HCM Software In The Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

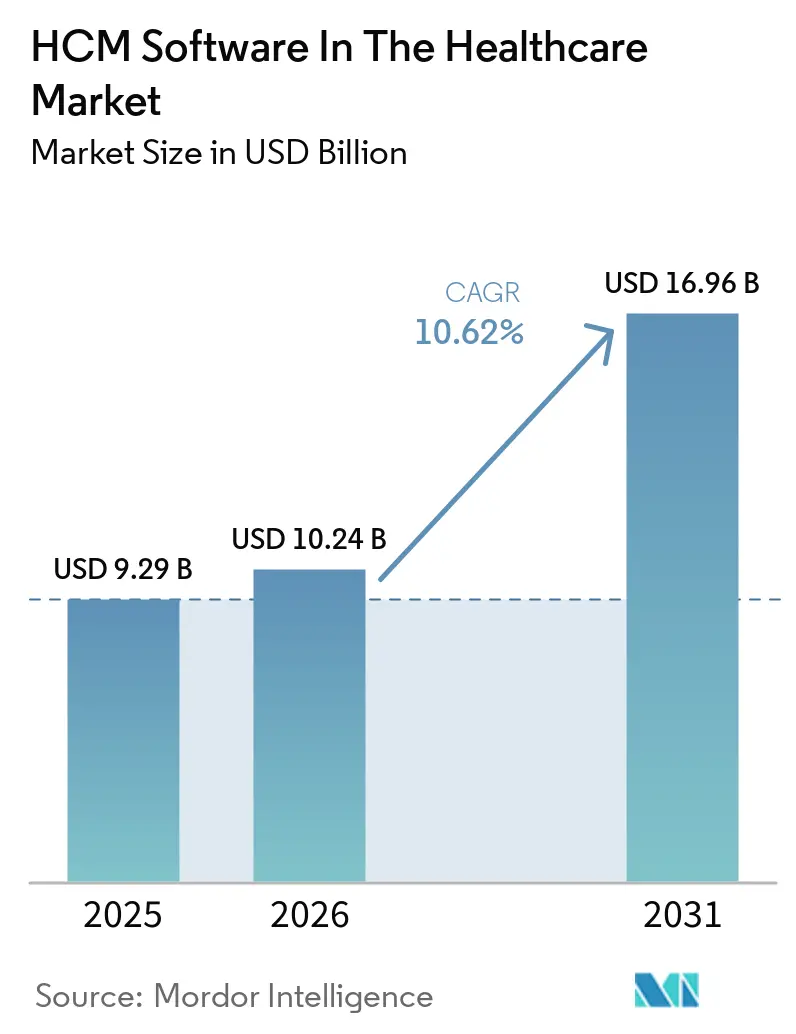

| Market Size (2026) | USD 10.24 Billion |

| Market Size (2031) | USD 16.96 Billion |

| Growth Rate (2026 - 2031) | 10.62% CAGR |

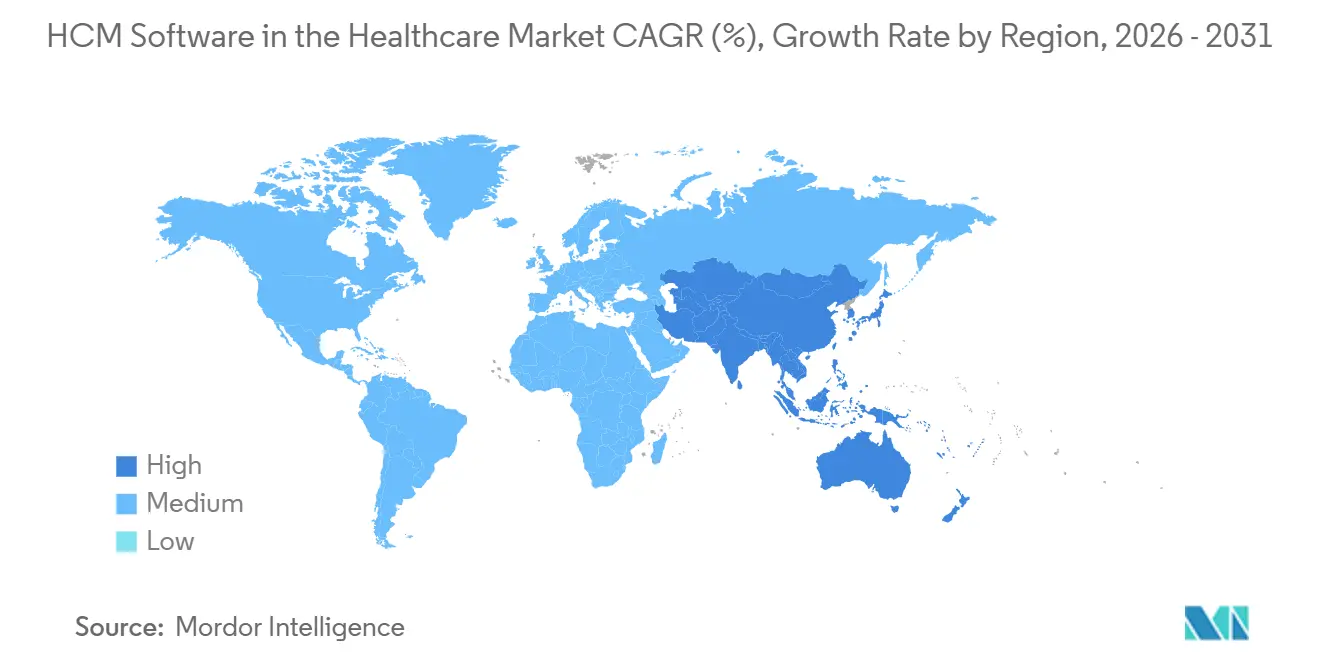

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HCM Software In The Healthcare Market Analysis by Mordor Intelligence

The HCM Software in the Healthcare Market is expected to increase from USD 9.29 billion in 2025 to USD 10.24 billion in 2026, and reach USD 16.96 billion by 2031, growing at a CAGR of 10.62% over 2026-2031. Surging labor expenses, tighter credentialing mandates, and a pivot toward subscription-based cloud suites are prompting hospitals, clinics, and home-health agencies to consolidate payroll, scheduling, and analytics on unified platforms. Large language models now surface overtime hotspots, burnout signals, and license expirations inside the same dashboard, allowing executives to balance quality scores against staffing costs in real time. Vendors are embedding earned-wage access and conversational scheduling agents that cut turnover, a critical lever as registered nurse wages climbed 26.6 percentage points ahead of general inflation in the United States. Heightened cybersecurity scrutiny is steering buyers to managed services that guarantee encryption, disaster recovery, and continuous patching, reducing the burden on overstretched hospital IT teams.

Key Report Takeaways

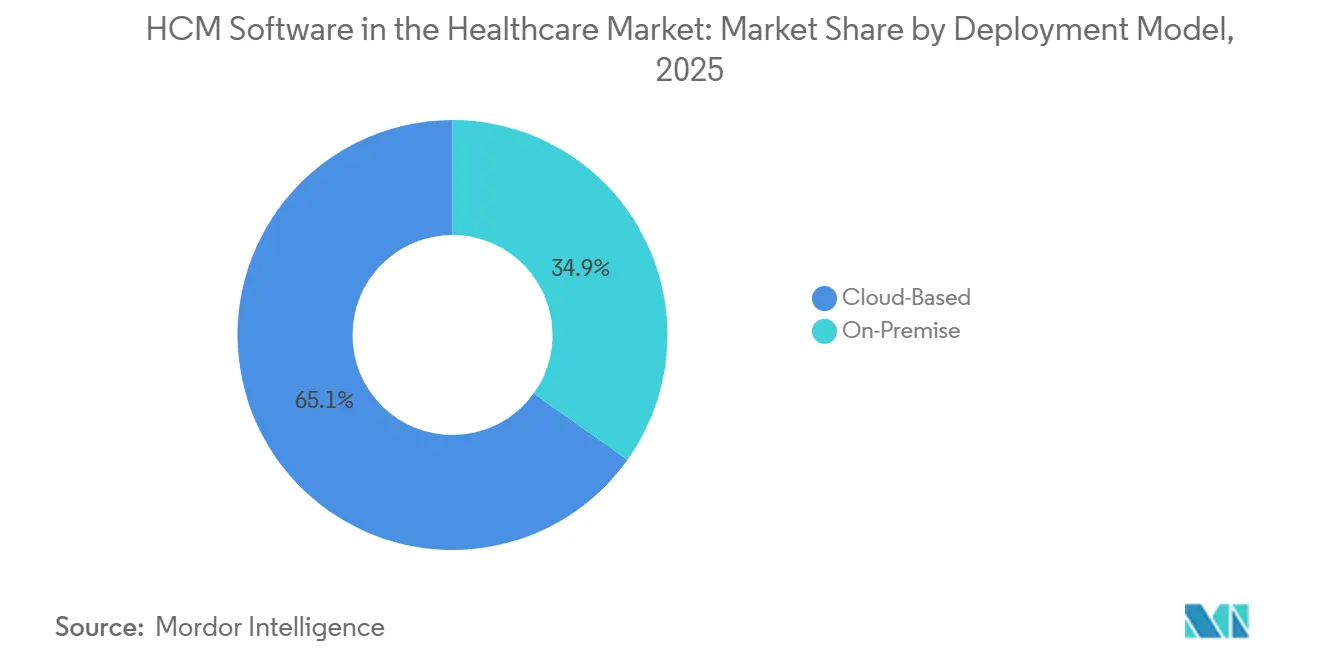

- By deployment model, cloud platforms led with 65.12% revenue share in 2025 and are advancing at a 12.83% CAGR through 2031.

- By solution module, workforce management and scheduling held 36.13% of the HCM software market share in 2025, while analytics and reporting are forecast to expand at a 13.45% CAGR to 2031.

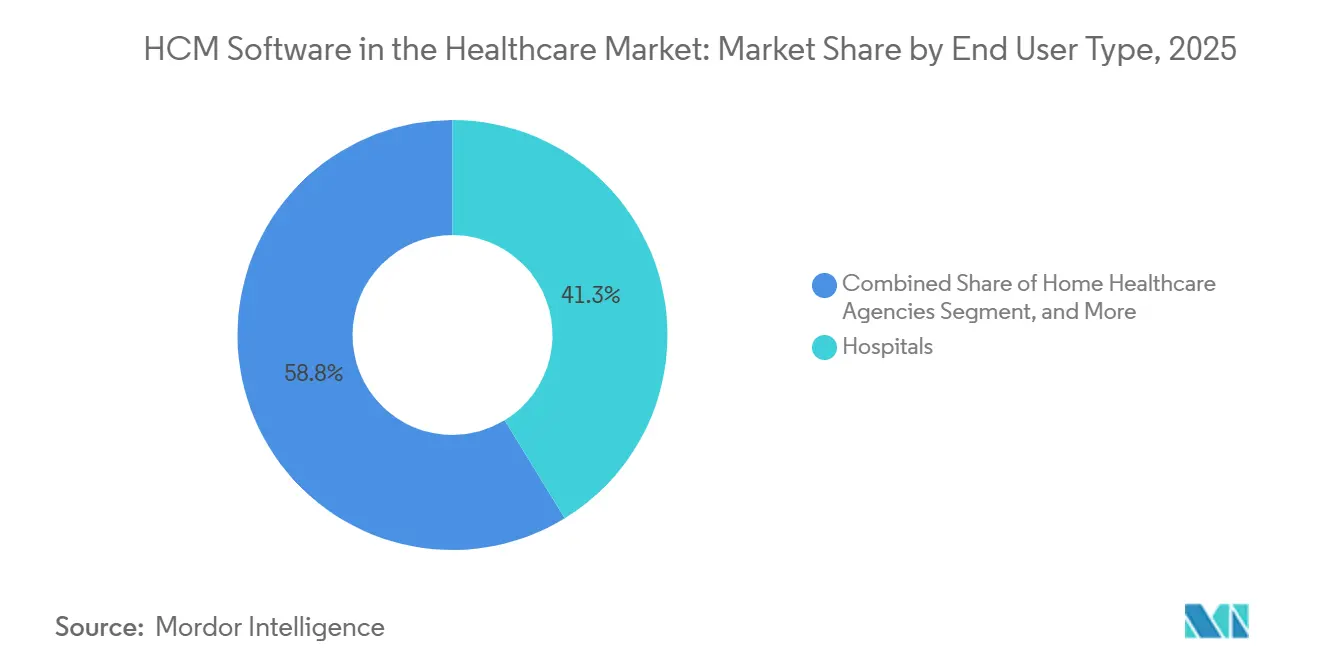

- By end user type, hospitals captured 41.25% of 2025 revenue, whereas home healthcare agencies are projected to post the fastest growth at a 14.63% CAGR between 2026 and 2031.

- By organization size, large health systems with at least 1,000 beds accounted for 46.23% of 2025 spending, yet small providers with fewer than 250 beds are projected to scale cloud adoption at a 13.91% CAGR over the forecast window.

- By geography, North America held a 38.82% share in 2025, while Asia-Pacific is projected to grow at a 13.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HCM Software In The Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Labor Cost Pressure in Healthcare Facilities | +3.2% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Accelerated Cloud Adoption after COVID Pandemic | +2.8% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) |

| Regulatory Mandates for Credential and Compliance Tracking | +2.1% | North America and Europe, emerging in Middle East | Medium term (2-4 years) |

| Workforce Shortages Requiring AI-Based Scheduling | +1.9% | Global, particularly North America and Asia-Pacific | Short term (≤ 2 years) |

| Shift to Skills-Based Staffing Models | +1.4% | North America and Europe, early adoption in Asia-Pacific | Long term (≥ 4 years) |

| Real-Time Earned-Wage Access Driving Platform Uptake | +1.2% | North America, expanding to Europe and Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Labor Cost Pressure In Healthcare Facilities

Nurse wage inflation and minimum-staffing regulations are compressing hospital margins, forcing administrators to extract productivity from existing headcounts rather than expand payrolls. Monthly labor expense updates show 5% year-over-year cost escalation through October 2025, while new federal rules mandate continuous registered-nurse coverage in long-term care, amplifying roster complexity. Cloud HCM suites automate license validation, competency matching, and overtime caps, enabling a 5,000-employee health network to save USD 6.2 million annually after migration.[1]Becker’s Hospital Review, “Hospital Labor Expenses Update,” beckershospitalreview.com Savings stem from unified payroll and time-tracking, which eliminates duplicate data entry and frees funds for clinical technology upgrades. North American and European systems experience the sharpest squeeze because collective bargaining limits wage concessions. Consequently, mature providers prioritize AI-driven scheduling agents that blend acuity forecasts with fatigue scores to reduce costly agency staffing.

Accelerated Cloud Adoption After COVID Pandemic

Pandemic-era remote work exposed the rigidity of on-premise HR systems, spurring rapid migration to multi-tenant SaaS suites that deliver automatic regulatory updates and mobile access. Adventist Health and Northwell Health each reported 39% IT overhead reduction and 21% operational savings after shifting to Oracle Cloud HCM. Rural hospitals follow suit via subscription bundles that bundle middleware, security monitoring, and disaster recovery, minimizing capital outlays. Hybrid coexistence persists in some academic centers that retain PeopleSoft for core HR while layering cloud analytics, but duplicated license fees and integration hurdles accelerate full-stack transitions. North America and Asia-Pacific lead, buoyed by federal funding in rural United States and digital-hospital buildouts across India and China.

Regulatory Mandates For Credential And Compliance Tracking

Monthly license checks now replace biennial reviews under updated Joint Commission rules, and United States long-term-care providers must submit Payroll-Based Journal staffing data tied to resident census.[2]The Joint Commission, “Monthly Monitoring Standards,” jointcommission.org Parallel standards in Europe link accreditation to reimbursement, while the United States Department of Health and Human Services classifies many scheduling algorithms as “high-impact,” demanding bias-monitoring logs by October 2026. Vendors respond by embedding audit trails that log every roster change, license verification, and pay-rate override. QGenda secured National Committee for Quality Assurance validation in December 2025, underscoring the commercial upside for compliant platforms. Heightened scrutiny accelerates demand for automated credentialing dashboards that push alerts to managers, curbing last-minute understaffing fines.

Workforce Shortages Requiring AI-Based Scheduling

Global clinician shortages are driving adoption of machine-learning engines that forecast census shifts, recommend float-pool deployments, and reconcile union rules in seconds. Peer-reviewed research found fewer shift clashes and higher schedule satisfaction after the AI rollout, compared with manual spreadsheets. UKG’s Advanced Scheduler predicts department-level volume and proposes coverage mixes, while mobile apps allow nurses to swap shifts without manager intervention, subject to license and rest-period constraints. Asia-Pacific hospitals, grappling with rapid bed additions, pilot similar tools to optimize multilingual teams. Reduced scheduling friction lessens burnout, improves retention, and ultimately safeguards care quality.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-Front Integration and Change-Management Costs | -1.8% | Global, most pronounced in small and mid-sized providers | Short term (≤ 2 years) |

| Data-Privacy and Cyber-Security Concerns | -1.3% | Global, heightened in North America and Europe | Medium term (2-4 years) |

| Vendor Lock-In Risks with End-to-End Suites | -0.9% | Global, particularly affecting mid-sized health systems | Long term (≥ 4 years) |

| AI-Bias Scrutiny from Healthcare Regulators | -0.7% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Up-Front Integration And Change-Management Costs

Subscription fees alone understate the total project cost, as interfaces, training, and consulting often equal or exceed license spend. A 2025 operations summit found weak governance and insufficient staffing derail many transformations, stretching payback timelines. Rural providers face the steepest hurdle: only 29% expect to upgrade their electronic health records in 2026, limiting their readiness for modern HCM add-ons. Federal rural-health grants reserve just 5% of awards for full platform swaps, pushing hospitals toward incremental modules rather than suite replacements. Managed-service templates from ADP and SAP compress payroll go-lives to under 12 months, but many mid-tier organizations still struggle to secure the upfront cash and project bandwidth.

Data-Privacy And Cyber-Security Concerns

Storing Social Security numbers, direct-deposit details, and wellness data makes healthcare HCM a prime target for ransomware. HIPAA guidance issued in 2025 requires encryption and access logs for wellness information crossing into clinical records. European Union rules restrict found that 67% wrestle with outdated interfaces that heighten breach risk, further delaying cloud adoptionbiometric time-clock data unless staff provide explicit consent, complicating cross-border payroll. A survey of 972 rural executives showed 67% wrestle with outdated interfaces that heighten breach risk, further delaying cloud moves. Vendors counter with anomaly-detection engines and zero-trust architectures, yet headline-grabbing breaches keep boards cautious, tempering near-term adoption.[3]U.S. Department of Health and Human Services, “HIPAA Guidance on Wellness Programs,” hhs.gov

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Platforms Capture Recurring Revenue

Cloud-based suites accounted for 65.12% of 2025 spending and are set to compound at a 12.83% CAGR as buyers prioritize elastic capacity, zero-downtime upgrades, and rapid access to generative AI features. This dominance translates into the largest HCM software market share among all deployment options. Early movers such as Adventist Health achieved 39% IT overhead savings after retiring on-premise servers, freeing funds for clinical AI pilots. On-premise environments persist in academic medical centers that cite data sovereignty and union provisions requiring local hosting, yet rising maintenance fees and talent shortfalls erode the case. Hybrid coexistence remains a transition tactic, but dual licensing and interface upkeep accelerate full cloud migration.[4]UKG Inc., “Advanced Scheduler Launch,” ukg.com

Vendor roadmaps favor agentic AI accessible only in multi-tenant architecture, nudging laggards toward subscription models. UKG’s alliance with Google Cloud pipes BigQuery analytics and Gemini models into schedule bots, cutting routine HR contacts and offering predictive insights absent in legacy stacks. IFS pairs its ERP with UKG Pro to simplify procure-to-pay plus workforce flows, widening the cloud’s appeal to integrated delivery networks. Consequently, decision-makers view managed SaaS as a risk mitigation against cyber threats and regulatory churn, reinforcing the the cloud’s trajectory.

By Solution Module: Workforce Management Dominates, Analytics Accelerates

Workforce management and scheduling commanded 36.13% of 2025 revenue, underscoring health care’s shift-heavy staffing patterns. That segment also delivered the highest HCM software market share among all modules in the healthcare market. AI-enabled rostering now matches patient acuity with nurse skill sets minute by minute, slashing premium labor and improving safety scores. Analytics and reporting log the fastest growth at 13.45% CAGR, turning payroll and attendance data into dashboards that reveal turnover hotspots or pay-equity gaps mandated under emerging transparency laws.

Core HR and payroll remain table stakes but mature, whereas talent acquisition garners fresh investment after Workday’s USD 1 billion Paradox buyout added conversational screening bots. Learning modules integrate context-aware chat, speeding compliance training across multi-facility systems. Performance management adoption lags because clinicians measure success by outcomes rather than corporate scorecards, yet integration with quality metrics shows promise. Overall, solution-mix preferences reflect a pivot from record keeping to predictive decision support.

By End User Type: Hospitals Lead, Home Health Surges

Hospitals accounted for 41.25% of 2025 outlays, given their large workforces, complex union rules, and the direct link between staffing compliance and reimbursement. The segment’s scale makes it the largest contributor to the HCM software market in healthcare. Yet home-health agencies are charting a 14.63% CAGR as aging populations and remote-monitoring mandates divert care to community settings. Mobile-first scheduling apps with GPS-verified timecards enable dispersed caregivers to clock in at patient homes while meeting labor-law documentation requirements.

Clinics and ambulatory centers prefer plug-and-play suites that sync scheduling with billing to avoid dual data entry. Long-term care operators are adopting credential tracking to demonstrate compliance with new nurse-to-resident hour thresholds. Assisted-living chains focus on payroll accuracy for high-turnover hourly staff. Collectively, end-user diversification expands vendor pipelines beyond the hospital core.

By Organization Size: Large Systems Dominate, Small Providers Accelerate

Health systems above 1,000 beds retained 46.23% of spending in 2025, leveraging enterprise contracts, dedicated project offices, and capital reserves to execute multi-year rollouts. Their combined purchasing power ensures early access to beta AI functions, reinforcing incumbency advantages. Conversely, providers with fewer than 250 beds are propelling a 13.91% CAGR by embracing cloud bundles with managed services that bypass ERP legacies. This cohort commands a growing share of future HCM software in the healthcare market.

Medium-sized hospitals straddle both camps, layering best-of-breed scheduling on legacy payroll to contain disruption. Federal grants earmarked for rural modernization sweeten the economics, though cost caps push incremental upgrades over rip-and-replace. As vendor templates mature, even solo critical-access facilities can activate rostering AI within 90 days, narrowing the digital divide.

Geography Analysis

North America harvested 38.82% of 2025 global revenue, propelled by strict credential audits and aggressive wage growth. Monthly license verification rules and overtime spikes make AI schedule optimization a board-level imperative. The United States AI compliance plan classifies several workforce algorithms as high impact, pushing health systems to deploy bias-monitoring dashboards. Canada’s provincial networks adopt similar controls, and Mexico’s hospital groups modernize payroll as near-shoring accelerates manufacturing-linked health benefits.

Asia-Pacific outpaces all regions at a 13.42% CAGR through 2031, buoyed by China’s and India’s hospital construction booms and government incentives for cloud payroll that handles multi-jurisdiction taxes. Japan leverages AI scheduling to offset nurse shortages triggered by rapid ageing, while Australia automates penalty-rate compliance. South Korea funds digital workforce tools that tie staffing ratios directly to single-payer reimbursements, tightening the data loop between operations and revenue.

Europe’s momentum centers on pay-transparency laws that force analytics adoption. SAP SuccessFactors now embeds compensation-gap dashboards aimed at EU directives, driving suite upgrades across United Kingdom trusts, German university clinics, and Nordic private chains. South America and Middle East and Africa remain nascent, yet pilots in Brazil, Saudi Arabia, and United Arab Emirates signal readiness as health ministries bankroll electronic record overhauls that demand integrated workforce modules.

Competitive Landscape

The market skews toward moderate concentration with Oracle, SAP, Workday, UKG, Ceridian, and ADP anchoring the top tier, collectively holding a majority of enterprise accounts. Workday’s healthcare vertical surpassed USD 1 billion annual recurring revenue in Q3 FY 2026 after embedding agentic AI across recruiting, learning, and document intelligence. UKG claims deployments at 90% of the largest United States systems and now pipes Google Cloud Gemini models into its Workforce Operating Platform for conversational roster edits and compliance checks.

Niche specialists sharpen focus: QGenda obtained National Committee for Quality Assurance validation and acquired New Innovations to cover residency management, while Kronos-Health targets nurse unions with contract-aware scheduling templates. Horizontal alliances proliferate: IFS links its ERP to UKG Pro, SAP and ADP co-deliver global payroll, and ServiceNow hosts UKG agentic AI within its workflow fabric, creating integrated employee-service hubs. Startups pitch API-first earned-wage access and AI roster bots, exploiting white space in rural settings where only 8% currently leverage predictive analytics.

Vendor lock-in concerns persist, especially for mid-sized providers wary of suite pricing escalations. Open APIs and adherence to the Trusted Exchange Framework and Common Agreement emerge as differentiators. Cybersecurity posture and audit logging also weigh heavily in request-for-proposal scoring as ransomware incidents rise.

HCM Software In The Healthcare Industry Leaders

Oracle Corporation

UKG Inc.

Automatic Data Processing, Inc.

SAP SE

Workday, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: SAP rolled out SuccessFactors 1H 2026 with agentic AI across recruiting, payroll, learning, and pay-equity analytics, aligning with evolving EU transparency rules.

- April 2026: The Centers for Medicare and Medicaid Services granted the first awards under its USD 50 billion Rural Health Transformation Program, earmarking funds for HCM module upgrades within existing electronic medical records.

- December 2025: QGenda secured National Committee for Quality Assurance validation, making its physician scheduling suite the first to meet payer-grade credentialing standards.

- September 2025: ADP and SAP launched a global payroll partnership, migrating 50 shared clients to SAP Cloud ERP in under 12 months.

Global HCM Software In The Healthcare Market Report Scope

The HCM Software in the Healthcare Market comprises digital platforms that manage healthcare workforce operations, including payroll, scheduling, recruitment, credentialing, compliance, learning, and performance management. These solutions help hospitals and care providers optimize staffing efficiency, maintain regulatory compliance, and improve workforce productivity through cloud and AI-enabled automation.

The HCM Software in the Healthcare Market Report is Segmented by Deployment Model (Cloud-Based and On-Premise), Solution Module (Core HR Administration, Payroll Management, Talent Acquisition and Recruitment, Workforce Management and Scheduling, Learning and Development, Performance Management, and Analytics and Reporting), End User Type (Hospitals, Clinics and Ambulatory Surgical Centers, Long-Term Care Centers, Assisted Living Facilities, Home Healthcare Agencies, and Others), Organization Size (Large Healthcare Systems 1000 Beds, Medium Healthcare Organizations 250-999 Beds, and Small Healthcare Providers 250 Beds), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud-Based |

| On-Premise |

| Core HR Administration |

| Payroll Management |

| Talent Acquisition and Recruitment |

| Workforce Management and Scheduling |

| Learning and Development |

| Performance Management |

| Analytics and Reporting |

| Hospitals |

| Clinics and Ambulatory Surgical Centers |

| Long-Term Care Centers |

| Assisted Living Facilities |

| Home Healthcare Agencies |

| Others End Users |

| Large Healthcare Systems (1000+ Beds) |

| Medium Healthcare Organizations (250-999 Beds) |

| Small Healthcare Providers (250 Beds) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Deployment Model | Cloud-Based | |

| On-Premise | ||

| By Solution Module | Core HR Administration | |

| Payroll Management | ||

| Talent Acquisition and Recruitment | ||

| Workforce Management and Scheduling | ||

| Learning and Development | ||

| Performance Management | ||

| Analytics and Reporting | ||

| By End User Type | Hospitals | |

| Clinics and Ambulatory Surgical Centers | ||

| Long-Term Care Centers | ||

| Assisted Living Facilities | ||

| Home Healthcare Agencies | ||

| Others End Users | ||

| By Organization Size | Large Healthcare Systems (1000+ Beds) | |

| Medium Healthcare Organizations (250-999 Beds) | ||

| Small Healthcare Providers (250 Beds) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current HCM software in the healthcare market size and growth outlook?

The market stood at USD 9.29 billion in 2025, reached USD 10.24 billion in 2026, and is forecast to hit USD 16.96 billion by 2031 at a 10.62% CAGR.

Which deployment model is growing the fastest among healthcare providers?

Cloud-based suites are advancing at a 12.83% CAGR as hospitals shift away from on-premise infrastructure to managed subscription platforms.

Why are analytics modules gaining traction in healthcare HCM suites?

Executives need real-time dashboards that link overtime, burnout risk, and pay-equity gaps to reimbursement outcomes, driving a 13.45% CAGR for analytics and reporting.

How are regulatory changes influencing credential management purchases?

Monthly license-verification mandates and AI-bias rules push providers to adopt automated credentialing and audit-trail features embedded in modern HCM software.

Which end-user segment offers the strongest future growth potential?

Home-health agencies lead with a projected 14.63% CAGR because remote monitoring and community care require mobile scheduling and payroll tools.

What factors limit adoption in rural and critical-access hospitals?

High integration costs, limited IT staff, and cyber-security fears slow modernization, though new U.S. federal grants aim to ease the financial burden.

Page last updated on: