Medical Protective Clothing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

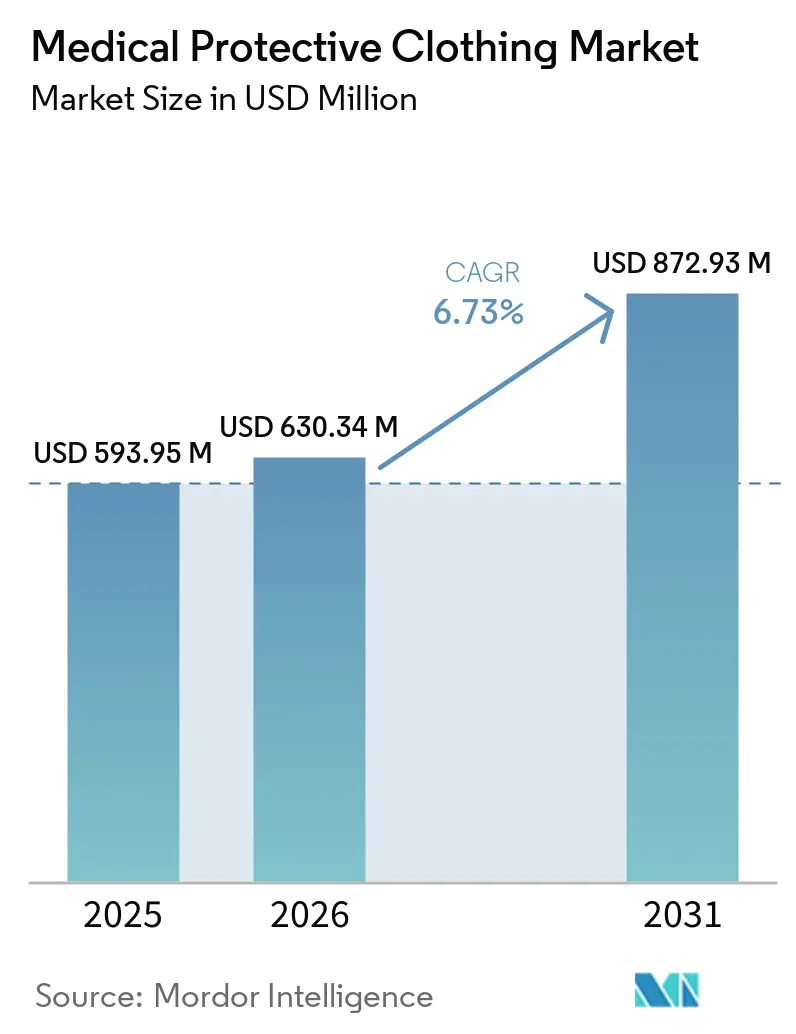

| Market Size (2026) | USD 630.34 Million |

| Market Size (2031) | USD 872.93 Million |

| Growth Rate (2026 - 2031) | 6.73% CAGR |

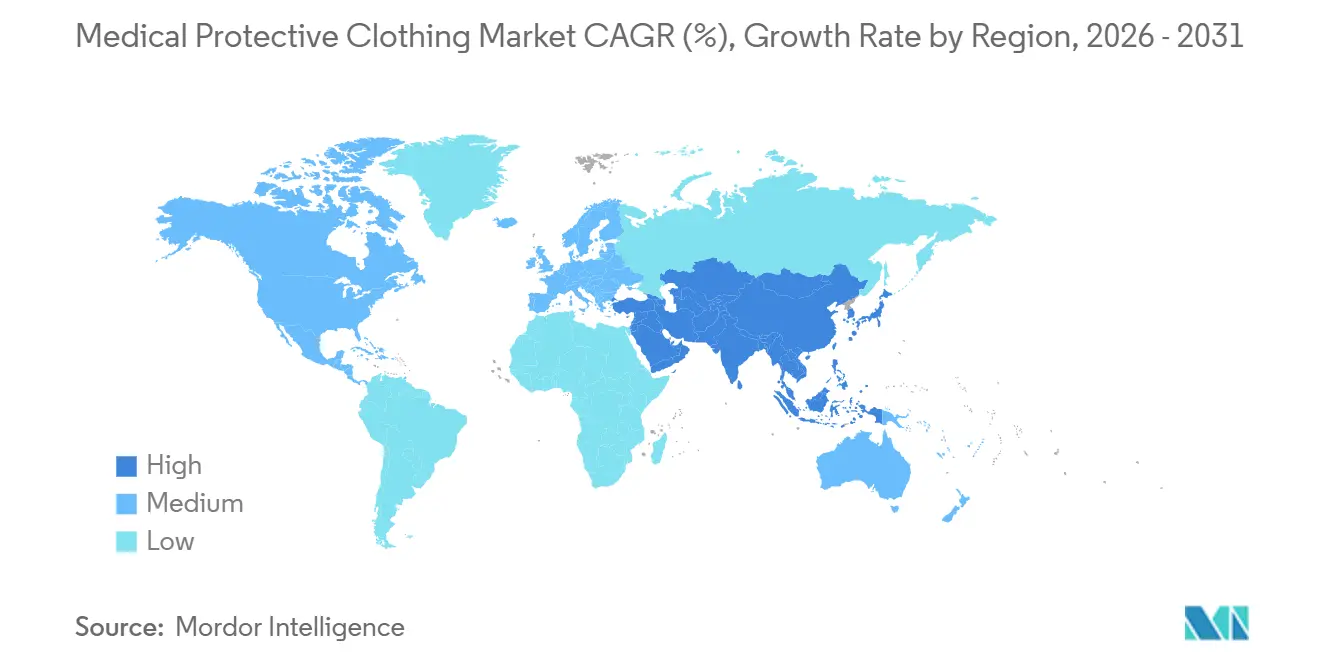

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

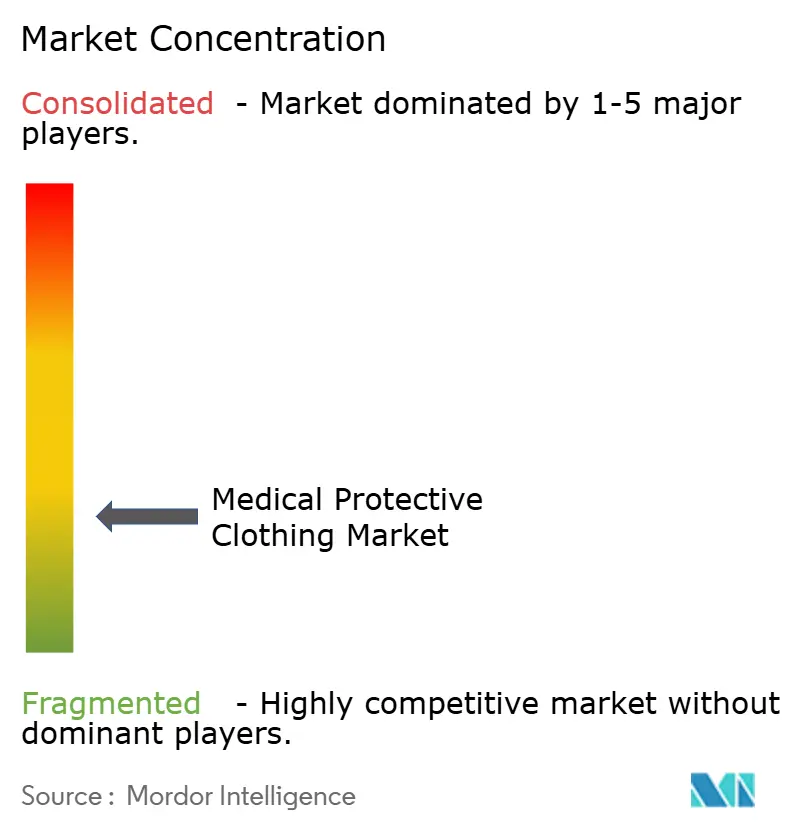

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Protective Clothing Market Analysis by Mordor Intelligence

The Medical Protective Clothing Market size is expected to grow from USD 593.95 million in 2025 to USD 630.34 million in 2026 and is forecast to reach USD 872.93 million by 2031 at 6.73% CAGR over 2026-2031.

The medical protective clothing market is now being supported by routine care delivery patterns rather than emergency stockpiling, with demand tied to surgery volumes, infection prevention rules, and tighter procurement discipline across health systems. Hospital-acquired infections remain a steady burden, and the CDC stated that 1 in 31 U.S. hospital patients had at least 1 healthcare-associated infection on any given day, which keeps barrier garments within essential clinical purchasing lists. Buyers are also placing more weight on product traceability, contract performance, and inventory rotation, which favors suppliers with certified portfolios and dependable supply programs. The medical protective clothing market is also seeing a broader mix of competition, with large institutional suppliers defending share through long-term relationships while digital brands and lower-cost certified manufacturers widen customer choice. Raw material swings and tighter textile waste rules are also shaping portfolio decisions, especially for suppliers balancing disposable volume with reusable programs and disposal compliance.

Key Report Takeaways

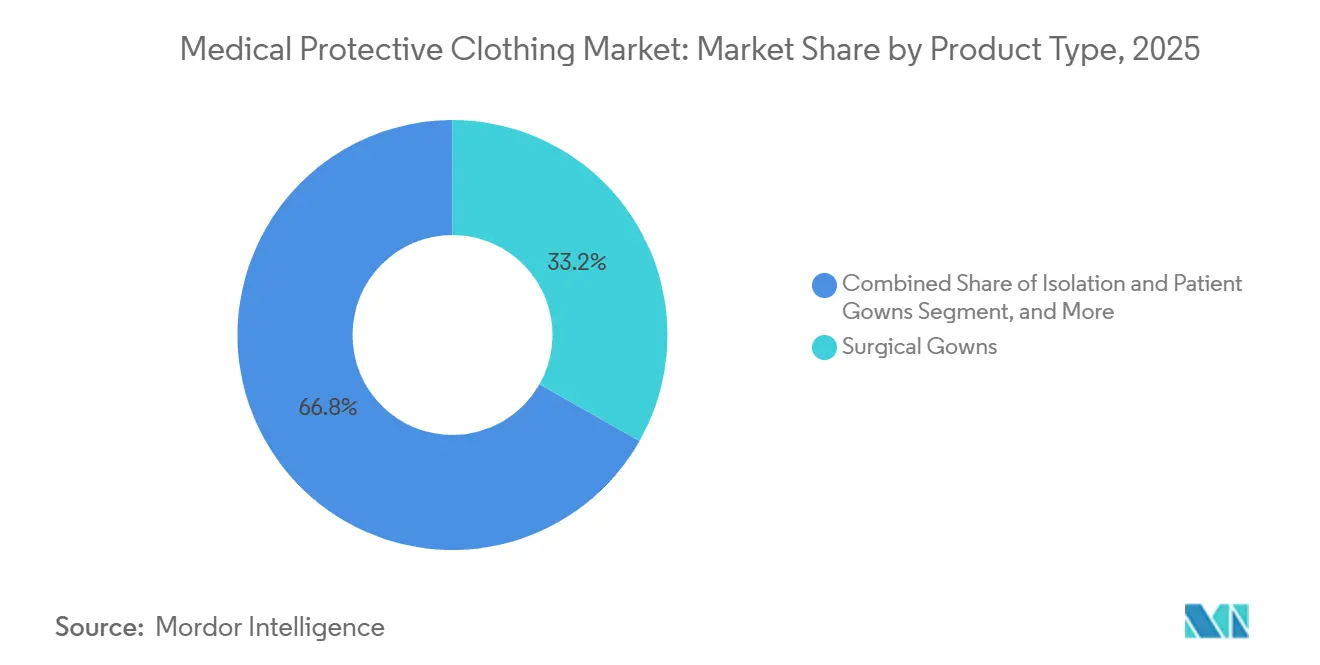

- By product type, surgical gowns led with 33.21% share in 2025, while compression and support garments are projected to record the highest CAGR at 7.14% through 2031.

- By usability, disposable formats held 72.83% share in 2025, while reusable products are forecast to grow fastest at 8.32% through 2031.

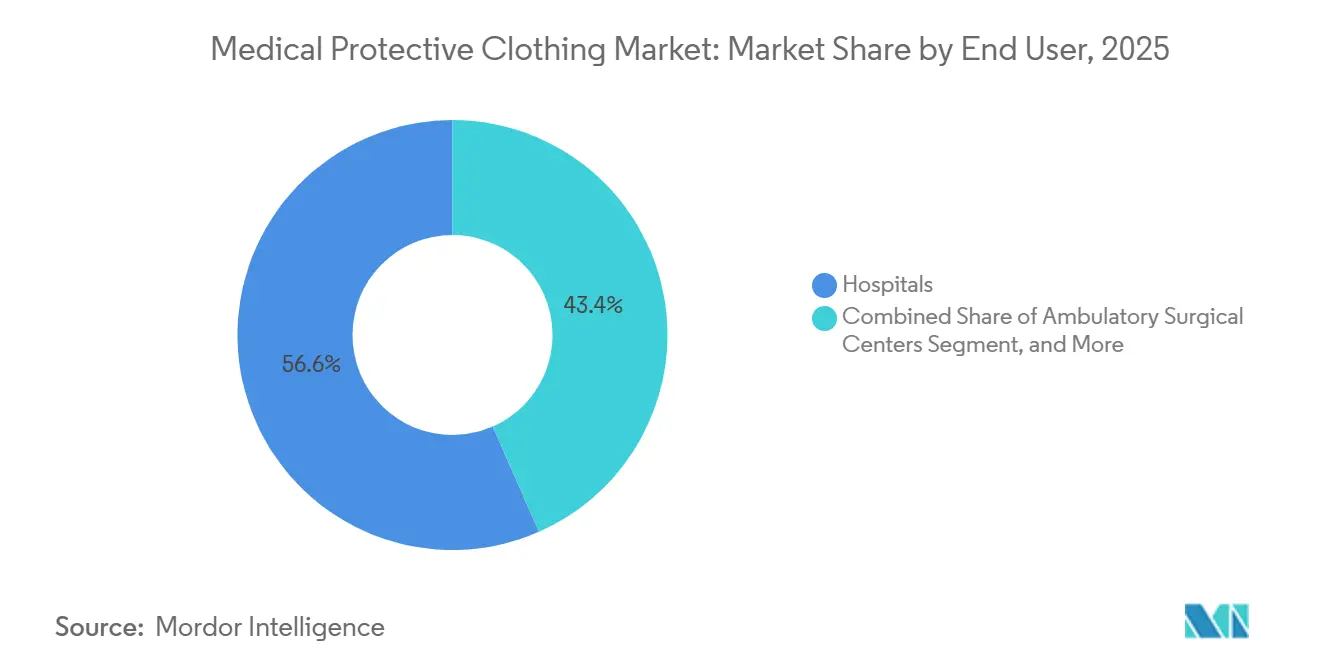

- By end user, hospitals accounted for 56.64% share in 2025, while home health and long-term care are expected to expand at the highest CAGR of 7.68% through 2031.

- By material, polypropylene SMS and SMMS represented 37.23% share in 2025, while antimicrobial-treated textiles are projected to grow fastest at 9.03% through 2031.

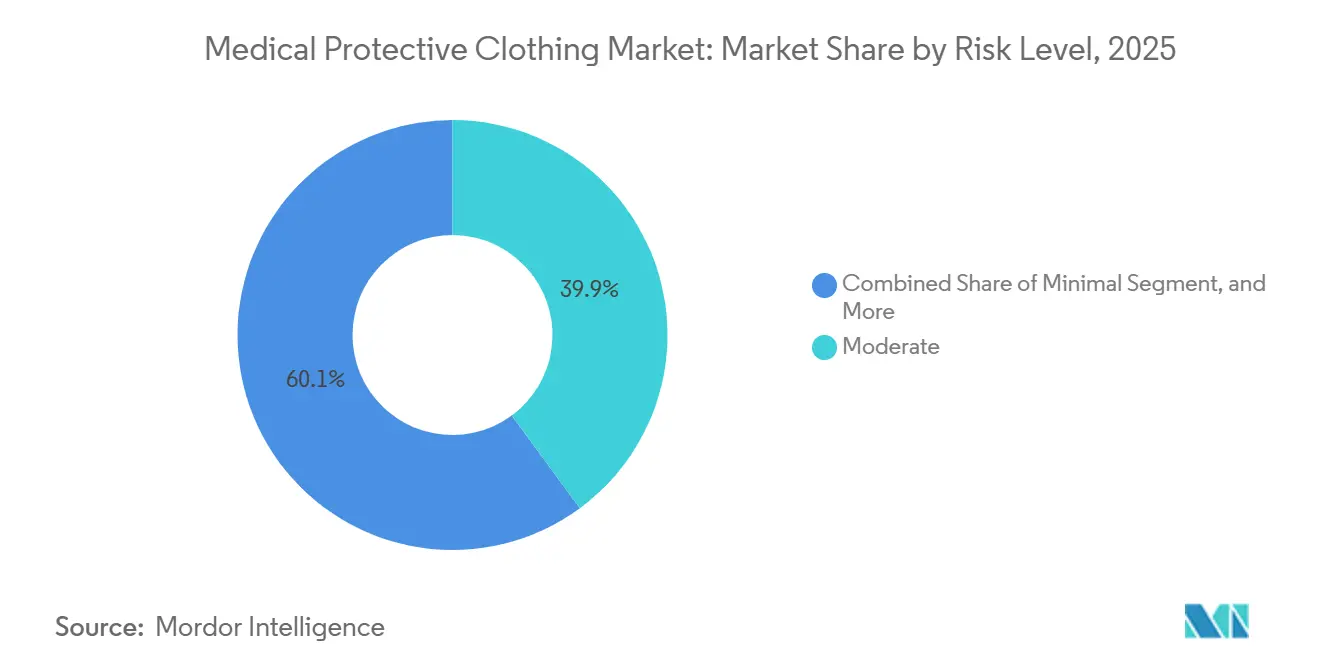

- By risk level, the moderate segment held 39.88% share in 2025, while the high segment is forecast to advance at the fastest CAGR of 7.04% through 2031.

- By distribution channel, direct institutional procurement captured 61.23% share in 2025, while e-commerce and B2B platforms are projected to grow fastest at 7.94% through 2031.

- By geography, North America held 38.41% share in 2025, while Asia-Pacific is expected to record the fastest CAGR at 6.87% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Medical Protective Clothing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Infection Control Protocols in Hospitals and Ambulatory Care | +2.1% | Global, with highest intensity in North America and Europe | Short term (≤ 2 years) |

| Expansion of Outpatient and Same-Day Surgical Volumes | +1.5% | North America and Europe leading, APAC accelerating | Medium term (2-4 years) |

| Demand for Fluid-Impervious and Antimicrobial Textile Structures | +1.3% | Global, concentrated in high-acuity hospital settings | Medium term (2-4 years) |

| Hospital Shift Toward B2B E-Procurement and Vendor-Managed Inventory | +0.5% | North America and Western Europe core, expanding to APAC | Short term (≤ 2 years) |

| Growth of Adaptive Garments for Geriatric and Bariatric Care | +0.7% | North America, Western Europe, and Japan | Long term (≥ 4 years) |

| Take-Back and Circular Textile Contracts in Large Health Systems | +0.4% | Europe and UK NHS system leading, with spillover to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Infection Control Protocols: Structural Gown Demand Below the Headline

Healthcare-associated infection exposure is not a temporary event for hospitals, and it continues to renew demand for gowns, scrubs, and other barrier apparel within the medical protective clothing market. The CDC stated that 1 in 31 hospital patients in the United States had at least 1 healthcare-associated infection on any given day, which keeps infection prevention at the center of routine purchasing decisions.[1]Centers for Disease Control and Prevention, “Healthcare-Associated Infections Reports and Data,” CDC, cdc.gov This pressure is reinforced by accreditation and operating standards that require documented protective clothing use in clinical settings. Ambulatory surgical centers are also absorbing more procedural work, and that keeps protective garment demand tied closely to procedure counts rather than only to bed capacity. Procurement teams in these settings often prefer standardized packs built around the needs of specific procedures, which shifts supplier competition away from simple unit pricing. The medical protective clothing market therefore benefits when suppliers can match barrier performance, regulatory fit, and dependable replenishment in the same offer.

Expansion of Outpatient and Same-Day Surgical Volumes: Demand Migration, Not Demand Growth

The shift toward outpatient and same-day care is changing where protective garments are purchased within the medical protective clothing market. Demand is moving from inpatient hospitals into ambulatory sites and specialty facilities that operate with different buying patterns and different inventory needs. These buyers often favor procedure-specific packs that bundle gowns, drapes, and accessories into a single orderable format, which can lower per-unit visibility but raise switching costs once a vendor is approved. Ansell reported that its cleanroom and surgical segment posted 2.8% organic constant currency growth in the first half of FY26, which aligns with steady volume expansion in controlled and procedure-heavy settings.[2]Ansell Limited, “FY26 Half Year Results,” Ansell Investor Relations, investor.ansell.com This setting rewards vendors that can combine credentialed products with reliable lead times and repeat ordering support. The medical protective clothing market is therefore gaining from care migration even when the total number of procedures does not rise at the same pace.

Demand for Fluid-Impervious and Antimicrobial Textile Structures: Beyond Barrier Performance

The medical protective clothing market is moving from basic barrier expectations toward fabrics that combine protection with active functional performance. Antimicrobial-treated textiles are projected to expand at a 9.03% CAGR through 2031, which shows that buyers are looking beyond simple fluid resistance. A 2025 paper in ACS Applied Materials & Interfaces stated that antimicrobial textiles can reduce microbial load on clinical surfaces, which supports their use within infection control strategies.[3]National Center for Biotechnology Information, “Advancements in Antimicrobial Textiles Fabrication, Mechanisms of Action, and Applications,” PMC, pmc.ncbi.nlm.nih.gov This shift also raises the cost of participation because antimicrobial claims require testing, revalidation, and documented performance. Larger suppliers are better placed to absorb those recurring costs, which makes premium tiers harder for small entrants to contest. The medical protective clothing market is therefore rewarding suppliers that can prove performance consistency and not only barrier compliance.

Growth of Adaptive Garments for Geriatric and Bariatric Care: The Underwritten Demographic Dividend

The medical protective clothing market is also being supported by rising demand for garments designed around post-surgical recovery and mobility-related care needs. Compression and support garments are expected to grow at 7.14% through 2031, which reflects broader use in bariatric, orthopedic, vascular, and recovery pathways. The United Nations stated that the global population aged 60 and above is expected to exceed 1.4 billion by 2030, which keeps age-related care demand on a firm upward path. Germany reported that 21.5% of its population was aged 65 and above in 2025, and Japan reported that seniors accounted for 28% of the population, which helps explain the strong pull for adaptive and support garments in mature care systems. These garments are used in settings that extend beyond the operating room, which widens the addressable demand base for suppliers. The medical protective clothing market therefore benefits from demographic expansion in a way that supports recurring replacement demand rather than one-time emergency buying.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Polypropylene and Cotton Price Volatility | -0.8% | Global, with the APAC manufacturing base most exposed | Medium term (2-4 years) |

| Disposal Compliance and Medical Textile Waste Scrutiny | -0.4% | Europe leading, with North America and APAC following | Medium term (2-4 years) |

| High Certification and Validation Cost for SME Entrants | -0.3% | Global, particularly acute in Asia-Pacific and South America | Long term (≥ 4 years) |

| Counterfeit and Non-Compliant PPE Diluting Buyer Confidence | -0.2% | Global, concentrated supply chain risk from non-certified suppliers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Polypropylene and Cotton Price Volatility: Margin Compression at the Manufacturing Layer

The medical protective clothing market remains exposed to input swings because polypropylene and cotton still anchor a large share of current product formats. Polypropylene is tied to petrochemical cost movements, and that creates earnings pressure for suppliers that depend heavily on disposable nonwoven output. The problem is sharper in fixed-price institutional contracts because manufacturers often cannot pass cost increases through until the next tender cycle. Cotton exposure adds a second layer of uncertainty for reusable lines that rely on wash durability, wearer comfort, and fiber availability. This cost pressure favors suppliers with broader portfolios because they can balance disposable demand with reusable products and mixed-material offerings. The medical protective clothing market therefore rewards manufacturers that manage procurement risk and material mix with more discipline than smaller single-format competitors.

Disposal Compliance and Medical Textile Waste Scrutiny: A Regulatory Gray Zone Narrowing

Waste regulation is becoming a more visible drag on the medical protective clothing market, especially for suppliers with large single-use portfolios. The European Commission stated that the revised Waste Framework Directive entered into force in October 2025 and introduced extended producer responsibility requirements for textiles across member states. EURATEX and EuroCommerce both called for explicit exclusion of PPE and medical device products from textile EPR scope in late 2025, warning that contaminated medical items should not be treated like household textile waste. This uncertainty complicates procurement planning because disposal costs and responsibilities may change during long product lifecycles. It also softens the case for expanding single-use ranges without a linked take-back or certified disposal solution. The medical protective clothing market is therefore seeing regulation influence not only product design, but also contract structure and end-of-life service expectations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Surgical Gowns Lead, But Compression Apparel Disrupts

Surgical gowns held 33.21% of the medical protective clothing market share in 2025, and that position reflected their required use in sterile operating environments and their direct link to infection control practice. Demand remained concentrated in hospitals and procedure-heavy settings where regulatory compliance and barrier performance are closely monitored. Medline stated that its surgical gowns were used in over 40% of U.S. operating rooms and supported more than 20 million procedures annually, which shows how deep supplier relationships can reinforce incumbent positions in this category. Isolation and patient gowns served broader ward, diagnostic, and outpatient use cases where volumes were high but unit value was lower. Protective coveralls and hazmat suits remained more specialized and were tied to chemical, biological, and controlled high-risk environments.

Compression and support garments are projected to grow at 7.14% through 2031, which makes them the fastest-growing product category in the medical protective clothing market. Their expansion is being supported by standardized recovery protocols for bariatric, orthopedic, and vascular patients across hospitals and longer-term care settings. Lab coats remained stable because diagnostic and academic use patterns were consistent and replacement needs were routine. Caps, masks, and shoe covers continued to move through volume-led procurement channels where pricing power was limited. Cleanroom apparel stayed smaller in volume, but it carried higher unit values because pharmaceutical and biopharma production sites require stricter particle control, and Ansell reported 2.8% organic constant currency growth in its cleanroom segment in FY26 H1.

By Usability: Disposable Dominates, but Reusable Growth Signals a Structural Inflection

Disposable products accounted for 72.83% of the usability segment in 2025, which reflected the appeal of simplified infection control workflows and the absence of laundering requirements. Smaller facilities especially favored disposable formats because they did not need to manage sterilization capacity, textile tracking, or outsourced reprocessing contracts. Reusable formats still gained more attention because procurement teams were reassessing total lifecycle cost instead of looking only at first-purchase price. NHS Health Innovation Northwest Cumbria reported in 2024 that reusable surgical gowns had 31% of the carbon footprint of comparable single-use gowns and delivered 45% cost savings per use, which strengthened the business case for institutional adoption. A 2024 BMJ analysis also stated that large U.S. medical centers using reusable PPE programs diverted substantial landfill waste while achieving nearly 50% per-gown cost savings with no measurable impact on infection rates.

Reusable products are projected to expand at an 8.32% CAGR through 2031, which makes them the fastest-growing usability option in the medical protective clothing market. The main barrier is not clinical acceptability, but operational readiness, because facilities need validated processing arrangements before they can scale reuse programs. ISO stated in 2025 that ISO/AWI 25199 was under development to provide guidelines for processing multiple-use healthcare textiles, which could reduce uncertainty for procurement teams reviewing reusable programs. A 2025 study of peri-operative professionals across 134 countries found that misconceptions about the protective performance of reusable gowns remained a major adoption barrier, which shows that education still matters alongside infrastructure. The medical protective clothing market is therefore not moving away from disposables all at once, but it is clearly opening more room for validated reusable pathways.

By End User: Hospitals Hold More Than Half, but Home Health Rewrites the Growth Map

Hospitals commanded 56.64% of the end-user segment in 2025, which reflected their role as the highest-volume buyers of surgical, isolation, and procedure-linked apparel. Large acute care sites usually run structured procurement systems, infection control reviews, and preferred supplier contracts, which keep institutional purchasing concentrated. Their demand also spans more product categories than any other setting, from sterile gowns and patient apparel to specialized high-risk garments. Ambulatory surgical centers remained the mid-tier growth setting because procedure volumes continued to shift toward outpatient formats. Diagnostic and imaging labs, dental clinics, veterinary clinics, and research institutions all contributed to a smaller but steady demand with different fit, barrier, and replacement needs.

Home health and long-term care are projected to grow at a 7.68% CAGR through 2031, which makes them the fastest-growing end-user group in the medical protective clothing market. This pattern reflects aging populations, more care delivered outside hospitals, and a broader need for garments that are easy for caregivers to use in lower-acuity settings. The Alzheimer’s Association continued to highlight the rising care burden linked to aging and cognitive decline in its 2025 facts and figures report, which supports the shift toward distributed care delivery and caregiver support demand. That shift creates demand for ergonomic, easy-donning protective apparel that differs from products designed for high-throughput hospital departments. The medical protective clothing industry, therefore, has room to grow beyond traditional hospital procurement, especially where suppliers tailor products and channel strategy to home-based and long-term care use.

By Material: Polypropylene Dominant, Antimicrobial Leads Growth

Polypropylene SMS and SMMS materials accounted for 37.23% share in 2025, and that led to their cost efficiency, fluid repellency, and large-scale manufacturing base. These materials remain central to disposable surgical and isolation gown production because hospitals value familiar performance and dependable supply availability. Cotton continued to hold relevance in reusable scrubs and adaptive patient garments where comfort, washability, and extended wear matter more than single-use sterility. Polyester and blended fabrics served the middle of the product range in scrubs and lab coats, while polyethylene addressed lower-cost isolation use. Aramid and other high-performance blends remained niche, but they carried higher value in chemical and biohazard applications where specialized resistance is required.

Antimicrobial-treated textiles are forecast to advance at a 9.03% CAGR through 2031, which makes them the fastest-growing material category in the medical protective clothing market. A 2025 study in ACS Applied Materials & Interfaces reported that antimicrobial textiles can reduce pathogen load on clinical surfaces, which supports their role as an active layer within infection control programs. This gives hospitals a reason to treat antimicrobial specification as part of performance-based buying rather than as an optional premium feature. Smart and sensor-integrated textiles remained early-stage, but they still held strategic value because garment tracking and data-linked inventory control are becoming more relevant in healthcare operations. Lenzing introduced a three-tier cellulosic fiber portfolio for protective wear in April 2025, including TENCEL lyocell and LENZING FR fibers with EU Ecolabel certification, which showed that sustainable bio-based inputs are moving closer to mainstream product development.

By Risk Level: Moderate Anchors the Core, High Follows Procedure Complexity

The moderate risk level segment held 39.88% of the medical protective clothing market size in 2025, which reflected its broad use across wards, outpatient procedures, and standard clinical interactions. These use cases commonly align with AAMI PB70 Level 2 and Level 3 garments, which balance protection and wearer comfort for routine procedural care. Moderate risk demand therefore forms the core volume base for many suppliers because it spans more departments than the high-risk tier. The high-risk segment remained smaller in absolute terms, but it was tied to more complex procedures and stricter barrier expectations. As lower-acuity work shifts into ambulatory settings, the procedures that remain in hospital operating rooms are increasingly concentrated in cardiovascular, orthopedic, transplant, and oncology care.

The high-risk segment is projected to grow at a 7.04% CAGR through 2031, which makes it the fastest-growing risk tier in the medical protective clothing market. This growth is drawing more focused product development because buyers want better comfort without lowering viral and fluid barrier protection. The FDA granted 510(k) clearance to Medline’s Level 4 Surgical Gown with Breathable Sleeves in February 2025, which showed how suppliers are trying to improve wearability inside maximum-barrier products. Minimal and low-risk tiers still served large user populations, but their growth remained more volume-based and less differentiated. The stronger margin opportunity therefore sits with suppliers that can prove performance consistency and user comfort in high-barrier products rather than compete only on commodity pricing.

By Distribution Channel: Direct Procurement Is the Core, E-Commerce Rewrites the Edge

Direct institutional procurement accounted for 61.23% of distribution share in 2025, which showed that large hospitals still prefer contract-based purchasing with known vendors and predictable supply terms. This channel fits group purchasing structures, preferred supplier programs, and long planning cycles for clinical inventory. It also benefits companies that can serve multiple product categories under a single relationship because hospitals value accountability and continuity. Distributors and wholesalers remained important for mid-sized facilities and specialty clinics that lacked the scale to negotiate directly with major vendors. Retail channels continued to serve individual practitioners and small-volume buyers, but they were less central to total category value.

E-commerce and B2B platforms are projected to grow at a 7.94% CAGR through 2031, which makes them the fastest-growing route within the medical protective clothing market. FIGS reported that its active customer count surpassed 3 million in Q1 2026 and that revenue rose 28% year over year to USD 159.9 million, which showed strong digital demand from healthcare professionals and expanding international reach. Digital ordering is also becoming more relevant in institutional settings where cloud-based procurement, reorder visibility, and inventory monitoring can reduce friction. That blurs the line between traditional direct sales and online procurement because the same supplier may serve both individual professionals and organizations through digital tools. The medical protective clothing market is therefore becoming more channel-diverse, even though institutional contracts still anchor the revenue base.

Geography Analysis

North America held 38.41% of the medical protective clothing market share in 2025, which made it the largest regional contributor. The region’s position rested on high healthcare spending, mature procurement systems, and established gown classification standards tied to ANSI/AAMI PB70 and FDA regulatory pathways. The United States remained the largest country-level market in the region because it concentrated procedure volumes, hospital purchasing power, and formal product credentialing. Canada and Mexico contributed smaller but stable volumes, with demand supported by hospital modernization and steady outpatient expansion. CDC infection control guidance continued to reinforce procedural use of protective apparel across the care system, which supported consistent replacement demand.

Europe remained the second-largest regional block in the medical protective clothing market, with Germany, the United Kingdom, France, and Italy as the main demand centers. Germany benefited from high healthcare spending and an older population, and Destatis reported that 21.5% of the population was aged 65 and above in 2025. The United Kingdom continued to stand out in reusable gown adoption, and NHS Health Innovation Northwest Cumbria documented 45% per-gown cost savings and a 69% carbon footprint reduction versus disposables in 2024. The revised Waste Framework Directive also introduced a new layer of uncertainty for textile producers in Europe, which kept disposal responsibility and product classification under closer review.

Asia-Pacific is projected to expand at a 6.87% CAGR through 2031, which makes it the fastest-growing geography in the medical protective clothing market. China remained the largest manufacturing and demand center within the region, while India continued to expand tertiary care capacity and tighten standards for medical textiles. Japan added a strong demand base through its aging population, and the Statistics Bureau of Japan reported that seniors accounted for 28% of the population in 2024. South Korea supported regional demand through advanced healthcare technology use and a high-quality care environment. South America remained a developing regional opportunity led by Brazil and Argentina, where procurement is becoming more structured after the pandemic period. Middle East and Africa demand was led by GCC healthcare infrastructure investment, while South Africa acted as an anchor market for Sub-Saharan procurement patterns.

Competitive Landscape

The medical protective clothing market remains moderately fragmented, with a visible group of multinational suppliers at the institutional end and a wider field of regional and specialized competitors across commodity and niche lines. The competitive strength is most visible in products where hospitals place high value on approval status, supply continuity, and category depth. Medline’s surgical gown presence in more than 40% of U.S. operating rooms illustrated how procedural integration can reinforce incumbency over time. Competition is still active, but the top tier has clear advantages in tender participation, contract execution, and multi-site account management.

Strategic moves in 2025 and 2026 showed that leading companies were trying to protect margins while investing in faster-growing pockets of demand within the medical protective clothing market. Ansell stated in its 2025 annual report that its Accelerated Productivity Investment Program delivered USD 50 million in savings, which showed a strong focus on cost recovery and operating discipline. Ansell also reported investment in a greenfield surgical facility in India in FY26 H1, which linked lower-cost production to Asia-Pacific demand expansion. Medline added product-focused differentiation through its FDA-cleared Level 4 surgical gown with breathable sleeves and its ComfortTemp patient warming system, which showed continued investment in adjacent hospital apparel solutions. Honeywell completed the sale of its PPE business to Protective Industrial Products in May 2025, which reflected continued portfolio reshaping across the broader protective equipment space.

The next layer of competition is coming from direct-to-professional brands, digital procurement models, and Asian manufacturers that have secured recognized quality certifications. FIGS remained the clearest example of digital brand strength, with full-year 2025 revenue of USD 631.1 million and international revenue growth of 27.5%, which showed that premium scrubwear can scale beyond the pandemic period. White-space opportunities remained strongest in antimicrobial products, RFID-linked garment management, and procedure-specific kit bundles that large incumbents have not fully standardized across all care settings. Mid-tier distributors faced the greatest pressure because many lacked both the digital tools to defend share online and the scale to match institutional pricing. The medical protective clothing market therefore favors suppliers that can combine compliance, manufacturing depth, channel flexibility, and data-backed service in one operating model.

Medical Protective Clothing Industry Leaders

Medline Industries, LP

3M

Cardinal Health, Inc.

Smith and Nephew plc

STERIS plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Ansell Limited reported FY26 first-half results; its Surgical segment grew 7.2% on an adjusted basis driven by synthetic product demand, while the Cleanroom segment advanced 2.8% in organic constant currency terms; the company is investing in a greenfield surgical facility in India through capital expenditure that included reverse osmosis water recycling capability, targeting APAC production scale.

- January 2026: Medline Industries issued a Field Safety Notice (ICN 3221) to NHS Supply Chain for sterile surgical drapes and gowns after discovering a supplier failed to adequately document calibrations for sealing equipment and sterilization-related sensors, placing sterility assurance at risk; NHS Supply Chain managed alternative supplier sourcing across 27 product codes.

- October 2025: The EU Waste Framework Directive revision entered into force, introducing mandatory EPR schemes for textiles across Member States; EURATEX and EuroCommerce separately petitioned the European Commission for explicit exclusion of products compliant with EU PPE Regulation (EU 2016/425) and EU MDR (EU 2017/745) from textile EPR scope, citing cross-contamination risk in household waste streams.

- July 2025: Medline launched the ComfortTemp Patient Warming System, a FDA 510(k) Class 2 medical device incorporating disposable patient warming blankets and gowns with an innovative lock-in hose mechanism, targeting perioperative temperature management and SKU consolidation in hospital procurement.

Global Medical Protective Clothing Market Report Scope

Medical protective clothing refers to specialized garments and personal protective equipment (PPE) designed to safeguard healthcare professionals, patients, and visitors from infectious agents, bodily fluids, and contamination. It includes surgical gowns, disposable coveralls, scrubs, and masks essential for infection control.

The Medical Protective Clothing Market is segmented by product type, usability, end user, material, risk level, distribution channel, and geography. By product type, the market includes Medical Scrubs, Surgical Gowns, Isolation and Patient Gowns, Protective Coveralls and Hazmat Suits, Lab Coats, Caps, Masks and Shoe Covers, Compression and Support Garments, Adaptive and Patient Clothing, and Cleanroom Apparel. By usability, products are classified as Disposable or Reusable. By end user, adoption spans Hospitals, Ambulatory Surgical Centers, Out-Patient Clinics, Diagnostic and Imaging Labs, Home Health and Long-Term Care, Dental and Veterinary Clinics, and Research and Academic Institutes. By material, the market covers Cotton, Polyester and Blends, Polypropylene (SMS and SMMS), Polyethylene, Aramid and High-Performance Blends, Antimicrobial-Treated Textiles, and Smart and Sensor-Integrated Textiles. By risk level, protective clothing is categorized as Minimal, Low, Moderate, or High. By distribution channel, products reach end users through Direct Institutional Procurement, Distributors and Wholesalers, Retail Stores, and E-Commerce and B2B Platforms.

| Medical Scrubs |

| Surgical Gowns |

| Isolation and Patient Gowns |

| Protective Coveralls and Hazmat Suits |

| Lab Coats |

| Caps, Masks and Shoe Covers |

| Compression and Support Garments |

| Adaptive and Patient Clothing |

| Cleanroom Apparel |

| Disposable |

| Reusable |

| Hospitals |

| Ambulatory Surgical Centers |

| Out-Patient Clinics |

| Diagnostic and Imaging Labs |

| Home Health and Long-Term Care |

| Dental and Veterinary Clinics |

| Research and Academic Institutes |

| Cotton |

| Polyester and Blends |

| Polypropylene (SMS and SMMS) |

| Polyethylene |

| Aramid and High-Performance Blends |

| Antimicrobial-Treated Textiles |

| Smart and Sensor-Integrated Textiles |

| Minimal |

| Low |

| Moderate |

| High |

| Direct Institutional Procurement |

| Distributors and Wholesalers |

| Retail Stores |

| E-Commerce and B2B Platforms |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Medical Scrubs | |

| Surgical Gowns | ||

| Isolation and Patient Gowns | ||

| Protective Coveralls and Hazmat Suits | ||

| Lab Coats | ||

| Caps, Masks and Shoe Covers | ||

| Compression and Support Garments | ||

| Adaptive and Patient Clothing | ||

| Cleanroom Apparel | ||

| By Usability | Disposable | |

| Reusable | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Out-Patient Clinics | ||

| Diagnostic and Imaging Labs | ||

| Home Health and Long-Term Care | ||

| Dental and Veterinary Clinics | ||

| Research and Academic Institutes | ||

| By Material | Cotton | |

| Polyester and Blends | ||

| Polypropylene (SMS and SMMS) | ||

| Polyethylene | ||

| Aramid and High-Performance Blends | ||

| Antimicrobial-Treated Textiles | ||

| Smart and Sensor-Integrated Textiles | ||

| By Risk Level | Minimal | |

| Low | ||

| Moderate | ||

| High | ||

| By Distribution Channel | Direct Institutional Procurement | |

| Distributors and Wholesalers | ||

| Retail Stores | ||

| E-Commerce and B2B Platforms | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2031 outlook for medical protective clothing?

The medical protective clothing market is expected to reach USD 872.93 million by 2031 from USD 630.34 million in 2026, growing at a 6.73% CAGR through the forecast period.

Which product category leads current demand for medical protective clothing?

Surgical gowns led with 33.21% share in 2025 because they remain essential in sterile operating environments and tightly regulated clinical workflows.

Which product area is growing fastest through 2031?

Compression and support garments are projected to grow fastest at 7.14% CAGR, supported by recovery protocols tied to bariatric, orthopedic, and vascular care.

Why are reusable gowns gaining attention in hospitals?

Reusable products are forecast to grow at 8.32% CAGR because hospitals are weighing lifecycle cost and waste reduction more carefully, with NHS data showing strong savings and a lower carbon footprint.

Which region currently leads demand for medical protective clothing?

North America led with 38.41% share in 2025 due to mature procurement systems, strong regulatory frameworks, and high healthcare spending.

Which sales channel is changing fastest for protective apparel suppliers?

E-commerce and B2B platforms are projected to grow at 7.94% CAGR through 2031 as healthcare professionals and institutions adopt more digital ordering and inventory workflows.

Page last updated on: