Vertigo Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.34 Billion |

| Market Size (2031) | USD 2.98 Billion |

| Growth Rate (2026 - 2031) | 4.89% CAGR |

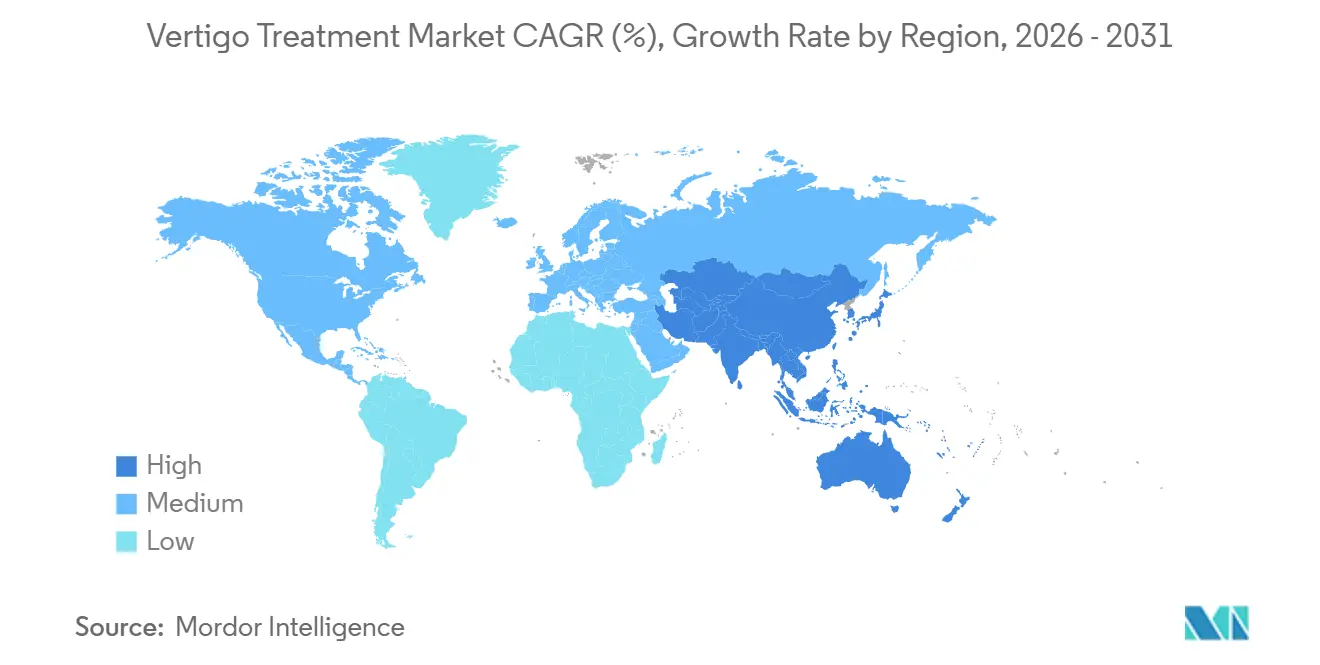

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

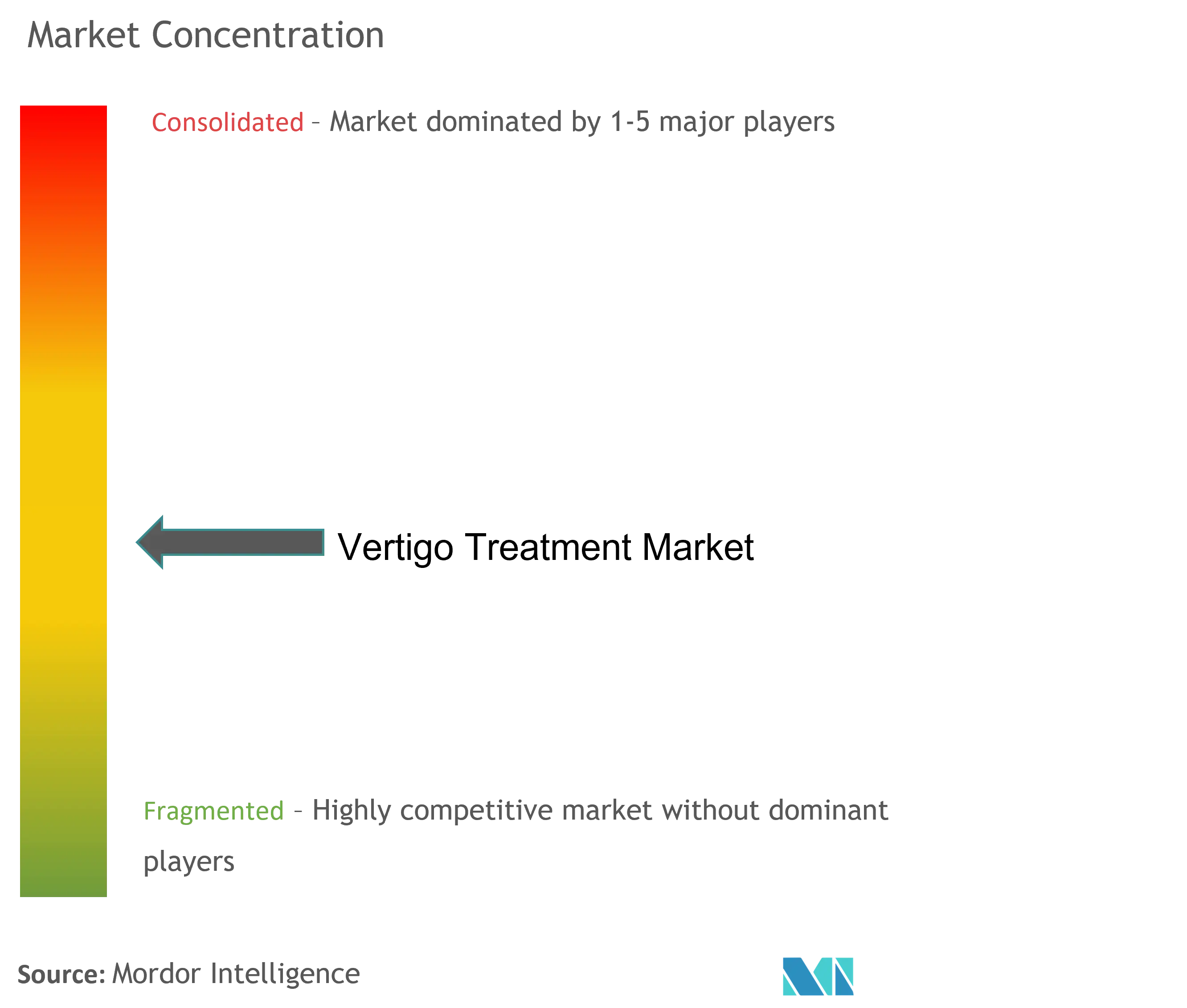

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vertigo Treatment Market Analysis by Mordor Intelligence

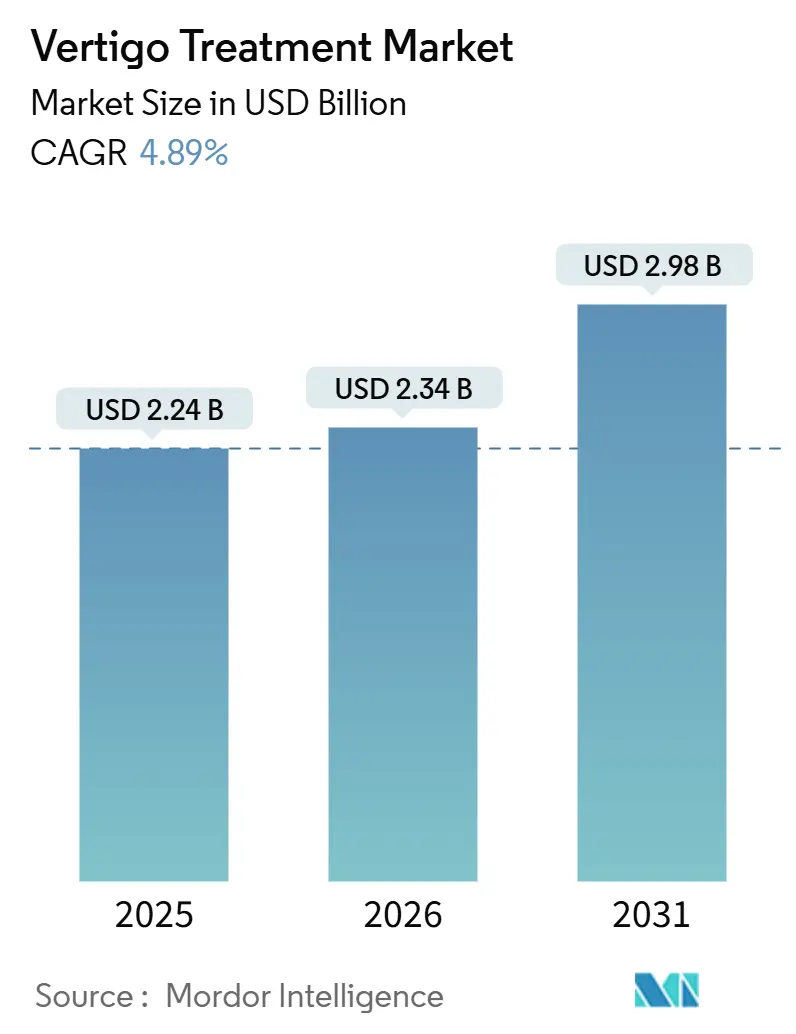

The Vertigo Treatment Market size is projected to expand from USD 2.24 billion in 2025 and USD 2.34 billion in 2026 to USD 2.98 billion by 2031, registering a CAGR of 4.89% between 2026 to 2031.

Growing life expectancy, a clear link between age-related vestibular decline and fall injuries, and a steady flow of therapeutic launches are sustaining demand across care settings. Regulatory acceptance of software-based interventions, evidenced by recent United States Food and Drug Administration (FDA) clearances, is broadening the therapeutic mix and reinforcing personalized care pathways. The vertigo treatment market benefits further from expanding vestibular rehabilitation networks, improved imaging techniques that shorten diagnostic latency, and regional healthcare funding that increasingly covers balance-disorder services. Competitive intensity is rising as biotechnology firms move from early-stage research toward commercial-scale manufacturing of precision medicines and digital therapeutics.

Key Report Takeaways

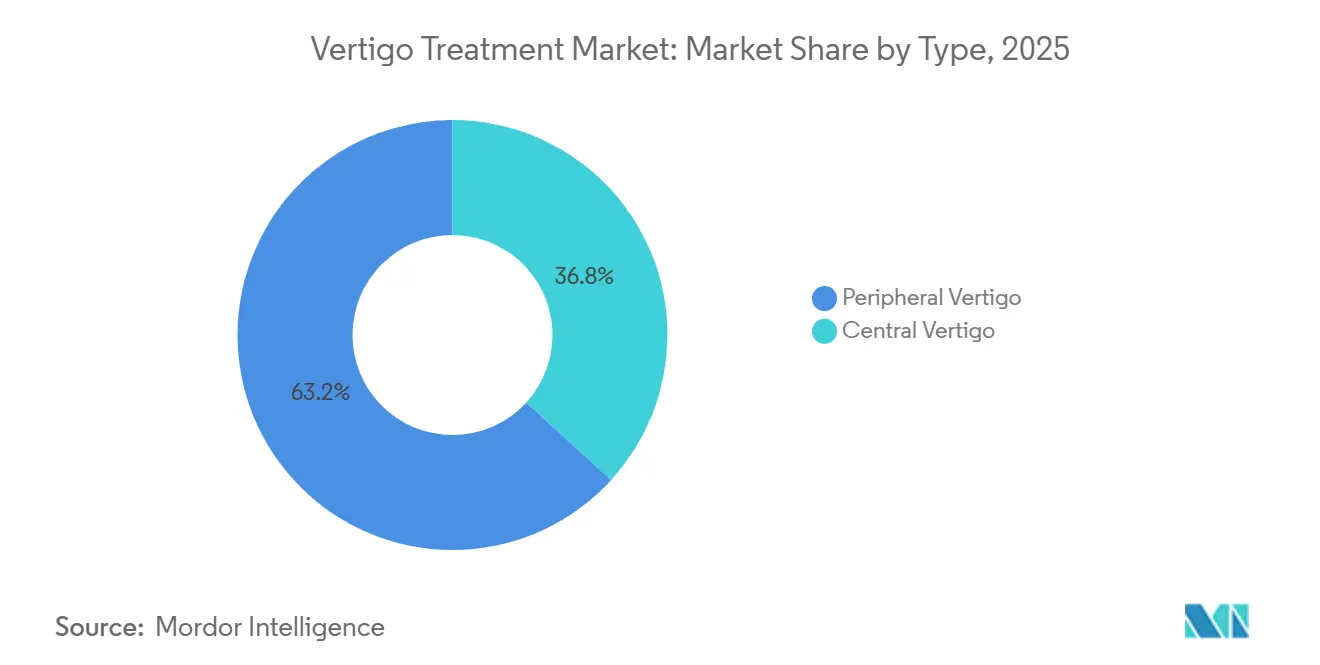

- By type, peripheral vertigo led with 63.23% of the vertigo treatment market share in 2025. Central vertigo is forecast to expand at a 6.54% CAGR through 2031.

- By treatment type, medication accounted for 71.50% of revenue in 2025. Surgical interventions are projected to grow at a 7.15% CAGR to 2031.

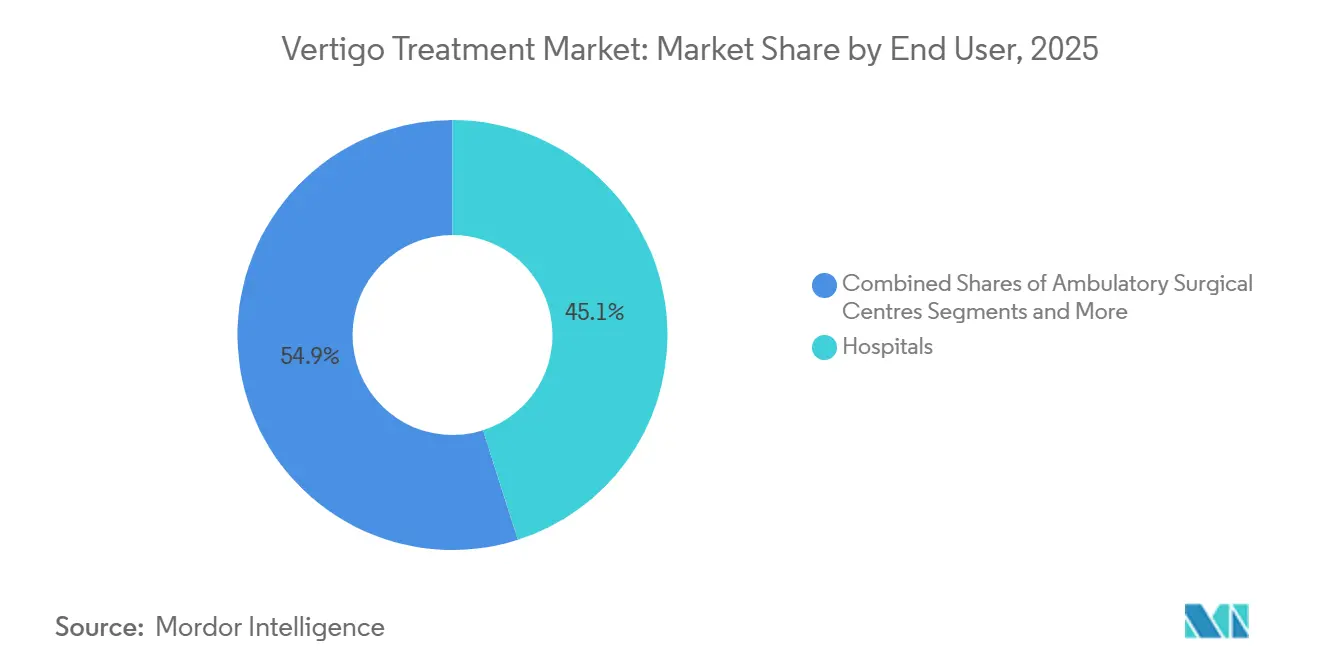

- By end user, hospitals held 45.07% of the vertigo treatment market share in 2025. Ambulatory surgical centers recorded the fastest projected growth at a 9.40% CAGR through 2031.

- By geography, North America captured 44.50% of global revenue in 2025. Asia-Pacific is projected to advance at a 7.24% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Vertigo Treatment Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rise in prevalence of vertigo among ageing population | +1.2% | Global, with concentration in North America, Europe, and Japan | Long term (≥ 4 years) |

| Growing healthcare expenditure in emerging economies | +0.9% | APAC core, China and India, with spillover to MEA and South America | Medium term (2-4 years) |

| Expanding ENT & neurology specialty centers | +0.7% | North America and EU, urban clusters in APAC | Medium term (2-4 years) |

| Increasing availability of vestibular rehabilitation therapists | +0.5% | North America, Western Europe, Australia | Medium term (2-4 years) |

| Ototoxic-drug-induced vestibular dysfunction surveillance programs | +0.3% | Global, led by United States, European Union, and select APAC nations | Long term (≥ 4 years) |

| Adoption of smartphone-based vestibular diagnostic apps | +0.6% | Global, early gains in United States, Canada, United Kingdom, South Korea | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rise in Prevalence of Vertigo Among Ageing Population

As the global population ages, the demand for vertigo care is increasing. A study highlighted that 27.1% of adults aged 55 and older experienced vestibular vertigo over a decade, with 39.8% reporting dizziness or vertigo, emphasizing the persistent nature of these symptoms in older demographics.[1]Johns Hopkins Medicine, “VertiGuide Smartphone App for Nystagmus Detection,” Johns Hopkins Medicine, hopkinsmedicine.org • Restraints By 2030, 2.1 billion individuals worldwide will be aged 60 or older, highlighting the growing patient pool for standardized diagnostic and therapeutic interventions.[2]World Health Organization, “Ageing and Health,” World Health Organization, who.int This shift aligns with the rise of adherence tools and remote monitoring. Additionally, the increasing recognition of vestibular migraines in older patients is driving the off-label use of CGRP-targeted therapies, particularly for patients unresponsive to standard treatments.

Growing Healthcare Expenditure in Emerging Economies

Increased public and private healthcare spending in China and India is improving access to specialized ENT and neurology services, expanding diagnosis and treatment volumes in the vertigo market. In 2024, China allocated significant funds to healthcare, enhancing hospital capacities, procuring essential equipment, and hiring specialists to manage vestibular cases. Similarly, India's 2024-25 Union Budget allocated substantial resources for health and family welfare, broadening coverage to previously uninsured populations.[3]Ministry of Finance, “Union Budget 2024–25,” Government of India, indiabudget.gov.in India's pharmaceutical sector, valued at USD 50 billion in 2024 and projected to reach USD 130 billion by 2030, is scaling up production of cost-effective vertigo medications. This expansion caters to domestic demands and strengthens export reliability for primary care.

Expanding ENT & Neurology Specialty Centers

Specialized centers are redirecting patient traffic from general clinics and emergency departments to dedicated hubs offering integrated pathways for diagnostics, rehabilitation, and surgical care in the vertigo treatment market. Cleveland Clinic is set to open a large neurological institute in 2027, centralizing vestibular diagnostics, rehabilitation, and surgery for complex cases. In 2024, Beacon Hospital in Ireland invested significantly to expand its neuroscience and ENT services, reducing outbound referrals for specialized vestibular care and reinforcing its commitment to tertiary services. A global survey in 2025 revealed varied practice patterns and inconsistent access to tools like video-oculography. Specialty centers are addressing these gaps through standardized protocols and strategic equipment investments.

Increasing Availability of Vestibular Rehabilitation Therapists

The growth of the vestibular rehabilitation workforce and the introduction of innovative care models are enhancing access to treatments, strengthening utilization across chronic and post-acute vertigo pathways. A 2024 review highlighted the effectiveness of telerehabilitation, noting that live video or web-based platforms significantly reduced dizziness severity and associated disabilities, leading to broader acceptance of remote therapy formats. The remote approach expands therapist reach while ensuring adherence checks.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Ignorance or late reporting of vertigo symptoms | -0.8% | Global, more pronounced in low-income and rural regions | Long term (≥ 4 years) |

| Limited long-term efficacy data for pharmacological options | -0.5% | Global, affecting clinical adoption and payer coverage | Medium term (2-4 years) |

| Shortage of trained neuro-otologists in low-income nations | -0.6% | Sub-Saharan Africa, South Asia, Latin America | Long term (≥ 4 years) |

| Reimbursement gaps for vestibular rehab and home-based care | -0.4% | United States, select EU markets, emerging economies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ignorance or Late Reporting of Vertigo Symptoms

Many patients perceive dizziness as a harmless aspect of aging, leading to delays in seeking care in the vertigo treatment market. A 2025 global survey of clinicians highlighted that patients typically consult only after experiencing recurrent episodes or a fall. By this time, compensation patterns may diminish the effectiveness of certain therapies. This delay is more pronounced in low-income and rural areas, where access to ENT specialists is limited, and primary care providers often lack confidence in vestibular triage. Fall prevention programs frequently overlook vestibular screening, missing an opportunity to reduce injuries. Despite the high risk of serious injuries from falls among older adults, routine care does not consistently include proactive vestibular assessments. Digital self-assessments and brief triage questionnaires show potential but require patient education and seamless integration into existing workflows to achieve scalability.

Limited Long-Term Efficacy Data for Pharmacological Options

Evidence gaps undermine confidence in the long-term pharmacological management of various vestibular conditions, limiting broad payer support in the vertigo treatment market. While Betahistine is commonly prescribed for Ménière’s disease outside the U.S., its benefits beyond 12 weeks remain uncertain despite a favorable safety profile. Antihistamines like meclizine and dimenhydrinate, though supported by extensive clinical use, lack large-scale, high-quality trials demonstrating long-term efficacy, positioning them as symptomatic relief agents rather than disease modifiers. CGRP monoclonal antibodies offer a targeted solution for vestibular migraines, but their high annual cost and off-label status for vestibular applications create reimbursement challenges. Pipeline innovations, such as intratympanic formulations for Ménière’s disease, aim to demonstrate durable efficacy in conditions with high placebo response rates. Establishing robust, long-term evidence could enhance clinical confidence and align payer support for these maintenance treatments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Central Vertigo Gains as Diagnostic Precision Improves

In 2025, peripheral vertigo accounted for 63.23% of the vertigo treatment market. However, the central category is projected to grow at a 6.54% CAGR through 2031, driven by improved recognition of stroke-related and vestibular migraine subtypes. Benign paroxysmal positional vertigo significantly contributes to dizziness clinic visits, with a 15% annual recurrence rate. Half of these recurrences occur within 2 to 3 years, sustaining demand for canalith repositioning and symptomatic therapy. Ménière’s disease, despite its lower prevalence, generates substantial pharmaceutical revenue due to chronic treatment needs, ranging from betahistine to intratympanic corticosteroids in select cases. Vestibular neuritis and labyrinthitis often require acute corticosteroids and vestibular suppressants, followed by rehabilitation to restore function. These conditions create recurring touchpoints across primary care, specialty clinics, and rehabilitation programs.

By Treatment Type: Surgical Growth Reflects Minimally Invasive Gains

In 2025, medication dominated the vertigo treatment market with a 71.50% share. Surgical interventions are expected to grow at a 7.15% CAGR, supported by advancements in techniques and improved outpatient economics. Antihistamines such as meclizine, dimenhydrinate, and promethazine remain the primary choice for symptom relief, with an expanded generic base, including a 2025 FDA approval for Zydus’s meclizine manufactured in Ahmedabad. Anticholinergics, typically reserved for motion sickness and acute vertigo, face limitations in older adults due to their anticholinergic burden. Benzodiazepines, constrained by risks of falls and dependence, are generally prescribed for short-term use. Corticosteroids and calcium channel blockers are targeted for specific conditions such as vestibular neuritis or vestibular migraine prophylaxis.

By End User: Ambulatory Centers Capture Outpatient Shift

In 2025, hospitals held a 45.07% share of the vertigo treatment market. Ambulatory surgical centers are the fastest-growing end user, with a 9.40% CAGR, as payers increasingly shift suitable procedures to outpatient settings. Hospitals remain referral hubs for complex diagnostics, inpatient stabilization, and procedures requiring anesthesia or multi-specialist teams. Specialty clinics, including ENT and neurology centers, provide advanced diagnostic tests such as video-oculography and rotary chair protocols, which are not always available in general hospitals. These clinics also manage chronic vestibular conditions, combining pharmacologic and rehabilitation strategies. Such comprehensive management accelerates discharges and reduces emergency revisits.

Geography Analysis

In 2025, North America accounted for 44.5% of the vertigo treatment market, driven by comprehensive coverage, a high concentration of specialists, and early adoption of digital solutions. Medicare provides coverage for vestibular rehabilitation under specific CPT codes, with reimbursement rates of USD 30 to 35 per 15-minute unit, establishing a baseline for therapy access. The United States leads in digital diagnostics, with the introduction of VertiGuide in 2024 to facilitate nystagmus assessment and triage beyond specialist clinics. Canada and Mexico hold smaller but growing shares, supported by cross-border telemedicine and increased availability of generics. Infrastructure developments, such as the Cleveland Clinic's upcoming neurological institute in 2027, further strengthen North America's position in advanced vestibular care.

Europe's vertigo treatment market is influenced by diverse reimbursement policies and prescribing practices, which shape therapy options and pricing. Betahistine remains widely used in Germany, France, and the United Kingdom, despite its lack of FDA approval in the United States, reflecting regional differences in regulatory standards. Germany's stable demand, along with aging populations in Italy and Spain, drives the need for chronic management and rehabilitation. The European Medicines Agency facilitates multi-country drug approvals, although national health bodies often prioritize generics to meet cost-effectiveness criteria. Northern and Eastern Europe are increasingly adopting telerehabilitation to address specialist shortages, improving adherence for older patients with mobility challenges.

The Asia-Pacific region is projected to grow at a 7.24% CAGR through 2031, fueled by expanding healthcare access in China and India and increased utilization of specialty ENT services in Southeast Asia's urban areas. China's significant healthcare investments in 2024 have enhanced hospital capacity and diagnostic capabilities for vestibular conditions. India's 2024-25 budget allocation for health and family welfare, supplemented by state-level spending and expanded coverage under Ayushman Bharat, supports the region's growth. India's pharmaceutical industry, valued at USD 50 billion in 2024 and expected to reach USD 130 billion by 2030, plays a key role in producing affordable antihistamines and vestibular suppressants for domestic and export markets, improving affordability across the region.

Competitive Landscape

Moderate fragmentation defines competitive dynamics because vertigo encompasses diverse etiologies that require different pharmacological and rehabilitative approaches. No single manufacturer exceeds a double-digit share, placing the vertigo treatment market firmly in a multi-player equilibrium. Multinational drug firms maintain broad oral portfolios and distribution scale advantages, while smaller biotechnology entrants focus on high-value niches such as gene therapy, ototoxicity prevention, and H4-receptor antagonism.

Sensorion illustrates the hybrid model by combining small-molecule work (SENS-401), gene therapy (SENS-501), and SENS-111, advancing each program through decentralized trials to shorten timelines. Sound Pharmaceuticals completed enrollment in a 221-patient phase 3 study of SPI-1005 for Ménière’s disease, showing the clinical traction possible for focused mid-cap companies. Click Therapeutics’ CT-132 migraine software win emphasizes how digital-first platforms can secure neurological labels, a template now migrating toward vertigo.

Strategic mergers are reshaping the branded-drug segment, as evidenced by Mallinckrodt and Endo’s USD 7 billion tie-up that increases exposure to specialty neurology portfolios. Big-tech collaborations are also appearing, with AI firms supplying diagnostic algorithms that integrate into otology instrument suites. As reimbursement shifts toward outcome-linked models, competitive advantage hinges less on sheer volume and more on demonstrable functional gains and fall-reduction metrics, a trend likely to redefine valuation in the vertigo treatment market.

Vertigo Treatment Industry Leaders

Viatris Inc.

Epic Pharma, LLC

AdvaCare Pharma

Lupin Ltd.

Pfizer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Aspire Biopharma Holdings, Inc. filed a provisional patent application with the United States Patent and Trademark Office (USPTO) for its proprietary sublingual powder formulation of Meclizine.

- September 2025: Dr Reddy's Laboratories finalized a definitive agreement with Johnson & Johnson, securing the Stugeron brand across EMEA regions, with a spotlight on key markets India and Vietnam. Stugeron, featuring Cinnarizine, serves as an antihistamine for vestibular disturbances and vertigo treatment.

- December 2025: Sound Pharmaceuticals (SPI) proudly announces that the FDA has bestowed its investigational new drug, SPI-1005, with Breakthrough Therapy Designation (BTD) for addressing hearing loss in Menière’s disease (MD) patients.

- March 2025: Mallinckrodt and Endo unveil a monumental USD 7 billion merger, birthing a more formidable entity in the branded-drug landscape, particularly attuned to vertigo treatments.

Global Vertigo Treatment Market Report Scope

Vertigo is a medical disorder that causes a person to believe that they or the items around them are moving when they are not. Walking difficulties, sweating, and nausea are all common symptoms. Vertigo is the most common form of dizziness, and the cause of this condition could be peripheral or central. Peripheral vertigo is related to the inner ear problem, and central vertigo is related to the central nervous system.

The Vertigo Treatment Market is segmented by Type (Peripheral Vertigo and Central Vertigo), Treatment Type (Medication (Over-the-counter Drugs and Prescription Drugs) and Surgery), End Users (Hospitals, Clinics, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (USD million) for the above segments.

| Peripheral Vertigo | Benign Paroxysmal Positional Vertigo (BPPV) |

| Meniere Disease | |

| Vestibular Neuritis & Labyrinthitis | |

| Central Vertigo | Vestibular Migraine |

| Stroke-related Vertigo | |

| Multiple Sclerosis & Tumor-related Vertigo |

| Medication | Antihistamines |

| Anticholinergics | |

| Benzodiazepines | |

| Calcium Channel Blockers | |

| Corticosteroids | |

| Others | |

| Surgery | Vestibular Nerve Section |

| Labyrinthectomy | |

| Semicircular Canal Plugging |

| Hospitals |

| Speciality Clinics |

| Ambulatory Surgical Centres |

| ENT & Neurology Centres |

| Homecare / Tele-rehabilitation Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Peripheral Vertigo | Benign Paroxysmal Positional Vertigo (BPPV) |

| Meniere Disease | ||

| Vestibular Neuritis & Labyrinthitis | ||

| Central Vertigo | Vestibular Migraine | |

| Stroke-related Vertigo | ||

| Multiple Sclerosis & Tumor-related Vertigo | ||

| By Treatment Type | Medication | Antihistamines |

| Anticholinergics | ||

| Benzodiazepines | ||

| Calcium Channel Blockers | ||

| Corticosteroids | ||

| Others | ||

| Surgery | Vestibular Nerve Section | |

| Labyrinthectomy | ||

| Semicircular Canal Plugging | ||

| By End User | Hospitals | |

| Speciality Clinics | ||

| Ambulatory Surgical Centres | ||

| ENT & Neurology Centres | ||

| Homecare / Tele-rehabilitation Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the vertigo treatment market?

The vertigo treatment market size is USD 2.24 billion in 2026 and is projected to reach USD 2.98 billion by 2031 at a 4.89% CAGR.

Which segment is growing fastest within the vertigo treatment ecosystem?

Central vertigo is the fastest growing type at a projected 6.5% CAGR to 2031, supported by better recognition of vestibular migraine and stroke-related cases.

How are care settings shifting for vertigo management?

Ambulatory surgical centers are expanding fastest at a 9.4% CAGR as payers favor outpatient settings for intratympanic injections and certain canal procedures.

Which region leads revenue and which is the growth leader?

North America led with 44.5% share in 2025, while Asia-Pacific is projected to grow fastest at a 7.2% CAGR through 2031.

What role do digital tools play in vertigo diagnosis and rehabilitation?

Tools like Johns Hopkins VertiGuide improve frontline nystagmus detection, and validated systems such as VestAid support remote rehabilitation adherence and outcomes tracking.

Which therapies dominate spending in vertigo care today?

Medications remain the largest revenue contributor at 71.5% in 2025, while surgical interventions are set to grow at 7.1% as minimally invasive techniques scale.

Page last updated on: