HCM Software In Education Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

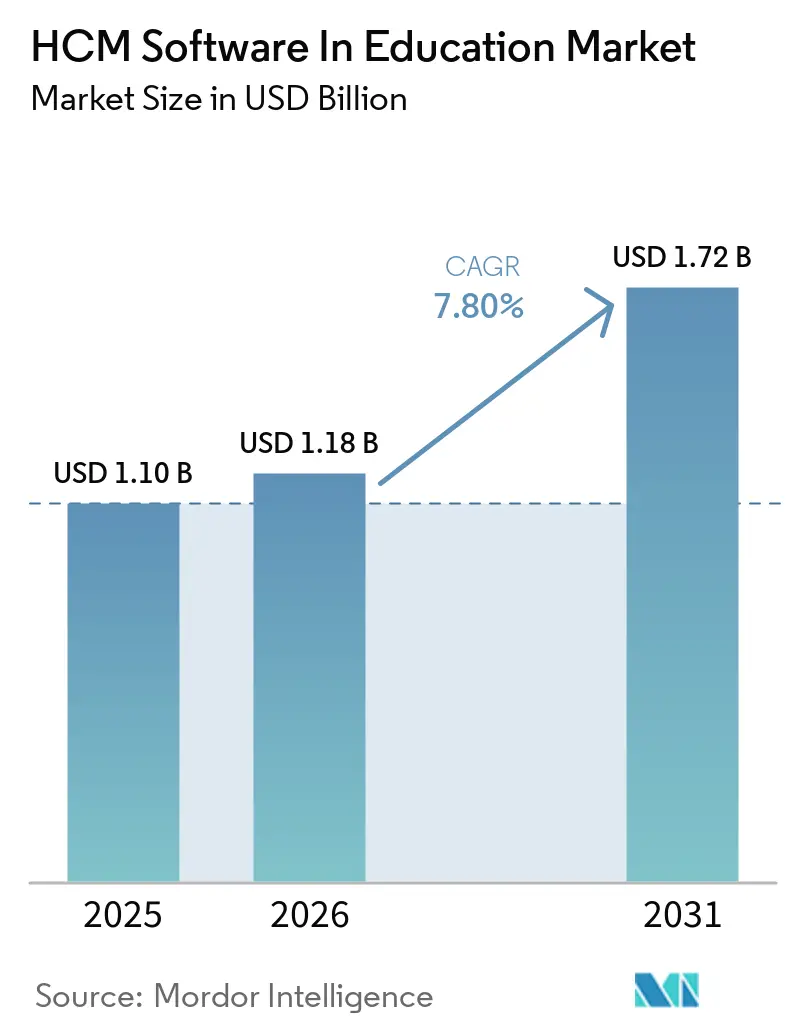

| Market Size (2026) | USD 1.18 Billion |

| Market Size (2031) | USD 1.72 Billion |

| Growth Rate (2026 - 2031) | 7.80% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HCM Software In Education Market Analysis by Mordor Intelligence

The HCM software in education market size is expected to be USD 1.10 billion in 2025, USD 1.18 billion in 2026, and reach USD 1.72 billion by 2031, growing at a CAGR of 7.8% from 2026 to 2031. Institutions are shifting core HR activities to the cloud to support hybrid teaching models, yet on-premises systems remain entrenched because many universities hesitate to write off legacy investments. Platform vendors now bundle compliance engines with analytics that join student and employee data, giving academic employers unified insight into payroll, scheduling, and faculty engagement. Meanwhile, budget freezes in public institutions prolong replacement cycles, forcing suppliers to offer phased deployments and consumption-based contracts. Competition is therefore pivoting toward modular offerings that wrap generative AI around talent analytics, enabling colleges to benchmark workloads, predict turnover, and map skills without committing to multi-year licenses.

Key Report Takeaways

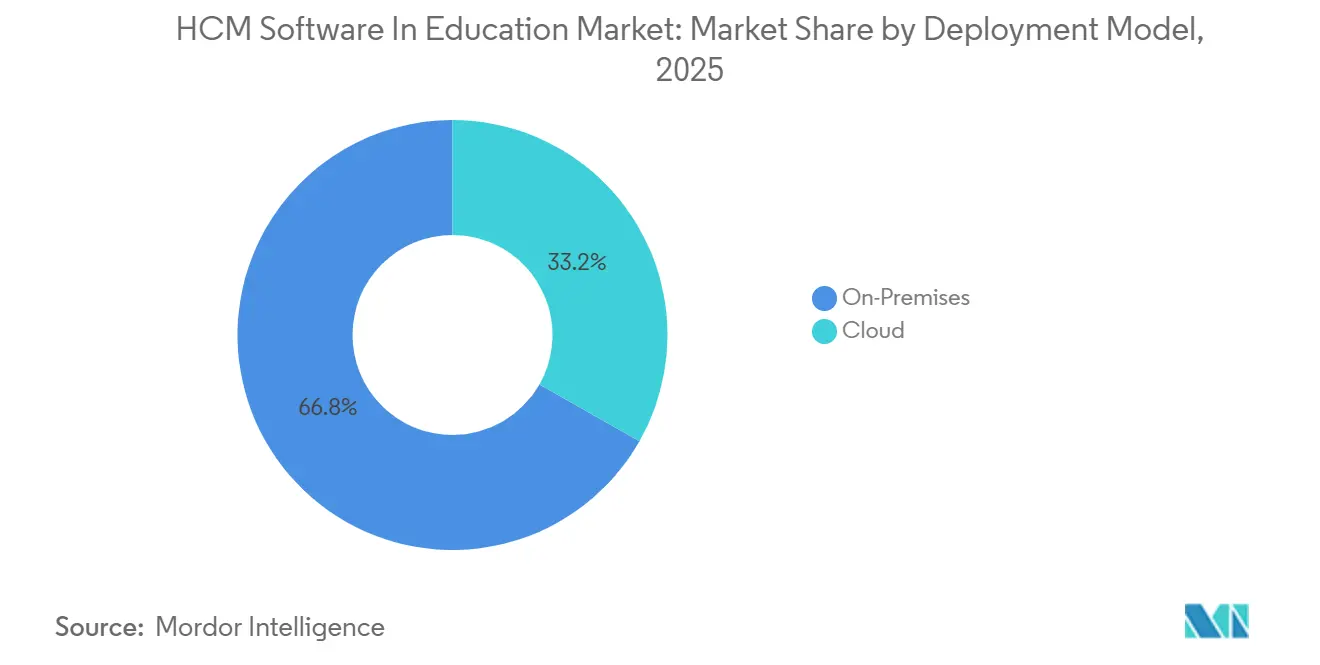

- By deployment model, on-premises installations commanded 66.78% share of HCM software in education market spending in 2025, whereas cloud solutions are expanding at a 10.72% CAGR through 2031.

- By solution, core HR modules led with 45.61% revenue share in 2025, while talent-management platforms are advancing at a 9.42% CAGR.

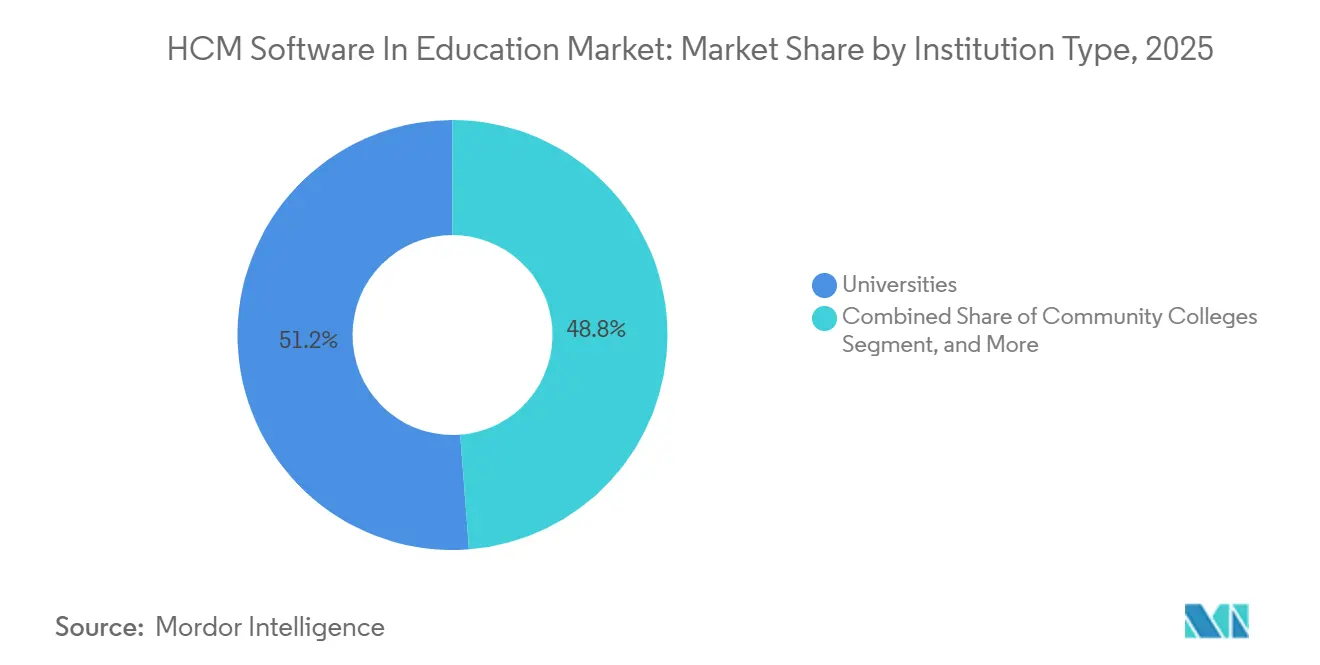

- By institution type, universities accounted for 51.22% of 2025 expenditure, yet vocational and technical institutes post the fastest growth at a 10.34% CAGR.

- By end user, faculty and staff represented 53.45% of active seats in 2025, although student-employee modules are scaling at a 9.81% CAGR.

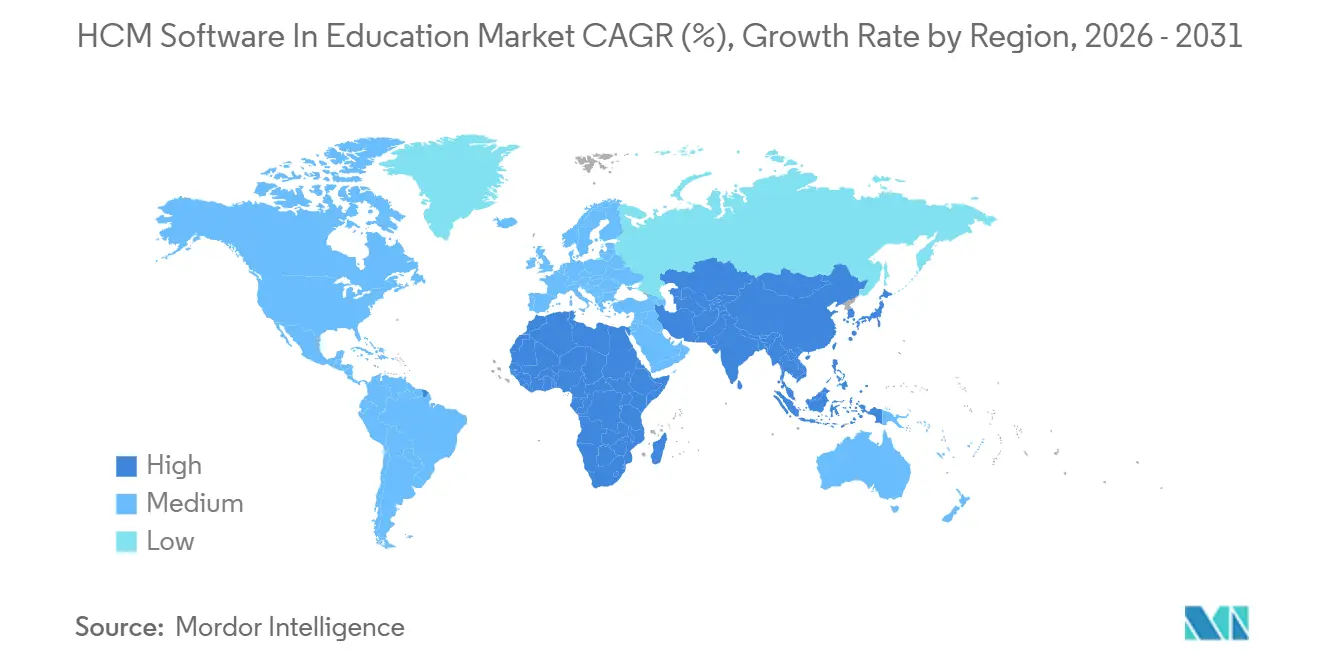

- By geography, North America captured 36.18% share of 2025 revenue of HCM software in education market, whereas Asia-Pacific is set to grow at an 8.98% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HCM Software In Education Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Cloud-First Strategies Among Universities | +2.1% | Global, led by North America and Europe | Medium term (2-4 years) |

| Increasing Emphasis on Faculty Experience Management | +1.6% | North America, Asia-Pacific, Europe | Medium term (2-4 years) |

| Integration of AI-Powered Skills Mapping | +1.4% | North America, Asia-Pacific, Middle East | Short term (≤ 2 years) |

| Rising Compliance Burden for Academic Payroll | +1.2% | Global, with strongest impact in North America and Europe | Long term (≥ 4 years) |

| Expansion of Hybrid Work Models in Campuses | +0.8% | North America, Europe, Australia | Short term (≤ 2 years) |

| Demand for Analytics-Driven Student Employment Programs | +0.7% | North America, Asia-Pacific urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Cloud-First Strategies Among Universities

Universities are accelerating migrations of payroll, benefits, and recruiting to cloud suites to eliminate data-center costs and support remote faculty access. The shift gained momentum after 2024 when hybrid teaching and multi-campus models exposed the limitations of fixed infrastructure. Providers now package data-conversion tools, sandboxes, and managed services that de-risk complex cutovers. Cloud editions also deliver quarterly feature releases, letting institutions adopt analytics and mobile self-service without long upgrade projects. Workday reported in its fiscal 2026 earnings that education-sector bookings grew by double digits, driven by large public universities replacing legacy ERP stacks with integrated cloud suites.[1]Workday Investor Relations, “Fiscal 2026 Earnings Report,” investor.workday.com As a result, the HCM software in education market records a steady transfer of workloads from on-premises to cloud subscriptions. Resistance persists where sunk costs in customized ERP stacks remain high, yet expiring maintenance contracts and the lure of elastic scaling continue to tip business cases in favor of cloud adoption.

Increasing Emphasis on Faculty Experience Management

Academic employers are elevating faculty satisfaction to strategic priority, embedding sentiment analysis, workload tracking, and professional-development dashboards into HR workflows. Experience-management tools surface data on teaching loads, research output, and service commitments, enabling deans to spot inequities early. The emphasis aligns with a competitive labor market for STEM professors, where burnout and poaching threaten program continuity. Solutions that recommend mentorship pairings, alert administrators to looming overloads, and integrate with learning-development libraries are gaining favor. Governance complexities remain, because faculty senates demand transparency on how metrics influence promotion and tenure, yet institutions now view holistic engagement analytics as essential for retention.

Integration of AI-Powered Skills Mapping

Generative AI is parsing curricula vitae, publications, and grant histories to create dynamic competency profiles of faculty and staff. Departments use these maps to assign instructors to emerging interdisciplinary courses and to form research teams with complementary strengths. Technical and vocational institutes benefit when aligning instructors’ certifications with evolving industry standards, supporting workforce-development mandates. AI engines also identify gaps, informing recruitment and upskilling plans that keep programs accredited. Adoption is brisk where unions are absent, but in heavily organized systems deployment slows until contract language clarifies that algorithmic suggestions do not replace peer review.

Rising Compliance Burden for Academic Payroll

Payroll teams must manage disparate rules for student workers, adjunct faculty, and cross-border researchers while honoring FERPA, GDPR, and local labor codes. Institutions therefore demand HCM suites with embedded regulatory intelligence that automates consent workflows, redacts sensitive data, and produces audit-ready reports. Non-compliance risks fines and reputational damage, especially as hybrid appointments multiply and wage classifications grow more complex. Vendors respond by updating tax tables weekly, embedding rule libraries, and offering data-segmentation features that separate student records from employee files. The compliance premium underpins continued investment even among budget-constrained colleges, sustaining growth in the HCM software in education market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budgetary Constraints in Public Institutions | -1.3% | Global, acute in United States state systems, Southern Europe, South America | Long term (≥ 4 years) |

| Data-Privacy Concerns Around Student Employees | -0.9% | North America, Europe, emerging Asia-Pacific | Medium term (2-4 years) |

| Fragmented Legacy SIS and ERP Stacks | -0.6% | North America, Europe | Long term (≥ 4 years) |

| Limited IT Talent in Small Colleges | -0.4% | Global, rural and regional campuses | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Budgetary Constraints in Public Institutions

Flat appropriations, enrollment dips, and inflationary pressures leave public universities extending the lives of aging HR systems rather than funding replacements. Boards often freeze hiring and defer IT capital outlays, reserving cash for instructional priorities. Consequently, vendors must propose phased deployments, deferred payment terms, or managed-service models that shift costs from capital to operating budgets. Even attractive total-cost-of-ownership analyses struggle to clear governance hurdles when fiscal forecasts remain uncertain. The funding squeeze therefore slows upgrade cycles and tempers overall expansion of the HCM software in education market.

Data-Privacy Concerns Around Student Employees

Workforce analytics rely on granular data about student employees’ academic status and performance, yet FERPA and GDPR restrict how institutions collect and share such information. HR teams must segregate education records, implement role-based access controls, and log every data access event. Customizing platforms to meet these rules increases deployment time and cost. Furthermore, AI models that infer student attributes from behavioral patterns raise discrimination risks, prompting additional scrutiny from legal counsel and ethics boards. Privacy frictions thus lengthen sales cycles and occasionally force institutions to throttle back advanced analytics features.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Gains Momentum Despite On-Premises Dominance

On-premises systems held 66.78% of 2025 revenue, reflecting universities’ desire to retain control of sensitive payroll and benefits records, yet cloud subscriptions are rising at a 10.72% CAGR. The HCM software in education market size for cloud deployments is expected to outpace on-premises growth through 2031 as mid-tier colleges convert fixed server costs into variable subscription fees.

Hybrid architectures now bridge legacy student systems and cloud HR modules, letting institutions meet data-residency mandates while adopting AI features delivered only in cloud releases. Vendors offer sovereign hosting options and pre-built connectors that synchronize records between environments, reducing the integration burden that once deterred migrations.

By Solution: Talent Management Outpaces Core HR

Core HR maintained 45.61% share in 2025, but talent-management suites are expanding at a 9.42% CAGR as universities compete to attract and retain specialized faculty. Learning-development catalogs, AI-driven recruiting, and micro-credential tracking give institutions tools once confined to corporate HR, broadening the HCM software in education market share for strategic talent modules.

Payroll engines remain indispensable because of ever-changing tax and benefit regulations, yet innovation concentrates on embedding conversational agents that resolve pay inquiries and surface anomaly alerts. ADP's launch of AI Agents in January 2026, which automate routine payroll inquiries and flag anomalies in pay runs, represents an effort to inject differentiation into a commoditized category.[2]ADP, “AI Agents Launch,” adp.com This indicates that differentiation is migrating from transactional processing to experience-centric capabilities.

By Institution Type: Vocational Institutes Accelerate Adoption

Universities represented 51.22% of 2025 spending, driven by large employee bases and complex hierarchies, but vocational and technical institutes are the fastest-growing buyers at a 10.34% CAGR. Accreditation bodies now require auditable tracking of instructor certifications, pushing trade schools to formalize HR processes through cloud platforms.

Community colleges favor bundled time-and-attendance and scheduling tools that accommodate adjunct faculty with variable workloads. K-12 districts, though numerous, purchase through centralized contracts that reward vendors offering end-to-end suites covering absence management, substitute placement, and professional development.

By End User: Student Workers Gain Formal HR Support

Faculty and staff comprised 53.45% of active seats in 2025, yet student-employee usage is climbing at a 9.81% CAGR as institutions integrate work-study programs with career services. The HCM software in education market size for student modules will rise further as federal audits demand granular hour and wage tracking.

Mobile self-service has become mandatory; student workers expect to accept shifts, submit timesheets, and obtain digital credentials on smartphones. Contractors and adjuncts likewise value unified portals that let them manage multiple campus appointments without paper forms.

Geography Analysis

North America remained the largest regional contributor with 36.18% revenue in 2025 thanks to early cloud adoption and strict FERPA governance. Private universities and flagship publics continue to fund integrated suites even amid state budget pressure, sustaining steady demand. Canada follows similar patterns as provinces sponsor digital-campus initiatives, while Mexico’s institutions begin phasing out manual timekeeping, albeit at slower pace because of limited IT infrastructure.

Asia-Pacific is the fastest-growing territory, posting an 8.98% CAGR. China and India channel government grants into digital-campus programs that standardize payroll and talent analytics, lifting local vendors that integrate with national insurance and accreditation systems. Australia shows high cloud penetration and mature learning-development adoption, whereas Japan remains cautious, keeping sensitive data in on-premises clusters but exploring cloud pilots at private universities.

Europe grows modestly as GDPR compliance and budget austerity in southern states elongate procurement cycles. The United Kingdom and Germany modernize HR and finance stacks to enhance audit readiness, yet centralized civil-service pay frameworks in France, Italy, and Spain slow deal flow. The Middle East accelerates as Saudi Arabia and the United Arab Emirates embed HCM requirements in national education-transformation plans, mandating faculty-development tracking inside integrated platforms. South America and Africa are nascent, but regional startups that localize payroll and language interfaces open the HCM software in education market to smaller colleges with constrained resources.

Competitive Landscape

The market shows moderate concentration as ERP heavyweights Workday, Oracle, and SAP cross-sell HR modules into campuses already using their finance or student systems. Workforce-management specialists such as UKG and Frontline Education compete by tailoring adjunct scheduling and substitute placement features for mid-tier colleges. Generative AI is the new differentiator, powering skills mapping, automated payroll anomaly detection, and conversational support bots.

Strategic partnerships expand reach and reduce integration pain. Ellucian teamed with UKG to create a shared data backbone, while ADP and SAP produced out-of-the-box connectors that shorten deployment timelines.[3]ADP and SAP, “Collaboration for Pre-Built Connectors,” adp.com Instructure embeds professional-development content inside Canvas, converging academic and HR learning under one login. Emerging challengers lure budget-tight colleges with pay-as-you-go pricing, prompting incumbents to unbundle suites and offer flexible term lengths.

Long-standing relationships with student-information systems confer switching costs that protect incumbents, yet the shift toward cloud and AI levels the field, allowing nimble vendors to win modules at institutions unwilling to embark on full-suite replacements. White space persists in K-12 districts still reliant on manual timecards, community colleges juggling hybrid faculty models, and vocational institutes seeking industry-credential alignment.

HCM Software In Education Industry Leaders

Workday Inc.

Oracle Corporation

SAP SE

UKG Inc.

ADP Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Instructure partnered with Brandon Hall Group to embed talent-development content and certification pathways directly into Canvas.

- April 2026: Instructure and K16 Solutions launched a migration service bundle that moves legacy LMS data to Canvas while integrating with existing HCM platforms.

- March 2026: ADP joined Pine Services Group to deliver integrated payroll and HR services to southeastern United States K-12 districts.

- January 2026: ADP released AI Agents inside Workforce Now, automating pay inquiries and compliance report generation.

Global HCM Software In Education Market Report Scope

HCM Software in the Education Market encompasses systems that handle faculty and staff information, scheduling, payroll, accreditation, onboarding, and academic workforce planning. Educational institutions deploy HCM solutions to manage unionized staff, adjunct faculty, and student worker programs. Cloud-based tools bolster operational transparency, compliance tracking, and employee engagement across multiple campuses. The market's growth is fueled by digital modernization, mandates for budgeting transparency, and a move towards unified administrative platforms in both K-12 and higher education.

The HCM Software in Education Market Report is Segmented by Deployment Model (Cloud, and On-Premises), Solution (Core HR, Talent Management, Workforce Management, Payroll, and Learning and Development), Institution Type (K-12 Schools, Community Colleges, Universities, and Vocational and Technical Institutes), End-User (Faculty and Staff, Administrative HR, Student Employees, and Contractors and Adjuncts), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud |

| On-Premises |

| Core HR |

| Talent Management |

| Workforce Management |

| Payroll |

| Learning and Development |

| K-12 Schools |

| Community Colleges |

| Universities |

| Vocational and Technical Institutes |

| Faculty and Staff |

| Administrative HR |

| Student Employees |

| Contractors and Adjuncts |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Deployment Model | Cloud | |

| On-Premises | ||

| By Solution | Core HR | |

| Talent Management | ||

| Workforce Management | ||

| Payroll | ||

| Learning and Development | ||

| By Institution Type | K-12 Schools | |

| Community Colleges | ||

| Universities | ||

| Vocational and Technical Institutes | ||

| By End-User | Faculty and Staff | |

| Administrative HR | ||

| Student Employees | ||

| Contractors and Adjuncts | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current HCM software in education market size and projected growth?

The market stood at USD 1.10 billion in 2025, is set to reach USD 1.18 billion in 2026, and is projected to climb to USD 1.72 billion by 2031 at a 7.8% CAGR.

Which deployment model is growing fastest inside academic institutions?

Cloud deployments are advancing at a 10.72% CAGR because universities seek elastic scaling and subscription pricing.

Why are talent-management modules gaining traction versus core HR?

Institutions now view faculty recruitment, retention, and upskilling as strategic levers, driving 9.42% CAGR growth for talent-management suites.

Which region offers the highest growth potential for vendors?

Asia-Pacific leads with an 8.98% CAGR, fueled by government-funded digital-campus programs in China, India, and Australia.

How are compliance requirements shaping product roadmaps?

Vendors embed FERPA and GDPR rule libraries, consent workflows, and automated audit logs to address rising regulatory complexity in academic payroll.

Page last updated on: