Lipid Disorder Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

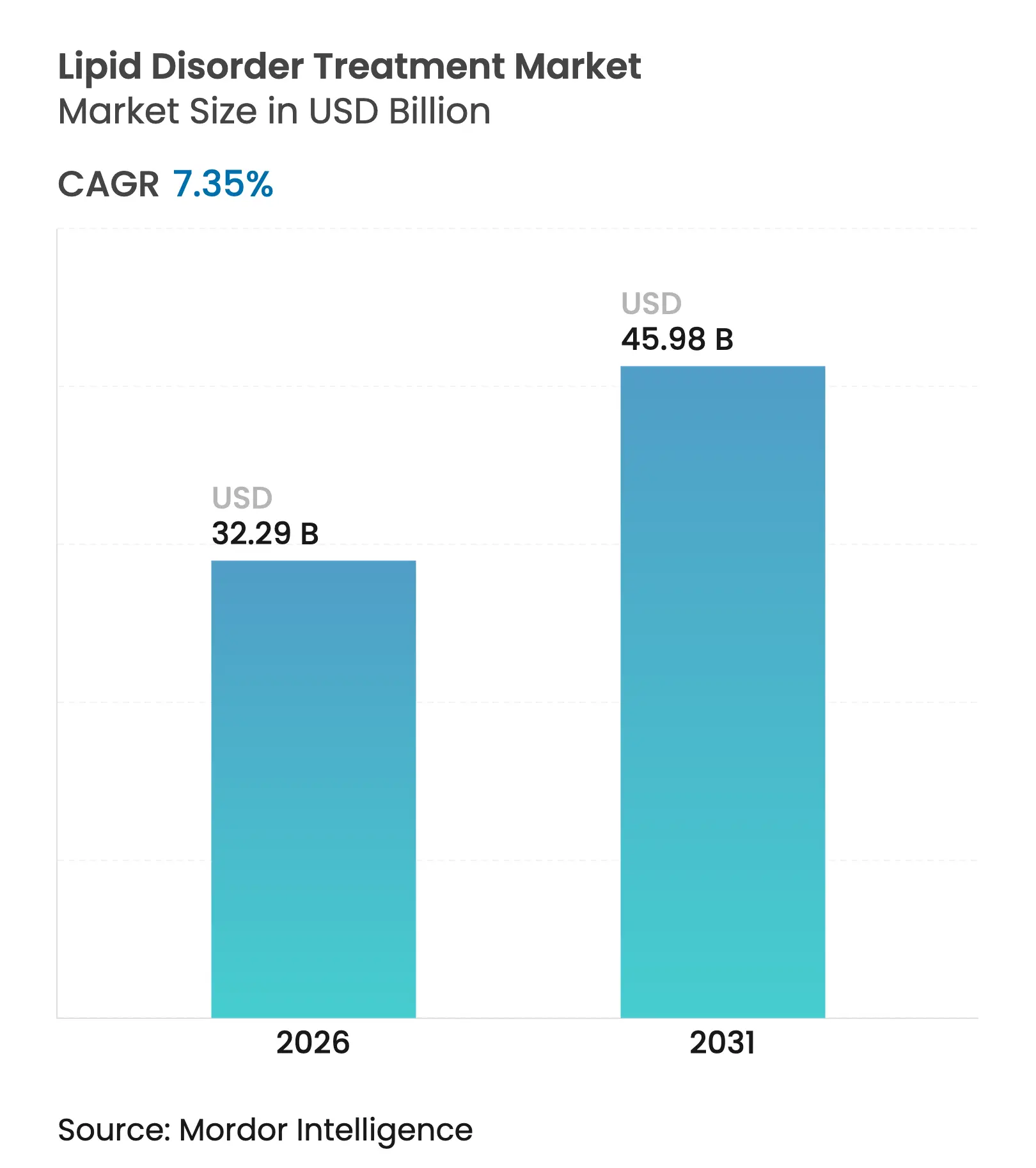

| Market Size (2026) | USD 32.29 Billion |

| Market Size (2031) | USD 45.98 Billion |

| Growth Rate (2026 - 2031) | 7.35 % CAGR |

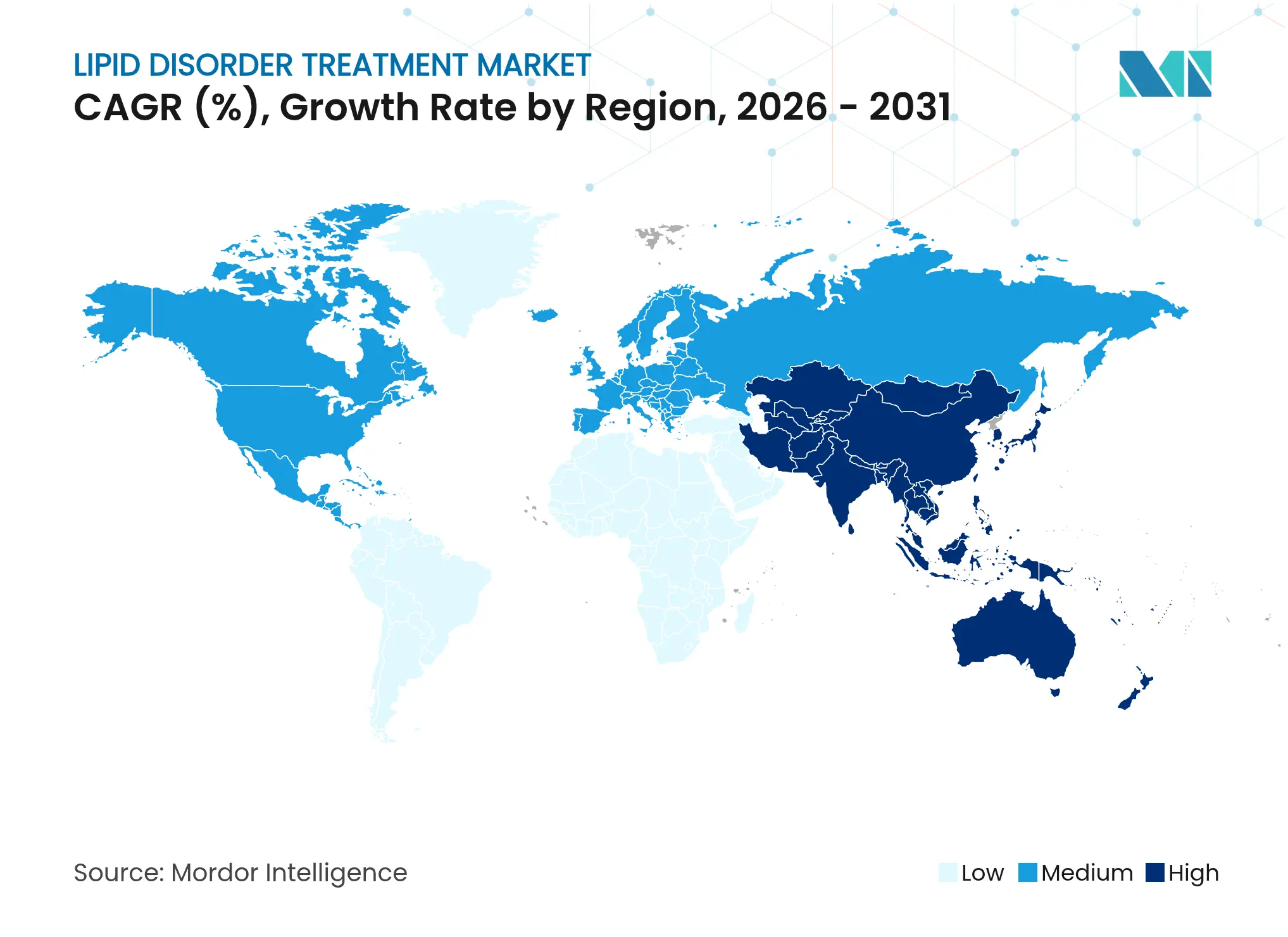

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

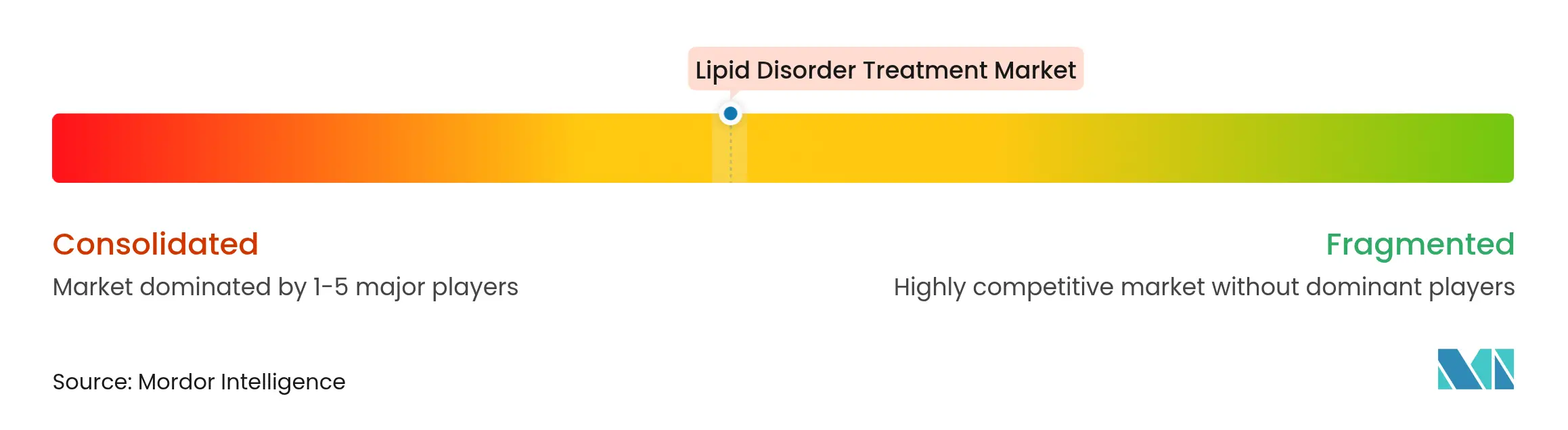

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Lipid Disorder Treatment Market Analysis by Mordor Intelligence

The lipid disorder treatment market size was valued at USD 30.08 billion in 2025 and estimated to grow from USD 32.29 billion in 2026 to reach USD 45.98 billion by 2031, at a CAGR of 7.35% during the forecast period (2026-2031). Accelerated growth stems from breakthrough gene-editing and small-interfering RNA (siRNA) therapies that promise durable LDL-C control, shifting care models away from lifelong pill regimens toward potential one-time interventions. Adoption is further propelled by expanding dyslipidemia prevalence among aging and obesity-prone populations, widening payer acceptance of outcomes-based contracts, and rising digital-pharmacy penetration that eases therapy access. Heightened M&A activity—typified by Eli Lilly’s USD 1.3 billion purchase of Verve Therapeutics—signals large-cap commitment to next-generation modalities and intensifies rivalry around pipeline differentiation. Regional momentum is tilting toward Asia-Pacific, where demographic transitions and rapid e-commerce uptake position the lipid disorder treatment market for double-digit expansion.

Key Report Takeaways

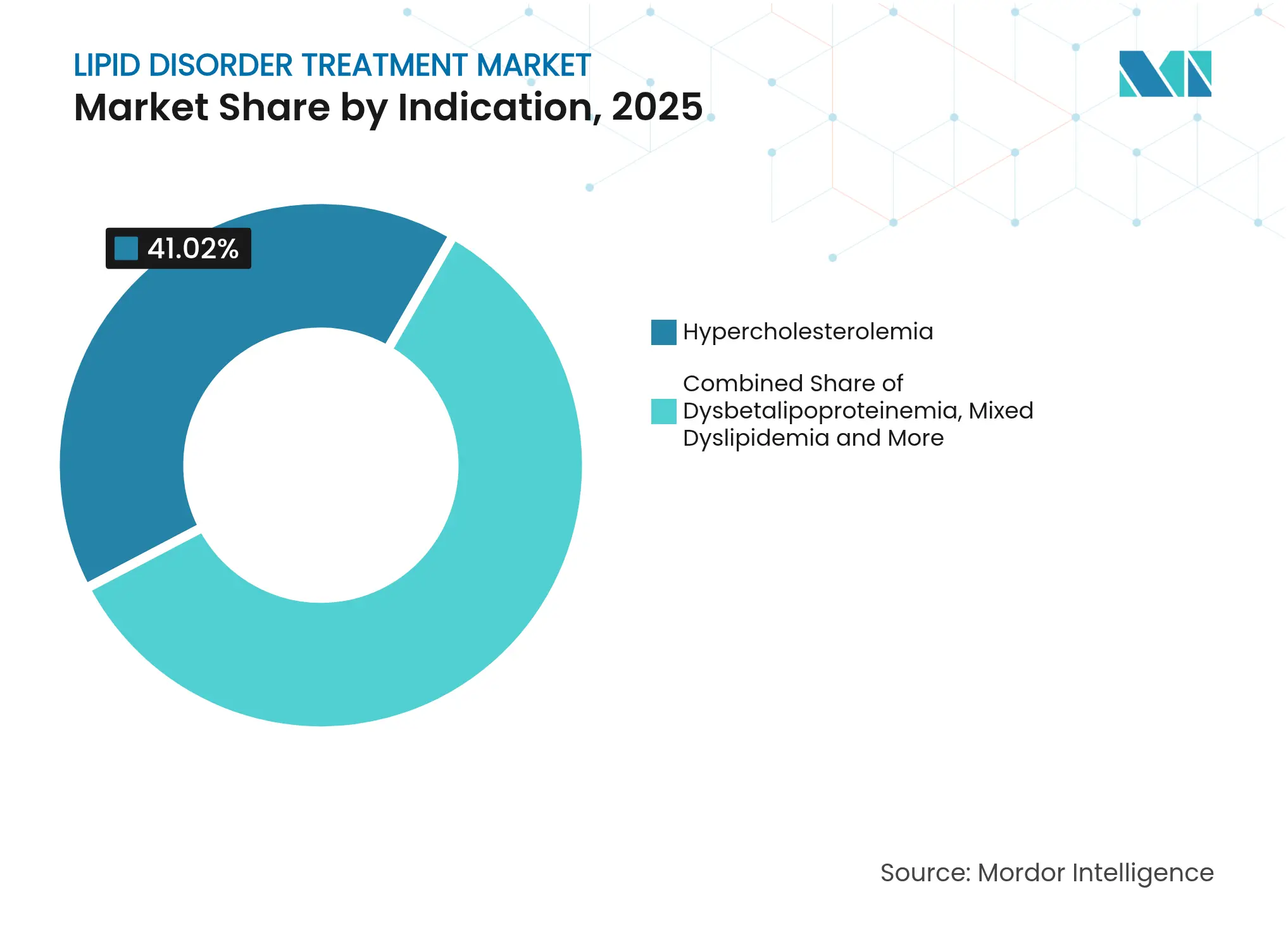

- By indication, hypercholesterolemia led with 41.02% revenue share in 2025; familial hypercholesterolemia is advancing at a 12.11% CAGR through 2031.

- By drug class, statins held 55.92% of the lipid disorder treatment market share in 2025, while PCSK9 inhibitors are projected to expand at a 16.2% CAGR to 2031.

- By distribution channel, retail pharmacies captured 45.68% revenue in 2025; online pharmacies are forecast to post a 13.22% CAGR through 2031.

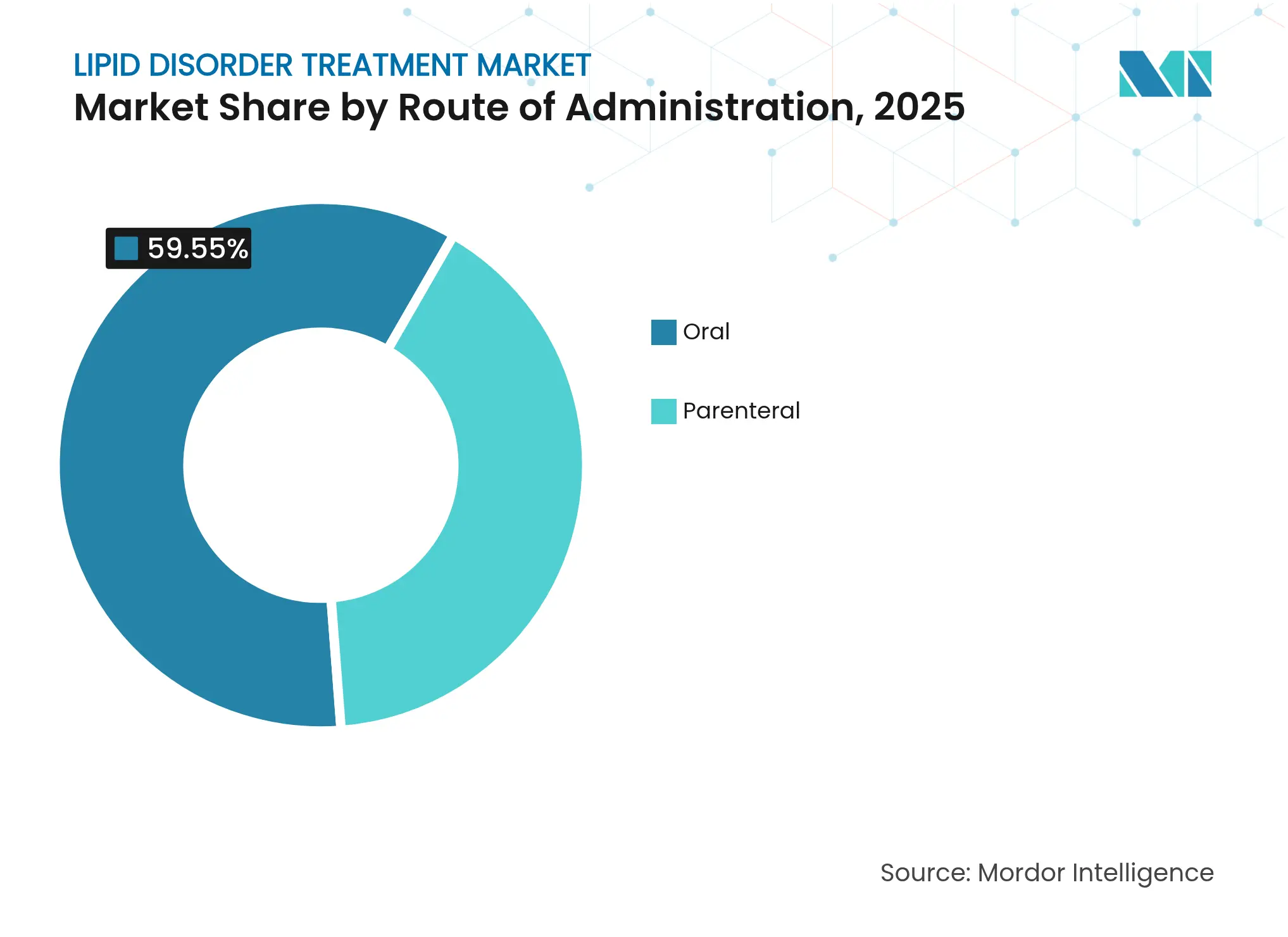

- By route of administration, oral formulations accounted for 59.55% of the lipid disorder treatment market size in 2025 and parenteral routes are progressing at an 11.18% CAGR through 2031.

- By patient type, high cardiovascular-risk patients commanded 54.85% share in 2025; the statin-intolerant subgroup is set to grow at a 12.02% CAGR between 2026-2031.

- By geography, North America contributed 35.98% of 2025 revenue, whereas Asia-Pacific is on track for a 10.2% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Lipid Disorder Treatment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Escalating prevalence of lifestyle-linked dyslipidemia

Escalating prevalence of lifestyle-linked dyslipidemia

| +2.1% | Asia-Pacific, Latin America, Middle East & Africa | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

+2.1%

| Geographic Relevance:

Asia-Pacific, Latin America, Middle East & Africa

| Impact Timeline:

Medium term (2-4 years)

|

Rapid growth in at-risk aging populations

Rapid growth in at-risk aging populations

| +1.8% | North America, Europe, Japan | Long term (≥ 4 years) | |||

Strong late-stage pipeline of novel LDL-lowering agents

Strong late-stage pipeline of novel LDL-lowering agents

| +1.5% | United States, European Union | Short term (≤ 2 years) | |||

Expansion of e-commerce & online pharmacy channels

Expansion of e-commerce & online pharmacy channels

| +1.2% | India, Southeast Asia, Middle East | Medium term (2-4 years) | |||

siRNA-based twice-yearly therapies improve adherence

siRNA-based twice-yearly therapies improve adherence

| +0.9% | North America, Western Europe | Medium term (2-4 years) | |||

Genomic screening driving earlier FH diagnosis

Genomic screening driving earlier FH diagnosis

| +0.6% | United States, Europe, Australia | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Escalating Prevalence of Lifestyle-Linked Dyslipidemia

Cardiovascular disease is projected to affect 61% of U.S. adults by 2050, with obesity prevalence climbing from 43.1% in 2024 to 60.6% in 2050 and hypertension from 51.2% to 61%. Comparable patterns in Europe, where cardiovascular disease already causes 3.9 million deaths annually, underscore the centrality of aggressive lipid management[1]European Society of Cardiology, “Cardiovascular Disease Statistics,” escardio.org. Rising middle-class wealth in Asia amplifies high-fat dietary intake and sedentary lifestyles, accelerating uptake of prescription lipid-lowering therapies. Consequently, the lipid disorder treatment market is experiencing sustained prescription volume growth across both primary and secondary prevention settings. Pharmaceutical companies are responding with culturally tailored adherence programs and tele-nutrition services that integrate lipid monitoring into everyday wellness applications.

Rapid Growth in At-Risk Aging Populations

Global life expectancy gains mean 17% of people will be ≥ 85 years old by 2050, amplifying cumulative LDL-C exposure and polymorbidity. Japan, already the world’s oldest society, expects heart failure cases to reach 1.3 million by 2030, prompting cardiogeriatric-specific treatment protocols. Older adults often present polypharmacy challenges and variable statin tolerance, fueling demand for lower-frequency injectables and gene-editing options that minimize daily pill burdens. Health-technology-assessment agencies are revising cost-effectiveness thresholds to accommodate high-priced but durable therapeutics for seniors.

Strong Late-Stage Pipeline of Novel LDL-Lowering Agents

Phase 2 data for Zerlasiran demonstrated 99% median reductions in lipoprotein(a), while Lepodisiran delivered up to 93.9% suppression with quarterly or semiannual dosing[2]New England Journal of Medicine, “Lepodisiran—A Long-Duration siRNA,” nejm.org. Gene-editing candidate VERVE-102 uses base-editing to silence PCSK9 permanently, signaling a potential one-time cure for hypercholesterolemia. Accelerated approval designations and breakthrough therapy tags from the FDA and EMA shorten regulatory timelines, making 2025-2027 pivotal launch years. Investors view these modalities as portfolio-defining assets, igniting above-market valuation multipliers in recent M&A deals.

Expansion of E-Commerce & Online Pharmacy Channels

Post-pandemic consumer behavior shifted decisively toward digital fulfillment: more than 30% of chronic-disease prescriptions in India were dispensed online in 2024. Telepharmacy platforms integrate e-prescriptions, automated refills, and pharmacist video consults, improving adherence in lipophilic disorders traditionally plagued by drop-off rates exceeding 40% at 12 months. Venture funding into pharmacy-tech startups surpassed USD 1.2 billion in 2024, underpinning logistics networks capable of same-day delivery in major metros. The lipid disorder treatment market therefore benefits from reduced last-mile friction and broader rural reach.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Statin intolerance & safety-concern non-adherence

Statin intolerance & safety-concern non-adherence

| -1.4% | Global, elderly skew | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

-1.4%

| Geographic Relevance:

Global, elderly skew

| Impact Timeline:

Medium term (2-4 years)

|

High cost & reimbursement hurdles for biologics

High cost & reimbursement hurdles for biologics

| -1.1% | Emerging markets, select OECD payers | Long term (≥ 4 years) | |||

Concentrated API supply chains raising shortage risk

Concentrated API supply chains raising shortage risk

| -0.8% | Dependence on China, India | Short term (≤ 2 years) | |||

Outcomes-based contracts pressure premium pricing

Outcomes-based contracts pressure premium pricing

| -0.5% | North America, Europe | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Statin Intolerance & Safety-Concern Non-Adherence

Real-world evidence indicates 6-10% of statin users discontinue therapy due to muscle symptoms or perceived hepatic risk. Genetic polymorphisms such as SLCO1B1 increase intolerance odds at standard doses, complicating first-line therapy selection. Patient surveys reveal that 51.5% prefer lifestyle changes over prescription escalation, and 17.1% cite pill burden as rationale for rejection. These dynamics heighten demand for alternatives like bempedoic acid, inclisiran, and ezetimibe combinations that occupy premium reimbursed positions but can erode overall lipid disorder treatment market penetration if access remains uneven.

High Cost & Reimbursement Hurdles for Biologics

Annualized treatment costs for PCSK9 inhibitors exceed USD 5,900 in the United States before rebates, necessitating prior authorization and step therapy[3]Federal Register, “Medicare Payment Policies 2024-2025,” federalregister.gov. Outcomes-based agreements, such as bluebird bio’s Medicaid deal tying gene-therapy reimbursement to clinical endpoints, portend broader application in lipid management. Yet small commercial plans often lack actuarial depth to model long-term benefits, slowing formulary inclusion. Emerging-market payers grapple with single-source biologic imports priced at 50-200% of median household income, limiting uptake.

Segment Analysis

By Indication: Familial Hypercholesterolemia Catalyzes Genetic Testing Uptake

Familial hypercholesterolemia (FH) accounted for 12.58% of the lipid disorder treatment market size in 2025 and is expected to deliver the fastest 12.11% CAGR through 2031. Hypercholesterolemia without genetic confirmation retained overall volume leadership, holding 41.02% share in 2025. Enhanced cascade testing uncovers undiagnosed FH relatives, driving prescription initiation of PCSK9 inhibitors and siRNA constructs. FH prevalence of 1 in 250 general population and up to 1 in 16 among premature coronary-artery-disease patients creates a sizable, genomically identifiable submarket. Societal guidelines increasingly recommend universal cholesterol screening by age 2, funneling pediatric cases into specialized lipid clinics that employ gene panels for definitive classification.

Precision-medicine reimbursement frameworks now classify FH therapies as high-value due to lifetime event avoidance. Payer pilots in Canada and the Netherlands demonstrate cost savings when relatives are proactively screened and treated early. Consequently, the lipid disorder treatment market registers escalating demand for next-generation agents positioned as first-line for genetically confirmed FH, accelerating sales traction well before statin failure.

Note: Segment shares of all individual segments available upon report purchase

By Drug Class: PCSK9 Inhibitors Lead the Innovation Wave

Statins maintained 55.92% share of the lipid disorder treatment market in 2025, buoyed by generics and entrenched guideline preference. However, PCSK9 inhibitors are projected to outpace all other classes at a 16.2% CAGR, energized by twice-yearly inclisiran and upcoming fully human monoclonal antibodies requiring quarterly injections. In pivotal trials, inclisiran sustained 50-55% LDL-C reductions over 18 months with adherence above 90%. Bempedoic acid offers 17-28% LDL-C lowering for statin-intolerant patients, occupying a niche yet expanding adjunct market. Antisense oligonucleotides targeting apo(a), CETP, and ANGPTL3 present pipeline diversity, ensuring multi-mechanistic competition that broadens physician choice.

Rebate dynamics evolve: manufacturers extend value-based contracts pegged to real-world LDL-C trajectories and cardiovascular outcomes, thus gaining earlier formulary positioning. This aligns economic incentives across stakeholders and augments penetration into risk-based insurance cohorts. As a result, the lipid disorder treatment industry increasingly pivots from volume-driven statin scripts to outcome-anchored biologic regimens.

By Distribution Channel: Digital Transformation Lifts Online Dispensing

Retail pharmacies captured 45.68% share of the lipid disorder treatment market in 2025 by leveraging neighborhood access and integrated vaccination services. Nevertheless, online pharmacies registered a 13.22% CAGR and are poised to erode brick-and-mortar dominance by 2031. Start-ups deploy AI to predict refill gaps and push adherence nudges, while established chains roll out same-day drone delivery pilots in suburban corridors. Hospital pharmacies remain essential for parenteral initiations but have begun shipping maintenance doses directly to patients under collaborative-practice agreements.

Policy tailwinds, such as e-prescription mandates and expanded telehealth reimbursement, boost digital-first channels. Fraud-detection algorithms and centralized license verification mitigate historical safety concerns, fostering regulator confidence. Consequently, multichannel strategies become mandatory for manufacturers seeking comprehensive patient reach within the lipid disorder treatment market.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Route of Administration: Parenteral Modalities Challenge Oral Dominance

Oral tablets retained 59.55% share in 2025, yet injectables are gaining ground with an 11.18% CAGR. Twice-yearly subcutaneous siRNA injections and quarterly monoclonal antibodies dramatically reduce dosing burden. Patient-friendly autoinjectors with hidden needles and temperature sensors enhance usability, while pharmacist-led administration programs streamline initiation. Single-dose intravenous gene editing represents a prospective leap, offering curative potential and redefining reimbursement calculus.

Extended-release microspheres and implantable pumps remain exploratory but underscore industry focus on convenience and adherence. Over time, rising confidence in self-injection could compress oral share below 50%, reshaping supply-chain forecasting for wholesalers serving the lipid disorder treatment market.

Note: Segment shares of all individual segments available upon report purchase

By Patient Type: Statin-Intolerant Cohort Spurs Alternative Uptake

High-cardiovascular-risk patients represented 54.85% of 2025 revenue; yet statin-intolerant individuals are growing fastest at 12.02% CAGR. Simulation studies indicate that 15-20% of high-risk patients fail to hit LDL-C targets on maximally tolerated statins, prompting therapy escalation to PCSK9 inhibitors or bempedoic acid. Revised 2024 ESC guidelines now recommend non-statin add-ons when LDL-C remains above 70 mg/dL after 8 weeks, legitimizing earlier biologic use. Personalized pharmacogenomics informs regimen selection, enhancing efficacy and limiting adverse events.

Manufacturers develop patient-support hubs offering muscle-symptom management education and copay assistance, improving persistence. As the statin-intolerant base enlarges, payers explore step-edit protocols that prioritize biannual injectables over costly monthly monoclonals, influencing formulary dynamics within the lipid disorder treatment industry.

Geography Analysis

North America dominated the lipid disorder treatment market with 35.98% revenue share in 2025, underpinned by robust insurance coverage, proactive screening, and rapid biotech adoption. Breakthrough therapy designations for inclisiran, olezarsen, and gene-editing assets streamline U.S. approvals, while CMS is aligning reimbursement to clinical performance metrics starting 2026. Real-world evidence platforms such as PCORnet facilitate post-marketing surveillance, strengthening payer confidence in innovative modalities. Canadian provinces pilot cascade FH screening programs funded through public registries, widening eligible patient pools.

Europe posted steady, mid-single-digit growth, sustained by national lipid-clinic networks and payer willingness to reimburse high-cost injectables when preventive value is demonstrable. EMA guideline revisions emphasize unmet medical need and accelerate adaptive licensing, helping the lipid disorder treatment market transition new mechanisms into clinical practice sooner. However, pricing negotiations in Germany’s AMNOG framework and France’s CEPS increasingly tie list prices to measurable cardiovascular outcomes, pressuring manufacturer margins.

Asia-Pacific is the fastest-growing region at a 10.2% CAGR, driven by China’s aging demographic and India’s expanding middle class. Government reimbursement lists in China added PCSK9 inhibitors in 2024, cutting patient co-pay by 60% and triggering prescription inflection. Japan invests in cardiac telerehabilitation and home-injection programs tailored for elderly patients, raising persistence rates. Meanwhile, e-pharmacy regulations in India legitimize nationwide mail-order cholesterol therapies, closing rural access gaps. Collectively, these trends cement Asia-Pacific as a prime contributor to incremental lipid disorder treatment market size through 2031.

Competitive Landscape

Market Concentration

The lipid disorder treatment market exhibits moderate concentration, with the top five companies having significant global revenue in 2024. Pfizer, Merck, and AstraZeneca hold entrenched statin portfolios, while Amgen and Regeneron anchor the PCSK9 franchise. Strategic acquisitions surged in 2024-2025: Eli Lilly acquired Verve Therapeutics for USD 1.3 billion to secure one-time PCSK9 gene editing; Novo Nordisk purchased Cardior for USD 1.1 billion to diversify into RNA therapies; and Johnson & Johnson added V-Wave for USD 1.7 billion to complement device-drug synergies.

Competition pivots on mechanism novelty, dosing convenience, and value-based contracting prowess. Biosimilar PCSK9 entrants are expected post-2027, likely compressing price but expanding volume in emerging markets. AI-enhanced drug discovery shortens cycle times: Viz.ai’s collaboration with three pharma partners illustrates hospital-network analytics feeding real-world data back into pipeline refinement. Companies that integrate digital-health ecosystems—spanning remote lipid monitoring, adherence gamification, and telecardiology—build durable differentiation in the lipid disorder treatment industry.

Lipid Disorder Treatment Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: FDA approved Ctexli (chenodiol) as the first therapy for cerebrotendinous xanthomatosis, broadening rare lipid-storage disease options.

- March 2024: Regeneron gained FDA clearance for pediatric use of Praluent (alirocumab) in heterozygous familial hypercholesterolemia.

Table of Contents for Lipid Disorder Treatment Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Escalating Prevalence Of Lifestyle-Linked Dyslipidemia

- 4.2.2Rapid Growth In At-Risk Ageing Populations

- 4.2.3Strong Late-Stage Pipeline Of Novel LDL-Lowering Agents

- 4.2.4Expansion Of E-Commerce & Online Pharmacy Channels

- 4.2.5siRNA-Based Twice-Yearly Therapies Improve Adherence

- 4.2.6Genomic Screening Driving Earlier FH Diagnosis

- 4.3Market Restraints

- 4.3.1Statin Intolerance & Safety-Concern Non-Adherence

- 4.3.2High Cost & Reimbursement Hurdles For Biologics

- 4.3.3Concentrated API Supply Chains Raising Shortage Risk

- 4.3.4Outcomes-Based Contracts Pressure Premium Pricing

- 4.4Porter's Five Forces

- 4.4.1Threat of New Entrants

- 4.4.2Bargaining Power of Buyers

- 4.4.3Bargaining Power of Suppliers

- 4.4.4Threat of Substitutes

- 4.4.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Indication

- 5.1.1Hypercholesterolemia

- 5.1.2Dysbetalipoproteinemia

- 5.1.3Familial Combined Hyperlipidemia

- 5.1.4Familial Hypercholesterolemia

- 5.1.5Mixed Dyslipidemia

- 5.1.6Others

- 5.2By Drug Class

- 5.2.1Statins

- 5.2.2PCSK9 Inhibitors

- 5.2.3Cholesterol Absorption Inhibitors

- 5.2.4Bempedoic Acid

- 5.2.5Fibrates

- 5.2.6Omega-3 Fatty Acids & Others

- 5.3By Distribution Channel

- 5.3.1Hospital Pharmacies

- 5.3.2Retail Pharmacies

- 5.3.3Online Pharmacies

- 5.4By Route of Administration

- 5.4.1Oral

- 5.4.2Parenteral

- 5.5By Patient Type

- 5.5.1Primary Hyperlipidemia

- 5.5.2Familial Hypercholesterolemia

- 5.5.3Statin-Intolerant Patients

- 5.5.4High CV-risk Patients

- 5.6Geography

- 5.6.1North America

- 5.6.1.1United States

- 5.6.1.2Canada

- 5.6.1.3Mexico

- 5.6.2Europe

- 5.6.2.1Germany

- 5.6.2.2United Kingdom

- 5.6.2.3France

- 5.6.2.4Italy

- 5.6.2.5Spain

- 5.6.2.6Rest of Europe

- 5.6.3Asia-Pacific

- 5.6.3.1China

- 5.6.3.2Japan

- 5.6.3.3India

- 5.6.3.4South Korea

- 5.6.3.5Australia

- 5.6.3.6Rest of Asia-Pacific

- 5.6.4Middle East and Africa

- 5.6.4.1GCC

- 5.6.4.2South Africa

- 5.6.4.3Rest of Middle East and Africa

- 5.6.5South America

- 5.6.5.1Brazil

- 5.6.5.2Argentina

- 5.6.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Pfizer Inc

- 6.3.2Novartis AG

- 6.3.3AstraZeneca plc

- 6.3.4Merck & Co.

- 6.3.5Amgen Inc

- 6.3.6Sanofi SA

- 6.3.7Regeneron Pharmaceuticals

- 6.3.8Esperion Therapeutics

- 6.3.9Amarin Corporation

- 6.3.10Kowa Pharmaceuticals America

- 6.3.11Teva Pharmaceuticals

- 6.3.12Viatris Inc

- 6.3.13Glenmark Pharma

- 6.3.14Sun Pharma

- 6.3.15Cipla

- 6.3.16Lupin Ltd

- 6.3.17Emcure Pharma

- 6.3.18Aegerion (Chiesi)

- 6.3.19Torrent Pharma

- 6.3.20Abbott Laboratories

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Lipid Disorder Treatment Market Report Scope

As per the scope of the report, lipid disorders comprise a broad spectrum of conditions where the blood lipid levels are affected. Generally, it is associated with an increase in the blood lipid levels.