMed Central, pubmed.ncbi.nlm.nih.gov Updated pneumococcal vaccination schedules, the emergence of probiotic prophylaxis, and the FDA’s support for office-based tympanostomy collectively expand therapeutic options. Meanwhile, artificial-intelligence-enabled otoscopy and ultrasound imaging reduce diagnostic uncertainty and cut unnecessary antibiotic use. Asia-Pacific now registers the fastest regional CAGR at 7.94%, fueled by universal health coverage programs that extend ENT care to previously underserved populations.

Key Report Takeaways

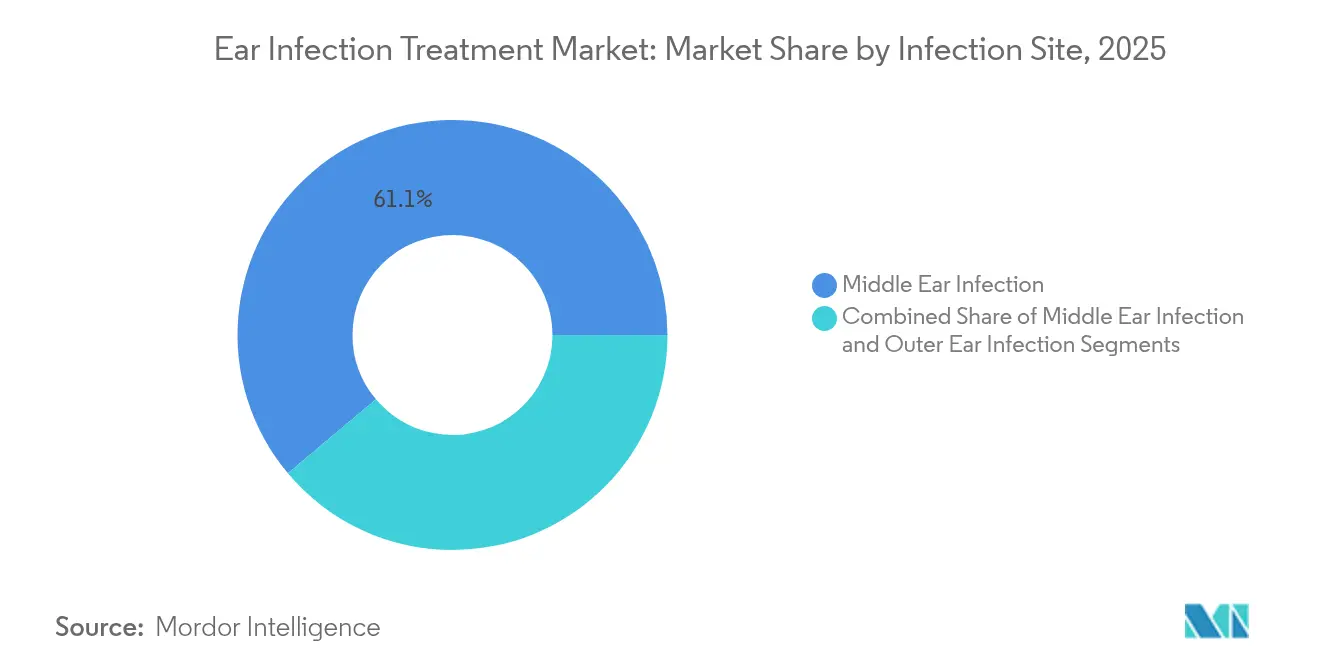

- By infection site, middle ear infection led with 61.12% revenue share in 2025; inner ear infection is expanding at a 6.48% CAGR through 2031.

- By cause pathogen, bacterial infections held 71.45% ear infection treatment market share in 2025, whereas viral infections are projected to record a 7.01% CAGR through 2031.

- By medication, antibiotics captured 48.35% of 2025 revenue; antivirals represent the fastest-growing modality at a 6.66% CAGR for the forecast period.

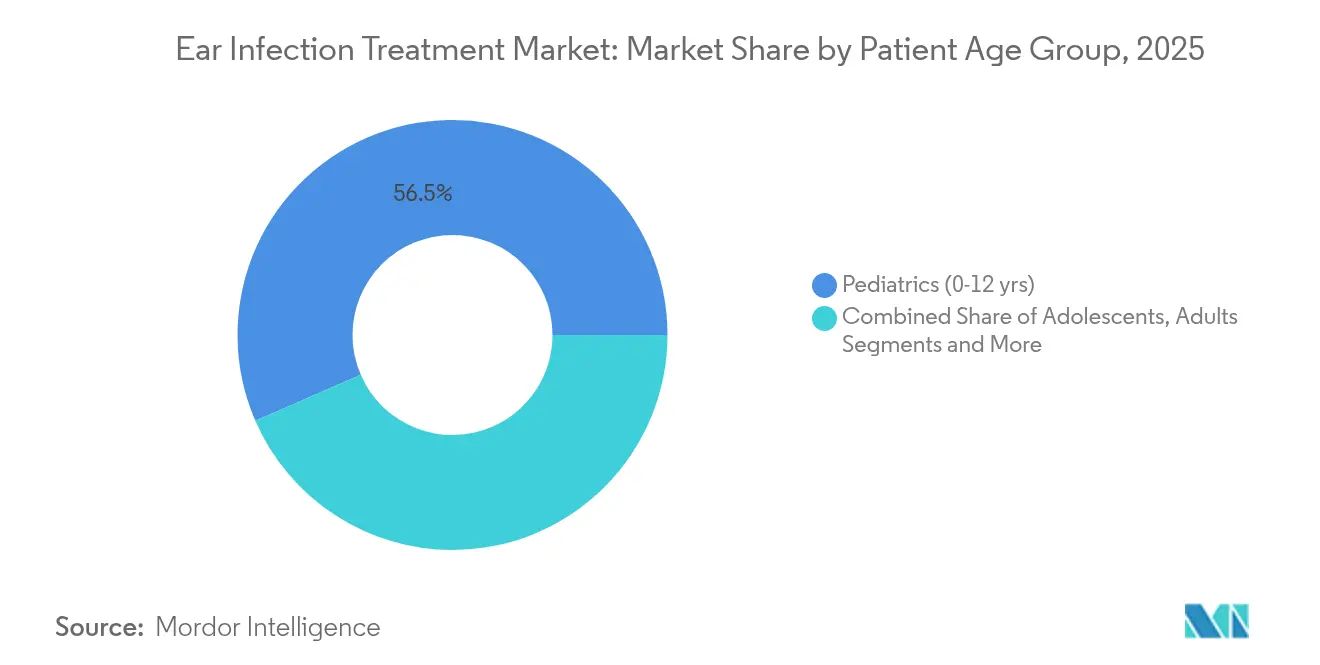

- By patient age group, the pediatric (0-12 yrs) segment commanded 56.52% of the ear infection treatment market size in 2025, while adults aged 18-64 years are forecast to advance at a 6.73% CAGR up to 2031.

- By end user, hospitals led with 47.05% revenue share in 2025, yet ambulatory surgical centers are expanding at a 6.78% CAGR through 2031.

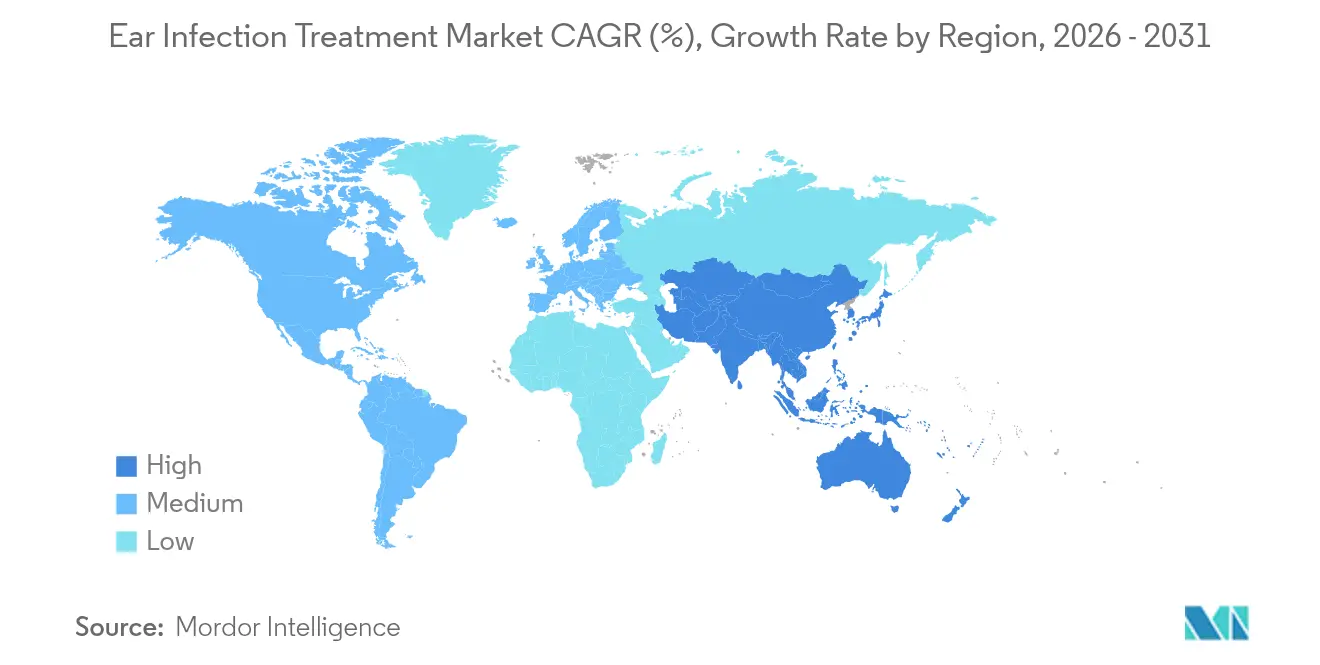

- By geography, North America accounted for 37.86% of 2025 revenue, whereas Asia-Pacific exhibits the highest 7.68% CAGR momentum to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ear Infection Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Recurrent Otitis Media Among Paediatric Population | +1.2% | Global, with highest impact in North America & Europe | Medium term (2-4 years) |

| Growing Adoption of Minimally-Invasive Tympanostomy Tube Devices | +0.8% | North America & Europe, expanding to APAC | Short term (≤ 2 years) |

| Availability of Fixed-Dose Antibiotic-Corticosteroid Otic Formulations | +0.6% | Global | Short term (≤ 2 years) |

| Expansion of Tele-Otoscopy and Remote ENT Consultations | +0.4% | North America & Europe, early adoption in urban APAC | Medium term (2-4 years) |

| Pipeline of Probiotic & Microbiome-Based Preventive Therapies | +0.7% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Government-Backed Childhood Vaccination and Surveillance Programmes | +0.9% | Global, with strongest impact in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Recurrent Otitis Media Among Paediatric Population

Clinical evidence indicates that 93% of children experience at least one acute otitis media episode by age 3, while daycare attendance accelerates cross-contamination and resistant pathogen spread.[2]Source: OtoNexus Medical Technologies, “Clinical Outcomes — OtoNexus,” otonexus.com Developmental delays and classroom absences associated with recurrent infections create economic and social pressure that fuels demand for both therapeutic and prophylactic solutions. Parents prioritize treatments with proven safety in infants, driving investment into age-appropriate drug formulations and needle-free delivery systems. Pharmaceutical companies respond with high-dose amoxicillin regimens that offset partial resistance without escalating toxicity. Payers in North America and Western Europe increasingly reimburse prophylactic measures, including pneumococcal vaccination boosters and probiotic supplements, to curb long-term costs.

Growing Adoption of Minimally Invasive Tympanostomy Tube Devices

The Hummingbird TTS and Tula Systems enable office-based ear tube placement in children as young as 6 months, eliminating general anesthesia and operating-room scheduling delays. FDA recognition through HCPCS code G0561 broadens third-party reimbursement and drives rapid uptake among pediatric otolaryngologists. Curved-lumen tube designs improve fluid drainage and resist biofilm formation, lowering failure rates. Early clinical data show a 40% reduction in repeat procedures compared with conventional straight tubes, encouraging adoption in cost-constrained hospital systems. Asia-Pacific clinics are beginning to import the technology under expedited regulatory pathways, supporting regional growth projections.

Availability of Fixed-Dose Antibiotic-Corticosteroid Otic Formulations

Combination drops such as ciprofloxacin–dexamethasone and ciprofloxacin–fluocinolone acetonide achieve 61.2% cure rates in pediatric otitis media with tubes, outperforming historical monotherapy benchmarks. Concomitant anti-inflammatory action relieves pain rapidly, improving adherence and reducing night-time emergency visits. Companies leverage 505(b)(2) pathways to reformulate legacy molecules, accelerating market entry and extending patent life. Caregiver preference for twice-daily dosing over traditional four-times schedules boosts real-world effectiveness. Widespread pediatric approval across the United States and Europe establishes a commercial foothold that new entrants replicate in Latin America.

Pipeline of Probiotic & Microbiome-Based Preventive Therapies

Randomized trials show that Lactobacillus salivarius PS7 supplementation lowers acute otitis media incidence by 20% in high-risk children. Streptococcus salivarius strains inhibit Haemophilus influenzae biofilm formation, providing a biologically plausible mechanism for relapse prevention. Industry analysts forecast regulatory approval of the first ENT-focused probiotic lozenge within five years in the European Union. Market access strategies centre on over-the-counter positioning to bypass reimbursement hurdles while partnering with paediatric associations for guideline inclusion. Over time, successful prophylaxis could dampen antibiotic demand, but near-term adoption primarily addresses resistance stewardship mandates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Antimicrobial Resistance to First-Line Antibiotics | -1.1% | Global, with highest impact in developing markets | Medium term (2-4 years) |

| High Cost & Post-Operative Complications of Ear Surgeries | -0.7% | Global, particularly impacting emerging markets | Short term (≤ 2 years) |

| Limited Reimbursement for Advanced Otic Devices in EMs | -0.5% | Emerging markets in APAC, MEA, and Latin America | Long term (≥ 4 years) |

| Regulatory Safety Warnings on Fluoroquinolone Ear Drops | -0.3% | Global, with strongest impact in North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Antimicrobial Resistance to First-Line Antibiotics

Escalating antimicrobial resistance fundamentally challenges traditional ear infection treatment paradigms, with genomic surveillance revealing alarming resistance patterns among primary otitis media pathogens. Studies report 100% ampicillin resistance and 90.9% cefoxitin resistance in Staphylococcus aureus isolates, while Pseudomonas aeruginosa shows only 65.2-67.4% fluoroquinolone susceptibility. Clinicians must escalate to second-line agents such as ceftriaxone, increasing direct drug spend and raising adverse-event risk. Empiric broad-spectrum prescribing amplifies selective pressure, perpetuating a resistance spiral that undercuts long-term market sustainability. The emergence of biofilm-forming resistant strains particularly complicates chronic and recurrent infections, necessitating alternative therapeutic approaches.

High Cost & Post-Operative Complications of Ear Surgeries

Surgical intervention costs create significant barriers to optimal ear infection management, with tympanostomy tube procedures ranging from USD 782 to USD 1,558 across different U.S. states, reflecting substantial geographic disparities in healthcare accessibility.[3]Source: Sidecar Health, “Cost of Ear Tube Surgery by State,” sidecarhealth.com Post-operative events such as blockage or premature extrusion necessitate revision in 7-20% of cases, adding to the economic load. Insurance prior authorization policies elongate wait times, risking progression to chronic infections and conductive hearing loss. The concentration of specialized ENT services in urban centers also creates access barriers for rural populations, exacerbating health disparities in ear infection treatment outcomes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Infection Site: Middle Ear Dominance Drives Innovation

Middle ear conditions accounted for 61.12% of 2025 revenue, making them the backbone of the ear infection treatment market. Innovations such as ultrasound otoscopy now detect middle ear effusion within seconds, increasing diagnostic certainty and cutting inappropriate antibiotics by up to 50%. The ear infection treatment market size for middle ear interventions is projected to expand in the coming years, reflecting continual demand for precise, site-specific therapies. Inner ear infections, though smaller in volume, post a 6.48% growth trajectory as imaging improves detection of vestibular sequelae. Outer ear infections remain steady, supported by topical antimicrobial advances.

Second-generation drug-delivery systems target the middle ear space with sustained-release gels and liposome carriers that achieve complete pathogen eradication in 24 hours in preclinical trials. Manufacturers plan clinical studies that could reshape standard-of-care regimens and reduce total antibiotic exposure. Meanwhile, single-dose intratympanic injections are undergoing pivotal trials aimed at lowering caregiver burden and improving adherence.

By Cause Pathogen: Bacterial Infections Lead Despite Viral Momentum

Bacterial pathogens retained 71.45% ear infection treatment market share in 2025. The introduction of higher-valency pneumococcal vaccines realigns bacterial serotype prevalence, necessitating agile formulation updates among antibiotic producers. Viral infections are the fastest-growing etiologic segment with a 7.01% CAGR to 2031 as molecular diagnostics reveal a larger viral contribution than previously recognized. Antiviral R&D pipelines respond with neuraminidase and endonuclease inhibitors tailored for otologic delivery.

Fungal infections remain niche yet clinically important in immunocompromised cohorts. Surveillance studies show fungi involved in 41.7% of refractory auricular perichondritis cases, underscoring the need for pathogen-specific therapeutics. Device makers investigate antifungal coatings for ventilation tubes to reduce postoperative colonization.

By Medication: Antibiotics Dominate Amid Antiviral Growth

Antibiotics garnered 48.35% of 2025 turnover, positioning them at the center of the ear infection treatment industry. However, stewardship policies and black-box warnings on ototoxicity spur parallel development of topical antiseptics, hypochlorous acid formulations, and nanowire bactericidal devices. Antivirals are expanding at 6.66% CAGR as rapid PCR panels direct therapy within minutes. Analgesics and non-steroidal anti-inflammatory drops support symptomatic relief, while device-based therapies such as negative-pressure ear pumps provide non-pharmacological options. Surgical interventions increasingly migrate to office settings, capturing patients previously unwilling to undergo general anesthesia.

The emergence of non-antibiotic treatments gains momentum as clinicians seek alternatives to traditional antimicrobial therapy. Systematic reviews demonstrate comparable efficacy between topical antiseptics and antibiotics for acute otitis externa, supporting antibiotic stewardship initiatives. Innovative approaches, including hypochlorous acid delivery systems and nanowire-based treatments, show promise in preclinical studies, potentially revolutionizing bacterial infection management. The integration of artificial intelligence in treatment selection optimizes therapeutic outcomes by matching pathogen profiles with optimal antimicrobial regimens.

By Patient Age Group: Pediatric Focus Sustains Market Evolution

The pediatric segment captured 56.52% of 2025 revenue, reflecting anatomical susceptibility and immature immune responses. Italian consensus guidelines recommend narrow-spectrum amoxicillin at 90 mg/kg/day as first-line therapy, supporting precision dosing initiatives. Adult disease is now the fastest-growing sub-segment at 6.73% CAGR because of heightened awareness of work-related productivity losses. Workplace health programs subsidize tele-otoscopy to limit absenteeism, driving adult diagnosis rates.

Geriatric patients present polypharmacy challenges; developers pursue low-interaction formulations, including fluoroquinolone-sparing regimens to avoid QT prolongation risks. Adolescents transition between pediatric and adult guidelines, necessitating flexible dosing tools embedded in electronic prescribing platforms.

By End User: Hospital Dominance Gives Way to Ambulatory Care

Hospitals maintained a 47.05% slice of 2025 revenue, yet outpatient migration accelerates. Ambulatory surgical centers exhibit a 6.78% CAGR as payers shift procedures away from high-cost inpatient settings. ENT clinics benefit from integrated imaging that speeds decision-making and reduces referrals. Home-care settings expand via telemedicine and smartphone diagnostics, particularly in rural locales. The ear infection treatment market size attributed to home-based monitoring is expected to double by 2030, aided by reimbursement for remote patient monitoring codes.

Ambulatory surgical centers benefit from regulatory changes supporting in-office procedures and improved reimbursement for minimally invasive interventions. The FDA's clearance of office-based tympanostomy systems eliminates traditional barriers to outpatient surgical care, reducing costs and improving patient convenience. Home-care adoption accelerates through smartphone-based diagnostic applications, with FDA-listed devices enabling caregiver-led ear infection screening. This care delivery evolution reduces healthcare system burden while improving patient access to timely interventions.

Geography Analysis

North America contributed 37.86% of 2025 global sales, leveraging robust insurance coverage and rapid technology uptake. Medicare now reimburses office-based tympanostomy, driving procedure volumes in outpatient suites. Canada’s single-payer system ensures near-universal vaccine coverage, lowering severe infection incidence but sustaining prophylactic demand. Mexico’s private hospital growth introduces premium device adoption.

Europe follows with strong public health systems that back probiotic and vaccination strategies. The region’s directive on antimicrobial stewardship limits broad-spectrum prescribing, stimulating fixed-dose combination launches. Middle East and Africa record gradual uptake hindered by fragmented reimbursement but benefit from philanthropic vaccination drives. South America sees private insurers piloting tele-otoscopy to reach remote Amazonian communities.

Asia-Pacific represents the fastest-growing region at 7.68% CAGR. China’s Healthy China 2030 plan expands ENT capacity, while India’s code of conduct for medical-device marketing fosters transparent commercialization. Japan addresses an aging demographic with integrated hearing and vestibular clinics. Australia’s telehealth incentives overcome geographic isolation.

Competitive Landscape

The ear infection treatment market shows moderate fragmentation. Traditional pharmaceutical incumbents such as Amneal focus on generic combination drops after securing FDA approval, while medical-technology startups offer disruptive diagnostic imaging that halves unnecessary antibiotic use. Smith & Nephew acquired Tusker Medical to gain the Tula System in July 2024, broadening its ENT device portfolio. Integra LifeSciences bought Acclarent in April 2024 to integrate minimally invasive ENT solutions.

Device makers invest in artificial intelligence that automatically grades tympanic membrane images, creating data moats. Pharmaceutical companies differentiate through pediatric-friendly flavoring and dropper ergonomics. Cross-licensing between diagnostic and therapeutic firms accelerates end-to-end care models. Venture capital interest rises in microbiome-based prophylaxis developers due to potential broad respiratory applications.

White-space opportunities emerge in pediatric-specific formulations, combination therapies, and preventive interventions that address the root causes of recurrent infections rather than merely treating active episodes.

Ear Infection Treatment Industry Leaders

American Diagnostic Corporation

Sanofi SA

Olympus Corporation

Novartis AG

Pfizer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Health Canada has granted Bausch + Lomb's Soothe antibiotic drops the green light for over-the-counter sales, targeting external infections in both the eye and ear.

- March 2024: Amneal Pharmaceuticals received FDA ANDA approval for ciprofloxacin–dexamethasone otic suspension, expanding U.S. access to fixed-dose combination therapy for acute otitis externa.

Global Ear Infection Treatment Market Report Scope

As per the scope of the report, an ear infection occurs due to invasion by bacteria or viruses, causing pain, inflammation, and fluid buildup in the ear. Most ear infections are acute. Some chronic ear infections can cause permanent damage to the middle and inner ears. Therefore, individuals take medications to get pain relief. Infection (Inner Ear Infection, Middle Ear Infection, and Outer Ear Infection), Cause (Viral Infection and Bacterial Infection), Type (Medication (Antibiotics, Analgesics, Antiviral), Surgery), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America) are the segments of the Ear Infection Treatment Market. The report offers the value (in USD million) for the above segments. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Inner Ear Infection |

| Middle Ear Infection |

| Outer Ear Infection |

| Viral Infection |

| Bacterial Infection |

| Fungal Infection |

| Medication | Antibiotics |

| Analgesics and Anti-inflammatory | |

| Antivirals | |

| Others | |

| Surgical Procedures |

| Pediatrics (0-12 yrs) |

| Adolescents (13-17 yrs) |

| Adults (18-64 yrs) |

| Geriatrics (65+ yrs) |

| Hospitals |

| ENT Clinics |

| Ambulatory Surgical Centres |

| Home-Care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Infection Site | Inner Ear Infection | |

| Middle Ear Infection | ||

| Outer Ear Infection | ||

| By Cause Pathogen | Viral Infection | |

| Bacterial Infection | ||

| Fungal Infection | ||

| By Treatment Type | Medication | Antibiotics |

| Analgesics and Anti-inflammatory | ||

| Antivirals | ||

| Others | ||

| Surgical Procedures | ||

| By Patient Age Group | Pediatrics (0-12 yrs) | |

| Adolescents (13-17 yrs) | ||

| Adults (18-64 yrs) | ||

| Geriatrics (65+ yrs) | ||

| By End User | Hospitals | |

| ENT Clinics | ||

| Ambulatory Surgical Centres | ||

| Home-Care Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

Why is the ear infection treatment market growing despite widespread antibiotic resistance?

The need for pediatric-friendly therapies, rising adoption of minimally invasive tympanostomy tube devices, and expanded vaccination programs offset resistance-related challenges, supporting a 5.05% CAGR to 2031.

Which region is projected to grow fastest, and what drives this acceleration?

Asia-Pacific shows the highest 7.68% CAGR owing to universal health coverage investments, rapid ENT infrastructure expansion, and increasing middle-class purchasing power.

How are office-based tympanostomy systems reshaping care delivery?

Devices such as the Hummingbird TTS enable tube placement without general anesthesia, lowering costs and increasing procedural access, which boosts ambulatory surgical center growth at 6.78% CAGR.

What role do probiotics play in ear infection prevention?

Clinical trials indicate probiotic supplementation can reduce acute otitis media incidence by 20% in high-risk children, complementing vaccination and reducing antibiotic use.

Clinical trials indicate probiotic supplementation can reduce acute otitis media incidence by 20% in high-risk children, complementing vaccination and reducing antibiotic use.

The ear infection treatment market size stands at USD 13.39 billion in 2026 and is set to reach USD 17.12 billion by 2031 under a 5.05% CAGR trajectory.

Which treatment type is expanding fastest?

Which treatment type is expanding fastest?

Page last updated on: