Learning Management System (LMS) In Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

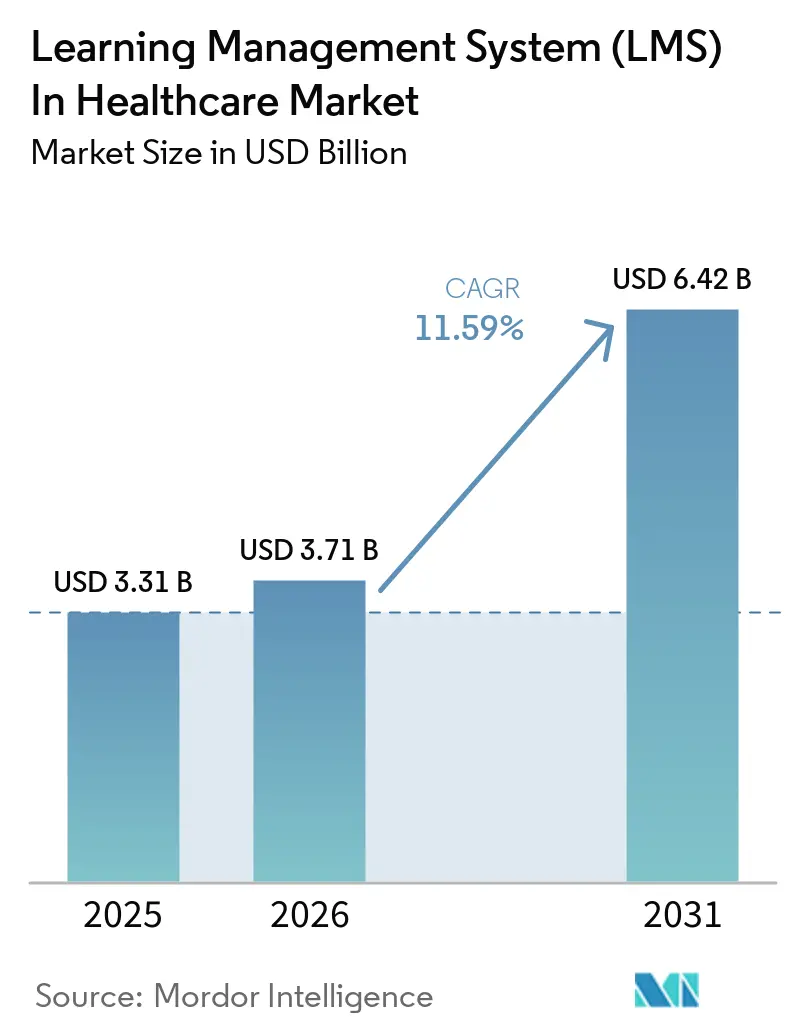

| Market Size (2026) | USD 3.71 Billion |

| Market Size (2031) | USD 6.42 Billion |

| Growth Rate (2026 - 2031) | 11.59% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Learning Management System (LMS) In Healthcare Market Analysis by Mordor Intelligence

The Learning Management System (LMS) in the Healthcare Market in healthcare reached USD 3.31 billion in 2025 and is forecast to reach USD 6.42 billion by 2031, growing at a CAGR of 11.59% over 2026-2031. The learning management system in the healthcare market is being shaped by 2 structural pressures that reinforce each other: stricter compliance tracking and the need to train a larger and more fluid care workforce. Health systems now treat auditable, role-specific training records as an operating requirement because onboarding, credentialing, policy acknowledgment, and continuing education must be tracked in one place across distributed care settings. The learning management system market in healthcare is also gaining support from workflow changes tied to AI-enabled documentation, as clinicians need retraining on revised protocols, output review, and governance controls as these tools move into daily use. Competitive positioning is widening between healthcare-native vendors with clinical content depth and general enterprise platforms that are adding healthcare overlays, integration features, and AI tools to win regulated accounts. The main commercial opening remains with buyers who want a single platform to handle compliance, clinical capability development, and workforce mobility without creating additional reporting friction across hospitals, clinics, and life sciences environments.

Key Report Takeaways

- By geography, North America held 36.58% of the healthcare learning management system market share in 2025, while Asia-Pacific is projected to expand at a 13.41% CAGR through 2031.

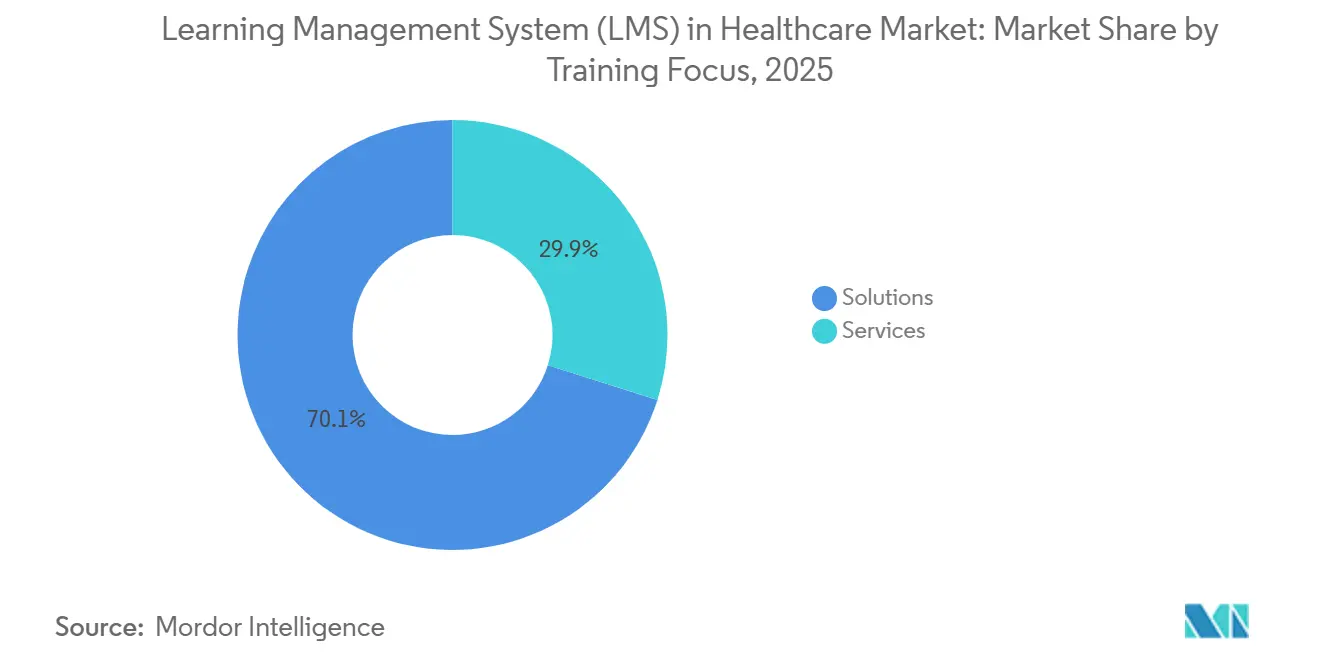

- By component, solutions accounted for 70.12% of the learning management system market in healthcare in 2025, while services are forecast to grow at a 12.23% CAGR through 2031.

- By deployment mode, cloud-based deployment held a 65.23% share in 2025 and is also projected to record the highest growth at a 12.46% CAGR through 2031.

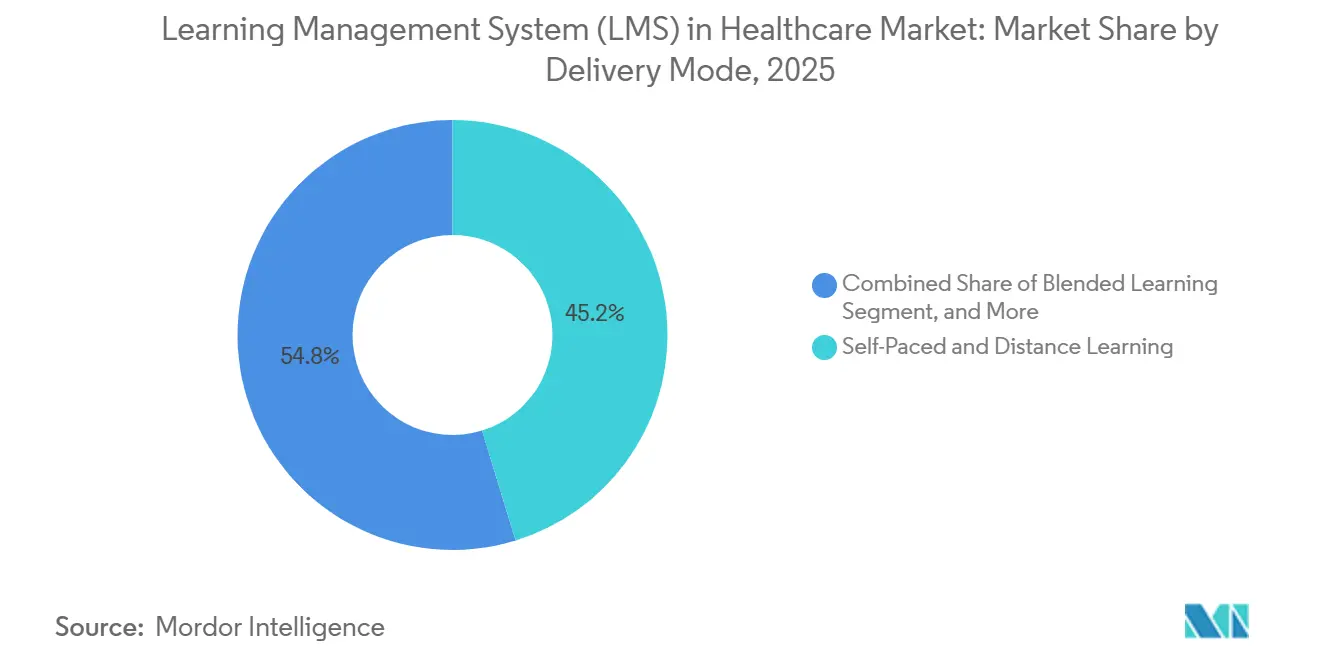

- By delivery mode, self-paced and distance learning represented 45.24% of the 2025 market, while blended learning is projected to grow at a 14.57% CAGR through 2031.

- By application, compliance training captured a 30.12% share in 2025, while clinical and care training is forecast to expand at a 13.81% CAGR through 2031.

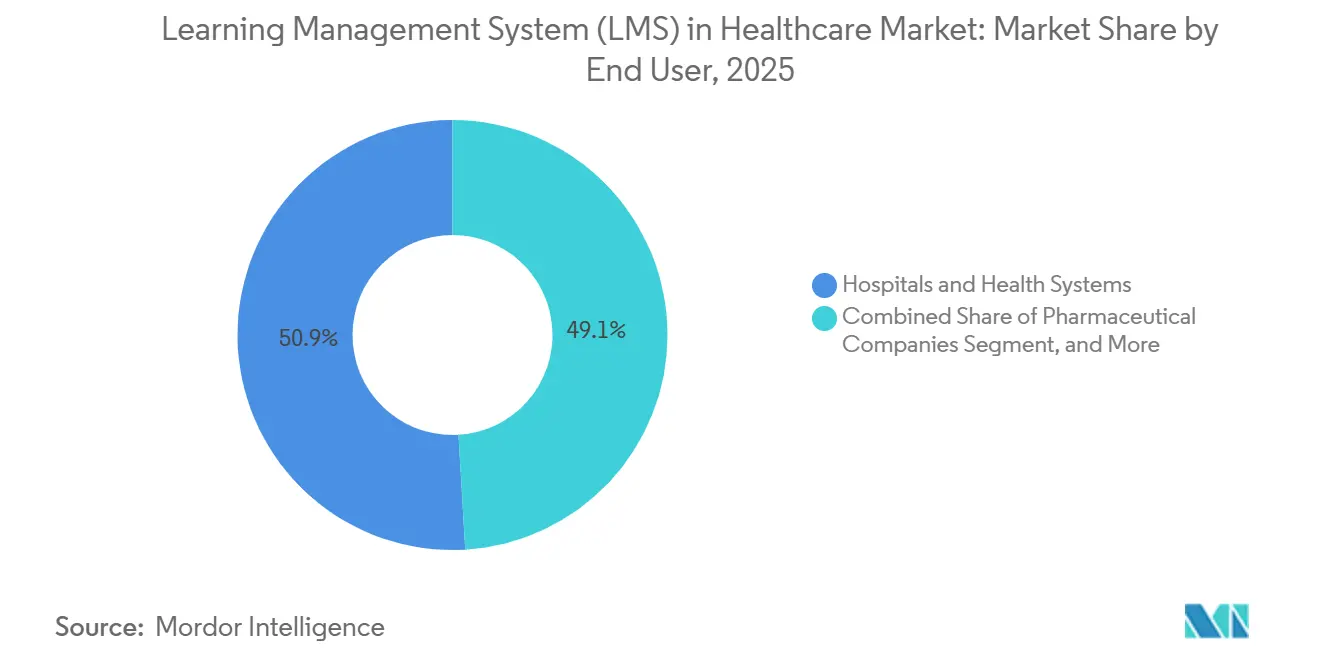

- By end user, hospitals and health systems accounted for 50.94% of 2025 demand, while pharmaceutical and medical device companies are expected to post the highest CAGR of 14.32% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Learning Management System (LMS) In Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Compliance and Accreditation Tracking | +3.0% | Global, with highest concentration in North America and Western Europe | Short term (≤ 2 years) |

| Workforce Shortages and Continuous Clinical Upskilling | +2.5% | Global, highest impact in North America and Asia-Pacific | Medium term (2-4 years) |

| AI-Enabled Personalized Learning and Skills Analytics | +2.0% | Global, leading adoption in North America and East Asia | Medium term (2-4 years) |

| Cloud-Based and Hybrid Training Delivery Adoption | +1.7% | Global, with spill-over to Middle East and Africa | Short term (≤ 2 years) to Medium term (2-4 years) |

| Retraining Demand From Ambient AI and Digital Workflow Adoption | +1.2% | North America and Western Europe, spill-over to APAC core | Medium term (2-4 years) |

| Cross-Site Auditability Needs After Cyber and Patient-Safety Incidents | +0.8% | Global, core impact in North America and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Compliance and Accreditation Tracking

The learning management system market in healthcare continues to draw steady demand from accreditation-linked training mandates that health systems cannot defer without increasing operating risk. Documented, role-specific competency validation has become embedded in routine workforce management, turning the LMS from a convenience tool into a compliance system tied to inspections, renewals, and internal audit readiness. This matters even more in large provider networks, where policy acknowledgment, competency sign-off, and retraining records need to be searchable across facilities, units, and job categories within a single evidentiary trail. The result is a strong switching-cost effect: once reporting architecture, audit logs, and accreditation evidence are aligned on a single platform, procurement teams become more cautious about vendor changes. The learning management system in the healthcare market also benefits as continuing education requirements expand across specialties, since the number of training events that must be recorded can rise even without a corresponding increase in headcount.

Workforce Shortages and Continuous Clinical Upskilling

The learning management system in the healthcare market is also being supported by staffing shortages that are forcing providers to rely on faster, more scalable training models. The American Hospital Association projected a shortfall of 64,000 nurses by 2030 and said health care is expected to account for 24% of all new U.S. jobs this decade, meaning every new role created will increase demand for onboarding and continuing education. The American Medical Group Association reported that total clinic staffing in primary care and medical specialties declined by 5% to 7% between 2022 and 2024, even as patient visits rose 2.3% in 2024, making classroom-only delivery harder to sustain in busy clinical settings.[1]American Hospital Association, “2026 Health Care Workforce Scan,” American Hospital Association, aha.org The same pressure is visible in frontline support roles, where high turnover expands the annual cycle of onboarding-linked training, and in pharmacy operations, where the Pharmacy Technician Certification Board found employer-based training programs rose 6.3% in 2025 across its survey base of 17,112 respondents. As care teams diversify and role scopes become more specialized, the learning management system in the healthcare market benefits from the need to standardize training across jurisdictions, credentials, and care pathways without relying on additional in-person administrative staff.

AI-Enabled Personalized Learning and Skills Analytics

The learning management system in the healthcare market is shifting from simple content delivery to adaptive competency development as AI tools are integrated into learning design and assessment. A 2026 randomized controlled trial in Frontiers in Medicine found that oncology residents using an AI-enabled intelligent teaching framework achieved a 91.2% knowledge retention rate, compared with 76.8% in the control group, while weekly study time fell from 20.62 hours to 10.63 hours.[2]Pharmacy Technician Certification Board, “The State of the Pharmacy Technician Workforce 2025,” PTCB, ptcb.org A separate 2025 study in Frontiers in Medicine showed that an AI-driven personalized learning platform increased daily learning time by 41.5% and increased classroom interaction frequency by 117%, suggesting stronger engagement without relying on manual enforcement. These performance gains matter in care settings because faster skill attainment reduces the time clinicians spend away from patient-facing work. Vendors that can link learning outcomes to observable skill development rather than simple module completion are likely to hold a stronger position as enterprise buyers demand clearer returns on training spend.

Cloud-Based and Hybrid Training Delivery Adoption

The learning management system in the healthcare market is moving toward cloud-native deployment because multi-site provider groups need consistent configuration, faster updates, and lower local IT burden across facilities. Cloud delivery also supports API-based workflows, which lets training assignments respond to role changes, shift schedules, new-hire activity, and credential expiration without extensive manual coordination. MedTrainer’s 2025 integration work on automated onboarding reflected buyers' increasingly strong expectations for tighter integration between workforce systems and compliance training tasks, rather than stand-alone course libraries. At the same time, data residency rules are making architecture decisions more important, especially for health systems operating across jurisdictions that want local control of learner and staff records. The European Health Data Space regulation reinforced this direction by advancing cross-border digital health governance, favoring vendors that can manage cloud-scale with regional compliance controls.[3]Yajun Chen, “Evaluation of the Impact of AI-Driven Personalized Learning Platform on Medical Students’ Learning Performance,” Frontiers in Medicine, frontiersin.org

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy and Cybersecurity Requirements | -1.5% | Global, highest impact in North America and EU | Short term (= 2 years) |

| Integration Complexity With EHR, HRIS, and Credentialing Systems | -1.2% | Global, most acute in North America and Asia-Pacific | Medium term (2-4 years) |

| Content Governance Bottlenecks in Fast-Changing Clinical Protocols | -0.9% | Global, most acute in high-acuity care settings | Medium term (2-4 years) to Long term (= 4 years) |

| Shift-Based Care Models Reduce Rich-Format Training Completion | -0.7% | Global, most acute in hospital and acute-care settings | Long term (= 4 years) |

| Source: Mordor Intelligence | |||

Data Privacy and Cybersecurity Requirements

The learning management system in the healthcare market faces a significant brake due to the security burden imposed by systems that store staff training records, compliance evidence, and user-level identifiers. A 2026 survey published in Applied Sciences noted that U.S. health care breaches peaked in 2024 with 276 million records exposed, and that incidents in the sector averaged 279 days to identify and contain in 2025.[4]Ramsha Qureshi and Insoo Koo, “A Comprehensive Survey of Cybersecurity Threats and Data Privacy Issues in Healthcare Systems,” Applied Sciences, mdpi.com This environment heightens buyer scrutiny of encryption, access controls, audit trails, testing procedures, and vendor documentation before contracts move forward. The cost of validating these controls can materially increase deployment expenses for smaller hospitals and federally qualified health centers, making the mid-market more price-sensitive than top-tier health systems. The learning management system market in healthcare, therefore, grows faster when vendors can centrally package security compliance and reduce the burden of local oversight for customers with limited internal cyber resources.

Integration Complexity With EHR, HRIS, And Credentialing Systems

The learning management system in the healthcare market also slows when providers struggle to connect new platforms to established EHR, HRIS, and credentialing environments. Health systems often use proprietary interfaces and multiple user directories, which means the real cost of a new LMS can rise well above the initial license price once middleware, mapping, and maintenance are included. This issue is more severe after mergers, when one organization may operate multiple EHR environments that use different data standards and renewal workflows. Healthcare-native vendors usually move faster because their products are built around these conditions, while general-purpose platforms often require extra development time before compliance workflows are usable. Integration complexity, therefore, acts like a renewal advantage for incumbents, because switching can delay training continuity in environments where auditable completion records cannot be interrupted.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Lead Revenue While Services Gain Traction Through Managed Support

Solutions captured 70.12% of the 2025 component split, making them the largest revenue stream in the healthcare learning management system market. Buyers favored integrated platforms because they combine content libraries, workflow automation, reporting, and user management in a single interface, rather than spreading accountability across multiple tools. That setup reduces audit friction because training completion, policy acknowledgment, and competency sign-off can be reviewed through a single evidence trail. It also supports enterprise standardization, which is important for health systems that need the same training logic across hospitals, clinics, and post-acute settings.

Services are the faster-growing component, with a 12.23% CAGR projected through 2031, reflecting a clear shift in buyer behavior within the learning management system in the healthcare industry. Many customers have moved past basic platform deployment and now want outside help with implementation, regulatory updates, content maintenance, and multi-site administration. MedTrainer said it released more than 250 new healthcare-specific courses and more than 130 software enhancements during 2025, while also expanding its engineering team by 25%, demonstrating how vendors are building recurring service layers on top of the software base. As use cases broaden into skills gap analysis, AI retraining, and distributed credentialing, services become a practical way for providers to keep the learning environment current without hiring large internal LMS teams.

By Deployment Mode: Cloud Consolidates Leadership While Hybrid Serves Regulated Architectures

Cloud-based deployment held a 65.23% share in 2025 and remains the leading configuration in the healthcare learning management system market. The main reason is operational, because cloud infrastructure lets role-based assignments, content updates, and reporting changes move across all sites without local system administration at each facility. It also supports faster onboarding for new locations and newly acquired provider groups that need to fit into an existing compliance framework. For buyers with large workforces and lean IT teams, these benefits make cloud the most efficient model for maintaining training continuity at scale.

Cloud is also the fastest-growing deployment mode, with a 12.46% CAGR through 2031, while hybrid demand remains relevant in more tightly regulated environments. The European Health Data Space regulation strengthened the case for platforms that can support digital interoperability together with jurisdiction-aware governance controls. Hybrid deployment remains a key option for large academic medical centers and integrated delivery networks that want on-premises control for selected records while still leveraging cloud elasticity for content delivery and analytics. On-premises systems continue to be used in high-security or resource-constrained environments, but the learning management system market in healthcare is clearly moving toward hosted architectures that offer compliance parity with lower maintenance overhead.

By Delivery Mode: Self-Paced Formats Hold the Base While Blended Learning Expands Faster

Self-paced and distance learning accounted for 45.24% of the 2025 market, maintaining its position as the largest delivery format in the healthcare learning management system market. This format aligns with the realities of shift-based care because clinicians can complete required modules without waiting for a live session or leaving patient care for extended periods. It also works well for recurring topics such as infection control, medication safety, privacy training, and annual competency refreshers, where standardized documentation matters as much as content depth. For organizations that need broad workforce coverage and reliable completion records, self-paced delivery remains the most practical default.

Blended learning is expanding faster, with a 14.57% CAGR projected through 2031, because many clinical topics need more than passive course completion. Complex judgment areas such as sepsis recognition, deteriorating patient identification, and team communication often benefit from guided feedback, debriefing, and scenario review after digital preparation. A 2026 randomized controlled trial in Frontiers in Medicine found that AI-enabled tutoring in a blended framework achieved a 90.3% specialty examination pass rate, compared with 67.6% in the control group, while burnout incidence fell to 35.2% from 61.5%. Instructor-led delivery, therefore, keeps a clear place for high-stakes procedural training, while blended models allow the learning management system in the healthcare market to support richer competency development without abandoning scheduling flexibility.

By Application: Compliance Training Anchors Spending While Clinical Care Use Cases Rise Faster

Compliance training accounted for 30.12% of the 2025 application split, making it the largest use case in the healthcare learning management system market. This spending is not discretionary, because hospitals, health systems, and many life sciences employers need documented completion records to satisfy regulatory, accreditation, and internal governance requirements. The same logic extends beyond provider settings, as pharmaceutical and medical device operations must maintain validated training records and audit trails tied to controlled processes. Cybersecurity education is also gaining weight inside the application mix as health care organizations respond to a more demanding risk environment and broader expectations for staff awareness.

Clinical and care training is the fastest-growing application, with a 13.81% CAGR through 2031, and its growth shows that buyers increasingly want the LMS to support real skill development rather than just mandatory completion. Health systems are using platforms to close the gap between credential attainment and observable bedside capability, especially in areas where standardized onboarding does not fully prepare new staff for the complexity of live care. Demand is also building around telehealth training, EHR workflow education, workforce credentialing, and competency management as digital-first care models spread across settings. The learning management system in the healthcare industry gains further support here because rapidly changing clinical protocols create content governance pressure, and providers often prefer vendors that can update content and reporting logic as rules and workflows change.

By End User: Hospitals Hold the Revenue Base While Life Sciences Buyers Lead Growth

Hospitals and health systems accounted for 50.94% of 2025 demand, making them the largest end-user group in the healthcare learning management system market. Their scale alone supports this position, because a large academic or integrated health system may employ thousands of people across many professional categories, all with different training obligations. Dense compliance requirements, multi-site operating models, and multi-year enterprise contracts also make this customer base central to current revenue. In practice, purpose-built LMS infrastructure becomes hard to replace in these accounts because training continuity, audit readiness, and renewal workflows are woven into daily operations.

Pharmaceutical and medical device companies are the fastest-growing end-user cohort, with a 14.32% CAGR expected through 2031. Their demand is shaped by validated electronic records, audit trail integrity, and launch-related training requirements that general-purpose platforms do not always address well. Outside acute care, long-term care, and home care are also moving further into digital training, and Activated Insights said CareAcademy had trained more than 800,000 caregivers across more than 2,000 provider organizations before the acquisition closed. Clinics and ambulatory providers usually favor cloud-native tools with lower IT overhead, leaving the learning management system in the healthcare industry open to vendors that can offer preconfigured compliance workflows and faster deployment for the mid-market.

Geography Analysis

North America held 36.58% of the healthcare learning management system market share in 2025, making it the largest regional market. The United States remained the dominant national market because CMS participation rules, accreditation standards, and privacy obligations make documented training an operational requirement rather than an optional software upgrade. This environment supports a stable demand for platforms that can manage onboarding, competency validation, policy acknowledgment, and recurring compliance at enterprise scale. Canada also showed active institutional adoption, and the University of Toronto Temerty Faculty of Medicine selected a cloud-based learner management platform in 2025 to support MD and postgraduate education aligned with the Competence by Design framework. Mexico remains a smaller opportunity in the region, but private hospital groups are gradually formalizing workforce development and competency documentation as payer and quality expectations rise.

Europe remains an important part of the learning management system in the healthcare market because it combines dense hospital networks with expanding digital health governance. The European Health Data Space regulation, adopted in 2025, created a stronger framework for cross-border health data management, which adds training needs for staff who handle digital records, system access, and compliance processes. The United Kingdom, Germany, and France remain the main national demand centers, while Spain, Italy, and Eastern Europe are moving forward from a smaller base as record digitization and workforce governance become more structured. This keeps Europe positioned as a market where vendors need both regional data awareness and the ability to adapt training structures to varied health system models.

Asia-Pacific is the fastest-growing region in the learning management system market for healthcare, with a 13.41% CAGR projected through 2031. Growth is being driven by state-led health system expansion in China and India, by scaling private hospital networks across Southeast Asia, and by a broader recognition that workforce quality assurance requires digital training infrastructure. The World Health Organization said in 2025 that only 30% of member states have well-functioning regulatory systems at Maturity Levels 3 or 4, and it launched a learning catalog to help upskill regulatory workforces, reflecting a wider need for structured training capacity across several developing health systems. A 2026 study in Frontiers in Medicine also showed strong engagement with AI-enabled clinical learning among Chinese medical students, with 45.6% participating in sessions of 15 to 30 minutes and 63.4% preferring mobile app delivery, pointing to mobile-first design expectations across the region. Australia and Singapore remain smaller but advanced digital health markets, while South America, the Middle East, and Africa continue to present earlier-stage opportunities led by Brazil, Saudi Arabia, and the UAE.

Competitive Landscape

The learning management system market in healthcare operates with a split competitive structure that is becoming more evident as buyers separate clinical depth from broad platform breadth. Healthcare-native vendors such as HealthStream, Relias, and MedTrainer hold a strong position in large provider accounts because they offer clinical content libraries, regulatory workflows, and integration models that better align with care delivery environments than horizontal systems. HealthStream reported USD 291.6 million in full-year 2024 revenue, with subscription revenue accounting for 96% of total revenue, and operating income rising 32.9% year over year, indicating that purpose-built platforms still defend premium economics in this space. Alongside these incumbents, general enterprise vendors such as Docebo, Cornerstone OnDemand, Absorb Software, and LearnUpon are building more targeted health care offerings to compete for regulated buyers.

Competition in the learning management system market in healthcare is now centered on 3 areas: AI capabilities, skills intelligence, and workflow embeddedness. Docebo’s April 2026 AgentHub launch combined skills intelligence from 365Talents with autonomous AI agents that generate onboarding content from enterprise knowledge sources, signaling a move toward self-configuring learning environments. Cornerstone’s March 2026 release added an Adaptive Learning Agent, an AI-powered Course Assistant, and a Galaxy Admin Dashboard to surface risk and automate skill-gap response. HealthStream had already pushed in the same direction with the January 2025 launch of its HLX application, an AI-first healthcare-specific learning experience platform designed for more personalized content delivery. This shift also connects to ambient AI adoption in care delivery, as Microsoft said by early 2025 that ambient AI tools were processing more than 3 million patient episodes each month across more than 600 healthcare systems globally, creating a direct need for workflow retraining and governance education.

A clear white space remains in the learning management system market for healthcare, with pharmaceutical and medical device training environments that require validated documentation, electronic signatures, and audit-ready controls in one package. That is why niche providers can still defend their position even when they are smaller than horizontal software groups. HealthStream expanded its workforce ecosystem in December 2025 by acquiring MissionCare Collective, while it also formed an educational partnership with Vanderbilt University School of Nursing to broaden nurse-focused learning content and continuing education access. MedTrainer, CareAcademy, Medbridge, and ACTO show the same pattern: deep domain relevance and strong workflow fit remain decisive when buyers place content quality and compliance readiness on par with platform functionality.

Learning Management System (LMS) In Healthcare Industry Leaders

HealthStream, Inc.

Relias LLC

Docebo S.p.A.

MedTrainer, Inc.

D2L Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Cornerstone and Questionmark partnered to integrate advanced workforce assessments into Cornerstone Galaxy for regulated industries like healthcare.

- April 2026: Docebo launched AgentHub with autonomous AI agents and MCP Server, positioning its LMS as a native knowledge source for AI assistants.

- March 2026: Cornerstone added an Adaptive Learning Agent, AI Course Assistant, and compliance-risk dashboard to Galaxy for healthcare workforce training.

- February 2026: MedStar Health partnered with EB Medicine to provide CME-accredited urgent care curricula for its fellowship program.

Global Learning Management System (LMS) In Healthcare Market Report Scope

In the healthcare market, a Learning Management System (LMS) is a technology platform and service that delivers, manages, and tracks training, compliance, and credentialing programs across healthcare organizations. These systems support applications such as clinical and care training, CME and certification, patient safety, infection control, telehealth, and cybersecurity. Deployed in the cloud, on-premises, or in hybrid models, and delivered through self-paced, instructor-led, or blended learning, healthcare LMS solutions enable hospitals, clinics, pharmaceutical firms, and medical institutions to meet regulatory requirements, enhance workforce skills, and improve patient outcomes.

The Learning Management System (LMS) in Healthcare Market is segmented by Component (Software and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Delivery Mode (Self-Paced and Distance Learning, Instructor-Led Training, and Blended Learning), Application (Compliance Training, Clinical and Care Training, CME and Certification Training, Product and Commercial Training, Patient Safety Training, EHR/Clinical Systems Training, Infection Control Training, Cybersecurity and Data Privacy Training, Telehealth Training, and Workforce Credentialing and Competency Management), End User (Hospitals and Health Systems, Clinics and Ambulatory Care Providers, Pharmaceutical Companies, Medical Device Companies, Academic Medical Institutions, Long-Term Care Facilities, and Home Healthcare Providers), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Self-Paced and Distance Learning |

| Instructor-Led Training |

| Blended Learning |

| Compliance Training |

| Clinical and Care Training |

| CME and Certification Training |

| Product and Commercial Training |

| Patient Safety Training |

| EHR/Clinical Systems Training |

| Infection Control Training |

| Cybersecurity and Data Privacy Training |

| Telehealth Training |

| Workforce Credentialing and Competency Management |

| Hospitals and Health Systems |

| Clinics and Ambulatory Care Providers |

| Pharmaceutical Companies |

| Medical Device Companies |

| Academic Medical Institutions |

| Long-Term Care Facilities |

| Home Healthcare Providers |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Solutions | |

| Services | ||

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By Delivery Mode | Self-Paced and Distance Learning | |

| Instructor-Led Training | ||

| Blended Learning | ||

| By Application | Compliance Training | |

| Clinical and Care Training | ||

| CME and Certification Training | ||

| Product and Commercial Training | ||

| Patient Safety Training | ||

| EHR/Clinical Systems Training | ||

| Infection Control Training | ||

| Cybersecurity and Data Privacy Training | ||

| Telehealth Training | ||

| Workforce Credentialing and Competency Management | ||

| By End User | Hospitals and Health Systems | |

| Clinics and Ambulatory Care Providers | ||

| Pharmaceutical Companies | ||

| Medical Device Companies | ||

| Academic Medical Institutions | ||

| Long-Term Care Facilities | ||

| Home Healthcare Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the learning management system in healthcare market?

The learning management system in healthcare market reached USD 3.31 billion in 2025 and is forecast to reach USD 6.42 billion by 2031, at an 11.59% CAGR over 2026-2031.

Which region leads learning management system adoption in healthcare?

North America led with a 36.58% share in 2025, supported by strong compliance requirements, mature IT procurement, and wide digital system adoption across provider networks.

Which region is growing the fastest through 2031?

Asia-Pacific is projected to grow the fastest at a 13.41% CAGR, driven by hospital modernization, workforce expansion, and growing demand for digital training infrastructure.

Why do hospitals invest in healthcare LMS platforms?

Hospitals use these platforms to manage auditable training records, role-based onboarding, credentialing, policy acknowledgment, and continuing education across large and diverse workforces.

Which application area generates the most revenue today?

Compliance training held the largest application share at 30.12% in 2025 because training completion and recordkeeping are required across many regulated care and life sciences settings.

Which end-user group is expanding the fastest?

Pharmaceutical and medical device companies are forecast to grow the fastest at a 14.32% CAGR through 2031, supported by validation, audit trail, and product training requirements.

What delivery format is gaining momentum fastest?

Blended learning is projected to grow at a 14.57% CAGR through 2031 because it combines schedule flexibility with instructor interaction needed for more complex clinical skill development.

Page last updated on: