Medical Gloves Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 15.01 Billion |

| Market Size (2031) | USD 25.36 Billion |

| Growth Rate (2026 - 2031) | 11.05% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Gloves Market Analysis by Mordor Intelligence

The Medical Gloves Market size was valued at USD 13.52 billion in 2025 and is estimated to grow from USD 15.01 billion in 2026 to reach USD 25.36 billion by 2031, at a CAGR of 11.05% during the forecast period (2026-2031).

That scale already places the Medical Gloves industry among the largest categories of single-use healthcare supplies, underscoring the indispensable role gloves play in every patient interaction. Demand is propelled by hospital accreditation rules that require gloves for even brief touchpoints, so revenue growth implicitly signals rising patient encounters as health systems clear surgical backlogs. A notable inference is that procurement teams are shifting toward multi-year contracts to lock in volume and pricing, an approach that was rare before the pandemic. This contracting trend increases visibility for manufacturers, encouraging capacity additions even in the face of raw-material price volatility.

The Medical Gloves market size outlook also reflects structural supply drivers. Nearly three-quarters of global output is located in Malaysia and Thailand, where manufacturers rely on automated dipping lines to hold down unit costs. Importers are diversifying sourcing portfolios in response to new United States tariffs on Chinese gloves and freight bottlenecks, a shift that reallocates Medical Gloves market share toward Southeast Asian suppliers. A fresh inference from distributor negotiations is that environmental, social and governance criteria now account for up to one-fifth of tender scores, effectively turning sustainability into a prerequisite for high-value bids. This new weighting pushes glove makers to invest simultaneously in volume expansion and greener chemistries, raising capital-spending requirements across the Medical Gloves industry.

Key Report Takeaways

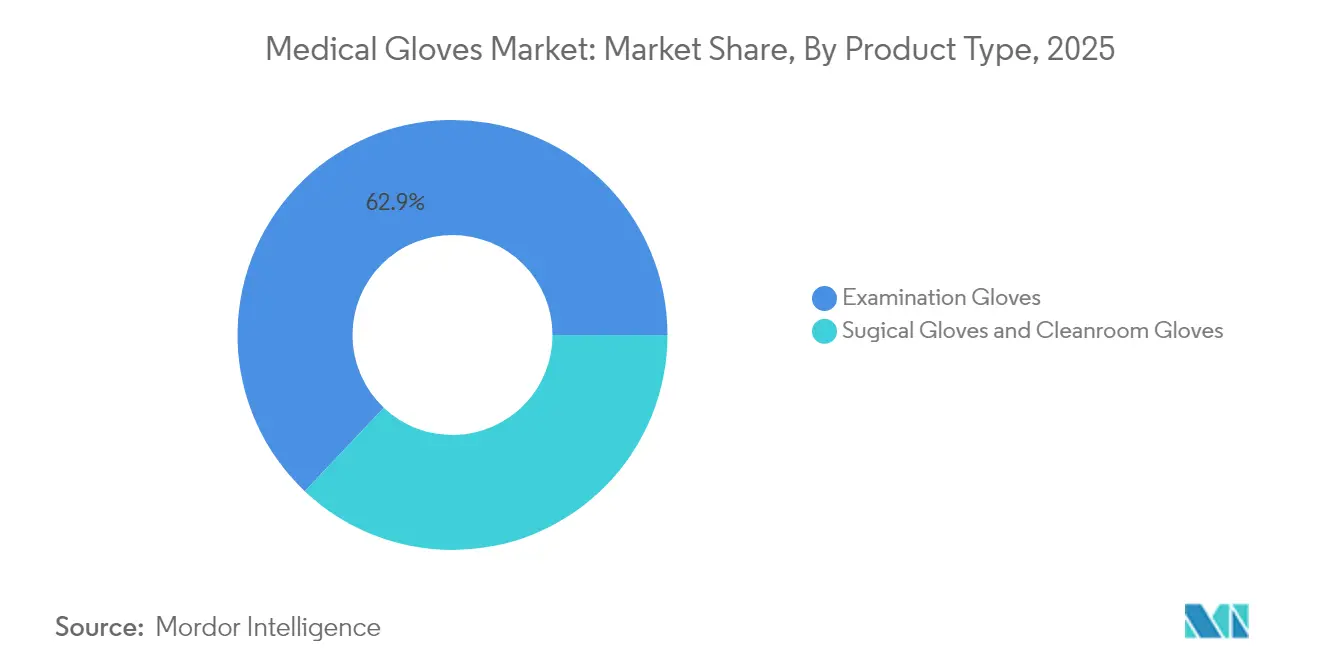

- By product type, examination gloves led with a 62.94% revenue share in 2025, while cleanroom gloves are projected to expand at a 11.92% CAGR through 2031.

- By material type, nitrile gloves held a 47.82% share in 2025, while neoprene gloves are forecast to grow at a 12.22% CAGR through 2031.

- By sterility, non-sterile gloves accounted for 71.64% of the medical gloves market share in 2025, while sterile gloves are projected to record a 12.68% CAGR from 2026 to 2031.

- By end user, hospitals and clinics held a 47.18% share in 2025, while ambulatory surgical centers are forecast to grow at a 12.55% CAGR through 2031.

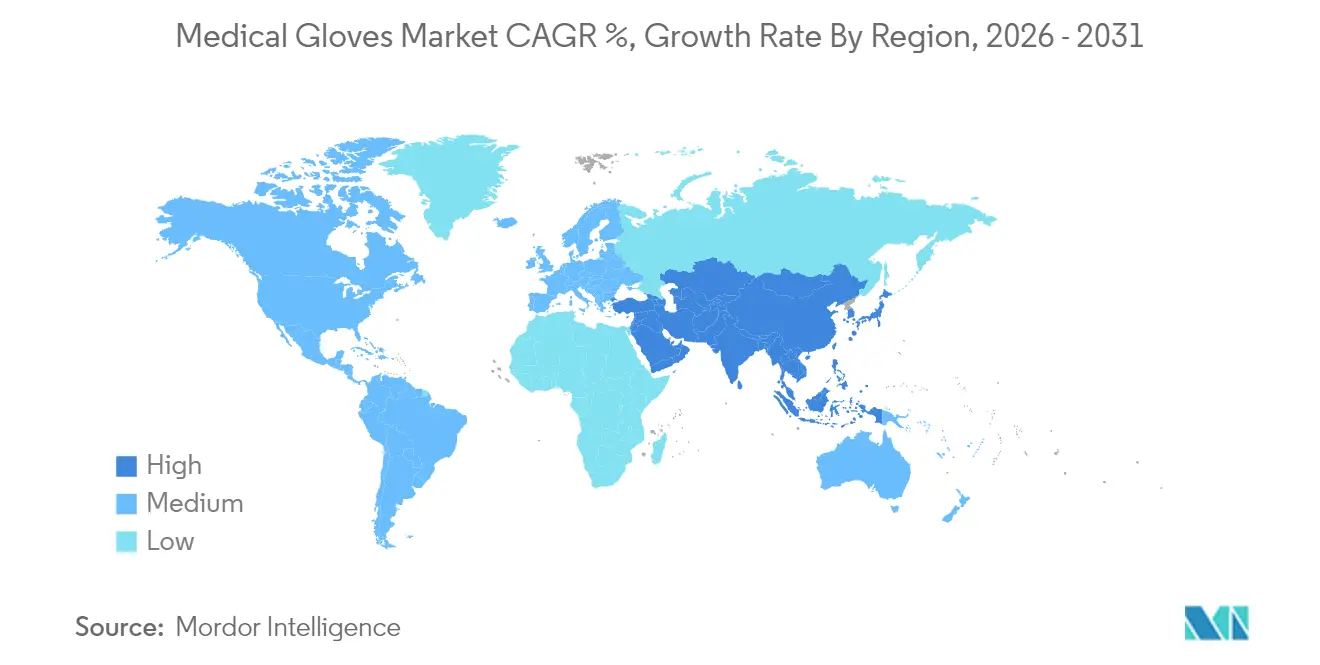

- By geography, North America retained a 34.45% share in 2025, while Asia-Pacific is anticipated to grow at a 13.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Gloves Market Trends and Insights

Drivers Impact Analysis*

| Driver | ~% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global Emphasis on Preventing Hospital-Acquired Infections | ~2.5% | United States, Germany, United Kingdom, France, Canada, Australia | Short term (≤ 2 yrs) |

| Rebound in Elective & Non-Urgent Surgical Procedures Post-Pandemic | ~2.8% | United States, Canada, Germany, United Kingdom, France, Italy, Japan | Short term (≤ 2 yrs) |

| Expansion of Cleanroom Manufacturing Across Semiconductor & Pharma Industries | ~1.8% | China, India, South Korea, United States, Germany, Japan, Malaysia, Thailand | Medium term (~ 2-4 yrs) |

| Broader Adoption of Universal Health Coverage in Emerging Economies | ~2.2% | India, China, Brazil, Argentina, South Africa, GCC Countries, Mexico | Medium term (~ 2-4 yrs) |

| Rapid Growth of Home-Based Point-of-Care Diagnostics | ~1.4% | United States, Canada, Germany, United Kingdom, Japan, Australia, China, India | Long term (≥ 5 yrs) |

| Government Incentives Catalyzing New Glove Manufacturing Capacity | ~0.9% | Malaysia, Thailand, United States, China, India | Short term (≤ 2 yrs) |

| Source: Mordor Intelligence | |||

Global Emphasis on Preventing Hospital-Acquired Infections

Hospitals are tightening glove protocols after the Centers for Disease Control and Prevention confirmed that one in 31 in-patients acquires at least one infection each day[1]Centers for Disease Control and Prevention. “HAIs: Reports and Data.” Nov 25 2024. www.cdc.gov. Facilities are moving from simple availability of gloves to procedure-specific selection, which favors indicator products for high-risk surgeries. A 2024 systematic review showing an 80 % drop in inner-glove perforations with double gloving has accelerated uptake of these premium variants. The new focus creates an insight that infection-control committees now analyse glove-use data in electronic dashboards alongside hand-hygiene metrics, embedding glove adherence into daily clinical reporting.

Rebound in Elective and Non-Urgent Surgical Procedures Post-Pandemic

Top Glove reported a 104 % year-on-year jump in sales volume for Q1 FY2025 as hospitals attack procedure backlogs [2]Top Glove Corporation Bhd. “A New Chapter for Top Glove: Profitability Surges with Stronger Growth in Sight.” Jan 27 2025. . Orthopedic and cardiovascular cases are rising fastest, each demanding gloves with fine tactile response and high puncture resistance. Surgeons adopting minimally invasive techniques now specify ultra-thin nitrile or polyisoprene layers to improve grip on delicate instruments. A practical inference is that the higher glove consumption per complex case is offsetting slowing growth in routine examinations, keeping overall unit demand on a strong upward slope.

Expansion of Cleanroom Manufacturing Across Semiconductor and Pharma Industries

Cleanroom gloves, projected to expand at 12.10 % CAGR through 2030, benefit from converging particulate standards in semiconductor fabs and pharmaceutical fill-finish suites. Halyard Health’s PUREZERO line, certified for ISO Class 3, illustrates how accelerator-free nitrile appeals to operators wary of dermatitis. Cross-industry demand allows producers to run longer, more efficient production batches, narrowing cost differences with high-volume examination gloves. An inference is that semiconductor investment cycles indirectly stabilize medical glove revenue, offering a hedge against fluctuations in healthcare procedure volumes.

Broader Adoption of Universal Health Coverage in Emerging Economies

Implementation of universal health coverage in populous nations is lifting examination glove volumes faster than global supply can grow. MARGMA expects a shortage of 80 billion pieces in 2024 even as members invest USD 706 million (RM 3 billion) per year in new capacity. New national formularies usually list nitrile as the default material to reduce allergy risks, accelerating the mix shift away from latex. The resulting inference is that capacity decisions now must factor government reimbursement rules alongside raw-material economics, intertwining public policy and factory planning more tightly than before

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Volatile Natural Rubber Pricing Driven by Climate-Linked Yield Shifts | -0.90% | Southeast Asia | Medium term (2–4 years) |

| Rising Allergic/Hypersensitivity Concerns Prompting Powdered Glove Bans | -0.70% | North America and Europe | Short to medium term (≤ 3 years) |

| Regulatory Approval Back‑Logs Delaying New Product Launches | -0.60% | North America and Europe | Short term (≤ 2 years) |

| Increasing Carbon‑Footprint Compliance Costs for Manufacturers | -0.50% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Natural Rubber Pricing Driven by Climate-Linked Yield Shifts

Climate variability is shrinking latex supply and driving unpredictable price swings that complicate cost forecasts for glove makers. The United States recently issued a waiver noting domestic shortfalls in nitrile-butadiene rubber feedstock, highlighting supply fragility even for synthetic options madeinamerica.gov. Manufacturers with vertical integration into chemical production can buffer these shocks, maintaining steadier pricing for hospital buyers. A clear inference is that access to diversified raw materials is becoming a core competitive moat, influencing lender perceptions of credit risk in the Medical Gloves industry.

Rising Allergic/Hypersensitivity Concerns Prompting Powdered Glove Bans

Allergies to latex proteins and chemical accelerators are prompting regulators to restrict powdered gloves and push for accelerator-free formulas. Ansell’s GAMMEX Non-Latex product shields wearers from both Type I and Type IV sensitivities. Hospitals that document lower dermatitis claims see measurable savings in staff sick leave, reinforcing adoption of hypoallergenic variants. The emerging inference is that worker-wellness data now influence purchasing committees almost as strongly as traditional cost-per-pair metrics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Product Type: Examination Gloves Lead While Cleanroom Accelerates

Examination gloves hold a 62.94 % Medical Gloves market share in 2025, underpinning daily patient care with cost-effective barrier protection. The segment’s volume allows factories to run long continuous lines, achieving economies that keep prices stable even amid feedstock swings. A fresh inference is that home-health kits shipped for telemedicine visits now include single-pair exam gloves, adding a modest but growing consumer channel.

Cleanroom gloves capture a modest slice of Medical Gloves market size yet grow at 11.92 % CAGR, the fastest of all product types. Demand comes from semiconductor and pharma plants that require ISO Class 1-3 compliance and electrostatic control. Manufacturers able to certify both sterility and low particulate generation win premium contracts. An observed implication is that cross-training sales teams for industrial and healthcare accounts boosts utilization of cleanroom lines.

Surgical gloves account for lower volume but higher revenue per thousand pieces because of stricter sterility and tactile demands. A 2025 study found that latex-free surgical gloves are 4.24 times more prone to perforation than latex, driving R&D into composite films doi.org. Hospitals are trialling double-layer polyisoprene designs that combine sensitivity with backup integrity, signaling possible market share shifts within the surgical subset.

Material Type: Nitrile Dominance Amid Neoprene’s Rapid Rise

Nitrile gloves own a commanding 47.82 % Medical Gloves market share in 2025, prized for broad chemical resistance and the absence of natural-rubber proteins. Their supply chain, however, is sensitive to acrylonitrile and butadiene feedstock prices, which have stayed elevated since late 2023. To insulate margins, top manufacturers are co-locating nitrile plants with glove factories, cutting transit and storage costs. Neoprene gloves, meanwhile, are growing at a 12.22 % CAGR, accelerated by surgical departments seeking latex-like elasticity minus protein allergens. One side effect is that polychloroprene demand is outpacing upstream supply, nudging chemical companies to reopen mothballed capacity.

Latex still holds a niche in procedures that require unmatched tactile fidelity, especially microneurosurgery. Vinyl remains the lowest-cost alternative for non-critical tasks, yet its weak barrier properties confine use to quick-turn applications. Polyisoprene, though premium-priced, is carving out space as a bridge between latex performance and nitrile safety. Regulatory trends under the FDA’s Quality Management System Regulation are catalyzing broader adoption of materials with stable supply profiles, encouraging R&D programs that emphasize recyclability and lower carbon intensity.

Sterility: Non-Sterile Volume Dominance vs. Sterile Premium Growth

Non-sterile gloves represent 71.64 % of Medical Gloves market size in 2025, supporting routine examinations and basic procedures. Bulk packaging formats cut waste and simplify ward logistics, keeping per-patient costs predictable. An inference is that bedside ultrasound-guided line insertions are prompting some wards to upgrade from non-sterile to sterile pairs, hinting at gradual share migration.

Sterile gloves exhibit the fastest 12.68 % CAGR due to growth in ambulatory centers and minimally invasive surgeries. Gamma irradiation and peel-pouch innovation add cost but also permit longer shelf life, which appeals to smaller facilities with irregular procedure schedules. Sustainability pilots now test recyclable sterile pouches, suggesting environmental pressures will soon influence even high-risk products.

End User: Hospitals Lead While Ambulatory Centers Surge

Hospitals hold 47.18 % Medical Gloves market share in 2025, reflecting broad procedural breadth and centralized purchasing. Integration with enterprise resource-planning systems lets hospitals monitor stock levels in real time, reducing last-minute shortages. A new inference is that predictive analytics on glove burn rate is guiding staffing plans, linking supply management to labor efficiencies.

Ambulatory surgical centers post a 12.55 % CAGR as insurers steer suitable cases away from costlier inpatient theaters. These centers favor premium gloves balancing feel and barrier protection because many procedures are short but precision-intensive. The implication is that product differentiation matters more in ASCs than in general wards, giving manufacturers a rationale for higher-margin SKUs.

Diagnostic laboratories need chemical-resistant gloves for reagent handling, anchoring steady demand independent of patient volumes. Home healthcare demand is rising as caregivers perform wound care and injections, creating small-pack opportunities at retail pharmacies. Dental practices require fine-textured fingertips for instrument grip, ensuring specialty designs remain viable

Geography Analysis

North America contributes 34.45 % of Medical Gloves market size in 2025, supported by advanced infrastructure and stringent infection-control rules. The region is reshaping sourcing after a 10 % tariff on Chinese gloves took effect in February 2025, steering orders toward Malaysian producers mida.gov.my. Distributors increasingly require suppliers to certify recycled content, signaling that green credentials are turning into market-entry tickets. An inference is that North American hospitals are bundling glove purchases within broader personal-protective-equipment contracts to leverage volume discounts.

Asia-Pacific is the fastest-growing geography with a 13.02 % CAGR outlook from 2026-2031. Malaysia alone manufactures 100 billion gloves annually, while Thai and Vietnamese producers expand automated lines. Domestic demand is also climbing as universal health insurance widens access to care across the region. One inference is that Asian governments adding gloves to national stockpiles create a built-in demand floor that cushions producers during global downturns.

Europe commands significant Medical Gloves market share thanks to universal coverage and strict chemical-safety laws. The EU Medical Device Regulation forces suppliers to document the absence of harmful substances, driving uptake of accelerator-free nitrile. Updated EU GMP Annex 1 tightens sterile manufacturing rules for pharma plants, bolstering demand for validated sterile gloves. An inference is that European hospital groups piloting glove-recycling loops could spark similar initiatives in North America once proof of cost savings emerges.

Mordor Intelligence provides coverage of the medical gloves market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns.

Competitive Landscape

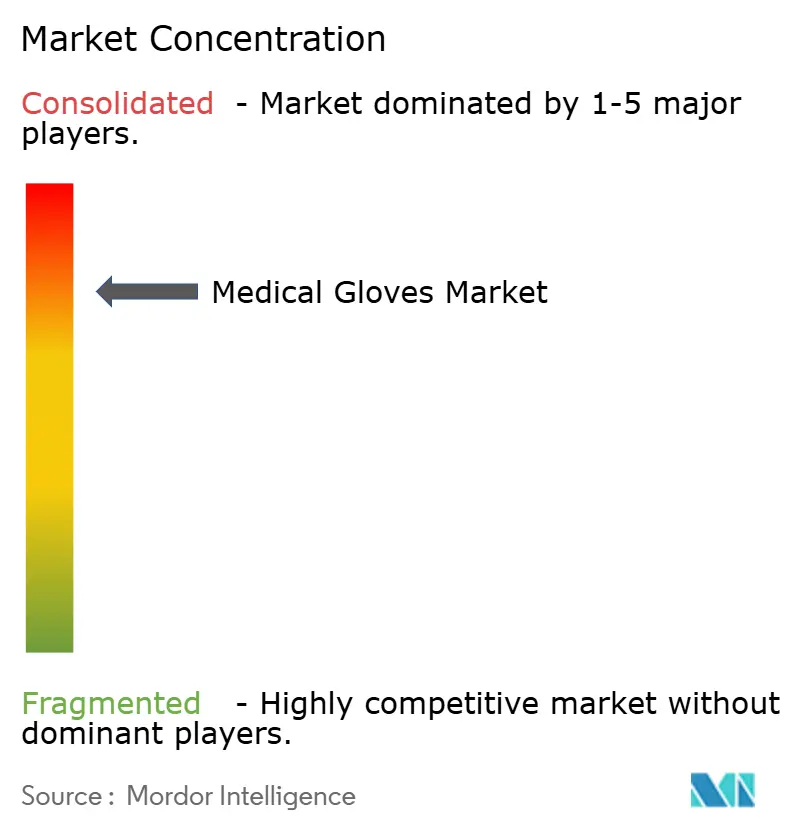

The Medical Gloves industry is moderately concentrated, led by companies with large automated capacities. Top Glove produces 100 billion pieces per year, exporting to 195 countries. Vertical integration into nitrile-butadiene rubber and packaging has helped leading firms buffer raw-material volatility. A fresh inference is that financiers now view integration as a credit-risk mitigant, lowering borrowing costs for fully integrated producers.

Strategic consolidation is gathering pace. Ansell’s USD 640 million acquisition of Kimberly-Clark’s PPE business strengthens its cleanroom and industrial portfolios and is expected to deliver USD 10 million annual synergies by year three. Tariff changes are redistributing Medical Gloves market share, with Malaysian producers Hartalega and Kossan positioned to win United States contracts that previously went to Chinese suppliers. An inference is that geopolitical trade dynamics are now as critical as price in shaping competitive outcomes.

Innovation focus is shifting toward sustainable and hypoallergenic offerings. Cranberry USA’s Bio Nitrile decomposes 80 % of its mass within 18 months, appealing to hospitals with carbon-reduction targets. Machine-vision inspection lines are lowering defect rates below 0.5 %, improving supplier audit scores and winning long-term contracts. An implication is that data transparency from these digital systems doubles as a sales tool in competitive tenders, making technology upgrades part of the marketing narrative.

Medical Gloves Industry Leaders

Top Glove Corporation Bhd

Hartalega Holdings Berhad

Ansell Limited

Kossan Rubber Industries Bhd

Supermax Corporation Berhad

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: The United States imposed a 10 % tariff on Chinese rubber gloves, pivoting sourcing toward Southeast Asia.

- June 2024: Halyard Health rolled out PUREZERO cleanroom gloves targeting ISO Class 3 environments with accelerator-free formulations

- April 2024: Ansell Limited secured USD 377 million long-term debt to finance its PPE acquisition, replacing a bridge facility.

- March 2024: The FDA issued technical amendments updating medical device citation references, subtly adjusting compliance documentation for glove makers.

- January 2024: The US Department of Health and Human Services announced a plan to procure over 55 million boxes of nitrile exam gloves for strategic stockpiles.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

In our analysis, and according to Mordor Intelligence, the medical gloves market covers all single-use examination, surgical, and clean-room gloves that meet ISO 11193 or equivalent standards and are purchased by hospitals, ambulatory centers, labs, dental settings, and home-health providers. We record values at factory-gate in constant 2024 USD and classify them by material (nitrile, latex, vinyl, neoprene, polyisoprene) and sterility.

Scope Exclusion: This study leaves out industrial, food-service, and household utility gloves, which Mordor profiles in a separate disposables overview.

Segmentation Overview

- By Product Type

- Examination Gloves

- Surgical Gloves

- Cleanroom Gloves

- By Material Type

- Nitrile

- Latex

- Vinyl

- Neoprene

- Polyisoprene

- By Sterility

- Sterile

- Non-Sterile

- By End User

- Hospitals & Clinics

- Ambulatory Surgery Centers

- Diagnostic Laboratories

- Home Healthcare Settings

- Dental Practices

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- GCC

- South Africa

- Rest of Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed surgeons, infection-control nurses, procurement managers, and distributors across North America, Europe, ASEAN, and Latin America. These discussions validated glove-change protocols, usage per procedure, price pass-through patterns, and regional policy shifts before we reconciled the desk findings.

Desk Research

We begin with publicly available datasets such as WHO's Global Surgery Database, UN Comtrade trade codes 401511 and 401519, US ITC HS 392620 flows, CDC-NHSN infection statistics, and shipment updates from the Malaysian Rubber Glove Manufacturers Association. Company filings, 10-Ks, and investor presentations reveal cost curves and contract ASPs, while paid platforms, D&B Hoovers, Dow Jones Factiva, and Volza, add supplier revenues and shipment trails. The sources listed are illustrative; many additional databases and peer-reviewed papers informed our work.

Market-Sizing & Forecasting

We derive the 2025 baseline through a top-down reconstruction of global output and cross-border trade, then corroborate it with selective bottom-up roll-ups of major producers' capacity disclosures and sampled ASP × volume data. Key variables like elective surgery volumes, hospital bed density, glove change frequency, nitrile and latex price indices, and regulatory bans on powdered gloves feed a multivariate regression model, while scenario analysis tests raw-material volatility assumptions. Where bottom-up evidence is thin, gap factors based on primary-research ranges are applied.

Data Validation & Update Cycle

Our analysts run variance checks against independent import tallies and hospital procurement benchmarks, flagging anomalies for peer review before sign-off. The model is refreshed every twelve months, with interim updates when trade policy or disease outbreak alerts materially alter demand.

Why Mordor's Medical Gloves Baseline Deserves Confidence

Published estimates often diverge because each publisher chooses unique scopes, price bases, and refresh cadences. By adhering to a healthcare-only scope, factory-gate pricing, and an annual update rhythm, Mordor delivers a balanced baseline decision-makers can trust.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 13.52 Bn (2025) | Mordor Intelligence | - |

| USD 19.02 Bn (2025) | Global Consultancy A | Bundles industrial and food-handling gloves and uses retail prices |

| USD 10.40 Bn (2024) | Trade Journal B | Focuses solely on disposable gloves, omitting surgical revenues |

The comparison shows that broader or narrower scopes, differing price points, and infrequent updates explain most headline gaps, underscoring why Mordor's disciplined approach offers the most reproducible baseline for strategic planning.

Key Questions Answered in the Report

What is the current Medical Gloves market size?

The market is valued at USD 15.01 billion in 2026

What CAGR is projected for the Medical Gloves industry through 2031?

The forecast compound annual growth rate is 11.05 %.

Which region will grow fastest in Medical Gloves market share?

Asia-Pacific is expected to expand at a 13.02 % CAGR from 2026 to 2031.

Why are nitrile gloves preferred over latex in many facilities?

They resist chemicals, avoid protein allergens and comply with more restrictive allergy-prevention policies.

How are sustainability goals influencing glove design?

Manufacturers are introducing biodegradable and recyclable gloves that keep barrier performance while cutting waste.

What impact will the FDA’s ISO 13485 alignment have on glove makers?

It raises documentation and risk-management requirements, favoring producers with advanced quality systems.

Page last updated on: