Medical Smart Textile Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.55 Billion |

| Market Size (2031) | USD 4.82 Billion |

| Growth Rate (2026 - 2031) | 13.56% CAGR |

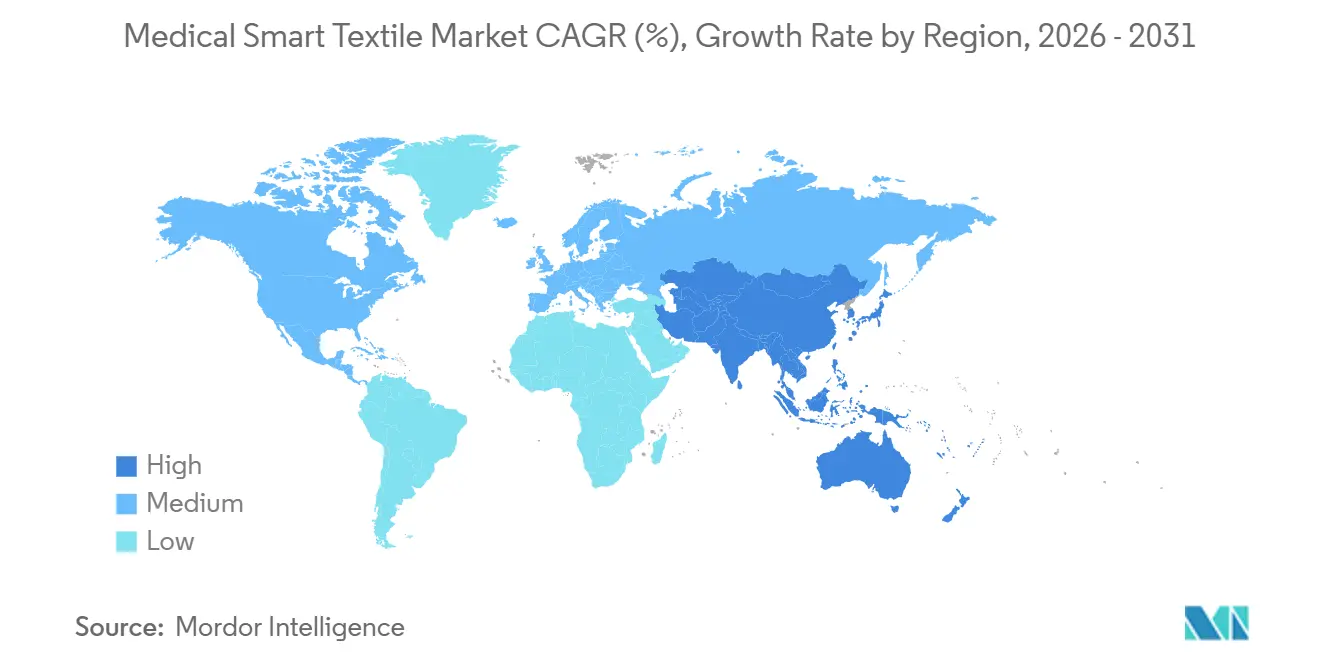

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

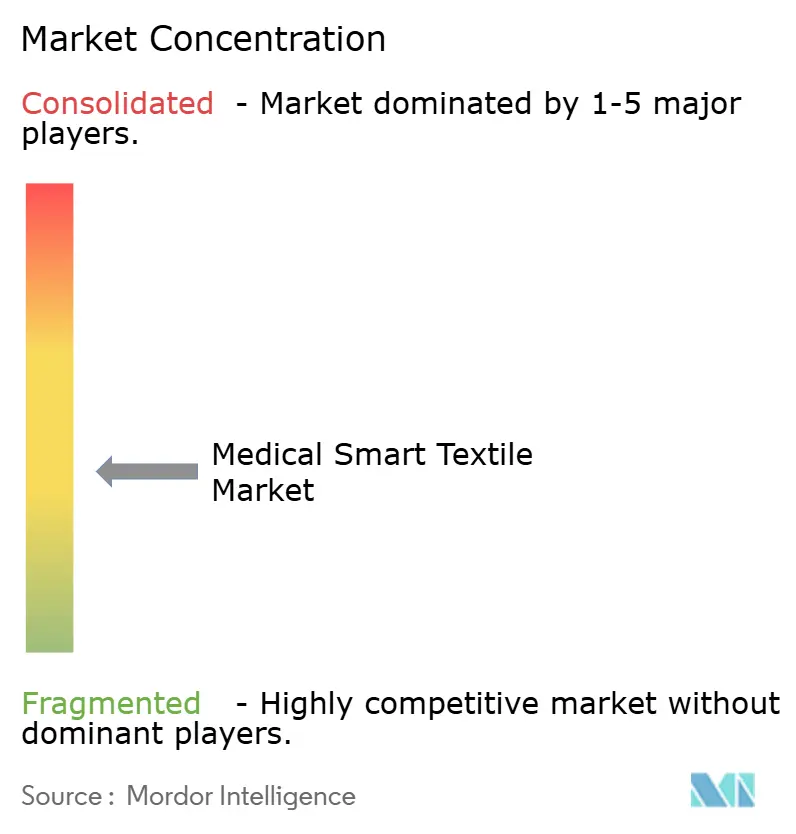

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Smart Textile Market Analysis by Mordor Intelligence

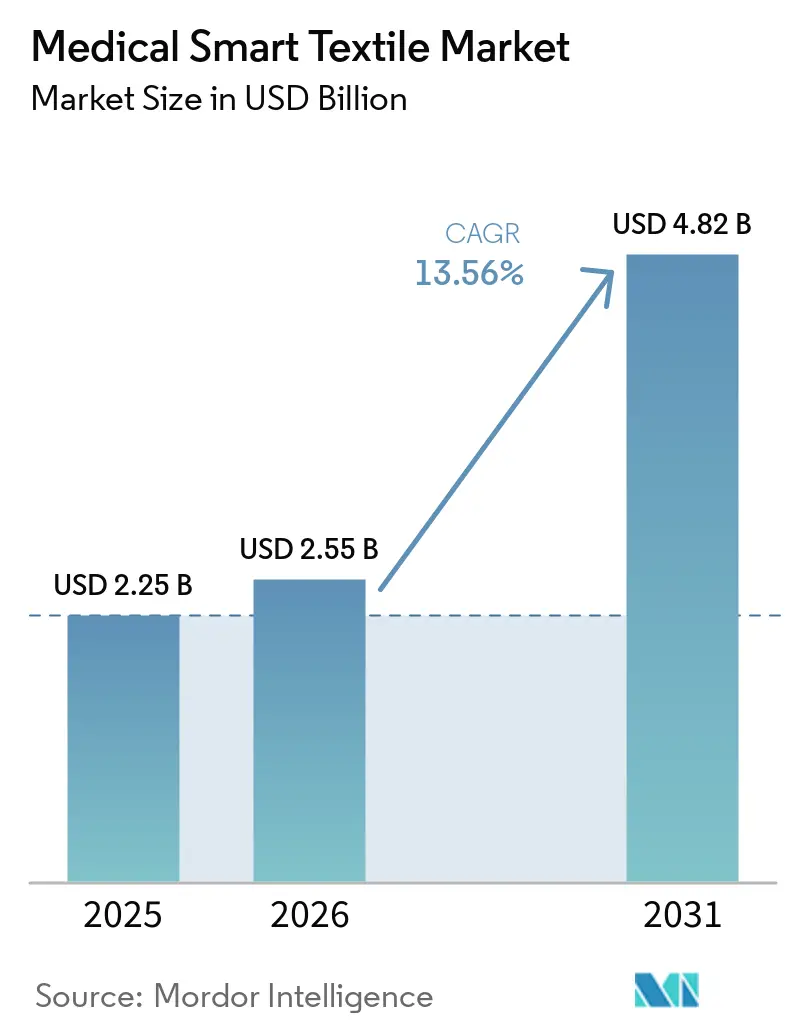

The Medical Smart Textile Market size is projected to be USD 2.25 billion in 2025, USD 2.55 billion in 2026, and reach USD 4.82 billion by 2031, growing at a CAGR of 13.56% from 2026 to 2031.

The market is moving forward as aging populations, higher chronic disease monitoring needs, and pressure on care systems are pushing more observation outside hospital walls and into daily life. Clinical validation is also strengthening the medical smart textile market because textile-based sensors are increasingly being treated as usable alternatives to separate monitoring hardware in perioperative, cardiopulmonary, and ambulatory settings. The July 2026 launch of the CMS ACCESS Model gives the medical smart textile market a stronger commercial base because FDA-authorized wearables can now fit more directly into payment structures tied to chronic care outcomes. The medical smart textile market is also benefiting from better conductive yarns, smaller sensing components, and machine-washable designs, which make repeated use more practical in home care and rehabilitation programs. Competition in the medical smart textile market remains moderately fragmented, and the companies best placed to gain are the ones that can combine regulatory progress, clinical proof, workflow integration, and useful interpretation of continuous patient data.

Key Report Takeaways

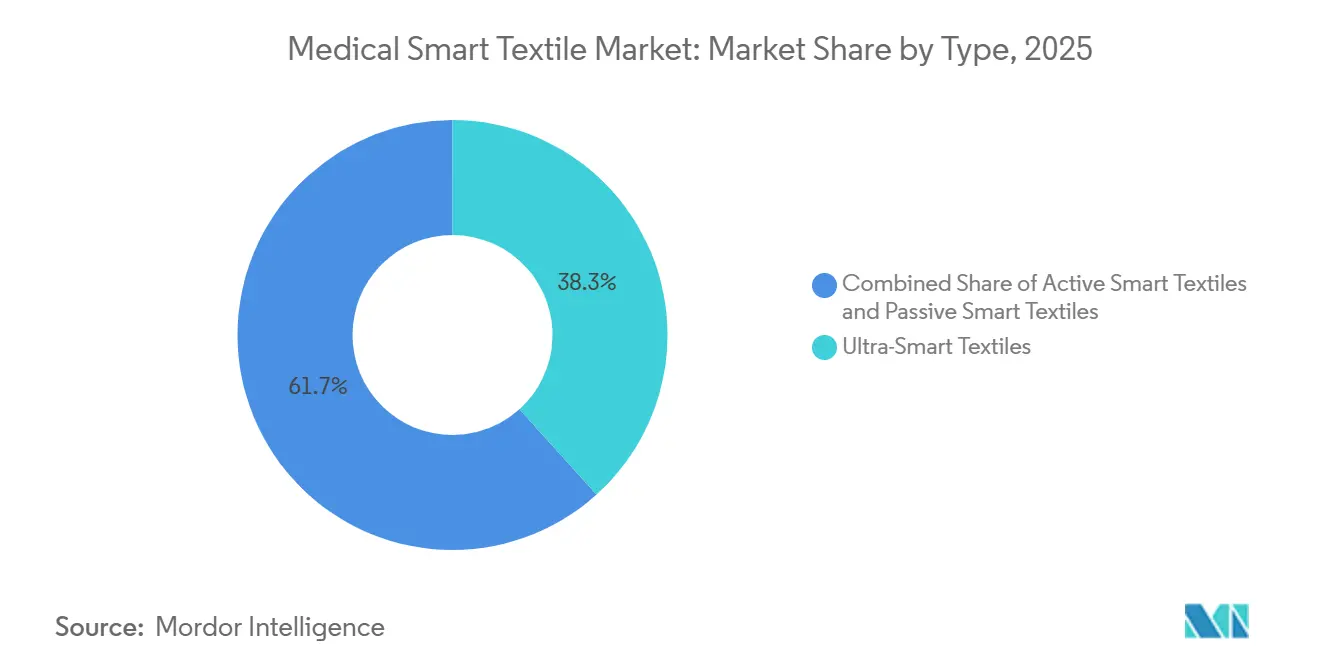

- By type, Ultra-Smart Textiles held 38.31% revenue share in 2025, while Active Smart Textiles are forecast to grow at a 14.38% CAGR through 2031.

- By technology, Wearable Technology commanded 38.24% revenue share in 2025, while Biomedical Wearables are projected to expand at a 14.52% CAGR through 2031.

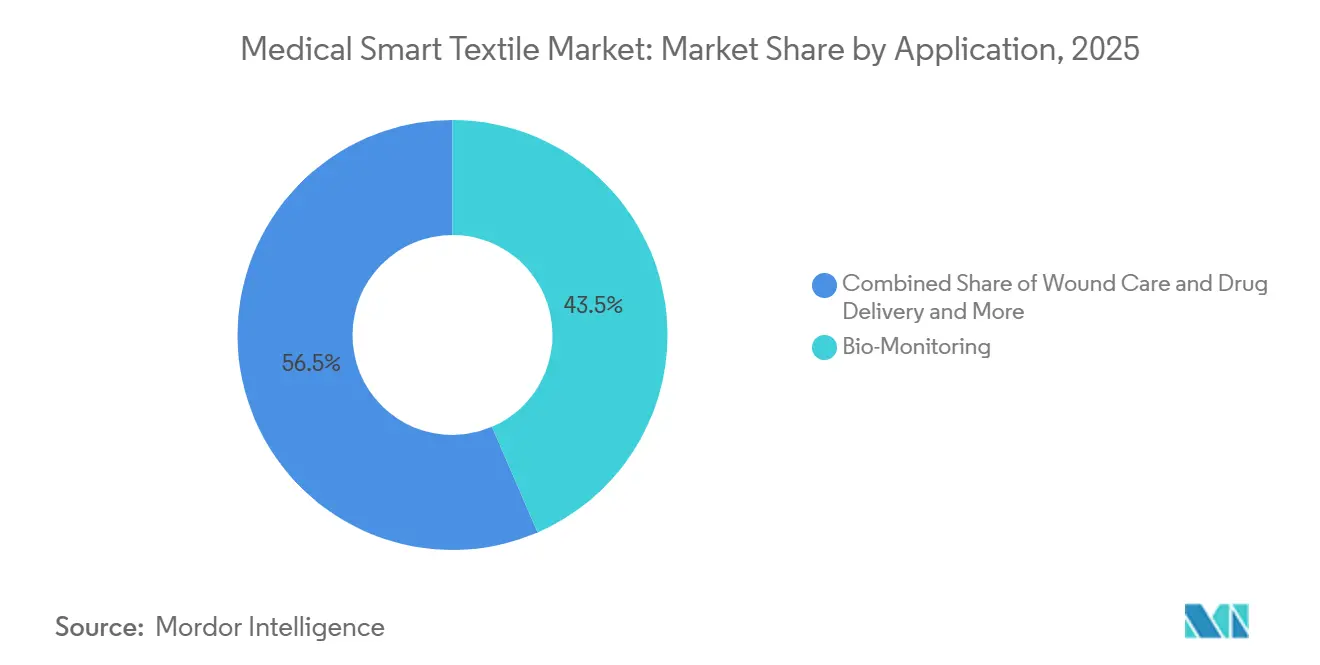

- By application, Bio-Monitoring accounted for 43.52% of the medical smart textile market size in 2025, while Wound Care and Drug Delivery is projected to advance at a 15.25% CAGR through 2031.

- By end user, Hospitals and Clinics held 54.34% revenue share in 2025, while Home Healthcare and Patients are expected to record the highest CAGR at 16.15% through 2031.

- By geography, North America held 38.22% of the medical smart textile market share in 2025, while Asia-Pacific is projected to record a 15.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Medical Smart Textile Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Remote Patient Monitoring | +2.8% | Global | Short term (≤ 2 years) |

| Shift Toward Continuous, Non-Invasive Vital Sign Tracking | +2.0% | Global, with early concentration in North America and Europe | Short term (≤ 2 years) |

| Wearable Integration With Digital Care Pathways | +1.6% | North America and Europe | Medium term (2-4 years) |

| Hospital Push for Post-Acute and Home-Care Extensions | +1.5% | North America and Europe | Medium term (2-4 years) |

| Textile Sensor Miniaturization and Washability Improvements | +1.8% | Global | Short term (≤ 2 years) |

| Reimbursement Support for Connected Care | +1.7% | North America, with early spillover to Western Europe | Short term (≤ 2 years) and Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Remote Patient Monitoring

Remote patient monitoring is becoming a regular part of chronic disease management, and that shift is giving the medical smart textile market a wider and more durable use case than short hospital episodes alone. The CMS ACCESS Model launches in July 2026 and directly includes FDA-authorized wearables within technology-supported chronic care for Medicare beneficiaries with conditions such as hypertension, diabetes, and chronic musculoskeletal pain[1]CMS Innovation Center, “ACCESS (Advancing Chronic Care With Effective, Scalable Solutions) Model,” Centers for Medicare & Medicaid Services, cms.gov. That matters because garments that collect physiological data can fit more naturally into daily routines than patches or separate monitoring hardware, which supports better adherence over longer periods. A June 2026 prospective study at Duke University Health System showed that wearable monitoring detected early postoperative deterioration before visible clinical presentation, which supports continuous monitoring beyond the hospital stay. The commercial effect is broader than long-term disease management because shorter monitoring windows can now make economic sense in post-surgical and post-acute care. As a result, the medical smart textile market is gaining access to a larger patient pool that sits between inpatient care and fully unmanaged home recovery.

Reimbursement Support for Connected Care in Key Markets

Reimbursement alignment has become one of the clearest demand supports for the medical smart textile market because payment rules now better match how connected care is delivered in real clinical practice. CMS proposed in July 2025 that remote patient monitoring codes could apply when data is transmitted for as few as 2 days in a 30-day period, rather than the prior 16-day minimum, which expands the fit for episodic care and discharge follow-up. That change is important because textile-based devices are often most useful when patients need observation after surgery, after discharge, or during therapy periods that do not last a full month. In January 2025, Mölnlycke Health Care invested USD 8 million in Siren Care, whose temperature-sensing diabetic foot socks were reported to reduce diabetic foot ulcer risk by 68% and amputations by 83%, while also lowering annual treatment costs per patient. That move shows that coverage discussions are increasingly shaped by measurable cost-of-care outcomes rather than by sensor novelty alone. Companies in the medical smart textile market that can show patient-level savings are therefore in a better position than companies offering strong hardware performance without comparable clinical and economic proof.

Textile Sensor Miniaturization and Washability Improvements

The medical smart textile market depends heavily on products that can stay comfortable on the body while still producing dependable signals through repeated use. Two engineering gains are central here, smaller sensing structures that stay close to the skin and washable garment designs that support repeated use in ambulatory and home programs. Hexoskin’s Medical System received FDA 510(k) clearance on November 19, 2025, as the first FDA-cleared smart shirt for long-term ECG, respiratory, and activity monitoring in a machine-washable garment for ambulatory patients. A May 2025 study in Nature Electronics described acoustic glass-microfibre sensing textiles that could monitor respiratory rate and muscle tension in a compact 10 mm × 10 mm sensing array using commercially available materials. These advances lower practical barriers to clinical deployment because repeated washing, user comfort, and compact sensing are all necessary for real-world adherence. They also shift more of the competitive burden in the medical smart textile market away from raw materials and toward validation, regulatory work, and dependable scale-up.

Wearable Integration With Digital Care Pathways

The medical smart textile market will not reach its full commercial value unless garment-based data can move easily into the clinical systems that providers already use every day. A 2025 review in Advanced Materials showed how AI-enabled wearable sensors are moving from basic tracking tools toward predictive and diagnostic support devices, which changes their role inside care delivery. That shift matters because hospitals and physicians do not need more raw data feeds when they cannot act on them inside existing workflows. They need structured outputs that fit electronic records, support alerts, and shorten the time between signal capture and clinical response. For the medical smart textile market, this means contract renewal and switching costs will increasingly depend on software integration and usable analytics rather than on fabric design alone. Companies that can connect sensing garments with digital care pathways are likely to hold stronger positions as connected care becomes more routine in cardiology, rehabilitation, respiratory monitoring, and long-term chronic disease management.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Production and Validation Costs | -1.6% | Global | Long term (≥ 4 years) |

| Regulatory and Certification Complexity | -1.3% | North America and Europe | Medium term (2-4 years) and Long term (≥ 4 years) |

| Data Accuracy and Long-Term Reliability Concerns | -1.0% | Global | Medium term (2-4 years) |

| Interoperability Friction With Clinical IT Systems | -0.8% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Production and Validation Costs

The medical smart textile market faces a cost structure that differs from many conventional device categories because validation needs can outweigh hardware production budgets by a wide margin. The fabric, yarn, and embedded sensor components may be manageable at scale, but the clinical studies required for clearance and reimbursement often consume far more capital. A 2024 review in the Journal of the Textile Institute noted that washability and durability remain persistent barriers because conductive components can degrade across repeated wash cycles in ways that are hard to predict and expensive to test[2]“Design and Development of Textile-Based Wearable Sensors for Real-Time Biomedical Monitoring: A Review,” Journal of the Textile Institute, tandfonline.com. That raises the cost of proving long-term performance across different patient groups, garment types, and use settings. Payer expectations are also increasing because cost-reduction evidence now matters as much as technical function in many coverage discussions. This leaves smaller innovators in the medical smart textile market under pressure because the same firms that move fastest on product ideas are often least able to fund large prospective studies.

Regulatory and Certification Complexity

Regulatory complexity continues to slow the medical smart textile market because these products often sit across medical device rules, software oversight, and textile performance standards at the same time. A 2025 report from the E-Textiles Network found that participants across academia, industry, and healthcare pointed to the lack of standards tailored specifically to smart textiles in health and care under the MHRA and UKCA setting. The problem is not only cost, because different approval routes in the United States and Europe often require different evidence packages and different timelines. That can force companies to choose between sequential launches, which delay revenue, and parallel submissions, which raise development spending sharply. Specialized players that have already moved through one route hold an advantage in know-how, but they still face a slower expansion path when entering new jurisdictions. The result is that the medical smart textile market can grow quickly in demand terms while still moving unevenly in commercial rollout and regional availability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Clinical complexity commands premium, but active systems set the pace

Ultra-Smart Textiles held 38.31% of the medical smart textile market share within the type split in 2025, showing that providers were willing to pay more for garments that combined multi-parameter sensing with more advanced functionality. Hospitals and step-down care settings valued these systems because one garment could capture ECG, respiratory rate, muscle activity, and skin temperature in a single form factor. That reduced the need for multiple devices and lowered the burden of gathering separate data streams during care delivery. The type mix also reflects where budget holders see the greatest practical return, since higher unit costs can still be acceptable when device consolidation improves workflow. In the medical smart textile industry, procurement decisions in higher-acuity settings continue to favor products that can replace several monitoring steps at once.

Active Smart Textiles are projected to grow at a 14.38% CAGR from 2026 to 2031, which makes them the fastest-moving type category in the medical smart textile market. Their growth is tied to products that do more than sense, including systems designed for rehabilitation support, therapeutic response, and other closed-loop functions. Passive Smart Textiles remain relevant in compression therapy, antimicrobial wound dressings, and positioning aids, where long wear life and lower cost matter more than embedded intelligence. A 2025 paper in npj Flexible Electronics outlined the material and structural requirements for textile-based therapeutic systems across electrical, thermal, and chemical modalities, which supports continued development in more responsive smart formulations. Over time, the boundary between Active and Ultra-Smart Textiles is likely to narrow as programmable features move into broader price ranges. That shift would keep the medical smart textile market focused on function and clinical use rather than on rigid category labels alone.

By Technology: Wearable technology leads, while biomedical wearables move fastest

Wearable Technology commanded 38.24% revenue share in 2025, which made it the largest technology segment in the medical smart textile market. Its lead came from the commercial maturity of garment-based health monitors across cardiopulmonary tracking, activity monitoring, and sleep-related observation in both clinical and home settings. Adoption favored this segment because garments usually fit patient routines better than separate devices or adhesive formats. Providers also benefited because wearable garments could support longer observation windows with less patient handling. That combination of ease of use and expanding clinical relevance kept Wearable Technology at the center of demand.

Biomedical Wearables are forecast to grow at a 14.52% CAGR from 2026 to 2031, the fastest pace within the technology split of the medical smart textile market. Growth here is tied to disease-specific uses that require more focused measurement, therapeutic response, or diagnostic support than broader wearable products. Textile Sensors and E-Textiles are increasingly functioning as enabling layers within larger systems rather than as standalone revenue categories, which compresses their direct sales visibility while widening their role in the value chain. Smart Fabrics continue to serve important specialty uses, including antimicrobial hospital apparel and thermal regulation applications. Research published in Nature in February 2025 described a single-fibre computer capable of distributed inference inside textile networks, which suggests that sensing and processing may become more tightly linked during the forecast period. As that happens, the medical smart textile market is likely to reward companies that can integrate material science, signal processing, and device usability into one product architecture.

By Application: Bio-monitoring anchors demand, while wound care and drug delivery open the fastest path

Bio-Monitoring accounted for 43.52% of the medical smart textile market size within the application split in 2025, reflecting the stronger clinical history behind cardiac, respiratory, and motion-based textile sensing. Hospitals, outpatient programs, and clinical research settings already had clearer use cases for continuous observation, which helped this segment keep the largest revenue base. The application also benefited from a growing record of device clearances that lowered perceived reimbursement and adoption risk. Hexoskin’s November 2025 FDA 510(k) clearance for long-term ambulatory ECG and respiratory monitoring reinforced that position by adding another clinically usable smart garment to the approved base[3]Hexoskin, “A Breakthrough in Remote Care: Hexoskin Medical System Receives FDA 510(k) Clearance for Long-Term ECG and Respiratory Monitoring,” Hexoskin, hexoskin.com. In the medical smart textile industry, bio-monitoring therefore remains the segment with the clearest bridge between technical capability and payment relevance.

Wound Care and Drug Delivery is expected to grow at a 15.25% CAGR from 2026 to 2031, which makes it the fastest-growing application in the medical smart textile market. Growth here is tied to closed-loop products that can sense wound conditions and respond through localized therapy within the same substrate. A 2025 Nature Communications study reported a skin-interfaced three-dimensional closed-loop sensing and therapeutic electronic wound bandage tested in a clinical cohort of 10 patients, showing how personalized wound management can be built into textile-linked systems. Surgery and Rehabilitation remain smaller but technically demanding applications because they require sterilizability, signal stability, and material compliance beyond what many general monitoring products need. Therapy and Wellness also continues to connect clinical and consumer use cases, which helps garment-based monitoring fit outcome-oriented care models rather than only reactive treatment. If major wound care suppliers start pairing smart dressings with remote nursing support, the medical smart textile market could see application boundaries and end-user boundaries shift together before 2031.

By End User: Hospitals remain largest, but growth is moving toward the home

Hospitals and Clinics retained 54.34% of end-user revenue in 2025, which kept them the largest demand center in the medical smart textile market. Their lead reflects purchasing scale as well as concentration of higher-acuity uses such as intraoperative monitoring, ICU telemetry, and post-surgical surveillance. Institutional buyers also served as the first commercial channel for many products because clinical validation requirements pushed adoption through formal procurement systems before wider consumer or home uptake. That pattern favored hospital settings where staff could evaluate performance, integrate data, and support early protocol design. It also explains why the largest current demand still sits inside organized care environments rather than fully decentralized settings.

Home Healthcare and Patients are projected to grow at a 16.15% CAGR through 2031, which makes this the fastest-growing end-user segment in the medical smart textile market. The shift is being supported by discharge pressure, payer demand for ongoing surveillance, and payment models that recognize technology-supported chronic care in residential settings. Rehabilitation Centers are also expanding as stroke recovery, orthopedic care, and neurodegenerative disease management move toward outpatient and home-based protocols that benefit from continuous motion and neuromuscular tracking. Academic and Industrial Research remains important because university labs and contract research settings generate the evidence base that later shapes hospital and home procurement. Companies are increasingly trying to connect institutional rehabilitation and home rehabilitation with continuous sensing platforms so that monitoring can continue without a break after discharge. That direction supports a broader medical smart textile market where long-term value comes from continuity of care rather than from isolated device episodes.

Geography Analysis

North America held 38.22% of the medical smart textile market share in 2025, which made it the largest regional contributor. The region’s lead rests on a stronger FDA clearance pipeline, wider use of remote physiological monitoring, and reimbursement structures that increasingly support wearable-enabled chronic care. The United States remains the main engine because product clearance activity and payment alignment are both more developed than in most other markets. Canada adds an innovation layer through companies such as Hexoskin and Myant, which continue to work with institutional research partners while selling into broader international healthcare programs.

Europe remained the second-largest geography in the medical smart textile market and also one of the most regulation-heavy. Germany, the United Kingdom, France, and the Nordic countries form the strongest adoption cluster because they combine digital health infrastructure, preventive care focus, and established textile and medical technology capabilities. Germany stands out for its industrial depth, and KOB GmbH has built a dedicated smart medical textiles team while maintaining international research collaborations. The European Commission and Euratex launched the Textiles of the Future partnership in 2025 with EUR 60 million, or USD 64.80 million, committed through 2030, which supports innovation momentum even as EU MDR compliance continues to shape commercial priorities.

Asia-Pacific is forecast to expand at a 15.65% CAGR through 2031, the fastest regional rise in medical smart textile market size. The region benefits from strong demographic demand and manufacturing scale at the same time, which few other geographies can match. Japan has one of the world’s oldest populations, which supports continuous home monitoring demand and gives clinically validated smart garments a clear place in aging care programs. The region also has strong materials capability because companies such as Toray Industries and Asahi Kasei supply specialty fibers that support smart textile platforms globally. China contributes large-scale conductive-fiber manufacturing, which improves cost positions for broader product tiers. South Korea is also becoming more relevant as its device regulation environment matures in step with other major frameworks. South America and the Middle East and Africa remain earlier-stage opportunities, with Brazil and GCC countries acting as the first visible growth points as healthcare infrastructure and digital health coverage continue to improve.

Competitive Landscape

The medical smart textile market remains moderately fragmented and shows a clear split between diversified medtech groups, specialist smart textile firms, and upstream material suppliers. Large companies are generally not building the entire category alone from the ground up. Instead, they are using partnerships, distribution arrangements, and targeted acquisitions to enter adjacent monitoring spaces more quickly. That pattern reflects the advantage that specialized developers still hold in rapid iteration, garment design, and early regulatory navigation.

Medtronic’s distribution agreement for the Corsano multi-parameter wearable shows how large device companies are trying to extend their reach across hospital and home monitoring without waiting for slow internal development. Johnson & Johnson’s completed acquisition of Atraverse Medical in Q2 2026 points to a similar approach, where procedural and cardiovascular capability is expanded through deal activity rather than only through organic build-out. DuPont’s work with technology partners around conductive material solutions shows that upstream suppliers can benefit from category expansion without carrying the full device-level regulatory burden. Schoeller Textil AG and Toray Industries occupy similar positions because they support downstream smart garment growth through functional textile inputs rather than through direct clinical device competition.

Specialist companies such as Hexoskin, Myant, Chronolife, and Siren Care compete more on clinical validation depth, niche application focus, and regulatory positioning than on sheer scale. Their challenge is that every new indication can require expensive trial work, which raises a cost burden that small firms often feel more strongly than diversified groups. The same issue shapes the broader medical smart textile market because new use cases do not become durable revenue streams until they are backed by reimbursement-ready evidence. Research published in Nature in February 2025 on single-fibre computers and work published in npj Biomedical Innovations on adaptive bioelectronic wound therapy both point toward a next stage where sensing, inference, and response are more tightly integrated inside textile systems. That means the most durable positions may go to companies that can process signals closer to the garment, reduce dependence on perfect connectivity, and fit more smoothly into home environments. White space still remains in intraoperative smart draping, pediatric monitoring garments, and textile-based neurostimulation for chronic pain, where no company has yet built a clearly dominant position.

Medical Smart Textile Industry Leaders

Sensoria Health

DuPont de Nemours, Inc.

Toray Industries, Inc.

Hexoskin

AiQ Smart Clothing Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Researchers at Georgia Tech launched a pilot of smart-fabric pressure-sensing sheets at Children's Healthcare of Atlanta to detect bedsore risk via flexible, reusable sensors embedded in crib sheets and connected to a monitoring app. The team aims to expand to 50 cribs and seek regulatory clearance to market to hospitals and nursing homes within two years.

- February 2026: A textile-based alignment-free electrophysiological sensing sleeve enabling comprehensive cardiovascular monitoring in real-world conditions was published in Microsystems & Nanoengineering, advancing the case for ambulatory cardiac surveillance without adhesive sensors.

Global Medical Smart Textile Market Report Scope

As per the scope of the report, a Medical Smart Textile is a type of fabric integrated with advanced technologies that enable it to monitor, respond to, or enhance health-related functions. These textiles can incorporate sensors, conductive materials, or other electronic components to track physiological parameters such as heart rate, temperature, or movement, providing real-time health data and improving medical care or patient comfort.

The segmentation of the medical smart textile market is categorized by type, technology, application, end user, and geography. By type, the market is divided into passive smart textiles, active smart textiles, and ultra-smart textiles. By technology, it includes textile sensors, smart fabrics, wearable technology, e-textiles, and biomedical wearables. By application, the market covers bio-monitoring, surgery, therapy and wellness, rehabilitation, and wound care and drug delivery. By end user, it is segmented into hospitals and clinics, academic and industrial research, home healthcare and patients, and rehabilitation centers. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Passive Smart Textiles |

| Active Smart Textiles |

| Ultra-Smart Textiles |

| Textile Sensors |

| Smart Fabrics |

| Wearable Technology |

| E-Textiles |

| Biomedical Wearables |

| Bio-Monitoring |

| Surgery |

| Therapy and Wellness |

| Rehabilitation |

| Wound Care and Drug Delivery |

| Hospitals and Clinics |

| Academic and Industrial Research |

| Home Healthcare and Patients |

| Rehabilitation Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Passive Smart Textiles | |

| Active Smart Textiles | ||

| Ultra-Smart Textiles | ||

| By Technology | Textile Sensors | |

| Smart Fabrics | ||

| Wearable Technology | ||

| E-Textiles | ||

| Biomedical Wearables | ||

| By Application | Bio-Monitoring | |

| Surgery | ||

| Therapy and Wellness | ||

| Rehabilitation | ||

| Wound Care and Drug Delivery | ||

| By End User | Hospitals and Clinics | |

| Academic and Industrial Research | ||

| Home Healthcare and Patients | ||

| Rehabilitation Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current and forecast value of the medical smart textile market?

The medical smart textile market stood at USD 2.25 billion in 2025, reaches USD 2.55 billion in 2026, and is forecast to reach USD 4.82 billion by 2031 at a 13.56% CAGR.

Which application leads revenue in medical smart textiles?

Bio-Monitoring leads the application mix with 43.52% revenue share in 2025, supported by stronger clinical validation and a growing base of approved monitoring garments.

Which end-user group is expanding the fastest?

Home Healthcare and Patients is the fastest-growing end-user segment, with a 16.15% CAGR through 2031, as discharge pressure and connected care reimbursement move monitoring into residential settings.

Which region leads and which region grows fastest?

North America held 38.22% share in 2025, while Asia-Pacific is projected to expand at a 15.65% CAGR through 2031, driven by aging populations and manufacturing depth.

What is pushing adoption of smart medical textiles in healthcare?

Remote patient monitoring demand, easier reimbursement for connected care, and better miniaturization and washability are all strengthening adoption across hospital, rehabilitation, and home-based care.

What is slowing wider commercialization?

The biggest barriers are high validation costs, difficult washability and durability testing, and regulatory complexity across medical device, software, and textile standards.

Page last updated on: