Learning Experience Platform (LXP) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.76 Billion |

| Market Size (2031) | USD 8.35 Billion |

| Growth Rate (2026 - 2031) | 17.30% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

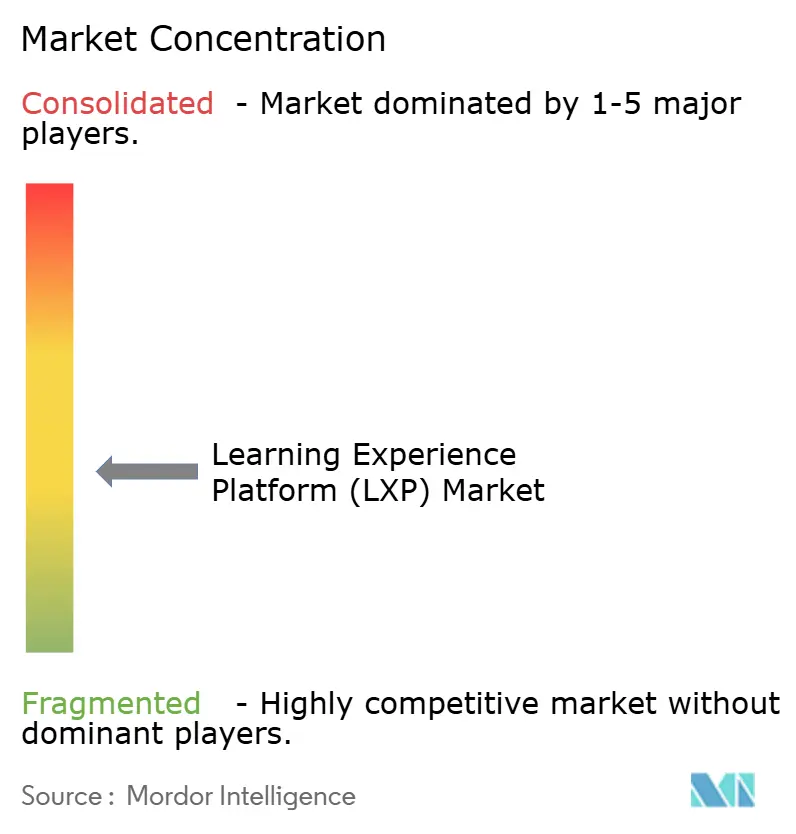

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Learning Experience Platform (LXP) Market Analysis by Mordor Intelligence

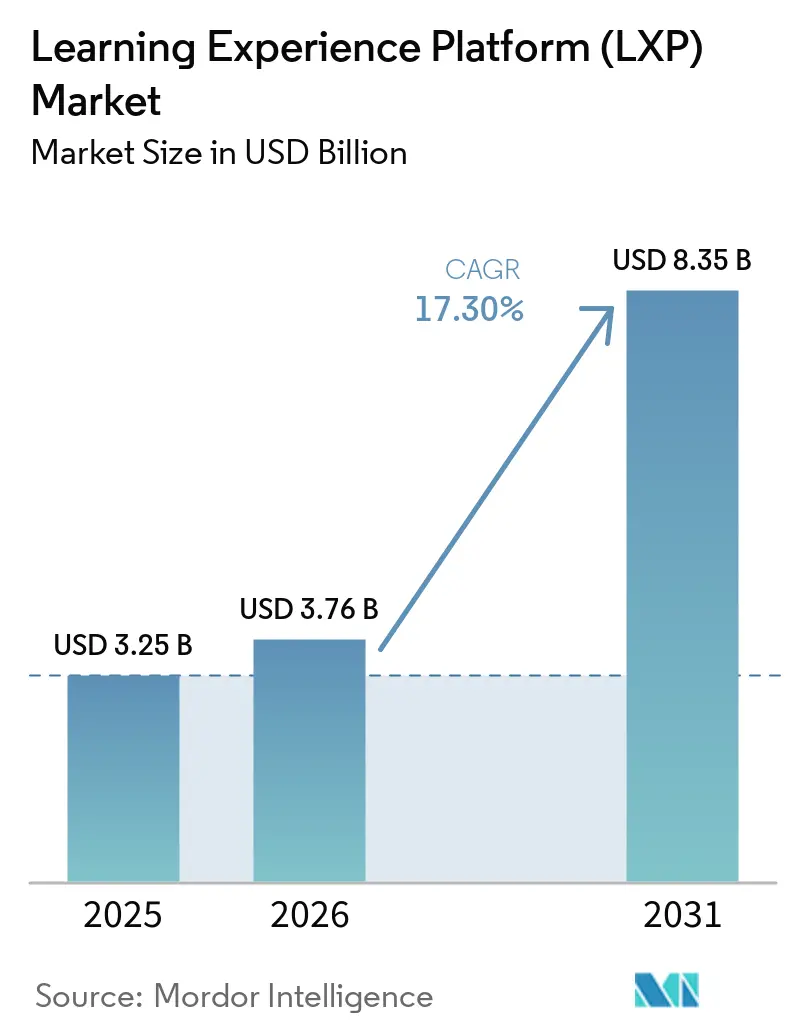

The learning experience platform (LXP) market size is expected to increase from USD 3.25 billion in 2025 to USD 3.76 billion in 2026 and reach USD 8.35 billion by 2031, growing at a CAGR of 17.30% over 2026-2031. The learning experience platform market is expanding as enterprise learning moves away from compliance delivery alone and toward skills-linked performance systems that can show measurable workforce outcomes. Hybrid work patterns have stabilized rather than reversed, which keeps training delivery fragmented across remote, hybrid, and on-site employee groups and strengthens demand for platforms built for multi-context learning. Buyers are also placing more weight on AI personalization, skills intelligence, and HRIS connectivity because these functions now shape adoption, engagement, and proof of value more than content hosting alone. Vendor competition is tightening as agentic AI launches shorten feature differentiation windows, which makes integration depth, data quality, and implementation capability more important in enterprise buying decisions. The strongest opening remains with organizations that need to connect learning records, role changes, and skills development in a single operating layer, but regulated sectors still face longer deployments because governance design has become part of platform selection rather than a later-stage compliance step.

Key Report Takeaways

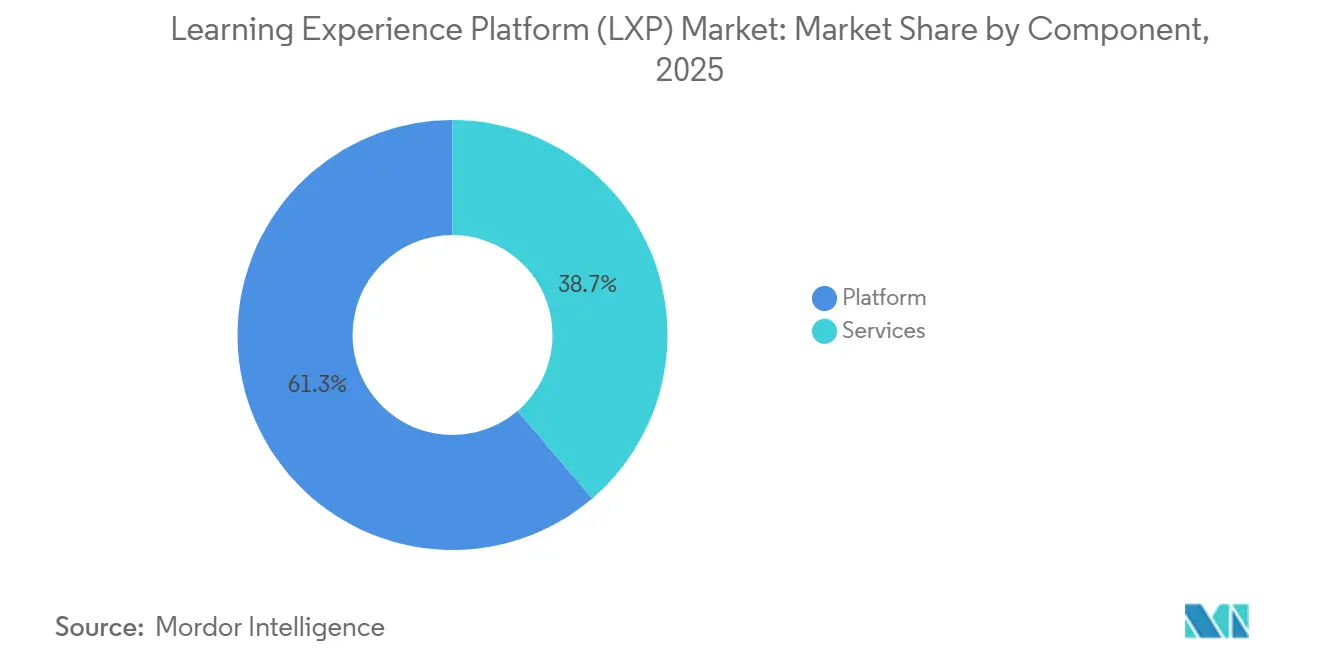

- By component, platform solutions accounted for 61.26% of the learning experience platform (LXP) market revenue in 2025, while services are projected to expand at a 18.37% CAGR through 2031.

- By deployment model, cloud-based deployment accounted for 76.24% of the LXP market revenue in 2025 and is expected to expand at a 21.49% CAGR through 2031.

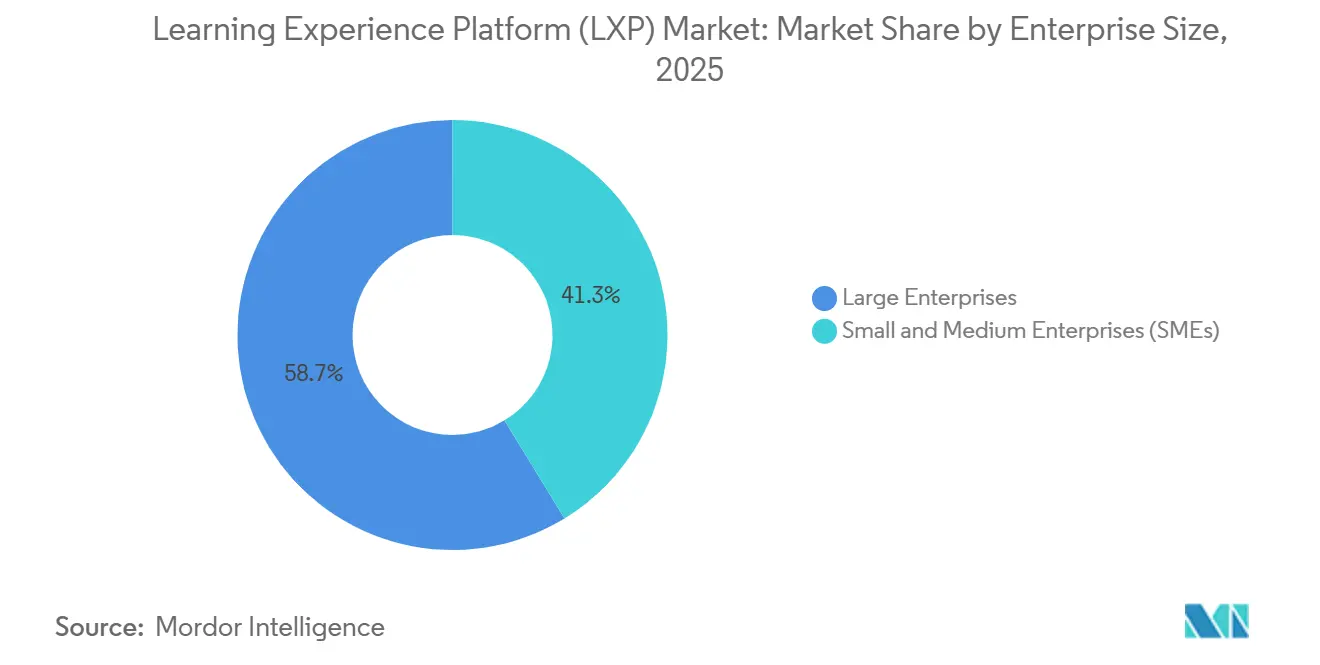

- By enterprise size, large enterprises held 58.72% of the learning experience platform market share in 2025, while SMEs are projected to record the highest CAGR at 23.61% through 2031.

- By end-user industry, corporate end users accounted for 64.37% of the learning experience platform (LXP) market revenue in 2025, while government and non-profit are projected to expand at a 20.91% CAGR through 2031.

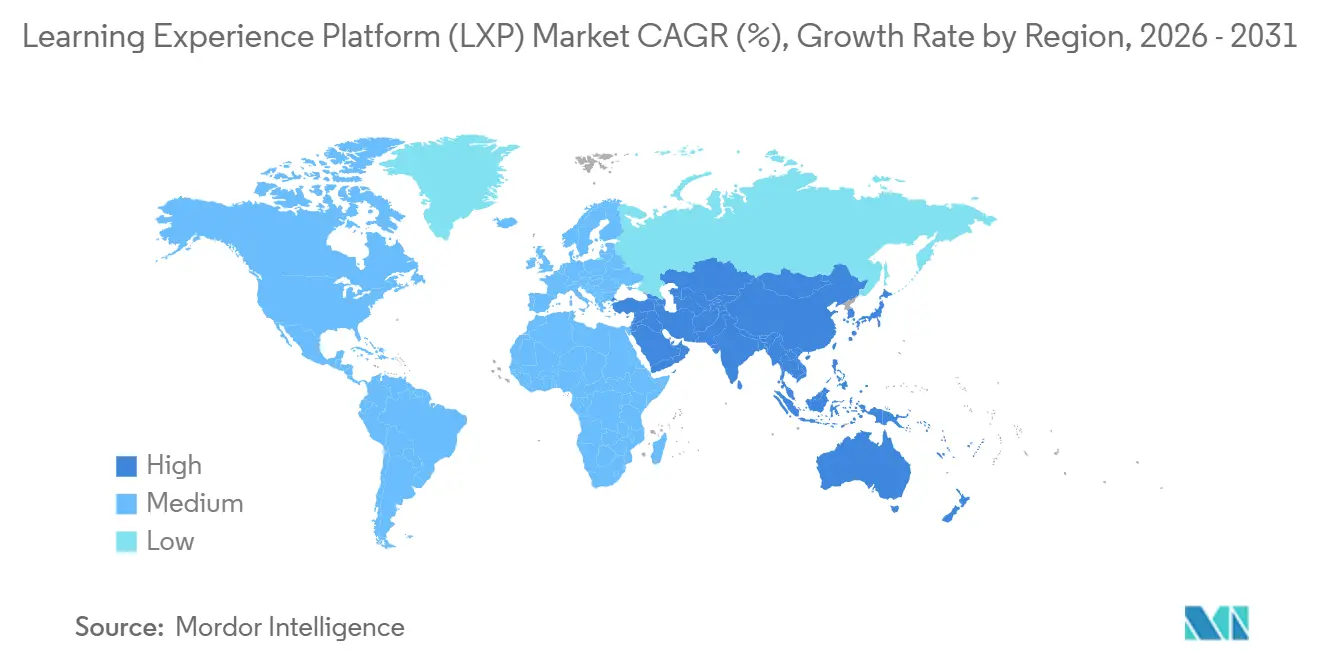

- By geography, North America accounted for 42.36% of the learning experience platform market size in 2025, while Asia-Pacific is projected to grow at an 18.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Learning Experience Platform (LXP) Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rapid Shift To Remote and Hybrid Workforce Learning | +4.2% | Global | Short term (≤ 2 years) |

| Need For AI-Driven Personalized Learning Paths | +3.8% | Global, with early concentration in North America and Europe | Medium term (2-4 years) |

| Upskilling For Enterprise Digital-Transformation Goals | +3.2% | Global, with early gains in the United States, India, and Germany | Long term (≥ 4 years) |

| Integrations With HRIS and Productivity Suites | +2.1% | North America and Europe | Medium term (2-4 years) |

| Skills-Ontology Linkage to Talent Marketplaces | +1.6% | North America and Europe, spill-over to the Asia-Pacific core | Medium term (2-4 years) |

| XAPI-Enabled LRS Analytics Proving ROI | +1.2% | North America and Europe, Asia-Pacific core | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Shift to Remote and Hybrid Workforce Learning

The learning experience platform (LXP) market continues to benefit from the normalization of hybrid work because organizations now train fully remote, hybrid, and on-site employees at the same time. In 2025, most remote-capable US workers were operating in hybrid arrangements, indicating that flexibility had become structural rather than temporary. In this environment, learning experience platform deployments are gaining traction because asynchronous content, mobile access, AI-curated pathways, and consistent user experience help organizations deliver the same learning outcome across different work settings. This shift also raises expectations around learner control, since employees who choose how they work increasingly expect similar control over how and when they learn. Companies that place rigid learning sequences on top of flexible platform architecture often see weaker engagement early in rollout, which makes platform design and content strategy equally important.

Need For AI-Driven Personalized Learning Paths

The learning experience platform (LXP) market is also being driven forward by the shift from simple content recommendations to AI-driven skill-gap closure. Docebo stated in its 2026 AI Readiness Gap Report that AI adoption and fluency had become the main pressure point for enterprise learning leaders, while many organizations were still using static learning models that could not keep pace with role change.[1]Docebo, “AI Readiness Gap Report 2026,” Docebo, docebo.com That makes personalization quality a central buying criterion, because platforms built on weak signals, such as job title or department, often produce recommendations that learners ignore. TalentLMS reported in 2026 that 73% of HR managers saw expanded digital skills as their main priority, which supports demand for systems that can map, recommend, and validate specific capabilities rather than present generic catalogs. Vendors with greater proprietary skills graphs therefore hold an advantage in the learning experience platform market because they can keep improving recommendations as more learner activity enters the system.

Upskilling For Enterprise Digital-Transformation Goals

The learning experience platform market is gaining from the fact that upskilling is now tied more directly to business execution. General Assembly reported in 2026 that 83% of HR leaders said business success depended more on upskilling current employees than on hiring new talent, which shows how learning budgets are being tied to transformation goals. This changes the role of an LXP from a training destination into a system that connects outside content, role-based pathways, and verified learning progress. Buyers are looking for platforms that can turn large learning libraries into targeted development actions tied to actual workforce gaps. That demand is strongest where role requirements shift quickly, because static training calendars cannot keep up with technology change or new operating models.

Integrations With HRIS and Productivity Suites

The learning experience platform (LXP) market is seeing stronger demand for platforms that sit inside the systems employees already use each day. Enterprise buyers now treat bidirectional HRIS connectivity as a basic requirement because role changes, performance signals, and verified skills records need to move across learning, talent, and workforce planning systems without manual intervention. SAP Community highlighted in 2025 that SAP SuccessFactors integration with Microsoft Teams through the Work Tech configuration enabled HR tasks, learning delivery, and notifications within the Microsoft 365 workflow, which showed how embedded delivery can reduce context switching. Learning that appears inside Microsoft Teams, Salesforce, or Slack tends to produce better daily usage because employees do not need to leave the flow of work to act on recommendations. This is raising procurement pressure on vendors in the LXP market that still rely on weak connector ecosystems or custom integration work.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High Implementation and Content-Curation Costs | -3.8% | Global, most acute for SMEs in emerging markets | Short term (≤ 2 years) |

| Data-Privacy And Security Concerns in Regulated Sectors | -2.4% | Europe (GDPR, EU AI Act), North America (HIPAA, FINRA) | Medium term (2-4 years) |

| Proprietary Skills Taxonomies Create Vendor Lock-In | -1.6% | Global, most acute in Asia-Pacific and multi-vendor environments | Medium term (2-4 years) |

| Legacy-LMS Integration Drains IT Bandwidth | -1.3% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Implementation And Content-Curation Costs

High first-year activation costs remain a real barrier for the learning experience platform market, especially outside large-enterprise budgets. Buyers often find that subscription pricing is only one part of the total outlay because implementation, skills-framework design, content licensing, and rollout support sit outside the core platform fee. The burden continues after go-live because multi-source learning environments require ongoing editorial work to retire outdated content, maintain pathway quality, and keep libraries aligned with changing role needs. That pressure is felt more sharply by SMEs and by organizations with lean learning teams that cannot dedicate staff to full-time curation. Vendors are reducing some friction with bundled content and AI-assisted curation, but the economics of maintaining high-quality, current learning experiences still slow broader adoption.

Data-Privacy and Security Concerns in Regulated Sectors

The learning experience platform (LXP) market also faces slower adoption in sectors where learning data sits close to regulated employee or operational records. The EU AI Act will make key high-risk obligations enforceable from August 2026, meaning organizations using AI-assisted learning tools will need stronger documentation, oversight, and impact-assessment processes, in addition to GDPR requirements.[2]European Union, “Regulation (EU) 2024/1689,” Official Journal of the European Union, eur-lex.europa.eu In the United States, healthcare and financial services buyers often require more detailed audit-trail architecture for attributed learning records, which adds technical and legal review to deployment plans. This creates a two-sided effect: regulation slows implementation while also favoring vendors that already offer data residency controls, anonymization features, and certified infrastructure. Smaller vendors in the LXP market, therefore, face a harder path in regulated accounts because governance readiness is now part of core product evaluation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platform Architecture Leads Revenue While Services Scale Fastest

Platform solutions held 61.26% of revenue in 2025, which shows that enterprise buyers still favor integrated suites over point tools in the learning experience platform (LXP) market. Within this category, demand has centered on AI-driven personalized learning modules, skills intelligence layers, content aggregation, and analytics tools that can connect learning activity to workforce performance. Learning analytics platforms have gained traction because executive buyers want more than completion dashboards and increasingly ask for auditable evidence of capability improvement. Content aggregation platforms also remain relevant because they give enterprises a practical route into the learning experience platform market without forcing a full replacement of existing content relationships.

Services are projected to grow at an 18.37% CAGR through 2031, which makes them the fastest-expanding component in the market. That pattern reflects a shift in buyer priorities from software deployment alone toward activation, governance, and measurable adoption. The Adecco Group reported in 2026 that only 33% of companies were actively investing in data insights to understand workforce skills capabilities, which points to a large need for implementation support and skills architecture services.[3]Adecco Group, “2026 Workforce Trends Report,” Adecco Group, adecco.com In practice, this means consulting around skills frameworks, managed analytics, and learning operations has become a recurring revenue stream rather than a one-time setup function. As a result, the LXP market is rewarding vendors that can combine product capability with operational support that makes the platform usable and visible to business leaders.

By Deployment Model: Cloud-Based Platforms Dominate Across All Enterprise Tiers

Cloud-based deployment accounted for 76.24% of revenue in 2025 and remained both the leading and the fastest-growing model, with a 21.49% CAGR through 2031. This part of the learning experience platform market benefits from continuous delivery because cloud-native systems can push AI-model updates, connector releases, and skills-graph improvements faster than on-premises installations. That speed matters because inference quality depends on current data, frequent model refresh, and broad interoperability with other enterprise systems. Growth markets in Asia-Pacific and South America are also moving directly to cloud-first architectures, which strengthens the long-term lead of cloud in the learning experience platform (LXP) market.

On-premises deployment still holds a place in environments where sovereignty rules or isolated networks limit cloud storage of employee learning records. Defense contractors, classified government entities, and certain industrial operations continue to favor this model because compliance limits outweigh the flexibility benefits of full cloud delivery. Hybrid deployment is therefore emerging as a practical middle path, especially in European financial services where sensitive data can stay on local infrastructure while cloud modules handle personalization and advanced analytics. This blended architecture allows the LXP market to expand in tightly governed sectors without forcing a full compromise on AI capability or security requirements.

By Enterprise Size: Large Enterprises Hold Revenue While SMEs Expand Faster

Large enterprises held 58.72% of revenue in 2025, which shows that the learning experience platform (LXP) market still depends heavily on complex multinational rollouts and centralized enterprise procurement. These buyers usually need multilingual delivery, multi-country governance, certified integrations, and enterprise-grade service commitments, which favors vendors with deeper product breadth and delivery capacity. Large organizations also gain from bundled content contracts and negotiated platform licenses that increase switching costs over time. That keeps revenue concentrated in bigger accounts even as adoption broadens across the rest of the learning experience platform market.

SMEs are projected to grow at a 23.61% CAGR through 2031, which makes them the fastest-moving enterprise cohort. TalentLMS reported in 2026 that upskilling or reskilling current workers was the main workforce strategy for 64% of HR managers, and that supports rising SME demand for structured learning infrastructure rather than spreadsheet-led tracking. Vendors are responding with modular pricing and entry tiers that let mid-sized buyers begin with personalization and skills tracking before adding talent marketplace links or advanced analytics. This phased model lowers adoption barriers and opens a wider buyer base to the LXP market. It also creates room for vendors to grow account value over time as SMEs build internal learning maturity and need stronger reporting, integration, and governance tools.

By End-User Industry: Corporate Buyers Lead While Public-Sector Demand Builds

Corporate end users contributed 64.37% of revenue in 2025, making them the largest demand base in the learning experience platform market. Spending remains strongest in technology, financial services, and professional services because these verticals face rapid role change, high labor costs, and constant pressure to keep skills current. Corporate buyers are also using LXPs less as standalone training destinations and more as a skills layer inside broader talent systems that support mobility, succession, and workforce planning. This makes skills-graph quality and system connectivity more decisive than library size in many large-account decisions across the learning experience platform (LXP) market market.

Government and non-profit is projected to grow at a 20.91% CAGR through 2031, which makes it the fastest-growing end-user group. The EU AI Act Article 4 requirement, in force since February 2025, requires organizations deploying AI systems to ensure documented AI literacy among relevant staff, which creates a clear compliance-linked demand driver for scalable learning systems. Public-sector organizations are also moving away from legacy learning management system environments toward experience-led platforms that can support continuous development rather than periodic compliance cycles. Academic institutions add a secondary growth layer because universities and other education providers are using LXP models to serve non-traditional and lifelong learners who want modular and self-directed content. Together, these patterns are widening the LXP market beyond its traditional corporate core.

Geography Analysis

North America held 42.36% of revenue in 2025, which gave the region the largest share of the learning experience platform (LXP) market. The United States remains the main anchor because it combines a dense base of large enterprises, mature HRIS ecosystems, and high willingness to spend on trackable workforce development. Canada also shows strong demand in financial services and government, where cloud security certifications increasingly shape vendor selection. Mexico is emerging faster as multinational manufacturers and technology-services firms invest in scalable Spanish-language training infrastructure for more complex cross-border operations. South America remains earlier in adoption, but Brazil and Argentina are creating steady demand for mobile-first and multi-language cloud deployments within the learning experience platform market.

Europe represents a high-value but compliance-heavy part of the learning experience platform market. Germany and the United Kingdom remain the largest national markets, with German demand supported by manufacturing digitization and workforce reskilling needs tied to vocational and apprenticeship pathways. In France, the professional training market exceeded EUR 32 billion, which equals USD 35.2 billion at the 2025 average EUR/USD rate of 1.10, and Qualiopi requirements have made content governance and audit-trail capability more important in vendor screening.[4]Internal Revenue Service, “Yearly Average Currency Exchange Rates,” Internal Revenue Service, irs.gov Unow reported in 2026 that a March survey of more than 500 HR and training professionals showed learning modality balance was stabilizing, which indicates a shift from remote-only growth toward deliberate blended optimization. Spain and Italy are building mid-market opportunity, while sanctions-related constraints continue to reduce Russia's role and shift regional weight toward the DACH cluster, France, and the United Kingdom. The Middle East, led by Saudi Arabia and the UAE, is advancing quickly on national upskilling agendas, while Africa remains earlier stage with demand centered on South Africa's financial services base and Nigeria's expanding technology workforce.

Asia-Pacific is projected to grow at an 18.11% CAGR through 2031, which makes it the fastest-growing regional block in the LXP market. India stands out because skill shortages remain acute and enterprise demand for applied AI capability, safety behavior, and compliance-linked learning continues to rise. Workera reported in 2026 that only 13% of enterprise employees possessed the critical skills needed to understand and work with AI agents, which shows how limited the current skills baseline remains. China's adoption path is shaped by workforce policy and data-localization rules, which favor domestic AI-learning providers and limit the reach of international platforms. Japan, Australia, and New Zealand remain mature mid-sized markets where high per-seat purchasing power and strong interest in workforce planning support ongoing demand for skills-intelligence features.

Competitive Landscape

The learning experience platform market remains moderately fragmented across the broader field of mid-market and specialist vendors. The main competitive shift in 2026 is moving from feature parity toward agentic AI differentiation, where vendors are automating skill reasoning, content generation, and next-step learning actions. Cornerstone OnDemand strengthened its position in May 2026 with the launch of Cornerstone Workforce AI, built on a People Graph covering more than 55,000 skills and over 1 billion workforce profiles, while also deepening integration with Salesforce Agentforce and Slack workflows. Docebo also advanced its standing when it acquired 365Talents in January 2026 for USD 54.6 million and later launched AgentHub in April 2026, giving it a tighter closed-loop structure between skills intelligence and learning execution. Patent activity around skills inference, xAPI normalization, and adaptive assessment is rising, which suggests that competition in the learning experience platform (LXP) market market is now tied not only to features but also to defensible technical assets.

White space in the learning experience platform market is most visible in frontline enablement, compliant multi-language SME delivery, and regulated-sector architecture. Axonify addresses one of these gaps by embedding learning into frontline workflow tools rather than requiring workers to enter a separate learning destination, which is especially relevant in retail, logistics, and manufacturing environments. Mid-tier vendors in Europe are also finding room through compliance-by-design offers that combine EU data residency, GDPR-aligned anonymization, and certified infrastructure. At the same time, the line between LXP, talent marketplace, and workforce intelligence platform is becoming less distinct, which is changing how enterprise buyers evaluate product fit. Smaller players that provide platform-agnostic skills ontology tools or AI-native content generation are reducing the cost of building capabilities that once acted as a moat for larger vendors.

Buyers in the LXP market are therefore placing more weight on execution depth than on surface-level feature lists. Integration quality, governance readiness, and skills-graph strength are becoming the main filters in enterprise evaluations, especially where deployment risk matters as much as feature breadth. Vendors that can combine these elements with workflow embedding are better placed to win larger and longer contracts. Vendors that cannot match this shift risk slower expansion, even if they continue to add visible AI features at a fast pace.

Learning Experience Platform (LXP) Industry Leaders

Cornerstone OnDemand, Inc.

Docebo Inc.

SAP SuccessFactors (SAP SE)

Skillsoft Corporation (SumTotal)

Degreed, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Degreed introduced Degreed Solution Accelerators, pre-built, outcome-based programs for Leadership Transformation and AI Fluency, at LENS 2026 in Orlando, and expanded Degreed Maestro with Guided Conversations and Skills Check-In capabilities designed to surface transformation friction and collect reliable enterprise skills data at scale.

- February 2026: Skillsoft announced the general availability of the next-generation Skillsoft Percipio Platform, repositioning from a content provider to a skills-management platform with capabilities spanning skills mapping at scale, gap identification, development prioritization, and reskilling-investment measurement aligned to business performance.

- January 2026: Docebo completed the acquisition of 365Talents, an AI-powered skills intelligence and workforce analytics company headquartered in Lyon, France, for approximately USD 54.6 million in cash, plus up to USD 5.1 million in contingent earn-out payments, embedding AI-driven skills detection and workforce analytics directly into the Docebo platform and creating a closed-loop skills-to-learning architecture.

- October 2025: Cornerstone OnDemand launched Cornerstone for Agentforce, an AI learning agent available on the Salesforce AppExchange Marketplace, enabling embedded skill-gap assessment and targeted training delivery directly within Salesforce's digital labor platform without leaving the Agentforce workflow.

Global Learning Experience Platform (LXP) Market Report Scope

A Learning Experience Platform (LXP) is an advanced digital learning solution that delivers personalized, engaging, and learner-centric experiences. Unlike traditional Learning Management Systems (LMS), which prioritize administrative oversight and compliance, an LXP focuses on curated content, social learning, AI-driven recommendations, and skill development pathways, enabling employees or learners to actively manage their professional growth.

The Learning Experience Platform (LXP) Market Report is Segmented by Component (Platform, and Services), Deployment Model (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and SMEs), End-user Industry (Corporate, Academic, Government and Non-profit, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Platform | Learning Experience Platforms |

| AI-driven Personalized Learning Platforms | |

| Skills Intelligence Platforms | |

| Learning Content Aggregation Platforms | |

| Learning Analytics and Engagement Platforms | |

| Services |

| Cloud-Based LXP |

| On-Premises LXP |

| Hybrid LXP |

| Large Enterprises |

| Small and Medium Enterprises |

| Corporate |

| Academic (K-12, Higher Ed) |

| Government and Non-profit |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of the Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Component | Platform | Learning Experience Platforms | |

| AI-driven Personalized Learning Platforms | |||

| Skills Intelligence Platforms | |||

| Learning Content Aggregation Platforms | |||

| Learning Analytics and Engagement Platforms | |||

| Services | |||

| By Deployment Model | Cloud-Based LXP | ||

| On-Premises LXP | |||

| Hybrid LXP | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By End-user Industry | Corporate | ||

| Academic (K-12, Higher Ed) | |||

| Government and Non-profit | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of the Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2026 size of the learning experience platform (LXP) market?

The learning experience platform (LXP) market stands at USD 3.76 billion in 2026 and is forecast to reach USD 8.35 billion by 2031, growing at a 17.30% CAGR.

Which component leads revenue in learning experience platforms?

Platform solutions lead revenue with 61.26% share in 2025, reflecting buyer preference for integrated suites that combine personalization, skills intelligence, and analytics.

Why are cloud-based LXPs growing faster than other deployment models?

Cloud-based systems held 76.24% of revenue in 2025 and are projected to grow at a 21.49% CAGR because they support faster AI updates, stronger interoperability, and easier scaling across regions.

Which buyer group is expanding the fastest in this space?

SMEs are the fastest-growing enterprise cohort at a 23.61% CAGR through 2031, supported by modular pricing and easier access to cloud-native platform capabilities.

Which region is growing the fastest for LXP adoption?

Asia-Pacific is projected to record the highest regional CAGR at 18.11% through 2031, supported by urgent skills-development needs and expanding demand for AI-linked workforce learning.

What is shaping vendor competition most strongly in 2026?

Competition is being shaped by agentic AI launches, deeper HRIS and workflow integration, and stronger skills-graph capability, which are becoming more important than content breadth alone.

Page last updated on: