Celiac Disease Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

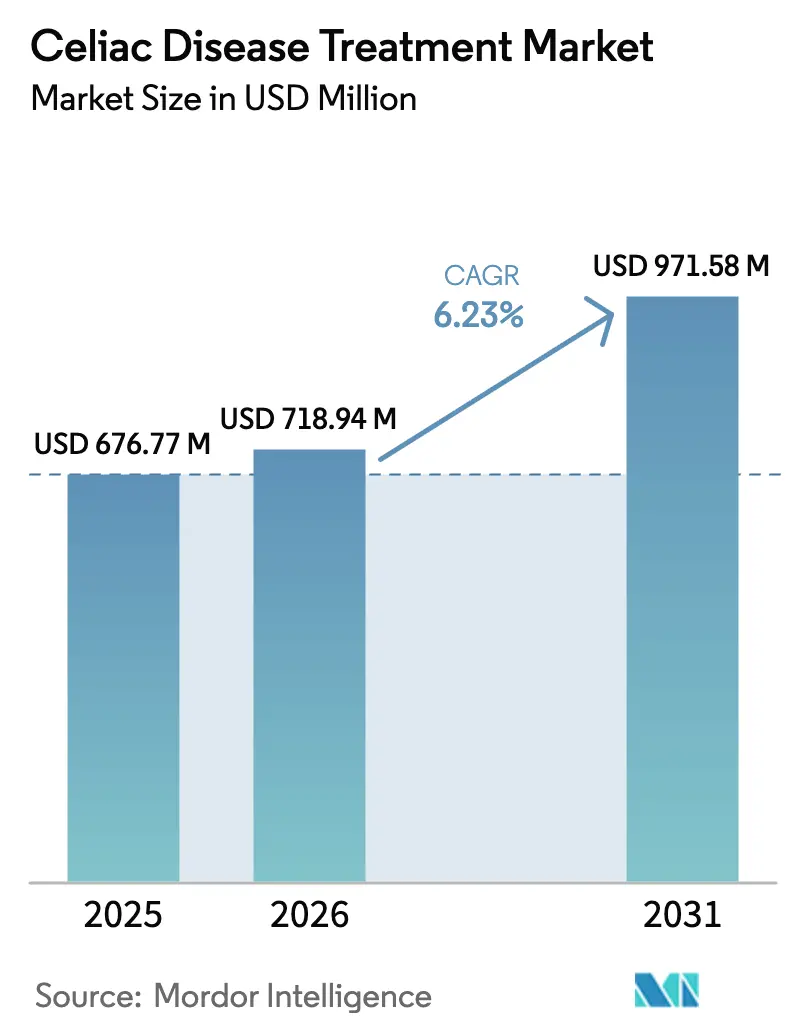

| Market Size (2026) | USD 718.94 Million |

| Market Size (2031) | USD 971.58 Million |

| Growth Rate (2026 - 2031) | 6.23% CAGR |

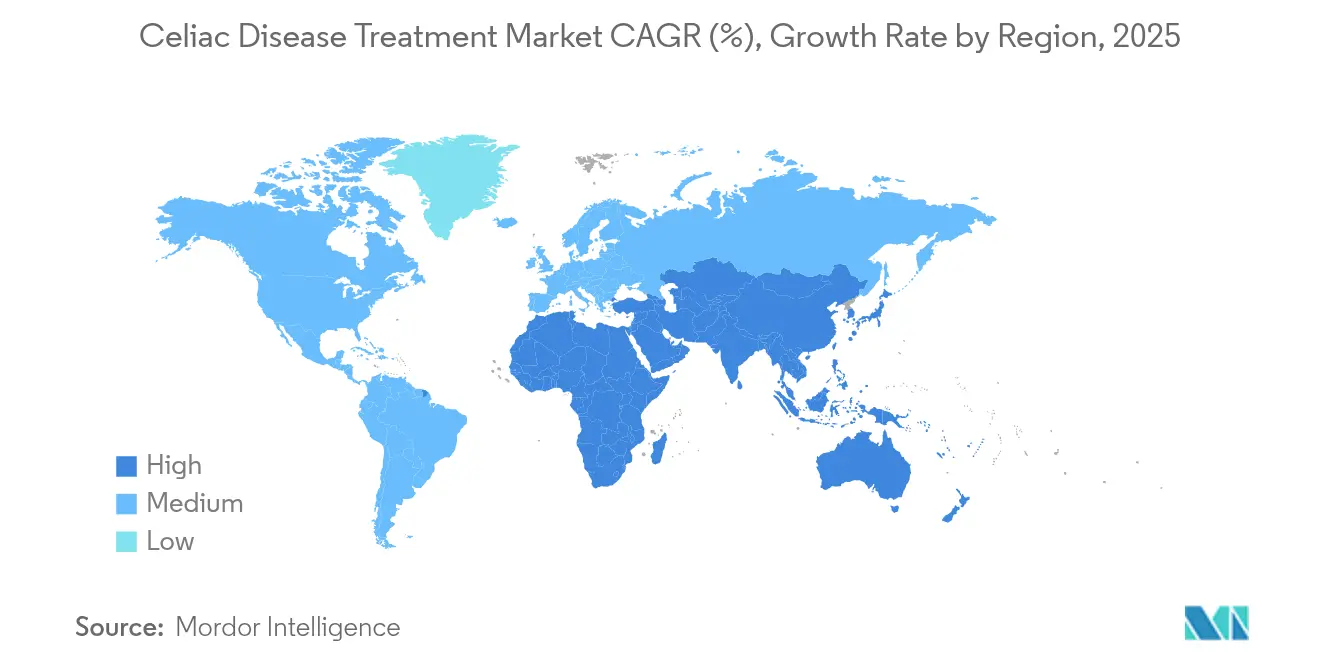

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

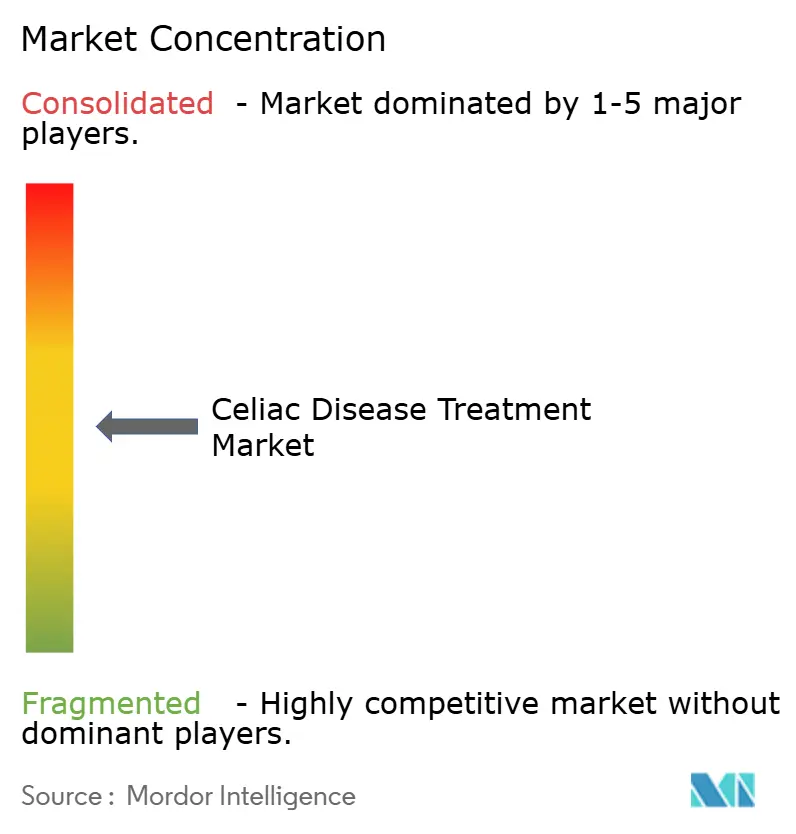

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Celiac Disease Treatment Market Analysis by Mordor Intelligence

Celiac Disease Treatment Market size in 2026 is estimated at USD 718.94 million, growing from 2025 value of USD 676.77 million with 2031 projections showing USD 971.58 million, growing at 6.23% CAGR over 2026-2031.

Rising prevalence across every major region, wider primary-care screening, and a late-stage pipeline spanning enzymes, biologics, and tolerance-inducing immunotherapies sustain forward momentum. North American adoption stays high because of specialist density and reimbursement clarity, whereas Asia-Pacific growth accelerates as serology access improves. Venture funding into oral enzyme platforms, coupled with digital pharmacy expansion, is shortening patient pathways to therapy. Intensifying competition among Takeda, Entero Therapeutics, and Anokion underlines the race for the first FDA approval in the celiac disease treatment market.

Key Report Takeaways

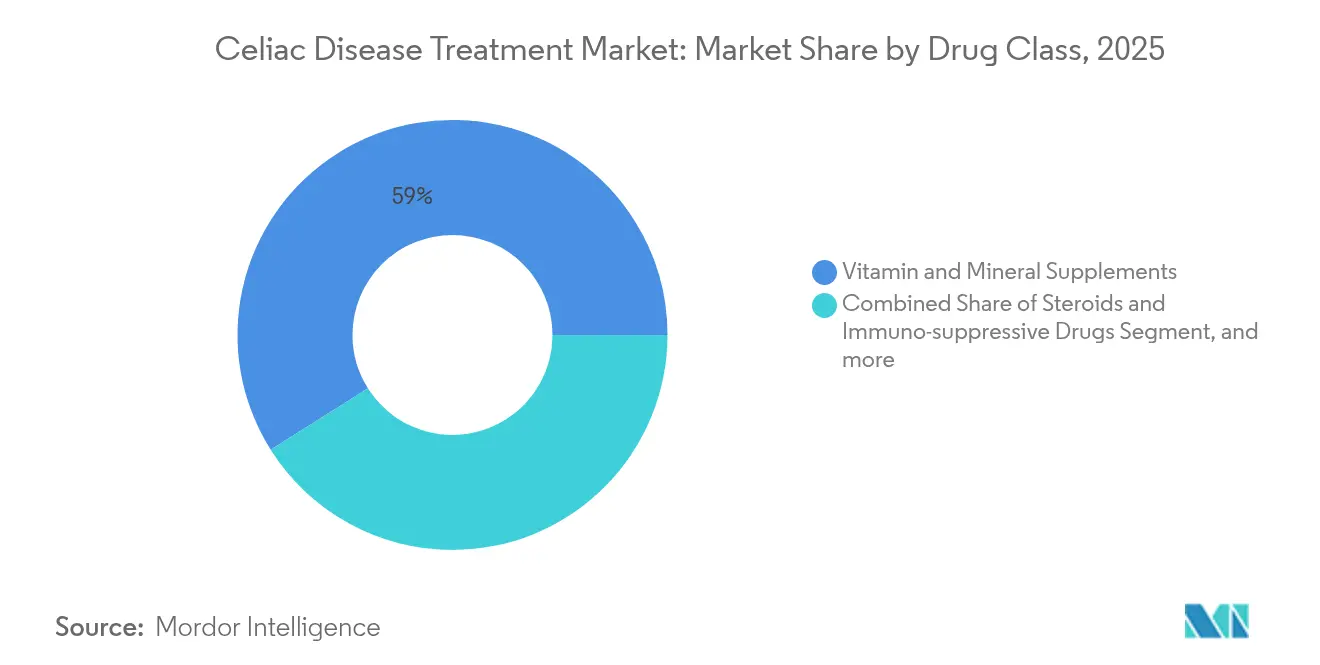

- By drug class, vitamin & mineral supplements led with 58.96% of celiac disease treatment market share in 2025, while enzyme-based therapies post the fastest 7.48% CAGR to 2031.

- By disease type, classical CD accounted for 72.25% of the celiac disease treatment market size in 2025; refractory CD is projected to expand at an 11.05% CAGR through 2031.

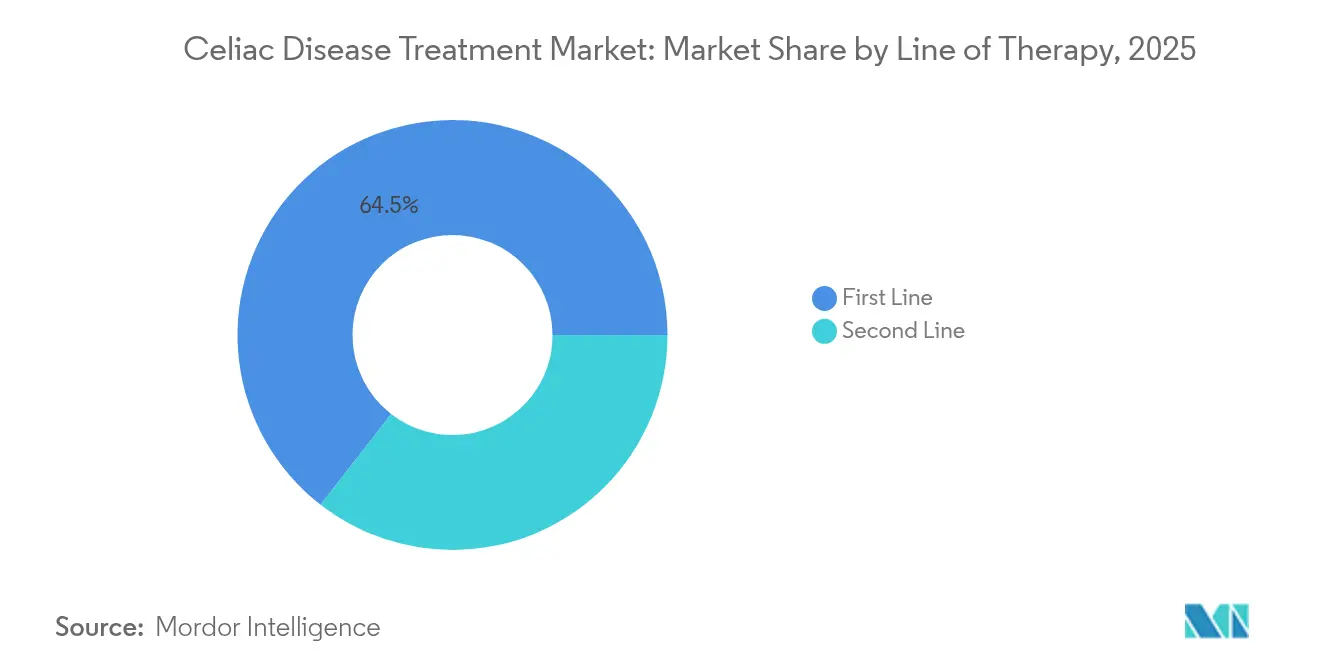

- By line of therapy, first-line care held 64.48% share in 2025; second-line options record a 8.91% CAGR to 2031.

- By route, oral delivery maintained 44.92% share; parenteral agents register the quickest 8.62% CAGR on the back of anti-IL-15 biologics.

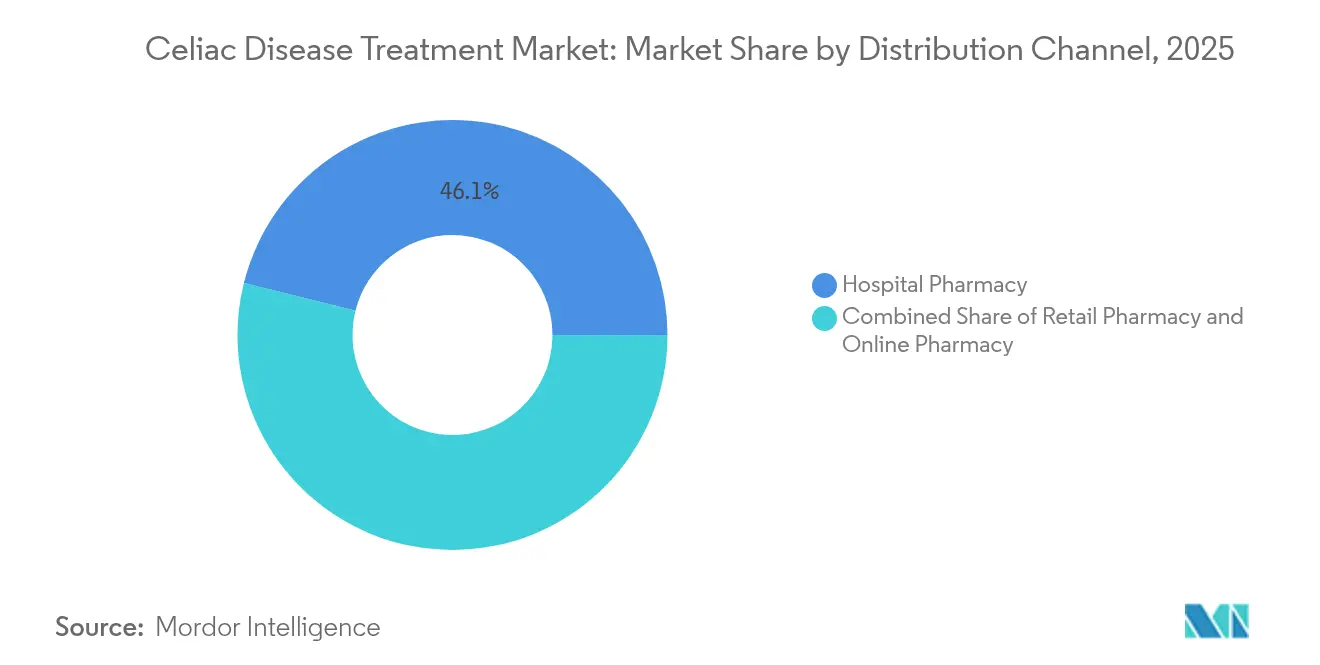

- By distribution channel, hospital pharmacy captured 46.12% share, whereas online pharmacy advances at a 9.92% CAGR.

- By geography, North America commanded 45.22% of the celiac disease treatment market in 2025; Asia-Pacific delivers the highest 9.24% CAGR over the period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Celiac Disease Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Prevalence & Diagnosis of Celiac Disease | +1.2% | Global, with higher impact in Asia-Pacific and developing regions | Medium term (2-4 years) |

| Patient Burden with Gluten-Free Diet Fuels Demand for Drugs | +0.9% | North America & Europe primarily, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Late-Stage Pipeline Momentum | +1.5% | Global, with regulatory focus in US and EU | Medium term (2-4 years) |

| Expansion of Digital Antibody Screening in Primary Care | +0.8% | North America & Europe, with spillover to urban Asia-Pacific | Short term (≤ 2 years) |

| Microbiome-Modulating Therapeutics Emerge as Adjuncts | +0.7% | Global, with research concentration in US and Europe | Long term (≥ 4 years) |

| Venture-Capital Surge into Oral Enzyme Delivery Platforms | +0.6% | Global, with funding concentration in US and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global Prevalence & Diagnosis

Broader serological studies position celiac disease at 1.2% in low-risk and 4.3% in high-risk Asia-Pacific populations, overturning the historical view of a Western-centric disorder.[1]Yanjun Bao, “Global Prevalence of Celiac Disease: A Comprehensive Review,” Scientific Reports, nature.com Government-backed pediatric screening in China and India moves detection upstream, reinforcing specialty demand. FDA clearance of the GlutenID kit in 2025 adds a home-test dimension that funnels more positives to gastroenterologists. Better recognition translates into earlier intervention, helping expand the Celiac disease treatment market across both adult and pediatric cohorts. The trend also underpins rising trial enrollment rates, de-risking sponsor timelines.

Patient Burden with Gluten-Free Diet Fuels Demand for Drugs

Strict diet adherence rarely yields full mucosal healing; biopsies still show villous damage in up to 40% of compliant patients.[2]Alessio Fasano, “Persistent Villous Atrophy in Treated Celiac Disease,” World Journal of Gastroenterology, wjgnet.com The psychological weight of constant label reading and social limitations drives willingness to consider adjunctive pharmacotherapy. Premium prices for gluten-free groceries continue to exceed conventional items, widening socioeconomic inequity. Cross-contamination remains rampant in restaurant and school settings, often invisible to the patient until symptom flare. Collectively, these pain points accelerate the shift from exclusive dietary management toward drug-supported care, reinforcing growth in the Celiac disease treatment market.

Late-Stage Pipeline Momentum

Eight Phase 2 or Phase 3 agents reported positive readouts since 2024, signaling a maturing evidence base. Latiglutenase lowered mucosal injury scores and symptoms in its 2024 Phase 2 study, prompting a pivotal trial launch in early 2025. KAN-101 induced durable immune tolerance with favorable safety at the January 2025 interim analysis. Fast-Track status for TEV-53408 and TAK-101 illustrates FDA intent to clarify endpoints and compress review cycles. This clustering of late-stage assets boosts investor confidence and encourages additional entrants into the celiac disease treatment market.

Expansion of Digital Antibody Screening in Primary Care

Multiplex lateral-flow assays now deliver anti-tTG and anti-DGP results in under 15 minutes, matching laboratory accuracy.[3]Sheila Crowe, “Diagnostic Accuracy of Point-of-Care Tests for Celiac Disease,” PubMed, pubmed.ncbi.nlm.nih.gov Novoviah’s Novoleukin test even detects T-cell reactivity in diet-adherent patients with 90% sensitivity. Embedding these devices in family practice cuts specialist wait times, reduces diagnostic delay, and enlarges the treated population. Digital dashboards feed anonymized prevalence data back to public-health agencies, guiding resource allocation and further fueling the Celiac disease treatment market expansion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| No FDA-Approved Drugs & Uncertain Regulatory Pathway | -1.8% | Global, with primary impact in US and EU regulatory jurisdictions | Medium term (2-4 years) |

| High Research & Development Cost | -1.1% | Global, with higher impact in regions with limited healthcare funding | Long term (≥ 4 years) |

| Auto-Immunity Risk of Tolerance-Inducing Therapies | -0.9% | Global, with heightened regulatory scrutiny in US and Europe | Long term (≥ 4 years) |

| Inconsistent Dietary Gluten Confounds Clinical End-Points | -0.7% | Global, with particular challenges in regions with limited gluten-free infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

No FDA-Approved Drugs & Uncertain Regulatory Pathway

Without precedent drugs, companies face shifting guidance on histological versus symptomatic endpoints. Gluten-challenge designs deter volunteers, elongate recruitment, and elevate ethical hurdles. EMA insistence on multi-year safety exposure extends trials and inflates capital needs. Sponsors consequently adopt adaptive protocols, but regulators still debate what magnitude of villous re-growth constitutes clinical benefit. This ambiguity depresses near-term revenue visibility in the Celiac disease treatment market.

High Research & Development Cost

Refractory CD incidence is low, so late-phase studies necessitate global site networks and specialized pathology services. Entero Therapeutics budgets USD 80 million for its latiglutenase Phase 3 program, a heavy lift for venture-backed firms. Biopsy confirmation, endoscopic monitoring, and dietary compliance verification add unique cost layers. Smaller innovators must partner with big pharma, trading equity for cash, thereby diluting upside potential and slowing new entrant velocity in the Celiac disease treatment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Supplement Dominance Meets Enzyme Upswing

The vitamin & mineral supplements segment held 58.96% of the celiac disease treatment market size in 2025 because clinicians routinely prescribe iron, vitamin D, and calcium to correct malabsorption. Enzymes captured a modest base today yet deliver a 7.48% CAGR, reflecting patient appetite for gluten-neutralizing options that enable dietary latitude. Biologics targeting IL-15 inch forward in refractory cohorts, while tight-junction modulators such as ZED1227 illustrate pipeline breadth. Competitive intensity rises as Takeda partners with Zedira to co-promote its leading protease inhibitor upon approval. Patient education campaigns stress that supplements do not treat villous injury, a nuance that redirects volume toward emerging actives. As efficacy data accumulates, payers may adjust formularies to favor enzymatic prophylaxis, unlocking incremental value within the Celiac disease treatment market.

Growth potential concentrates around stomach-stable enzyme cocktails designed to degrade the 33-mer fragment before it reaches the duodenum. Phase 2 readouts show latiglutenase reducing symptom scores by 40% compared with placebo, attracting insurer interest in coverage criteria. Probiotic-enzyme co-formulations enter early investigation, aiming to bundle microbiome restoration with peptide cleavage. Supplemental SKUs stay relevant for baseline nutrient repletion, but margin pressure mounts from private-label entries. Ultimately, dual-therapy frameworks combining vitamins and enzymes could optimize outcomes and preserve share for incumbent brands in the celiac disease treatment market.

By Disease Type: Classical Bulk, Refractory Upside

Classical CD absorbed 72.25% of 2025 revenue, underscoring its high detection rate in symptomatic adults. Screening expansion identifies more silent cases, yet refractory CD charts the steepest curve with an 11.05% CAGR, mirroring unmet need where the gluten-free diet falters. Biologic lines of therapy concentrate here, with anti-IL-15 antibodies aiming to intercept intra-epithelial lymphocyte activation. Health-system burden remains higher in refractory cases because of hospitalization for malnutrition and osteoporosis, pushing policymakers to subsidize novel options. The Celiac disease treatment market therefore expects faster formulary inclusion once efficacy is proven.

Silent CD, often incidentally spotted via serology, draws attention as long-term risks of lymphoma become clearer. These patients extend lifetime therapeutic windows even if symptom severity is low. Non-responsive CD, where mucosal healing stalls despite adherence, becomes a priority subgroup for enzyme trials. Researchers refine stratification biomarkers, directing high-risk genotypes into drug arms. This precision approach can improve overall responder rates, enhancing the competitiveness of late-stage assets in the Celiac disease treatment market.

By Line of Therapy: Diet First, Drugs Next

First-line care, dominated by nutritional counseling and gluten-free staples, held 64.48% share in 2025. Yet second-line options are slated for a 8.91% CAGR as physicians seek adjuncts that address residual inflammation. Op-ex savings from reduced endoscopy frequency could offset drug costs, supporting reimbursement. Pivotal data demonstrating histological healing within 12 weeks could shift guidelines, encouraging earlier pharmaceutical escalation. The Celiac disease treatment market thus primes for a staged treatment algorithm that mirrors inflammatory bowel disease pathways.

Third-line measures, including immunosuppressants like azathioprine, remain reserved for severe refractory cases due to toxicity. Pipeline agents hope to displace steroids by offering targeted action with fewer systemic effects. Post-approval real-world evidence will clarify the optimal sequence, but early modeling suggests enzyme prophylaxis may sit ahead of biologics for cost-effectiveness. As patient support programs mature, adherence hurdles ease, further driving the evolution of therapy lines in the celiac disease treatment market.

By Route of Administration: Oral Familiarity, Parenteral Precision

Oral dosage forms generated 44.92% revenue in 2025, reflecting patient comfort and pharmacist accessibility. Enteric-coated tablets and sprinkle capsules drive convenience and consistent exposure. Parenteral biologics grow at 8.62% CAGR, capitalizing on monthly or quarterly dosing that appeals to refractory patients seeking sustained control. Home-injection devices reduce clinic visits, lowering indirect costs. Sublingual and intranasal routes sit in early pipeline stages, aiming to induce tolerance through mucosal antigen presentation.

Advances in peptide nanocarriers hint at oral delivery for antibodies, potentially collapsing the distinction between routes. However, stability hurdles remain, so injection continues as the preferred vehicle for cytokine blockers in the near term. Device ecosystem support, including smart pens that log adherence, raises value propositions to payers tracking outcomes. A balanced mix of administration methods enhances therapeutic reach, reinforcing overall growth in the Celiac disease treatment market.

By Distribution Channel: Hospitals Anchor, Web Platforms Surge

Specialist-led hospital pharmacies secured 46.12% share in 2025 due to biopsy dependence and infusion services. They remain indispensable for initiating biologics and managing adverse-event surveillance. Online pharmacies demonstrate a 9.92% CAGR, fueled by prescription digital therapeutics and doorstep delivery of cold-chain biologics. Tele-gastroenterology clinics partner with e-pharmacies to expedite script fulfillment, shortening therapy onset by up to two weeks.

Retail outlets sustain over-the-counter supplement traffic, yet face substitution pressure as direct-to-consumer brands leverage social media. Regulatory frameworks in the United States now allow pharmacist-administered antibody injections, which could redirect some volume from hospitals. Integrated care platforms that bundle serology kits, dietician consults, and drug refills create a one-stop model, appealing to younger patient cohorts. Diversified channel strategies therefore extend footprint of the Celiac disease treatment market beyond traditional brick-and-mortar settings.

Geography Analysis

North America retained 45.22% share of the Celiac disease treatment market in 2025, anchored by robust payer support, aggressive patient advocacy, and top-tier diagnostic infrastructure. US gastroenterology societies updated guidelines in late 2024 to endorse adjunctive drug use when biopsy healing lags after 12 months on diet, enlarging the second-line pool. Canada’s centralized health data aids epidemiological surveillance, enabling targeted screening in high-risk First Nations communities. Mexico begins integrating serology into national nutrition programs, hinting at latent upside as household wheat intake climbs.

Europe maintains entrenched awareness and coordinated care pathways across Germany, the United Kingdom, and Scandinavia. Prescription adherence benefits from region-wide gluten-free food reimbursement schemes, enhancing disposable income for pharmaceutical copays. EMA guidance issued in 2024 on villous height:crypt depth ratios standardizes histological endpoints for trials, accelerating sponsor filings. Southern Europe catches up as Italy and Spain expand dietician training modules, supporting consistent counseling quality across urban and rural clinics. Cross-border clinical collaborations, particularly between Finland and Italy, leverage population genetics to elucidate differential drug response, enriching the evidence base for the celiac disease treatment market.

Asia-Pacific demonstrates the fastest 9.24% CAGR through 2031, rooted in rising wheat adoption and urban lifestyle shifts. China’s tier-1 hospitals pilot dual-antibody point-of-care tests, flipping the diagnostic pyramid toward primary-care initiation. India partners with non-profits to train 10,000 dieticians by 2028, mitigating counseling gaps. Japan’s universal coverage accelerates uptake of and insurance support for emerging enzyme pills. Australia continues large-scale cohort studies tracking pediatric sero-conversion, generating longitudinal data that de-risks future drug approvals regionally. Collectively, these dynamics position Asia-Pacific as the pivotal frontier for the celiac disease treatment market.

Competitive Landscape

The absence of an approved therapy keeps rivalry in the discovery phase, fragmenting share across more than 30 active developers. Takeda leverages global scale to fast-track TAK-062 enzyme tablets, pairing with Zedira for regional co-promotion once licensed. Anokion partners with Pfizer Ignite, exchanging equity for manufacturing and regulatory muscle to accelerate KAN-101. Entero Therapeutics focuses on a digital-first patient community that integrates symptom tracking into its Phase 3 design, enhancing real-world evidence capture. Together, these strategies highlight how alliances compensate for funding demands in the Celiac disease treatment market.

Risk-sharing deals proliferate as venture investors seek liquidity ahead of Phase 3 readouts. Novartis’ 2024 acquisition of Calypso Biotech signaled big-pharma appetite for mechanism diversity, prompting comparable takeovers of smaller enzyme startups. Meanwhile, Teva and Provention Bio co-develop TEV-53408, splitting commercialization territories to hedge regulatory risk. Smaller entities pursue niche angles such as nanoparticle antigen-sequestration, hoping to license out after proof-of-concept. Intellectual-property landscapes remain open, but patent cliffs loom for first-generation enzymes post-2035, encouraging multi-asset portfolios that can sustain revenue in the maturing Celiac disease treatment market.

Commercial launch planning already shapes competitive postures despite absent approvals. Survey data show 68% of US gastroenterologists willing to prescribe an enzyme adjunct within six months of approval if annual cost stays under USD 8,000 (sponsor polling). Digital adherence tools, including smart blister packs, differentiate offerings and justify value-based contracts with payers. Companies invest in patient-community education to counter misconceptions about drug-induced diet liberalization, positioning therapy as an adjunct rather than a permission slip for gluten exposure. This narrative aims to secure broad acceptance and accelerate uptake across the Celiac disease treatment market.

Celiac Disease Treatment Industry Leaders

General Mills, Inc.

Innovate Biopharmaceuticals

Takeda Pharmaceuticals

IMTherapeutics

ImmunogenX

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Teva Pharmaceutical Industries Ltd. has achieved a significant regulatory milestone with the U.S. Food and Drug Administration (FDA) granting Fast Track designation to its investigational candidate, TEV-53408. This anti-IL-15 monoclonal antibody is being developed for the treatment of adults with celiac disease who remain symptomatic despite following a gluten-free diet highlighting regulatory commitment to accelerating development of promising therapeutic candidates targeting immune pathways involved in gluten-induced intestinal damage.

- January 2025: Anokion SA, a clinical-stage biotechnology company dedicated to treating autoimmune diseases through the restoration of immune tolerance, has announced encouraging symptomatic data from its Phase 2 ACeD-it trial. This study evaluates the company’s lead candidate, KAN-101, in individuals with celiac disease.

- July 2024: Tampere University in Finland has unveiled promising clinical progress on ZED1227, a novel therapeutic candidate for celiac disease. Designed to be used in conjunction with a gluten-free diet, ZED1227 offers a potential new approach for managing symptoms and improving the quality of life for individuals affected by the condition. The emerging data suggests that ZED1227 could significantly enhance treatment outcomes by targeting the disease mechanism directly, rather than relying solely on dietary restrictions.

- February 2024: Beyond Celiac, a leading advocate for accelerating a cure for celiac disease, has announced the launch of Beyond Celiac Investments (BCI), a strategic investment initiative aimed at fast-tracking the development of treatments and ultimately a cure for the condition.

Global Celiac Disease Treatment Market Report Scope

People with celiac disease have a variety of nutritional concerns. Gluten, a protein naturally found in certain grains like wheat, barley, rye, and some oats, triggers an autoimmune response that causes inflammation and damages the small intestine's lining. This damage can lead to abnormal digestion and reduced nutrient absorption. There are two types of celiac disease: Type I (RCeDI), which might be driven by an extreme sensitivity to gluten traces, and Type II (RCeDII), which is a severe form associated with a higher risk of cancer. The main treatment is to opt for a gluten-free diet and treatment plans.

The celiac disease treatment market is segmented by product type, type, treatment type, distribution channel, and geography. By product type, the market is segmented into vitamin and mineral supplements, steroids, and immunosuppressive drugs. By type, the market is segmented into non-responsive celiac disease and refractory celiac disease. By treatment, the market is segmented into first line and second line. By distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, online pharmacy, and others, including home care settings and specialty clinics. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report also offers the market sizes and forecasts for 17 countries across the region. For each segment, the market sizing and forecasts were made on the basis of value (USD).

| Vitamin & Mineral Supplements |

| Steroids & Immuno-suppressive Drugs |

| Enzyme-based Therapies |

| Tight-Junction Modulators |

| Tolerance-Inducing Immunotherapies |

| Others |

| Classical CD |

| Non-Responsive CD |

| Refractory CD (Type I & II) |

| Asymptomatic / Silent CD |

| First Line |

| Second Line |

| Oral |

| Parenteral |

| Others |

| Hospital Pharmacy |

| Retail Pharmacy |

| Online Pharmacy |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Vitamin & Mineral Supplements | |

| Steroids & Immuno-suppressive Drugs | ||

| Enzyme-based Therapies | ||

| Tight-Junction Modulators | ||

| Tolerance-Inducing Immunotherapies | ||

| Others | ||

| By Disease Type | Classical CD | |

| Non-Responsive CD | ||

| Refractory CD (Type I & II) | ||

| Asymptomatic / Silent CD | ||

| By Line of Therapy | First Line | |

| Second Line | ||

| By Route of Administration | Oral | |

| Parenteral | ||

| Others | ||

| By Distribution Channel | Hospital Pharmacy | |

| Retail Pharmacy | ||

| Online Pharmacy | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the celiac disease treatment market?

The market is valued at USD 718.94 million in 2026 and is projected to reach USD 971.58 million by 2031.

Which drug class leads revenue today?

Vitamin & mineral supplements hold 58.96% of celiac disease treatment market share as of 2025.

What pipeline agent is closest to approval?

Enzyme therapy TAK-062 from Takeda is in Phase 3 and carries Fast-Track status, positioning it for early approval consideration.

Why is Asia-Pacific growing faster than other regions?

Rising wheat consumption, broader serology access, and pooled sero-prevalence reaching 1.2% in low-risk groups drive a 9.24% CAGR.

How does the absence of FDA-approved drugs affect investment?

Regulatory uncertainty inflates trial costs and lengthens timelines, but late-stage successes and Fast-Track designations are renewing investor confidence.

Will pharmaceutical therapy replace the gluten-free diet?

Current regulatory guidance supports adjunctive rather than replacement use, meaning drugs will complement but not eliminate dietary management.

Page last updated on: