Medical Textile Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

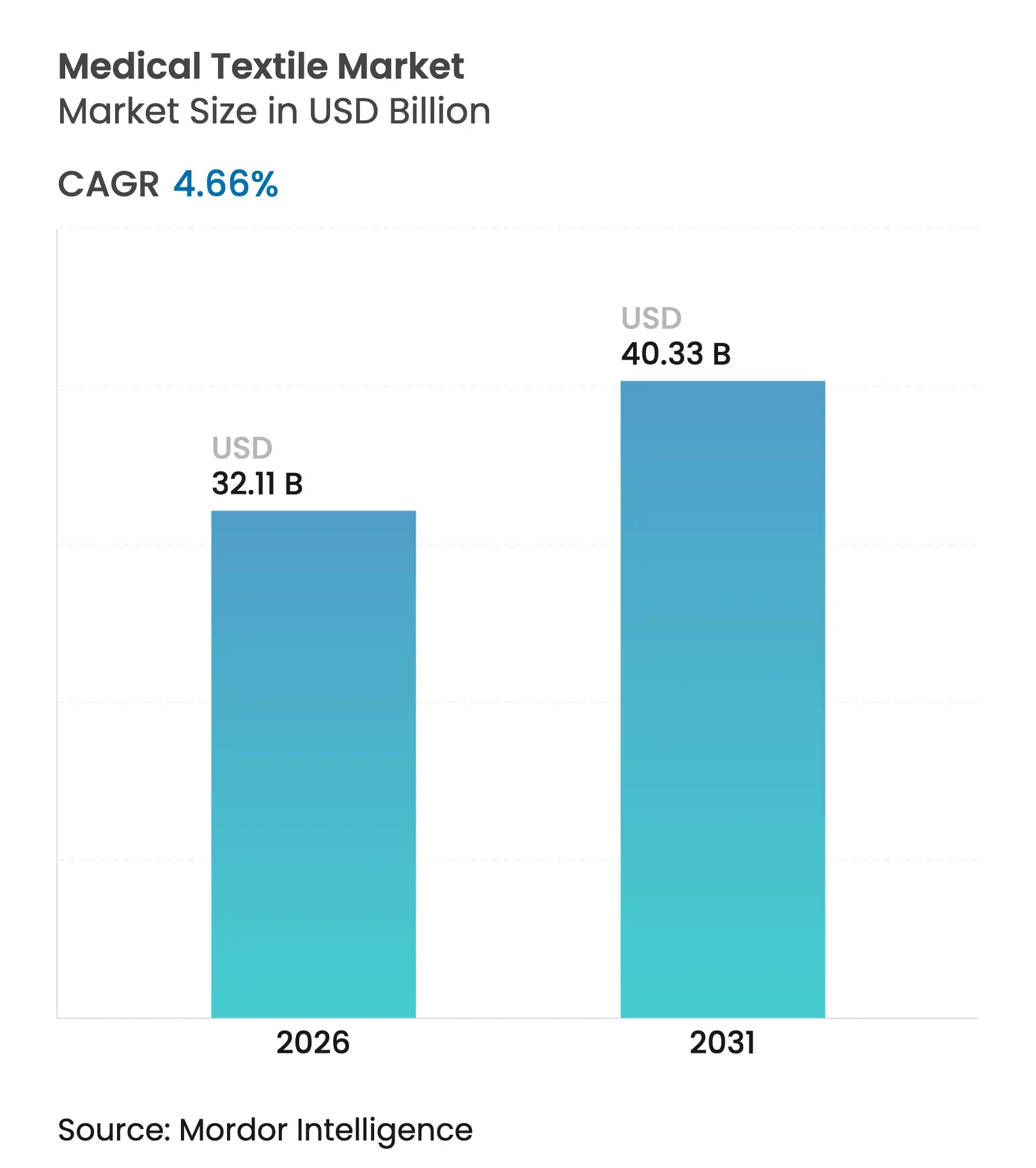

| Market Size (2026) | USD 32.11 Billion |

| Market Size (2031) | USD 40.33 Billion |

| Growth Rate (2026 - 2031) | 4.66 % CAGR |

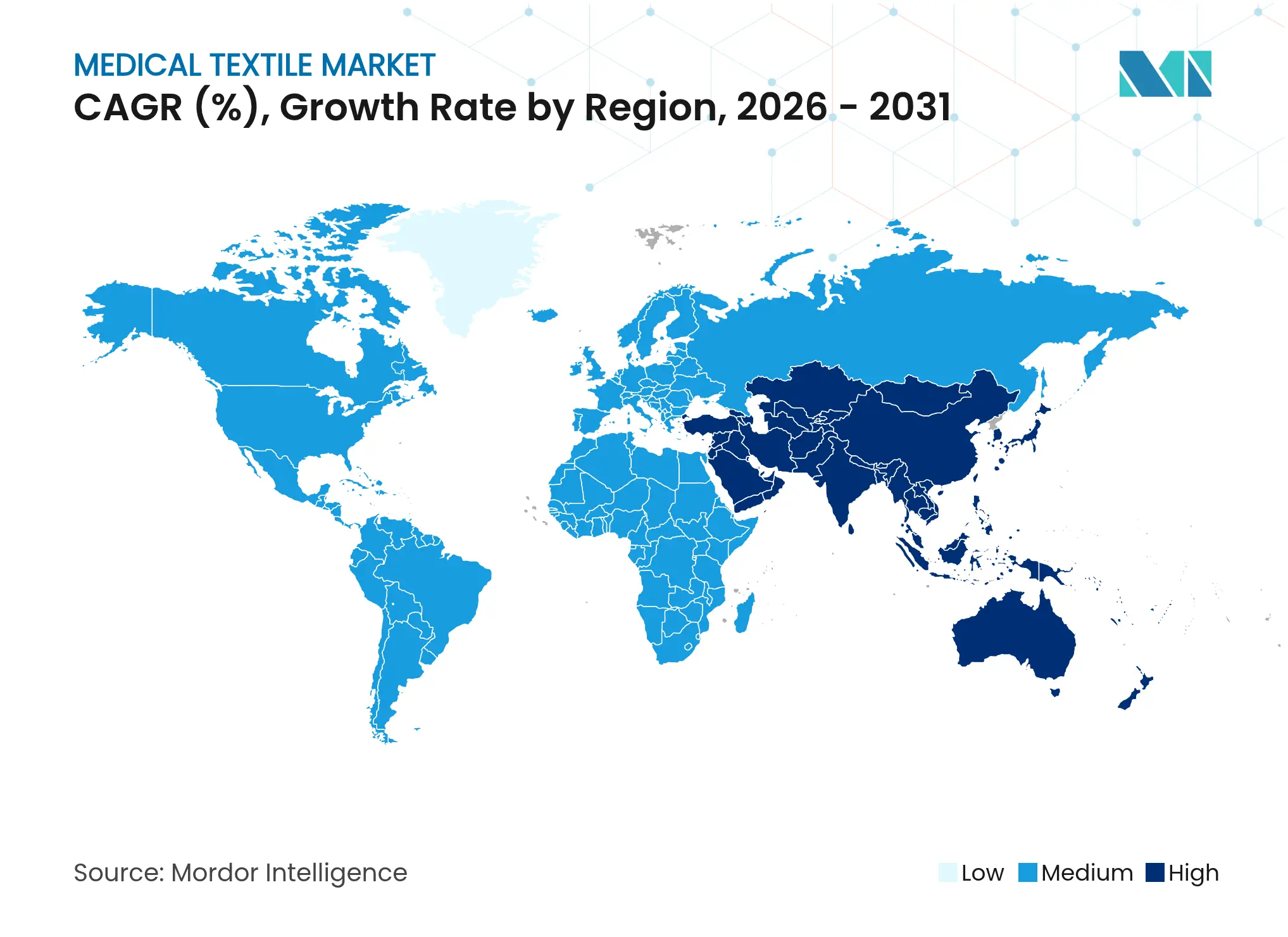

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Medical Textile Market Analysis by Mordor Intelligence

The expansion comes as procurement normalizes after pandemic surges and pivots toward structural forces such as regulatory mandates favoring single-use materials, chronic wound prevalence linked to aging populations, and the commercialization of antimicrobial coatings. Competitive positioning is shaped by moderate concentration, with integrated suppliers leveraging combined scale and specialty innovators targeting high-margin niches. Geographically, North America leads in installed capacity and product breadth, whereas Asia Pacific delivers the most rapid volume gains as governments channel capital into healthcare infrastructure and strategic stockpiles. Europe’s emerging PFAS restrictions and strict sustainability targets are beginning to reconfigure raw-material preferences and procurement criteria, an adjustment that may realign supplier share over the forecast period.

Key Report Takeaways

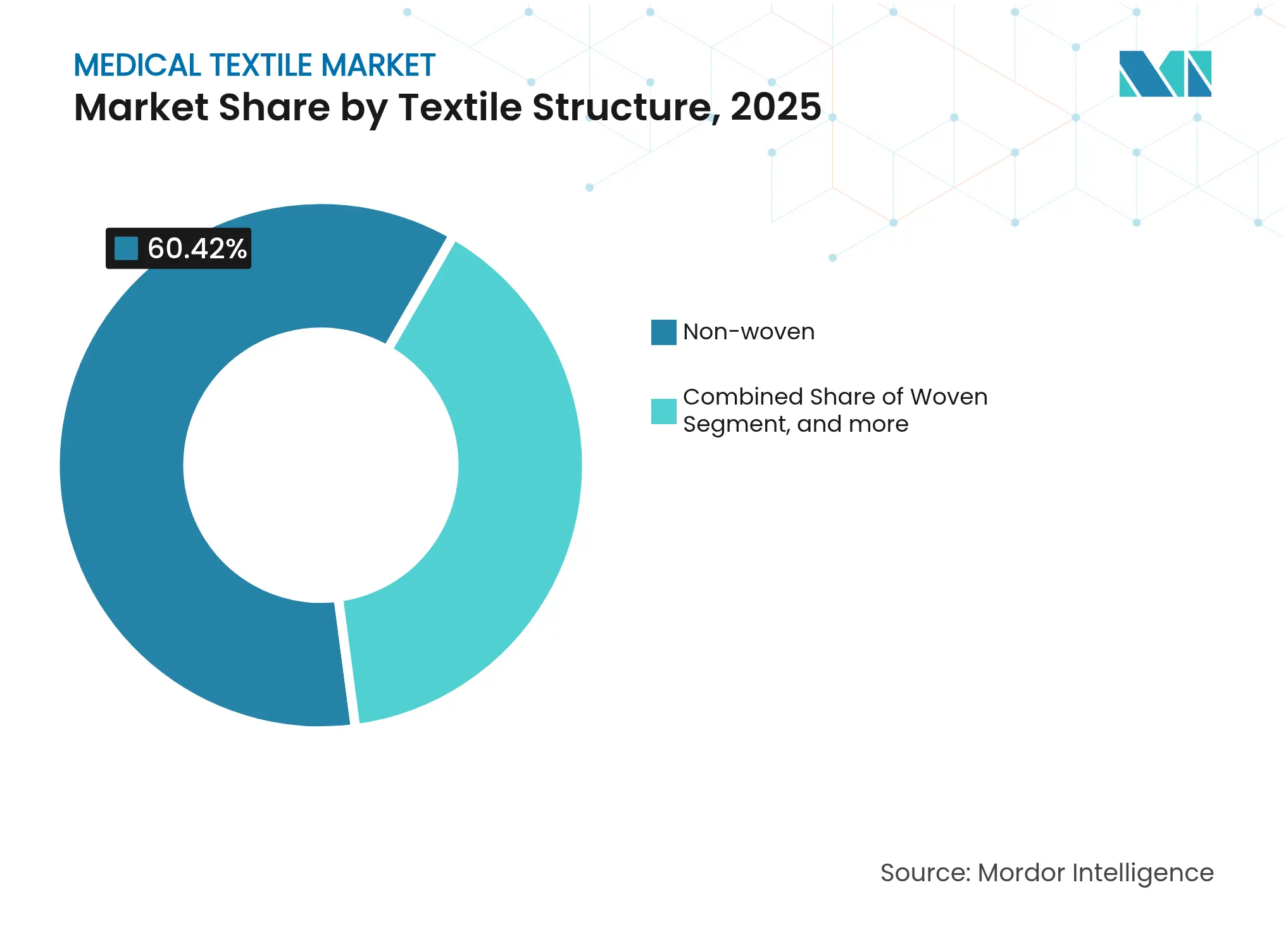

- By textile structure, non-wovens led with 60.42% of medical textile market share in 2025, while knitted materials are projected to expand at a 6.49% CAGR through 2031.

- By biodegradability, non-biodegradable products captured 73.85% share of the medical textile market size in 2025; biodegradable alternatives are set to advance at a 5.82% CAGR by 2031.

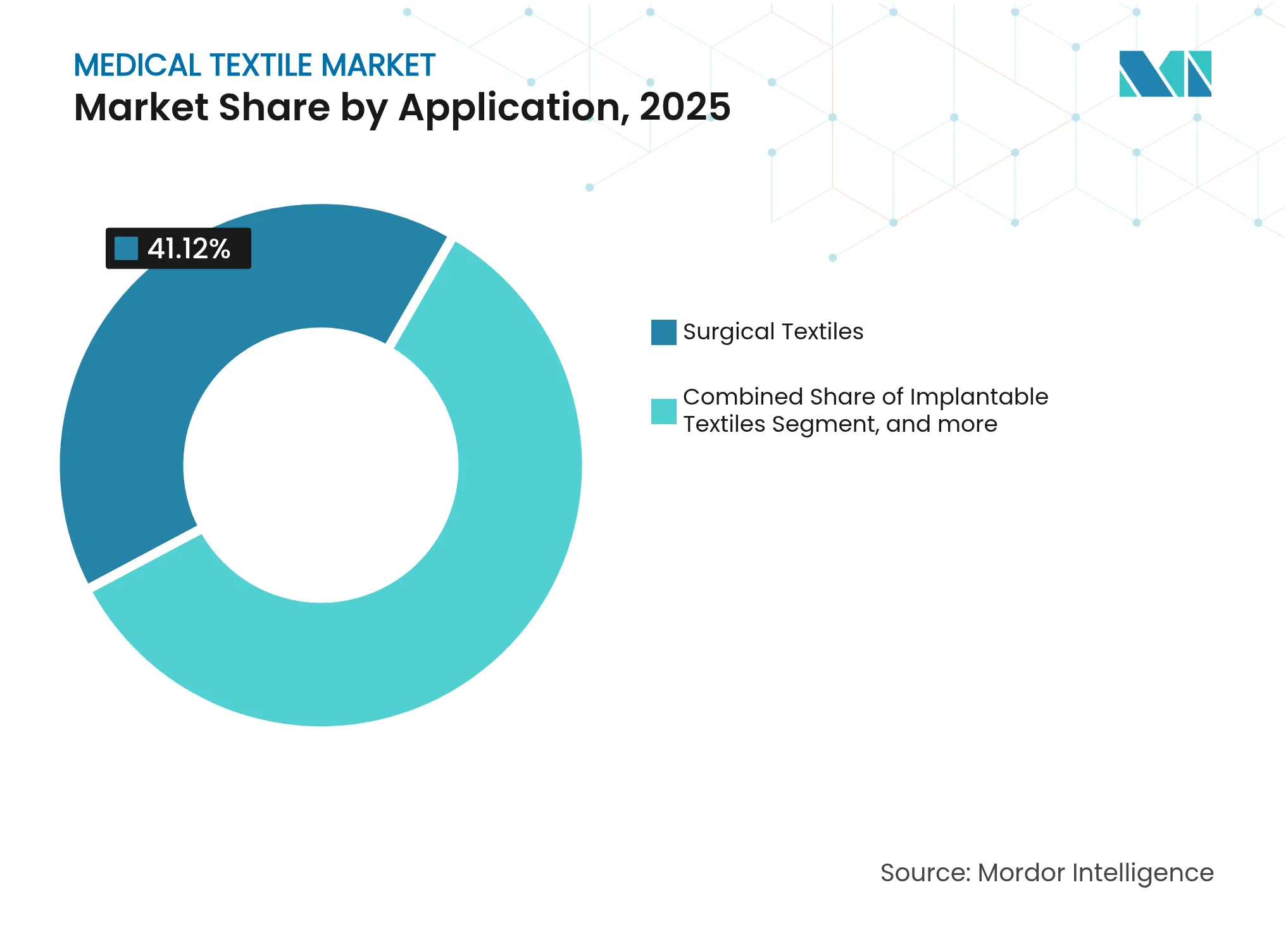

- By application, surgical textiles held 41.12% revenue share in 2025, whereas implantable textiles are pacing the field with an 7.74% CAGR through 2031.

- By end user, hospitals and clinics accounted for 57.49% of the medical textile market size in 2025, and ambulatory surgical centers are growing fastest at 6.86% CAGR to 2031.

- By geography, North America commanded 33.62% medical textile market share in 2025; Asia Pacific is on track for a 7.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Textile Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Regulatory

Push for Single-Use Non-Woven Drapes & Gowns

Regulatory

Push for Single-Use Non-Woven Drapes & Gowns

| +0.8% | Global, with strongest enforcement in North America & EU | Medium term (2-4 years) |

(~) %

Impact on CAGR Forecast

:

+0.8%

|

Geographic

Relevance

:

Global, with

strongest enforcement in North America & EU

|

Impact

Timeline

:

Medium term

(2-4 years)

|

Aging

Population Driving Chronic Wound Prevalence

Aging

Population Driving Chronic Wound Prevalence

| +1.2% | Global, concentrated in developed markets | Long term (≥ 4 years) | |||

Smart

Antimicrobial Coatings Reaching Commercial Scale

Smart

Antimicrobial Coatings Reaching Commercial Scale

| +0.9% | North America & EU leading, APAC adoption following | Short term (≤ 2 years) | |||

Hospital

Sustainability Programs Favouring Bio-Based Fibers

Hospital

Sustainability Programs Favouring Bio-Based Fibers

| +0.5% | EU leading, North America following | Long term (≥ 4 years) | |||

Sports

Orthopedics Boom in Emerging Markets

Sports

Orthopedics Boom in Emerging Markets

| +0.6% | APAC core, spill-over to Latin America | Medium term (2-4 years) | |||

Military

& Disaster-Relief Stockpiling

Military

& Disaster-Relief Stockpiling

| +0.4% | APAC core, MEA emerging | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Regulatory Push for Single-Use Non-Woven Drapes & Gowns

Post-pandemic infection-control updates from the U.S. FDA in 2024 tightened barrier-efficacy thresholds for surgical drapes, solidifying demand for polypropylene-based non-wovens. Parallel provisions under the EU Medical Device Regulation now impose higher validation protocols for reusable fabrics, disincentivizing multi-use systems. Hospitals respond by standardizing single-use kits, pushing bulk tenders toward integrated suppliers. The resulting volume visibility supports capacity additions across staple-fiber melt-blown lines in North America. Incumbents benefit from locked-in approved-supplier lists that raise entry barriers for low-cost competitors.

Aging Population Driving Chronic Wound Prevalence

The global rise in diabetes and vascular disease increases chronic wound incidence, directly lifting consumption of advanced dressings that rely on activated-carbon cloth and silver-impregnated fabrics. Home-health adoption climbs as seniors seek self-care solutions, boosting sales of compression garments and easy-apply dressings. Asia Pacific, led by Japan and South Korea, experiences the fastest incremental demand yet still depends on imports, widening the addressable market for foreign producers. Suppliers positioned in antimicrobial and moisture-management technologies realize premium margins as clinical outcomes drive formulary inclusion.

Smart Antimicrobial Coatings Reaching Commercial Scale

Nanocomposite coatings incorporating magnesium-enriched polyurethane deliver infection-resistant properties without antibiotics, reducing the risk of resistance development.[1]Phys.org Staff, “Magnesium-Enriched Polyurethane Nanofibers Show Antimicrobial Strength,” phys.org Patent filings for biomedical textiles surpassed 113,000 in 2024, signaling a race to secure intellectual-property territory.[2]PLOS ONE Editors, “Patent Landscape for Biomedical Textiles,” journals.plos.org Early adopters monetize through value-based pricing to hospitals seeking lower post-operative infection rates. Pilot orders in North America validate scale-up economics, prompting contract expansions with OEM gown assemblers. Regulatory approvals for coating chemistries shorten as data accumulate, compressing time-to-market for second movers.

Hospital Sustainability Programs Favoring Bio-Based Fibers

European procurement frameworks now score bids on lifecycle emissions, giving biodegradable fibers a selectable advantage.[3]European Commission, “Green Public Procurement Criteria for Textiles,” ec.europa.eu Polyhydroxyalkanoate (PHA) yarns produced via bacterial fermentation meet tensile thresholds while offering full compostability. Early-stage hospital pilots demonstrate waste-handling cost reductions once separate collection streams exist. Supplier credibility hinges on transparent chain-of-custody documentation, pushing certification demand under ISO 14067. The economic incentive combines reduced disposal fees with reputational value, accelerating commercialization pathways for bio-based innovators.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Stringent

Multi-Jurisdictional Biocompatibility Tests

Stringent

Multi-Jurisdictional Biocompatibility Tests

| -0.7% | Global, most stringent in EU and North America | Medium term (2-4 years) |

(~) %

Impact on CAGR Forecast

:

-0.7%

|

Geographic

Relevance

:

Global, most

stringent in EU and North America

|

Impact

Timeline

:

Medium term

(2-4 years)

|

Supply-Chain

Volatility in Medical-Grade Polypropylene

Supply-Chain

Volatility in Medical-Grade Polypropylene

| -0.9% | Global, with acute impact in APAC manufacturing hubs | Short term (≤ 2 years) | |||

Reimbursement

Gaps for Advanced Wound Dressings

Reimbursement

Gaps for Advanced Wound Dressings

| -0.5% | North America & EU primarily, emerging in APAC | Long term (≥ 4 years) | |||

Lack of

End-of-Life Recycling Infrastructure

Lack of

End-of-Life Recycling Infrastructure

| -0.3% | Global, most pronounced in developing markets | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Stringent Multi-Jurisdictional Biocompatibility Tests

Expanded ISO 10993 protocols and EU eIFU mandates oblige manufacturers to fund granular cytotoxicity and sensitization studies before market clearance. Parallel UDI harmonization links every SKU to the EUDAMED database, adding documentation overhead. Mid-tier firms redirect R&D funds to regulatory compliance, slowing pipeline velocity. Large incumbents view the hurdle as a moat protecting share, while smaller innovators partner with notified bodies to share validation costs. The cumulative delay lengthens commercial payback periods, limiting risk appetite for radical material science projects.

Supply-Chain Volatility in Medical-Grade Polypropylene

Medical-grade polypropylene capacity remains concentrated along petrochemical corridors vulnerable to weather and geopolitical disruption. Force majeure events in 2024 curtailed resin supply, inflating spot prices by more than 20% against contract baselines. Non-woven converters, unable to substitute resin grades without requalification, absorbed margin compression or rationed client allocations. Regional diversification strategies emerge, including backward integration into resin lines in the United States and joint-venture feedstock agreements in Southeast Asia. Inventory buffers, while mitigating immediate outages, elevate working-capital burdens and raise finished-good cost bases, dampening price competitiveness in tender cycles.

Segment Analysis

By Textile Structure: Knitted Innovation Drives Premium Growth

In 2025 non-wovens sustained 60.42% of medical textile market share, yet knitted solutions are poised for 6.49% CAGR expansion through 2031 as demand shifts toward compression garments, flexible supports, and sensor-embedded fabrics. Knitted interlock and rib patterns enable controlled elasticity essential for orthopedic bracing and sports therapy, whereas jersey constructions facilitate drape and patient comfort. The medical textile market size tied to knitted formats benefits from automation advances that cut change-over time and waste, thus lowering per-unit cost in short production runs. Concurrently, woven fabrics hold stable use in sutures and implant meshes, supplying dimensional stability but capturing limited incremental revenue. Braided structures remain niche, servicing vascular grafts that merit premium pricing due to exacting diameter tolerances.

Knitted producers leverage design software to integrate conductive yarn paths, allowing real-time pressure mapping and physiological monitoring, which underpins higher average selling prices. Material suppliers capitalizing on elastomeric blends and bioabsorbable fiber options differentiate on resilience and post-implant degradation profiles. Non-woven market incumbents invest in melt-blown capacity for commoditized drapes and gowns, banking on volume contracts to offset lower margins. The coexistence of commodity and specialty tiers indicates a bifurcated competitive field where operational scale and technical sophistication both secure defensible positions.

Note: Segment shares of all individual segments available upon report purchase

By Biodegradability: Sustainability Mandates Accelerate Bio-Based Adoption

Non-biodegradable products retained 73.85% of medical textile market share in 2025, yet biodegradable variants are advancing at a 5.82% CAGR, propelled by procurement directives that internalize disposal costs. The medical textile market size attached to biodegradable offerings grows as hospitals trial PHA and polylactic-acid blends that achieve sterilization compatibility while decomposing under industrial composting settings. Product developers address historical performance gaps by engineering multilayer hybrids where a biodegradable barrier coats a mechanical-strength substrate, maintaining infection control without permanent waste streams.

Regulatory measures, such as the EU’s separate textile-waste collection mandate effective 2025, levy extended producer responsibility fees on non-biodegradable suppliers, compressing their price advantage. Early movers in biodegradable fibers secure first-in-class certifications, insulating against later entrants given multi-year validation cycles. Performance-sensitive arenas, such as cardiovascular implants, continue to rely on non-degradable polyethylene terephthalate for long-term stability. Still, hospital sustainability committees increasingly weigh end-of-life impacts, suggesting a gradual pivot toward degradable formats in high-turn items like bandages. Suppliers capable of delivering cost-neutral substitutions are positioned for accelerated adoption.

By Application: Implantable Textiles Lead Innovation Premium

Surgical textiles held 41.12% revenue share in 2025, forming the stable cash-flow base of the sector, while implantable textiles are projected to grow at an 7.74% CAGR through 2031 by leveraging 3D-printed scaffolds and bioabsorbable meshes. The medical textile market size for implantables expands as clinical trials validate rapid tissue integration and controlled degradation timelines, enabling higher reimbursement thresholds. Implantable innovations encompass electro-conductive sutures that facilitate micro-current stimulation, boosting wound-closure rates and shortening hospital stays.

Wound-care textiles integrate hydrogel matrices and nanofiber overlays that maintain a moist environment while delivering antimicrobial agents locally, balancing efficacy and patient comfort. Health-and-hygiene disposables, though volumetrically dominant, face margin squeeze as hospital buyers bundle tenders. Extracorporeal applications like dialysis filters require precise porosity control and biocompatibility, commanding premium unit values despite low volumes. Suppliers with cross-application portfolios offset volatility in high-innovation segments by leaning on steady surgical-gown turnover.

Note: Segment shares of all individual segments available upon report purchase

By End User: Ambulatory Centers Drive Decentralized Growth

Hospitals and clinics represented 57.49% of the medical textile market size in 2025, yet ambulatory surgical centers exhibit a 6.86% CAGR thanks to payer incentives for cost-effective outpatient care. Portable wound-care kits and single-patient-use drape packs tailored for quick-turn procedures align with ASC workflows. Home-care settings employ smart mattresses with integrated pressure sensors to mitigate pressure ulcers, exemplified by Trelleborg’s 2025 collaboration with Nottingham Trent University.

The evolving care-delivery landscape prioritizes user-friendly designs with intuitive color coding and simplified fastening to support non-professional application. Wearable glucose monitors based on moisture-impermeable yet breathable fabrics enable continuous data collection outside clinical environments, creating aftermarket sales in sensor patches. Hospitals remain the anchor customer group for mass-volume sterile supplies, but growth tilts toward decentralized channels that value agility over scale. Manufacturers deploying omni-channel distribution and modular packaging capture switching demand while maintaining compliance across varied regulatory contexts.

Geography Analysis

North America held 33.62% medical textile market share in 2025, supported by high per-capita healthcare spending, mature reimbursement systems, and a robust contract-manufacturing base. The region continues to absorb premium-priced innovations such as nanofiber antimicrobial gowns as hospitals pursue outcome-based purchasing agreements. Recent consolidation, including Medline’s USD 1 billion acquisition of Ecolab’s surgical solutions unit, signals commitment to vertically integrated supply models that guarantee sterility and logistical reliability.

Asia Pacific tracks a 7.08% CAGR and is positioned to erode the North American lead by 2031 as China scales capacity beyond commodity exports into implantable and smart-textile domains. Japanese conglomerates invest in U.S. biotech startups to secure next-generation materials while maintaining domestic production quality benchmarks. India leverages sports-medicine demand and government‐funded health schemes to seed domestic consumption, drawing multinational joint ventures into textile parks with fiscal incentives.

Europe advances under stringent environmental legislation that is phasing out PFAS finishes and mandating recyclable inputs, prompting re-engineering of product portfolios and opening market gaps for bio-based entrants. Germany’s non-woven segment leads regional output, buoyed by technical-fabric heritage and state support for research clusters. The Middle East and Africa experience emerging uptake driven by military procurement and disaster-relief stockpiles that value shelf-stable disposable kits. South America remains comparatively small, constrained by economic fluctuations, yet targets niche growth in wound-care products aligned with expanding private insurance coverage in Brazil and Chile.

Competitive Landscape

Market Concentration

Market concentration remains moderate as integrated multinationals share space with niche innovators. 3M leverages a diversified health-care portfolio and in-house film technology to cross-sell barrier fabrics and advanced dressings, shielding margins through scale efficiencies. Freudenberg extends competency in filtration and interlining to medical non-wovens, pairing breadth with local service centers for rapid delivery into European hospital networks.

Strategic consolidation accelerated in 2024, highlighted by Medline’s surgical-solutions acquisition and Teleflex’s purchase of BIOTRONIK’s vascular intervention assets, a move expanding implantable reach and adding distribution synergies. Such deals underscore the value of turnkey portfolios that reduce supplier counts for hospital groups. Meanwhile, Bally Ribbon Mills applies aerospace-grade weaving to E-WEBBINGS conductive tapes, entering smart-textile niches where incumbents lack deep process know-how.

Patent density in biomedical textiles drives defensive R&D investment, with global filings topping 113,000 in 2024. Incumbents exploit intellectual property to sustain pricing power, while start-ups carve white-space by specializing in 3D-printed scaffolds or biodegradable composites. Regulatory barriers slow commoditization, maintaining profitability for first movers able to finance extended validation. Suppliers that fuse material science excellence with compliance expertise occupy resilient positions, dampening the competitive threat from low-cost producers.

Medical Textile Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: The German Institutes of Textile and Fiber Research (DITF) in Denkendorf announced their advancement in the development of elastic, conductive inks designed specifically for smart textile applications. These innovative inks can be directly printed onto fabric surfaces, maintaining reliable electrical conductivity even under mechanical stresses like stretching, bending, and repeated washing.

- April 2025: Trelleborg, a leading innovator in engineered coated fabrics, is advancing smart healthcare solutions through a Knowledge Transfer Partnership (KTP) with Nottingham Trent University’s Medical Technologies Innovation Facility. Supported by Innovate UK, this 26-month collaboration aims to develop a cutting-edge smart mattress system to enhance patient care. This project combines academic research with Trelleborg’s industry expertise to push the boundaries of smart medical textiles and redefine comfort and clinical efficiency in care environments.

- October 2024: Revolution-ZERO, a medical textile solutions provider based in Truro, Cornwall, has secured a significant equity investment of GBP 1 million (approximately USD 1.28 million) from the South West Investment Fund, managed by The FSE Group. This funding is part of a broader GBP 1.6 million (USD 2.05 million) round that includes contributions from private angel investors.

- September 2024: Health Care Without Harm, in collaboration with the Norwegian Retailers' Environment Fund (NREF), has launched a two-year global initiative to revolutionize sustainable textile production and consumption in healthcare across Latin America, Southeast Asia, and Europe.

Table of Contents for Medical Textile Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Regulatory Push for Single-Use Non-Woven Drapes & Gowns

- 4.2.2Aging Population Driving Chronic Wound Prevalence

- 4.2.3Sports Orthopedics Boom in Emerging Markets

- 4.2.4Smart Antimicrobial Coatings Reaching Commercial Scale

- 4.2.5Hospital Sustainability Programs Favouring Bio-Based Fibers

- 4.2.6Military & Disaster-Relief Stockpiling

- 4.3Market Restraints

- 4.3.1Stringent Multi-Jurisdictional Biocompatibility Tests

- 4.3.2Supply-Chain Volatility in Medical-Grade Polypropylene

- 4.3.3Reimbursement Gaps for Advanced Wound Dressings

- 4.3.4Lack of End-of-Life Recycling Infrastructure

- 4.4Porter’s Five Forces Analysis

- 4.4.1Threat of New Entrants

- 4.4.2Bargaining Power of Buyers/Consumers

- 4.4.3Bargaining Power of Suppliers

- 4.4.4Threat of Substitute Products

- 4.4.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value in USD)

- 5.1By Textile Structure

- 5.1.1Woven

- 5.1.2Non-woven

- 5.1.3Knitted

- 5.1.4Braided

- 5.2By Biodegradability

- 5.2.1Biodegradable

- 5.2.2Non-biodegradable

- 5.3By Application

- 5.3.1Wound Care

- 5.3.2Surgical Textiles

- 5.3.3Health & Hygiene

- 5.3.4Implantable Textiles

- 5.3.5Extracorporeal Devices

- 5.3.6Others

- 5.4By End User

- 5.4.1Hospitals & Clinics

- 5.4.2Ambulatory Surgical Centres

- 5.4.3Home-Care Settings

- 5.4.4Other End Users

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4Australia

- 5.5.3.5South Korea

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East & Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East & Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.13M

- 6.3.2Freudenberg Performance Materials

- 6.3.3Medline Industries

- 6.3.4Cardinal Health

- 6.3.5Smith & Nephew

- 6.3.6Mölnlycke Health Care

- 6.3.7Halyard Health (Owens & Minor)

- 6.3.8Winner Medical

- 6.3.9Ahlstrom-Munksjö

- 6.3.10Kimberly-Clark Health Care

- 6.3.11ATEX Technologies

- 6.3.12Bally Ribbon Mills

- 6.3.13Precision Fabrics Group

- 6.3.14medi GmbH & Co. KG

- 6.3.15Toray Industries

- 6.3.16Asahi Kasei

- 6.3.17Lohmann & Rauscher

- 6.3.18DuPont de Nemours

- 6.3.19Eastex Products

- 6.3.20Paul Hartmann AG

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Global Medical Textile Market Report Scope

As per the scope of the report, the textiles used for medical purposes are usually referred to as medical textiles. Medical textiles are specialized materials designed for medical applications, including wound care, surgical procedures, and hygiene products.

The medical textiles market is segmented by type of textile structure, biodegradability, application, and geography. By type of textile structure, the market is segmented into woven, nonwoven, braided, and knitted. In terms of biodegradability, the market is segmented into biodegradable and non-biodegradable. By application, the market is segmented into wound care, surgical, health and hygiene, and other applications. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (USD) for the above segments.