Cerebral Palsy Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 3.76 Billion |

| Market Size (2031) | USD 4.39 Billion |

| Growth Rate (2026 - 2031) | 3.18% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cerebral Palsy Treatment Market Analysis by Mordor Intelligence

The cerebral palsy treatment market size was valued at USD 3.64 billion in 2025 and estimated to grow from USD 3.76 billion in 2026 to reach USD 4.39 billion by 2031, at a CAGR of 3.18% during the forecast period (2026-2031). Continued demand for botulinum-toxin injections, growing adoption of programmable intrathecal baclofen pumps, and steady reimbursement expansion underpin this moderate headline growth. Behind the topline numbers, artificial-intelligence-enabled gait analysis, soft exoskeletons, and adaptive neuromodulation are shifting clinical pathways toward earlier, less invasive, and more personalized care. Regulatory agencies in the United States and Europe now expedite clearances for mini-pump systems and long-acting botulinum-toxin formulations, shortening commercialization timelines and broadening patient access. Simultaneously, Asia-Pacific governments invest in pediatric neuro-rehabilitation hubs that integrate robotics and tele-monitoring, creating attractive downstream opportunities for device manufacturers. Technology convergence also fuels the home-care segment, where portable stimulators and remote dashboards reduce hospital dependency while improving quality-of-life metrics.

Key Report Takeaways

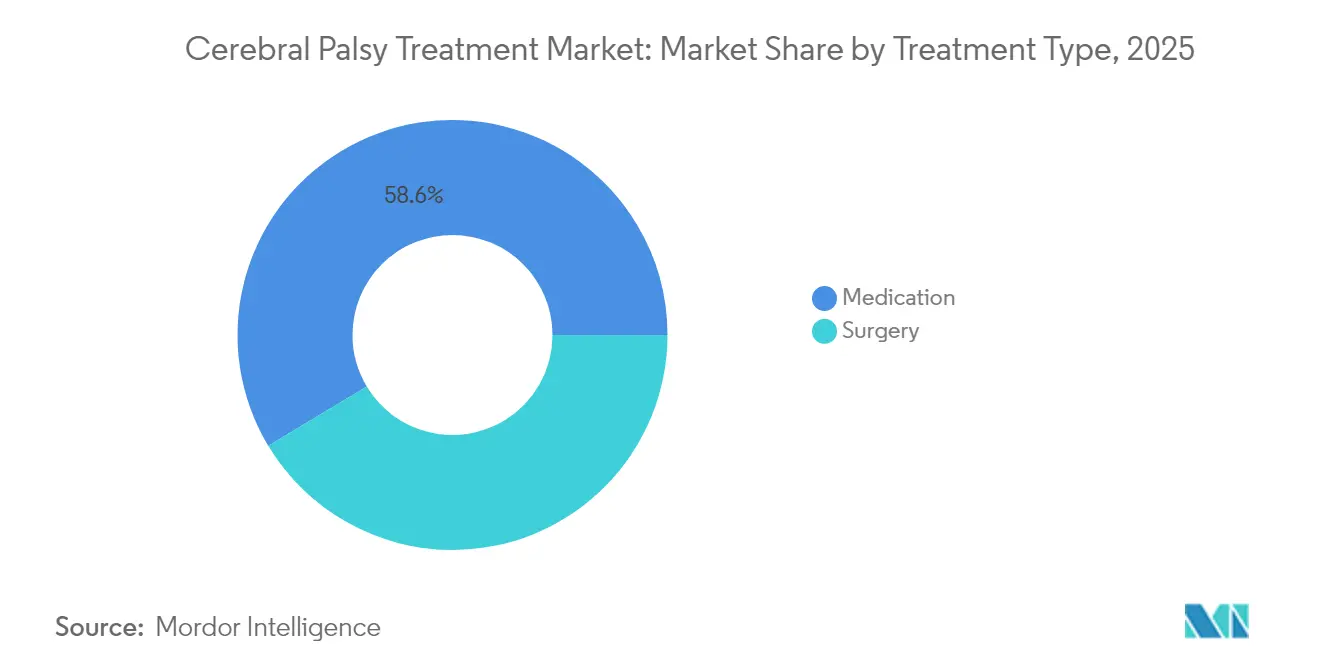

- By treatment type, medication interventions led with 58.61% revenue share of the cerebral palsy treatment market in 2025, while surgical procedures are projected to advance at a 3.82% CAGR through 2031.

- By type of cerebral palsy, spastic presentations accounted for 68.15% of the cerebral palsy treatment market share in 2025, whereas the dyskinetic subset is poised to grow quickest at 4.19% CAGR over the forecast window.

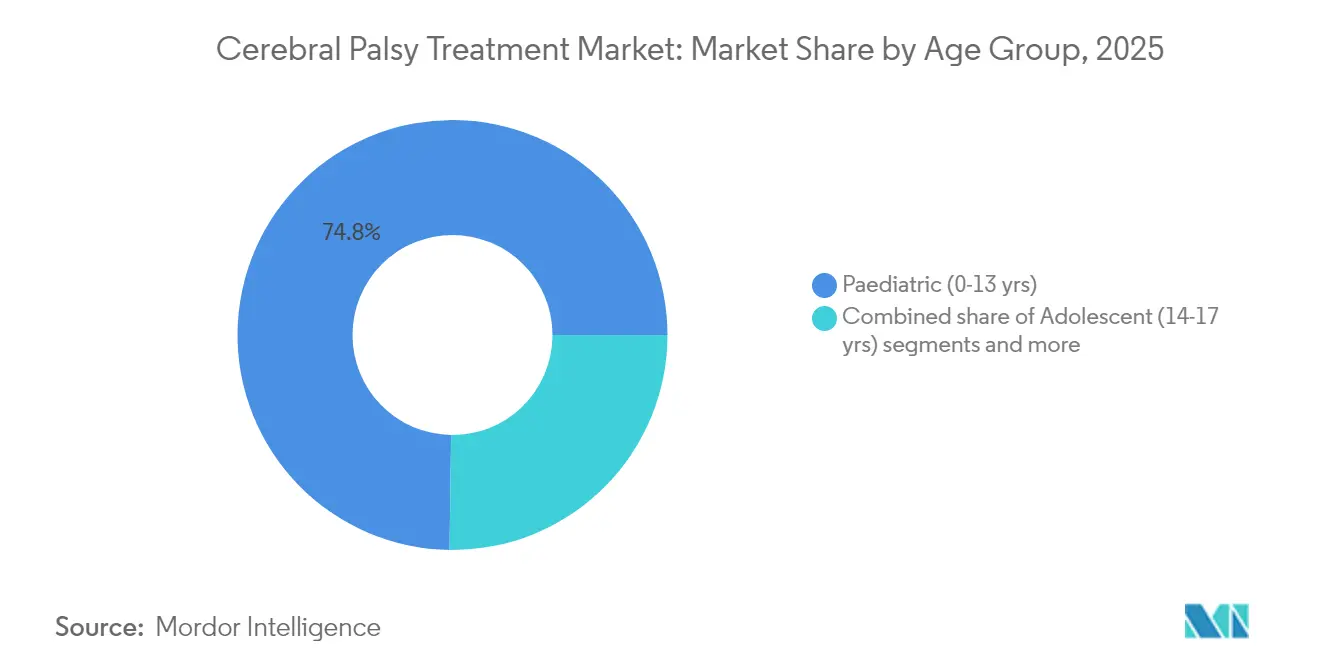

- By age group, children aged 0–13 years represented 74.78% of the cerebral palsy treatment market size in 2025 and are set to expand at a 4.87% CAGR to 2031.

- By end user, hospitals retained 53.10% share in 2025, yet home-care settings will register the fastest 4.74% CAGR as tele-rehab and wearables gain traction.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cerebral Palsy Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising diagnosis rates due to universal neonatal screening | +0.8% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Wider reimbursement for botulinum-toxin injections | +0.6% | North America & EU core, expanding to APAC | Short term (≤ 2 years) |

| Mini-pump intrathecal baclofen gaining FDA/CE clearances | +0.4% | Global, led by North America regulatory approvals | Medium term (2-4 years) |

| Growth of paediatric neuro-rehab centres in Asia-Pacific | +0.5% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| AI-guided gait analysis enabling personalised orthotics | +0.3% | North America & EU, expanding globally | Long term (≥ 4 years) |

| Spinal neuromodulation + ABNT showing Phase II efficacy | +0.2% | North America & EU research centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Diagnosis Rates via Neonatal Screening

Universal neonatal screening now incorporates General Movement Assessment and Hammersmith Infant Neurological Examination protocols capable of predicting cerebral palsy with more than 95% accuracy in infants under five months. Earlier identification accelerates therapy initiation during peak neuroplasticity windows, which improves gross-motor outcomes and lowers long-term care costs. Systematic reviews of wearable accelerometers confirm high sensitivity and specificity for early motor-development assessment. Governments that link metabolic newborn screening with neuro-developmental referral networks report declining disability burden and reduced surgical demand in later childhood. These successes explain why neonatal screening programs are spreading from the United States and Western Europe to high-volume maternity hospitals in Nepal and Indonesia.

Broader Reimbursement for Botulinum-Toxin Injections

Recent Centers for Medicare & Medicaid Services regulations cover botulinum-toxin use in upper and lower limb spasticity, removing previous age and dosage caps. Long-acting formulations such as daxibotulinumtoxinA extend clinical benefit to 28 weeks, cutting annual injection frequency in half and heightening compliance. Expanded coverage drives hospital formularies to stock Dysport, Botox, and Xeomin, fostering competitive pricing. European payers are adopting similar protocols, and pilot reimbursement schemes in India and Brazil earmark subsidies for pediatric spasticity care. Cumulative uptake helps sustain the cerebral palsy treatment market even as drug prices moderate in mature economies.

Mini-Pump Intrathecal Baclofen Clearances

Programmable intrathecal baclofen (ITB) pumps such as Medtronic’s SynchroMed III deliver precise spinal dosing that cuts systemic side effects while lowering oral baclofen requirements by 90%. Meta-analysis finds a 40.25% reduction in spasticity scores and 9.62% motor-function gain after pump implantation. Pediatric-sized pumps now reach CE and FDA approvals, enabling implantation in children weighing as little as 13 kg. Device telemetry allows clinicians to adjust dosing remotely, promoting outpatient titration and reducing clinic visits. High patient satisfaction—99% of users request pump replacement at battery end-of-life—adds commercial momentum for vendors.

Expansion of Pediatric Neuro-Rehab Centers in APAC

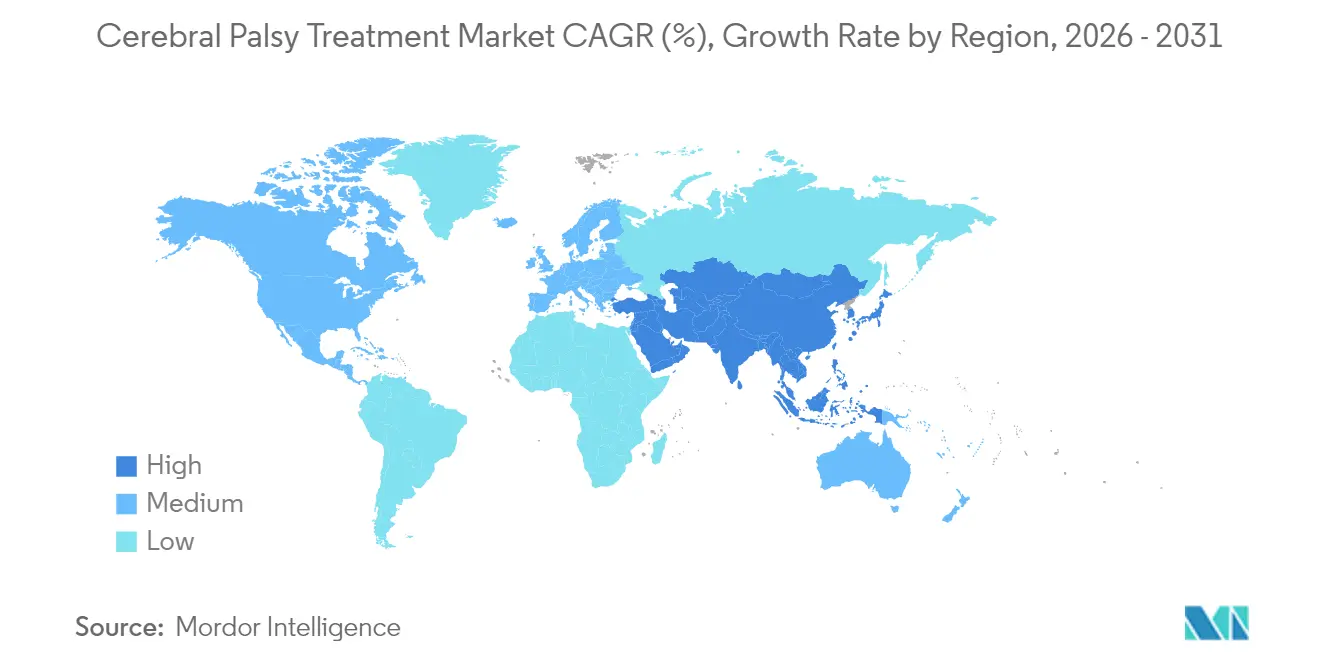

Across Asia-Pacific, governments and private investors co-fund centers that integrate robotics, virtual-reality therapy, and AI-based motion capture. Hope Abilitation Medical Center exemplifies the model, offering interdisciplinary care that bundles physiotherapy, speech therapy, and feeding programs under one roof. These hubs recruit international clinicians, embed tele-consult platforms to reach rural districts, and attract medical tourists from the Gulf and Africa. Regional birth-rate trends guarantee a sustained pediatric caseload, while insurance schemes in Singapore, South Korea, and the United Arab Emirates now reimburse intensive neuro-rehab sessions. Collectively, these initiatives give the cerebral palsy treatment market its highest regional CAGR through 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High therapy cost for life-long care | -0.9% | Global, particularly acute in emerging markets | Long term (≥ 4 years) |

| Long-term safety concerns with repeat botulinum-toxin use | -0.4% | Global, regulatory scrutiny in North America & EU | Medium term (2-4 years) |

| Shortage of multidisciplinary CP-specialist teams | -0.6% | Global, severe in rural and emerging regions | Long term (≥ 4 years) |

| Limited commercial incentive for adult-onset CP therapies | -0.3% | Global, affecting R&D investment priorities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Therapy Cost over Patient Lifetime

Annual direct costs can exceed USD 50,000 when ITB refills, orthotics, and intensive therapy are bundled, a figure that outstrips average household income in many emerging economies. Advanced exoskeletons attract Medicare payments of USD 91,031.93 yet remain unaffordable outside insured markets. For hospitals, capital budgets must cover robotics, motion-capture labs, and neuromodulation suites, limiting adoption to tertiary centers. Caregiver absenteeism and productivity losses add intangible burdens that rarely enter reimbursement calculations. Cost constraints slow market uptake despite proven clinical benefit, applying the largest negative drag on the cerebral palsy treatment market CAGR.

Long-Term Safety Concerns with Repeat Botulinum-Toxin

Systematic reviews note potential antibody development, muscle atrophy, and systemic diffusion after prolonged injection cycles in pediatric cohorts. Regulators now request post-marketing studies tracking cumulative exposure and functional outcomes over ten-year horizons. Clinicians respond by spacing treatments or alternating with phenol neurolysis, which can introduce scheduling gaps that reduce treatment adherence. Payers increase prior-authorization demands, adding administrative delays. These uncertainties discourage some families from pursuing aggressive botulinum-toxin regimens, trimming incremental revenue growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Medication Leads, Surgery Accelerates

Medication interventions anchored by botulinum-toxin injections delivered 58.61% of 2025 revenue in the cerebral palsy treatment market. Combination regimens that pair abobotulinumtoxinA with selective physiotherapy reduce spasticity scores within four weeks, reinforcing the clinical status quo. Anticonvulsants and antidepressants address comorbid seizures and mood disorders, enlarging pharmacy baskets and supporting steady prescription renewals. The cerebral palsy treatment market size for surgical procedures is forecast to climb at a 3.82% CAGR, reflecting breakthroughs in minimally invasive selective dorsal rhizotomy and adaptive deep-brain stimulation.

Robotic guidance platforms shorten operative time and enhance precision, reducing postoperative infection rates. Intrathecal baclofen pump implantation straddles medical and surgical domains, delivering 99% device survival at seven years. Spinal neuromodulation trials using percutaneous leads report Ashworth scale improvements from 3.0 to 1.14, sparking interest among payers seeking long-term cost offsets.

By Type of Cerebral Palsy: Spastic Dominance Spurs Focused Innovation

Spastic presentations commanded 68.15% cerebral palsy treatment market share in 2025, ensuring that tone-modulating drugs and neurosurgical options receive disproportionate investment. Continuous infusion of baclofen via micro-pumps stabilizes lower limb posture and reduces surgical hip relocations. Dyskinetic presentations expand at 4.19% CAGR because deep-brain stimulation and novel cerebellar targets now show Phase II promise.

Ataxic subtypes, though numerically smaller, benefit from balance-training robots and transcranial direct-current stimulation under early feasibility studies. Mixed phenotypes often require sequential therapy layering, driving multidrug use and complex care pathways that add to the cerebral palsy treatment industry revenue base.

By Age Group: Pediatric Care Drives Lifetime Demand

Children under 14 accounted for 74.78% of the cerebral palsy treatment market size in 2025, with universal neonatal screening and AI-based motor assessment accelerating case detection. Early initiation of constraint-induced therapy yields superior fine-motor gains, nurturing steady demand for occupational-therapy services. The segment grows fastest at 4.87% CAGR as governments prioritize early-intervention funding.

Adolescents experience growth-related orthopedic complications that boost surgical volumes, while adults face chronic pain and fatigue, encouraging uptake of multimodal pain management. Transitional clinics bridge pediatric and adult systems to maintain therapy continuity. Wearable exoskeletons like MyoStep adjust to user stature, allowing long-term device use throughout growth phases.

By End User: Hospital Scale Meets Home-Care Flexibility

Hospitals generated 53.10% of 2025 revenue in the cerebral palsy treatment market, supported by multidisciplinary teams and operating-room capacity. Tertiary centers concentrate complex surgeries and research trials, sustaining referral pipelines. Home-care environments will rise at a 4.74% CAGR as portable stimulators and tele-supervised physiotherapy prove clinically equivalent for selected cases.

Rehabilitation centers maintain specialized expertise in gait-training robotics and hydrotherapy pools, while specialty clinics offer one-stop spasticity services that combine injection, orthotics, and therapy. Pay-for-performance models shift follow-up visits to virtual channels, enhancing convenience and reducing caregiver travel costs.

Geography Analysis

North America held 41.85% of 2025 revenue thanks to comprehensive reimbursement, world-class research hospitals, and early adoption of AI-enabled diagnostics. FDA Breakthrough Device designations accelerate time-to-market for neuromodulation and brain-computer interface products, reinforcing the region’s innovation edge. Nonetheless, rural clinics face specialist shortages that impede consistent access, and cost pressures prompt insurers to renegotiate hospital contracts.

Europe follows with integrated public health systems that prioritize early intervention and multidisciplinary care. CE-marking harmonization enables cross-border device sales, and national formularies have added Dysport pediatric indications, widening market reach. Outcome-registry initiatives support value-based payment models that favor technologies with clear functional-gain metrics.

Asia-Pacific delivers the fastest regional CAGR at 4.41% to 2031 as governments invest in pediatric neuro-rehabilitation hubs and expand insurance coverage. High birth rates in India, Indonesia, and the Philippines guarantee a steady patient pipeline, while medical-tourism corridors to Singapore and the United Arab Emirates attract international clientele. Newborn metabolic screening programs in Nepal illustrate the preventive shift underway. South America and the Middle East & Africa remain nascent yet draw investment through public-private partnerships aimed at robotics deployment and tele-medicine networks.

Competitive Landscape

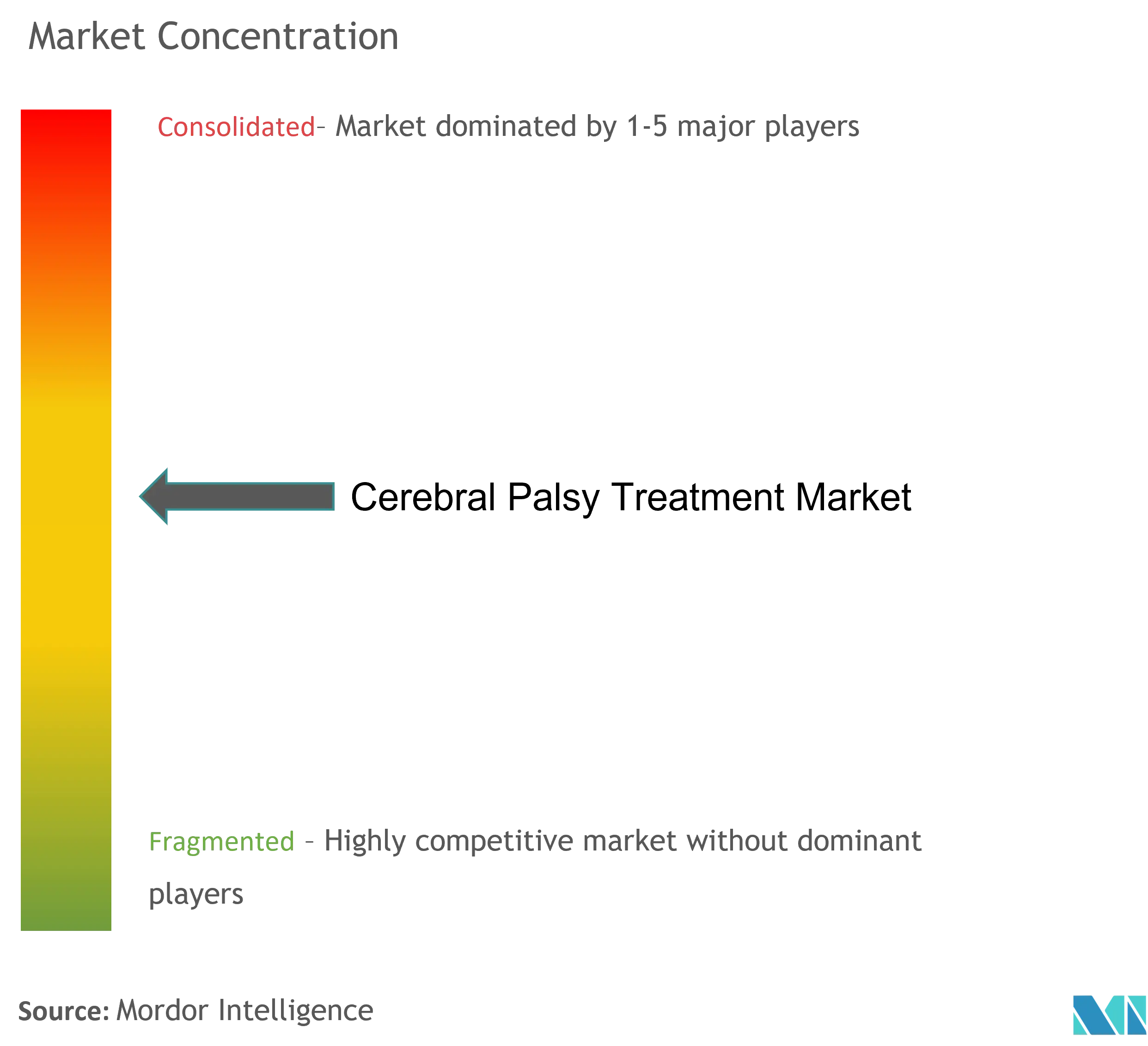

The cerebral palsy treatment market features moderate fragmentation, with no player exceeding a double-digit global share. Ipsen, AbbVie, and Merz Pharma dominate the botulinum-toxin arena, leveraging extensive sales forces and post-marketing data to defend formulary positions. Medtronic, Zimmer Biomet, and Stryker supply implantables and surgical hardware, while Ekso Bionics and Trexo Robotics pioneer gait-training exoskeletons.

Strategic activity centers on platform integration. Pharmaceutical firms collaborate with device makers to bundle drugs, pumps, and analytics dashboards into comprehensive care packages. Ekso Bionics partners with Shepherd Center to refine clinical protocols and evidence collection. Venture funding flows to AI start-ups that analyze motion-sensor streams, creating acquisition targets for incumbents seeking data capabilities.

Regulatory navigation and reimbursement coding expertise shape competitive advantage, particularly in the United States where CMS determinations dictate capital-equipment adoption. White-space opportunities persist in adult spasticity management and value-tier products for emerging markets, areas currently underserved by premium-priced Western offerings. Players that localize manufacturing or create scalable subscription models are positioned to outpace the broader cerebral palsy treatment market.

Cerebral Palsy Treatment Industry Leaders

Ipsen Biopharmaceuticals Inc.

Merz GmbH & Co. KGaA

Teva Pharmaceutical Industries Ltd.

Supernus Pharmaceuticals, Inc.

Abbvie Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Neuralink won FDA Breakthrough Device status for its speech-restoration brain-computer interface for severe paralysis, including cerebral palsy patients.

- March 2025: FDA issued a warning to Exer Labs for marketing Exer Scan without pre-market clearance for neurological indications

Global Cerebral Palsy Treatment Market Report Scope

Cerebral palsy refers to a group of symptoms that involve difficulty moving and muscle stiffness (spasticity). It results from brain malformations that occur before birth as the brain is developing or from brain damage that occurs before, during, or shortly after birth.

The cerebral palsy treatment market is segmented by disease type (spastic cerebral palsy, dyskinetic cerebral palsy, ataxic cerebral palsy, mixed cerebral palsy), treatment type (surgery and medication), distribution channel (hospital pharmacies, retail pharmacies, and online pharmacies), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally.

The report offers the value (in USD) for the above-mentioned segments.

| Surgery | |

| Medication | AntiCholinergic aganet |

| Botulinum-Toxin Injections | |

| Anticonvulsants | |

| Antidepressants | |

| Antispastic | |

| Other Medication |

| Spastic CP |

| Dyskinetic CP |

| Ataxic CP |

| Mixed/Other |

| Paediatric (0–13 yrs) |

| Adolescent (14–17 yrs) |

| Adult (18 yrs +) |

| Hospitals |

| Specialty Clinics |

| Rehabilitation Centres |

| Home-Care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Treatment Type | Surgery | |

| Medication | AntiCholinergic aganet | |

| Botulinum-Toxin Injections | ||

| Anticonvulsants | ||

| Antidepressants | ||

| Antispastic | ||

| Other Medication | ||

| By Type of Cerebral Palsy | Spastic CP | |

| Dyskinetic CP | ||

| Ataxic CP | ||

| Mixed/Other | ||

| By Age Group | Paediatric (0–13 yrs) | |

| Adolescent (14–17 yrs) | ||

| Adult (18 yrs +) | ||

| By End User | Hospitals | |

| Specialty Clinics | ||

| Rehabilitation Centres | ||

| Home-Care Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected revenue for the cerebral palsy treatment market in 2031?

The cerebral palsy treatment market is expected to reach USD 4.39 billion by 2031.

Which therapy type is growing fastest within the cerebral palsy treatment market?

Surgical interventions are forecast to climb at a 3.82% CAGR, the highest among treatment categories.

Why is the pediatric segment critical to market growth?

Children under 14 drive a 4.87% CAGR because universal neonatal screening and AI-based assessments enable earlier, more intensive intervention.

Which region offers the strongest growth outlook?

Asia-Pacific shows the highest 4.41% regional CAGR, supported by new pediatric neuro-rehabilitation centers and rising healthcare investments.

What are the main cost barriers hindering therapy adoption?

High lifetime expenses for intrathecal pumps, exoskeletons, and intensive rehabilitation can surpass USD 50,000 annually, limiting accessibility.

Page last updated on: