Medical Supplies Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 198.17 Billion |

| Market Size (2031) | USD 318.77 Billion |

| Growth Rate (2026 - 2031) | 9.97% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

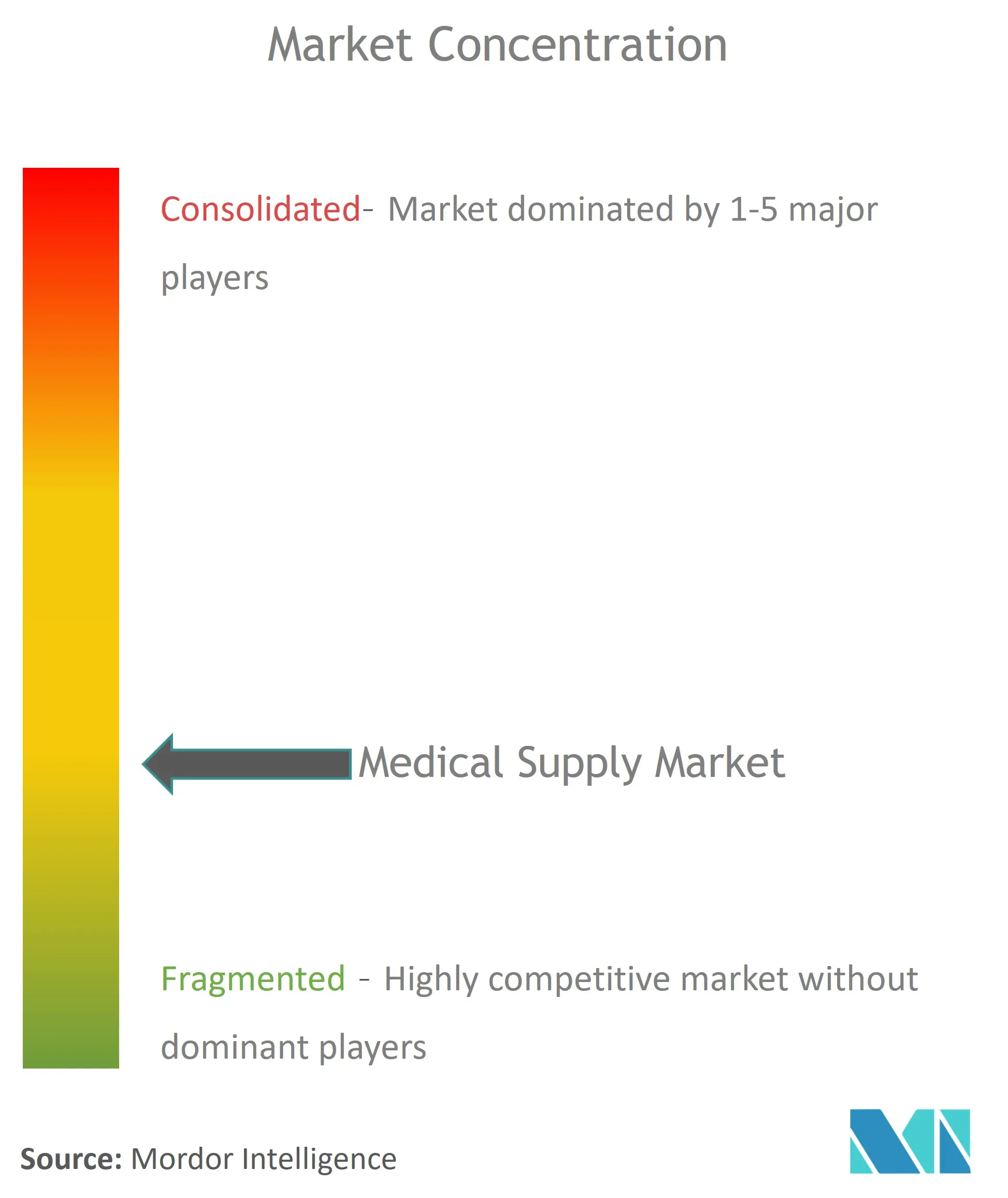

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Supplies Market Analysis by Mordor Intelligence

The medical supplies market size was valued at USD 180.2 billion in 2025 and estimated to grow from USD 198.17 billion in 2026 to reach USD 318.77 billion by 2031, at a CAGR of 9.97% during the forecast period (2026-2031). Demand expands well beyond population growth as infection-control norms, value-based reimbursement, and care decentralization elevate supplies from commodity inputs to essential enablers of health-system performance. Higher personal protective equipment (PPE) baselines, broader acceptance of single-use procedure kits, and regulatory alignment with ISO 13485:2016 are lowering compliance frictions for global producers while driving up minimum quality thresholds. Regional trajectories diverge: North America protects its lead through entrenched reimbursement and early adoption. Asia Pacific records the fastest growth as capacity and chronic-disease incidence climb, and Europe balances new Medical Device Regulation (MDR) obligations with sustainability rules that catalyze product reformulation. Competitive positioning now hinges on the ability to deliver total-cost-of-ownership gains, infection-rate reductions, and home-care-ready formats, reinforcing consolidation and technology partnerships that blend devices, consumables, and data services.

Key Report Takeaways

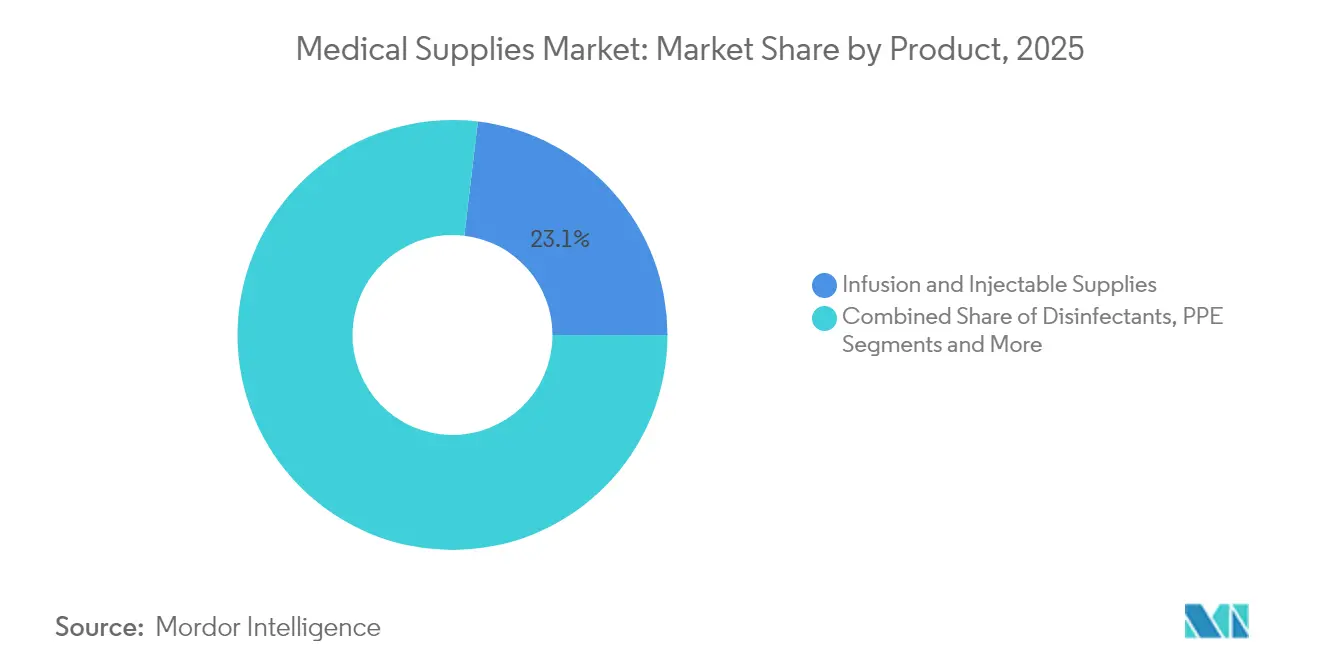

- By product type, infusion and injectable supplies led with 23.12% of the medical supplies market share in 2025, while dialysis consumables are projected to expand at a 7.55% CAGR to 2031.

- By application, infection control held 19.08% revenue share in 2025; respiratory applications are set to advance at an 8.31% CAGR through 2031.

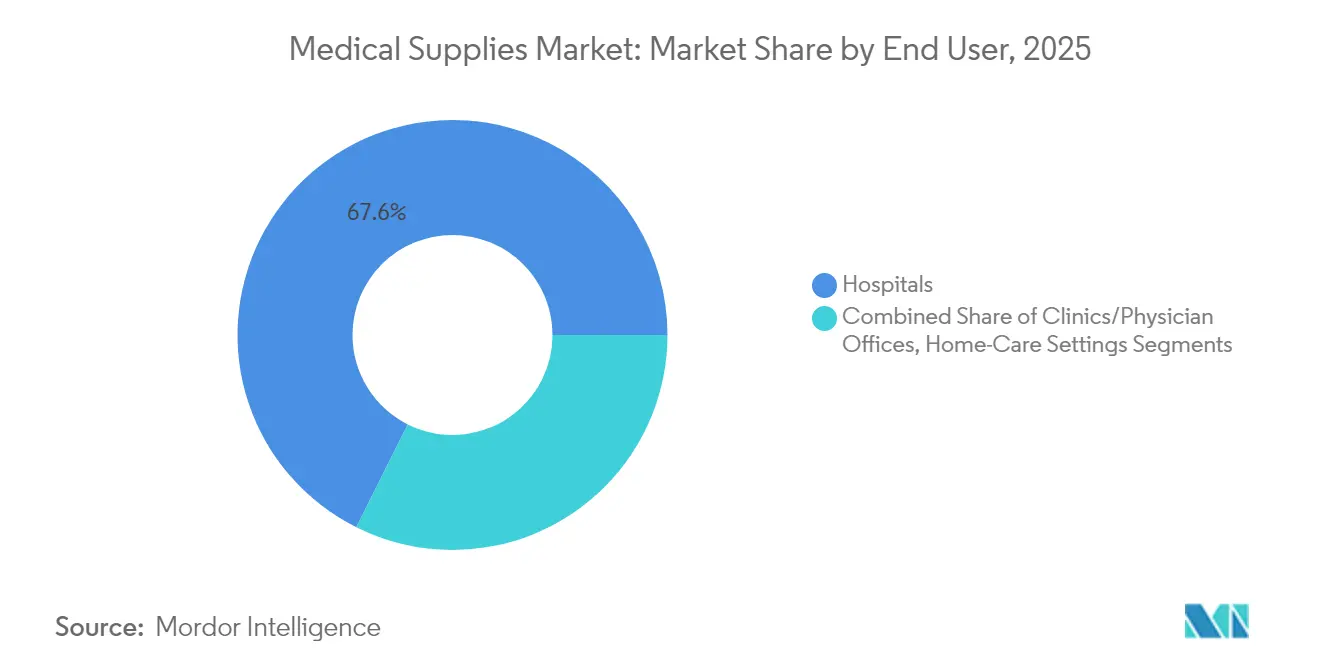

- By end-user, hospitals commanded 67.62% share of the medical supplies market size in 2025, whereas home-care settings represent the fastest rising channel with a 8.98% CAGR to 2031.

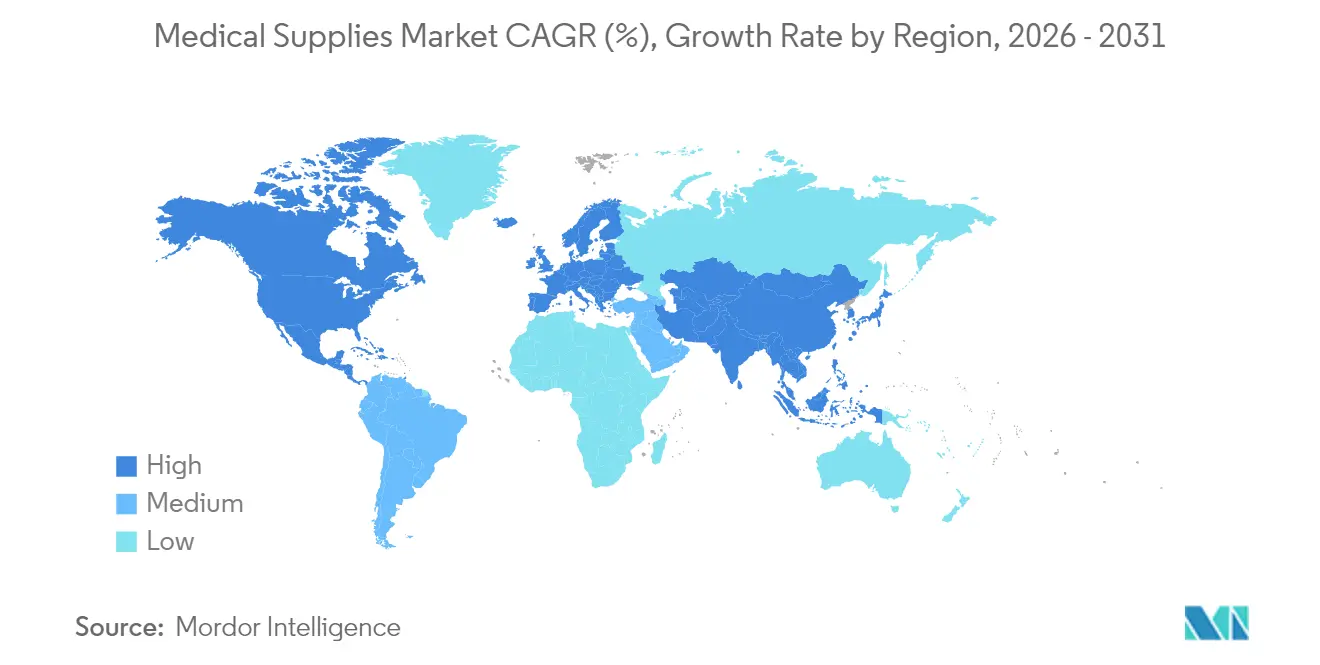

- By geography, North America captured 40.75% of the medical supplies market size in 2025, but Asia Pacific is forecast to register the highest regional CAGR at 11.45% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Supplies Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth of ambulatory surgery centers | +1.50% | North America and Europe, expanding to Asia Pacific | Medium term (2-4 years) |

| Shift to home-based care and hospital-at-home | +1.80% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Growing chronic-care patient pool | +1.20% | Global, concentrated in aging populations | Long term (≥ 4 years) |

| Rising PPE replenishment cycles | +0.80% | Global, health-system emphasis | Short term (≤ 2 years) |

| AI-enabled predictive maintenance | +0.60% | North America and Europe, pilot programs in Asia Pacific | Medium term (2-4 years) |

| Circular-economy mandates | +0.50% | Europe leading, expanding to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth of Ambulatory Surgery Centers

Ambulatory surgery centers (ASCs) now handle more than 25 million U.S. procedures each year, growing 3-4% annually as payers widen approved procedure lists.[1]Centers for Medicare & Medicaid Services, “Hospital-at-Home Program Expansion,” cms.gov ASCs deliver 40-60% cost savings over hospital outpatient departments, so suppliers are redesigning single-use kits that compress turnover times and cut waste. The Food and Drug Administration (FDA) guidance on Predetermined Change Control Plans, effective August 2024, lets manufacturers iterate devices faster to match ASC workflow needs.[2]Food and Drug Administration, “Quality Management System Regulation Amendments,” fda.gov Portfolio shifts toward low-complexity disposables with embedded safety features boost recurring revenue and deepen penetration of the medical supplies market.

Shift to Home-Based Care & Hospital-at-Home Programs

Hospital-at-home models cover more than 300 U.S. health systems and deliver 25-30% cost reductions with higher patient-satisfaction scores than inpatient wards. Medical supplies must now feature simpler packaging, longer shelf life and intuitive instructions suited to residential caregivers. Suppliers are investing in last-mile logistics and digital reorder platforms to maintain uninterrupted supply streams. As decentralized care expands in Europe, Australia and Japan, the medical supplies market gains a durable growth avenue anchored in recurring home-therapy consumption.

Growing Chronic-Care Patient Pool

Chronic conditions are projected to account for 73% of global deaths by 2030.[3]World Health Organization, “Projections of Mortality and Causes of Death,” who.int Dialysis consumables illustrate the impact: the treated renal population is rising 6-8% annually, with home-dialysis uptake further lifting per-patient utilization. Producers targeting the medical supplies industry segment for diabetes, cardiovascular and renal care are emphasizing user-friendly designs that enable self-management and command premium pricing.

Rising PPE Replenishment Cycles Post-COVID

Strategic national stockpiles now retain rolling 90-day inventories, and most acute-care facilities have doubled their on-hand PPE buffers relative to pre-2020 levels. This institutionalized demand removes the boom-bust procurement swings seen during the pandemic and supports steadier revenue for glove, mask, and gown manufacturers within the medical supplies market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened FDA & MDR Post-Market Surveillance Recalls | -0.80% | North America & Europe primarily | Medium term (2-4 years) |

| Volatile Resin & Nitrile Prices Squeezing Consumable Margins | -0.60% | Global, with supply chain concentration in Asia | Short term (≤ 2 years) |

| ESG Pressure Against Single-Use Plastics In Hospitals | -0.40% | Europe leading, expanding to North America & APAC | Long term (≥ 4 years) |

| Tight Global Ethylene Oxide Sterilization Capacity | -0.30% | Global, with critical bottlenecks in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Heightened FDA & MDR Post-Market Recalls

Class I recalls climbed 35% in 2024 and predominantly involved sterility lapses. In Europe, MDR audits expose latent quality issues and trigger market withdrawals. Providers facing shortages shift to substitute products, but manufacturers absorb 8-12% higher compliance costs that thin margins across the medical supplies market.

Volatile Resin & Nitrile Prices

Nitrile prices oscillated 40-60% in 2024, while key resins saw 25-35% swings driven by feedstock volatility and environmental curbs. Commodity-heavy product lines such as examination gloves and syringes suffer margin compression because reimbursement schedules lag material inflation. Larger players hedge through vertical integration and multi-year supply contracts, but smaller firms in the medical supplies industry risk contract losses when unable to hold quoted pricing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Infusion Supplies Retain Leadership as Dialysis Outpaces

Infusion and injectable supplies contributed 23.12% of the medical supplies market size in 2025, underscoring the universal requirement for intravenous therapy across every care level. Growth is held steady by safety-engineered needles and smart infusion pumps that curb medication errors. Emerging volume now stems from home-infusion programs backed by reimbursement expansion, prompting vendors to bundle devices and disposables for at-home regimens.

Dialysis consumables deliver the swiftest rise with a 7.55% CAGR through 2031. Prevalence gains in diabetes and hypertension enlarge the renal patient pool, while policy incentives for home peritoneal dialysis push demand for compact bags, cassettes and sterile connectors. Suppliers that document reduced infection rates and easier self-administration can capture share in this premium slice of the medical supplies market. Advanced polymer membranes and antimicrobial coatings remain differentiation levers as competition intensifies.

By Application: Infection Control Dominates, Respiratory Surges

Infection control accounted for 19.08% of the medical supplies market share in 2025 and continues to anchor procurement priorities. Hospitals invest in surface disinfectants, sterile wraps, and barrier drapes to meet zero-infection targets, and regulators heighten penalties tied to hospital-acquired events. Vendors offering complete system bundles such as chemistries, indicators, and sterilizer consumables position themselves as strategic partners rather than suppliers of single SKUs.

Respiratory applications, projected to expand at 8.31% CAGR to 2031, benefit from rising diagnoses of sleep apnea and chronic obstructive pulmonary disease. Technological progress in non-invasive ventilation masks and disposable humidifier chambers supports home-care adoption and enhances patient adherence. Combined, these trends reinforce a multi-year uplift across the broader medical supplies market.

By End-User: Hospitals Hold Scale; Home Care Accelerates

Hospitals commanded 67.62% of the medical supplies market size in 2025, reflecting their role in trauma, critical care, and complex surgery. Purchasing teams now emphasize lifetime value, favoring suppliers that quantify infection-rate reductions and workflow efficiencies. Integrated supply agreements covering broad SKU portfolios simplify vendor management and secure volume commitments.

Home-care settings post the sharpest gain at a 8.98% CAGR through 2031. Remote monitoring, home infusion, and renal self-care reshape demand toward small-pack formats with tamper-evident seals and clear pictorial guides. Logistics partners that guarantee two-day replenishment or offer subscription models win provider contracts. Clinics, physician offices, and long-term-care facilities grow at mid-single-digit rates as they broaden procedural capabilities, sustaining a diversified demand base within the medical supplies market.

Geography Analysis

North America remained the most significant contributor in 2024, owing to entrenched reimbursement schemes and rapid uptake of best-in-class infection-control products. Predictable FDA user-fee structures and alignment with ISO 13485:2016 lower regulatory friction for international suppliers. Canada accelerates device approvals through its Medical Device Single Audit Program, while Mexican private hospitals import premium disposables to serve medical tourism. Together, these factors stabilize regional growth and sustain high purchasing power within the medical supplies market.

Europe’s trajectory is steadier as MDR documentation expenses and PFAS restrictions weigh on smaller suppliers. Germany leads export value with its embedded manufacturing base, and the United Kingdom refines its post-Brexit conformity rules to mirror global standards, providing dual-pathway access for transatlantic producers. Southern European markets, despite fiscal constraints, channel structural funds into infection-prevention upgrades, securing incremental expansion for sterilization and respiratory disposables.

Asia Pacific delivers the fastest CAGR at 11.45% through 2031. China’s volume-based procurement favors cost-efficient domestic producers for high-volume items, while preference remains for imported premium consumables in tertiary hospitals. Japan’s aging society drives steady uptake of wound-care and ostomy supplies, and South Korea layers digital connectivity onto disposables to enable device-agnostic data capture. India scales its Pradhan Mantri Jan Arogya Yojana insurance scheme, broadening access to interventional procedures that utilize medical supplies market offerings. Manufacturing clusters in Malaysia, Thailand and Vietnam expand export capacity, reducing dependence on single-country sourcing.

Competitive Landscape

The medical supplies market shows moderate concentration. Cardinal Health controls about 15.36% of the market through distribution, kitting, and logistics advantages. Becton Dickinson holds 2.11% by focusing on safety-engineered syringes and infection-control disposables, while ICU Medical reaches 1.55% with niche strength in infusion therapy. Consolidation remains active: the USD 950 million Medline-Ecolab infection-prevention alliance merges consumable production with chemistries to offer bundled value.

Technology partnerships differentiate leaders. Firms embed RFID tags and barcode systems that integrate into hospital inventory platforms, cutting stockouts by up to 30%. AI-driven demand forecasts reduce unused inventory and align replenishment with contracted volumes. Sustainability has become a procurement criterion; DuPont’s 2024 acquisition of Donatelle Plastics added low-energy sterilization packaging, and B. Braun’s 50% packaging-reduction pledge targets both cost and carbon metrics.

New entrants gravitate toward home-care niches and bio-based materials, yet scale barriers in sterile manufacturing and validation temper their advance. ISO 13485:2016 harmonization by February 2026 favors multinational incumbents already compliant across regions. Overall, competitive intensity shifts from pure price toward outcome-linked contracts and integrated service bundles that deepen switching costs.

Medical Supplies Industry Leaders

Medtronic plc

Cardinal Health

Becton, Dickinson and Company

B. Braun Melsungen AG

Boston Scientific Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: WACKER acquired Bio Med Sciences to expand its medical-grade silicone platform for high-growth wound-care and implantable components.

- January 2025: Henry Schein completed the USD 380 million purchase of Acentus, enlarging its North American distribution footprint.

- December 2024: UFP Technologies bought AQF Medical for USD 45 million, adding clean-room single-use capacity.

- October 2024: Merit Medical Systems paid USD 120 million for Biolife, entering the peripheral vascular disposables market.

Global Medical Supplies Market Report Scope

As per the scope of the report, medical supply is known as medical or surgical items used in a healthcare setup that are consumable, expendable, disposable or non-durable and that are used for the treatment or diagnosis of a patient's specific illness, injury, or condition. The Medical Supplies Market is segmented by Product Type (Diagnostic Supplies, Infusion & Injectable Supplies, Intubation & Ventilation Supplies, Disinfectants, Personal Protective Equipment, Sterilization Consumables, Wound Care Consumables, Dialysis Consumables, Radiology Consumables, Catheters, Sleep Apnea Consumables, and Other Medical Supplies), Application (Urology, Wound Care, Radiology, Respiratory, Infection Control, Cardiology, IVD, and Other Applications), End-User (Hospitals, Clinics/Physician Offices and Other End-Users), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Diagnostic Supplies |

| Infusion & Injectable Supplies |

| Intubation & Ventilation Supplies |

| Disinfectants |

| Personal Protective Equipment |

| Sterilization Consumables |

| Wound-Care Consumables |

| Dialysis Consumables |

| Radiology Consumables |

| Catheters |

| Other Product Types |

| Urology |

| Wound Care |

| Radiology |

| Respiratory |

| Infection Control |

| Cardiology |

| In-Vitro Diagnostics |

| Other Applications |

| Hospitals |

| Clinics / Physician Offices |

| Home-Care Settings |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Diagnostic Supplies | |

| Infusion & Injectable Supplies | ||

| Intubation & Ventilation Supplies | ||

| Disinfectants | ||

| Personal Protective Equipment | ||

| Sterilization Consumables | ||

| Wound-Care Consumables | ||

| Dialysis Consumables | ||

| Radiology Consumables | ||

| Catheters | ||

| Other Product Types | ||

| By Application | Urology | |

| Wound Care | ||

| Radiology | ||

| Respiratory | ||

| Infection Control | ||

| Cardiology | ||

| In-Vitro Diagnostics | ||

| Other Applications | ||

| By End-User | Hospitals | |

| Clinics / Physician Offices | ||

| Home-Care Settings | ||

| Other End-Users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the medical supplies market?

The medical supplies market is valued at USD 198.17 billion in 2026.

How fast is the medical supplies market expected to grow?

It is projected to expand at a 9.97% CAGR, reaching USD 318.77 billion by 2031.

Which product category presently holds the largest medical supplies market share?

Infusion and injectable supplies led with 23.12% share in 2025.

Which region will grow the fastest through 2031?

Asia Pacific is forecast to post the highest CAGR at 11.45% during 2026-2031.

Why are home-care settings attracting medical supplies investment?

Hospital-at-home programs, reimbursement for home infusion and remote monitoring drive a 8.98% CAGR for home-care consumption, spurring demand for simplified, home-ready supplies.

How are stricter regulations affecting suppliers?

ISO 13485:2016 alignment and tougher post-market surveillance raise compliance costs but standardize quality expectations, benefiting firms with established global quality systems.

Page last updated on: