Medical Footwear Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

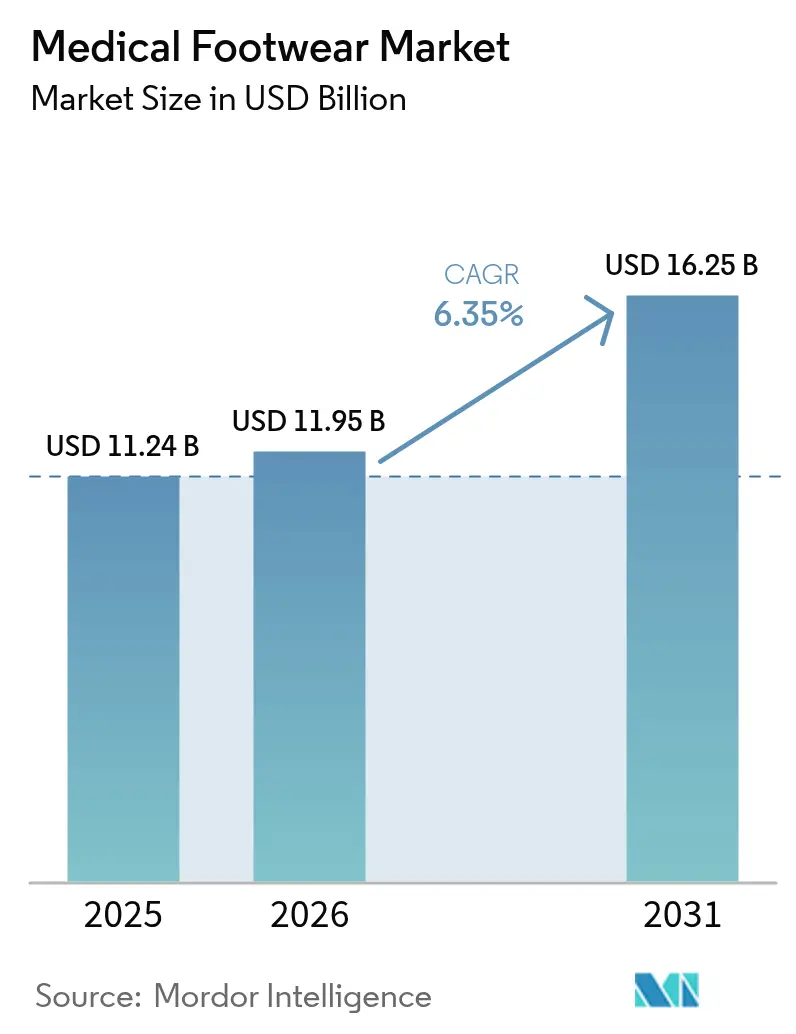

| Market Size (2026) | USD 11.95 Billion |

| Market Size (2031) | USD 16.25 Billion |

| Growth Rate (2026 - 2031) | 6.35% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Footwear Market Analysis by Mordor Intelligence

The medical footwear market size was valued at USD 11.24 billion in 2025 and estimated to grow from USD 11.95 billion in 2026 to reach USD 16.25 billion by 2031, at a CAGR of 6.35% during the forecast period (2026-2031). Growth rests on three pillars: the continuing rise in diabetes cases, rapid gains in additive manufacturing, and wider insurance recognition of therapeutic shoes as preventive devices. In 2024, North America held the lead thanks to insurance coverage for diabetic shoes, while Asia-Pacific delivered the quickest expansion as urbanization and e-commerce improved access. Manufacturers are also benefiting from improved FDA guidance that accelerates product approvals and fuels global export opportunities. At the same time, smart-sensor insoles and bio-based antimicrobial materials are elevating performance expectations for clinicians and consumers alike.

Key Report Takeaways

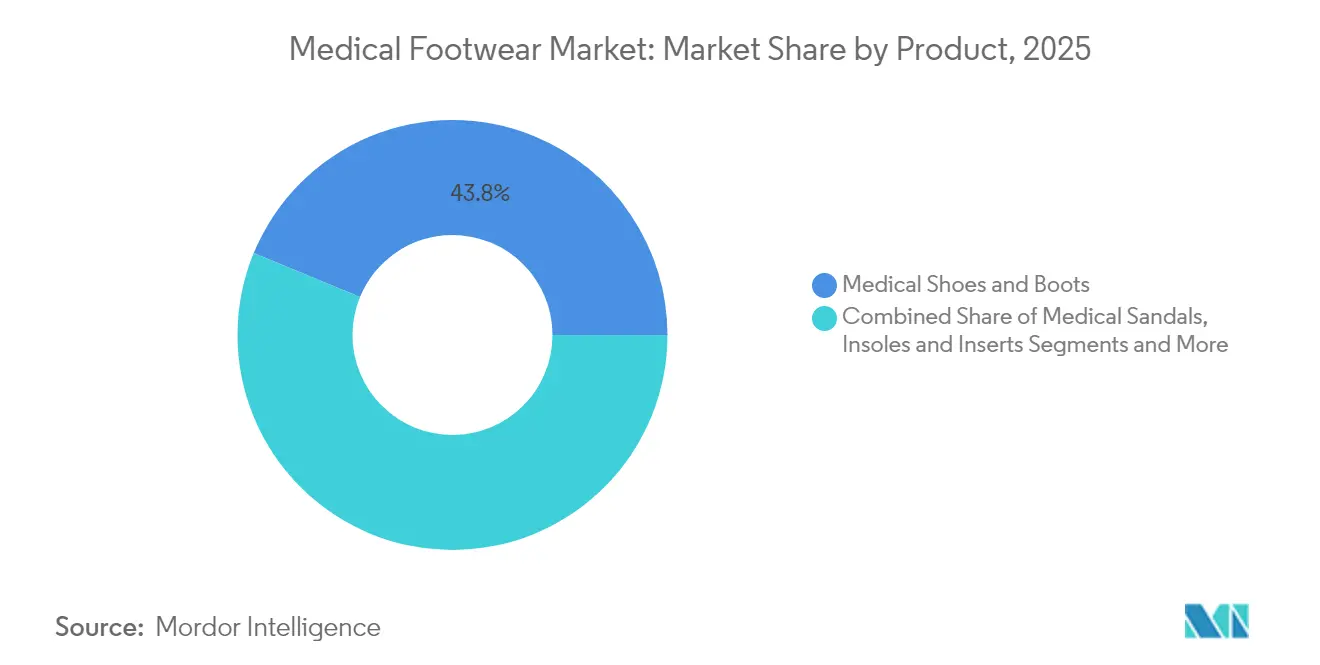

- By product category, medical shoes and boots led with 43.78% revenue share in 2025; insoles and inserts are projected to expand at a 9.54% CAGR to 2031.

- By medical condition, diabetes accounted for 67.72% of the medical footwear market share in 2025, while plantar fasciitis treatments record the highest projected CAGR at 7.28% through 2031.

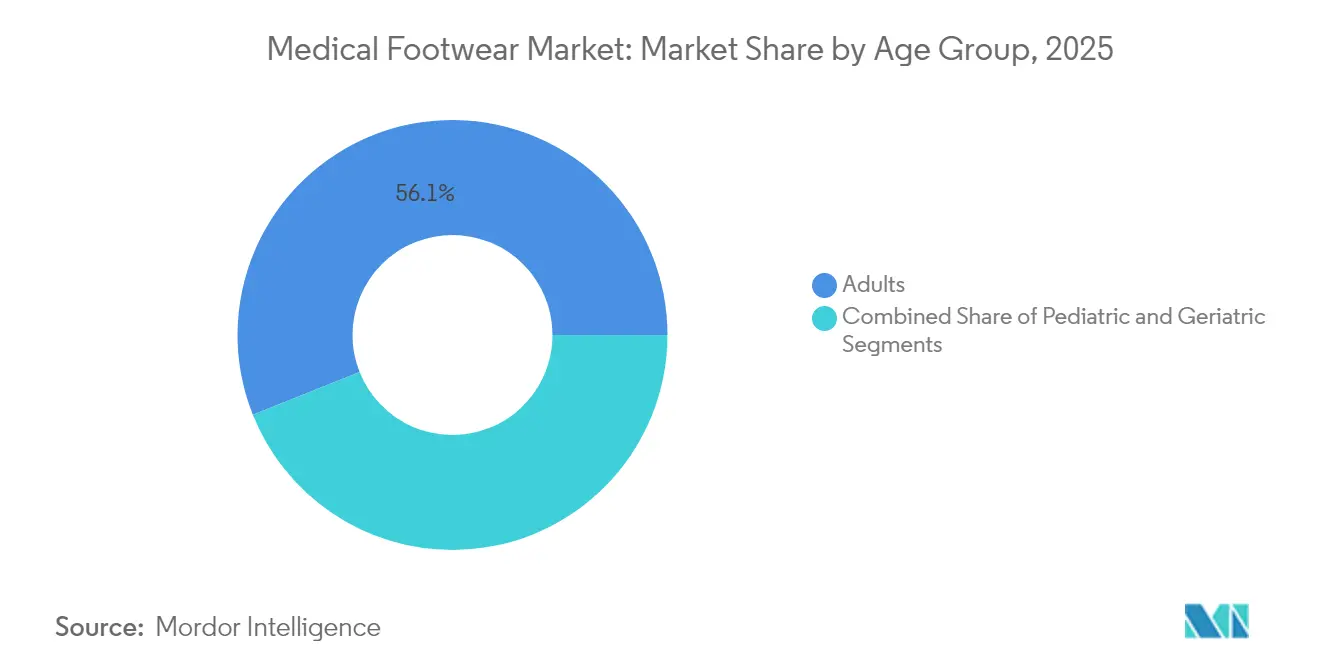

- By age group, adults 18-60 captured 56.05% share of the medical footwear market size in 2025; the geriatric population is advancing at a 8.86% CAGR through 2031.

- By distribution channel, specialty stores and clinics held 60.12% share in 2025, whereas online platforms are set to grow at a 10.19% CAGR to 2031.

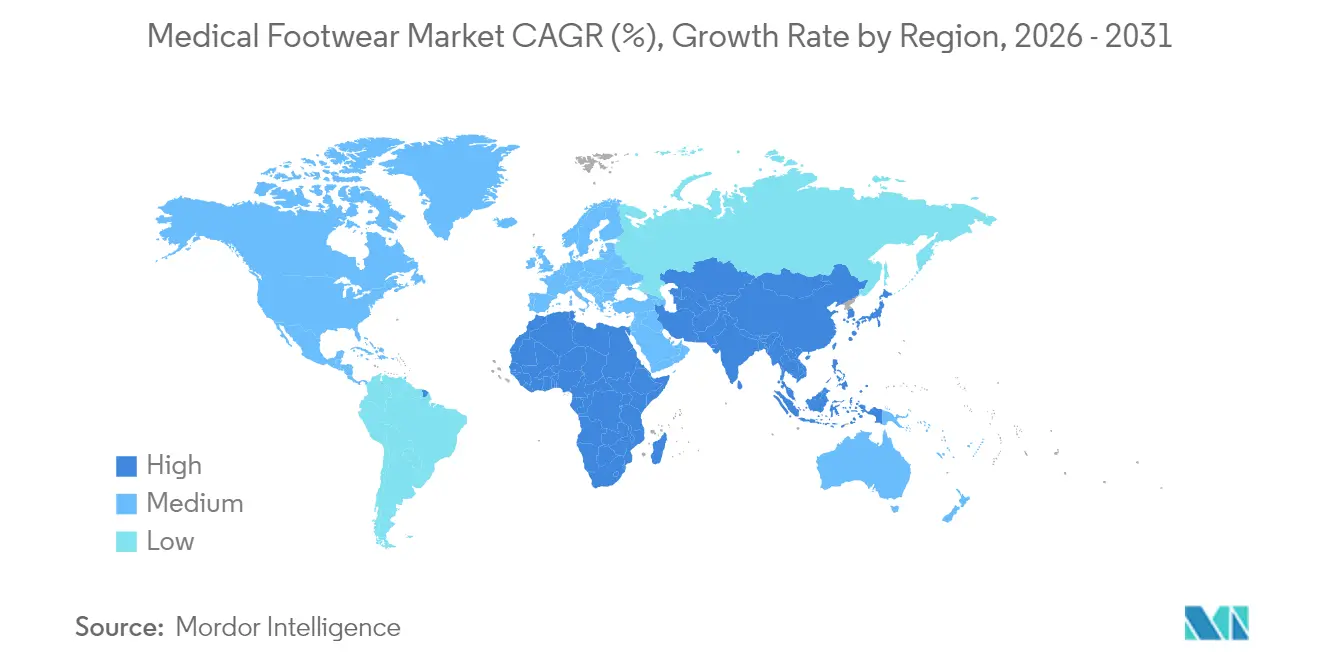

- By geography, North America commanded 33.08% share in 2025; Asia-Pacific is forecast to accelerate at an 8.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Footwear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Diabetes & Foot-Related Disorders | +1.8% | Global, with highest impact in North America & APAC | Long term (≥ 4 years) |

| Ageing Population Driving Orthopaedic Needs | +1.5% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Technological Advances In Custom 3-D Printed Orthotics | +1.2% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| E-Commerce Expansion Improving Product Accessibility | +0.9% | Global, with early gains in North America & Europe | Short term (≤ 2 years) |

| Integration Of Smart Sensors For Remote Patient Monitoring | +0.7% | Developed markets, pilot programs in emerging economies | Medium term (2-4 years) |

| Bio-Based Antimicrobial Materials Boosting Sustainability | +0.4% | Europe & North America, spreading globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Diabetes and Foot Disorders

The accelerating diabetes burden keeps the medical footwear market at the center of preventive care strategies. Worldwide, diabetic foot ulcers affect 6.3% of patients and cost the U.K. NHS USD 7,800 per ulcer case.[1]Ahmad H. Alghadir, “Prevalence of Peripheral Neuropathy, Amputation, and Quality of Life in Patients with Diabetes Mellitus,” nature.com Evidence shows that 44.4% of patients have peripheral neuropathy and 21.7% progress to amputation, establishing clear clinical benefits for protective footwear. U.S. researchers created a pressure-alternating insole that improves blood flow, directly tackling ulcer risk for 39 million Americans.[2]Muthu B. J. Wijesundara, “Shoe Technology Reduces Risk of Diabetic Foot Ulcers,” sciencedaily.com Ill-fitting shoes raise ulcer odds by more than 10 times, while studies confirm 50-80% of infections are preventable with proper footwear wjgnet.com. As insurers focus on cost offsets, therapeutic shoes move from discretionary purchase to essential medical device within the medical footwear market.

Ageing Population Driving Orthopaedic Needs

Population ageing is amplifying demand for orthopedic footwear across all developed regions. In 2024, 81% of Americans reported foot pain, reflecting both lifestyle shifts and longer lifespans. Colombia expects 39,270 lower-limb arthroplasty procedures by 2050, with women requiring roughly twice as many surgeries as men—a signal that gender-specific designs have a clear audience. Older adults face purchase barriers such as travel costs and complex insurance coding, creating space for mobile fitting services and subscription models. Design studies on fall prevention highlight wider heels, low profiles, and firm midsoles as critical for stability. These findings guide suppliers as they tailor ranges for seniors within the medical footwear market.

Technological Advances in Custom 3-D Printed Orthotics

Additive manufacturing is redefining speed and scope of customization. Engineers now 3-D print ankle braces for Charcot-Marie-Tooth patients, producing precise fits that conventional molding cannot match.[3]Difei Lu, “Insoles Treated with Bacteria-Killing Nanotechnology Bio-Kil Reduce Bacterial Burden,” ncbi.nlm.nih.gov A new spacer technique delivers insoles with gradual stiffness zones and scan-to-print workflows, cutting cost and production time. Embedded sensors track force and center of pressure with error rates below 9%, rivaling laboratory equipment at a fraction of the price. These innovations shorten design cycles and widen access, especially in emerging markets that lack extensive orthotic labs. The result is a faster-moving, high-specification medical footwear market.

E-Commerce Expansion Improving Product Accessibility

Digital commerce is breaking geographic barriers for the medical footwear market. FDA programs launched in 2024 reduce approval timelines for connected devices, positioning U.S. innovators for global reach. Direct-to-consumer websites bundle educational videos, virtual size guides, and tele-podiatry consults, reducing reliance on physical store visits. Consumer surveys show that 88% of Americans now shop with foot-pain relief in mind, spending USD 228 per month on associated care. COVID-19 turbo-charged online adoption, making e-commerce a permanent fixture in device procurement. Consequently, digital channels will exert outsized influence on pricing transparency and brand loyalty.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Of Specialised Medical Footwear | -1.1% | Global, most pronounced in emerging economies | Short term (≤ 2 years) |

| Limited Reimbursement In Emerging Economies | -0.8% | APAC, Latin America, MEA | Medium term (2-4 years) |

| Proliferation Of Counterfeit / Grey-Market Orthotics | -0.5% | Global, concentrated in unregulated markets | Long term (≥ 4 years) |

| Supply-Chain Bottlenecks For Medical-Grade Materials | -0.4% | Global, with regional variations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Specialised Medical Footwear

Affordability remains a headwind, particularly where households pay most healthcare costs. Indian studies show diabetic patients shoulder substantial out-of-pocket expenses, making price the deciding factor in shoe adoption. The Medicare coding maze inflates U.S. dispensing costs, as extra documentation raises clinic overheads. Therapeutic pairs can cost 300-500% more than regular shoes, limiting reach beyond insured or affluent demographics. As a result, lower-priced local brands and leasing models are gaining ground. Without cost relief, the medical footwear market risks leaving vast segments unserved.

Limited Reimbursement in Emerging Economies

Governments in many developing countries have not yet integrated preventive footwear into insurance packages. Complex billing codes for custom orthotics deter doctors from prescribing them, particularly when clinic administrators lack the capacity to process claims. Prediabetic adults, who account for over one-third of the population in some regions, rarely qualify for coverage despite clear prevention benefits. Adoption, therefore, hinges on donor programs, tiered pricing, or public-private partnerships. Until reimbursement frameworks mature, growth in the medical footwear market could trail clinical need.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Insoles Extend Innovation Frontiers

The medical footwear market size for shoes and boots stood at 43.78% revenue share in 2025, confirming their role as the default solution for complex pathologies. Demand remains stable among diabetics and post-surgical patients who require full-foot protection. Meanwhile, insoles and inserts show the fastest clip at a 9.54% CAGR, propelled by 3-D printed models that disperse plantar pressure and integrate force sensors. Research highlights insoles that combine 22 sensors with solar charging to warn wearers of loading anomalies. Antimicrobial nanocoatings such as Bio-Kil further differentiate premium inserts by lowering infection risk for ulcer-prone users.

Orthopaedic and post-operative shoes maintain a solid base linked to growing joint-replacement volumes and hospital protocols that specify rigid-sole footwear during recovery. Medical sandals gain traction in warm climates for low-level wound care and edema management. Slippers round out the line for at-home use during lengthy therapy cycles. As customization costs fall, suppliers can offer modular kits where insoles, uppers, and fastening systems match specific gait profiles, broadening consumer choice within the medical footwear market.

By Medical Condition: Plantar Fasciitis Gains Momentum

Diabetes continues to anchor demand, holding 67.72% share in 2025 on the strength of robust clinical guidelines that mandate protected footwear. Preventive shoes lower amputation risk, trimming expensive hospital stays and securing payer support. Yet plantar fasciitis is closing the gap with a 7.28% CAGR as awareness rises that 25% of sufferers experience severe pain and 61% report daily discomfort. Endoscopic plantar fasciotomy delivers 95% pain-free outcomes in six months, elevating the need for supportive shoes during rehabilitation.

Arthritis and osteoporosis shoes gain incremental volume as population ageing accelerates, with orthopaedists recommending designs featuring wide toe boxes and targeted cushioning. Sports injury footwear appeals to a growing cohort of amateur athletes who seek quick returns to activity and value integrated sensor feedback. Wound-care footwear remains a niche but vital category tied directly to surgical throughput. The diversification of conditions served enhances resilience in the medical footwear market.

By Age Group: Seniors Propel Future Uptake

Adults aged 18-60 remain the core buyers, accounting for 56.05% of 2025 revenue. Workplace standing and fitness routines drive prophylactic purchases. Health plans that emphasize preventive orthotics further sustain this cohort’s spending. However, the geriatric segment posts 8.86% CAGR to 2031, outpacing all others as longevity rises. Studies prove that stability-focused shoe designs cut fall risk among older adults, prompting caregivers to budget for high-traction outsoles and firm heel counters.

Pediatric demand is modest but strategic. Custom braces for conditions like Charcot-Marie-Tooth disease illustrate how 3-D printing yields lightweight, child-friendly designs. Across all ages, the focus shifts from passive cushioning to dynamic support that adapts as body weight and biomechanics change. This life-stage approach broadens the addressable audience for the medical footwear market.

By Distribution Channel: Digital Models Re-Shape Access

Specialty stores and clinics retained 60.12% of sales in 2025, supported by in-house gait labs and podiatry partnerships that validate fit. These outlets handle complex prescriptions and provide ongoing adjustments, sustaining their relevance despite higher costs. Online channels, however, are projected to post a 10.19% CAGR, reflecting consumer comfort with telehealth and virtual try-ons. Interactive measurement apps and AI size engines reduce return rates while widening geographic reach. Pharmacies and orthotic centers bridge the gap between clinical oversight and convenience, especially for ready-made inserts.

COVID-19 taught health systems to value remote solutions, and suppliers now integrate click-to-consult links on product pages. As insurers reimburse virtual visits, online sales will attract first-time users in rural and low-mobility populations. Diversified distribution safeguards revenue streams and helps companies meet the varied service expectations within the medical footwear market.

Geography Analysis

North America’s 33.08% stake in the medical footwear market reflects mature insurance coverage and deeply embedded diabetes management protocols. In the United States alone, 39 million people live with diabetes, many qualifying for Medicare-funded therapeutic shoes. Canadian public health data reveal that 80% of diabetes-related leg amputations are preventable through proper footwear, a statistic that underpins provincial funding schemes. Mexico’s expanding middle class is beginning to prioritize preventive shoe purchases, especially as private insurers widen podiatry benefits.

Asia-Pacific is the growth engine, charting an 8.67% CAGR through 2031. India’s large diabetic population and improving e-commerce logistics are unlocking latent demand despite reimbursement gaps. China and Japan leverage aging demographics and strong orthopaedic traditions to stimulate uptake of smart insoles and custom sandals. Regulatory harmonization under the ASEAN Medical Device Directive promises smoother entry for foreign brands, provided they adapt to local price points. Innovative offloading devices such as the Mandakini system demonstrate how indigenous solutions can flourish when global designs remain unaffordable.

Europe delivers steady gains anchored by universal healthcare and long-standing orthopaedic craft. Germany and the United Kingdom lead clinical research on sensorized footwear, while France and Italy expand geriatric fall-prevention programs that recommend stable shoes. Sustainability regulations create a conducive environment for bio-based uppers and recyclable midsoles. In contrast, the Middle East and Africa record modest but rising volumes as governments boost healthcare budgets and awareness campaigns emphasize diabetic foot care. Collectively these trends strengthen the worldwide footprint of the medical footwear market.

Competitive Landscape

The medical footwear market is moderately fragmented, with a mix of heritage orthopaedic brands, specialty diabetic-shoe makers, and tech-driven newcomers. Enovis Corporation’s EUR 800 million acquisition of LimaCorporate created a USD 1 billion platform that blends reconstructive surgery know-how with rehabilitation footwear, signalling a tilt toward integrated care offerings. Similar tie-ups could follow as firms chase economies of scale in R&D and distribution.

Technology remains the decisive differentiation lever. Companies that master 3-D printing and sensor fusion can deliver custom, data-rich products at consumer-friendly price points. FDA efforts to streamline premarket approvals encourage early adoption of smart insoles and antimicrobial fabrics. Yet market share still hinges on clinician endorsement, making evidence-backed performance claims crucial.

Direct-to-consumer startups leverage social media and subscription models to bypass clinic mark-ups, but they must invest heavily in clinical trials to satisfy regulators and insurers. Meanwhile, established players shore up margins with tiered product families and localized manufacturing to dodge supply-chain disruptions. Competition is expected to intensify as payers move toward outcomes-based contracts that reward devices proven to cut ulcer incidence and hospital stays. All told, the medical footwear industry is set for dynamic consolidation and innovation in equal measure.

Medical Footwear Industry Leaders

Drewshoe, Incorporated

Orthofeet Inc.

Enovis (Dr. Comfort)

DARCO International, Inc.

Clearwell Mobility Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Researchers at Queen Margaret University, Edinburgh developed a shoe that reduces trips and falls in people with stroke and multiple sclerosis.

- April 2025: Ohio State University unveiled a smart insole with 22 pressure sensors and solar panels that transmits gait data for early detection of plantar fasciitis and Parkinson’s disease, with commercialization expected within five years.

Global Medical Footwear Market Report Scope

Medical footwear is those that are specifically designed to support or accommodate the mechanics and structure of the foot, ankle, and leg, and they have several medically beneficial features and functions that separate them from everyday footwear.

The medical footwear market is segmented by product (medical shoes & boots, medical sandals, and other products), end-user (men and women), distribution channel (offline and online), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally.

The report offers the value (in USD) for the above segments.

| Diabetic Shoes & Boots |

| Orthopaedic/Post-Op Shoes |

| Medical Sandals |

| Insoles & Inserts |

| Other Products (Slippers, Flip-flops, etc.) |

| Diabetes |

| Arthritis & Osteoporosis |

| Plantar Fasciitis |

| Sports Injuries |

| Post-Operative / Wound-Care |

| Others (e.g., Neuropathy) |

| Pediatric (<18) |

| Adult (18-60) |

| Geriatric (>60) |

| Specialty Stores & Clinics |

| Pharmacies & Orthotic Centres |

| Online |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Diabetic Shoes & Boots | |

| Orthopaedic/Post-Op Shoes | ||

| Medical Sandals | ||

| Insoles & Inserts | ||

| Other Products (Slippers, Flip-flops, etc.) | ||

| By Medical Condition | Diabetes | |

| Arthritis & Osteoporosis | ||

| Plantar Fasciitis | ||

| Sports Injuries | ||

| Post-Operative / Wound-Care | ||

| Others (e.g., Neuropathy) | ||

| By Age Group | Pediatric (<18) | |

| Adult (18-60) | ||

| Geriatric (>60) | ||

| By Distribution Channel | Specialty Stores & Clinics | |

| Pharmacies & Orthotic Centres | ||

| Online | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the medical footwear market?

The market is valued at USD 11.95 billion in 2026.

Which region leads the medical footwear market?

North America holds the top spot with 33.08% revenue share in 2025.

Which product segment is expanding the fastest?

Insoles and inserts are growing at a 9.54% CAGR through 2031.

Why is plantar fasciitis a key growth area?

Rising awareness and high pain prevalence are driving a 7.28% CAGR for plantar fasciitis footwear solutions.

How are smart sensors changing medical footwear?

Embedded electronics provide real-time gait analysis, enabling earlier intervention and better clinical outcomes.

Page last updated on: